Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

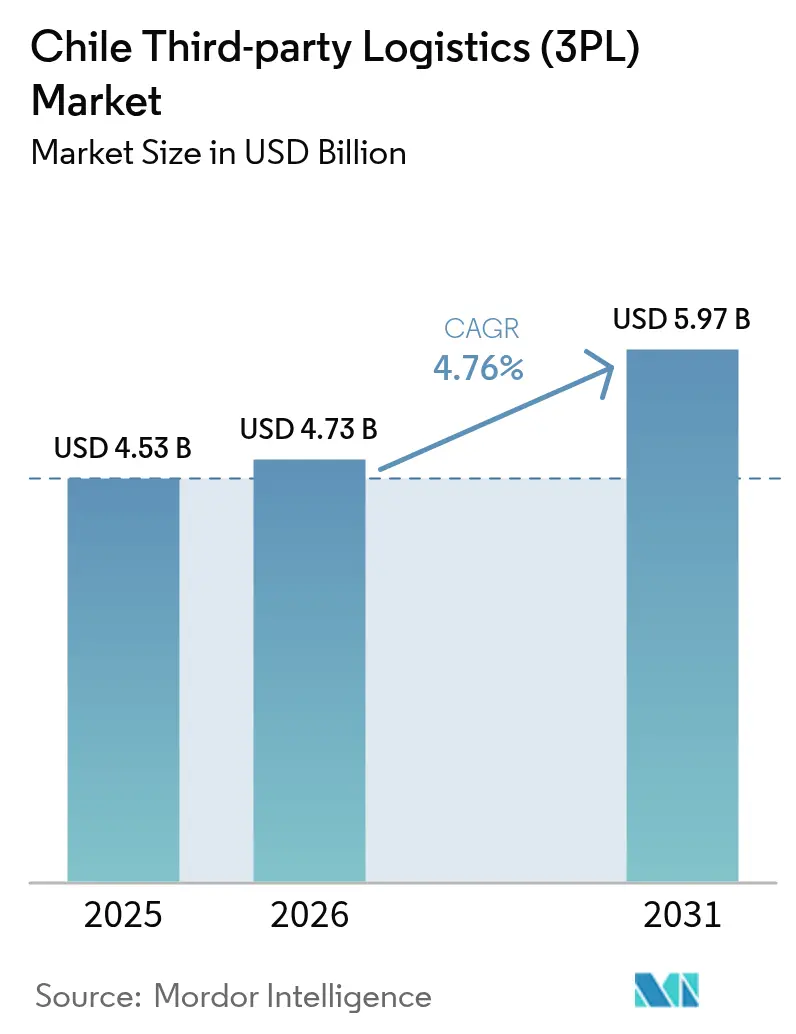

| Base Year Market Size (2025) | USD 4.53 Billion |

| Market Size (2026) | USD 4.73 Billion |

| Market Size (2031) | USD 5.97 Billion |

| Growth Rate (2026 - 2031) | 4.76% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chile Third-party Logistics (3PL) Market Analysis by Mordor Intelligence

The Chile third-party logistics (3PL) market size is expected to grow from USD 4.53 billion in 2025 to USD 4.73 billion in 2026 and is forecast to reach USD 5.97 billion by 2031 at 4.76% CAGR over 2026-2031.

A lithium-driven surge in bulk cargo, a booming aquaculture export base, and rapid digitalization of customs processes are reshaping the Chile third-party logistics market by shifting capacity toward heavy-haul, temperature-controlled, and cross-border freight. The country’s elongated 4,270-kilometer geography, coupled with 65 free-trade agreements, places a premium on multimodal orchestration, real-time visibility, and bonded inland facilities that help operators avoid coastal congestion and defer duties. Heavy-lift demand tied to utility-scale renewable-energy builds and lithium expansion is encouraging hybrid asset strategies, while cold-chain nodes proliferate in southern corridors as salmon exporters race to maintain shelf life across long hauls to Asia and North America. Competitive intensity continues to rise as regional consolidators and global integrators, fresh from multibillion-dollar mergers, chase share in the Chile third-party logistics market even as port strikes, driver shortages, and escalating tolls compress domestic haulage margins.

Key Report Takeaways

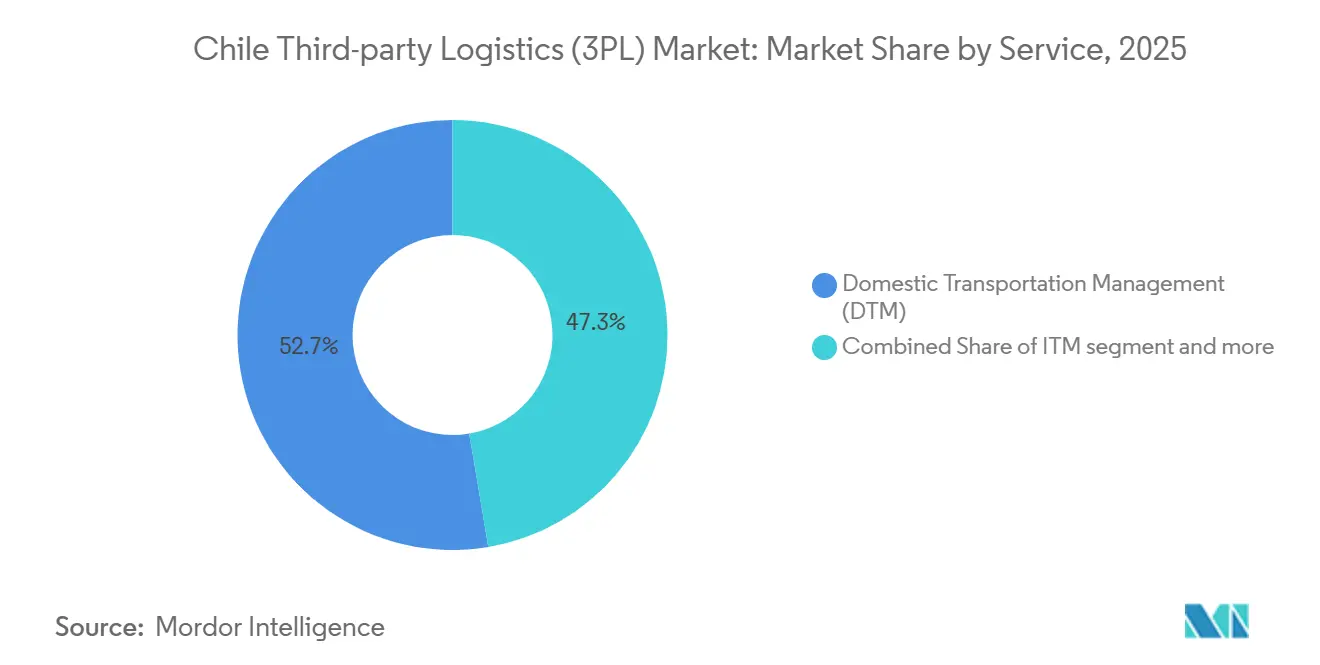

- By service, domestic transportation management led with 52.66% of Chile third-party logistics (3PL) market share in 2025, whereas international transportation management is the fastest-growing service, advancing at a 5.83% CAGR through 2031.

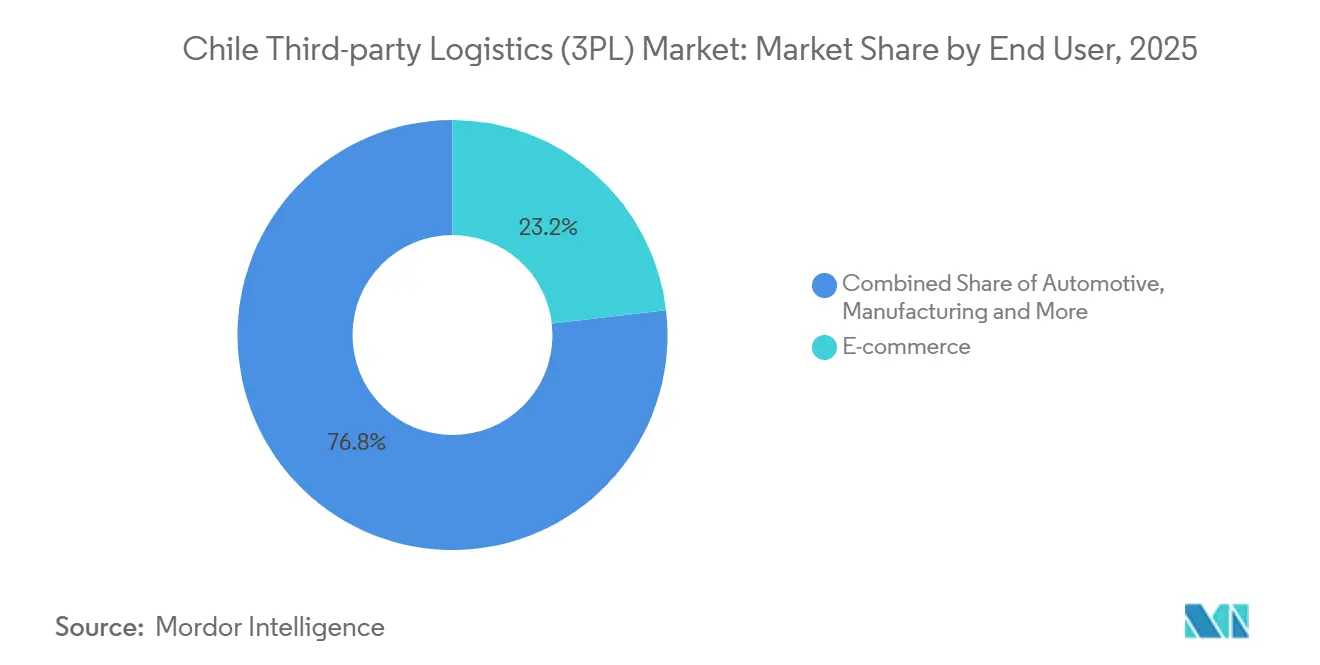

- By end user, e-commerce accounted for 23.17% of Chile third-party logistics (3PL) market size in 2025; life sciences & healthcare is rising at a 7.42% CAGR through 2031 as Santiago’s biotech cluster and national vaccine output expand.

- By logistics model, asset-light providers accounted for 39.04% of revenue in 2025, but hybrid models are forecast to grow at a 6.18% CAGR, reflecting a need for both dedicated cold-chain assets and flexible subcontracting.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Chile Third-party Logistics (3PL) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lithium-mining upswing accelerating bulk & project-cargo demand | +1.3% | Antofagasta, Atacama | Long term (≥ 4 years) |

| Salmon & aquaculture export boom boosting temperature-controlled logistics | +1.0% | Los Lagos, Aysen corridors | Medium term (2-4 years) |

| National e-customs single-window (VUCE) is slashing border dwell times | +0.8% | Major ports, land crossings | Short term (≤ 2 years) |

| Pacific Alliance cross-docking hubs spurring regional fulfillment flows | +0.7% | Santiago, Valparaíso zones | Medium term (2-4 years) |

| Renewable-energy mega-projects requiring remote heavy-lift services | +0.6% | Atacama Desert, Patagonia | Long term (≥ 4 years) |

| Bonded “dry-port” parks in the Santiago peri-urban belt, unlocking capacity | +0.5% | Santiago metropolitan area | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lithium-Mining Upswing Accelerating Bulk & Project-Cargo Demand

The Codelco-SQM partnership targets an extra 300,000 tons of lithium between 2025 and 2030, then 280,000-300,000 tons per year to 2060, ensuring decades of oversized-load movements for specialized 3PLs. These shipments originate over 1,600 kilometers from Santiago and 200 kilometers from the nearest deep-water berth, demanding convoy escorts, modular plant transport, and chemical-grade tank ISO containers. Environmental mandates on closed-loop water systems require additional certification steps, giving operators with ISO 14001 credentials and dust-sealed rolling stock a strategic advantage in the Chile third-party logistics (3PL) market.

Salmon & Aquaculture Export Boom Boosting Temperature-Controlled Logistics

Chile exported USD 6.5 billion in salmon in 2025, about a 3% increase from 2024. Maintaining a strict -25 °C to 4 °C band over a 1,000-kilometer south-to-north corridor obliges 3PLs to deploy IoT-enabled reefers, real-time telemetry, and contingency nodes for rapid cross-dock. Temperature excursions can devalue cargo by up to 30%, so providers offering automated alerts and blockchain traceability secure premium rates within the Chile third-party logistics (3PL) market.

National E-Customs Single-Window (VUCE) Slashing Border Dwell Times

By consolidating 27 agency checks into a single digital portal, VUCE reduces compliant release times to under 24 hours and streamlines preferential-tariff calculations across 65 FTAs[1]World Bank, “Single Window Systems: What We Have Learned,” worldbank.org . 3PLs that link VUCE APIs into warehouse and TMS platforms slash buffer stock and speed cash conversion. Digital disparities at minor crossings drive route realignment toward high-throughput gateways, altering lane economics throughout the Chile third-party logistics (3PL) market.

Pacific Alliance Cross-Docking Hubs Spurring Regional Fulfillment Flows

Mutual AEO recognition between Chile, Peru, Colombia, and Mexico trims inspection delays 40-60% and encourages consolidated backhauls that lift load factors[2]SELA, “The Pacific Alliance: A Successful Integration Mechanism,” sela.org . Santiago’s mid-continent time zone supports late order cut-offs, and Valparaiso cross-docks combine sea-air flows for next-day delivery northward. Continued tariff harmonization promises sustained throughput gains for the Chile third-party logistics (3PL) market, although divergent fiscal policies could slow integration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Truck-driver shortage & aging workforce inflating labor costs | −0.9% | National, southern farm belts | Short term (≤ 2 years) |

| Rising electronic toll-road tariffs are squeezing domestic haulage margins | −0.7% | Pan-American Route 5, urban rings | Medium term (2-4 years) |

| Sparse rail-freight network limiting modal shift potential | −0.6% | Central & southern regions | Long term (≥ 4 years) |

| Coastal shipping cabotage rules restricting short-sea options | −0.4% | Entire coastline | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Truck-Driver Shortage & Aging Workforce Inflating Labor Costs

The median driver age exceeds 50 years, and licensing hurdles deter new entrants, pushing seasonal wage premiums to 35% above baseline. Rest-hour ceilings further cap productivity. These pressures raise the cost-per-kilometer and compel the use of relay models, trimming net margins across Chile's third-party logistics (3PL) market.

Rising Electronic Toll-Road Tariffs Squeezing Domestic Haulage Margins

More than 3,000 kilometers of electronic tollways account for 12% of long-haul operating expenses, with hikes frequently surpassing inflation[3]Office of the United States Trade Representative, “Chile Country Commercial Guide – Transportation Services,” ustr.gov . Multi-tag billing disputes, no rebates for empty returns, and unavoidable toll chokepoints erode EBIT for asset-heavy fleets within the Chile third-party logistics (3PL) market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: International Flows Outperform Domestic Stalwarts

Chile third-party logistics (3PL) market share stood at 52.66% for domestic transportation management in 2025, while international transportation management is expanding at a CAGR of 5.83%. The dominance of domestic transport reflects Chile’s long geography and limited rail infrastructure, making road freight the backbone of logistics. However, escalating toll costs and driver shortages continue to constrain profitability for service providers.

To mitigate these pressures, many operators are deploying telematics-guided platooning and dynamic load-matching technologies to enhance fleet utilization and asset efficiency. At the same time, international transportation growth is supported by Chile’s extensive network of trade agreements and the VUCE digital clearance platform, which enables forwarders to pre-release cargo and reduce border processing times.

By End User: Healthcare Cold Chain Breaks into Double-Digit Growth

Chile third-party logistics (3PL) market size is led by e-commerce at 23.17%, while life sciences & healthcare is the fastest-growing vertical at a CAGR of 7.42%. Growth in healthcare logistics is driven by vaccine fill-and-finish investments and the development of a Santiago biotech hub, increasing demand for GDP-compliant storage, validated temperature sensors, and end-to-end serialization capabilities. Although E-commerce remains the largest vertical, it is gradually maturing, prompting logistics providers to prioritize operational efficiency and cost optimization over aggressive capacity expansion. Meanwhile, mining and energy shipments provide a steady base load for logistics activity, as ongoing large-scale investment programs continue to generate consistent demand for heavy-haul and project cargo transportation across key industrial corridors.

The food & beverages segment relies on highly controlled cold-chain networks, particularly for export-oriented perishables such as cherries, grapes, and salmon, requiring precise temperature management and time-sensitive distribution. At the same time, technology & electronics are emerging as a higher-value logistics stream, driven by expanding digital infrastructure and data-center development, which is increasing the need for secure, time-critical movement of specialized equipment and high-value spare parts across Chile’s third-party logistics (3PL) network.

By Logistics Model: Hybrids Balance Capital and Agility

Chile third-party logistics (3PL) market share shows asset-light brokers accounting for 39.04% of the 2025 mix, while hybrid operations are projected to expand at a CAGR of 6.18% through 2031. Asset-light models remain attractive due to their flexibility and lower capital requirements, allowing providers to scale capacity without significant fixed investments. However, specialized cargo such as lithium-processing equipment, wind turbine components, and temperature-sensitive vaccine shipments requires dedicated assets and specialized technical handling capabilities. As a result, hybrid providers are gaining traction by owning mission-critical assets such as refrigerated fleets and heavy-lift trailers while outsourcing more standardized transport legs.

This balanced operating approach enhances resilience against external cost pressures such as toll increases and workforce shortages by combining owned strategic assets with outsourced capacity for standardized routes. It allows providers to maintain service reliability while preserving financial flexibility. At the same time, asset-heavy incumbents continue to focus on specialized, high-barrier segments where direct asset ownership delivers clear operational advantages. In these niches, companies are increasingly prioritizing predictive maintenance technologies and advanced utilization analytics to optimize performance, control costs, and protect margins in a more competitive and efficiency-driven environment.

Geography Analysis

Northern macro-zones led by Antofagasta and Atacama form a major freight hub within the Chile third-party logistics (3PL) market, primarily driven by mining and related industrial supply chains, thanks to copper, molybdenum, and fast-growing lithium output tied to multi-decade concessions[4].Oficina Económica y Comercial de España en Santiago, “El Sector de la Minería en Chile 2024,” Convoys face dust, altitude, and limited rest stops, so operators station mobile workshops and satellite-linked control towers at desert hubs. The Bioceanic Corridor will connect these ports to Paraguay and Brazil, opening access to the Atlantic and repositioning cross-border flows.

Central Chile, especially the Santiago metropolitan area, accounts for over 40% of the population and more than half of bonded warehouse square footage. The forthcoming Valparaiso-Santiago rail upgrade is expected to reduce transit times by 40% and GHG emissions by 20%, fostering intermodal viability. Cross-docks in Pudahuel and Quilicura already handle 26% of international inbound unit loads, reinforcing Santiago’s role as a nerve center of the Chile third-party logistics market.

Southern corridors, including Los Lagos, Aysen, and Magallanes, anchor temperature-controlled supply chains for salmon, mussels, and certified grass-fed beef. Reefers queue during the December-to-March harvest peaks, and capacity premiums rise by 18-22% above norms. Puerto Montt offers direct Asia sailings that shave three days from transit, but limited deep-freeze storage can clog flows. Investments in IoT-linked reefer yards and solar-assisted chillers aim to mitigate bottlenecks and solidify southern lanes as high-margin pillars of the Chile third-party logistics (3PL) market.

Competitive Landscape

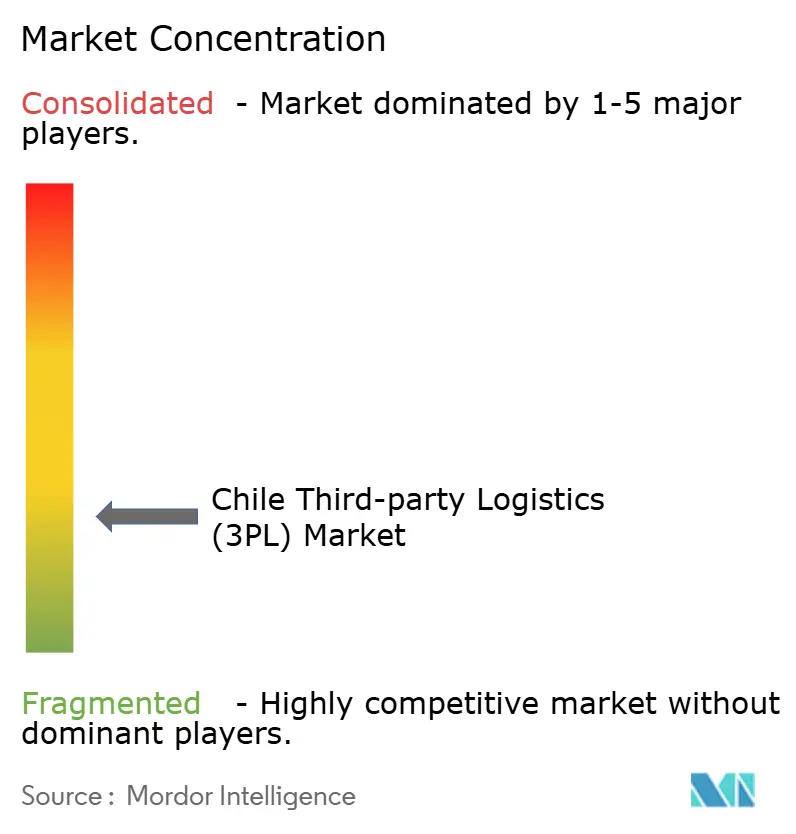

The third-party logistics (3PL) market in Chile is highly fragmented, with a low level of concentration among service providers. Ransa’s Loginsa buyout in 2024 vaulted it into cold-chain leadership, delivering 95 sites across 12 countries along the Pacific Coast. DSV’s EUR 14.3 billion (USD 15.5 billion) Schenker acquisition in 2025 boosted combined revenue to EUR 41.6 billion (USD 45.8 billion) and granted deeper capacity to carve share from local incumbents. Chilean specialists AGUNSA and Sitrans defend home turf via port concessions and mining expertise, often embedding staff in client pits.

Mercado Libre’s Mercado Envios funnels BRL 23 billion (USD 4.8 billion) into robotics, doubling Brazilian DCs to 21 and expanding regional air fleets. These moves let the platform bypass intermediaries, rerouting parcels directly through its own nodes and challenging small-parcel incumbents in the Chile third-party logistics (3PL) market. Technology adoption differentiates winners: robotics trims order cycles by 20% and lifts storage density by 15%. Chile’s revamped public procurement law elevates transparency and performance metrics, rewarding operators who document on-time scores over 98% and carbon footprints below corridor averages.

White-space opportunities persist in GDP-certified pharma cold chain and renewable-energy heavy-lift. Providers combining temperature validation, specialized rigs, and AI-driven routing expect premium yields, underscoring how depth of capability, not fleet size, dictates competitive leverage inside the Chile third-party logistics (3PL) market.

Chile Third-party Logistics (3PL) Industry Leaders

Agunsa

Deutsche Post DHL

Andes Logistics

Sitrans Servicios Integrados de Transportes

DSV A/S (incl. DB Schenker)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Mercado Libre extended its logistics network to San Pedro de Atacama to improve delivery speed in northern Chile (3,000 packages monthly).

- December 2025: Grupo Ransa will evaluate new warehouse sites and logistics investments in Chile toward 2026 to further strengthen its network.

- August 2025: Kuhene+ Nagel expanded its contract logistics services in Chile with a strategic collaboration with ABB, adding last-mile transport, warehousing, and integrated logistics from its Pudahuel facility.

- August 2025: Agunsa secured a long-term contract to operate 20,000 m² of warehouses in Coronel Bay, tripling cargo handling capacity in southern Chile.

Chile Third-party Logistics (3PL) Market Report Scope

By Service

| Domestic Transportation Management (DTM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| International Transportation Management (ITM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| Value-Added Warehousing & Distribution (VAWD) |

By End User

| Automotive |

| Energy & Utilities |

| Manufacturing |

| Life Sciences & Healthcare |

| Technology & Electronics |

| E-commerce |

| Consumer Goods & FMCG |

| Food & Beverages |

| Others |

By Logistics Model

| Asset-Light (Management-Based) |

| Asset-Heavy (Own Fleet & Warehouses) |

| Hybrid |

| By Service | Domestic Transportation Management (DTM) | Roadways |

| Railways | ||

| Airways | ||

| Waterways | ||

| International Transportation Management (ITM) | Roadways | |

| Railways | ||

| Airways | ||

| Waterways | ||

| Value-Added Warehousing & Distribution (VAWD) | ||

| By End User | Automotive | |

| Energy & Utilities | ||

| Manufacturing | ||

| Life Sciences & Healthcare | ||

| Technology & Electronics | ||

| E-commerce | ||

| Consumer Goods & FMCG | ||

| Food & Beverages | ||

| Others | ||

| By Logistics Model | Asset-Light (Management-Based) | |

| Asset-Heavy (Own Fleet & Warehouses) | ||

| Hybrid | ||

Key Questions Answered in the Report

How large will the Chile third-party logistics (3PL) market be by 2031?

It is forecast to reach USD 5.97 billion by 2031, expanding from USD 4.73 billion in 2026 at a 4.76% CAGR.

Which service segment is growing the fastest in Chilean logistics?

International Transportation Management shows the highest pace, advancing at a 5.83% CAGR, driven by 65 free trade agreements and streamlined customs.

Why is lithium production important for Chilean 3PL demand?

The Codelco–SQM alliance will add 300,000 tons of lithium output by 2030, triggering sustained requirements for project-cargo, heavy-haul, and chemical-grade container services.

What makes Life Sciences logistics a priority in Chile?

A 7.42% CAGR arises from vaccine fill-and-finish lines and Santiago’s biotech cluster, driving GDP-compliant cold-chain needs and serialization tracking.

How are hybrid logistics models gaining traction?

Operators blend owned reefers or heavy-lift fleets with outsourced general transport, balancing capital and agility and growing at a 6.18% CAGR through 2031.

Which regions inside Chile generate the most specialized logistics demand?

Antofagasta and Atacama dominate heavy-haul mining flows, Santiago concentrates bonded warehousing, and Los Lagos–Aysen corridors anchor temperature-controlled salmon exports.

Page last updated on: