Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

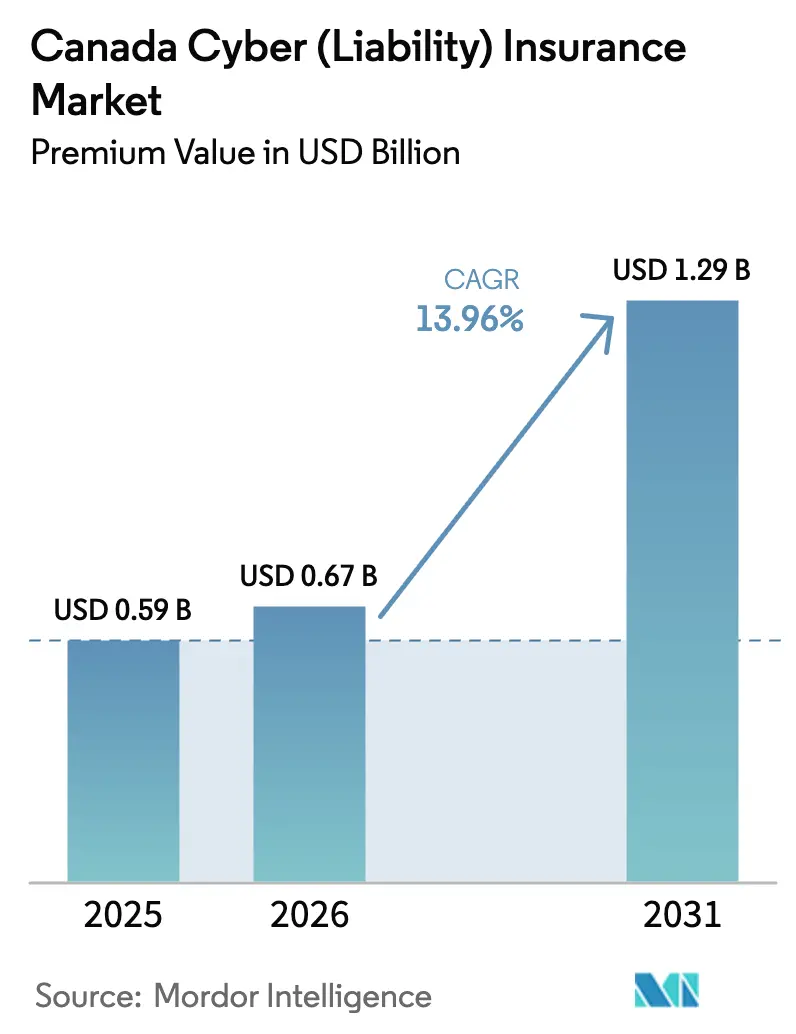

| Base Year Market Size (2025) | USD 0.59 Billion |

| Market Size (2026) | USD 0.67 Billion |

| Market Size (2031) | USD 1.29 Billion |

| Growth Rate (2026 - 2031) | 13.96% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canada Cyber (Liability) Insurance Market Analysis by Mordor Intelligence

The Canadian cyber insurance market size in 2026 is estimated at USD 0.67 billion, growing from 2025 value of USD 0.59 billion with 2031 projections showing USD 1.29 billion, growing at 13.96% CAGR over 2026-2031. This expansion is underpinned by the rapid digital transformation of SMEs, stricter regulatory frameworks, and the increasing frequency of ransomware attacks, which collectively broaden the scope of insurable risks. Despite rising demand, capacity remains constrained as reinsurers exercise caution regarding systemic risks, compelling primary insurers to adopt advanced underwriting practices that incorporate real-time security telemetry. The distribution model is transforming, with brokers still managing the majority of policies, while MGA-led digital platforms are progressively capturing market share, influencing product innovation, and accelerating time-to-market. These dynamics highlight the evolving nature of the market, where technological advancements and regulatory pressures are reshaping both risk assessment and distribution strategies.

Key Report Takeaways

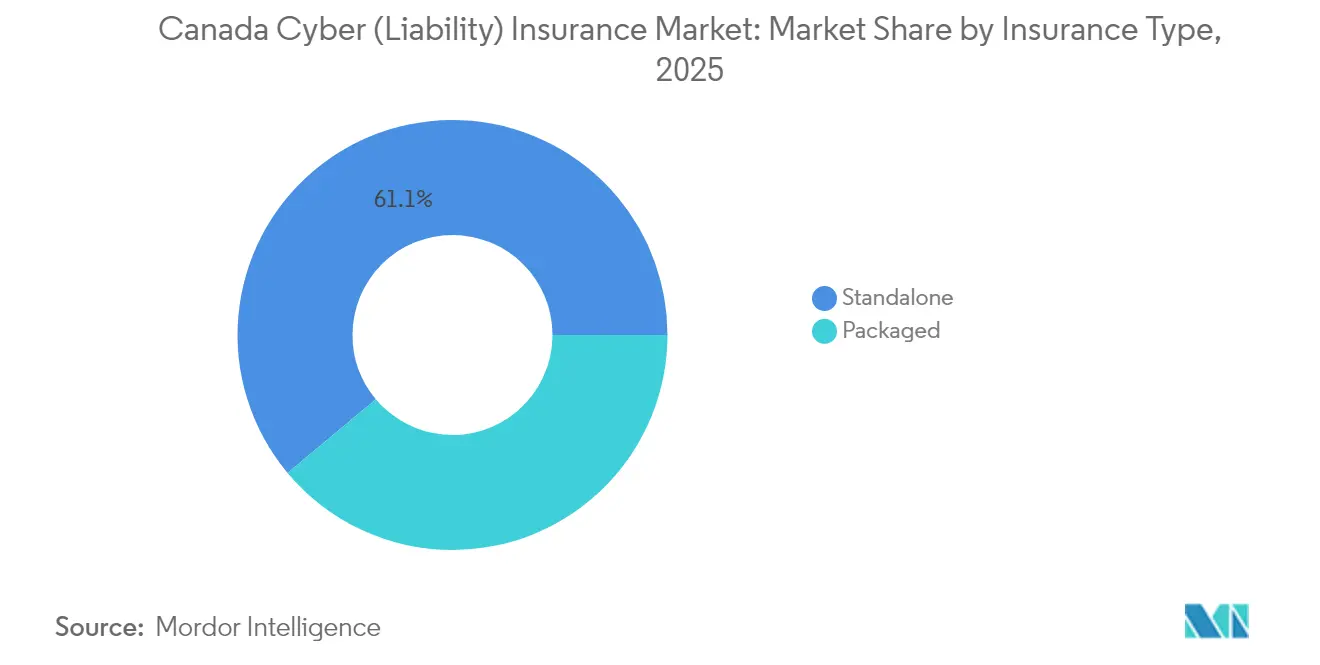

- By insurance type, standalone policies held 61.08% of the 2025 written premium of the Canadian cyber insurance market, while packaged products for SMEs are forecast to grow at a 15.35% CAGR through 2031.

- By organization size, large enterprises controlled 45.75% revenue share of the Canadian cyber insurance market in 2025, whereas small enterprises are set to grow at 17.25% CAGR to 2031.

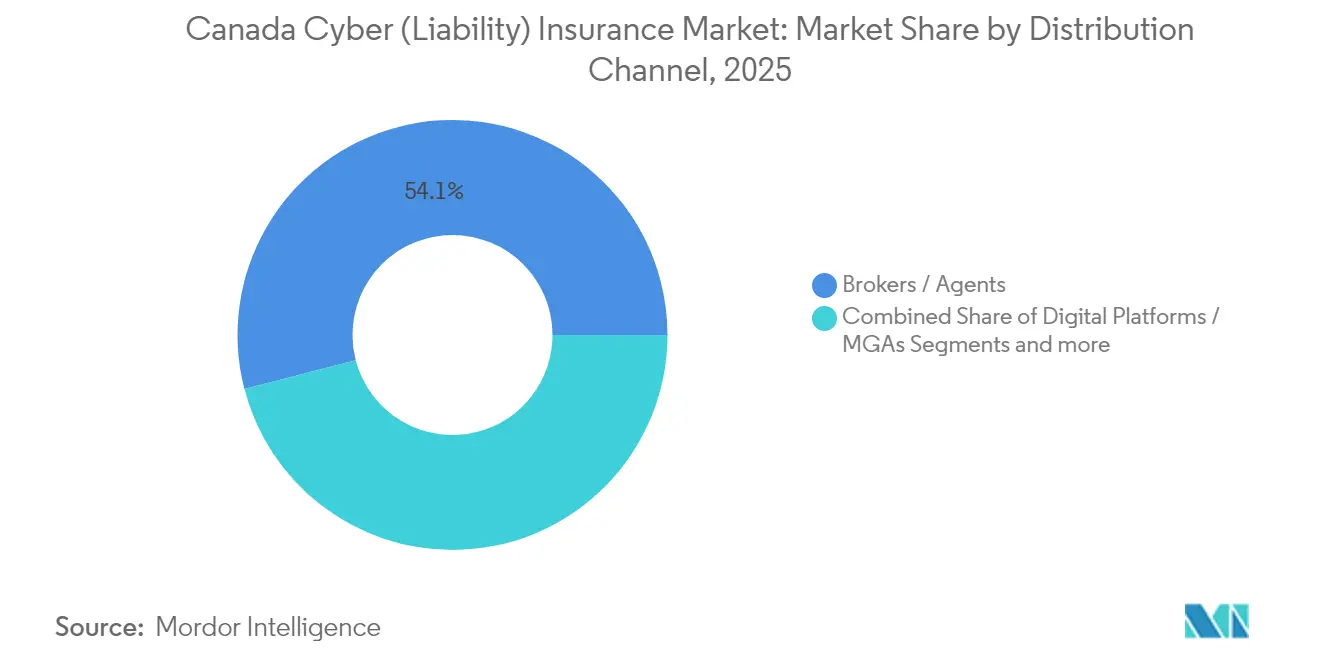

- By distribution channel, brokers and agents retained 54.05% of the 2025 premium of the Canadian cyber insurance market, yet digital platforms and MGAs are expanding at a 18.85% CAGR.

- By end-use industry, financial services captured 27.55% of the Canada cyber insurance market size in 2025; critical infrastructure is advancing fastest at 18.05% CAGR.

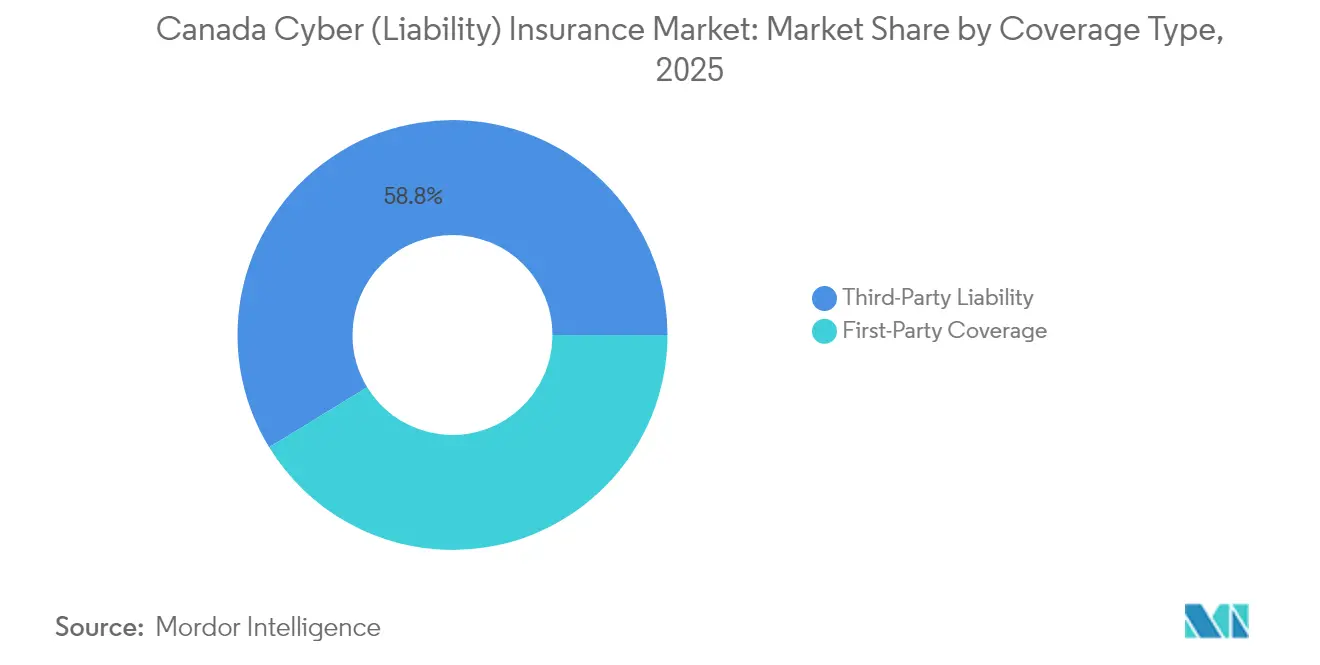

- By coverage type, third-party liability accounted for 58.75% of the Canada cyber insurance market share in 2025, while first-party protections are increasing at 16.55% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Cyber (Liability) Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid digitization of SMEs | +3.2% | Ontario, Quebec, British Columbia | Medium term (2-4 years) |

| Rising ransomware severity & frequency | +4.1% | National, highest in urban critical-infrastructure hubs | Short term (≤ 2 years) |

| Mandatory breach-notification under PIPEDA | +2.8% | National, strongest in federally regulated sectors | Medium term (2-4 years) |

| Premium tax deductibility (CRA 2026 ruling) | +1.9% | National, strongest among tax-sensitive SMEs | Long term (≥ 4 years) |

| Cyber-security frameworks in infrastructure | +2.3% | Energy, telecom, and banking clusters | Long term (≥ 4 years) |

| MGA-led managed cyber-insurance platforms | +1.5% | Major metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid digitization of Canadian SMEs

Over 71,000 businesses have tapped the Canada Digital Adoption Program’s CAD 1.2 billion pool of grants, loans, and wage subsidies since 2022, speeding adoption of e-commerce, cloud, and hybrid-work tools [1]Innovation, Science and Economic Development Canada, “Canada Digital Adoption Program,” ised-isde.canada.ca . This technology leap has broadened SMEs’ attack surfaces because security controls trail behind new deployments. Human error remains the proximate cause in many data-loss events, underscoring the gap between operational and security maturity. Insurers respond by bundling risk-assessment and employee-training modules into policies, which raises the perceived value proposition. As these firms increasingly transact online, cyber cover is evolving from discretionary spend to a prerequisite for supplier contracts and financing.

Rising ransomware severity & frequency

Ransomware is projected to remain the leading threat to critical infrastructure in Canada through 2026, as identified by the Canadian Centre for Cyber Security [2]Communications Security Establishment Canada, “National Cyber Threat Assessment 2025-2026,” cyber.gc.ca . The adoption of cybercrime-as-a-service models by state-sponsored actors and organized crime groups has lowered the entry barrier for attackers, enabling the use of advanced cyber tools by less experienced individuals. In 2023, the average cost of resolving a data breach in Canada reached CAD 6.9 million, driving organizations to prioritize high-limit first-party insurance coverage to address ransom payments, forensic analysis, and business interruption recovery. Insurance providers are increasingly implementing stricter incident cooperation clauses, requiring insured entities to report incidents within hours to ensure coverage eligibility. These developments underscore the growing financial and operational risks posed by cyber threats, compelling businesses to enhance their cybersecurity strategies and risk management frameworks.

Mandatory breach notification under PIPEDA

Since the 2024 enforcement of Quebec’s Law 25 and Ontario’s Bill 194, organizations now juggle overlapping provincial and federal requirements that raise the stakes of non-compliance. Breach disclosure triggers legal fees, notification expenses, and potential class actions, making liability insurance indispensable. For insurers, the richer flow of claims data improves actuarial insight, yet it also highlights the magnitude of unanticipated costs such as post-incident credit monitoring. Consequently, underwriters are adding sub-limits for notification expenditures while offering pre-breach consultancy credits to policyholders that adopt recommended safeguards. The additional transparency is expected to narrow data gaps in pricing models over the next three years.

Cyber-insurance premium tax deductibility (CRA ruling)

The 2024 Budget outlines a provision enabling corporations to categorize cyber insurance premiums as operating expenses, which could significantly lower their after-tax expenditures depending on their tax brackets. This measure is anticipated to alleviate financial constraints for companies with limited cash flow, allowing them to secure higher insurance limits and enhance their cyber risk management capabilities. Industry associations are proactively urging businesses to align their quoting processes with fiscal year-end schedules to fully capitalize on the expected tax benefits. Insurance providers, while preparing for increased price competition in the short term, are also leveraging this opportunity to bundle cybersecurity services and establish multi-year agreements before the policy is implemented. Actuarial analysis suggests that expanding the premium base will likely reduce loss-ratio volatility by diversifying the risk pool, thereby contributing to greater market stability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited historical actuarial loss data | -2.1% | All provinces, most acute in specialty risks | Long term (≥ 4 years) |

| Capacity pull-back by global reinsurers | -1.8% | Large-limit accounts nationwide | Medium term (2-4 years) |

| Tight underwriting on nation-state threats | -1.4% | Critical infrastructure and government contractors | Short term (≤ 2 years) |

| Low awareness among <50-employee firms | -1.2% | Rural and non-metro SMEs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited historical actuarial loss data

Traditional lines benefit from decades of claims history, but cyber threats mutate quickly, weakening the predictive power of back-testing. The Insurance Bureau of Canada attributes the 153% combined ratio from 2019-2023 to the underestimation of correlated ransomware losses and breach-response inflation [3]Insurance Bureau of Canada, “Cyber Insurance Premiums and Claims 2019-2023,” ibc.ca . Carriers now integrate threat-intel feeds and scenario stress tests alongside classical frequency-severity curves, yet remain judgmental. Over the long term, mandatory disclosures will enlarge datasets, but model calibration lags means prudence will dominate pricing strategy through at least 2029. This restraint tempers growth by keeping premiums high, especially for high-aggregate limits.

Tight underwriting linked to nation-state threats

Unclear attribution in early incident stages complicates the distinction between cybercrime and state-linked espionage. Consequently, insurers survey insureds about geopolitical exposure, software supply chain governance, and segmentation of operational technology networks. Entities handling critical infrastructure face exclusionary war-risk clauses or hefty rate-on-line uplifts until they document segmentation and incident-response playbooks. The Canadian Centre for Cyber Security’s alerts provide valuable context, yet carriers anticipate retaining carve-outs for hostile-state actions through at least 2027. Buyers respond by enhancing monitoring and threat-intelligence subscriptions to retain broader coverage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Standalone Policies Anchor Growth

Standalone policies dominated 2025 with a 61.08% share, reflecting organizations’ need for bespoke terms covering ransom demands, data-restoration fees, and systemic-business-interruption losses. Underwriters continuously tweak terms, adding sub-limits for social-engineering fraud and cryptojacking as threat vectors evolve. Packaged add-ons bundled into business-owner or errors-and-omissions forms remain attractive for SMEs seeking convenience. High-touch brokers pitch standalone cover to regulated verticals like finance and healthcare that require comprehensive wordings. As incident costs rise, average standalone limits are trending upward, emphasizing deep carrier-reinsurer collaboration.

Packaged products, while smaller in scale, are demonstrating a strong compound annual growth rate (CAGR) of 15.35%, reflecting their growing relevance in the market. These offerings incorporate advanced value-added services, such as 24/7 breach coach hotlines and phishing-simulation platforms, which are designed to strengthen clients' cyber hygiene practices. Insurance carriers strategically position these packages as entry-level solutions, intending to transition clients to more comprehensive standalone policies as their operational scale increases. This approach underscores the dual-track model within the Canadian cyber insurance market, which effectively aligns the complexity of coverage with the evolving maturity of organizations. As a result, the market is well-positioned to cater to diverse organizational needs, ensuring scalability and adaptability in its offerings.

By Organization Size: Enterprise Dominance Meets SME Momentum

Large enterprises held 45.75% of the 2025 premium because their complex, multi-jurisdictional exposures demand broad indemnification and sophisticated incident-response vendors. These buyers negotiate manuscript wordings and layered towers blending domestic and London-market capacity to reach limits exceeding CAD 400 million. They also invest in continuous-monitoring tools that integrate with insurers’ loss-prevention platforms, yielding underwriting credits and reduced retentions. Board-level scrutiny of cyber operations ensures annual coverage reviews, often resulting in expanded endorsements for technology errors and reputational-harm costs.

SMEs, particularly those under CAD 20 million revenue, represent the fastest-growing cohort at 17.25% CAGR. Digitization grants compressed technology-adoption timelines, exposing gaps in security staffing and process maturity. MGA platforms leverage automated scans and public-threat intel to produce instant, bindable quotes, shortening sales cycles from weeks to minutes. Mid-market firms (CAD 20-200 million revenue) fall between the two extremes, often lacking IT scale yet facing sophisticated threats. They are key targets for hybrid distribution—brokers harness MGA tools to deliver advisory depth alongside digital speed, ensuring the Canada cyber insurance market captures spend across the organizational spectrum.

By Distribution Channel: Digital Platforms Disrupt Brokerage Primacy

Brokers and agents intermediated 54.05% of premiums in 2025, continuing to deliver bespoke advisory services to complex accounts. Their competitive edge lies in policy-comparison expertise and claim-advocacy capabilities, yet manual workflows encumber speed. Digital MGA platforms, clocking 18.85% CAGR, automate application intake, leverage AI scoring, and bundle risk-mitigation software. They resonate with tech-savvy SMEs that prefer self-service models and near-instant coverage confirmation. Direct carrier portals occupy a middle ground, targeting mid-sized firms seeking brand assurance without brokerage fees.

Brokerages are adapting through technology alliances, deploying application-programming-interface (API) connectivity to pull MGA quotes into comparative rating dashboards. Meanwhile, MGAs partner with security-operations-center vendors to add continuous-monitoring subscriptions, creating sticky renewal economics. As these models converge, buyers will likely toggle between channels depending on transaction complexity: high-limit placements via brokerage advisory and low-limit renewals through embedded digital touchpoints. The interplay ensures competitive tension that benefits clients through broader product choice and service innovation.

By End-Use Industry: Financial Services Leads While Infrastructure Accelerates

Financial services captured 27.55% of the Canada cyber insurance market size in 2025 because OSFI’s Guideline B-13 mandates robust governance, risk, and compliance frameworks. Banks and credit unions routinely purchase full-suite coverage, including funds-transfer fraud and operational-technology (OT) outages tied to payment-system disruptions. High board engagement sustains multi-year policy partnerships that bundle analytics dashboards and tabletop exercises. Claims trends show rising costs for regulatory investigation and customer-notification obligations, reinforcing the need for third-party liability layers.

Critical-infrastructure sectors—energy, utilities, transport—log the highest growth rate at 18.05% CAGR as Bill C-26 compels robust OT safeguards. Cyber incidents in these verticals risk physical consequences, elevating business-interruption and contingent-BI exposures. Insurers respond with specialised wordings that contemplate property damage and environmental liabilities triggered by cyber events. Healthcare, retail, manufacturing, government, and education each display unique triggers: patient-data privacy, PCI-DSS compliance, intellectual-property theft, and system outages. The diversity underscores segmentation granularity, enabling insurers to fine-tune coverages and pricing.

By Coverage Type: Liability Core Expands to Operational Protections

Third-party liability maintained 58.75% of the Canada cyber insurance market share in 2025, driven by stringent privacy obligations and class-action prevalence. PIPEDA and provincial statutes oblige prompt disclosure and remediation, which pushes legal expenses higher. Consequently, carriers include dedicated panels of breach coaches, privacy counsel, and media-crisis advisors to mitigate reputational fallout. Limit adequacy is a growing board concern as breach-notification thresholds expand to encompass supply-chain incidents.

First-party covers are advancing at 16.55% CAGR, reflecting ransomware’s dominance. Policies now encompass extortion payments, digital-asset restoration, and reputational-harm mitigation expenses. Many carriers offer sub-limits for business-interruption measured in hourly revenue rather than daily aggregates, better aligning indemnity with high-velocity digital commerce. Some insurers bundle proactive services—penetration testing, patch-management audits—to reduce loss frequency in exchange for premium credits. The blending of liability and first-party protections positions the Canada cyber insurance market to deliver holistic risk-transfer solutions.

Geography Analysis

Adoption correlates strongly with economic concentration, making Ontario, Quebec, and British Columbia the largest buyers by premium. Toronto’s financial corridor, Montreal’s aerospace and AI clusters, and Vancouver’s burgeoning tech sector face intense ransomware and supply-chain threats, driving higher average limits. Quebec’s Law 25 goes beyond federal standards, elevating liability exposure and prompting local firms to negotiate broader notification-cost coverage. British Columbia’s energy pipeline infrastructure brings OT-centric risks that require bespoke endorsements for physical-damage triggers.

Alberta’s energy and midstream operators demand solutions for OT and SCADA vulnerabilities, drawing capacity from carriers versed in industrial-control-system exposures. The province’s cyber-maturity initiatives dovetail with Bill C-26, encouraging policy uptake among mid-tier oilfield-services firms. Atlantic provinces, while smaller, show steady growth as provincial grants spur digital trade adoption in aquaculture and logistics. Northern territories remain nascent due to sparse population and limited broadband, though federal infrastructure projects could stimulate uptake over time.

National threat-information-sharing agreements facilitate uniform underwriting, but premium differentials persist based on local incident frequency and legal milieu. Urbanized provinces experience higher cybercrime reporting rates, influencing carrier loss models and pricing granularity. Rural resilience programs, including subsidised cyber-awareness workshops, aim to close coverage gaps for micro-businesses. As cloud adoption equalises access to advanced tools across geographies, insurers expect risk dispersion to narrow, reducing the variance of base rates between provinces.

Competitive Landscape

The top five players—Intact, Aviva, Chubb, Zurich, and CNA—control approximately half of the premium, giving the Canada cyber insurance market a moderate concentration score while leaving room for specialist MGAs and Lloyd’s syndicates to contest share. These incumbents leverage multi-line relationships and scale to bundle cyber endorsements with property and casualty placements, deepening client stickiness. Technology investment is a clear differentiator: Intact’s CAD 2.25 million commitment to the Université de Sherbrooke cybersecurity hub enhances analytical capability, while Zurich’s North America platform integrates predictive analytics for middle-market cyber underwriting.

Strategic partnerships abound. Incumbents increasingly underwrite MGAs’ fronting programs, exchanging capacity for data analytics that refine their models. Reinsurers’ cautious stance on aggregate cyber exposure incentivises carriers to diversify retrocession through capital-markets instruments such as cyber-cat bonds. Consolidation remains active: Definity’s CAD 3.3 billion purchase of Travelers Canada elevates its commercial-lines footprint and injects fresh cyber expertise into its portfolio mix. Foreign specialists like Beazley and Hiscox maintain Lloyd’s platforms to provide high-excess layers, filling gaps left by domestic primary capacity caps.

Competitive intensity is tempered by underwriting discipline necessitated by systemic-risk uncertainty. Carriers cross-sell pre-breach services—vulnerability scans, threat-hunting retainers—to differentiate beyond price. MGAs pioneer parametric triggers that pay out when widely used cloud providers suffer outages, addressing contention points around business-interruption coverage. As cyber incidents increasingly involve overlapping property, liability, and crime elements, carriers with integrated claims and forensics infrastructure are better positioned to manage loss costs and sustain profitability. Overall, the market structure encourages continuous product innovation while preserving sufficient stability for reinsurer confidence.

Canada Cyber (Liability) Insurance Industry Leaders

-

Intact Financial Corp.

-

Chubb

-

AIG Canada

-

Zurich Canada

-

CNA Canada

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Definity Financial Corporation agreed to acquire Travelers’ Canadian operations for CAD 3.3 billion, adding CAD 1.6 billion gross written premium and expanding commercial cyber capabilities.

- April 2025: Coalition introduced its Active Cyber Policy featuring affirmative AI endorsements for incidents caused by artificial-intelligence systems.

- November 2024: Zurich North America unveiled its 2025-2027 strategic plan, committing to expand middle-market, excess & surplus, and specialty cyber offerings in Canada after doubling business size and improving combined ratios in 2024.

- October 2024: Intact Financial Corporation committed CAD 2.25 million to launch the Intact Cybersecurity Hub at Université de Sherbrooke.

Canada Cyber (Liability) Insurance Market Report Scope

Cyber liability insurance serves as a protective contract for entities engaged in online business, helping to mitigate associated financial risks. By paying a monthly or quarterly premium, businesses can transfer a portion of their online risks to the insurer.

The Canadian cyber (liability) insurance market is segmented by insurance type, coverage, enterprise size, and end user. By insurance type, the market is segmented into package and stand-alone. By coverage, the market is segmented into data breach, cyber liability, first-party coverage, third-party coverage, and other coverages. By enterprise size, the market is segmented into large enterprises and SMEs. By end user, the market is segmented into BFSI, IT and telecommunication, retail and e-commerce, healthcare, manufacturing, government and public sector, and other end users. The report offers market size and forecasts in value (USD) for all the above segments.

By Insurance Type

| Standalone |

| Packaged |

By Organization Size

| Small Enterprises |

| Mid-Sized Enterprises |

| Large Enterprises |

By Distribution Channel

| Brokers / Agents |

| Direct Sales (Insurer-Owned Channels) |

| Digital Platforms / MGAs |

By End-Use Industry

| Financial Services |

| Healthcare |

| Retail & E-Commerce |

| Manufacturing |

| Critical Infrastructure (Energy, Utilities, Transport) |

| Government & Public Sector |

| Others (Education, Non-Profit) |

By End-Use Coverage Type

| First-Party Coverage (Ransom, Downtime, Forensics) |

| Third-Party Liability (Legal, Privacy Breach, Fines) |

| By Insurance Type | Standalone |

| Packaged | |

| By Organization Size | Small Enterprises |

| Mid-Sized Enterprises | |

| Large Enterprises | |

| By Distribution Channel | Brokers / Agents |

| Direct Sales (Insurer-Owned Channels) | |

| Digital Platforms / MGAs | |

| By End-Use Industry | Financial Services |

| Healthcare | |

| Retail & E-Commerce | |

| Manufacturing | |

| Critical Infrastructure (Energy, Utilities, Transport) | |

| Government & Public Sector | |

| Others (Education, Non-Profit) | |

| By End-Use Coverage Type | First-Party Coverage (Ransom, Downtime, Forensics) |

| Third-Party Liability (Legal, Privacy Breach, Fines) |

Key Questions Answered in the Report

What is the projected value of the Canada cyber insurance market by 2031?

It is expected to reach USD 1.29 billion, reflecting a 13.96% CAGR.

Which coverage type currently dominates Canadian cyber policies?

Third-party liability leads with a 58.75% share, though first-party protections are expanding fastest.

Why are MGA digital platforms gaining share in Canada?

They automate underwriting, embed security services, and appeal to SMEs by cutting quote-to-bind time to minutes.

How will CRA’s forthcoming tax ruling influence adoption?

Allowing premiums to be tax-deductible has the potential to reduce effective costs for SMEs, thereby stimulating latent demand beyond 2026.

Which sector is growing fastest in cyber-insurance uptake?

Critical infrastructure (energy, utilities, transport) is advancing at 18.05% CAGR due to Bill C-26 compliance pressures.

How concentrated is the competitive landscape?

The top five carriers account for nearly half of the total premiums, highlighting their significant market concentration.

Page last updated on: