Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 16.61 Billion |

| Market Size (2031) | USD 29.86 Billion |

| Growth Rate (2026 - 2031) | 12.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Precision Farming Market Analysis by Mordor Intelligence

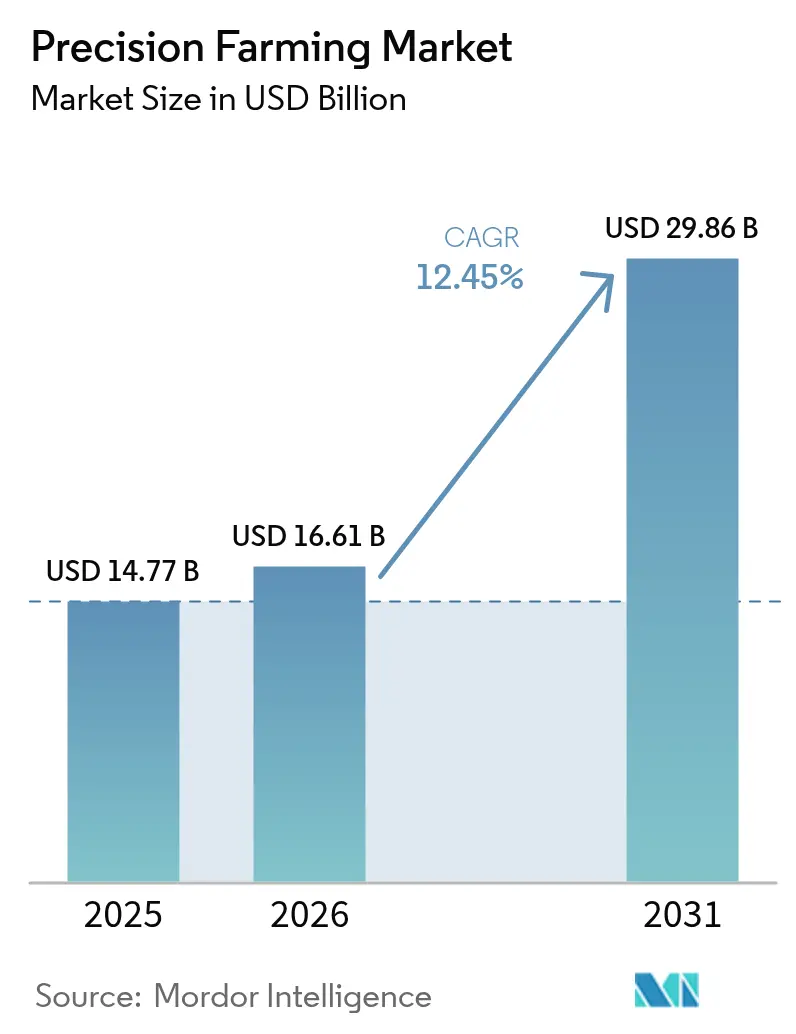

Precision Farming market size in 2026 is estimated at USD 16.61 billion, growing from 2025 value of USD 14.77 billion with 2031 projections showing USD 29.86 billion, growing at 12.45% CAGR over 2026-2031.

Satellite IoT constellations, GNSS-guided auto-steering, and AI-enabled autonomous equipment are widening digital farming’s addressable base and translating carbon-credit incentives into tangible return on investment. John Deere’s collaboration with SpaceX for sub-inch telemetry in cellular dead zones, AGCO’s PTx Trimble joint venture for mixed-fleet retrofits, and the USDA’s Climate-Smart Commodities program are reinforcing a technology cycle that rewards variable-rate input optimization. Hardware still dominates spending, yet software and edge-AI analytics are outpacing with double-digit growth, mirroring the industry shift from data collection to real-time decision automation. North America retains the largest regional share, while Asia Pacific delivers the fastest CAGR on the back of India’s smart-ag ecosystem and China’s precision farming policy mandates.

Key Report Takeaways

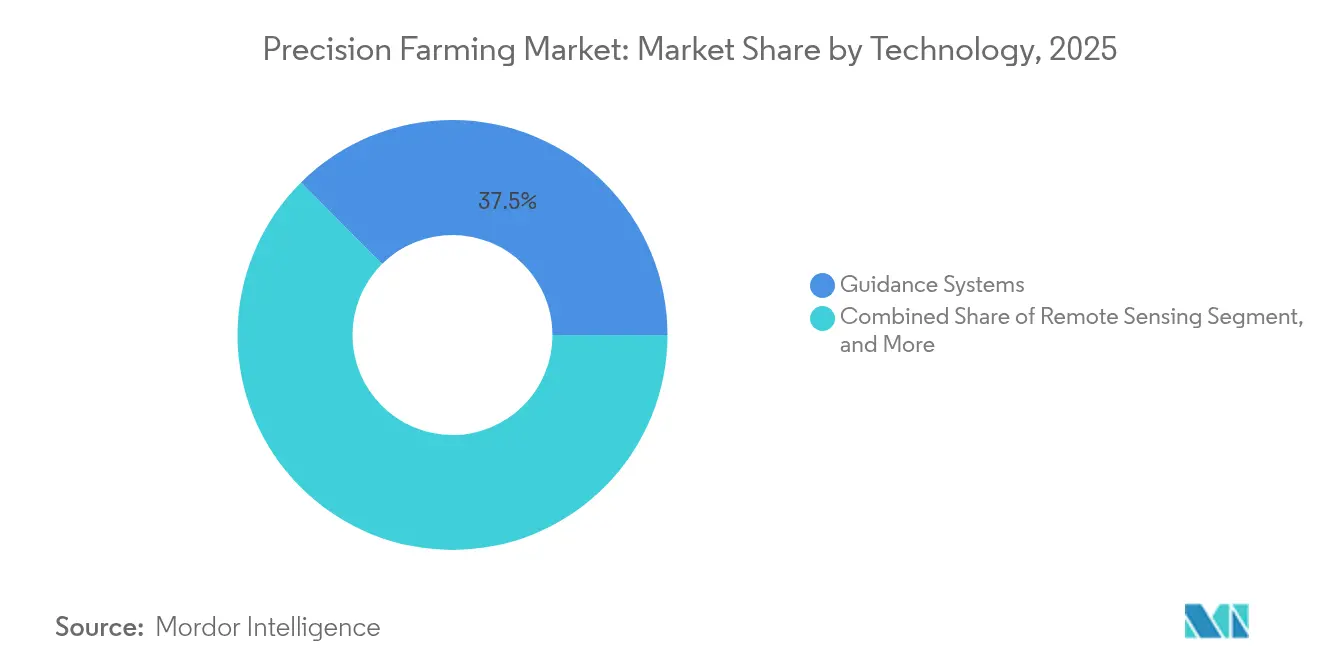

- By technology, Guidance Systems led with 37.45% of precision farming market share in 2025, whereas Variable-Rate Technology is set to rise at a 13.55% CAGR through 2031.

- By component, Hardware accounted for 51.20% of the precision farming market size in 2025, while Software is expected to advance at a 13.40% CAGR to 2031.

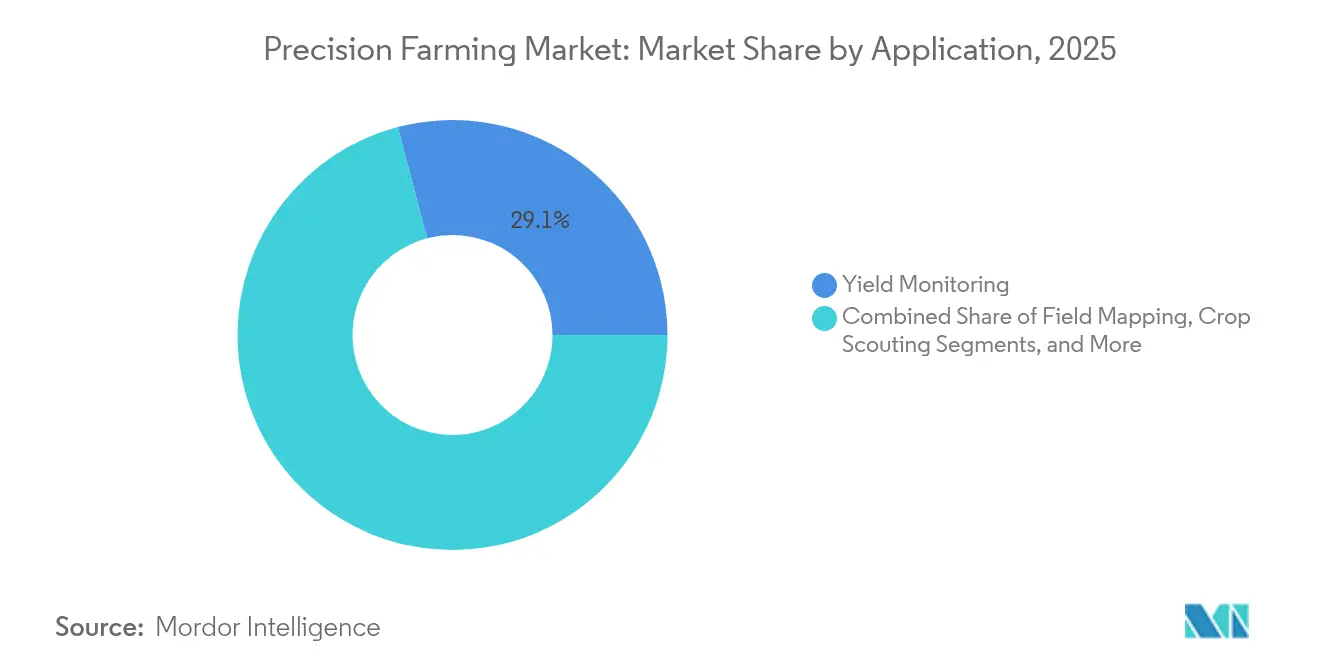

- By application, Yield Monitoring held 29.10% of precision farming market share in 2025; Drones-based Scouting is projected to expand at a 12.85% CAGR to 2031.

- By farm size, Large Farms (>1,000 ha) commanded 54.25% share of the precision farming market in 2025, yet Small Farms (<100 ha) exhibit the highest projected CAGR at 12.95% through 2031.

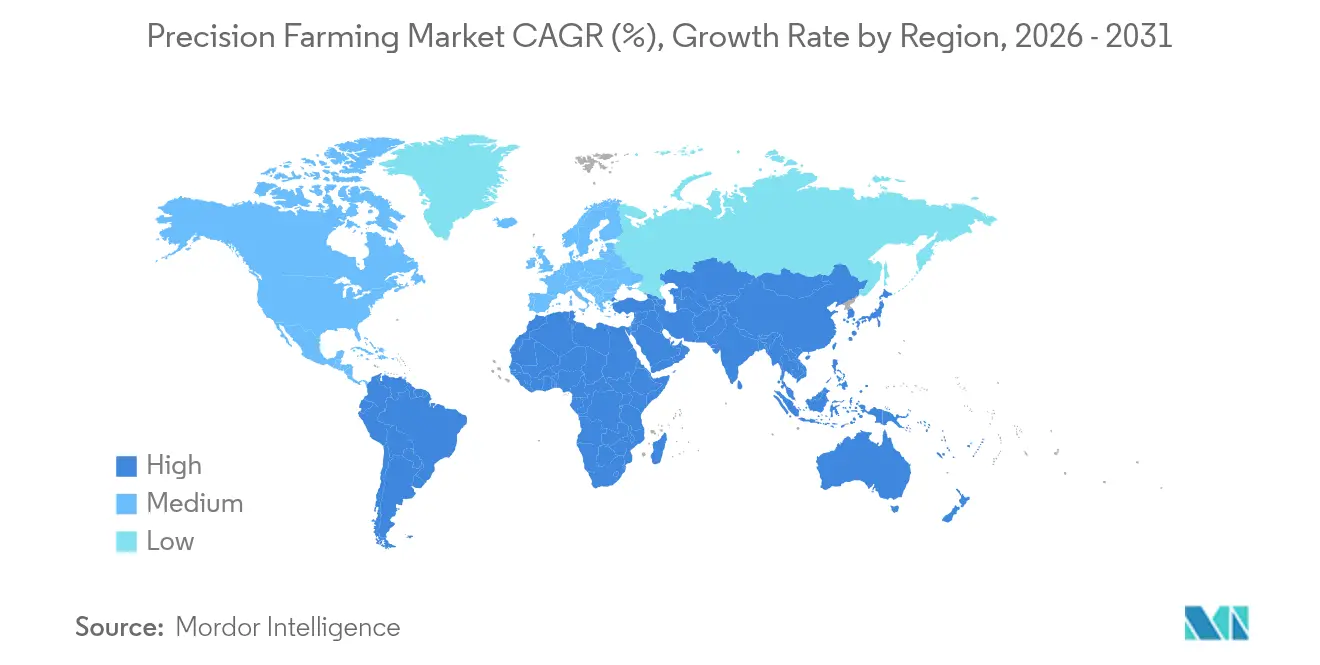

- By geography, North America captured 41.15% of the precision farming market share in 2025; the Asia Pacific is forecast to accelerate at a 13.95% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Precision Farming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GNSS-enabled auto-steering on large farms | +2.1% | North America & Europe, expanding to Asia Pacific | Medium term (2-4 years) |

| Multispectral/thermal drone sensor cost declines | +1.8% | Global, early adoption in developed markets | Short term (≤2 years) |

| Carbon-credit schemes rewarding variable-rate inputs | +1.5% | Europe, North America, emerging Asia Pacific | Long term (≥4 years) |

| Satellite IoT constellations for sub-inch telemetry | +2.3% | Global, priority in remote regions | Medium term (2-4 years) |

| Insurance discounts tied to AI-based farm risk scores | +1.2% | North America & Europe, pilot programs in Asia | Medium term (2-4 years) |

| Venture funding shift to edge-AI robotics | +1.4% | Global, focused on innovation hubs | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

GNSS-Enabled Auto-Steering on Large Farms

Adoption of GNSS auto-steering has reached 70% on farms over 1,000 ha versus 52% on midsize holdings, a trend increasingly shaping the precision farming market, aided by John Deere’s StarFire 7000 receiver that locks onto more satellite bands for faster convergence.[1]USDA Economic Research Service, “Adoption of Precision Agriculture Technologies,” ers.usda.gov SpaceX Starlink backhauls the guidance data where cellular networks fail, letting operators run autonomous passes throughout the day and night. AGCO’s OutRun retrofit kit democratizes steering upgrades for mixed fleets, supporting tractors from rival brands. Labor shortages heighten the value proposition by substituting scarce operators with robotics that maintain perfectly straight rows, suppress overlap, and conserve diesel. Return on investment is amplified through reduced fuel costs and higher field-hour utilization that push machinery farther during tight planting windows.

Rapid Cost Declines in Multispectral/Thermal Drone Sensors

More than 300,000 agricultural drones now treat over 500 million ha worldwide, with DJI’s Mavic 3 Multispectral priced below the threshold once reserved for large farms. Farm trials on Montana wheat show 90-95% herbicide savings when spot-spray drones are paired with WEED-IT vision systems. Sensor miniaturization has lowered payload weight, doubling flight endurance while preserving spectral resolution for chlorophyll and canopy moisture readings. Regulatory easing in Brazil and the United States has widened the operational envelope for beyond-visual-line-of-sight flights, accelerating adoption on broad-acre crops. AI-enabled anomaly detection now flags nutrient stress a week sooner than the naked eye, letting growers intervene before yield loss sets in.

Carbon-Credit Schemes Rewarding Variable-Rate Input Cuts

The USDA’s USD 3.1 billion Climate-Smart Commodities initiative aims to sequester 60 million tCO₂e through field-level verification of precision practices, strengthening financial incentives across the precision farming market, and paying growers who document fertilizer and fuel savings via sensor logs. Variable-rate technology already reaches 69% penetration in major U.S. corn and soybean farms, a level set to climb as carbon premiums boost breakeven ROI timelines. Europe’s Farm to Fork strategy mandates a 50% cut in chemical use by 2030, effectively forcing adoption of prescription-based spraying regimes. China’s carbon trading platform lets Farmer Professional Cooperatives sell verified emission reductions, creating a direct monetary feedback loop. Legislative clarity provided by the 2024 Rural Prosperity and Food Security Act further unlocks conservation loans earmarked for hardware and software that underpin variable-rate programs.

Satellite IoT Constellations for Sub-Inch Telemetry

Satellite IoT revenues are projected to jump from USD 1.3 billion in 2022 to USD 8.7 billion in 2032, with agriculture tagged as the largest use case. John Deere’s JDLink Boost pipes telematics through Starlink, letting support staff push over-the-air vehicle updates that cut downtime. OneWeb offers low-latency backhaul for fleets in vast Canadian prairies, where 77% of cropland sits outside 4G coverage. Continuous connectivity enables machine-to-machine coordination for swarms of autonomous sprayers working within inches of one another. Economic upside could surpass USD 500 billion in added global farm GDP once reliable links remove the data-outage constraint on autonomy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-interoperability gaps in mixed-brand fleets | -1.6% | Global, acute in mixed-fleet operations | Medium term (2-4 years) |

| Rural cybersecurity threats to farm OT networks | -1.2% | Developed markets with high digitalization | Long term (≥4 years) |

| Plateauing RTK-network coverage in Sub-Saharan Africa | -0.8% | Sub-Saharan Africa, spillover to remote regions | Long term (≥4 years) |

| Farmer resistance to algorithmic decision loss | -0.9% | Global, stronger in traditional communities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Interoperability Gaps Among Mixed-Brand Machinery

Roughly 73% of growers operate tractors, planters, and sprayers from multiple OEMs, creating data silos that handicap end-to-end analytics. The OGC SensorThings API promises a universal wrapper for geospatial and machinery data, yet proprietary file formats and differing CAN bus protocols block seamless flows. AGCO’s PTx Trimble venture pledges brand-agnostic steering and data sync, but retrofits on legacy rigs are costly and require dealership expertise. Europe’s push for open standards and MQTT transport layers is a positive signal, though adoption lags smaller vendors who fear commoditization. Without convergence, farmers continue to juggle USB sticks and cloud portals, capping the productivity gains that full autonomy could deliver.

Rural Cybersecurity Threats Targeting Farm OT Networks

As planters, pumps, and weather stations join the internet, operational technology becomes a target for ransomware and data theft. The EU’s NIS-2 Directive will add compliance overhead for ag-tech providers; similar guidance is moving through U.S. federal channels. IEC 62443 controls written for manufacturing plants must be mapped to open fields where physical security is low and connectivity is intermittent. Smallholders lack in-house specialists, leaving default passwords and unpatched firmware on solar-powered gateways. Federated-learning pilots show promise by training disease-detection models without exporting raw field data, but they demand computation at the edge that inflates bill-of-materials costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Autonomous Systems Drive Market Evolution

Guidance Systems held the leading 37.45% precision farming market share in 2025, sustained by robust GNSS receivers that steer machinery to sub-inch paths under variable terrain. The precision farming market size for Variable-Rate Technology is forecast to grow at a 13.55% CAGR through 2031, driven by rising fertilizer and chemical prices that incentivize targeted application. Drone-based remote sensing leverages cheaper multispectral payloads, with DJI reporting a 67.78% cut in chemical volumes when maps feed prescription sprayers. Robots are gaining traction as venture funding pivots to edge-AI platforms; Four Growers and Bonsai Robotics collectively raised USD 24 million to automate harvesting on 500,000 acres. Satellite IoT rounds out the stack, relaying sensor inputs from fields outside cellular reach so models stay current for autonomy modules.

Edge and cloud analytics work in tandem: edge hardware processes vision streams in real time, while cloud engines crunch seasonal patterns. John Deere’s second-generation autonomy stack merges both layers to target full corn and soybean autonomy by decade’s end. Farmers increasingly prefer mixed-fleet retrofits over single-brand replacements, a shift AGCO capitalized on with its OutRun kit that omits a high-cost tractor swap. Given these dynamics, technology suppliers who pair open APIs with hardware-agnostic components are best positioned to capture incremental acreage.

By Component: Software Acceleration Transforms Hardware Dominance

Hardware captured 51.20% of the precision farming market in 2025, covering sensors, controllers, drones, and autonomous platforms. Yet, software revenue is climbing at a 13.40% CAGR as edge-AI delivers actionable prescriptions within seconds, even when the network drops. Sensors have shrunk to postage-stamp footprints, letting small farms afford dense soil-moisture grids that feed variable-rate irrigation maps. Displays like John Deere’s G5-Plus add Ethernet to pass richer datasets from implements back to the cab. On-board computers integrate GNSS, machine vision, and telemetry onto a single board, slashing latency for autonomy loops.

The precision farming market size for managed services is set to widen as operators lean on third-party partners to patch software and monitor cyber threats in real time. Data analytics suites from CNH and Raven trim herbicide by 77% with AI-directed selective spraying. Satellite backhaul ensures prescriptions sync during fieldwork, a crucial fail-safe for 77% of cropland without 4G. As hardware margins compress, vendors seek recurring revenue through subscriptions that bundle updates, algorithms, and carbon-credit reporting dashboards.

By Application: Precision Spraying Redefines Crop Management

Yield Monitoring remains the backbone, supplying the spatial variability data that trains every prescription; it accounted for 29.10% precision farming market share in 2025. Drones-based Scouting is accelerating at 12.85% CAGR thanks to AI models that spot nutrient stress early, prompting micro-dosed foliar sprays instead of blanket treatments. Variable-Rate Application outperforms blanket spreading with documented savings of USD 40.74 per acre and fertilizer cuts up to 66% using John Deere’s ExactShot system. Soil and Crop Health Monitoring weaves IoT probes with satellite data, letting analytics warn of disease onset several days earlier than conventional scouting.

The precision farming market size for harvest automation is set to rise as John Deere’s S7 combine automates grain-loss settings and groundspeed, improving throughput by 20%. Irrigation Management platforms like Verdi balance water and nutrient delivery, a capability vital for drought-prone regions where every millimeter of rainfall counts. Downstream logistics gain from autonomous grain carts that sync location and fill-level data to the combine, minimizing idle time. As sustainability metrics grow stringent, compliance modules now sit alongside agronomic tools, allowing carbon verification to happen in-season rather than post-harvest.

By Farm Size: Small Farm Digitalization Accelerates

Large farms over 1,000 ha held 54.25% of the precision farming market in 2025, leveraging bigger capital pools and dedicated agronomy staff. Small farms under 100 ha clock the highest 12.95% CAGR as low-cost IoT kits, satellite backhaul, and government grants lower entry barriers. The precision farming market size for smallholders is set to widen under India’s INR 450 crore (USD 5.12 million) Digital Agriculture Mission, which subsidizes sensors and cloud dashboards. Medium farms span 100-1,000 ha and show 52% adoption, catalyzed by retrofit kits that avoid full machinery turnover.

UNDP frameworks now bundle mobile apps in local languages, cloud analytics, and remote sensing so smallholders bypass upfront server costs. Large farms face growing scrutiny on emissions, pushing them to quantify every input through digital twins for ESG reporting. Medium operations find equilibrium by deploying core guidance and variable-rate modules without venturing into fully autonomous fleets. Despite differing paces, convergence is clear: equipment that once demanded high CapEx is now available via subscription, closing the digital divide between farm sizes.

Geography Analysis

North America retained 41.15% regional share in 2025, aided by mature GNSS networks, an established dealer ecosystem, and a regulatory environment that recognizes digital records for carbon programs. The market has plateaued in growth rate relative to emerging regions, partly because 2025 farmer sentiment surveys show cautious capital plans amid volatile commodity prices. Nevertheless, active replacement cycles for legacy displays and expansion into full-machine autonomy should preserve the continent’s demand floor.

The Asia-Pacific region recorded the fastest growth rate of 13.95% in the precision farming market, propelled by India’s smart-ag market, projected to reach USD 886.21 million by 2028, and China’s policy mandates around digital agriculture. Government-funded satellite constellations, low-cost drones, and rural broadband investments underpin adoption across smallholder plots. Venture capital flows of more than USD 1.2 billion in 2024 concentrated on automated orchard sprayers and agri-fintech credit scoring that ties input loans to sensor-verified field data. Australia adds incremental acreage with autonomous broad-acre fleets that alleviate chronic labor shortages.

Europe advances steadily under environmental legislation requiring a 50% cut in chemicals by 2030, positioning precision spraying as a compliance lever. Field trials in Germany confirm 10-20% pesticide reductions without yield sacrifice, bolstering farmer confidence. Latin America’s adoption pace diverges: Brazil and Argentina slowed tractor purchases by 14% in 2024 due to drought-linked income declines, yet accelerated drone spraying after regulatory relaxation. The Middle East and Africa remain early in the curve; satellite IoT is a lifeline for Sub-Saharan growers where RTK networks stall at 40% coverage, but affordability and skills gaps temper speed.

Regulatory Landscape

Precision farming regulation is increasingly shaped by sustainability compliance, data governance, and safety rules for AI-enabled machinery. In the European Union, Farm to Fork targets a 50% reduction in chemical pesticide use by 2030, which reinforces demand for recordkeeping and prescription-based application workflows. The EU AI Act (Regulation 2024/1689) also treats AI used as a safety component in agricultural machinery as high-risk, tying compliance to existing EU type-approval pathways under Regulation 167/2013.

In the United States, federal attention is rising around incentives and interoperability standards. The PRECISE Act (S. 1616/H.R. 6143) proposes expanded support for implementing precision agriculture under conservation programs, while S. 507 directs USDA to work with NIST and the FCC on voluntary, consensus-based, private-sector-led interconnectivity standards within two years of enactment. This aligns policy with the market need to reduce mixed-fleet data fragmentation.

Value Chain Analysis

The precision farming value chain starts with upstream electronics and sensing inputs, including GNSS receivers, cameras, multispectral and thermal sensors, controllers, and connectivity modules, before flowing into OEM and system integration layers led by equipment manufacturers and precision brands such as John Deere, AGCO (including PTx Trimble), CNH Industrial, and Kubota. Specialist providers contribute differentiated capabilities across vision autonomy and crop intelligence, including Bonsai Robotics, Agtonomy, and Taranis, while satellite and digital infrastructure players supply imagery and data layers that feed analytics and prescription generation, including Planet Labs and software platforms such as Climate FieldView and OEM operations centers.

Downstream, distribution and enablement are concentrated in dealer networks, agronomy retailers, and service partners who install, calibrate, and support variable-rate, guidance, and spraying systems. These players convert field data into operational decisions and compliance artifacts, including chemical-use records and carbon program documentation. Interoperability across mixed-brand fleets, data ownership and privacy concerns, and the limited availability of trained precision service personnel remain key friction points, keeping integration services, managed services, and API-led partnerships central to turning hardware deployments into repeatable outcomes.

Competitive Landscape

Industry structure is consolidating. AGCO paid USD 2 billion for 85% of Trimble’s agriculture division, forming PTx Trimble with a goal to surpass USD 2 billion precision revenue by 2028. John Deere extends leadership through SpaceX connectivity, an expanded 2025 product line, and its second-generation autonomy stack that integrates vision, AI, and remote diagnostics.[4]AgWeb, “John Deere S7 Combine Launch,” agweb.com CNH absorbs Raven Industries to embed real-time machine learning into Case and New Holland fleets, while DJI keeps a global drone share that exceeds every Western peer combined.

Strategic playbooks emphasize open APIs, cross-brand retrofits, and as-a-service pricing to win mixed-fleet hectares. Edge-AI firms such as Four Growers and Bonsai Robotics target narrow tasks—greenhouse harvesting and row-crop perception—yet their success forces majors to speed internal R&D or partner. Venture funding tilts away from pure farm-management SaaS toward autonomy modules that work offline, reflecting investor appetite for tangible productivity leaps.

Competitive intensity is not siloed to technology; downstream agribusinesses bundle input financing with sensor installations, creating lock-in. At the same time, cooperatives in Europe and Asia contract shared fleets of autonomous sprayers, adding a service layer that bypasses hardware ownership. Patents around machine vision and variable-rate application will shape royalty flows, making intellectual property a frontline battlefield.

Precision Farming Industry Leaders

-

AGCO Corporation

-

Ag Junction Inc

-

John Deere

-

DICKEY-john Corporation

-

TeeJet Technologies

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Policy and program design is creating whitespace for standards-compliant and auditable precision workflows that tie agronomic actions to verified outcomes. In the United States, draft language for the Agricultural Act of 2026 includes reforms to the Environmental Quality Incentives Program (EQIP), with revised definitions and increased payment limits for precision agriculture practices. This reinforces demand for systems that can document variable-rate decisions, application logs, and sensor-based evidence. At the same time, the proposed PRECISE Act (S. 1616/H.R. 6143) and the interconnectivity standards effort in S. 507 focus attention on both financial support and cross-vendor connectivity, strengthening opportunities for brand-agnostic retrofits, standards-aligned data exchange, and cybersecurity-ready deployments.

Commercial momentum is also building around manufacturing localization and autonomy-first field operations that reduce operator time per acre. Ecorobotix committed USD 50 million over three years to establish assembly operations for its ARA ultra-high precision sprayer in Lyons, Kansas, while Orbia Netafim opened a 30,000-square-meter manufacturing plant in Hermosillo, Mexico to expand production capacity for drip irrigation solutions, supporting faster regional delivery of precision spraying and irrigation hardware. On the platform side, Deere reported 440,000 monthly active users on the John Deere Operations Center and a 10-year, USD 20 billion commitment to U.S. manufacturing, highlighting the monetization path for integrated precision stacks that bundle hardware, analytics, and reporting into renewal-oriented digital services.

Recent Industry Developments

- July 2026: John Deere confirmed See and Spray Gen 2 sprayers for Model Year 2027, adding updated AI weed detection, improved nighttime spraying capability, and four-wheel steer features. The release extends precision spraying beyond core row-crop use cases by improving operating windows and detection performance, increasing the data capture footprint of sprayer passes for broader farm decision automation.

- May 2025: John Deere acquired Sentera to bring aerial imagery and AI agronomics deeper into its precision agriculture stack. Folding scouting data into the OEM platform tightens the link between remote sensing, prescriptions, and machine execution, strengthening subscription-driven workflows anchored in the Operations Center.

- January 2025: John Deere unveiled its second-generation autonomy stack with longer perception range and mobile app control. The upgrade supports higher utilization of autonomous operations and simplifies day-to-day control of autonomous workflows, raising the baseline capability for connected equipment and mixed-field task automation.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the precision farming market covers the value of technologies, software, and related services that help farmers measure field conditions and apply inputs more accurately to improve yields and reduce waste.

Scope exclusions: Traditional farm machinery without precision features, basic irrigation hardware sold without connected controls, and general agronomy consulting that is not tied to precision tools are excluded.

Segmentation Overview

-

By Technology

-

Guidance Systems

- GNSS / GPS

- GIS

-

Variable-Rate Technology

- Variable-Rate Fertilizer

- Variable-Rate Seeding

- Variable-Rate Pesticide

- Remote Sensing

- Drones and UAVs

- Robotics and Autonomous Equipment

- Edge and Cloud Analytics Platforms

- Other Technologies

-

Guidance Systems

-

By Component

-

Hardware

- Sensors and Actuators

- Controllers and Displays

- On-board Computing and Connectivity

-

Software

- Farm-Management SaaS

- Data Analytics and AI

-

Services

- Integration and Consulting

- Managed Services

-

Hardware

-

By Application

- Yield Monitoring

- Variable-Rate Application

- Field Mapping

- Soil and Crop Health Monitoring

- Irrigation Management

- Crop Scouting

- Harvest Automation and Logistics

- Other Applications

-

By Farm Size

- Small Farms (less than 100 ha)

- Medium Farms (100 - 1,000 ha)

- Large Farms (greater than 1,000 ha)

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Netherlands

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

-

Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

-

Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

-

Middle East

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

We start by mapping the value chain and adoption logic using public sources that are stable and easy to cross-check across countries. Common reference points include government agriculture statistics such as USDA and Eurostat, remote sensing and crop monitoring outputs from sources such as NASA and FAO, and agronomy research papers that describe yield response and input-use efficiency.

To anchor pricing and unit assumptions, we review company filings, investor presentations, import-export trade disclosures where relevant, and reputable press coverage of farm technology rollouts. For market structure checks, patent databases are used to understand where innovation is concentrated, and we selectively use a paid subscription for company financials and news to keep revenue signals and event timing consistent. These desk research sources are illustrative only, and many other public and paid references are used for data collection, validation, and clarification.

Primary Interviews and Surveys

Our primary work focused on confirming real purchase behavior and usage patterns across large farms and smaller operators, then aligning those inputs with what distributors and service providers see in the field. Interviews and surveys covered equipment makers, software providers, agronomy and service partners, dealers, and farm managers across the Americas, EMEA, and APAC, so gaps from desk research could be closed and assumptions re-checked before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 15% | APAC: 46% |

| Mid tier: 51% | Functional/Unit leaders: 41% | EMEA: 29% |

| Smaller Players: 21% | Managers: 44% | Americas: 25% |

Market-Sizing & Forecasting

Sizing was built using top-down and bottom-up logic in one workbook, so results stay explainable and easy to update. On the top-down side, we reconstruct the demand pool by linking cropped area, farm-size mix, and technology penetration rates, and then translate it into value using typical system pricing and service attach rates (which vary by technology maturity).

To keep totals realistic, we use selective bottom-up approximations as checks, such as sampled average selling price times estimated installed units for guidance, sensing, and variable-rate solutions, followed by channel checks from dealers and service partners. When a country lacked clean public signals, we handle the gap by using proxy markets with similar farm sizes and crop profiles, then re-scaling with local price levels and adoption feedback from interviews.

For forecasting, scenario analysis is applied, because adoption moves with crop prices, input cost inflation, farm labor availability, and the pace of subsidy and compliance programs that encourage digital reporting. Key inputs we track include hectares under major crops, precision-enabled equipment shipments, software subscription renewal behavior, drone and imaging use intensity, and the mix shift from one-time hardware sales toward recurring services and software.

Data Validation & Update Cycle

We validate the outputs by comparing the model to independent signals such as regional adoption surveys, equipment shipment trends, and the direction of farm income and input cost cycles. Outliers are flagged and reviewed, and if a variance cannot be explained by a clear market event, assumptions are revisited and interview follow-ups are triggered.

Before sign-off, the numbers go through a multi-step review where calculations are rechecked and the year-to-year movements are tested for logical consistency by region and technology. Reports are refreshed annually, and interim updates are made when major policy shifts, supply constraints, or pricing changes materially affect demand. A final pass is done right before delivery so clients receive the latest view.

Mordor Intelligence's Global Precision Farming Market Market Size Versus Other Published Estimates

Published market sizes for precision farming often vary because the scope line is drawn differently and the input assumptions do not always follow the same timing. The spread usually comes from what is counted as precision farming versus adjacent smart agriculture categories, and also from how pricing is converted and updated across regions.

The benchmark table shows a higher 2026 value versus some 2025 figures. In Mordor Intelligence's model, the total is built from technology adoption and farm-size weighted penetration, while excluding adjacent categories that are not directly linked to precision field operations and paid farm management workflows.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 16.61 B (2026) | |

| Global Consultancy A | USD 11.20 B (2025) | Uses a 2025 base year with a narrower inclusion of recurring software and services, and applies conservative adoption curves that reduce multi-technology stacking on the same farm. |

| Industry Research Group B | USD 10.50 B (2024) | Back-solves from a 2024 starting point and tends to blend precision farming with broader smart farming themes, which can undercount service attach and create mismatched currency timing across regions. |

Taken together, the differences mostly trace back to what gets counted as a paid precision farming solution, how quickly adoption is assumed to expand beyond early users, and whether software and services are treated as a meaningful value layer. By keeping the inputs tied to hectares, farm mix, penetration, and price logic that can be checked and refreshed, the final number stays traceable and repeatable year over year.

Key Questions Answered in the Report

What is the global value of precision farming in 2026?

Precision farming is valued at USD 16.61 billion in 2026.

How much growth is expected for precision farming by 2031?

The segment is projected to reach USD 29.86 billion in 2031, reflecting a 12.45% CAGR.

Which region is adopting precision farming solutions the fastest?

Asia Pacific leads in growth with a 13.95% CAGR from 2026 to 2031.

Which technology area is expanding the quickest within precision farming?

Variable-Rate Technology is advancing at a 13.55% CAGR through 2031 as growers target input optimization.

How do carbon-credit incentives encourage the uptake of precision farming tools?

Government programs pay growers for verifiable fertilizer and chemical cuts, making variable-rate applications more profitable and accelerating adoption.

Why is satellite IoT connectivity critical for precision farming deployments?

Satellite links serve 77% of cropland that lacks reliable cellular coverage, ensuring continuous data flow for autonomous equipment and analytics.

Page last updated on: