Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

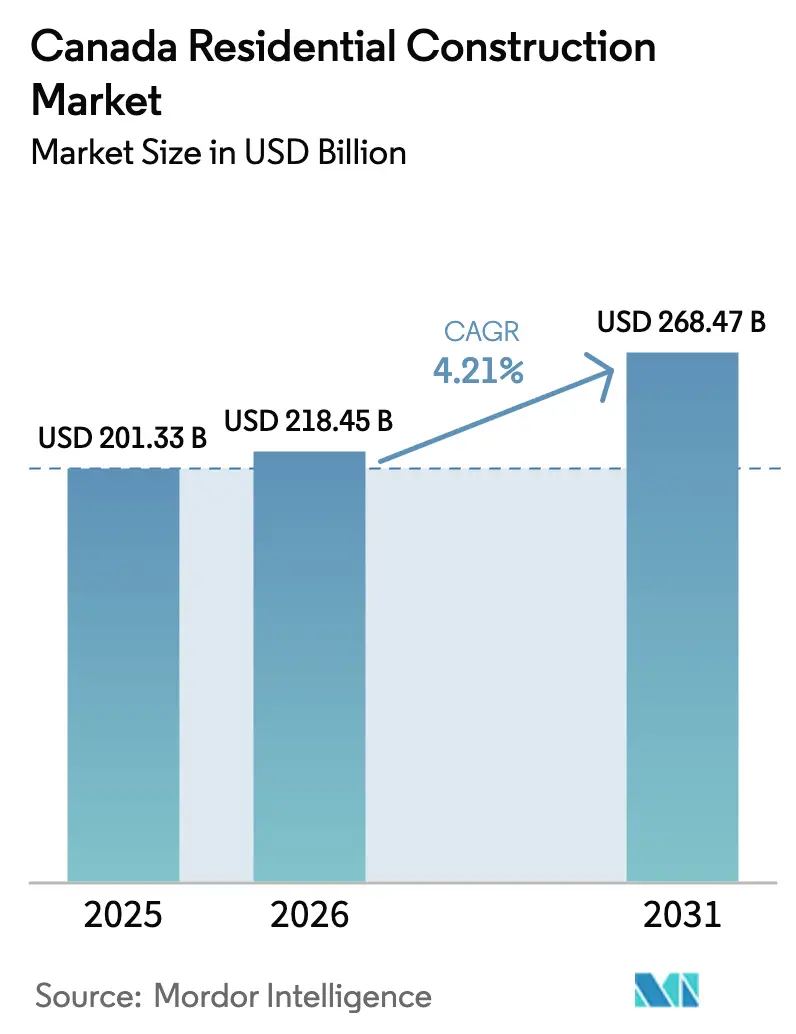

| Base Year Market Size (2025) | USD 201.33 Billion |

| Market Size (2026) | USD 218.45 Billion |

| Market Size (2031) | USD 268.47 Billion |

| Growth Rate (2026 - 2031) | 4.21% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Residential Construction Market Analysis by Mordor Intelligence

Canada residential construction market size is expected to increase from USD 210.33 inUSD 218.45 billion in 2026 to reach USD 268.47 billion by 2031, growing at a CAGR of 4.21% over 2026-2031. Federal financing that subsidizes rental apartments, modular-first procurement, and density-friendly zoning reforms are redirecting capital toward purpose-built rental supply. Immigration keeps household formation elevated in gateway metros even as the federal cap on temporary residents tempers national demand growth. Builders are pivoting to factory-controlled modular methods to mitigate skilled-trade shortages while municipalities expedite multiplex approvals to unlock infill land. Meanwhile, higher material and labor costs squeeze margins, incentivizing renovation over demolition in aging stock and accelerating adoption of low-carbon timber and prefab solutions.

Key Report Takeaways

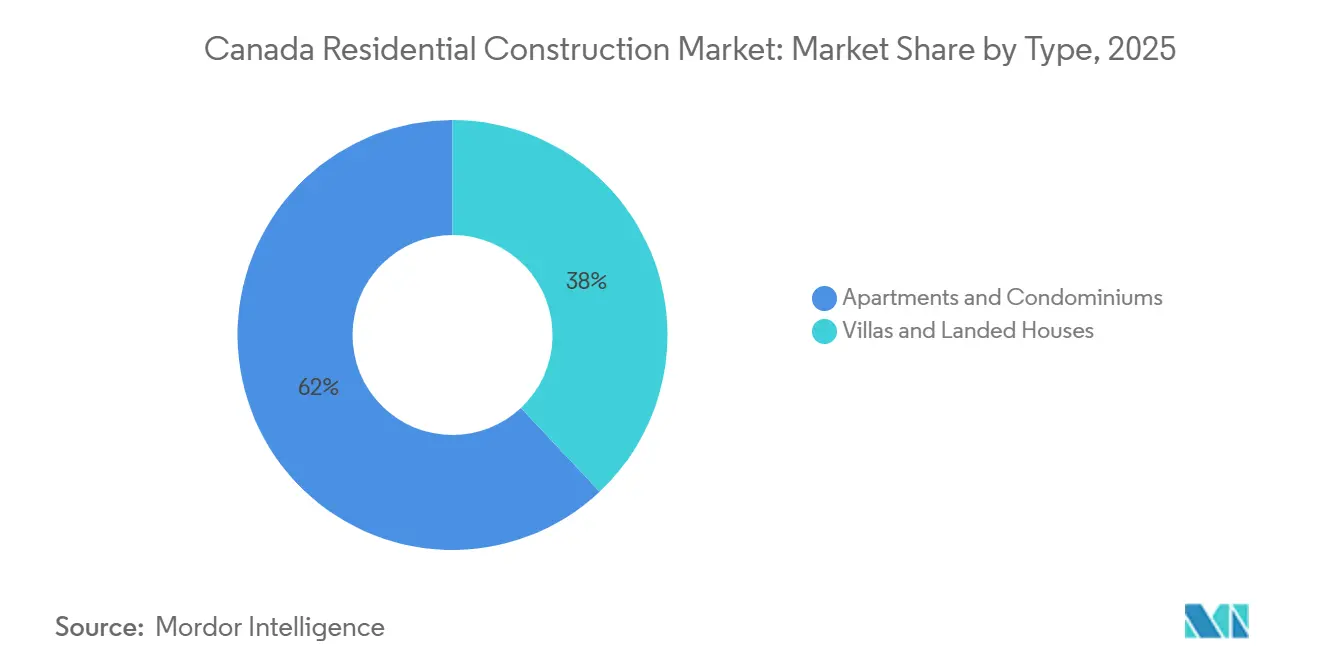

- By housing type, apartments and condominiums led with 62.0% of Canada residential construction market share in 2025 and is the fastest growing at a 6.30% CAGR through 2031.

- By construction type, new construction commanded a 59.4% share of the Canada residential construction market size in 2025, and renovation is projected to expand at a 5.20% CAGR to 2031.

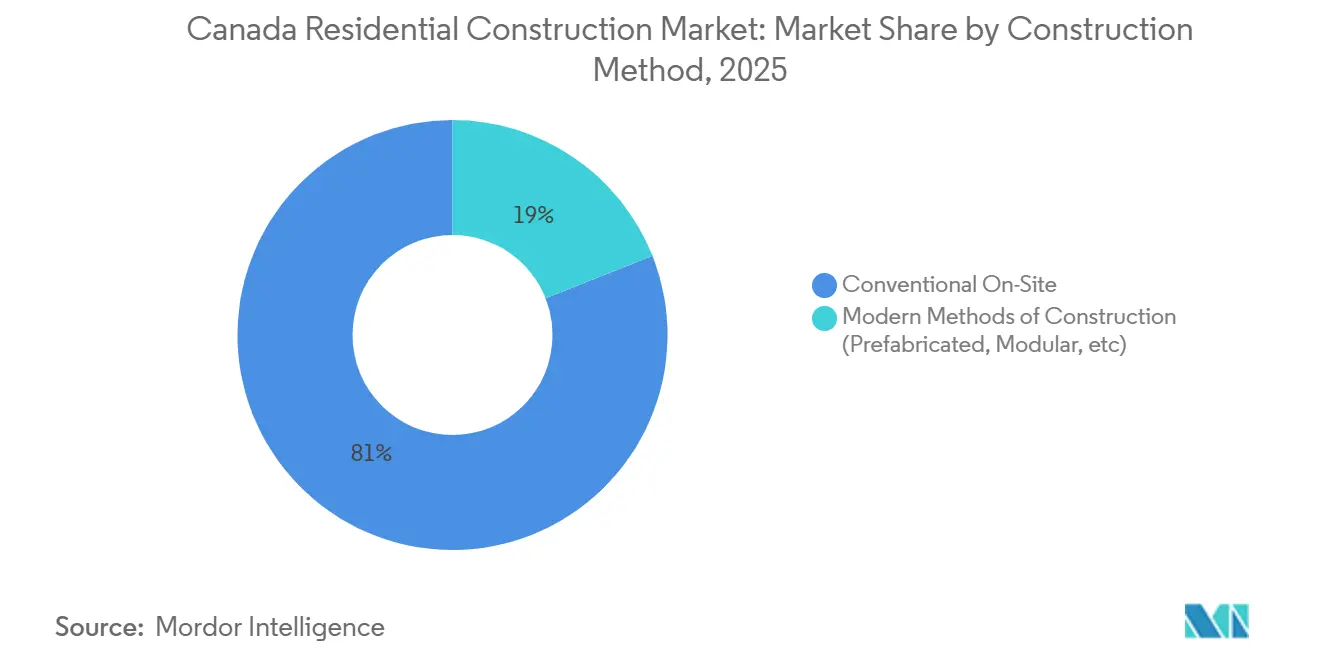

- By construction method, conventional on-site methods retained 81.0% of the Canada residential construction market share in 2025, while modern methods of construction are forecast to grow at a 7.40% CAGR through 2031.

- By investment source, private investment represented 78.0% of market activity in 2025, yet public funding will expand at a 6.1% CAGR as CMHC scales loan commitments to USD 56.25 billion by 2028.

- By city, Toronto captured 34.2% of the Canada residential construction market size in 2025, while Calgary is expected to post the highest growth at a 6.8% CAGR through 2031 driven by interprovincial migration and faster approvals.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Residential Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal housing incentives & CMHC financing | +1.2% | National, concentrated in Toronto, Vancouver, Montreal | Medium term (2-4 years) |

| Population growth & immigration-led demand | +0.9% | National; strongest in Toronto, Vancouver, Calgary | Short term (≤ 2 years) |

| Deteriorating ownership affordability | +0.8% | Toronto, Vancouver; spillover to Hamilton, Kelowna | Medium term (2-4 years) |

| Urban-density zoning reforms | +0.6% | Vancouver, Toronto, Victoria; mandates spreading | Long term (≥ 4 years) |

| Build Canada Homes modular pipeline | +0.5% | National; early gains in Ontario, British Columbia | Medium term (2-4 years) |

| Embodied-carbon codes | +0.3% | British Columbia, Ontario, Quebec | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Federal Housing Incentives & CMHC Financing

CMHC’s Apartment Construction Loan Program reached CAD 55 billion (USD 41.25 billion) in commitments by December 2025, delivering 50-year amortizations at rates 100-150 basis points below bank debt. Developers consequently accept 12% returns instead of the prior 18%, unlocking marginal rental sites. The Housing Accelerator Fund has transferred CAD 4.5 billion (USD 3.4 billion) to 179 municipalities, but only for those that shrink permitting time and allow multiplexes as-of-right. Build Canada Homes guarantees CAD 13 billion (USD 9.75 billion) of modular orders, removing volume risk for new factories. Together these levers push purpose-built rentals ahead of ownership condos and lower financing friction in high-cost markets.

Population Growth & Immigration-Led Demand

Canada gained 1.27 million residents in 2024, its largest annual increase on record, even as Ottawa now targets a 20% cut in temporary residents by 2027[1] Statistics Canada, “Population Estimates and Projections,” STATCAN.GC.CA. Toronto absorbed 37% of 2024 newcomers and keeps rental vacancies under 2%, pressuring rents despite record completions. Calgary gains from inter-provincial inflows; its 56,245 net migrants in 2024 tripled 2019 levels and lifted townhome sales. Demand clusters around 3-bedroom rentals because 62% of economic-class immigrants arrive with dependents, yet less than one-fifth of new rental supply offers three bedrooms. Builders able to deliver family-sized units capture out-sized absorption.

Deteriorating Ownership Affordability Shifting Demand to New Multifamily Supply

A resale median of CAD 1.14 million (USD 0.86 million) in Toronto now requires CAD 240,000 in household income, a hurdle only 9% of renter households clear. Capital exits condos and flows to institutionally financed rentals, evidenced by USD 9.6 billion in multifamily investment during 2024. Vancouver’s July 2024 up-zoning of 67,000 single-family lots unleashed a 340% surge in multiplex permits, absorbing teardown land at CAD 2.8 million (USD 2.10 million) and selling residual land at CAD 4.1 million (USD 3.07 million). The result is persistent rent growth of 5-7% even as ownership demand stalls.

Urban-Density Zoning Reforms

Ontario’s Bill 23 and British Columbia’s Housing Supply Act override municipal zoning to legalize 3-6-unit builds on former single-family parcels. Toronto single-family lots re-entitled for fourplexes now trade 35-40% above legacy parcels, unlocking land value and pushing builders to assemble infill sites near transit. Density-by-right trims soft-cost risk: projects that once cycled 18 months in discretionary review now secure permits inside 90 days, accelerating starts and broadening investor appetite for multiplex product.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating material & labor costs | -0.7% | National; acute in Toronto, Vancouver | Short term (≤ 2 years) |

| Lengthy municipal approvals & charges | -0.5% | Ontario municipalities, Metro Vancouver | Medium term (2-4 years) |

| Skilled-trade retirements | -0.4% | National; severe in Alberta, Ontario | Long term (≥ 4 years) |

| Urban grid capacity limits | -0.2% | Downtown Toronto and Vancouver cores | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Material & Labor Costs

Structural lumber rose 8.4%, reinforcing steel 5.1%, and concrete 4.3% in 2024, trimming margins by 150-200 basis points for projects underwritten 18 months ago. Wage growth averaged 4.8% as 23% of tradespeople are 55 plus, letting carpenters and electricians command premiums. A 6-story rental in Toronto now costs CAD 340 ft² (USD 255 ft²), USD 31 ft² higher than 2022. Modular contracts buffer inflation because material is purchased up-front, yet limited factory slots cap market share at 8% of multifamily starts.

Lengthy Municipal Approvals & High Development Charges

Greater Toronto municipalities demand CAD 95,000 (USD 71,250) per unit in fees versus CAD 28,000 (USD 21,000) in Calgary. Toronto’s site-plan approvals averaged 11.2 months in 2024 despite a statutory 90-day cap[2]City of Toronto Planning Department, “Approval Timeline Report 2024,” TORONTO.CA. Financing carry at 7% interest adds USD 9,000 per unit during each six-month delay, punishing thinly capitalized builders and steering them to cities like Montreal where Bill 16 caps charges at 5% of cost.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Housing Type: Rental Apartments Reshape Tenure Mix

Apartments and condominiums held 62.0% of Canada residential construction market share in 2025. Institutional investors favored stabilized yields of 4.2% that outstrip 10-year bond returns, channeling USD 9.6 billion into rentals in 2024. The Canada residential construction market size tied to apartments will widen as CMHC’s 50-year debt trims equity requirements. Detached villas trail because multiplex rezoning disincentivizes large-lot greenfield builds.

Ownership condos face absorption headwinds; mortgage stress-test thresholds of USD 135,000-180,000 exclude most renters. Developers shift land banks to transit-oriented parcels fit for 6-10-story rentals that achieve 2.5-3.5 FAR and quintuple revenue per acre versus single-family. Alberta and Atlantic provinces still record villa demand thanks to cheaper detached prices, yet their collective volume cannot offset the pivot to dense rental product nationally.

Note: Segment shares of all individual segments available upon report purchase

By Construction Type: Renovation Gains as Retrofit Mandates Bite

New construction dominated 69.92% of the Canada residential construction market size in 2025, a position enhanced by incentives exclusive to newly built homes. Thirty-year amortizations and full GST rebates tip buyer calculus toward new units, while immigrant families seeking larger households gravitate to purpose-built rentals. Developers prioritize shovel-ready sites near transit nodes to maximize absorption speed and meet lender covenants[3]National Research Council Canada, “National Building Code 2025,” NRC.CA.

Renovation posts a healthy 5.48% CAGR fueled by aging stock, energy-efficiency mandates, and climate resilience upgrades. The Canada Greener Homes program and provincial tax credits underwrite deep retrofits that lower utility bills and carbon output. Quebec expects USD 14.8 billion in residential renovation outlays in 2025, powered by Bill 16 rules that require detailed maintenance plans for condominiums. Contractors skilled in heat-pump installation, floodproof basements, and wildfire-resistant cladding benefit from rising homeowner awareness. This retrofit wave complements but does not displace new supply, together expanding the Canada residential construction market.

By Construction Method: Modular Gains Factory Capacity

Conventional on-site work still comprised 81.0% of Canada residential construction market share in 2025. Modern methods of construction, however, are expected to post a 7.40% CAGR, accelerating the Canada residential construction market size linked to prefab systems. British Columbia requires modular consideration for social housing over 50 units and already counts 12% of starts as modular. Factory environments trim project schedules by up to 40% and lock costs, attractive amid 4.8% wage inflation.

High-rise concrete towers keep standard formwork advantages—tighter floor-to-floor heights and acoustic performance—but 4-6-story wood-frame rentals now default to modules priced at USD 214-233 ft² versus USD 248-270 for site-built equivalents. The strategic risk is lumpy order flow; break-even needs 70-80% factory utilization, pressing firms like EllisDon-Horizon North’s Winnipeg plant to chase public contracts as volume anchors.

Note: Segment shares of all individual segments available upon report purchase

By Investment Source: Public Capital Tilts Toward Rental

Private sources supplied 78.0% of capital in 2025, yet public investment will rise at 6.1% CAGR as CMHC expands its loan book to CAD 75 billion (USD 56.25 billion) by 2028. Social and affordable projects often blend 60-70% subsidy, pulling otherwise infeasible rental developments into viability with sub-4% cap rates.

Pension funds and REITs poured USD 9.6 billion into multifamily assets in 2024, tripling 2019 allocations, chasing inflation-hedged returns. Municipalities vie for Housing Accelerator Fund dollars, waiving fees and shaving months off approvals, thereby lowering private developers’ hurdle rates and further growing blended-capital deal structures.

Geography Analysis

Toronto commanded 34.2% of market value in 2025, yet housing starts fell 8.2% in 2024 as development charges climbed to CAD 95,000 (USD 71,250) per unit and approvals averaged 11-14 months. The Greater Toronto Area still absorbed 37% of Canada’s permanent immigrants in 2024, keeping rental vacancies under 1.8%. Bill 23 legally caps approval timelines at 90 days, but compliance reached only 42% in 2024, prolonging financing carry. Developers now target “major transit station areas” where provincial density permissions grant 8-12 stories as-of-right, unlocking 18,000 hectares of under-used employment land.

Vancouver’s blanket rezoning of 67,000 single-family parcels to fourplex status in July 2024 produced 1,847 permit filings in six months, compressing per-door land cost by 35-40% and pushing average 1-bedroom rents to USD 1,988—18% above Toronto. Provincial mandates legalizing 3-6 units near transit touch 85% of Metro lots, feeding a decade-long multiplex pipeline. Modular usage hit 12% of multifamily starts in 2025 as social-housing contracts stipulate factory production.

Calgary looks set to grow at 6.8% CAGR through 2031 thanks to 56,245 net provincial in-migrants in 2024, a flat 10% income tax, and no provincial sales tax. Serviced land costs hover at USD 135,000-165,000 per acre, letting builders price 3-bedroom townhomes at USD 364,000—half of Toronto equivalents. Nine-month approvals slice USD 13,500-18,750 per unit in interest carry compared with Toronto timelines. Montreal benefits from a provincial 5% fee cap that shrinks break-even by 14-18 months and secures stabilized yields above 5%, despite slower population gains.

Competitive Landscape

PCL Construction, EllisDon, and Graham Construction command tall-tower formwork through proprietary climbing systems and track records that pension funds trust for on-time delivery. Their gross margins compress to 8-10% amid rising wages, propelling each to pilot modular joint ventures for higher 12-15% margin targets.

Vertical integration is the emerging battleground. EllisDon partnered with Horizon North to open a USD 71 million Winnipeg modular plant slated for 1,200 units annually by 2027, locking in Build Canada Homes pipeline demand. Graham Construction completed a USD 165 million CLT-based Vancouver tower, capturing municipal carbon bonuses and gaining a 48-unit entitlement bump. Smaller regionals like Urban One Builders exploit 4-6-story wood-frame niches in Vancouver, shaving three months off schedules and earning outsized share of Housing Accelerator Fund-backed projects.

Digital adoption differentiates bids. EllisDon’s BIM-twin platform cut six months off Toronto’s 65-story The One tower, winning a follow-on USD 315 million rental contract. Contractors lacking robust VDC teams lose out on design-build jobs where owners value certainty over lowest cost. M&A remains limited; family ownership dominates 60% of firms and balks at 6-8× EBITDA sale multiples. Consequently, the landscape will likely stay fragmented outside a handful of national integrators.

Canada Residential Construction Industry Leaders

PCL Construction

EllisDon Corporation

Graham Construction

Ledcor Group of Companies

Pomerleau Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: PCL Construction won a USD 289 million contract for a 42-story rental tower in Toronto financed via CMHC loans and local fee waivers, achieving a sub-4% cap rate.

- January 2026: EllisDon and Horizon North committed USD 71 million to a Winnipeg modular factory with 1,200-unit annual capacity under Build Canada Homes offtake guarantees.

- December 2025: Graham Construction delivered a USD 165 million 38-story Vancouver condo tower using mass-timber podiums that cut embodied carbon 35%.

- November 2025: Pomerleau acquired a Montreal site for USD 31 million, planning 850 rentals near the REM light-rail extension with 5% capped fees.

Canada Residential Construction Market Report Scope

Residential construction is a process that involves the expansion, renovation, or construction of a new home or spaces intended to be occupied for residential purposes. These structures range from single-family homes and multi-family units to townhouses, condominiums, and apartment buildings. The Canadian residential construction market is segmented by type (apartments/condominiums and villas/landed houses), and by key city (Edmonton, Calgary, Toronto, Vancouver, Ottawa, Montreal, and Rest of Canada). The Report Offers Market Sizes (USD) and Forecasts for all the Above Segments.

By Housing Type

| Apartments & Condominiums |

| Villas & Landed Houses |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Modular, Prefab) |

By Investment Source

| Public |

| Private |

By City

| Toronto |

| Vancouver |

| Montréal |

| Calgary |

| Rest of Canada |

| By Housing Type | Apartments & Condominiums |

| Villas & Landed Houses | |

| By Construction Type | New Construction |

| Renovation | |

| By Construction Method | Conventional On-Site |

| Modern Methods of Construction (Modular, Prefab) | |

| By Investment Source | Public |

| Private | |

| By City | Toronto |

| Vancouver | |

| Montréal | |

| Calgary | |

| Rest of Canada |

Key Questions Answered in the Report

How large is the Canada residential construction market today?

The Canada residential construction market size reached USD 218.45 billion in 2026 and is projected to climb to USD 268.47 billion by 2031.

What is driving growth in Canadian residential construction?

Federal low-cost loans, immigration-driven household formation, and zoning reforms that legalize multiplexes are the primary catalysts.

Which housing segment is expanding fastest?

Apartments & Condominiums are forecast to grow at a 6.30% CAGR through 2031 as investors seek inflation-hedged, long-duration income.

Why are builders adopting modular methods?

Guaranteed federal offtake, shorter schedules, and labor scarcity make modules attractive, pushing modern-method growth to a 7.40% CAGR.

Which city offers the best growth prospects?

Calgary leads with an expected 6.8% CAGR through 2031, supported by net in-migration, abundant serviced land, and quicker approvals.

How will renovation activity evolve?

Retrofit mandates tied to the 2025 building code push renovation to a 5.20% CAGR, targeting upgrades in 1.2 million pre-1980 units.

Page last updated on: