Cell Analysis Instruments Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 24.55 Billion |

| Market Size (2031) | USD 34.49 Billion |

| Growth Rate (2026 - 2031) | 7.02% CAGR |

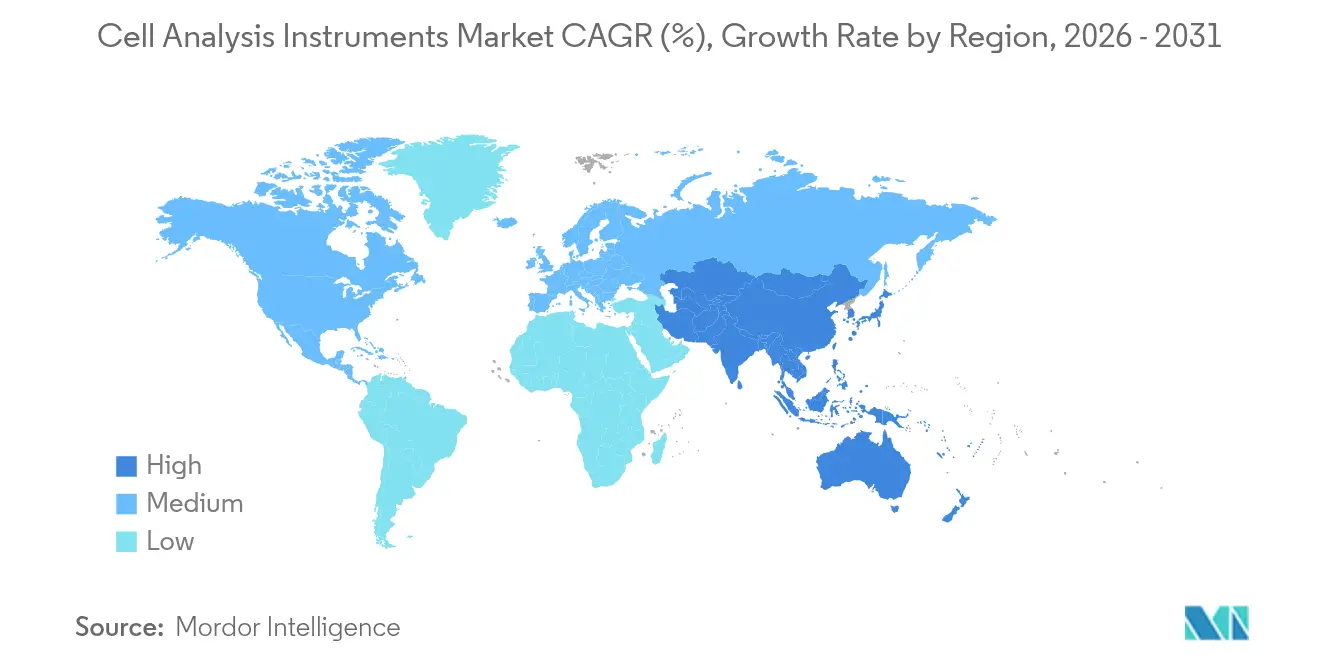

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cell Analysis Instruments Market Analysis by Mordor Intelligence

The cell analysis instruments market size is expected to grow from USD 22.94 billion in 2025 to USD 24.55 billion in 2026 and is forecast to reach USD 34.49 billion by 2031 at 7.02% CAGR over 2026-2031. Demand rises as chronic disease management shifts toward early molecular detection, artificial-intelligence (AI) driven imaging, and large-scale single-cell sequencing workflows that are now affordable for mid-sized laboratories. Consumables keep laboratories operational on a daily basis and already account for nearly half of 2024 revenue, while instrument innovation pushes spectral, high-content, and automation features into routine bench work. Geographically, North America continues to set the purchasing pace through generous National Institutes of Health (NIH) and National Science Foundation (NSF) instrumentation grants, whereas Asia-Pacific registers double-digit growth on the back of expanding biomanufacturing capacity. Regulatory clarity is improving; the US Food and Drug Administration (FDA) in 2025 classified multiplexed antimicrobial susceptibility cell-analysis systems as Class II devices, signalling confidence in advanced analytical platforms. Mergers and acquisitions—such as Thermo Fisher Scientific’s multi-year USD 40-50 billion expansion budget—underscore how scale and portfolio breadth will determine long-term competitive advantage.

Key Report Takeaways

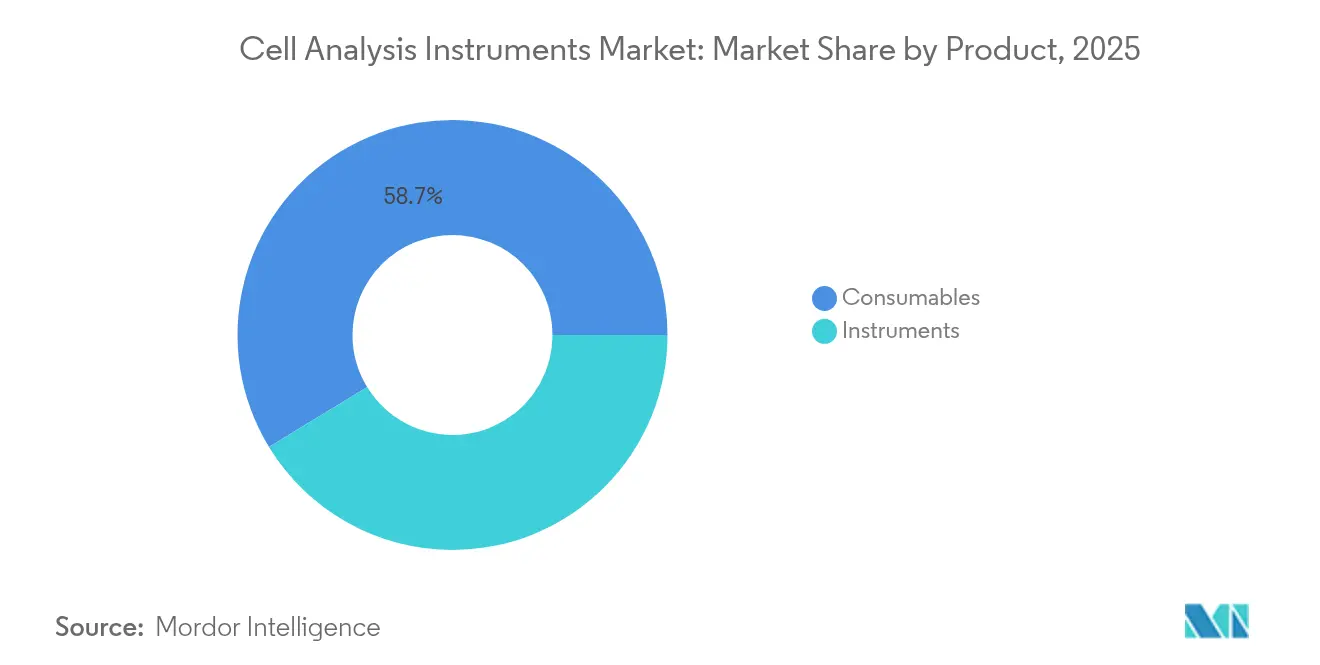

- By product category, consumables led with 58.72% revenue share in 2025, whereas instruments are forecast to expand at a 11.94% CAGR to 2031.

- By application, cell counting held 37.96% of the cell analysis instruments market share in 2025, while PCR/qPCR is projected to rise at a 12.54% CAGR through 2031.

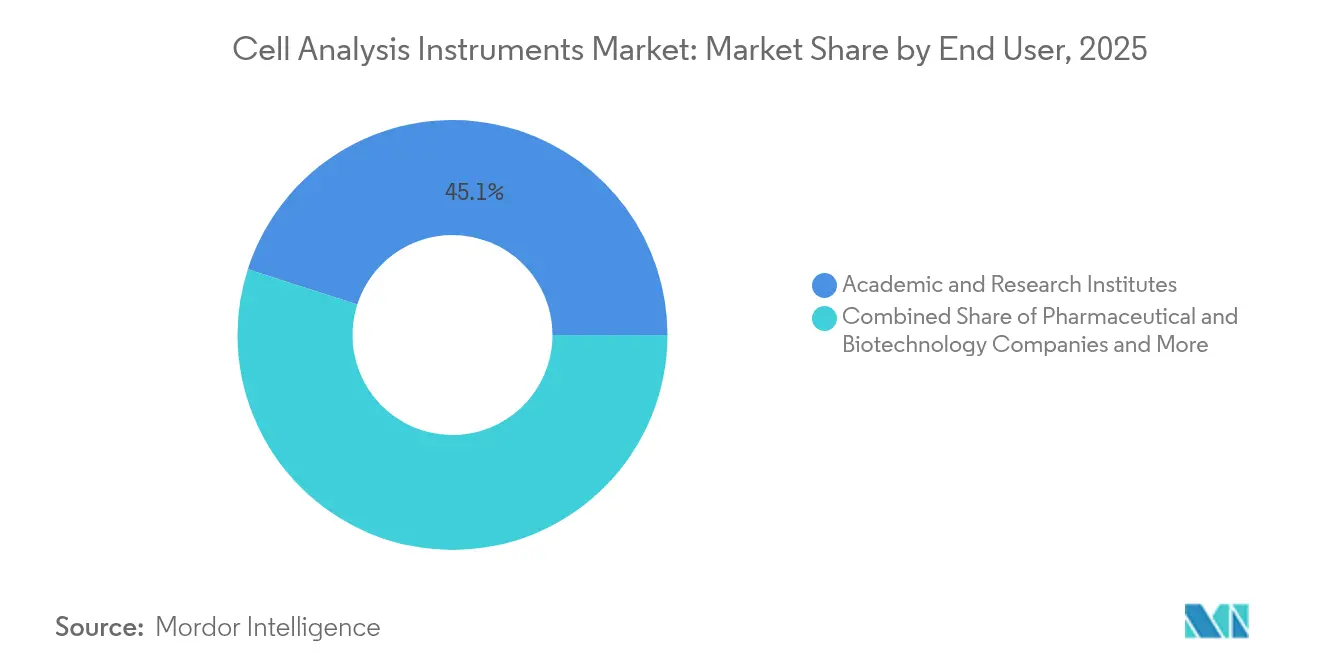

- By end user, academic and research institutes captured 45.05% of 2025 revenue, whereas contract research and CDMOs will post the fastest 12.06% CAGR.

- By geography, North America commanded 40.21% of 2025 revenue; Asia-Pacific is the fastest-growing region at an 11.75% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cell Analysis Instruments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic disease prevalence | +1.2% | Global, concentrated North America & Europe | Long term (≥ 4 years) |

| Biotech & cell-therapy pipeline expansion | +1.8% | North America & EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Falling single-cell sequencing costs | +1.5% | Global, led by North American research institutions | Short term (≤ 2 years) |

| Government funding for life-science tools | +0.9% | Primarily North America & EU; selective Asia-Pacific programs | Medium term (2-4 years) |

| AI-enabled image analysis | +1.1% | Global, concentrated in advanced research centers | Short term (≤ 2 years) |

| Demand for closed GMP-compliant microfluidics | +0.7% | Global, driven by cell-therapy manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in chronic disease prevalence

Growing cancer, cardiovascular, and metabolic disorder caseloads force health systems to prioritise early detection, pushing demand for high-throughput cellular profiling platforms that can uncover subtle phenotypic changes before symptoms manifest. The FDA’s 2024 approval of the Shield blood-based assay—with 83% colorectal cancer detection accuracy—demonstrates how multiparametric cell analysis supports mainstream screening[1]Center for Devices and Radiological Health, “Shield – P230009,” fda.gov. AI-enhanced histopathology algorithms now outperform manual reads in identifying invasive breast-tumour patterns. Cervical-cancer programmes that must screen 70% of women aged 35-45 by 2030 are adopting automated slide readers to compensate for pathologist shortages. These use cases cement a feedback loop in which clinical adoption validates technology and, in turn, draws further investment into the cell analysis instruments market.

Expansion of biotech and cell-therapy pipelines

More than 1,200 active US cell- and gene-therapy trials in 2024 propel purchases of spectral sorters, high-content imagers, and GMP-grade flow cytometers for in-process control. Roche’s USD 1.0-1.5 billion acquisition of Poseida Therapeutics highlights the rush to secure allogeneic CAR-T platforms that require rigorous cell phenotyping during scale-up. Tenpoint Therapeutics plans first-in-human retinal cell therapy studies by late 2025, widening analytical demand beyond oncology. Contract development and manufacturing organisations (CDMOs) fill capability gaps for smaller biotechs, bolstering instrument sales as they build analytical suites to serve multiple clients. Consequently, the cell analysis instruments market sees growth in both instrument platforms and consumable kits optimised for GMP environments.

Falling single-cell sequencing costs

Sequencing a single human genome once cost USD 100 million; by 2023 that figure dropped to just above USD 500, and further decreases unlock single-cell RNA-seq protocols for standard bench science. Comparative testing shows 10x Genomics’ fixed RNA profiling kit outperforming peers on transcript capture, whereas Becton Dickinson’s Rhapsody kit delivers lower cost per cell[2]De Simone et al., “Comparative Analysis of Commercial Single-Cell RNA Sequencing Technologies,” biorxiv.org. Droplet microfluidics now screens millions of individual cells in hours, reshaping expectations for throughput. As a result, institutions that once outsourced sequencing now buy integrated instruments, expanding the addressable cell analysis instruments market across academic, clinical, and industrial labs.

AI-enabled image analysis boosting throughput

Machine learning automates the extraction of dozens of morphological and fluorescence-based parameters from every cell image. BD’s FACSDiscover A8 analyser collects spectral flow and real-time images on 50-plus markers in one run, thereby collapsing weeks-long manual work into a single day. Nikon’s AX R microscope records six-times faster and four-times wider fields than previous confocal systems, making live-cell dynamics observable in near real time. Synthetic labelling via generative AI promises to replace certain immunofluorescence steps, lowering reagent spend while preserving information content. Collectively, these advances improve per-run economics, further accelerating adoption across the cell analysis instruments market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of flagship instruments | -0.8% | Global, more acute in emerging markets | Long term (≥ 4 years) |

| Complex multi-jurisdiction regulatory path | -1.2% | Global, centered North America & European Union | Medium term (2-4 years) |

| Bio-informatics talent shortage | -0.9% | Global, acute in specialised research centres | Long term (≥ 4 years) |

| Rare-earth supply chain risk | -0.6% | Global, impacts high-end optics and detectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High capital cost of flagship instruments

State-of-the-art spectral flow cytometers, high-content imagers, and mass cytometry platforms often list above USD 500,000, pricing out many teaching hospitals and public universities. NIH attempts to bridge the gap with High-End Instrumentation grants that award USD 750,000-2 million for single items. Yet the number of eligible proposals still far exceeds available funds, evidenced by Bio-Rad’s 5.4% year-over-year decline in academic sales during Q1 2025. Shared-use cores improve utilisation but lengthen queue times, occasionally compromising experimental timelines. Currency swings and import levies amplify costs in developing markets, dampening unit shipments and slowing cell analysis instruments market penetration where unmet medical need is rising fastest.

Complex multi-jurisdiction regulatory path

The FDA’s final rule on laboratory-developed tests mandates a five-stage transition from 2025 through 2029, imposing new pre-market review obligations that will cost laboratories USD 566 million to USD 3.56 billion annually. Europe continues to refine In Vitro Diagnostic Regulation (IVDR) implementation, while Japan and China maintain separate device-registration pathways. Vendors must customise labelling, firmware, and quality-system documentation for every major jurisdiction, stretching regulatory affairs budgets. Smaller innovators often seek strategic alliances or acquisition exits rather than navigate alone, indirectly feeding consolidation within the cell analysis instruments market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Consumables Sustain Revenue Streams

Consumables generated 58.72% of 2025 revenue and deliver predictable margins because laboratories reorder assay kits, reagents, and disposable cartridges throughout an instrument’s life cycle. Flagship instrument launches nevertheless propel top-line growth; the BD FACSDiscover S8 spectral sorter marries high-speed imaging with traditional fluorescence to enable phenotype-based sorting, a first for the category. Yokogawa’s CellVoyager CQ3000 offers live 3-D imaging of organoids using sCMOS cameras, broadening single-plate analytical capacity. As new optical paths and on-board AI shorten protocols, laboratories replace older hardware earlier than the typical seven-year depreciation curve, supporting a 11.94% CAGR for instruments. Spectrophotometers, microarrays, and advanced microscopes plug into cloud-based analytic dashboards that automate compliance documentation, securing recurring software subscriptions that anchor vendors deeper into the cell analysis instruments market.

Second-order effects further reinforce consumable demand. AI-assisted assays often multiplex more biomarkers per run, increasing reagent pull-through. Spectral flow cytometry requires proprietary dye panels optimised for narrow emission bins, converting technique adoption directly into consumable sales. Collectively, these drivers ensure that consumables remain the volume backbone, while big-ticket hardware remains the swing factor in annual revenue for the cell analysis instruments industry.

By Application: PCR/qPCR Accelerates Beyond Traditional Counting

Cell counting still led with a 37.96% slice of 2025 spending, reflecting routine viability checks, dose calculations, and basic QC across research and clinical labs. Yet PCR/qPCR applications are projected to expand at 12.54% annually through 2031 as laboratories migrate toward molecular endpoints. The ClearLLab 10C panel analyses samples at 0.0469 × 10⁶ cells/mL—far below conventional thresholds—underscoring how sensitive reagent mixes unlock low-input workflows for oncology and immune profiling. Coupling cell culture monitoring with real-time polymerase reads collapses days of incubator waiting into hours, increasing experimental throughput.

Target-identification workflows, especially CRISPR screens, now integrate transcriptomic and proteomic readouts, escalating data volume exponentially. This multi-omics convergence elevates informatics requirements and pushes demand for turnkey analysis software that accompanies instrument installs. Drug-screening and biomarker-discovery labs adopt microfluidics to evaluate thousands of conditions in parallel, further enlarging the cell analysis instruments market size for high-throughput platforms.

By End User: CDMOs Drive Manufacturing Transformation

Academic and research institutions dominated 2025 revenue at 45.05%, buoyed by public funding streams like the NIH S10 programmes and NSF biotechnology allocations. Yet the fastest growth—12.06% CAGR—comes from CDMOs that scale cell-therapy manufacturing for multiple sponsors. These facilities require validated, 21 CFR Part 11-compliant analytics to release GMP batches, stimulating purchases of inline flow cytometers, sterility testers, and automated microscopy. Pharmaceutical and biotech companies remain steady buyers but increasingly outsource late-stage process development, shifting incremental demand toward CDMOs. Clinical laboratories round out the segment mix as FDA clarifies pathways for integrating multiplex cell-analysis systems into routine diagnostic testing, which bolsters confidence to invest in high-end instruments.

Geography Analysis

North America retains leadership with 40.21% of 2025 revenue, anchored by NIH High-End Instrumentation grants of USD 750,000-2 million per award and USD 421 million in NSF biotechnology budget for fiscal 2025. Robust venture funding, a mature biopharma cluster, and early-adopter culture pushed laboratories to adopt AI-enabled analytical platforms ahead of other regions. Canada’s federal innovation funds and Mexico’s burgeoning contract-manufacturing footprint add to regional demand; Shimadzu’s new Mexican subsidiary aims for 150% business growth by 2028, signalling instrument vendors’ confidence in the market. The current cell analysis instruments market size for North America supports vendors specialising in premium instrumentation, bioprocess analytics, and cloud-connected data services.

Asia-Pacific registers the highest growth rate at 11.75% CAGR through 2031. China’s pivot toward Southeast Asian biopharma investments and control of 90% global rare-earth output influences supply security for optical components. India’s ambition to become a Quad biomanufacturing hub positions the region for demand in closed, GMP-compliant analytical suites. Japan’s Nikon and Yokogawa supply cutting-edge imagers that feed back into domestic adoption, while South Korea invests heavily in precision-medicine infrastructure. Consequently, the cell analysis instruments market enjoys both manufacturing cost advantages and large untapped clinical segments across Asia’s diverse economies.

Europe maintains a solid installed base thanks to clustered pharma activity in Germany, the United Kingdom, and France. Coordinated research funding, combined with IVDR roll-out, ensures a stable if moderate demand trajectory. Eastern European nations look to EU structural funds to modernise laboratory infrastructure, creating future unit-growth pockets. Meanwhile, the Middle East and Africa begin to modernise pathology labs and life-science education facilities, often bundled with technology-transfer agreements. These regions contribute a small but rising share of the global cell analysis instruments market as governments diversify away from hydrocarbon-driven economies.

Competitive Landscape

Market structure tilts toward moderate concentration as leading players use acquisitions to broaden technology stacks. Danaher generated USD 24 billion across biotechnology, life-science, and diagnostics units in 2023 while investing USD 1.5 billion in R&D, demonstrating the fiscal firepower needed to sustain innovation cycles. Roche, Agilent, and Bruker augment internal pipelines with targeted buys that extend into spatial, proteomic, or environmental analytics, creating interlocking ecosystems of instruments, reagents, and software.

Technology differentiation now centres on AI, spectral analysis, and single-cell depth. BD’s spectral sorter and analyser launches combine real-time imaging with cytometry to offer phenotypic gating previously impossible on traditional sorters. Nikon introduces super-resolution confocal systems packaged with neural-network image-reconstruction tools, recasting microscopy as a data science problem. Vendors with proprietary chemistries—fluorochromes, antibody panels, and microfluidic cartridges—lock-in recurring consumables revenue, raising switching costs for end users and deepening vendor relationships in the cell analysis instruments market.

Still, white-space remains. Mid-tier firms exploit gaps for cost-effective single-cell proteomics or microfluidic-based drug-screening platforms. Supply-chain dependency on rare-earth magnets and specialised lasers incentivises near-shoring strategies, with US rare-earth output reaching 45,000 tons valued at USD 260 million in 2024[3]U.S. Geological Survey, “Mineral Commodity Summaries 2025,” usgs.gov. Start-ups offering AI-native software suites for multi-omics data integration attract venture funding, frequently partnering with instrument majors for distribution. As consolidation proceeds, competitive intensity will continue to hinge on the ability to deliver complete, compliant, and cost-efficient workflows.

Cell Analysis Instruments Industry Leaders

Becton Dickinson and Company

Sartorius AG

Merck KGaA

Thermo Fisher Scientific

Danaher Corp. (Beckman Coulter Life Sciences)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Bruker Corporation unveiled the timsMetabo platform and integrated RECIPE ClinMass kits with EVOQ DART-TQ+ for therapeutic drug monitoring.

- May 2025: BD launched the FACSDiscover A8 cell analyser, combining spectral cytometry with real-time imaging to profile more than 50 parameters per cell.

Global Cell Analysis Instruments Market Report Scope

As per the scope of the report, cell analysis deals with the study of cells, which are isolated from tissues in multicellular organisms and unicellular organisms. Cellular analysis plays a vital role in gene identification, protein identification, epigenomics, and other life science-related areas. It is a natural process to study the genetic and phenotypical characteristics of an organism. Cell analysis instruments include consumables such as reagents, assays, kits, and instruments that are required during cell analysis.

The cell analysis instruments market is segmented by Product (Instruments and Consumables), Application (Cell Counting, Cell Viability, Cell Identification, Target Identification, PCR, Others), End-User (Academic and Research Institutes, Pharmaceutical & Biotechnology Companies, Others), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above-mentioned segments.

| Instruments | Microscopes |

| Flow Cytometers | |

| Spectrophotometers | |

| Cell Microarrays | |

| Other Instruments | |

| Consumables |

| Cell Counting |

| Cell Viability |

| Cell Identification |

| Target Identification |

| PCR / qPCR |

| Other Applications |

| Academic & Research Institutes |

| Pharmaceutical & Biotechnology Companies |

| Contract Research & CDMO |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Instruments | Microscopes |

| Flow Cytometers | ||

| Spectrophotometers | ||

| Cell Microarrays | ||

| Other Instruments | ||

| Consumables | ||

| By Application | Cell Counting | |

| Cell Viability | ||

| Cell Identification | ||

| Target Identification | ||

| PCR / qPCR | ||

| Other Applications | ||

| By End-User | Academic & Research Institutes | |

| Pharmaceutical & Biotechnology Companies | ||

| Contract Research & CDMO | ||

| Other End-Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected size of the cell analysis instruments market by 2031?

The market is forecast to reach USD 34.49 billion by 2031, growing at a 7.02% CAGR over 2026-2031 from its USD 22.94 billion valuation in 2025.

Which product segment grows fastest within the cell analysis instruments industry?

Instrumentation platforms—particularly spectral flow cytometers and high-content imagers—are set to advance at a 11.94% CAGR between 2026 and 2031.

Why is Asia-Pacific the fastest-expanding region?

Local biomanufacturing investments, rare-earth supply advantages, and rising healthcare expenditure lift Asia-Pacific demand, yielding an 11.75% CAGR through 2031.

How do AI tools influence adoption?

AI automates image interpretation and multiparameter gating, which cuts analysis time dramatically and justifies upgrades to advanced platforms.

What challenges limit faster uptake?

High capital expenditure, multi-jurisdiction regulatory complexity, shortages of bio-informatics talent, and rare-earth supply risks temper otherwise strong growth drivers.

Page last updated on: