Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 7.10 Billion |

| Market Size (2026) | USD 7.45 Billion |

| Market Size (2031) | USD 9.23 Billion |

| Growth Rate (2026 - 2031) | 4.38% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Kitchen Appliances Market Analysis by Mordor Intelligence

The Canada kitchen appliances market size reached USD 7.45 billion in 2026 and is forecast to climb to USD 9.23 billion by 2031 at a 4.38% CAGR, following USD 7.1 billion in 2025 as the sector sustained steady product refresh cycles and premium feature adoption. Large kitchen appliances continued to anchor revenue, while small kitchen appliances advanced faster on the back of countertop innovations and flexible price points that align with household budgeting dynamics in a cautious spending environment. Policy momentum shaped design and purchasing choices as federal minimum energy performance standards tightened and provinces advanced repairability and electrification frameworks that reset the competitive baseline for durability, software support, and integration capability. Housing activity supported steady unit placements in multi-residential formats even as single-family starts slowed in higher-cost metros, which created mixed conditions across provinces and product tiers. Digital channels expanded reach through omnichannel fulfillment and direct engagement, reinforcing service differentiation and accelerated replenishment cycles as more products connected to energy and home platforms.

Key Report Takeaways

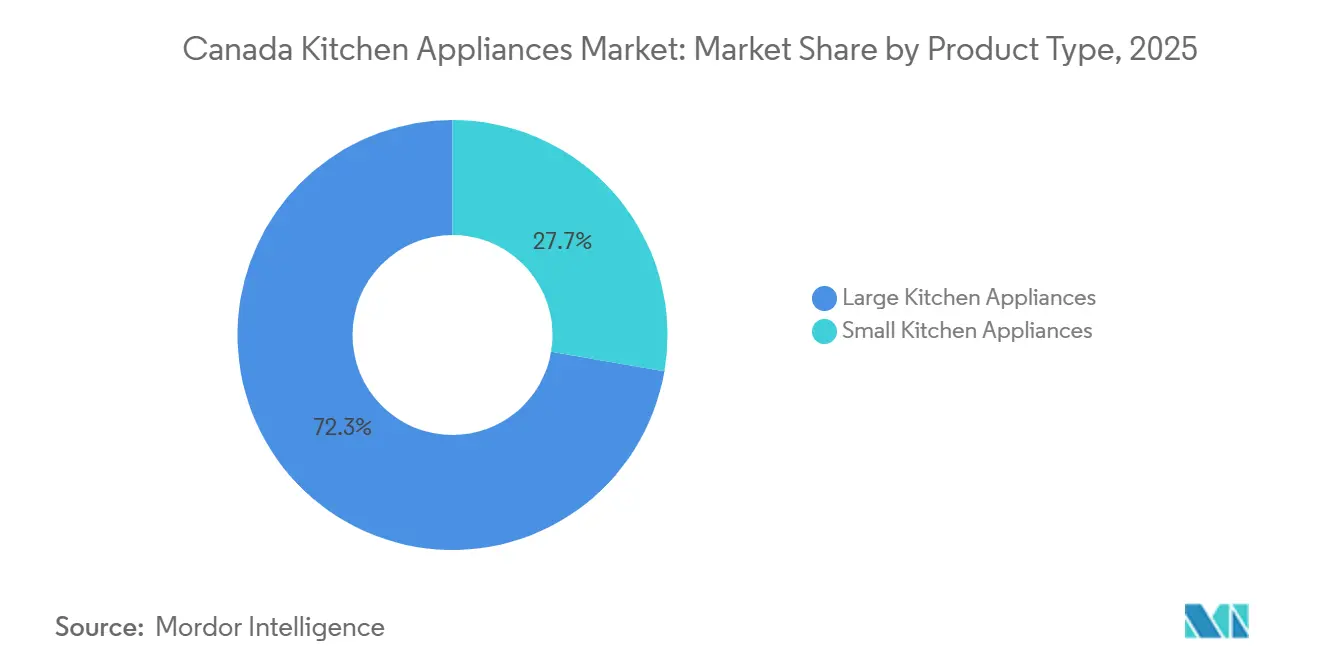

- By product, large kitchen appliances led with 72.31% of the Canada kitchen appliances market share in 2025, while the Canada kitchen appliances market size for small kitchen appliances is projected to expand at a 4.45% CAGR between 2026 and 2031.

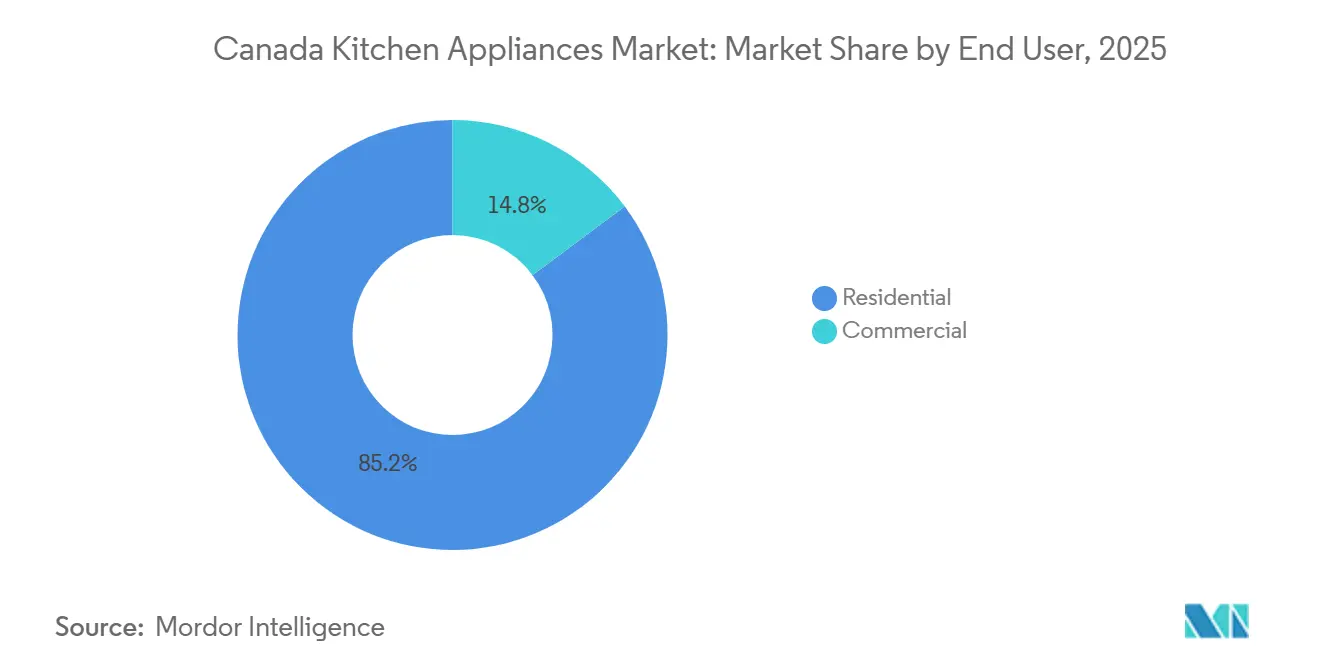

- By end user, the residential segment accounted for 85.21% of the Canada kitchen appliances market share in 2025, while the Canada kitchen appliances market size for commercial buyers is projected to grow at a 4.71% CAGR through 2031.

- By distribution channel, multi-brand stores held 39.95% of the Canada kitchen appliances market share in 2025, while the Canada kitchen appliances market size for online channels is projected to advance at a 4.98% CAGR from 2026 to 2031.

- By geography, Ontario captured 38.71% of the Canada kitchen appliances market share in 2025, while the Canada kitchen appliances market size for Alberta is forecast to expand at a 5.21% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Kitchen Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver / Restraint (as applicable in title case) | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal MEPS tightening and ENERGY STAR alignment pipeline | +0.8% | National, with Ontario, Quebec, British Columbia most affected | Long term (≥ 4 years) |

| New-build and rental housing pipeline sustaining appliance demand | +1.2% | National, early gains in Calgary, Edmonton, Montreal, Ottawa-Gatineau | Medium term (2-4 years) |

| Smart/connected kitchens adoption and utility-backed efficiency upgrades | +0.9% | Ontario, Quebec, British Columbia | Medium term (2-4 years) |

| E-commerce scale and click-and-collect expanding appliance access | +0.7% | National, urban cores and improving rural logistics | Short term (≤ 2 years) |

| Québec repairability and durability mandates reshaping products/services | +0.6% | Quebec core, national spillover | Long term (≥ 4 years) |

| Provincial EPR fees enabling trade-in/refurbishment and circular flows | +0.5% | National, strongest in Ontario, Quebec, British Columbia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Federal MEPS Tightening and ENERGY STAR Alignment Pipeline

Amendment 18 to Canada’s Energy Efficiency Regulations was promulgated in May 2025, mandating minimum energy performance standards across a wide set of end uses and projecting USD 1.7 billion in annual consumer energy savings by 2030 while avoiding 1.6 million tonnes of carbon emissions each year, which raises the technical floor for compressors, motors, and control systems in appliances sold nationwide. Policymakers intend to maintain harmonization with U.S. Department of Energy rulemakings through ongoing consultations for Amendment 19 in 2026, while preserving room for tighter measures calibrated to Canada’s colder climate and emissions targets. Civil and criminal penalties under the proposed Energy Efficiency Act amendments would increase, which strengthens enforcement and reduces the commercial viability of low-efficiency models in the Canada kitchen appliances market. ENERGY STAR certification remains a signal of quality and efficiency for buyers and channel partners, with leading OEMs expanding certified portfolios to align with program recognition and utility incentives. This compliance trajectory pressures product roadmaps toward higher-efficiency platforms such as induction cooking and variable-speed refrigeration, magnifying the role of digital controls and remote updates in post-purchase performance management within the Canada kitchen appliances market.

New-build and Rental Housing Pipeline Sustaining Appliance Demand

Canada recorded 259,028 housing starts in 2025, up 5.6% from 2024 and among one of the highest annual totals on record, with rental housing starts accounting for more than half of urban starts and supporting baseline placements of builder-grade and multi-unit retrofit appliances[1]Media Relations, “Housing starts up 5.6% in 2025 from 2024,” Canada Mortgage and Housing Corporation, cmhc-schl.gc.ca. Calgary and Edmonton set record annual starts, while Montreal surged 58% and Ottawa-Gatineau rose 12%, even as Toronto and Vancouver softened under higher construction costs and weaker condominium demand. December 2025 activity spiked to the highest December on record for large centers, though momentum faded late in the year, placing the market on a weaker footing heading into 2026 within the Canadian kitchen appliances market. The February 2026 outlook from CMHC indicates a near-term decline in new home construction through 2028, with Ontario and British Columbia below ten-year averages while the Prairies and Quebec hold above historical norms, which creates uneven demand by province and product tier. Urban rental strength sustains shipments of ranges, refrigerators, and dishwashers into multi-unit projects even as homeowners start in major centers sit well below historical peaks, emphasizing value-focused SKUs in the Canada kitchen appliances market. As vacancy rates rise and rent growth moderates in cities adding rental supply, replacement cycles and amenity upgrades in existing buildings become an important buffer for the Canada kitchen appliances market.

Smart/Connected Kitchens Adoption and Utility-Backed Efficiency Upgrades

Ontario’s Peak Perks program has enrolled large volumes of households and funds thermostat-driven load management, which aligns with growing adoption of connected devices that enable time-of-use optimization and demand-response participation in the Canada kitchen appliances market[2]Media Relations, “Housing Market Outlook 2026,” Canada Mortgage and Housing Corporation, cmhc-schl.gc.ca . Manufacturers are integrating connectivity and AI into appliances so that refrigerators, ranges, and laundry pairs can orchestrate usage and respond to utility signals, a shift reinforced by ENERGY STAR recognition and Matter interoperability rollouts from leading OEMs. British Columbia communities representing a significant share of provincial housing starts adopted the Zero Carbon Step Code effective January 2025, which catalyzes electrification and raises the importance of devices that pair efficient hardware with smart control features. Provincial retrofit programs in British Columbia complement these codes with incentives for multi-unit residential building upgrades that favor connected equipment and integrated controls, thereby creating a supportive backdrop for smart-ready SKUs in the Canada kitchen appliances market. Leading brands are now delivering unified software experiences, multi-year update commitments, and security frameworks across connected appliances, which anchors lifetime value beyond the initial unit sale. Over time, residential demand response and virtual power plant models increase the utility of connected appliances as controllable assets, positioning the Canada kitchen appliances market to benefit from incentives that reward flexible load.

E-Commerce Scale and Click-and-Collect Expanding Appliance Access

E-commerce accounted for 6.1% of all retail sales in Canada in December 2024, with retail e-commerce sales peaking near USD 3.19 billion that month, which underpins channel growth for appliances as shoppers navigate high-consideration purchases with richer content and transparent comparisons. November 2025 retail data show electronics and appliances retailers posting CAD 1.84 billion in current-dollar sales, while overall seasonally adjusted e-commerce represented 5.7% of total retail trade that month within the broader consumer backdrop[3]Media Relations, “Retail trade, November 2025,” Statistics Canada, statcan.gc.ca . Omnichannel players such as Canadian Appliance Source scaled from digital roots to over 40 showrooms with same-day or next-day delivery in select metros, which tightens post-purchase service loops and elevates delivery experience expectations in the Canada kitchen appliances market. Retailers and brands are applying targeted marketing and augmented visualization to lower friction for large-ticket decisions while offering flexible finance and installation options that increase conversion. Major brands continue to invest in owned retail experiences and service footprints to complement marketplace reach, which strengthens discovery and attachment opportunities across premium and mainstream tiers in the Canada kitchen appliances market. Digital scale and fulfillment precision are now part of competitive strategy in appliances, influencing assortment design, packaging, reverse logistics, and post-sale software engagement in the Canada kitchen appliances market.

Restraints Impact Analysis*

| Driver / Restraint (as applicable in title case) | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mature penetration and lengthening replacement cycles for core appliances | -0.6% | National, acute in Ontario and British Columbia | Long term (≥ 4 years) |

| Slowing housing starts/affordability headwinds dampening big-ticket buys | -0.9% | Ontario and British Columbia core, spillover to Atlantic | Medium term (2-4 years) |

| Compliance costs from rising efficiency and repairability obligations | -0.7% | National, with pronounced effects in Quebec and under federal MEPS | Long term (≥ 4 years) |

| Foodservice margin squeeze delaying commercial back-of-house capex | -0.4% | National, most visible in Toronto, Vancouver, Montreal | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mature Penetration and Lengthening Replacement Cycles for Core Appliances

High penetration across major household categories means sales are tied more closely to replacement and renovation than to first-time ownership, which constrains upside in the Canada kitchen appliances market during periods of weak housing turnover. Public OEM disclosures point to intense promotional activity and pricing pressure, especially in North America, where consumers gravitated to value offerings as interest rates and sentiment weighed on premium mix. Market commentary highlighted consumer reluctance in 2025, with leading brands posting subpar margins in consumer goods segments and prioritizing cost takeout to stabilize performance[4]. Replacement cycles lengthened for refrigerators, ranges, and dishwashers, which delayed demand recovery and elevated the role of service and extended warranties in purchase decisions in the Canada kitchen appliances market. This environment favored small-appliance categories that deliver quick utility at lower price points, while large-appliance buyers deferred upgrades outside of necessity in key provinces. Promotional cadence remained high at retail, which supported unit volumes but limited price realization in the Canada kitchen appliances market.

Slowing Housing Starts/Affordability Headwinds Dampening Big-Ticket Buys

CMHC’s February 2026 outlook projects a decline in new home construction through 2028, with sales below historical averages, which reduces near-term tailwinds for major appliance placements in costly metros of Ontario and British Columbia. Toronto’s housing starts are projected to remain low in 2026 as condominium activity slows, and Vancouver’s starts are expected to trend down as elevated construction costs and weakening demand pressure multi-unit projects. Rising vacancy as new rental supply completes in several urban centers is expected to moderate rent growth, which reduces the urgency of amenity upgrades at scale for some property owners in the Canada kitchen appliances market. Homeowner starts in large centers were subdued in 2025 relative to past highs, signaling a structural skew toward rental that supports baseline appliance demand but dampens premium mix in some corridors. While Montreal, Calgary, and Ottawa-Gatineau generated strength off high rental starts, the national pattern remains fragmented and sensitive to financing conditions in the Canada kitchen appliances market. This backdrop keeps price competition elevated and pushes brands to sharpen value propositions around efficiency and connectivity to maintain conversion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Countertop Innovations Drive Small-Appliance Acceleration

Large kitchen appliances held 72.31% of 2025 revenue as core categories like refrigerators, ranges, cooktops, ovens, and dishwashers continued to anchor household replacements and builder-grade placements in multi-unit projects within the Canada kitchen appliances market. Small kitchen appliances are set to grow at a 4.45% CAGR from 2026 to 2031 as air fryers, espresso machines, frozen-drink makers, and food processors capture discretionary spend with shorter lifecycles and viral use cases, reinforcing an upgrade cadence distinct from major appliances. Leading brands refreshed lineups with personalization, induction-forward cooking, and connected features, while ENERGY STAR expansion across dishwashers, washers, and refrigerators signaled efficiency leadership that channels could market in value and premium tiers. Strategic capacity moves in North America supported reshoring of select product families, enabling shorter lead times and portfolio flexibility across gas, electric, and induction platforms that align with regulatory and consumer shifts in the Canada kitchen appliances market. Within small appliances, premium espresso, versatile countertop ovens, and multifunction cookers remained resilient as households sought convenience and quality without committing to full kitchen remodels in the Canada kitchen appliances market.

The Canada kitchen appliances industry also benefited from rapid innovation cycles that introduced AI-assisted cooking and Matter-enabled connectivity, with product ecosystems that improved discoverability and usage through unified apps and voice integrations. Brands rolled out advanced refrigerators, smart induction ranges with air fry and sous vide features, and connected hood-to-hob orchestration that improved cooking outcomes and energy profiles across kitchens in diverse dwelling types. At the premium end, ultra-luxury suites extended differentiation through materials, design, and integrated software, while mid-market lines offered durable finishes and app-enabled functions at accessible prices within the Canada kitchen appliances market. Small-appliance disruptors posted strong growth, with product pipelines in beverages, food prep, and cooking gaining share through direct-to-consumer models that reinforce higher-margin channels. The Canada kitchen appliances market will continue to balance durable, high-ticket upgrades with frequent, lower-cost countertop additions that sustain brand engagement between major purchases.

By End User: Residential Dominance Persists as Commercial Foodservice Automates

The residential segment accounted for 85.21% of the 2025 value, supported by urban living needs, durable replacement cycles, and steady adoption of smart features that enhance convenience and energy management in the Canada kitchen appliances market. Disposable income gains through 2024 expanded room for home improvement purchases, while dense metros such as Toronto, Vancouver, and Montreal favored space-efficient, connected products that fit smaller kitchens and modern layouts. Buyers increasingly prioritized ENERGY STAR certification to manage utility bills and environmental impact, with utility incentive programs and retail promotions focusing attention on efficient SKUs. Within the Canada kitchen appliances industry, app control, voice assistance, and remote monitoring are now mainstream features, creating post-sale engagement opportunities and software-driven improvements during the product lifecycle. These dynamics helped sustain unit velocity even as single-family housing starts softened in select provinces.

The commercial segment is projected to grow at a 4.71% CAGR from 2026 to 2031 as restaurants and foodservice operators pursue high-efficiency equipment and workflow enhancements to respond to labor and cost pressures in major urban centers within the Canada kitchen appliances market. Full-service restaurants continued to favor premium equipment that supports quality and consistency, while quick-service formats focused on energy-efficient fryers, combi-ovens, and connected refrigeration that reduce waste and improve uptime. Operators leveraged digital tools for inventory, ordering, and kitchen display systems, extending appliance lifecycles where possible and bundling service contracts to align costs with cash flow. Despite near-term constraints, medium-term plans point to greater use of connected, predictive maintenance platforms that reduce downtime and service calls in the Canada kitchen appliances market. This segment’s trajectory complements residential stability and offers targeted growth in high-traffic dining corridors across Canada.

By Distribution Channel: Multi-Brand Stores Lead as Online Gains Share

Multi-brand stores captured 39.95% of 2025 value as shoppers continued to rely on side-by-side comparisons, expert advice, and immediate availability for complex kitchen purchases in the Canada kitchen appliances market. Online channels are projected to expand at a 4.98% CAGR from 2026 to 2031 as retailers and brands elevate content, reviews, and configuration tools that reduce decision friction and support logistics execution at scale. Retail e-commerce represented a measurable share of total trade in November 2025, and broader omnichannel adoption is tightening delivery and installation windows in large metros. Canadian Appliance Source scaled from digital to over 40 showrooms with premium delivery options, exemplifying a hybrid model that builds brand trust and fulfillment advantage in the Canada kitchen appliances market. Exclusive brand outlets and experience centers by premium OEMs strengthened education and design services, deepening engagement with high-end customers in targeted cities.

Other channels such as specialty independents and wholesale continue to serve niche needs, particularly in regional markets and project-based sales in the Canada kitchen appliances market. B2B relationships with builders, property managers, and hospitality groups anchor volume for standardized packages that balance cost, durability, and serviceability. Online platforms now deploy advanced analytics and virtual showrooms that bring large-appliance shopping closer to in-store experiences, improving conversion rates alongside financing and installation bundles. Major marketplaces enhance same-day and next-day coverage across leading metros, while brands cultivate direct-to-consumer sales to capture margin and first-party data advantages in the Canada kitchen appliances market. The Canada kitchen appliances industry will continue to balance physical touchpoints with digital convenience as households and businesses manage complex purchase journeys.

Geography Analysis

Ontario captured 38.71% of sales in 2025 as the province’s dense urban base, higher average incomes, and broad retail infrastructure provided a durable foundation for new placements and replacements in the Canada kitchen appliances market. The province’s energy-efficiency programs supported household upgrades through appliance incentives and thermostat-driven demand-response, which increased attention on connected and ENERGY STAR-certified models. While Toronto’s condominium starts slowed, rental strength sustained baseline demand for builder-grade packages and retrofit activity across multi-unit buildings within the Canada kitchen appliances market. Quebec’s sizable share reflected the scale of Montreal’s metro population and the province’s repairability mandates that will take effect for major appliances in October 2026, which reshaped product planning, warranty design, and after-sales service models. The Canada kitchen appliances market will continue to see spillover of Quebec’s requirements as national portfolios converge on standardized serviceability.

British Columbia’s emphasis on electrification and building performance, including widespread adoption of the Zero Carbon Step Code across dozens of communities, is incentivizing induction and efficient electric ranges in new construction and retrofits in the Canada kitchen appliances market. Vancouver’s housing starts trended lower in 2026 due to construction costs and demand softening, which cooled near-term unit volumes even as code-driven upgrades support efficiency-led product mix. Alberta is set to grow at a 5.21% CAGR from 2026 to 2031, supported by record 2025 housing starts in Calgary and Edmonton and solid employment in energy and construction that boost household purchasing power within the Canada kitchen appliances market As recent rental supply comes online in Calgary and Edmonton, rising vacancy and moderating rent growth temper momentum, yet baseline demand remains resilient given population and labor conditions. The Canada kitchen appliances market in Alberta is therefore positioned for steady gains in both large and small appliances as new households form and upgrade cycles proceed.

The Rest of Canada, including Atlantic provinces, Manitoba, Saskatchewan, and the Territories, maintained steady demand tied to homeownership rates, regional migration patterns, and selective government housing initiatives, although dispersed geographies can raise logistics costs for heavy goods in the Canada kitchen appliances market. In Atlantic Canada, the shift from historic highs in housing starts to more moderate conditions shaped a balanced outlook where baseline replacements continue but large-scale expansions may ease alongside cooling migration. Across provinces, utility incentives, building codes, and repairability rules will influence mix, with connected and efficient products gaining share as standards and rebates shape household value assessments in the Canada kitchen appliances market. Geographic portfolio strategies will therefore continue to reflect local housing cycles and policy environments to stabilize volumes and protect margins.

Competitive Landscape

The market concentration in the Canada kitchen appliances market is high, with the top five players, including Whirlpool, LG, Samsung, GE Appliances, and Electrolux, dominating the market share. This dominance is supported by extensive distribution networks, well-recognized brands, and expanding connected product portfolios. Whirlpool outlined strategic deleveraging and cost actions while advancing product personalization, induction downdraft integration, and category extensions that update the value equation for core kitchen segments. Samsung expanded its ENERGY STAR-certified lineup and introduced unified software experiences across appliances with extended security and update commitments, which reinforced platform differentiation in the Canada kitchen appliances market.

Electrolux reported 2024 organic growth alongside cost actions while rolling out AI-assisted European kitchen platforms and ENERGY STAR Most Efficient laundry pairs in North America, aligning with efficiency and premiumization trends in the Canada kitchen appliances market. LG highlighted design-forward refrigeration with zero-clearance features and smart induction ranges at North American trade shows, underlining its emphasis on space efficiency and app integration. Small-appliance specialists sustained momentum through rapid product cycles and robust direct-to-consumer strategies, strengthening their presence in beverages, food prep, and cooking subcategories in the Canada kitchen appliances market. Retail partners with omnichannel depth, enhanced last-mile capabilities, and service models to support white-glove experiences and accelerated installation windows in large metros. This combination of product innovation, software integration, and service execution continues to define share dynamics across tiers in the Canada kitchen appliances market.

White-space opportunities include modular designs that meet Quebec repairability obligations, compact 24-inch induction-centric built-in suites for urban dwellings, and electrification-forward packages that align with provincial codes, incentives, and sustainability goals in the Canada kitchen appliances market. Circular strategies integrated with EPR regimes can unlock trade-in and refurbishment flows that expand customer touchpoints while lowering lifecycle costs for price-sensitive buyers. Competitive strategies now emphasize long-term software support, AI-enabled features, and interoperability across appliances, which elevates the importance of cybersecurity and reliability as buyers evaluate connected offerings. Localized manufacturing footprints and supplier contracts improve responsiveness and mitigate global risks, which is relevant for Canadian channel inventory planning. Execution will hinge on aligning regulatory readiness, channel excellence, and post-sale service as households and businesses weigh total cost of ownership in the Canada kitchen appliances market.

Canada Kitchen Appliances Industry Leaders

LG Electronics Inc.

Electrolux AB

Samsung Electronics Co. Ltd

Whirlpool Corporation

GE Appliances (a Haier company)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: BSH Home Appliances unveiled Bosch Cook AI at CES 2026, integrating agentic AI with appliance sensors and the Home Connect app for coordinated cooking, alongside new espresso solutions with natural-language control.

- December 2025: Samsung previewed its AI-connected living lineup ahead of CES 2026, including upgraded Bespoke AI Laundry Combo and Bespoke AI WindFree Pro Air Conditioner with motion-aware airflow.

- November 2025: GE Appliances awarded more than USD 150 million in contracts to U.S. suppliers for its new laundry manufacturing plant in Louisville, Kentucky, tied to its multi-year investment program.

- September 2025: LG Electronics Canada announced its 2025 appliance lineup featuring the Counter-Depth MAX Refrigerator with Zero Clearance and a Smart Induction Range with Air Fry and ThinQ connectivity.

Canada Kitchen Appliances Market Report Scope

A complete background analysis of the Canadian kitchen appliances market, which includes an assessment of the national accounts, economy, and emerging market trends by segments, significant changes in the market dynamics, and market overview in the report.

By Product

| Large Kitchen Appliances | Refrigerators & Freezers |

| Dishwashers | |

| Range Hoods | |

| Cooktops | |

| Ovens | |

| Other Large Kitchen Appliances | |

| Small Kitchen Appliances | Food Processors |

| Juicers and Blenders | |

| Grills and Roasters | |

| Air Fryers | |

| Coffee Makers | |

| Electric Cookers | |

| Toasters | |

| Electric Kettles | |

| Countertop Ovens | |

| Other Small Kitchen Appliances (bread makers, waffle makers, egg cookers, etc.) |

By End User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B (directly from the manufacturers) |

By Geography

| Ontario |

| Québec |

| British Columbia |

| Alberta |

| Rest of Canada |

| By Product | Large Kitchen Appliances | Refrigerators & Freezers |

| Dishwashers | ||

| Range Hoods | ||

| Cooktops | ||

| Ovens | ||

| Other Large Kitchen Appliances | ||

| Small Kitchen Appliances | Food Processors | |

| Juicers and Blenders | ||

| Grills and Roasters | ||

| Air Fryers | ||

| Coffee Makers | ||

| Electric Cookers | ||

| Toasters | ||

| Electric Kettles | ||

| Countertop Ovens | ||

| Other Small Kitchen Appliances (bread makers, waffle makers, egg cookers, etc.) | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B (directly from the manufacturers) | ||

| By Geography | Ontario | |

| Québec | ||

| British Columbia | ||

| Alberta | ||

| Rest of Canada | ||

Key Questions Answered in the Report

What is the size and growth outlook of the Canada kitchen appliances market through 2031?

The Canada kitchen appliances market size is USD 7.45 billion in 2026 and is projected to reach USD 9.23 billion by 2031 at a 4.38% CAGR.

Which product and end-user segments are leading and growing fastest in Canada?

Large kitchen appliances led with 72.31% in 2025, while small kitchen appliances are projected to grow at 4.45% CAGR, and residential accounts for 85.21% as commercial demand is projected at a 4.71% CAGR.

How are regulations and standards influencing Canada’s appliance choices?

Federal MEPS under Amendment 18 and planned Amendment 19 align with U.S. rules and raise efficiency baselines, while Quebec’s repairability mandates are pushing modular, durable designs and extended service models.

What role do housing trends play in the Canada kitchen appliances market?

Rental-led strength in 2025 supported baseline appliance demand even as single-family starts softened in Toronto and Vancouver, with CMHC projecting lower new home construction through 2028.

How are connected features changing value propositions for buyers?

Unified software experiences, security frameworks, and multi-year updates are turning appliances into connected assets that interact with utility programs and home platforms, improving lifetime value and efficiency.

Which provinces stand out for share and growth within Canada?

Ontario captured 38.71% in 2025 due to scale and retail depth, while Alberta is projected to grow at 5.21% CAGR on the back of strong housing and labor markets.

Page last updated on: