Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

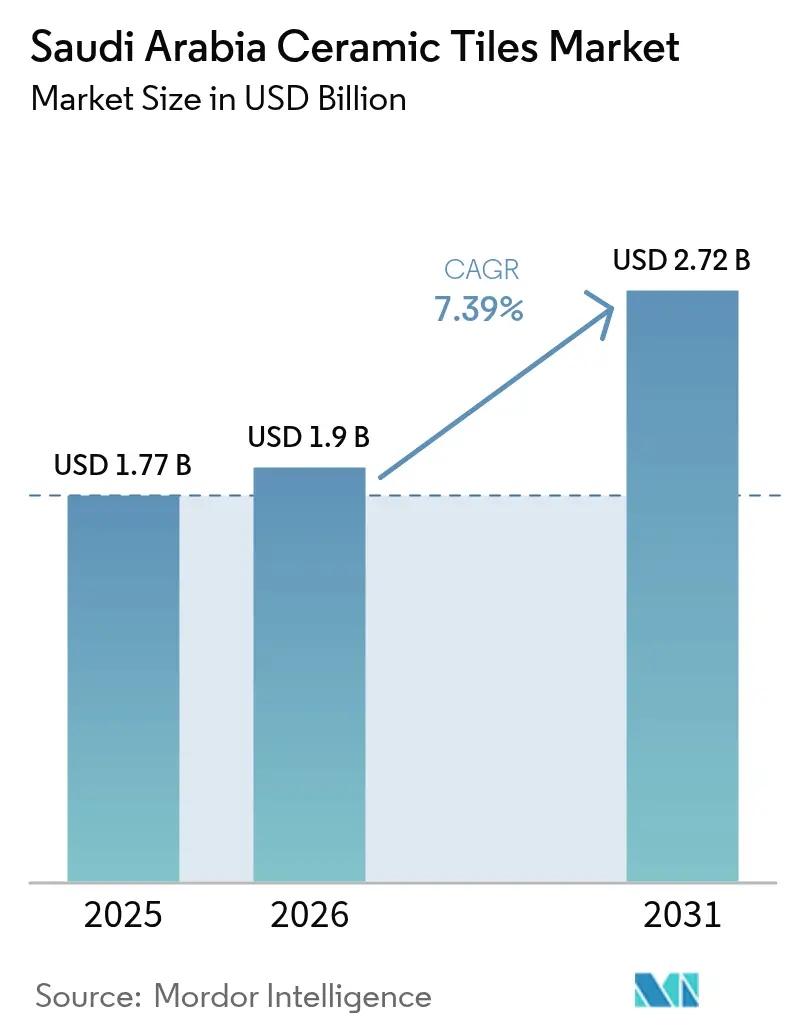

| Base Year Market Size (2025) | USD 1.77 Billion |

| Market Size (2026) | USD 1.9 Billion |

| Market Size (2031) | USD 2.72 Billion |

| Growth Rate (2026 - 2031) | 7.39% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Ceramic Tiles Market Analysis by Mordor Intelligence

Saudi Arabia ceramic tiles market size in 2026 is estimated at USD 1.90 billion, growing from 2025 value of USD 1.77 billion with 2031 projections showing USD 2.72 billion, growing at 7.39% CAGR over 2026-2031. Massive construction spending tied to Vision 2030, highlighted by mega-projects such as NEOM’s SAR 1.3 billion (USD 0.35 billion) automation joint venture and ROSHN’s SAR 37.5 billion (USD 10.0 billion) residential contracts, is the primary volume catalyst. The USD 950 billion national project pipeline, equal to 62% of total MENA construction value, positions the Kingdom as the world’s largest construction arena by 2028 [1]JLL, “Saudi Construction Pipeline Outlook 2025,” jll.com. Climate-driven shifts toward porcelain and glazed surfaces, together with a premium turn to large-format and anti-bacterial finishes, are reshaping product specifications. Mandatory 70% local-content thresholds under the IKTVA program and rising natural-gas tariffs are further steering manufacturers toward efficient kilns and dry-granulation technology that lowers gas use from 46 m³/ton to 15 m³/ton [2]Saudi Aramco, “IKTVA Program Supplier Manual 2024,” aramco.com

Key Report Takeaways

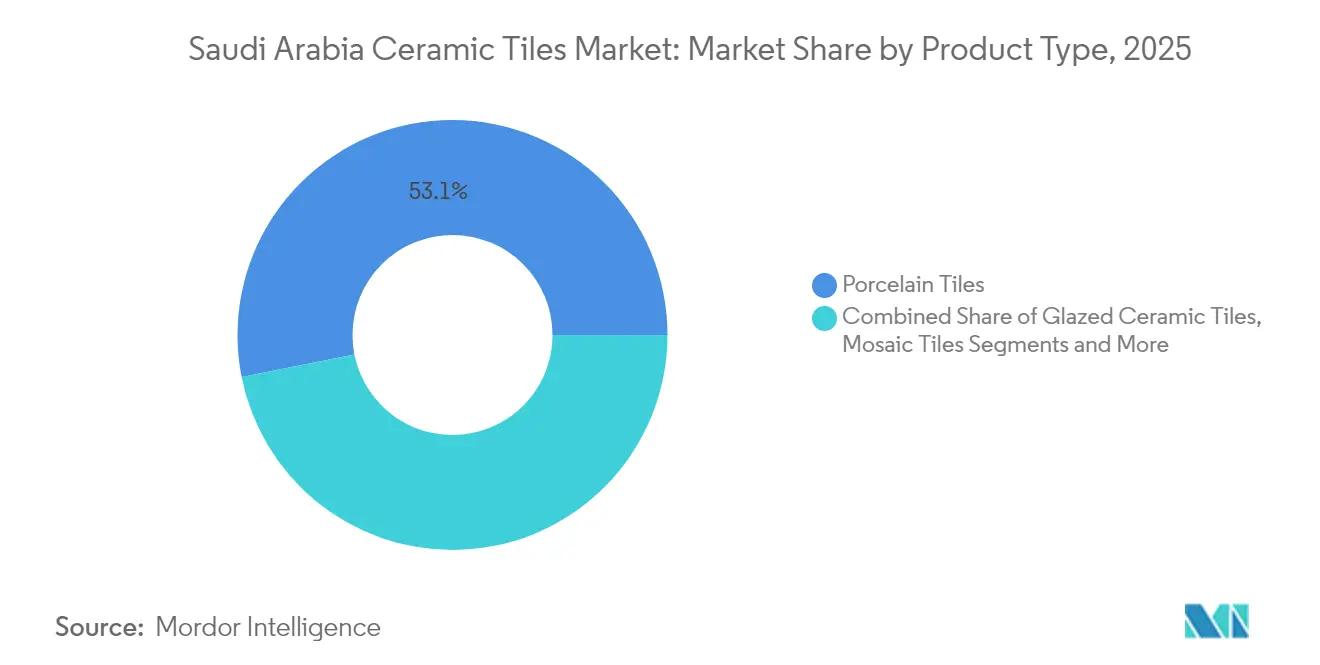

- By product type, porcelain tiles held 53.12% of Saudi Arabia ceramic tiles market share in 2025 while unglazed tiles are projected to record the fastest 8.10% CAGR to 2031.

- By application, floor coverings captured 61.78% of the Saudi Arabia ceramic tiles market size in 2025 and are expected to advance at a 7.72% CAGR through 2031.

- By end-user, residential construction accounted for 59.34% of 2025 revenue and is on track for an 7.86% CAGR on the back of more than 400,000 new housing units in the pipeline.

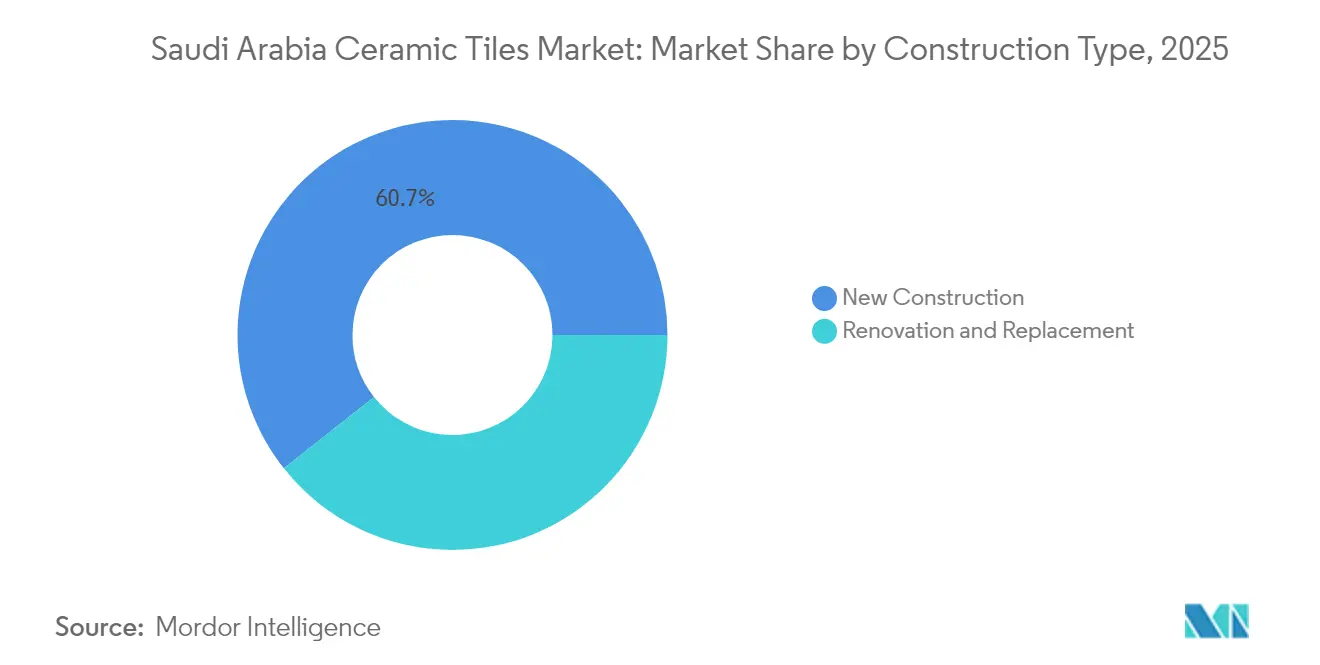

- By construction type, new-build activity contributed 60.65% of demand in 2025, expanding at an 8.18% CAGR as giga-projects move from design to execution.

- By distribution channel, specialty tile stores led with 47.55% share in 2025, whereas online platforms represent the fastest-growing outlet at an 7.96% CAGR.

- By geography, Riyadh commanded 31.75% of 2025 sales; the Eastern Province is the quickest climber with a 7.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in residential construction | +1.8% | Nationwide; early gains in Riyadh, Eastern Province, Makkah | Medium term (2-4 years) |

| Mega-projects (NEOM, Red Sea, Qiddiya) | +2.1% | Western & Northern regions; spillover to Riyadh | Long term (≥ 4 years) |

| Climate-driven preference for porcelain | +0.9% | Country-wide; strongest in Eastern & Western regions | Short term (≤ 2 years) |

| Premiumization toward large-format tiles | +1.2% | Riyadh, Makkah, Madinah | Medium term (2-4 years) |

| Adoption of energy-efficient kilns | +0.7% | National industrial clusters | Short term (≤ 2 years) |

| Local-content incentives | +1.1% | National; focus on Eastern Province industrial hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Residential Construction Under Vision 2030 Housing Schemes

Vision 2030 aims to lift the home-ownership rate above 70% by 2030, and ROSHN alone plans 400,000 units across nine cities, including the 30,000-unit SEDRA community in northern Riyadh. [3]ROSHN, “SEDRA Master Plan Overview,” roshn.sa. Government-backed mortgages and infrastructure outlays are encouraging private developers to accelerate ground-breaking schedules, locking in multi-year demand visibility for ceramic floor and wall packages. Standards issued by SASO now require higher energy efficiency and low-VOC finishes, pressuring suppliers to deliver compliant tile formulations. Rising suburban projects in secondary cities are broadening geographic consumption beyond Riyadh, Jeddah, and Dammam. Collectively these factors underpin sustained volume growth for producers meeting local-content and sustainability benchmarks.

Mega-Projects Boosting Tile Demand Through NEOM, Red Sea, and Qiddiya

NEOM’s SAR 1.3 billion (USD 0.35 billion) robotics investment with Samsung C&T signals unprecedented construction scale, with early civil works already consuming large-format porcelain for infrastructure command centers. The Port of NEOM, designed for net-zero operations, mandates high-performance, chemically resistant flooring for logistics halls exposed to salt spray. Red Sea Global requires durable, UV-stable glazed tiles for resort boardwalks, while Qiddiya’s entertainment venues specify anti-slip ceramic for pedestrian zones and aquatic attractions. Phased rollouts ensure overlapping procurement cycles, smoothing order intake for tile makers through 2029. Successful material trials at these giga-sites are expected to ripple into conventional projects nationwide.

Climate-Driven Preference for Porcelain and Glazed Tiles

Porcelain’s sub-0.5% water-absorption rate delivers dimensional stability during daily 20 °C temperature swings common in Riyadh summers. Glazed finishes minimize dust adhesion, simplifying maintenance in desert environments where airborne particulates exceed 200 µg/m³ on peak days. Recent R-&D has embedded silver-ion antimicrobial layers into porcelain glazes, supporting infection-control protocols in expanding healthcare and hospitality facilities. Light-toned surfaces reflect solar gain, trimming interior cooling loads and aligning with the Kingdom’s building-energy code. Architects now prespecify porcelain for façades in coastal sites such as Jeddah Corniche to avoid efflorescence, further widening its usage envelope.

Premiumization Toward Large-Format and Anti-Bacterial Tiles

Tile dimensions above 600 mm×600 mm are increasingly standard in luxury villas and Grade-A offices where seamless aesthetics and reduced grout maintenance drive specifier decisions. On NEOM pilot plots, robotic setters laid 1,200 mm×2,400 mm slabs 25% faster than traditional sizes, demonstrating labor savings that offset higher unit prices. Healthcare campuses in Dammam have shifted purchase orders to titanium-dioxide coated porcelain that provides continuous antimicrobial protection, dovetailing with Ministry of Health hygiene directives. Digital inkjet printing now renders marble-look slabs at 600 dpi, meeting high-end design briefs while avoiding natural stone’s weight and porosity drawbacks. Producers capable of large-format firing and advanced surface treatments command price premiums up to 18% over commodity SKUs.

Restraints Impact Analysis*

| Restraint | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material and energy cost volatility | -1.4% | Nationwide; highest in Eastern Province clusters | Short term (≤ 2 years) |

| Price-led competition from Asian imports | -0.8% | Whole market; acute in Riyadh & Dammam | Medium term (2-4 years) |

| Water-scarcity constraints | -0.6% | Central & northern regions | Long term (≥ 4 years) |

| Stricter silica-dust emission regulations | -0.3% | Established manufacturing zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material and Energy Cost Volatility

Global price swings in clay, feldspar, and silica sand can lift production costs by up to 20% within a quarter, compressing margins for smaller Saudi kilns that lack hedging programs. Domestic energy reforms raised natural-gas tariffs, forcing a shift to energy-saving presses and low-friction rollers that demand fresh capex. Limited local clay reserves oblige import reliance, exposing buyers to currency swings versus EUR and CNY. The Ministry of Industry’s plan to issue 22 quarry licenses may ease pressure, yet full output is not expected before 2027. [4]Ministry of Industry & Mineral Resources, “Quarry Licensing Round III,” mim.gov.sa Volatility complicates fixed-price tenders for giga-projects where penalties apply for late delivery or price escalation.

Price-Led Competition From Asian Imports

The 2023 removal of GCC anti-dumping duties on Indian tiles reopened a trade lane once subject to surcharges of 106%, pushing CIF prices down by 12-15%. Indian shipments rebounded from USD 245 million in 2022 toward pre-duty levels, while Chinese suppliers exploit scale economies to undercut domestic quotes in the mid-market. Private developers, less bound by IKTVA, increasingly award contracts to importers offering 60-day payment terms and consolidated container loads. Local brands respond by promoting faster delivery, customized cutting, and on-site technical support—services importers struggle to match. Nevertheless, sustained price pressure may push smaller Saudi plants into mergers or niche specializations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Porcelain Dominance Drives Premium Shift

Porcelain held 53.12% of 2025 revenue owing to its sub-0.5% water absorption, thermal-shock endurance, and superior abrasion resistance, attributes ideally matched to harsh Gulf climates. Saudi Arabia ceramic tiles market size for porcelain is projected to extend its lead as architects favor 20 mm outdoor slabs and slim 6 mm interior panels that cut structural weight without sacrificing strength. Unglazed tiles, while cost-efficient, are positioned for workshops and budget housing; still, their 8.10% CAGR makes them the fastest-growing slice due to condensed firing cycles that lower selling prices. Glazed formats keep a foothold in hospitality and retail décor where stain-proof finishes command premiums. Digital-printing advances allow all segments to replicate marble, travertine, and hardwood visuals, erasing aesthetic gaps between porcelain and legacy products.

Manufacturers investing in SACMI CONTINUA+ lines can press porcelain slabs up to 30 mm thick with less than 1.5% waste, raising yields and positioning plants for mega-project tender lists. Energy-reduced roller kilns let producers widen color palettes without cost spikes, unlocking margin lift in premium designs. Unglazed output benefits from localized clay beneficiation in Eastern Province, trimming freight costs and carbon footprint. Producers that bundle matching skirting and step tiles secure add-on revenues while simplifying contractor procurement. Over the forecast horizon, product-portfolio breadth will differentiate winners more than sheer capacity volume.

By Application: Floor Tiles Lead Through Durability Demands

Floor installations represented 61.78% of 2025 turnover as every new villa, apartment, or shopping mall requires large-area coverage versus selective wall cladding. Saudi Arabia ceramic tiles market share for floor products is forecast to stay above 60% given giga-project footprints exceeding 2 million m² of gross floor area each. Wall applications grow steadily as bathroom and kitchen renovations adopt 300 mm×900 mm glazed options that minimize grout joints. Roofing remains niche because flat concrete roofs dominate local architecture, though heritage restorations in Diriyah deploy clay barrel tiles for authenticity. High-traffic commercial venues mandate PEI Class 4 or Class 5 floor ratings, effectively steering demand to porcelain and high-fired ceramics.

The rise of radiant-cooling slabs in luxury residences supports thicker porcelain floor modules that integrate hydronic coils, adding technical complexity and value per square meter. Mall developers in Jeddah and Khobar specify oversized 1,000 mm tiles to create uninterrupted visual planes that enhance shopper experience. Advanced slip-resistant micro-texture glazes are adopted in airport concourses to meet ICAO safety codes. Wall-tile suppliers market stain-proof inks that resist turmeric and coffee splashes, responding to local cuisine influences. Overall, application-driven specification adds resilience to average selling prices even as raw-material volatility persists.

By End-User: Residential Sector Drives Volume Growth

Residential projects captured 59.34% of demand in 2025 and will expand at 7.86% CAGR as Vision 2030 accelerates housing handovers across 30+ master-planned communities. Saudi Arabia ceramic tiles market size gains in residential will concentrate on 400×400 mm porcelain formats ideal for standard villa layouts. Commercial demand fragments across hospitality, healthcare, retail, and office builds, each requiring tailored slip ratings, chemical resistance, or design motifs. Hospitals lean toward anti-bacterial glazes certified to ISO 22196, while hotels seek wood-look planks for guest-room warmth without maintenance burden. Educational campuses undergo refurbishment programs that retrofit durable floor tiles into high-traffic corridors, swelling medium-term institutional orders.

Developers now exploit Building Information Modeling to pre-specify tile SKU codes, allowing manufacturers to align production batches months ahead, reducing supply shocks. Design-and-build contractors for Riyadh Metro stations favor granite-effect porcelain for mezzanine floors to ensure 30-year lifecycle durability. Leasing-driven office towers install large-format lobby tiles to create premium first impressions, driving higher value per square meter relative to standard residential kitchens. End-user requirements around lifecycle cost and maintenance ease increasingly outweigh first-cost considerations, advantaging suppliers with proven performance data.

By Construction Type: New Construction Dominates Development Pipeline

New-build orders supplied 60.65% of total square meters in 2025, powered by a USD 950 billion national backlog that remains unrivaled globally. The Saudi Arabia ceramic tiles market size tied to new construction is projected to outpace renovation as giga-projects cross into intensive finishing phases between 2026 and 2029. Renovation demand still rises as Riyadh’s 1990s apartment stock cycles into refit stage, with occupants swapping small-format ceramics for seamless 600 mm floor plates. New-build projects leverage economies of scale, ordering entire shipments of matching tiles, skirting, and trim to streamline installation logistics. Conversely, renovations emphasize premium looks and rapid-cure adhesives to minimize downtime, pushing unit prices higher.

Prefabrication methods gain traction, with bathroom pods arriving on-site pre-tiled, reducing wet-work hours by 40% and elevating quality consistency. Dry-lay mock-ups on factory floors allow specifiers to approve color shade and tonality before shipment, cutting rework. Contractors increasingly demand just-in-time deliveries synced with slab-pour schedules, compelling suppliers to digitize production planning. In renovation, dustless tile-removal systems shorten project timelines, encouraging more frequent upgrades. Together, these trends cement dual growth tracks: high-volume price-sensitive new builds and agile, specification-rich retrofit jobs.

By Distribution Channel: Specialty Stores Maintain Market Leadership

Specialist tile retailers controlled 47.55% of 2025 revenue by providing mock-up rooms and in-store consultants who guide selection on PEI ratings, shade variation, and grout color compatibility. Online portals, although only 5.30% of sales today, will log an 7.96% CAGR as contractors increasingly source via B2B marketplaces offering real-time inventory and digital datasheets. Home-improvement chains appeal to DIY renovators looking for immediate stock and turnkey accessory packs. Direct-to-contractor deals dominate giga-projects, with manufacturers staging inventory at site-adjacent depots to curb handling damage. Multichannel strategies, where a brand showcases flagship showrooms, maintains e-commerce, and services key accounts directly, are becoming standard.

Augmented-reality apps letting homeowners “see” tiles on their floors drive retail engagement, lifting conversion rates by 12–15% according to pilot studies in Jeddah. Loyalty programs offering next-day delivery of cut-size inserts attract repeat small-scale contractors. Specialty shops host CPD seminars for architects on slip-resistance testing, reinforcing thought-leadership positioning. Online price-matching guarantees expand but are offset by shipping-insurance fees that sustain margin. Overall, distribution influence is shifting from pure product availability to bundled service and technical-support capabilities.

Geography Analysis

Riyadh Region generated 31.75% of 2025 tile turnover, anchored by flagship neighborhoods such as SEDRA where 30,000 villas are under construction. A steady pipeline of ministerial headquarters and financial-district towers further stabilizes demand, especially for high-specification lobby and façade ceramics. Localized production units in Sudair Industrial City shorten lead times, granting Riyadh retailers stock versatility across colorways and sizes. Rapid metro expansion boosts station-fit-out orders, including high-abrasion porcelain for concourse floors. Retail-driven foot-traffic growth in shopping centers like The Avenues Riyadh sustains replacement cycles for slip-resistant mall walkways.

Eastern Province posts the fastest 7.52% CAGR, fueled by petrochemical complexes in Jubail and mining clusters in Wa’ad Al-Shamal that require factory flooring and worker housing. Quarries licensed in Dammam and Hafr Al-Batin improve raw-material access, prompting two kiln expansions slated for 2026. Port upgrades at King Fahd Industrial Port ease import of glazes and polishing pads, while highway links drop freight costs into the Empty Quarter projects. Industrial diversification plans also spur demand for acid-resistant service corridors inside chemical plants. Residential demand climbs as expatriate workforces settle in new integrated communities, boosting sales of mid-priced porcelain.

Makkah and Madinah share uplift from pilgrimage infrastructure where slip-resistant and easy-clean tiles are mandated for ablution areas. Western and Northern Regions, led by NEOM and Red Sea luxury resorts, order large-format, salt-spray-resistant slabs for coastal installations. Northern residential clusters leverage proximity to Jordan and Egypt supply chains, promoting cross-border sourcing synergies. In the South, Jazan’s port-city revamp and Asir’s tourism strategy nurture steady but smaller off-take volumes. Nationwide logistics upgrades, including land bridge rail lines, gradually smooth regional price differentials, but design preferences-light colors in desert interiors and darker tones on humid coasts-will preserve localized SKU mixes.

Competitive Landscape

The market remains moderately fragmented; no player holds more than a majority share, and the top five collectively hold significant market share in 2024, leaving room for niche entrants. Saudi Ceramic Company leverages its domestic quartz-rich clay resources to supply mass-market SKUs at competitive cost while retaining pricing power in sanitaryware cross-sales. Arabian Ceramics Manufacturing Company differentiates itself via low-porosity porcelain slabs certified for chemical-plant floors, targeting the Eastern Province industrial boom. International majors RAK Ceramics and Kajaria Ceramics deepen local footprints through Riyadh showrooms and joint procurement ventures to satisfy IKTVA quotas, narrowing the historical edge enjoyed by incumbents. Importers from India, revitalized by duty elimination, challenge on price but face delays in customs clearance and post-sales service responsiveness.

Technology investment is the prime performance separator. Plants installing Industry 4.0 sensor grids report 3% scrap reduction and 6% overall-equipment-effectiveness gains, translating directly into bid competitiveness for giga-projects. SACMI CONTINUA+ slab presses, which trim hydraulic-oil use 90% and curb waste below 1.5%, are operational at two Saudi sites, giving early adopters a marketing storyline around sustainability. Digital printing heads capable of 400×1200 dpi output allow firms to tailor micro-batch designs for boutique projects, locking in higher margins. Local firms also benefit from preferential financing at 2% below prevailing commercial rates under NIDLP, partially offsetting scale deficits against Asian giants.

Strategic alliances proliferate. A 2025 memorandum between a domestic kiln builder and a Spanish glaze specialist aims to localize anti-bacterial coating production, cutting imports by 40 containers annually. RAK Ceramics’ new 600 m² Riyadh flagship illustrates a direct-to-specifer approach, offering mock-up spaces that accelerate decision cycles. Meanwhile, Saudi Ceramics’ 8.25 million m²/year porcelain plant, inaugurated July 2024, raises national capacity by roughly 7%, mitigating supply-risk perceptions among giga-project managers. Competitive intensity is expected to rise as energy subsidies fade and compliance costs climb, pushing low-efficiency kilns toward consolidation or closure.

Saudi Arabia Ceramic Tiles Industry Leaders

Saudi Ceramics

RAK Ceramics

Al Jawdah Ceramics

Future Ceramics

Arabian Ceramics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: RAK Ceramics launched Maximus Mega Slab and Signature Collection lines at its second 600 m² Riyadh showroom to showcase lifestyle-scale mock-ups.

- July 2024: Saudi Ceramics began trial production at its new porcelain facility with 8.25 million m² annual capacity, backed by a SAR 249.3 million (USD 66.9 million) investment.

- June 2024: Arabian Ceramics Manufacturing Company received Environmental Product Declaration (EPD) certification valid through June 2029, launching a new line of sustainable porcelain tiles with 70% recyclability and 75-year service life specifications.

Saudi Arabia Ceramic Tiles Market Report Scope

Ceramic tiles are composed of a mixture of clay and other natural materials, including sand, quartz, and water. They are majorly used in homes, restaurants, offices, and shops, particularly for bathroom walls and kitchen floors. These tiles are known for their ease of installation, cleaning, and maintenance, and they are available at affordable prices.

The Saudi Arabian ceramic tile market is segmented into product, application, and end user. By product, the market is segmented into glazed, porcelain, scratch-free, and others. By application, the market is segmented into wall tiles, floor tiles, and other applications. By end user, the market is segmented into residential and commercial. The report offers market size and forecasts for the Saudi Arabian ceramic tiles market in terms of value in (USD) for all the above segments

By Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others (Decorative, Patterned, Handmade) |

By Application

| Floor |

| Wall |

| Roofing |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices & Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airports, Metro, Bus Terminals) | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Renovation and Replacement |

By Distribution Channel

| Specialty Tile & Stone Stores |

| Home Improvement & DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

By Geography

| Riyadh Region |

| Makkah & Madinah Region |

| Eastern Province |

| Western & Northern Regions |

| Southern Region (Asir, Jazan) |

| By Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Others (Decorative, Patterned, Handmade) | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices & Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airports, Metro, Bus Terminals) | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Renovation and Replacement | ||

| By Distribution Channel | Specialty Tile & Stone Stores | |

| Home Improvement & DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| By Geography | Riyadh Region | |

| Makkah & Madinah Region | ||

| Eastern Province | ||

| Western & Northern Regions | ||

| Southern Region (Asir, Jazan) | ||

Key Questions Answered in the Report

What is the current value of the Saudi Arabia ceramic tiles market?

The market stands at USD 1.90 billion in 2026 and is projected to reach USD 2.72 billion by 2031.

Which product category leads sales?

Porcelain tiles dominate with 53.12% share owing to their durability and low water absorption.

How fast is online distribution growing?

Online retail is expanding at an 7.96% CAGR, the fastest among all sales channels.

Why are large-format tiles gaining popularity?

They reduce grout lines, speed up installation, and satisfy aesthetic preferences in luxury and mega-project applications.

Which region is the fastest-growing consumer of ceramic tiles?

The Eastern Province posts a 7.52% CAGR due to extensive industrial and mining investments.

How will energy reforms affect manufacturers?

Higher gas prices are pushing plants to adopt energy-efficient kilns and dry-granulation to protect margins.

Page last updated on: