Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

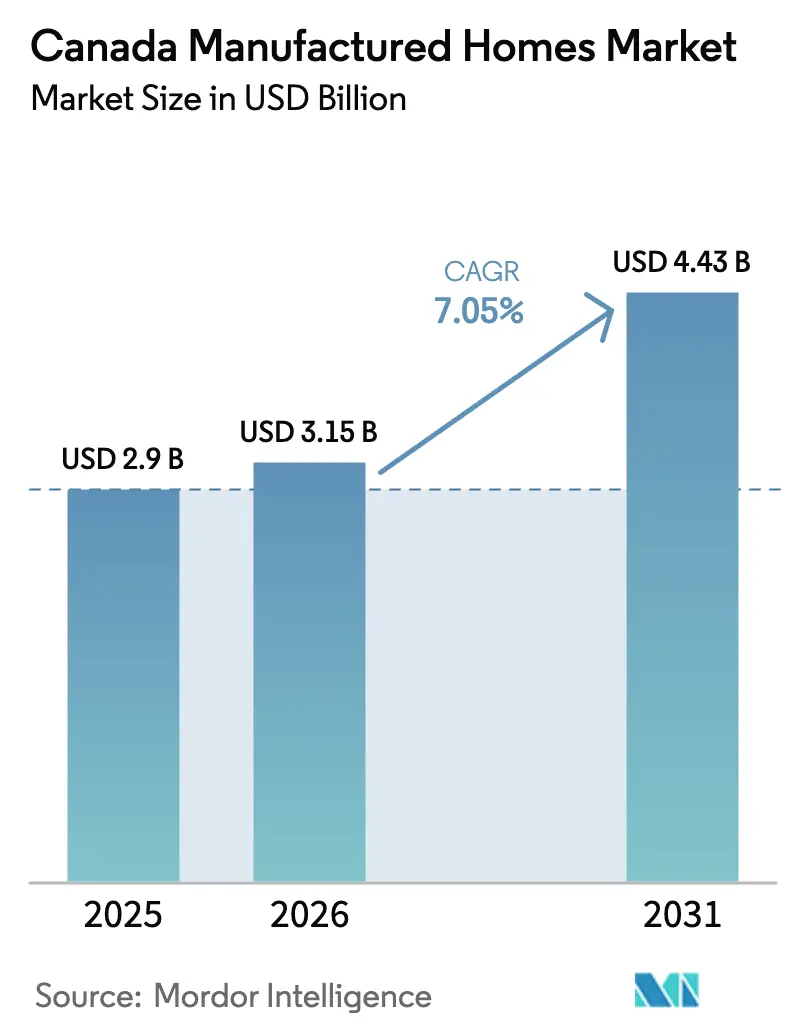

| Base Year Market Size (2025) | USD 2.9 Billion |

| Market Size (2026) | USD 3.15 Billion |

| Market Size (2031) | USD 4.43 Billion |

| Growth Rate (2026 - 2031) | 7.05% CAGR |

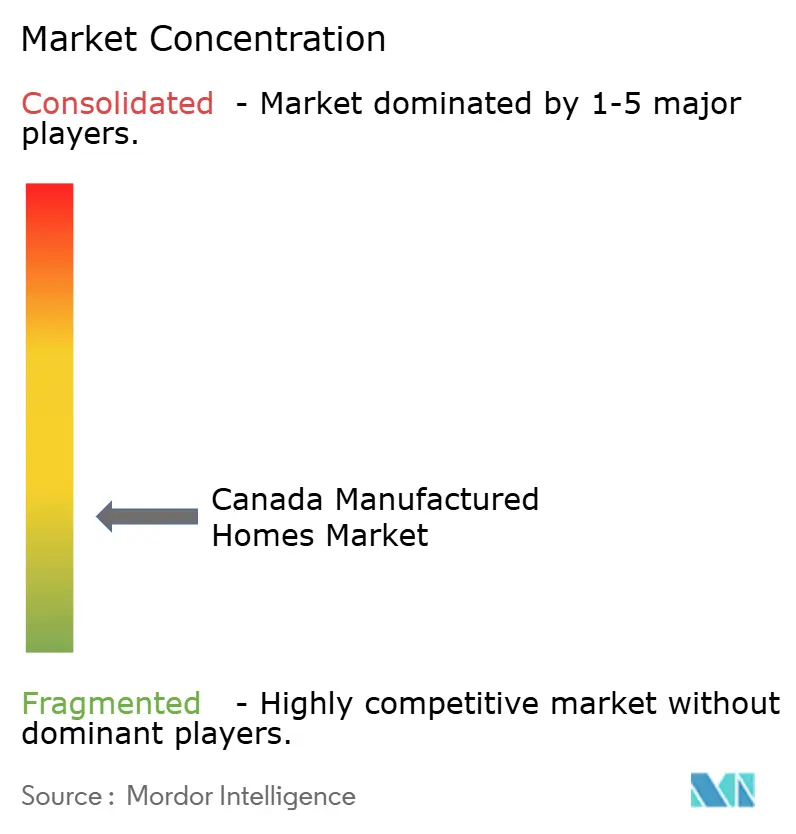

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Manufactured Homes Market Analysis by Mordor Intelligence

The Canada Manufactured Homes Market size is expected to increase from USD 2.9 billion in 2025 to USD 3.15 billion in 2026 and reach USD 4.43 billion by 2031, growing at a CAGR of 7.05% over 2026-2031.

Steady federal appropriations into factory-built housing, rising on-site labor costs, and zoning reforms that legalize higher urban densities together anchor this expansion. In 2025, the Canada Mortgage and Housing Corporation recorded 259,028 housing starts, a 5.6% annual gain, yet supply still trailed population growth in every major metro. The USD 13 billion Build Canada Homes program, announced in Budget 2025, directs volume-purchase contracts to modular producers, effectively guaranteeing a production floor and de-risking new plant investments. Factory assembly shortens build cycles by 40%–50%, a critical benefit in markets where winter weather restricts site activity to eight months. Together, these dynamics keep the Canada manufactured homes market on a durable growth path while creating operating leverage for well-capitalized manufacturers.

Key Report Takeaways

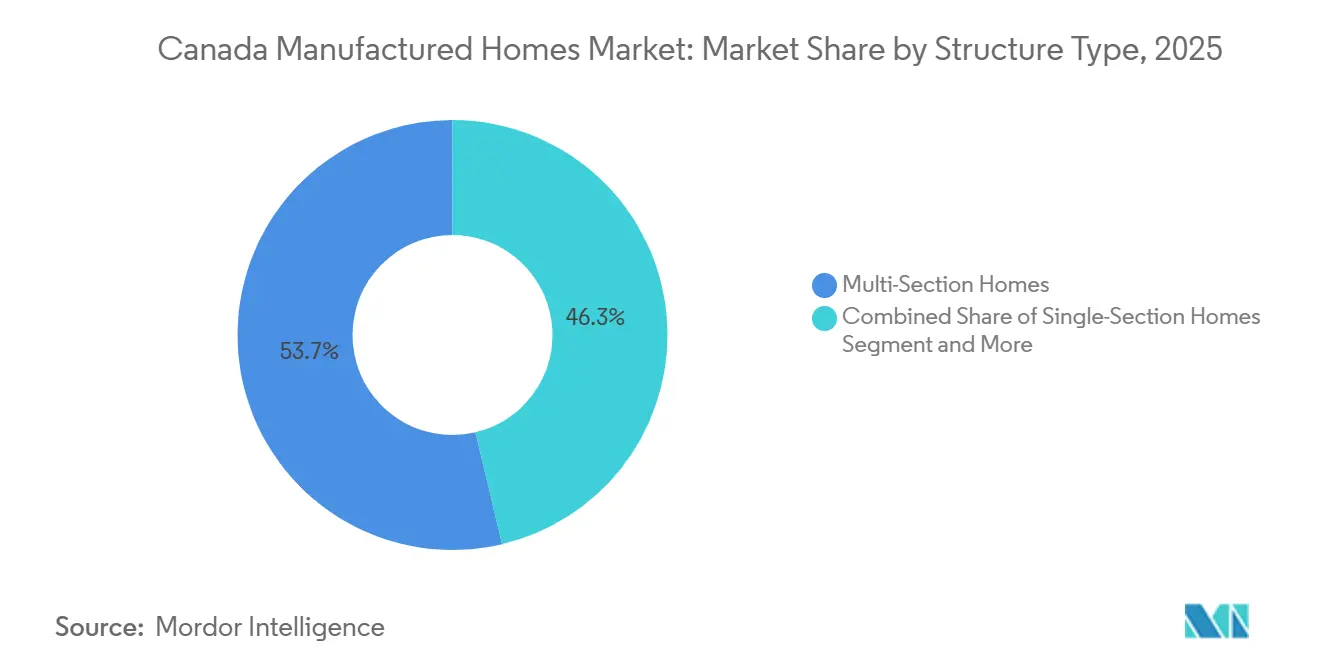

- By structure type, multi-section homes captured 53.7% of the 2025 Canada manufactured homes market share.

- By application, single-family installations held 73.5% of 2025 shipments, while multi-family units are projected to post a 7.59% CAGR through 2031.

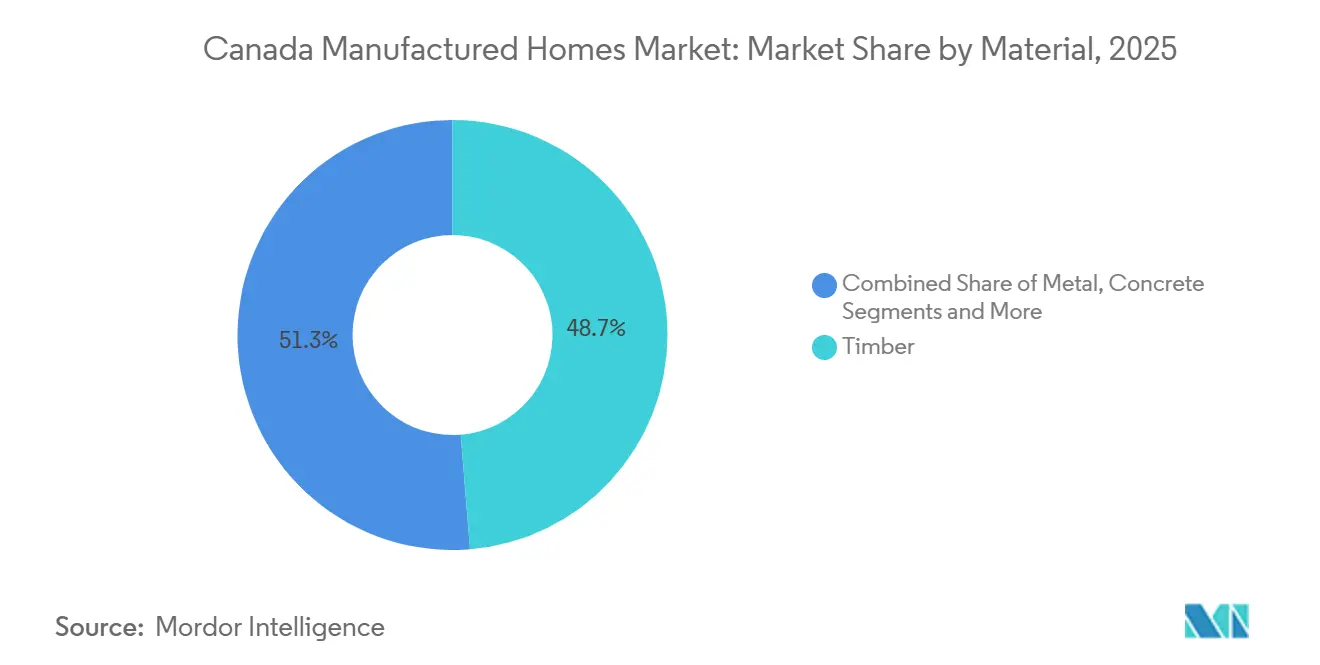

- By material, timber accounted for 48.7% of the 2025 Canada manufactured homes market size, yet concrete-based systems are advancing at a 7.92% CAGR.

- By province, Ontario led with 30.6% of 2025 sales; Alberta is forecast to expand at an 8.03% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Manufactured Homes Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Affordable Housing Shortages Increasing Demand for Manufactured Homes | +2.1% | Ontario, British Columbia, Alberta | Medium term (2–4 years) |

| Rising Construction Costs Supporting the Shift Toward Cost-Efficient Manufactured Homes | +1.8% | British Columbia, Ontario | Short term (≤ 2 years) |

| Shorter Build Timelines Driving Adoption of Off-Site Construction | +1.5% | Alberta, British Columbia | Short term (≤ 2 years) |

| Growing Acceptance in Suburban and Rural Developments | +1.0% | Alberta, Saskatchewan, Atlantic provinces | Medium term (2–4 years) |

| Energy-Efficient Factory Construction Enhancing Long-Term Affordability | +0.9% | British Columbia, Ontario | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Affordable Housing Shortages Increasing Demand For Factory-Built Housing Solutions

CMHC estimated in 2026 that Canada must add 3.5 million units by 2030 to restore 2004 affordability levels[1]Canada Mortgage and Housing Corporation, “Housing Supply Shortfall Update,” cmhc-schl.gc.ca . Conventional pipelines cannot bridge that gap because permitting and skilled-labor bottlenecks limit annual site-built completions. Factory producers are only at one-third of installed capacity, enabling rapid volume expansion without greenfield investment. The federal Build Canada Homes initiative released an RFI in February 2026 that prioritizes modular and panelized suppliers under multi-year offtake contracts, effectively guaranteeing baseline demand. British Columbia and Ottawa committed CAD 810 million in 2025 to deliver 1,100 modular dwellings, anchoring the Digitally Accelerated Standardized Housing program that mandates factory construction. Such commitments create counter-cyclical demand for manufacturers even when resale markets soften.

Rising Construction Costs Supporting Shift Toward Cost-Efficient Manufactured Homes

Statistics Canada recorded a 6.8% year-over-year rise in residential construction costs in Q3 2025[2]Statistics Canada, “Construction Cost Index Q3 2025,” statcan.gc.ca . Skilled-trade wages now top CAD 85 (USD 63) per hour in British Columbia and Ontario, yet factory production cuts on-site labor inputs by up to 35%. October 2025 lumber tariffs increased framing costs by 12%-18%; however, manufacturers hedge with bulk purchasing and forward contracts that small builders cannot match[3]Natural Resources Canada, “Lumber Market Monitor 2025,” nrcan.gc.ca . Champion Home Builders reported USD 352.2 million of inventory in its FY 2026 Q2 filing, buffering near-term price spikes.

Shorter Build Timelines Driving Adoption Of Off-Site Manufactured Housing

Factory schedules compress overall delivery by 40%-50% because site prep and module fabrication occur in parallel, an advantage in provinces with harsh winters that constrain field work to eight-month windows. Alberta’s October 2024 guidance endorses modular housing to accelerate delivery under its affordable-housing strategy. ATCO strengthened capacity by purchasing NRB Modular Solutions for CAD 40 million in 2024, then opened a 122,000 square-foot automated plant in Grimsby, Ontario in 2025. British Columbia requires completion within 120 days for Digitally Accelerated Standardized Housing awards, a deadline unattainable for conventional builds.

Growing Acceptance Of Manufactured Homes In Suburban And Rural Developments

Legislative reforms normalize factory-built dwellings in higher-density suburban lots once reserved for single-detached houses. British Columbia’s Bill 44 (2023) and Bill 25 (2025) mandate that municipalities approve 3-6 units per lot by June 2026, implicitly favoring modular typologies. Alberta’s 2024 guidance urges municipalities to drop zoning barriers and adopt expedited approvals. Premium examples, such as Discovery Dream Homes’ Whistler employee complex, prove that design quality can match site-built standards even in luxury markets. CSA Z240 and A277 certifications supply lenders and buyers with nationally recognized performance benchmarks, widening finance options and lowering perceived risk.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Financing and Mortgage Options Constraining Buyer Access | -1.2% | Nationwide, particularly in rural regions | Medium term (2–4 years) |

| Zoning Restrictions and Local Permitting Challenges Limiting Site Availability | -0.9% | Ontario and Quebec | Long term (≥ 4 years) |

| Transportation and Setup Costs Eroding Overall Affordability | -0.7% | Atlantic provinces and northern territories | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Financing and Mortgage Options Constraining Buyer Adoption

CMHC insurance limits, a 5.25% stress-test floor, and chattel loan premiums of 100-200 basis points reduce the borrowing capacity of median-income households. High-ratio insurance caps at CAD 2 million exclude many modular units in Metro Vancouver and the Greater Toronto Area, while resale manufactured homes remain ineligible for the 30-year amortization extension introduced in 2024. Cavco’s Country Place Acceptance observes that finance scarcity still curbs volume growth despite government incentives.

Zoning Restrictions And Local Permitting Challenges Limiting Site Availability

Municipal bylaws in Ontario and Quebec restrict manufactured homes to designated parks or rural zones, blocking entry into land-rich suburban subdivisions. Although British Columbia’s Bills 44 and 25 override density limits, municipalities may impose design standards that raise site-prep costs. Calgary demands professional-engineer approval for modular projects, while Ontario’s Bills 23 and 109 streamline certain housing types but omit mandates for factory-built homes, sustaining approval uncertainty.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Structure Type: Multi-Section Homes Anchor Volume

Multi-section designs captured 53.7% of the 2025 Canada manufactured homes market share, reflecting consumer appetite for 1,500-plus-square-foot layouts that mirror site-built residences. Manufacturers such as Champion Home Builders reported that multi-section orders formed about 60% of Canadian volume in fiscal 2026, buoyed by financing advantages when the units are fixed to owned land. The segment benefits from higher average selling prices that improve plant utilization and gross margins, reinforcing its primacy in the Canada manufactured homes market.

Other formats—park models, expandable units, and tiny homes—will grow at a 7.71% CAGR to 2031, outpacing single sections. Recreation-oriented developers in resort regions increasingly use park models certified under CSA Z240 to capture seasonal rentals. Edmonton-based Northern Comfort Modular Homes and British Columbia’s Viceroy Homes both added park-model lines in 2025 to tap this upswing. As rural broadband improves, a subset of remote workers is also choosing mobile tiny homes, a micro-niche that keeps the Canada manufactured homes market size diversified across buyer personas.

By Application: Single-Family Dominance Masks Multi-Family Acceleration

Single-family placements accounted for 73.5% of 2025 shipments, anchoring the largest slice of the Canada manufactured homes market size. Detached modular units appeal to suburban buyers seeking fee-simple land ownership without the prolonged disruption of on-site building. However, policy-driven density goals are steering capital toward stacked modules; multi-family projects are forecast to post a 7.59% CAGR through 2031, outpacing all other applications.

Stack Modular’s 3- to 6-story steel-frame platform, already field-tested in Vancouver, can cut development schedules nearly in half, an edge that attracts institutional investors facing construction-interest drag. The USD 500 million Apartment Construction Loan Program, launched in 2025, offers 50-year debt at sub-market rates exclusively for modular multi-family schemes, adding a financial tailwind. These dynamics collectively broaden the demand base within the Canada manufactured homes market.

By Material: Timber Leads, Concrete Gains on Energy Mandates

Timber held 48.7% of the 2025 Canada manufactured homes market share on the back of well-established supply chains and builder familiarity. Interfor’s softwood lumber still underpins wall and roof assemblies despite duty-driven cost spikes, and most plants retain high-throughput saw lines dedicated to SPF framing. Yet cost volatility has nudged producers to hedge by adding alternative-material work cells, ensuring the Canada manufactured homes market remains resilient to commodity swings.

Concrete-centric systems will advance at a 7.92% CAGR through 2031, the speediest clip among materials. Insulated concrete forms and precast sandwich panels deliver sub-1.0 air-changes-per-hour performance that easily clears British Columbia Step Code 4. Quebec’s Lofts de l’Aluminium proved that factory-installed expanded polystyrene cores can hit R-42 walls without bloating budgets. As energy codes tighten, concrete’s low leakage and thermal mass advantages will carve deeper into the Canada manufactured homes market size.

Geography Analysis

Ontario’s 30.6% share in 2025 underscores the province’s concentration of both demand and production assets. The Grimsby Innovation Centre, opened in October 2025, now feeds quick-turn projects across the Greater Toronto Area, helping developers sidestep labor bottlenecks. Streamlined approvals under Bill 109 further shorten cycle times, yet lingering municipal resistance still corrals many manufactured homes into edge-city zones, leaving untapped potential in high-priced inner suburbs.

British Columbia enforces progressive zoning that compels every municipality to allow three to six units on formerly single-family lots by June 2026. The province’s USD 600 million modular procurement package already earmarks 400 stacked units, a pipeline that lifts plant utilization from one-third to nearer one-half capacity. British Columbia manufacturers also tout 43% lower carbon emissions and up to 70% less construction waste than site-built comparables, a positioning that resonates with environmentally minded local governments.

Alberta represents the velocity story, heading for an 8.03% CAGR through 2031. The 230,000-square-foot Lethbridge plant acquired by ATCO in 2023 anchors Western Canadian production, supplying both prairie metros and resource-sector camps. In Atlantic Canada and the territories, sparse populations keep absolute volumes low, yet logistical advantages—single-trip delivery and rapid set-up in harsh climates—continue to justify premium freight rates. Collectively, these regional currents confirm that the Canada manufactured homes market is neither monolithic nor static, but a mosaic of local drivers moving in the same structural direction.

Competitive Landscape

The Canada manufactured homes market is moderately fragmented, with the top five players controlling just under half of national shipments. ATCO Structures, Cavco Industries, and Champion Home Builders each operate multi-province footprints, while region-specific firms such as Viceroy Homes and Stack Modular focus on niche products or geographies. Cross-border players benefit from U.S. scale economies that lower material input costs, a structural edge over single-plant Canadian peers.

Strategic moves since 2024 center on vertical integration and capacity consolidation. ATCO spent USD 29.6 million on NRB Modular Solutions and retooled the Grimsby site into an automated hub capable of 1,000-plus units annually. Cavco, via CountryPlace Acceptance, extends credit directly to buyers, softening the financing bottleneck that constrains the broader Canada manufactured homes industry. Champion ramped inventories to USD 352.2 million in fiscal 2026, cushioning supply shocks and keeping lead times stable.

Innovation is moving from isolated pilots to factory-wide upgrades. Stack Modular’s BIM-driven steel platform supports up to six stories, opening urban infill verticals where wood modules fall short of fire-rating requirements. CABN pursues accessory dwelling units optimized for net-zero energy, targeting the segment unlocked by zoning reforms in British Columbia and, soon, Ontario. Federal grants under the USD 50 million Homebuilding Technology and Innovation Fund reward such process digitization, setting a new baseline that late adopters must match.

Canada Manufactured Homes Industry Leaders

Cavco Industries

Champion Home Builders

NRB Modular Solutions

Alta-Fab Structures

Viceroy Homes

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The Government of Canada issued an RFI for modern methods of construction under the Build Canada Homes initiative, seeking turnkey modular supply agreements.

- November 2025: Cavco Industries posted Q1 FY 2026 revenue of USD 476.2 million, with 5,176 homes sold, a 6.2% volume gain.

- November 2025: Champion Home Builders reported Q3 FY 2026 net sales of USD 456.4 million and 1,577 homes sold, including 196 units in Canada.

- October 2025: ATCO Structures opened Phase 1 of the USD 89 million Grimsby Innovation Centre, adding 122,000 square feet of automated capacity.

Canada Manufactured Homes Market Report Scope

By Structure Type

| Single-Section Homes |

| Multi-Section Homes |

| Other Types |

By Application

| Single Family |

| Multi Family |

By Material

| Timber |

| Metal |

| Concrete |

| Others |

By Province

| Ontario |

| Quebec |

| British Columbia |

| Alberta |

| Rest of Canada |

| By Structure Type | Single-Section Homes |

| Multi-Section Homes | |

| Other Types | |

| By Application | Single Family |

| Multi Family | |

| By Material | Timber |

| Metal | |

| Concrete | |

| Others | |

| By Province | Ontario |

| Quebec | |

| British Columbia | |

| Alberta | |

| Rest of Canada |

Key Questions Answered in the Report

How large is the Canada manufactured homes market today?

The Canada manufactured homes market size reached USD 3.15 billion in 2026 and is on track for USD 4.43 billion by 2031, underpinned by a 7.05% CAGR.

Which structure type sells the most units?

Multi-section homes lead with 53.7% of 2025 shipments, thanks to spacious layouts that rival site-built houses.

Which province is growing fastest for manufactured homes?

Alberta is projected to register an 8.03% CAGR through 2031, outpacing all other provinces as policy shifts accelerate modular adoption.

What materials are gaining traction beyond timber?

Concrete-based panels and insulated concrete forms are advancing at a 7.92% CAGR because they simplify compliance with new energy codes.

How do factory-built homes address Canada’s affordability gap?

Off-site production cuts labor costs, shortens build cycles by up to half, and qualifies for federal financing programs that lower buyer carrying costs.

Page last updated on: