Transcranial Doppler Ultrasound Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

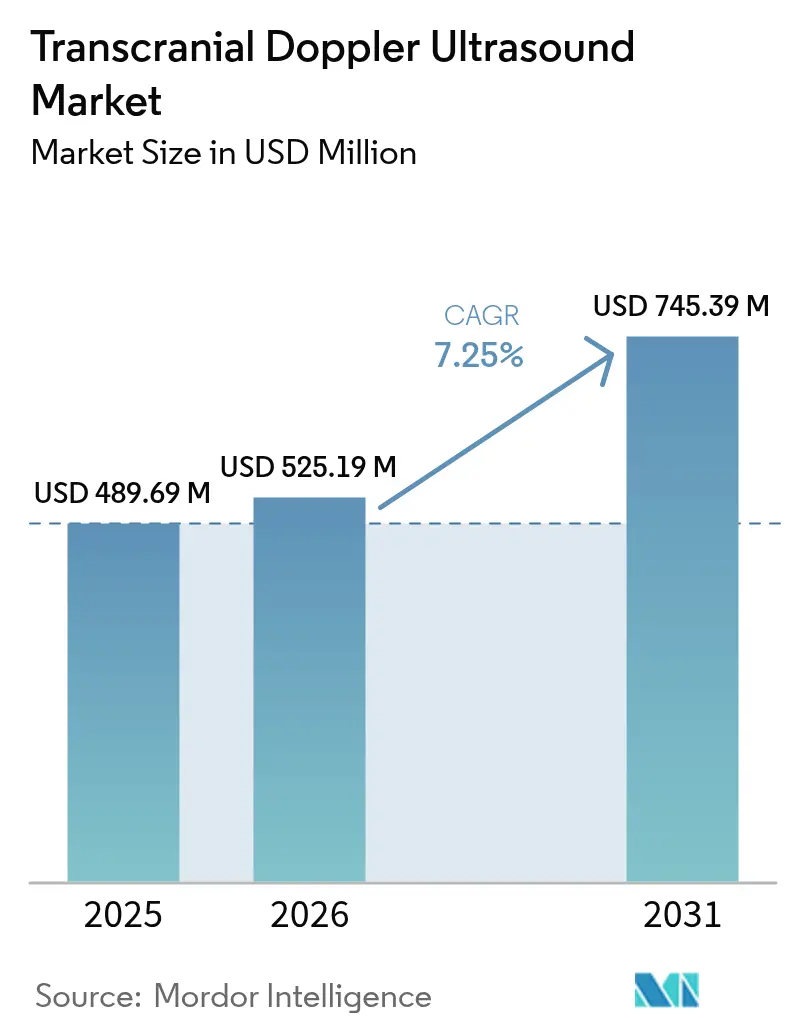

| Market Size (2026) | USD 525.19 Million |

| Market Size (2031) | USD 745.39 Million |

| Growth Rate (2026 - 2031) | 7.25% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Transcranial Doppler Ultrasound Market Analysis by Mordor Intelligence

The Transcranial Doppler Ultrasound market size is expected to grow from USD 489.69 million in 2025 to USD 525.19 million in 2026 and is forecast to reach USD 745.39 million by 2031 at 7.25% CAGR over 2026-2031.

Rapid clinical uptake of non-invasive cerebrovascular monitoring, expanding stroke center networks, and AI-enabled diagnostic enhancements are the core growth catalysts. Portable and robotic devices are broadening access beyond tertiary hospitals, while reimbursement reforms in key countries are gradually easing capital constraints. Intensifying competition around automation, probe miniaturization, and cloud-based analytics is redefining value propositions. Meanwhile, persistent operator dependency and heterogeneous payment policies temper the pace of standardized roll-outs, especially in resource-constrained settings.

Key Report Takeaways

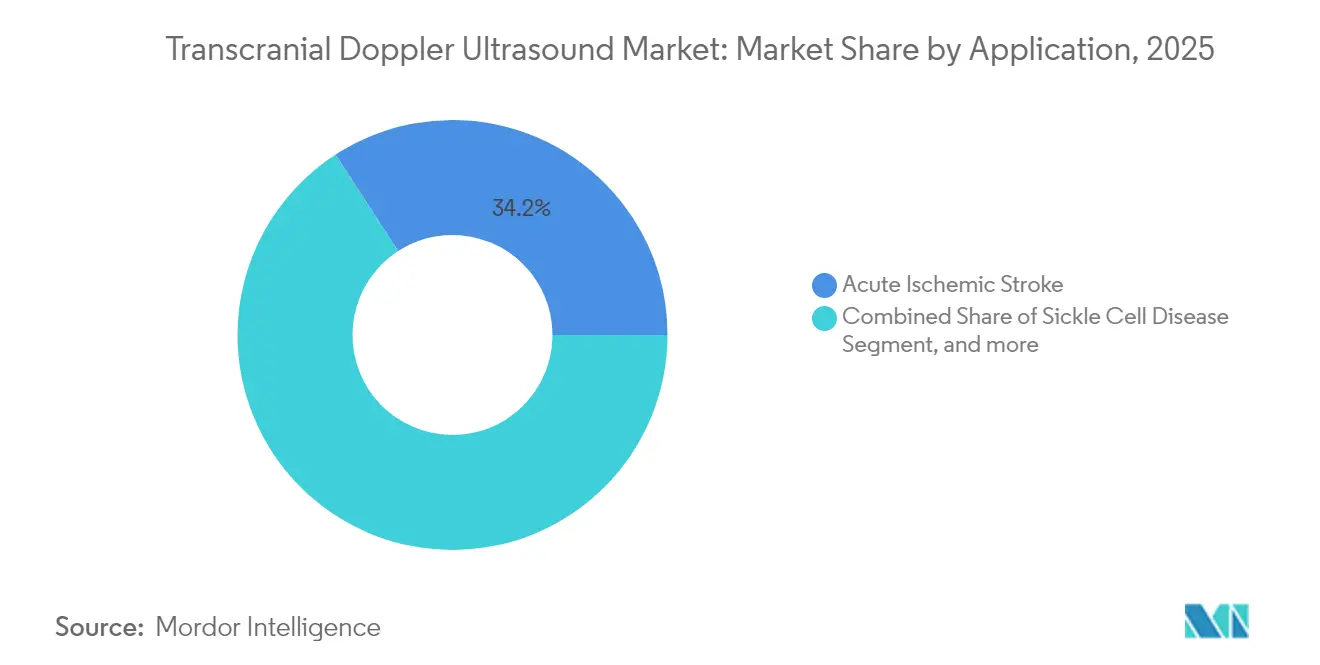

- By application, acute ischemic stroke held 34.15% of transcranial doppler ultrasound market share in 2025; traumatic brain injury monitoring is advancing at an 8.62% CAGR to 2031.

- By device type, stand-alone systems captured 61.72% revenue share in 2025, while portable units are expanding at a 10.15% CAGR through 2031.

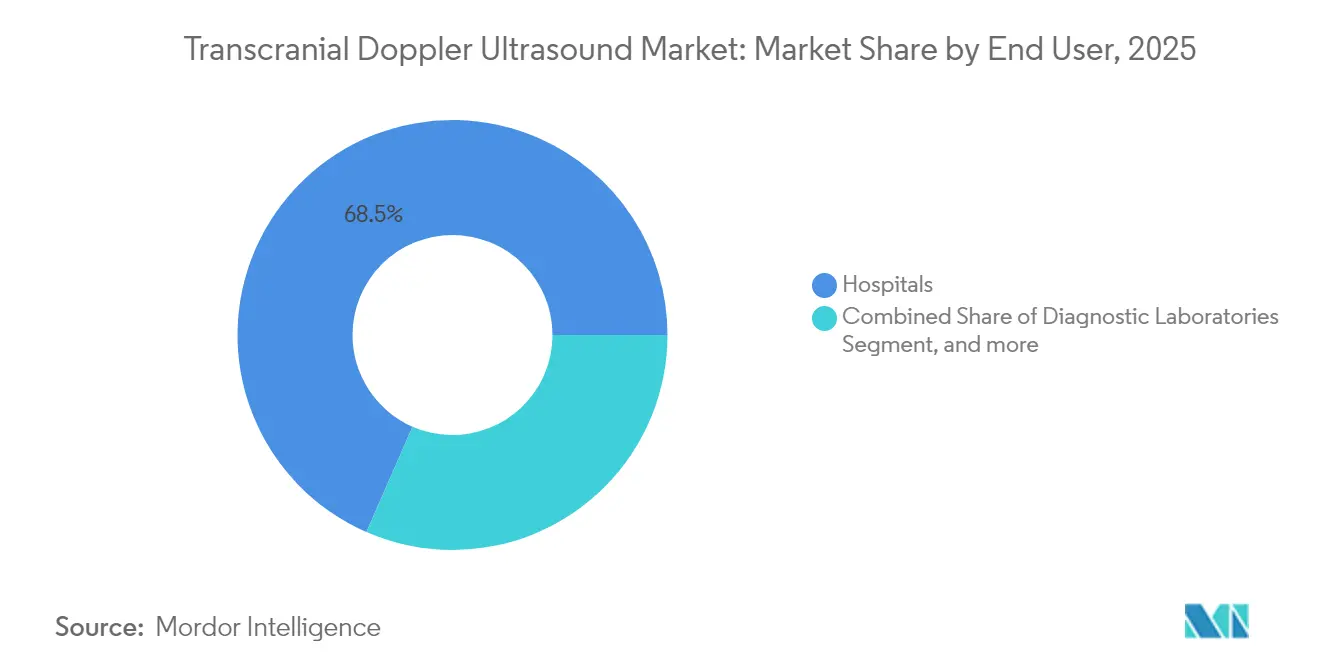

- By end user, hospitals accounted for 68.45% of the transcranial doppler ultrasound market size in 2025 and ambulatory surgical centers are growing at 8.75% CAGR between 2026-2031.

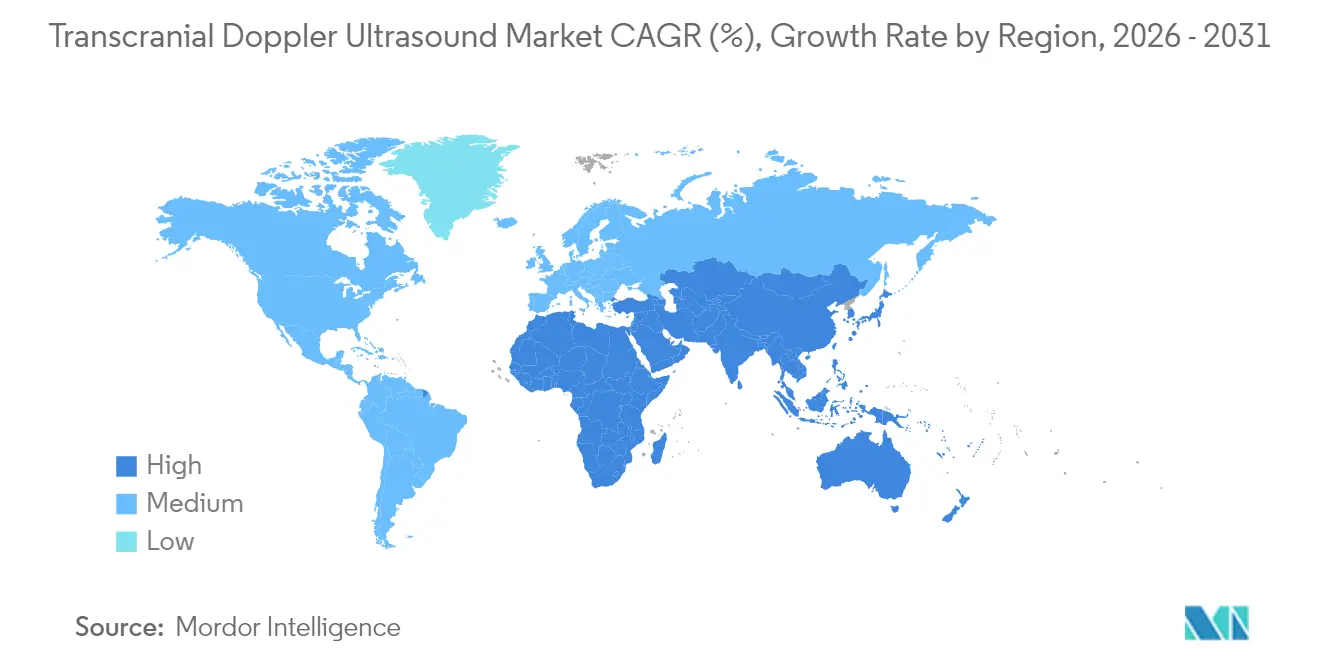

- By geography, North America commanded 41.32% of the 2025 transcranial doppler ultrasound market share; Asia-Pacific is set to grow at 7.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Transcranial Doppler Ultrasound Market Trends and Insights

Drivers Impact Analysis*

| Market Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global stroke incidence & aging demographics | +2.1% | North America, Europe, East Asia | Medium term (2–4 years) |

| Proliferation of comprehensive stroke centers & tele-stroke networks | +1.8% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Expansion of point-of-care ultrasound programs | +1.4% | Global, early adoption in developed markets | Medium term (2–4 years) |

| Technological convergence improving diagnostic yield & accessibility | +1.9% | North America, Europe | Medium term (2–4 years) |

| Rising emphasis on preventive neurological screening | +1.3% | Europe, East Asia | Long term (≥ 4 years) |

| Adoption of portable & AI-integrated TCD systems | +1.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Stroke Incidence & Aging Demographics Elevating Demand for Rapid Neuro-vascular Screening

The worldwide rise in ischemic stroke cases, now surpassing 11.9 million annually, is intensifying demand for fast, bedside cerebrovascular assessments.[1]The Global Burden of Stroke Collaborators, “Global, regional, and national burden of stroke, 1990-2024,” The Lancet, thelancet.com Aging populations in Europe, Japan, and the United States magnify this trend as hypertension and obesity prevalence remain high. Governments and health systems are prioritizing early-stage detection, placing Transcranial Doppler Ultrasound market solutions at the center of stroke prevention pathways. Large data sets linking middle cerebral artery flow patterns to functional outcomes strengthen clinical confidence and reimbursement prospects. Consequently, procurement budgets for portable neuro-vascular scanners are rising in neurology, cardiology, and emergency departments.

Proliferation of Comprehensive Stroke Centers & Tele-stroke Networks Enhancing TCD Utilization

National stroke strategies are accelerating licensure of advanced thrombectomy hubs, each requiring around-the-clock neuro-diagnostics. In France, mechanical thrombectomy capacity remains at 7,500 procedures versus a 20,500-case potential, driving hospitals to integrate automated Transcranial Doppler Ultrasound market platforms for collateral-flow triage. Tele-stroke networks further leverage real-time Doppler waveforms to guide patient transfer decisions. These service expansions shorten door-to-reperfusion intervals and underscore the modality’s critical role, directly lifting device sales and service contracts.

Expansion of Point-of-Care Ultrasound Programs Boosting Neuro-sonology Training & Adoption

Sixty-three percent of pediatric neurocritical-care centers now apply bedside Doppler exams; 74% modify care plans instantly based on results.[2]Laura B. Maitland et al., “Point-of-Care Transcranial Doppler in Pediatric Neurocritical Care,” Journals.LWW.com Residency curricula increasingly incorporate neuro-sonology modules, reducing the skills gap that historically limited penetration. The Lucid Robotic System secures reliable windows in 56 seconds, allowing nurses to initiate monitoring during stabilization. Such productivity gains make the Transcranial Doppler Ultrasound market viable for intensive-care units and ambulance services, spurring recurrent demand for disposable probes and cloud analytics.

Technological Convergence Improving Diagnostic Yield & Accessibility

AI-driven flow-pattern classifiers now flag large-vessel occlusion with 93% sensitivity, while 3D ultrasound localization microscopy maps vessels as small as 60 μm through an intact skull.[3]Jingwei Fan et al., “Three-Dimensional Ultrasound Localization Microscopy of Cerebral Microvasculature,” arxiv.org Wearable patches developed at UC San Diego capture thousands of images each second, supporting continuous cerebral autoregulation tracking. Combined, these breakthroughs diminish operator variability and unlock new chronic-care applications such as non-invasive intracranial pressure estimation. Investors consequently channel capital into start-ups focused on portable Transcranial Doppler Ultrasound market endpoints for home-based stroke surveillance.

Restraints Impact Analysis*

| Market Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High operator dependency & learning curve | -1.6% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Reimbursement variability across regions | -1.2% | North America, Europe | Medium term (2–4 years) |

| Increasing availability & cost decline of alternative neuro-imaging modalities | -1.3% | Global | Long term (≥ 4 years) |

| Lack of standardized protocols across clinical settings | -1.1% | Global | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Operator Dependency and Learning Curve Limiting Standardized Interpretations Across Sites

Traditional systems require expert sonographers to identify acoustic windows; waveform variability of 40% day-to-day in severe TBI illustrates the challenge. Differing pressure-flow relationship categories complicate treatment algorithms. These technical hurdles deter smaller hospitals from purchasing systems and restrain broad reimbursement approvals. Robotics and AI partially offset the problem but do not fully eliminate the need for structured credentialing.

Reimbursement Variability Across Regions Constraining Capital Procurement Budgets

Medicare in the United States reimburses transcranial doppler ultrasound market exams only for narrowly defined indications such as sickle-cell screening or collateral-flow checks during carotid surgery. Coupled with a 4.6% decline in inflation-adjusted neurosurgical payments, administrators hesitate to allocate funds for new consoles. Divergent coding frameworks in Europe create similar uncertainty, leading to regional adoption gaps despite clinical consensus on utility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Stroke Care Leads While TBI Gains Traction

Acute ischemic stroke accounted for the largest transcranial doppler ultrasound market share at 34.15% in 2025, supported by guideline endorsements for collateral-flow mapping prior to mechanical reperfusion. Integration into multimodal stroke pathways sustains equipment refresh cycles across comprehensive centers. Traumatic brain injury monitoring is the fastest climber with an 8.62% CAGR, propelled by defense-sector research and sports-medicine protocols. Pediatric sickle-cell screening remains a stable revenue stream anchored by mandatory annual protocols, while cerebral vasospasm surveillance after subarachnoid hemorrhage holds steady due to strong evidence backing daily Doppler checks.

Continuous innovation overlays all applications. AI-augmented decision support now suggests shunt gradings within seconds, narrowing interpretation variance. Cloud-based reporting accelerates neurosurgeon consults, allowing rapid escalation to angiography when flow velocities exceed critical thresholds. Collectively, these advances deepen clinical reliance on transcranial doppler ultrasound market solutions and extend monitoring beyond acute episodes into secondary-prevention regimes.

By Device Type: Portable Systems Alter Point-of-Care Landscape

Stand-alone consoles retained 61.72% revenue in 2025, underpinned by sophisticated waveform analytics and integrated patient-record interfaces in tertiary hospitals. However, portable units are registering a 10.15% CAGR, reflecting clinician preference for rapid bedside deployment. The transcranial doppler ultrasound market size attached to handheld devices is projected to double by 2031, driven by ambulance pilots and rural stroke-network roll-outs. Wearable patches now provide continuous bilateral flow trending, bridging gaps between periodic examinations.

Manufacturers enhance stand-alone offerings with robotic probe arms and AI libraries, preserving relevance for high-complexity cases. Hybrid carts embed battery-powered Doppler transceivers that dock into larger workstations, blurring category lines. A growing refurbished-equipment channel in Southeast Asia and Latin America further broadens access, although it exerts downward pressure on average selling prices.

By End User: Hospital Dominance Persists Amid Outpatient Surge

Hospitals controlled 68.45% of expenditure in 2025 as stroke teams expand neuro-vascular imaging arsenals. High-acuity needs keep demand resilient even as payers push procedures to lower-cost sites. The transcranial doppler ultrasound market share in ambulatory surgical centers is set to climb, supported by portable device economics aligning with short-stay reimbursement models. Diagnostic laboratories leverage cloud-linked Doppler fleets for routine sickle-cell screenings, while academic institutes drive prototype evaluations, securing grants for algorithm training on large flow-velocity datasets.

Industry partnerships between device OEMs and university hospitals facilitate validation of novel indices such as pulsatile cranial-expansion correlations with intracranial pressure. These collaborations seed future chronic-care applications and reinforce the Transcranial Doppler Ultrasound industry innovation pipeline.

Geography Analysis

North America led with 41.32% revenue in 2025, anchored by dense stroke-center networks and structured neuro-critical-care pathways. Favorable CPT codes for sickle-cell and carotid assessments support baseline volumes, though wider indication gaps remain. Pilot programs equipping paramedic teams with lightweight scanners illustrate the region’s appetite for pre-hospital adoption.

Europe ranks second, benefiting from universal coverage and robust research funding. France’s under-utilization of thrombectomy underscores latent demand for diagnostic capacity expansion; the United Kingdom’s GBP 6.5 (USD 8.7) million ultrasound brain-computer interface trial underscores public-sector commitment to frontier neuro-technologies. Meanwhile, Germany and the Nordics pursue national registry initiatives that integrate Doppler metrics, fostering evidence-based reimbursement dialogues.

Asia-Pacific is the fastest-growing territory at 7.95% CAGR as stroke incidence rises sharply and governments invest in tele-medicine. China’s provincial stroke-care maps mandate Doppler access in secondary hospitals, while India’s new stroke units boost procurement of portable consoles suitable for district facilities. Japan advances preventive screening programs targeting silent cerebral infarcts in seniors, amplifying recurring probe and maintenance revenues. Smaller but strategically important markets in the Middle East & Africa and South America embrace public-private financing models to import Transcranial Doppler Ultrasound market technologies alongside broader critical-care upgrades.

Competitive Landscape

The transcranial doppler ultrasound market is moderately concentated. NovaSignal, Viasonix, Rimed, and DWL Elektronische Systeme concentrate on neuro-sonology exclusives, differentiating through AI-embedded workflow automation. GE Healthcare, Koninklijke Philips N.V., Fujifilm Sonosite, and Samsung Medison leverage enterprise imaging ecosystems to bundle Doppler with cardiac and vascular ultrasound lines, capturing health-system-wide contracts.

Strategic collaborations accelerate feature roll-outs: Bracco Imaging’s alliance with BURL aims at ischemic stroke detection using advanced contrast agents. Patent activity around wearable transducers surged in 2024, highlighted by Novosound’s flexible-membrane sensor grant that paves the way for continuous monitoring bands. Robotics integration, epitomized by the Lucid System, eliminates expert sonographer dependency and signals a shift toward unattended monitoring stations in emergency rooms.

Pricing competition intensifies as Chinese entrants offer cost-effective portable units, prompting incumbents to emphasize software subscriptions and analytics dashboards. White-space opportunities persist in non-invasive intracranial pressure estimation, cerebral autoregulation trending, and home-based secondary stroke prevention kits areas where start-ups can carve niches before conglomerates replicate features.

Transcranial Doppler Ultrasound Industry Leaders

Viasonix

Rimed

B. Braun Melsungen AG

Konica Minolta Healthcare India Pvt. Ltd.

NovoSignal Corp

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key white-space area is moving from conventional nonimaging TCD toward more reproducible imaging-led workflows (TCDi/triplex), paired with automation that reduces operator dependency in emergency and neurocritical pathways. This aligns with the market shift toward point-of-care deployment, where portable and hand-held systems are the fastest-growing device type, and with clinical pathways that require rapid, repeatable cerebral hemodynamics monitoring across stroke and neuro-ICU settings.

Differentiation is also focused on expanding usable access in difficult acoustic windows, with roadmap work that includes contrast-enhanced approaches and signal-processing advances aimed at improving sensitivity and spatial resolution for transcranial applications. Opportunity also appears in protocol standardization and software-led decision support for high-volume, guideline-driven indications where TCD is already embedded, including vasospasm monitoring after subarachnoid hemorrhage, pediatric sickle-cell disease screening, and right-to-left shunt (PFO) evaluation. In shunt detection, institutional pathways increasingly pair contrast-enhanced TCD with contrast echocardiography, which supports demand for integrated reporting, cloud collaboration, and standardized grading across sites. On the regulatory and productization side, FDA 510(k) activity in ultrasonic pulsed Doppler imaging (for example, Sonio Detect v3, K252433, received for review in 2026 under 21 CFR 892.1550) highlights continued device iteration that supports broader clinical adoption and refresh cycles, particularly when combined with AI-assisted interpretation and workflow integration in stroke-center networks and tele-stroke programs.

Recent Industry Developments

- June 2026: Rimed disclosed data from the Digi-Lite program at the ARVO Annual Meeting, highlighting retinal-cerebral coupling measurements and the potential for continuous physiologic monitoring. The updates indicate momentum toward expanded clinical adoption.

- January 2025: Viasonix received FDA 510(k) clearance for its Falcon/Xpress vascular system. US clearance expands the addressable installed base for vascular and neurosonology workflows in hospitals that standardize procurement and clinical protocol roll-outs on cleared platforms.

- December 2024: Viasonix received CE MDR approval for the Falcon/Xpress vascular system. MDR readiness supports access to European tenders and refresh programs as providers prioritize compliant devices for long-lived capital equipment and associated software updates.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenues generated from transcranial Doppler ultrasound systems used to assess cerebral blood flow in clinical and screening settings, including associated software modules sold as part of the overall system offering.

Scope exclusions: We exclude ultrasound consumables, general neuro-ultrasound carts not configured for transcranial use, and service contracts billed separately from equipment sales.

Segmentation Overview

- By Application

- Sickle Cell Disease

- Acute Ischemic Stroke

- Intracranial Steno-Occlusive Disease

- Cerebral Vasospasm Monitoring

- Traumatic Brain Injury Management

- By Device Type

- Stand-alone Systems

- Portable/Hand-held Systems

- By End User

- Hospitals

- Diagnostic Laboratories

- Ambulatory Surgical Centers

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with mapping how TCD is used across stroke assessment, sickle cell screening, and stenosis monitoring, and then checking how those use cases translate into equipment demand in major care settings. We used public sources such as the World Health Organization, the US CDC, NIH, and PubMed-indexed clinical literature, along with government health statistics portals, to size the addressable patient pool and understand guideline-driven screening patterns.

To keep assumptions grounded, we also reviewed regulatory and product information in databases such as the US FDA device listings. We then cross-checked with hospital and radiology association materials that describe neurovascular workflow. Company annual reports, investor decks, and credible press releases were used to understand product mix shifts such as portable adoption and typical replacement cycles. Where needed, paid subscriptions for company financials and a patent database were referenced to support directional shares and innovation intensity. These examples are not exhaustive, and many other public sources were used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys focused on validating real-world buying behavior, average selling price ranges, and the split between stand-alone and portable systems across routine neurology and emergency use. We spoke with a mix of device-side leaders, distributors, and clinical users, so demand drivers, tender behavior, and replacement timing could be checked across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 13% | APAC: 46% |

| Mid tier: 57% | Functional/Unit leaders: 28% | EMEA: 29% |

| Smaller Players: 17% | Managers: 59% | Americas: 25% |

Market-Sizing & Forecasting

Sizing used a top-down and bottom-up approach. First, disease prevalence and screening intensity were used to rebuild the annual equipment demand pool by region, then translated into revenue through typical system pricing. Since TCD is linked to stroke pathways and sickle cell screening programs, we relied on indicators such as diagnosed stroke volumes, sickle cell screening coverage, neurovascular procedure load in hospitals, installed base replacement cycles, and the shift in demand toward portable systems.

Those outputs were corroborated with selective bottom-up approximations, including channel feedback on unit shipments, sampled price quotes for portable versus stand-alone systems, and sanity checks against supplier revenue exposure to neuro-ultrasound. Where data gaps appeared in smaller countries, the model used proxy ratios from similar health system profiles, and then the values were adjusted after expert feedback.

For forecasting, we used scenario analysis supported by short multivariate checks, so growth followed a set of transparent drivers such as guideline adoption, hospital capital spending, and portable device penetration. Assumptions were kept consistent in currency timing and inflation handling, so year-to-year changes are not overstated by exchange-rate noise.

Data Validation & Update Cycle

Validation was done in steps, starting with internal checks on volumes, pricing, and implied penetration so that no single assumption could swing the output without being visible. We compared results against independent signals like regional stroke burden direction, procurement activity patterns, and the pace of portable adoption discussed in interviews, then reviewed outliers before sign-off.

If a large variance was found during review, the analyst team re-checked inputs. When needed, we re-contacted relevant experts to confirm whether the change was real or just a data timing issue. The report is refreshed annually, and interim updates are made when material events occur, such as policy shifts, reimbursement changes, or major product launches. Before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Transcranial Doppler Ultrasound Market Size Measured Against Other Published Estimates

Different published numbers for this market can still look reasonable because firms may count different things, use different base years, or apply different price and volume logic. The biggest gaps usually come from whether the estimate sticks to dedicated transcranial Doppler systems or blends in broader neuro-ultrasound equipment. Another source of divergence is how strongly growth is tied to screening policy versus general hospital spending.

The table shows a wide spread. In Mordor Intelligence's model, the value reflects only transcranial Doppler ultrasound systems (stand-alone and portable) sold into defined clinical use settings, rather than bundling adjacent brain monitoring tools or unrelated ultrasound hardware into the same total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.53 B (2026) | |

| Global Consultancy A | USD 0.27 B (2024) | Uses an earlier base year and a narrower device definition that can undercount portable systems sold through broader ultrasound channels, and it may apply limited regional coverage and fewer end-user settings. |

| Industry Research Group B | USD 0.59 B (2024) | Shows a higher 2024 level that likely blends adjacent neuro-ultrasound or broader technology buckets, and it may assume faster ASP progression and more aggressive adoption tied to long-range forecasts. |

Taken together, the comparison suggests that scope boundaries and pricing assumptions are the main reasons the totals diverge. Our approach stays traceable because the model is built from a clear demand pool, checked with channel and clinical feedback, and then reviewed for year-to-year consistency before numbers are finalized.

Key Questions Answered in the Report

What is the current transcranial doppler ultrasound market size?

The transcranial doppler ultrasound market size is USD 525.19 million in 2026.

How fast will the transcranial doppler ultrasound market grow?

The market is forecast to register a 7.25% CAGR between 2026 and 2031.

Which application segment leads the transcranial doppler ultrasound market?

Acute ischemic stroke leads with 34.15% market share as of 2025.

Why are portable systems gaining traction in the transcranial doppler ultrasound market?

Portable units offer point-of-care flexibility and are growing at a 10.15% CAGR, driven by stroke-network deployments and ambulance integration.

Which region is the fastest-growing for transcranial doppler ultrasound solutions?

Asia-Pacific leads growth with an 7.95% CAGR, supported by expanding stroke centers and healthcare investment.

Page last updated on: