Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

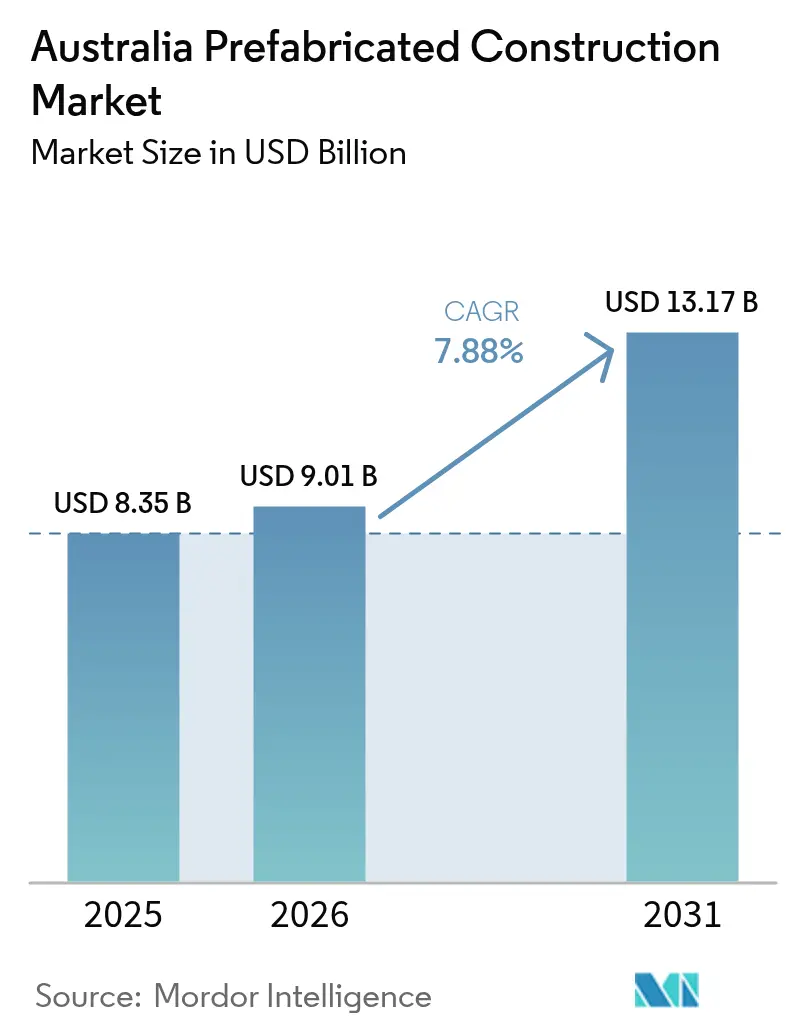

| Base Year Market Size (2025) | USD 8.35 Billion |

| Market Size (2026) | USD 9.01 Billion |

| Market Size (2031) | USD 13.17 Billion |

| Growth Rate (2026 - 2031) | 7.88% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Prefabricated Construction Market Analysis by Mordor Intelligence

The Australia Prefabricated Construction Market size was valued at USD 8.35 billion in 2025 and estimated to grow from USD 9.01 billion in 2026 to reach USD 13.17 billion by 2031, at a CAGR of 7.88% during the forecast period (2026-2031). Tight housing supply, persistent skilled-labour shortages, and stricter energy-performance rules under the National Construction Code 2022 are steering developers toward factory-based production lines that compress schedules and curb cost overruns. Federal and state programs, including the Housing Australia Future Fund and National Housing Accord, guarantee multi-year volume, while institutional capital is flowing into build-to-rent pipelines that demand repeatable, quality-assured modules. Productivity losses in traditional construction deepen the shift; dwellings completed per hour worked have dropped 53% since the mid-1990s, making industrialized methods a structural necessity. At the same time, modern prefabrication aligns with rising ESG mandates, because controlled assembly minimizes site waste and supports low-carbon materials such as cross-laminated timber.[1]https://www.housingaustralia.gov.au/

Key Report Takeaways

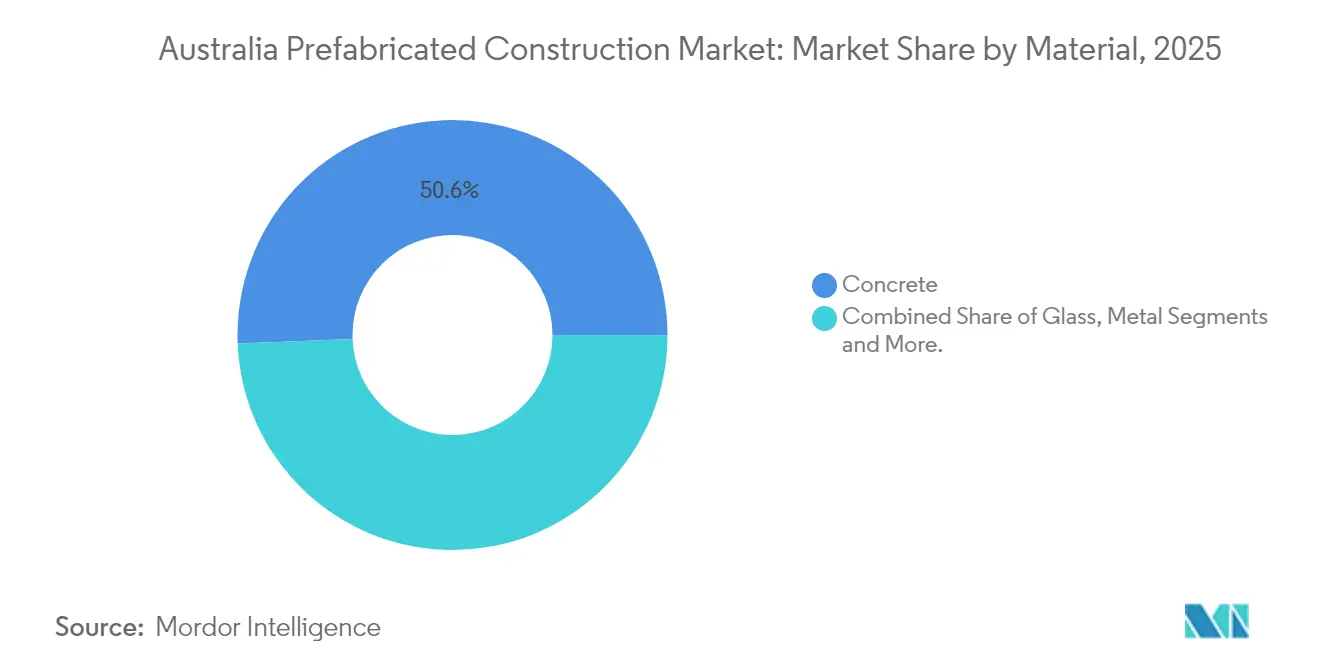

- By material, concrete led with a 50.63% revenue share of the Australia prefabricated buildings market in 2025, whereas engineered cross-laminated timber is poised for the fastest 8.15% CAGR through 2031.

- By application, residential construction held 56.92% of the Australia prefabricated buildings market share in 2025, while commercial schemes are projected to register an 8.29% CAGR to 2031.

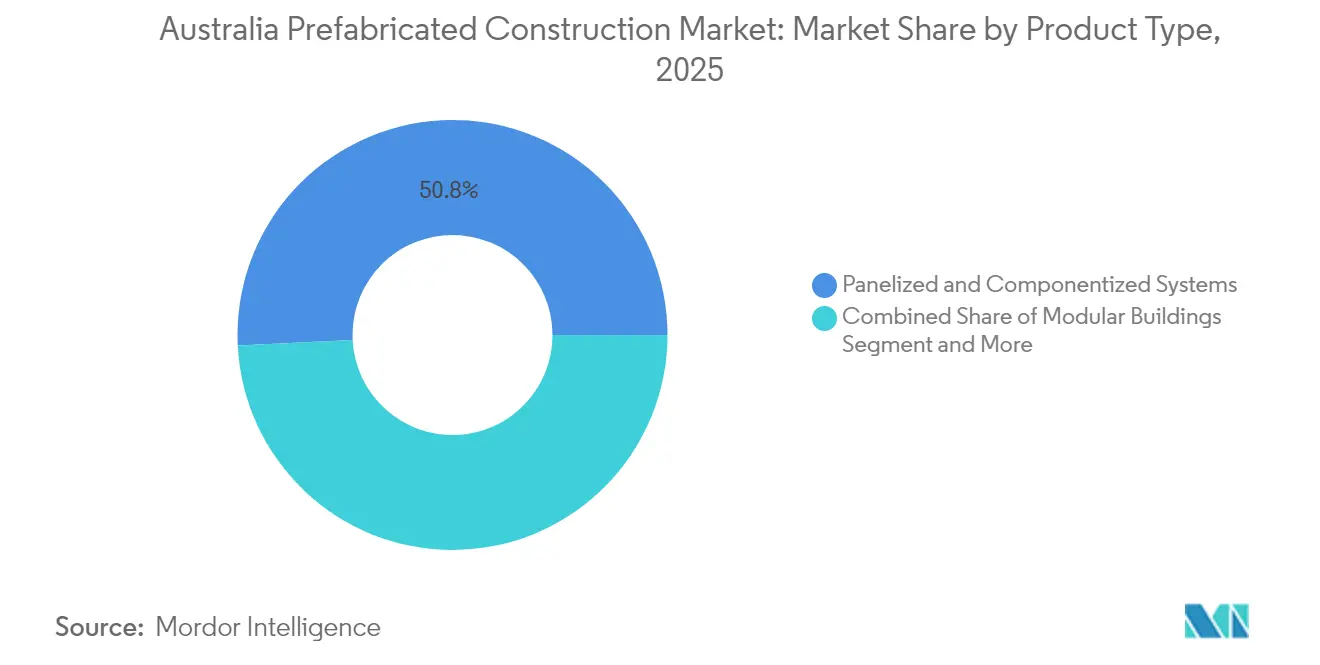

- By product type, panelized and componentized systems captured 50.78% of the Australia prefabricated buildings market size in 2025 and are forecast to grow at an 8.52% CAGR during 2026-2031.

- By city, Sydney accounted for 23.66% of 2025 demand, whereas Perth is forecast to expand at an 8.46% CAGR through 2031, the quickest among major cities.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Prefabricated Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute housing undersupply and government-backed social/affordable programs favor faster offsite delivery | +2.1% | National, with early gains in NSW, Victoria, Queensland, Western Australia | Medium term (2-4 years) |

| Skilled-labor shortages and high site wages make factory fabrication more cost-predictable | +1.8% | National, acute in Sydney, Melbourne, Brisbane metro construction zones | Short term (≤ 2 years) |

| NCC 2022 energy standards and net-zero goals driving demand for high-performance modular envelopes | +1.4% | National, strongest in Victoria and ACT with aggressive net-zero timelines | Medium term (2-4 years) |

| Rapid-delivery needs in education, healthcare, defense, and disaster recovery suit modular rollouts | +1.2% | National, concentrated in regional Queensland, Northern Territory, and disaster-prone NSW coastal zones | Short term (≤ 2 years) |

| CLT/GLT timber and steel modular growth for mid-rise, BTR, and student housing in major cities | +1.0% | Sydney, Melbourne, Brisbane, Perth CBD and inner-ring suburbs with mid-rise zoning | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acute Housing Undersupply and Government-Backed Social/Affordable Programs Favor Faster Offsite Delivery

Australia’s National Housing Accord sets a 1.2-million-unit goal by 2030, a scale impossible for site-built techniques to match under present labour constraints. New South Wales has committed to 90 modular dwellings by mid-2026, and Victoria reports 40-50% faster build times plus 60% lower in-process energy when prefabrication is used. Queensland’s 600-unit modular pledge for 2024 underscores statewide momentum. Large-scale funds funnelling capital into social housing now score bidders on ISO 9001 accreditation, automated lines, and delivery track record, limiting access for small, site-only builders. The guaranteed volume enables manufacturers to invest in robotics and lean workflows that push unit costs below conventional builds.

Skilled-Labor Shortages and High Site Wages Make Factory Fabrication More Cost-Predictable

The Housing Industry Association calculates a shortfall of 83,348 tradespeople, inflating wages yet failing to lift output. Centralizing labour in factories lifts productivity through repetitive tasks and optimized tooling; Lendlease Podium installed 137 hospital modules in eight weeks, a pace unattainable on open sites. Automation is advancing: the QUENDA-BOT robot achieved ±5 mm accuracy on mass-timber screws and could trim schedules by 20%. Prefabrication also curbs remote-site costs, because worker travel and accommodation are captured once in plant overhead rather than repeated daily on site.

NCC 2022 Energy Standards And Net-Zero Goals Driving Demand For High-Performance Modular Envelopes

Seven-star residential energy ratings and mandatory photovoltaics now apply nationally, forcing airtight assemblies and robust insulation that factory settings deliver reliably. The Legacy Living Lab in Perth showed 58% of materials can be reused, cutting waste to 1% at end-of-life. Developers such as Mirvac embed modular timber to satisfy embodied-carbon targets without elongating schedules. Standards Australia highlights digital twins as a route to halve design cycles, letting teams validate compliance virtually before cutting a single panel.

Rapid-Delivery Needs in Education, Healthcare, Defence, And Disaster Recovery Suit Modular Rollouts

Modular classrooms at Bellbird Park Secondary were delivered in 32 weeks for AUD 14 million, letting the school open on schedule for the new academic year. Modscape expanded Waverley Private Hospital without shutting sensitive wards. Defense tenders now specify relocatable units so bases scale quickly, and pandemic centres added 2,000 beds across three capitals using volumetric blocks. In disaster-prone NSW zones, 12,000 eligible property buybacks signal rising demand for temporary modular housing.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented state permitting/certification and limited standardization slowing approvals | -1.3% | National, most acute in NSW, Victoria, Queensland due to differing state building codes | Medium term (2-4 years) |

| Transport/cranage over long distances and urban last-mile constraints raising delivered costs | -0.9% | National, concentrated in remote Western Australia, Northern Territory, and dense Sydney/Melbourne CBD zones | Short term (≤ 2 years) |

| Financing pressures and developer insolvencies creating pipeline volatility for manufacturers | -0.7% | National, most severe in NSW and Victoria where developer insolvencies peaked in 2024 | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented State Permitting/Certification And Limited Standardization Slowing Approvals

Each state enforces unique inspection and paperwork sequences, forcing manufacturers to tweak identical modules for separate approvals. The Victorian Building Authority is researching unified pathways, but adoption remains voluntary. A University of Melbourne digital-twin eApprovals pilot that began in 2025 aspires to auto-check compliance, yet full rollout depends on multi-state cooperation. Until a national system mirrors Europe’s ETA model, prefabricators carry duplicated engineering and legal costs that blunt scale advantages.

Transport/Cranage Over Long Distances And Urban Last-Mile Constraints Raising Delivered Costs

The National Heavy Vehicle Regulator caps modules at 2.5 m width and 4.3 m height, compelling some designs to split for haulage then reassemble on site. Remote mine deliveries can exceed AUD 50,000 per module in escorts and road-user charges. Dense CBD precincts face night-lift fees of AUD 20,000–40,000 per crane pick, with narrow windows that push labor to overtime rates. Regional micro-factories and flat-pack geometries ease costs but cannot yet offset all distance penalties.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Concrete Leads While Timber Accelerates

Concrete accounted for 50.63% of 2025 revenue, underscoring its fire resistance and structural capacity in mid- and high-rise shells. Automation in batching plants and steel-cage prefabrication enables tight tolerances and rapid curing, giving concrete a reliability edge for podiums and industrial warehouses. The Australia prefabricated buildings market size attributed to precast concrete is further supported by long-term service records in harsh climates. However, embodied-carbon penalties spur developers to evaluate lighter alternatives when design codes permit.

Engineered cross-laminated timber is projected to grow at an 8.15% CAGR, the strongest rate among materials. Cedar Pacific and Sumitomo Forestry are scaling CLT output, while builders leverage the material’s carbon-sequestration benefit to meet ESG commitments. Mass-timber panels allow mid-rise frames to top out weeks earlier than steel or concrete, supporting faster cash flow for build-to-rent investors. Robotics such as QUENDA-BOT improve precision to ±5 mm, lowering rework and positioning timber as a prime beneficiary of digital fabrication. Glass curtain-wall panels and steel-framed modules preserve niche roles for premium façades and rugged mining camps, ensuring the Australia prefabricated buildings market remains multipolar rather than converging on a single dominant material.

By Application: Residential Dominates, Commercial Picks Up Pace

Residential projects held 56.92% of the Australia prefabricated buildings market in 2025, a position anchored by social-housing mandates and the steep supply gap. Catalogue-style modular homes let buyers select finishes without triggering new engineering, shortening approvals and holding costs. The National Housing Accord pipeline secures volume for at least five years, enhancing factory utilization and price stability. Developers like Mirvac channel modular design into a USD 1.8 billion build-to-rent vehicle, expanding the residential addressable base.

Commercial prefabrication is forecast to post an 8.29% CAGR to 2031, buoyed by office fit-outs and mixed-use podiums where faster lease-up boosts investor returns. Lendlease’s 127-module Northern Hospital wing, installed in five weeks, illustrates the throughput edge, which feeds into tenant income sooner. Retail expansions deploy panelized shells to avoid multi-month shutdowns, while logistics operators retrofit distribution centres with modular mezzanines. The Australia prefabricated buildings industry also finds traction in education, healthcare, and defense where repeatable room sizes optimize volumetric layouts. Disaster-recovery housing rounds out demand, anchored by state buyback schemes in flood-prone corridors.

By Product Type: Panelized Systems Maintain Lead and Growth

Residential projects held 56.92% of the Australia prefabricated buildings market in 2025, a position anchored by social-housing mandates and the steep supply gap. Catalogue-style modular homes let buyers select finishes without triggering new engineering, shortening approvals and holding costs. The National Housing Accord pipeline secures volume for at least five years, enhancing factory utilization and price stability. Developers like Mirvac channel modular design into a USD 1.8 billion build-to-rent vehicle, expanding the residential addressable base.

Commercial prefabrication is forecast to post an 8.29% CAGR to 2031, buoyed by office fit-outs and mixed-use podiums where faster lease-up boosts investor returns. Lendlease’s 127-module Northern Hospital wing, installed in five weeks, illustrates the throughput edge, which feeds into tenant income sooner. Retail expansions deploy panelized shells to avoid multi-month shutdowns, while logistics operators retrofit distribution centres with modular mezzanines. The Australia prefabricated buildings industry also finds traction in education, healthcare, and defense where repeatable room sizes optimize volumetric layouts. Disaster-recovery housing rounds out demand, anchored by state buyback schemes in flood-prone corridors.

Geography Analysis

Sydney’s 23.66% slice of Australia's prefabricated buildings market in 2025 rests on high-rise infill and a social-housing drive that mandates rapid delivery. The Building Homes for NSW program finances 90 modular dwellings before mid-2026, and flood-buyback zones add demand for both temporary and permanent units. Wild Modular handed over the state’s first factory-built social homes in Smithfield, indicating official comfort with prefabrication at scale. Yet crane-time premiums of AUD 20,000–40,000 per lift constrain adoption in the tight CBD core, pushing developers to order lighter panel sets that fit smaller rigs.

Perth is set for the highest growth thanks to mining workforce accommodation and state-backed social housing efforts. Long-haul freight charges remain stiff, but major resource clients accept premiums to avoid scarce site labor. The city’s less congested grid simplifies cranage, and low-cost land invites larger automated factories that feed Western Australia and export paths to Asia. Circular-design pilots such as Legacy Living Lab elevate Perth’s ESG narrative, aiding capital raising for green bonds linked to modular assets.

Melbourne secures the second-largest share through institutional pipelines, including Mirvac’s USD 1.8 billion build-to-rent fund and AustralianSuper’s rent-to-own model, both committed to modular rollouts. The Victorian Building Authority’s reform project, expected to finish in 2025, should harmonize certification for industrialized construction, smoothing approvals and encouraging further plant investment. Brisbane benefits from Queensland’s 600-unit modular target and modular classrooms, while remote regions leverage prefabrication for defense expansions and cyclone-recovery housing despite transport mark-ups. Consolidation through Stockland-Supalai’s 2024 purchase of Lendlease’s master-planned communities spreads demand across capitals, giving factories long-range order visibility.

Competitive Landscape

Australia's prefabricated buildings market remains fragmented, yet strategic moves signal accelerating consolidation. Incumbents such as Lendlease Podium, Fleetwood, Ausco Modular, and Hickory Group scale via ISO 9001 plants, extensive project logs, and proprietary BIM toolkits. Mirvac confirmed modular adoption across a USD 29 billion pipeline, indicating top-tier developers now internalize offsite capacity to hedge subcontractor risk. Emerging entrants deploy robotic screw-fixing, digital twins, and patent-protected connection nodes. Construction Systems Australia holds US Patent 8151539 for a panel link, showing IP as a defensive moat.

Strategic patterns include vertical integration of design studios and MEP engineers, guaranteeing end-to-end control and de-risking interfaces. Manufacturers form 10-year offtake pacts with superannuation funds to supply build-to-rent apartments, trading volume certainty for price rebates. Meanwhile, credit tightening after high-profile insolvencies (Nicheliving, Roberts Co, Cubitt’s Granny Flats) raises counterparty risk; plants now demand larger deposits, squeezing small developers from the order book. Technology is the new differentiator: firms using automated compliance checking halve design cycles and cut RFIs, lifting bid-win rates on state tenders.

White-space opportunities persist in regional micro-factories that slice haul distances and in circular logistics models that refurbish and redeploy modules instead of scrapping them. Robotic fabrication lines for timber panels can lower unit costs as material offcuts shrink and accuracy rises. Policy support is reinforcing advantages for quality-focused players; the December 2024 ABCB handbook standardizes inspection pathways, shrinking approval variance across states. Over the next five years, expect tier-one contractors to deepen alliances with module specialists while private equity scouts’ margin-rich specialty niches such as healthcare pods and defense barracks.

Australia Prefabricated Construction Industry Leaders

Ausco Modular Construction Pty Ltd

Fleetwood Australia

Modscape

Hickory Group (TBS)

Archiblox Pty Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The University of Melbourne launched the ePlanning & eApprovals digital-twin project to automate permit checks and cut approval times.

- January 2025: Standards Australia published a digital-engineering paper advocating BIM and twin adoption across construction.

- December 2024: The ABCB released a national prefabrication handbook harmonizing inspection protocols for modular systems.

- September 2024: ACCC cleared Stockland-Supalai’s acquisition of 12 Lendlease community projects, signaling developer consolidation.

Australia Prefabricated Construction Market Report Scope

Prefabrication, under modular construction, is the practice of assembling components of a structure in a factory or other manufacturing site and transporting complete assemblies or sub-assemblies to the construction site. A comprehensive background analysis of the market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, emerging trends in the segments, market dynamics, geographical trends, and COVID-19 impact, is covered in the report.

The Australian modular construction market is segmented by material type (concrete, glass, metal, timber, and other material types) and application (residential, commercial, and other applications (infrastructure and industrial)). The report offers market sizes and forecasts in value terms (USD) for all the above segments.

By Material (Value)

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Application (Value)

| Residential |

| Commercial |

| Others |

By Product Type (Value)

| Modular Buildings |

| Panelized & Componentized Systems |

| Other Prefab Types |

By Key City (Value)

| Sydney |

| Melbourne |

| Brisbane |

| Perth |

| Rest of Australia |

| By Material (Value) | Concrete |

| Glass | |

| Metal | |

| Timber | |

| Other Materials | |

| By Application (Value) | Residential |

| Commercial | |

| Others | |

| By Product Type (Value) | Modular Buildings |

| Panelized & Componentized Systems | |

| Other Prefab Types | |

| By Key City (Value) | Sydney |

| Melbourne | |

| Brisbane | |

| Perth | |

| Rest of Australia |

Key Questions Answered in the Report

How large is the Australia prefabricated buildings market in 2026?

It stands at USD 9.01 billion and is forecast to grow to USD 13.17 billion by 2031.

What growth rate is expected for prefabricated buildings in Australia?

The sector is projected to register a 7.88% CAGR between 2026 and 2031.

Which material segment is expanding the fastest?

Engineered cross-laminated timber is forecast to post an 8.15% CAGR through 2031.

Why are developers in Australia favoring factory-built modules?

They compress schedules, offset skilled-labor shortages, and meet stricter energy-performance codes.

Which city is forecast to record the highest growth through 2031?

Perth is expected to advance at an 8.46% CAGR, the quickest among major metros.

What policy steps support modular construction nationally?

The National Housing Accord, the Housing Australia Future Fund, and the ABCB’s prefabrication handbook all streamline demand and compliance.

Page last updated on: