Financial Services and Investment Intelligence

29th JulyWealth Management Intelligence for the Middle East

4 Min Read

The Canada Mortgage/Loan Brokers Market Report is Segmented by Loan Type (Residential Mortgages, Commercial Mortgages, Home Equity Lines of Credit, and More), Borrower Profile (First-Time Home Buyers, Repeat/Move-Up Buyers, and More), Distribution Channel (Traditional Face-To-Face, Online/Digital-Only, Hybrid), and Geography (Canada). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

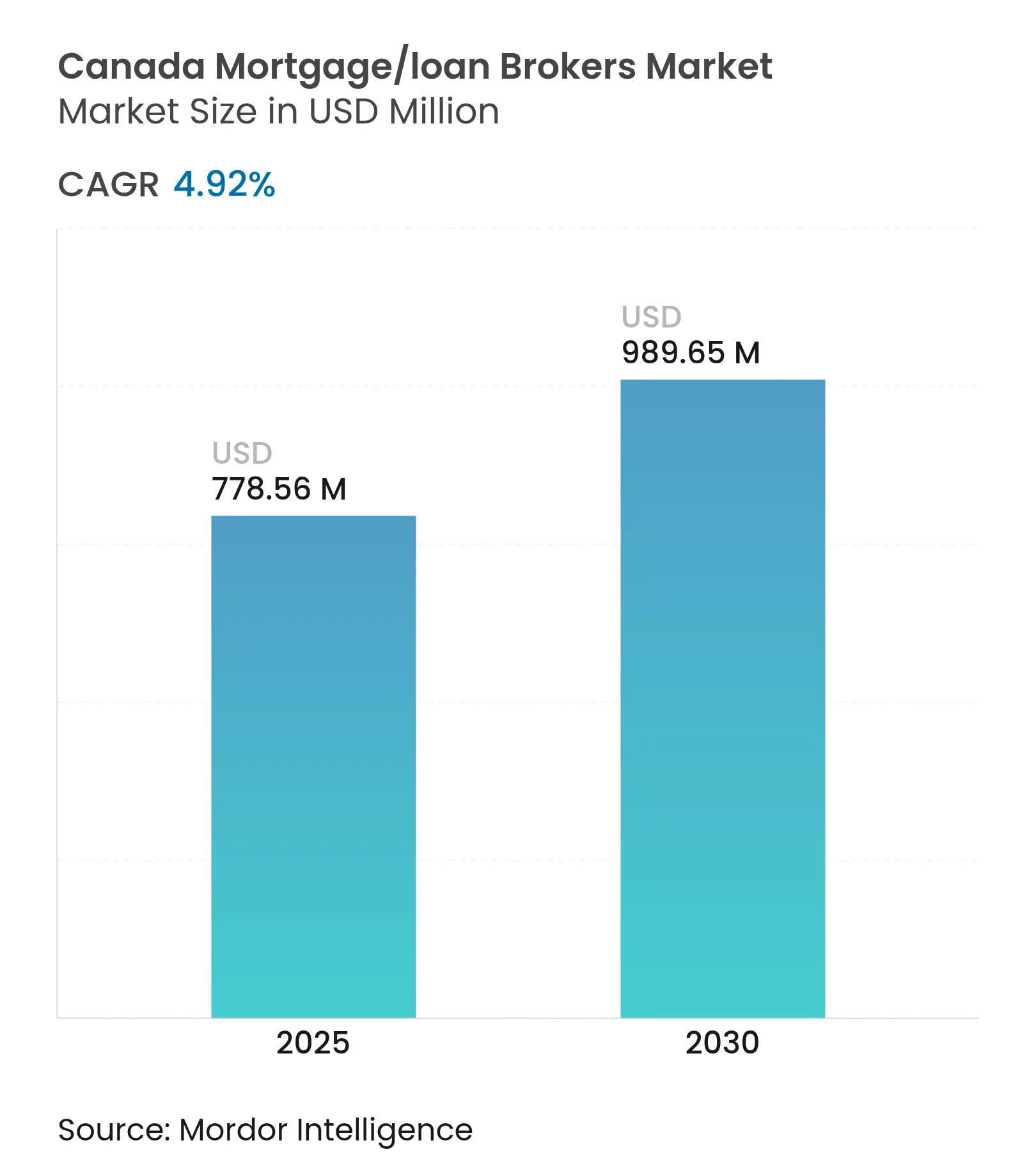

| Market Size (2025) | USD 778.56 Million |

| Market Size (2030) | USD 989.65 Million |

| Growth Rate (2025 - 2030) | 4.92 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Canada Mortgage/loan Brokers Market size reached USD 778.56 million in 2025 and is forecast to advance at a 4.92% CAGR to USD 989.65 million by 2030. Escalating renewal volumes, chronic housing supply deficits, and accelerating immigration underpin sustained growth even as borrowers confront higher contract rates[1]Centris, “Residential Real-Estate Statistics Q1 2025,” centris.ca. Broker relevance deepens because 60% of mortgages will reset by 2026, exposing 1.2 million households to payment shocks that demand refinancing advice. Competitive intensity among prime and alternative lenders compresses rate spreads and stimulates product innovation that flows largely through broker channels. Federal incentives such as the First Home Savings Account (FHSA) amplify first-time buyer activity, adding incremental demand that brokers are uniquely positioned to serve.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising

housing demand amid chronic supply shortage

Rising

housing demand amid chronic supply shortage

| +1.8% | National, most acute in Toronto, Vancouver, Montreal | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:+1.8% |

Geographic

Relevance

:

National,

most acute in Toronto, Vancouver, Montreal

|

Impact

Timeline

:

Long

term (≥ 4 years)

|

Sustained

rate competition among prime & alt-A lenders

Sustained

rate competition among prime & alt-A lenders

| +1.2% | National, with regional variations in alternative lending penetration | Medium term (2-4 years) | |||

Federal

incentives for first-time buyers

Federal

incentives for first-time buyers

| +0.9% | National, with higher uptake in high-cost markets | Short term (≤ 2 years) | |||

Expansion

of alternative-lending channels boosts broker relevance

Expansion

of alternative-lending channels boosts broker relevance

| +1.1% | National, concentrated in Ontario, BC, Alberta | Medium term (2-4 years) | |||

Pending

open-banking rollout enabling rapid, data-driven approvals

Pending

open-banking rollout enabling rapid, data-driven approvals

| +0.7% | National, with early adoption in urban centers | Medium term (2-4 years) | |||

Accelerating

immigration inflows requiring multicultural mortgage advice

Accelerating

immigration inflows requiring multicultural mortgage advice

| +0.6% | National, concentrated in Toronto, Vancouver, Montreal gateway cities | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Housing Demand Amid Chronic Supply Shortage

National active listings fell 4% year-over-year to 34,479 units in Q1 2025, positioning inventory 29% below the historical norm and compressing days-on-market to 4.6 months. Quebec recorded 24,070 home sales in the same quarter, up 14%, while time-to-sell in Quebec City touched a 25-year low of 2.7 months. Toronto and Vancouver continue to exhibit multiple-offer scenarios on roughly 40% of transactions, reinforcing the need for broker-orchestrated pre-approvals. Supply-demand imbalances are unlikely to ease quickly as CMHC estimates a deficit of 3.5 million units by 2030[2]Canada Mortgage and Housing Corporation, “Housing Supply Gap 2030,” cmhc-schl.gc.ca. These structural constraints anchor origination momentum by compelling households to secure financing swiftly in competitive markets.

Sustained Rate Competition Among Prime & Alt-A Lenders

The Bank of Canada’s policy rate decline from 5.0% to 3.25% by December 2024, unleashed aggressive mortgage repricing, with brokers sourcing rates 10–25 basis points below posted bank offers. Alternative lenders are capturing share through broker networks, as evidenced by Fairstone Bank’s merger with Home Trust, which formed a USD 15 billion loan book distributed largely via brokers. MCAN Financial originated USD 637.1 million through brokers in Q2 2025, scaling uninsured securitizations to preserve pricing flexibility[3]MCAN Financial Group, “Q2 2025 Performance Highlights,” mcanfinancial.com. Product innovation is visible in adjustable-rate insured mortgages and construction financing marketed explicitly to broker partners. The competitive environment narrows lender margins yet enlarges consumer choice, cementing brokers as vital intermediaries.

Federal Incentives for First-Time Buyers

Thirty-year amortizations on insured mortgages launched in December 2024 shave monthly payments by roughly 12%, enabling more borrowers to satisfy OSFI’s stress test. The First-Time Home Buyer Incentive now pairs with raised Home Buyers’ Plan withdrawal limits of USD 60,000, while the FHSA permits USD 8,000 annual tax-deductible contributions[4]Canada Revenue Agency, “First Home Savings Account Details,” cra-arc.gc.ca. Centris polling shows 58% of Quebec first-time buyers intend to deploy FHSA funds in 2025, up from 46% in 2023. Higher insured caps of USD 1.5 million for single units and USD 2.0 million for multi-family, widen the pipeline of transactions eligible for mortgage insurance. These policy levers stimulate pipeline volume that disproportionately flows through brokers skilled in incentive navigation.

Expansion of Alternative-Lending Channels Boosts Broker Relevance

Non-bank institutions now originate more than 20% of new mortgages, driven by Mortgage Investment Corporations, credit unions, and fintech lenders. The proposed Kawartha and Libro Credit Union merger will create a USD 11 billion regional powerhouse with expanded broker partnerships. Fintech aggregators such as BorrowWell harness open-banking APIs to deliver under-one-minute credit decisions that slot seamlessly into broker workflows. As tier-one banks tighten debt-service ratios, alternative channels capture self-employed borrowers and new immigrants who require flexible underwriting. Brokers monetize this complexity by aligning borrower risk profiles with the optimal source of capital.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Stringent AML / KYC compliance burdens

Stringent AML / KYC compliance burdens

| -0.7% | Global, with emerging markets most affected | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-0.7%

|

Geographic Relevance

:

Global, with emerging markets most affected

|

Impact Timeline

:

Short term (≤ 2 years)

|

Geopolitical trade tensions & sanctions

Geopolitical trade tensions & sanctions

| -0.5% | Global, concentrated in conflict-affected regions | Medium term (2-4 years) | |||

Shrinking correspondent-banking network in frontier

markets

Shrinking correspondent-banking network in frontier

markets

| -0.4% | Africa, Latin America, Central Asia frontier markets | Long term (≥ 4 years) | |||

Rising trade-credit-insurance premiums

Rising trade-credit-insurance premiums

| -0.3% | Global, with higher impact in high-risk regions | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Stricter OSFI Stress-Test Limits Borrowing Capacity

Loan-to-income caps at 4.5× effective January 2025 restrict high-ratio mortgages, clipping purchasing power for moderate-income households in expensive markets. The guidelines require lenders to collect enhanced climate-risk disclosures on collateral, raising compliance costs that may be passed to borrowers. Brokers mitigate these pressures by steering clients toward extended amortization insured products and alternative lenders with more flexible ratios. Nevertheless, the new cap could depress approval rates by 8–10 percentage points in Vancouver and Toronto for first-time buyers earning below the median income. Over time, elevated equity positions among repeat buyers partly offset the tightening, but net origination headwinds persist.

Rising Interest-Rate Environment Dampens Origination Volumes

Although policy rates eased in 2024, average 5-year fixed rates still hover near 4%, markedly above the sub-1% lows of 2021, raising monthly payments 30–50% at renewal. CMHC projects 1.2 million mortgages will renew by 2026, testing household budgets as inflation lingers above 2%. Prospective buyers delay discretionary purchases, awaiting deeper cuts, reducing near-term demand for speculative investment properties. Brokers specializing in debt consolidation and extended amortization refinancing pick up business, but overall origination volumes remain sensitive to macro-outlook shifts. Regional economies tied to oil and gas demonstrate amplified elasticity, with Alberta approvals falling 12% in 2024 when benchmark rates spiked.

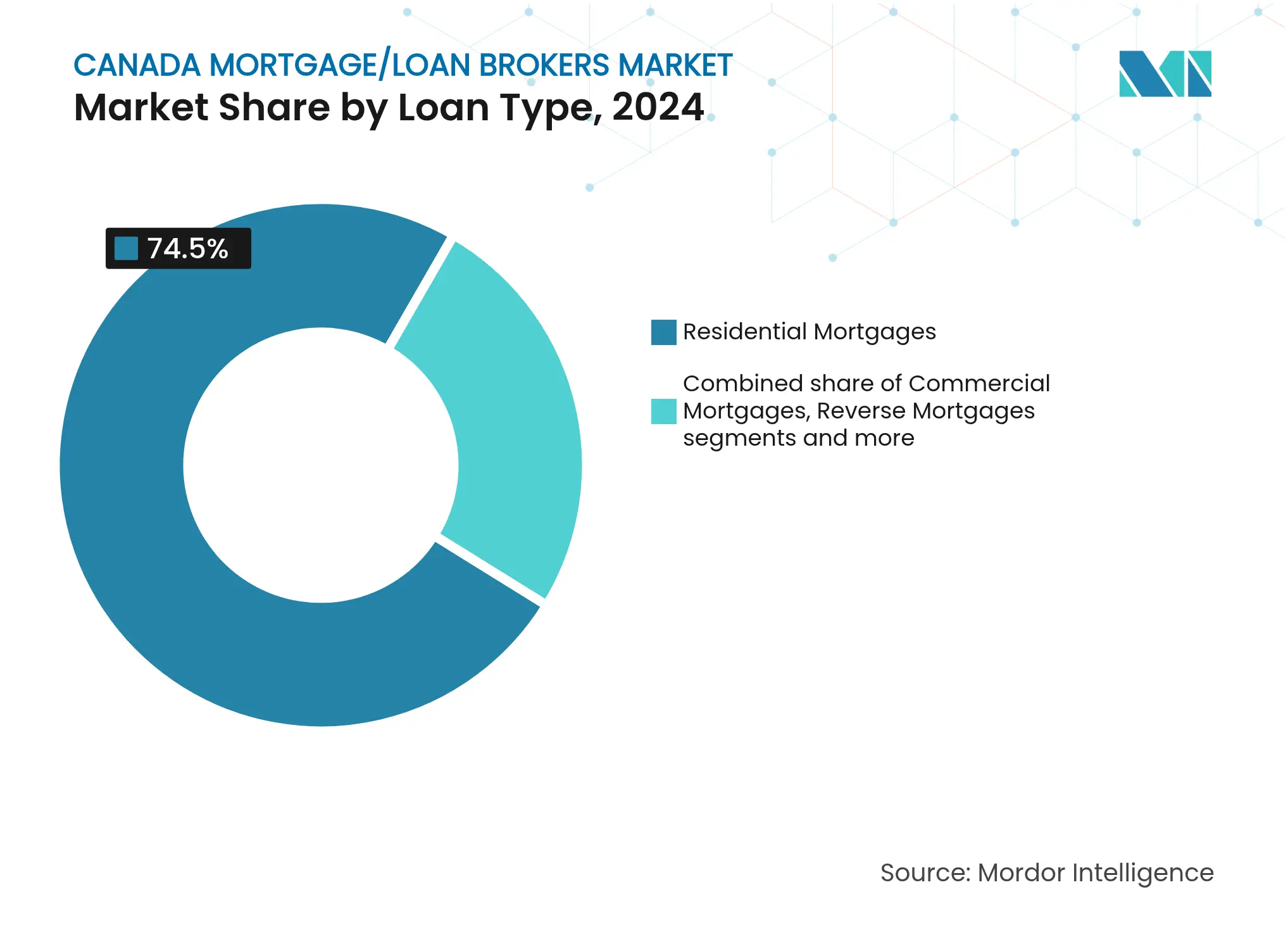

By Loan Type: Residential Mortgages Drive Market Leadership

Residential mortgages held 74.5% of the Canada mortgage/loan brokers market share in 2024, underscoring the pivotal role traditional home-purchase financing plays in origination flows. This dominance is rooted in CMHC-backed insurance schemes and stable borrower demand that together generate predictable underwriting pipelines. Reverse mortgages, though niche at 3% of volume, are growing at a 5.63% CAGR as homeowners aged 60 plus unlock equity without relocation. The Canada mortgage/loan brokers market size for residential products is projected to rise by USD 158 million between 2025 and 2030, reflecting resilient demand despite affordability headwinds. Product diversification continues as Equitable Bank’s Laneway House Mortgage lends up to 95% loan-to-cost on accessory dwelling construction, expanding brokerable opportunities.

Commercial mortgages, HELOCs, and construction loans collectively capture the remaining share. Growth in purpose-built rental financing accelerates following GST removal on new units, a policy that improves developer economics and broadens broker mandates. Home Equity Line balancing rules that cap combined mortgage-HELOC exposure at 65% of property value constrain HELOC expansion but elevate second-lien origination handled by specialty lenders. Brokers straddle prime and subprime pools to originate bespoke bridge loans for renovation and new-build projects, often tapping MIC capital. As housing densification intensifies, product innovation is likely to sustain broker value beyond standard amortizing mortgages.

Note: Segment shares of all individual segments available upon report purchase

By Borrower Profile: Repeat Buyers Dominate While New Immigrants Show Strongest Growth

Repeat and move-up buyers accounted for 46.8% of the Canada mortgage/loan brokers market size in 2024, benefiting from accumulated equity that smooths stress-test hurdles. Work-from-home reversals catalyze relocation from exurban to urban cores, keeping move-up transactions brisk in Toronto and Vancouver. First-time buyers gained ground through enhanced FHSA and 30-year insured amortizations, yet still face down-payment challenges in million-dollar markets. Investors confront heightened capital-gains inclusion rates, now 66.67%, compressing after-tax returns and chilling speculative demand. Brokers offset investor softness by pivoting to debt-consolidation refinances for rate-shocked households.

New immigrants represent the fastest-growing borrower segment at 5.12% CAGR, propelled by 485,000 permanent residents expected annually through 2026. Limited Canadian credit files and non-standard income verification propel these borrowers toward broker-facilitated alternative lending. Self-employed professionals, another broker mainstay, continue to leverage stated-income products and bank-statement programs available primarily through MICs. Seniors increasingly tap reverse mortgages to supplement pensions, with origination volumes up 37% year-over-year according to OSFI filings. Borrower heterogeneity underscores brokers’ consultative advantage in aligning loan structures with complex financial profiles.

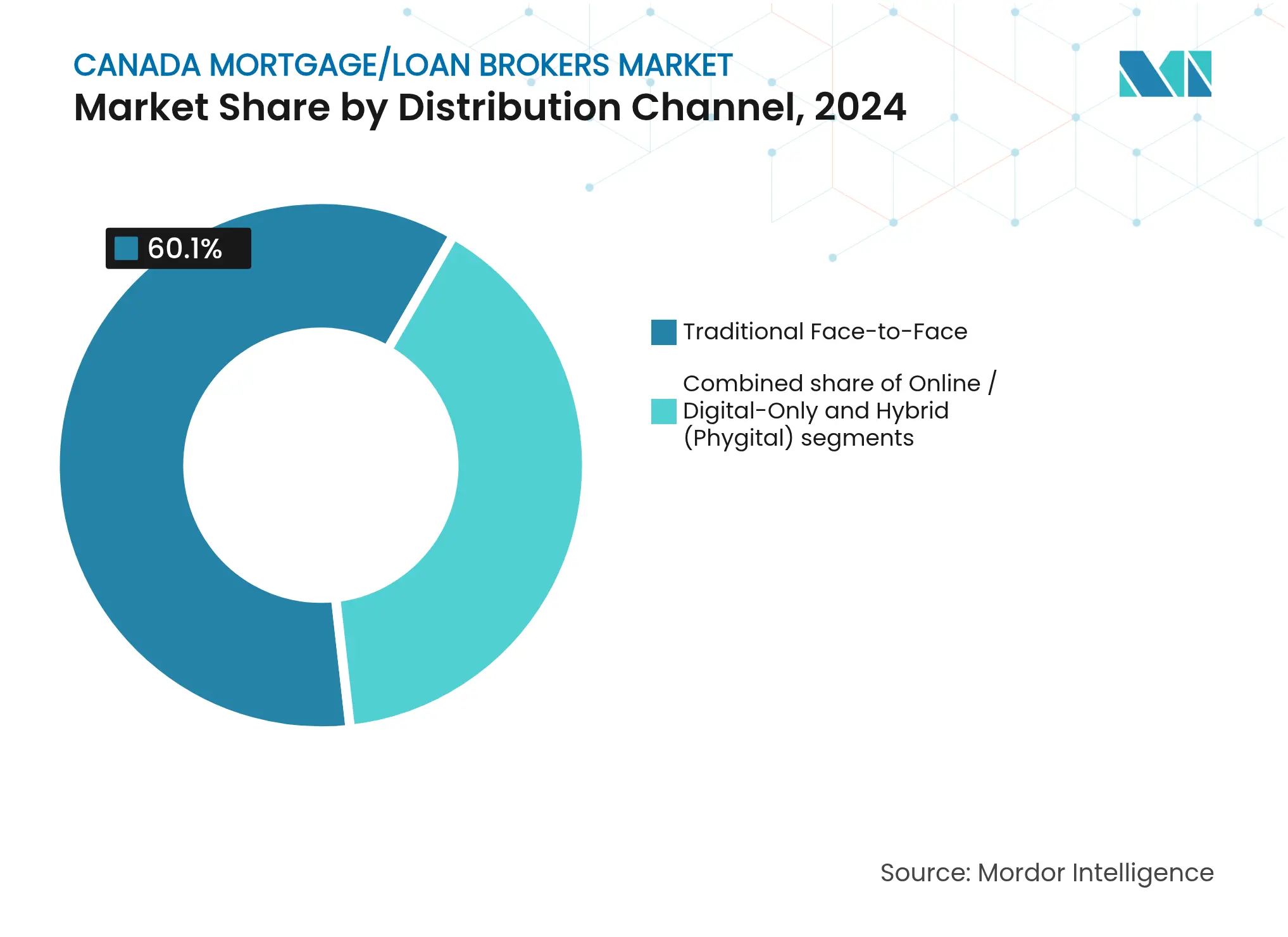

By Distribution Channel: Digital Transformation Accelerates Despite Traditional Dominance

Traditional in-person brokerage captured 60.1% of the Canada mortgage/loan brokers market size in 2024, favored for high-touch guidance through multifaceted regulations. Referral ecosystems, real-estate agents, accountants, and lawyers continue to funnel retail leads into established brick-and-mortar offices. Yet hybrid models integrating virtual document collection with on-site consultation help brokers cut cycle times by 15–20% while retaining personal rapport. Compliance obligations introduced by FINTRAC in October 2024 spurred investments in secure e-signature and KYC tools that elevate client convenience and audit readiness.

Digital-only channels expand at 6.13% CAGR, anchored by fintech platforms delivering instant pre-qualifications and AI-driven rate comparisons. Consumers prize 24/7 application access and transparent fee structures, traits increasingly replicated by top broker franchises to blunt pure-play entrants. Dominion Lending Centres’ 2025 rollout of a fully integrated borrower portal with automated document recognition exemplifies incumbent adaptation. Despite digital momentum, complex cases, self-employed, multi-unit, or private lending still migrate to experienced brokers for manual structuring, preserving traditional channel primacy in aggregated volume.

Note: Segment shares of all individual segments available upon report purchase

Ontario and British Columbia together generate more than 55% of Canada's mortgage/loan brokers market activity, propelled by high-priced urban centers where alternative lending thrives amid affordability challenges. Toronto’s average detached home price exceeded USD 1.0 million in 2025, necessitating creative financing structures that brokers are best suited to arrange. Vancouver mirrors this dynamic, with 40% of brokered deals involving non-conforming products and extended amortizations.

Quebec maintains a distinct regulatory backdrop under the Autorité des marchés financiers (AMF), yet logged 24,070 transactions in Q1 2025, up 14% year-over-year, spotlighting robust Francophone broker networks. The province’s cultural affinity for professional intermediaries drives higher broker penetration rates relative to other regions. Atlantic Canada gains prominence as interprovincial migration lifts 2025 sales 11% in Nova Scotia and 9% in New Brunswick, putting pressure on limited inventory but opening fresh broker revenue pools.

Alberta and Saskatchewan exhibit cyclical volatility aligned to commodity markets; brokers in Calgary report 12% fewer approvals in 2024 amid oil-price softness before a rebound sparked by WTI gains in mid-2025. Prairie brokers specialize in self-employed and variable-income underwriting that conventional banks view cautiously. National FINTRAC harmonization mandates enacted in 2024 have created a baseline compliance framework across provinces, facilitating multi-province brokerage expansion. Yet provincial licensing persists, demanding localized oversight that entrenches established regional players. Geographic diversification strategies help large networks buffer regional downturns while boutique brokers rely on hyper-local expertise to sustain share.

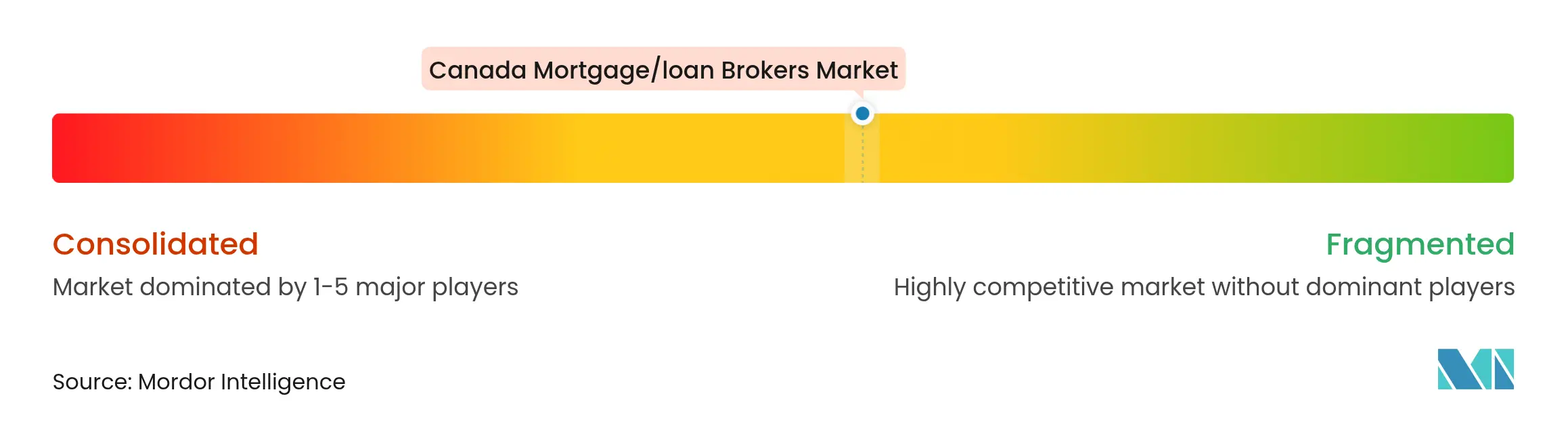

Market Concentration

The Canada Mortgage/loan Brokers Market hosts more than 15,000 licensed professionals, yet volume is disproportionately concentrated among national networks such as Dominion Lending Centres, Mortgage Alliance, and M3 Group. DLC’s 1,500-plus brokers and 50-lender panel confer economies of scale in rate negotiation and technology investments. Mortgage Alliance leverages parent M3 Group’s centralized underwriting engine to shave turnaround times for prime and alt-A files.

Consolidation pressures mount as nearly 47% of brokers closed fewer than 12 deals in 2023, prompting predictions that one-third could exit by 2027 without productivity gains. Technology emerges as a decisive differentiator; platforms like Ownwell automate post-close retention, lifting cross-sell revenue per client by 18%. Compliance rigor following FINTRAC’s 2024 rule change further strains small shops, steering them toward franchise affiliation for shared infrastructure.

Product specialization also sets leaders apart. Equitable Bank’s broker-exclusive Laneway House Mortgage illustrates lenders’ reliance on brokers to penetrate novel segments quickly. Alternative lender expansion post-Fairstone, Home Trust merger funnels considerable flow to brokers who master stated-income and bruised-credit guidelines. The competitive field, therefore, balances scale economies, niche expertise, and regulatory competence in determining share trajectory through 2030.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities & Future Outlook

A mortgage broker acts as a middleman for people or businesses and manages the mortgage loan application process. In essence, they form relationships between mortgage lenders and borrowers without investing any of their own money.

The Canada Mortgage/Loan Brokers Market Is Segmented By Enterprise Size (Large, Small, And Medium-Sized), By Application (Home Loans, Commercial And Industrial Loans, Vehicle Loans, Loans To Governments, And Others), And By End-User (Businesses And Individuals). The Market Sizes And Forecasts Are Provided In Terms Of Value (USD) For All The Above Segments.

Wealth Management Intelligence for the Middle East

4 Min Read

Driving Growth in the Embedded Insurance Market

4 Min Read

Feasibility Analysis for FBO Services in East Africa

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.