UK Electronic Gadgets Insurance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

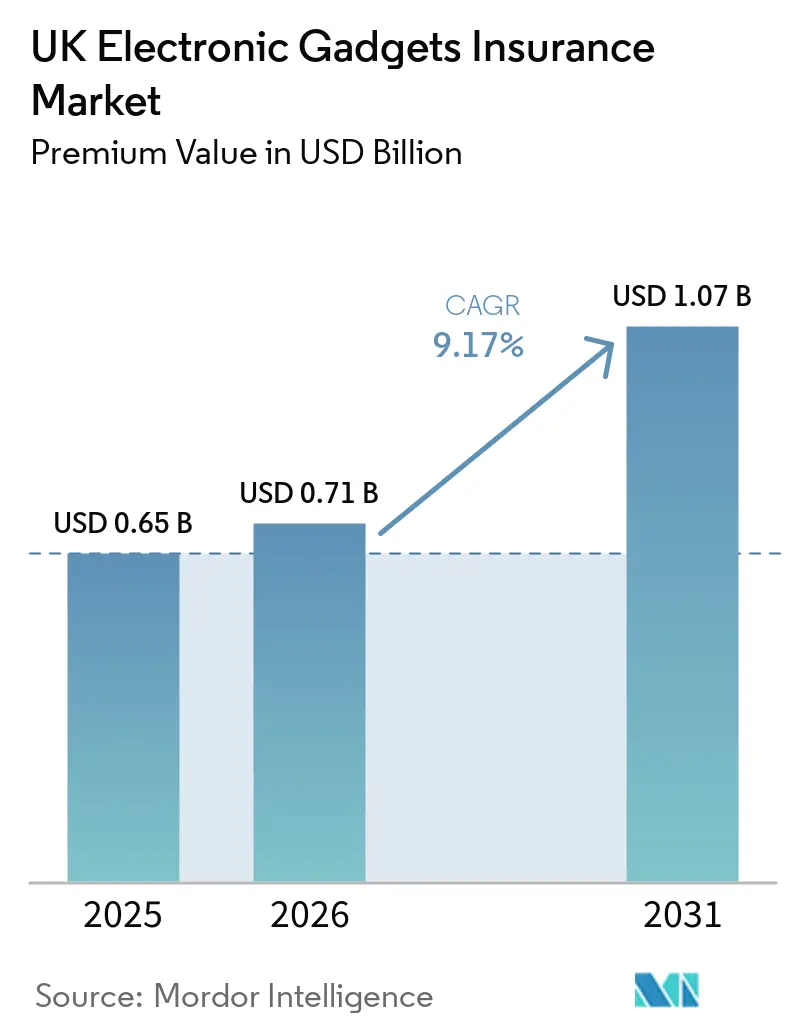

| Base Year Market Size (2025) | USD 0.65 Billion |

| Market Size (2026) | USD 0.71 Billion |

| Market Size (2031) | USD 1.07 Billion |

| Growth Rate (2026 - 2031) | 9.17% CAGR |

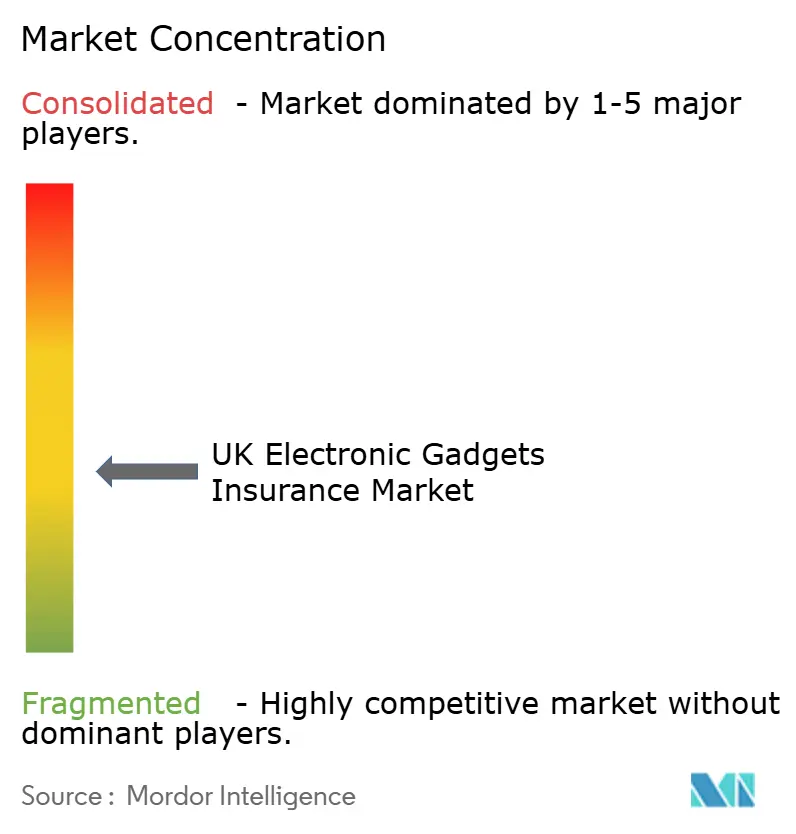

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UK Electronic Gadgets Insurance Market Analysis by Mordor Intelligence

The UK Electronic Gadgets Insurance Market size in terms of premium value is projected to be USD 0.65 billion in 2025, USD 0.71 billion in 2026, and reach USD 1.07 billion by 2031, growing at a CAGR of 9.17% from 2026 to 2031.

Demand concentrates in high-usage personal tech where damage, loss, and theft risk is persistent across home, travel, and work settings. Multi-device bundles and embedded protection at telco and retail points of sale raise visibility, while standalone products adapt to Consumer Duty requirements on fair value. Claims handling quality, repair logistics, and rapid settlement are central to purchase decisions as buyers balance price with service speed. Tighter oversight and clearer outcomes continue to shape product design, disclosures, and post-sale support within the UK electronic gadgets insurance market.

Key Report Takeaways

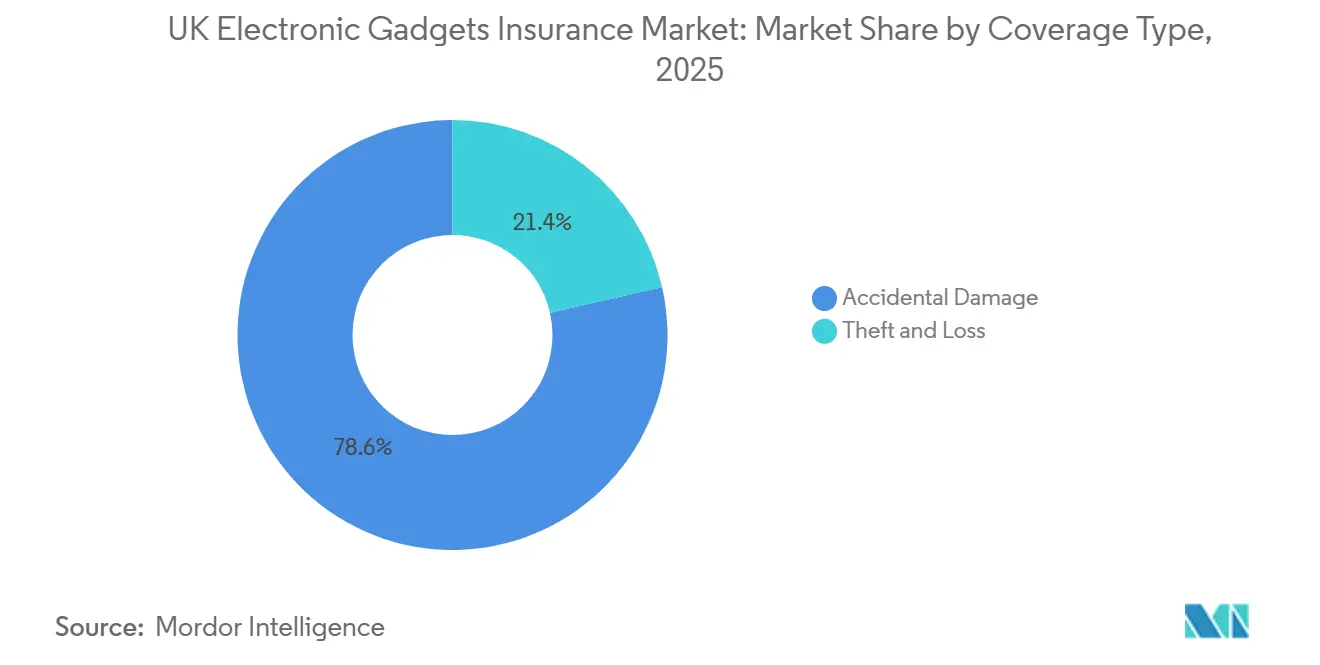

- By coverage type, accidental damage led with 78.57% of the UK electronic gadgets insurance market share in 2025, while theft and loss is forecast to expand at a 10.04% CAGR through 2031.

- By device type, mobile devices held 46.83% of the UK electronic gadgets insurance market share in 2025, while drones are projected to advance at a 12.82% CAGR through 2031.

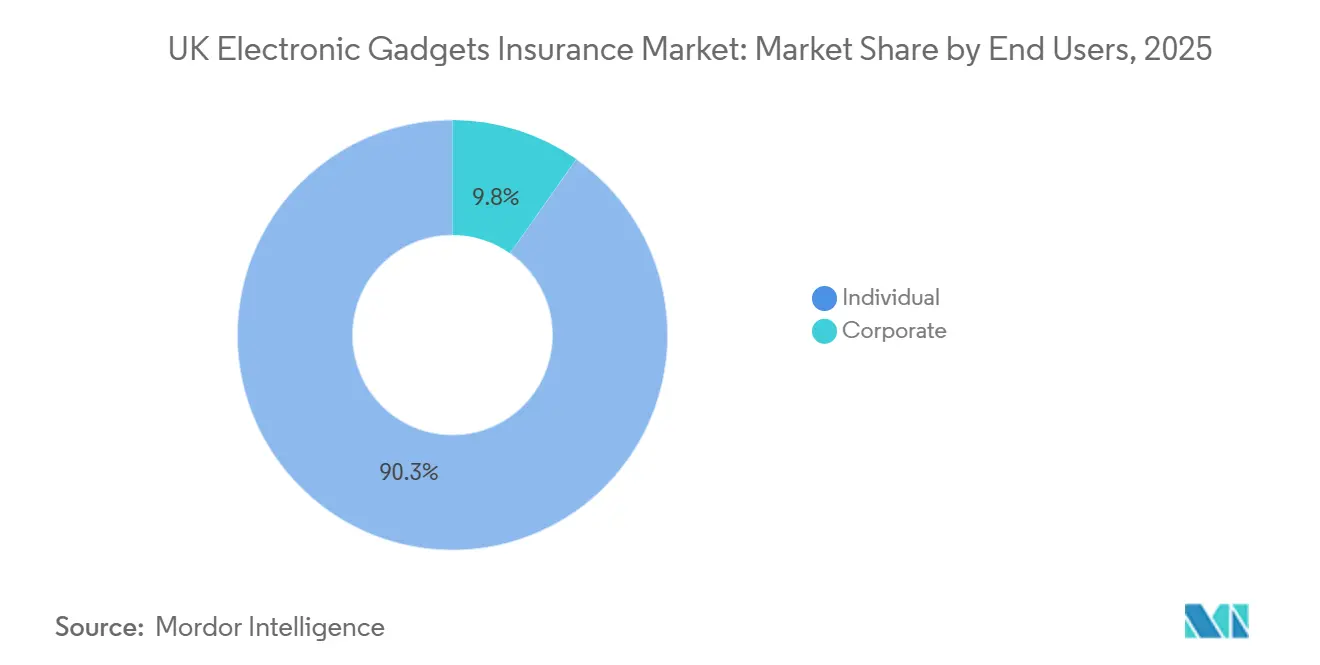

- By end users, individuals accounted for 90.25% of the UK electronic gadgets insurance market share in 2025, while corporate buyers are forecast to grow at a 14.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UK Electronic Gadgets Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing penetration of smart devices driving protection demand | +2.3% | Global, with APAC core spill-over to MEA | Short term (≤ 2 years) |

| Rising device replacement costs increasing financial exposure | +2.1% | North America & EU | Medium term (2-4 years) |

| Digital distribution channels improving insurance accessibility | +1.8% | Global | Short term (≤ 2 years) |

| Product innovation catering to tech-savvy and connected users | +1.6% | North America & EU | Medium term (2-4 years) |

| Heightened cybersecurity awareness fueling specialized coverage | +1.4% | Global | Long term (≥ 4 years) |

| Expansion of e-commerce and IoT enabling bundled insurance models | +1.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Penetration of Smart Devices Driving Protection Demand

High device penetration and multi-device ownership strengthen the addressable base, which supports sustained demand in the UK electronic gadgets insurance market. Participation Survey results indicate 68% of UK adults owned laptops in 2024 to 2025, reflecting elevated reliance on portable computing for work, study, and entertainment[1]Department for Culture, Media & Sport and Department for Science, Innovation & Technology, “Main Report for the Participation Survey (April 2024 to March 2025),” GOV.UK, gov.uk. Research on children’s digital access shows widespread mobile adoption by age 11 with near-universal smartphone use among 12 to 15-year-olds, which encourages family and student-oriented device protection. Platform dynamics shape household spending as the Competition and Markets Authority reports 55% of UK smartphone users operate iOS and many own additional Apple devices, increasing multi-device value concentration. Contactless adoption remains mainstream, with iOS and Android users conducting tap-to-pay transactions at high rates, which raises the perceived need for rapid replacement in loss or theft events. As devices connect communications, payments, and productivity, multi-device policies and straightforward claims experiences remain a priority in the UK electronic gadgets insurance market.

Rising Device Replacement Costs Increasing Financial Exposure

Households and small firms look to reduce the financial strain of repairs or replacements, which supports protection adoption in the UK electronic gadgets insurance market. New plan designs extend eligibility to a wider set of devices with defined claim limits and multiple claims per year to manage real-life usage and breakage patterns. EE’s Multi Tech Cover launched in January 2026 at GBP 15.99 monthly for damage-only and GBP 22.99 for full loss and theft cover, allowing up to five claims in any 12-month period and extending breakdown cover to devices under five years old[2]EE, “EE Sets Benchmark for UK Tech Protection with the Launch of Multi Tech Cover,” EE Newsroom, newsroom.ee.co.uk. On the contents side, Aviva increased personal belongings limits to GBP 50,000 and lifted business equipment limits to GBP 15,000, explicitly covering mobile phones and student devices at term-time addresses, which integrates device protection into broader household policies. For self-employed workers and SMEs, insurers emphasize quick decisions to reduce downtime, so settlement speed and clear coverage terms often outweigh minor price differences. These features maintain buyer interest in plans that balance affordability with dependable claims service in the UK electronic gadgets insurance market.

Product Innovation Catering to Tech-Savvy and Connected Users

AI-enabled operations and broader device eligibility enhance user experience while improving efficiency in the UK electronic gadgets insurance market. Aviva began rolling out a generative AI-powered summarization tool in November 2025 to condense lengthy GP medical reports for life underwriting after an 18-month test program, signaling broader adoption of AI capabilities in complex insurance workflows. On device protection, EE’s Multi Tech Cover supports phones, tablets, laptops, headphones, smartwatches, e-readers, home security accessories, fitness trackers, gaming consoles, controllers, and VR headsets, which aligns with modern households that manage several devices across family members. Ecosystem partners expand capacity for service enhancements as Genstar Capital’s majority stake in Likewize supports AI-driven claims handling and premium support across a large device footprint. Clear acceptance regimes and transparent pricing for high-frequency product lines, including student laptop cover options, help buyers weigh the value of rapid repair or replacement against premiums and deductibles. Over time, product breadth and service automation reinforce trust and repeat purchase, which supports steady penetration in the UK electronic gadgets insurance market.

Heightened Cybersecurity Awareness Fueling Specialized Coverage

The incidence of cyber breaches and the financial impact on firms highlight the need for protection that combines equipment and cyber elements. The Cyber Security Breaches Survey records that 50% of UK businesses experienced breaches or attacks in 2024 while only 7% held stand-alone cyber coverage, which underscores a protection gap relevant to device-heavy operations. Average breach costs were GBP 1,025 across all businesses, rising to GBP 10,830 for medium and large firms, which supports interest in SME bundles that link device protection with cyber assistance and response. Large carriers continue to invest in research partnerships to better quantify AI-related and digital risks, as seen in AXA UK’s academic collaboration focused on methods to understand and insure complex technology exposures. For small firms and remote workers, device policies that integrate cyber elements or offer add-ons create a practical route to improve resilience without managing multiple separate products[3]AXA UK, “Business Insurance | Get a quote online,” AXA UK, axa.co.uk. This combination strengthens the value proposition for SMEs and sole traders as they navigate digital operations in the UK electronics gadgets insurance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing premium pricing limiting adoption among cost-conscious users | -1.9% | Global | Short term (≤ 2 years) |

| Complicated claims procedures impacting customer experience | -1.3% | North America & EU | Medium term (2-4 years) |

| Claims fraud leading to stricter underwriting norms | -1.1% | Global | Long term (≥ 4 years) |

| Competitive intensity and market crowding constraining profitability | -0.8% | North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complicated Claims Procedures Impacting Customer Experience

Variation in claims acceptance and processing quality shapes buyer perceptions and switching behavior in the UK electronic gadgets insurance market. FCA value measures for 2024 show acceptance rates for home claims ranged from 50 to 55% at the lower end up to 95 to 100% for the top tier, demonstrating how wording clarity and process execution influence outcomes. Consumer Duty pushes providers to simplify documents, set realistic expectations for evidence and process steps, and maintain timely updates to reduce friction. Device protection policies that depend on third-party repairs must maintain reliable logistics and parts availability to avoid extended downtime. As brand standards tighten, carriers focus on faster decisions with clearer eligibility to differentiate in high-volume categories such as phones and laptops. These measures aim to stabilize customer satisfaction while aligning with outcomes-focused supervision in the UK electronic gadgets insurance market.

Claims Fraud Leading to Stricter Underwriting Norms

Detected fraud represents a material challenge across non-life lines and influences verification steps for device categories with frequent claims. The Association of British Insurers reports that fraudulent general insurance claims totaled GBP 1.16 billion in 2024 as detected cases rose 12% to 98,400, which supports continued investment in screening tools and investigative capability[4]Association of British Insurers, “Fraudulent Insurance Claims Continue to Top £1 Billion,” Association of British Insurers, abi.org.uk. Opportunistic exaggeration and false documentation remain common, while image manipulation raises new verification burdens in fast-turnaround device claims. Insurers clarify documentary expectations at inception and standardize evidence requirements to balance fraud deterrence with a predictable customer journey. Communication quality and channel choice become critical as providers explain why specific checks protect honest policyholders. These steps aim to maintain trust while reducing leakage pressure in the UK electronic gadgets insurance market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coverage Type: Loss Prevention Costs Eclipse Damage Payouts

Accidental damage captured 78.57% of the UK electronic gadgets insurance market share in 2025, while theft and loss is projected to expand at a 10.04% CAGR through 2031. The UK electronic gadgets insurance market size for theft and loss is expected to grow in line with mobility and payment-linked usage, which raises the stakes for speedy replacement. Consumer Duty strengthens attention to value and clarity, which leads to simpler wording on exclusions and more transparent evidence requirements that reduce later disputes. Buyers prioritize fair deductibles, dependable repair logistics, and fast settlement where devices are essential to daily routine. For younger cohorts, added services such as data recovery or premium technical support increase perceived value when comparing budget and full-cover plans. The UK electronic gadgets insurance market benefits when plan structures balance fraud control with prompt claim outcomes in repeat-use categories.

Theft and loss coverage faces distinct risk dynamics linked to commuting, travel, and contactless usage patterns. The CMA reports high contactless adoption across smartphone users, which increases the urgency to disable or replace a device after theft or loss and supports full-cover preference among heavy users. Family and multi-device policies help households cover watches, earbuds, and tablets alongside primary phones under unified claims and limits, which simplifies administration in multi-user settings. Providers refine acceptance criteria and align documentary steps to deter opportunistic claims while maintaining service speed for genuine events. Clear communication on what evidence is needed and when it is required reduces frustration during stressful incidents. These improvements support steadier adoption of full-cover options across the UK electronics gadgets insurance industry.

By Device Type: Mobile Dominance Challenged by Drone Acceleration

Mobile devices accounted for 46.83% of the UK electronic gadgets insurance market share in 2025, while drones are projected to grow at a 12.82% CAGR through 2031. Smartphones remain central to communications, payments, and media, and laptop ownership reached 68% of UK adults in 2024 to 2025, which sustains the largest share of device protection demand. Household contents policies contribute to the baseline by extending protection across belongings used inside and away from home, including mobile phones and student devices at term-time addresses. Student laptop products that publish clear acceptance metrics give budget-sensitive buyers confidence in the claims journey, which encourages uptake in the academic cycle. Platform overlap is common as households manage multiple device types across operating systems and brands, which supports multi-device lists under a single policy. These needs keep mobile and portable computing at the center of the UK electronic gadgets insurance market.

Drones advance as commercial applications expand across inspection and media, which increases the relevance of specialized endorsements and liability coverage for operators. Public liability and equipment protection are core to product selection, and providers add ancillary options to align with diverse use cases and operating profiles. As the regulatory environment continues to emphasize safety and accountability, insurers fine-tune wording to fit real-world workflows and fleet sizes. Some households and micro-enterprises consider multi-device plans where eligibility fits, while commercial operators often prefer dedicated policies with clear liability limits. This pathway keeps the UK electronics gadgets insurance market mobile-led while extending into specialized categories that need tailored protection.

By End Users: Corporate Segment Accelerates Through BYOD Adoption

Individuals represented 90.25% of policies in 2025, while corporate buyers are projected to grow at a 14.57% CAGR through 2031. Device usage spans home and work contexts, which creates demand for policies that cover laptops, phones, and accessories under clear limits and simple claims steps. Insurers respond with business equipment endorsements that explicitly list work tech and specialist cameras, which are practical for SMEs and self-employed professionals. Embedded protection paths at telco and partner channels allow small firms to enroll when purchasing or upgrading devices, which reduces administrative effort and speeds onboarding. For equipment-dependent SMEs, settlement speed and predictable outcomes matter as much as price when incidents interrupt operations. These preferences support a steady runway for corporate and SME uptake in the UK electronic gadgets insurance market.

Cyber exposure and device dependence converge as remote work and SaaS tools remain part of daily operations. The Cyber Security Breaches Survey indicates that 50% of UK businesses experienced breaches or attacks in 2024, with average incident costs of GBP 1,025, which strengthens the case for bundled equipment and cyber options among SMEs and sole traders. Household contents policies that extend to business equipment also support freelancers and students who need protection beyond the home setting. Employers evaluate BYOD arrangements, clarifying responsibilities and insurance coverage to avoid gaps during claims. Clearer disclosures and endorsements reduce ambiguity at the point of sale and at claim time. These shifts support a more nuanced end-user structure within the UK electronic gadgets insurance industry, where consumer-led volumes coexist with faster-growing SME demand.

Geography Analysis

Platform dynamics shape household spending patterns as multi-device ownership grows. CMA findings indicate a 55% iOS share among UK smartphone users with high rates of additional Apple devices, which drives interest in bundled cover and family plans that align with connected ecosystems. Contactless usage is common across iOS and Android, which strengthens the preference for policies that emphasize rapid replacement after loss or theft events. These patterns align with unlimited-device cover options that offer multiple claims per year and defined claim caps that are easy to understand at the point of sale.

Risk signals tied to cyber and fraud influence product structure and verification. The Cyber Security Breaches Survey shows that half of UK businesses faced incidents in 2024, while stand-alone cyber adoption remained limited, which supports bundled paths for SMEs and sole traders who depend on multi-purpose devices. ABI data confirms that detected fraud exceeded GBP 1.16 billion in 2024, which explains why insurers strengthen upfront checks and communicate evidence requirements more clearly. Contents policies that raise personal belongings and business equipment limits contribute to baseline protection for households, students, and small businesses that use devices across locations, adding optionality in the UK electronic gadgets insurance market.

Competitive Landscape

The UK electronic gadgets insurance market is fragmented, with only moderate concentration in telco point-of-sale channels. Telcos and OEM-aligned administrators distribute embedded device protection while general insurers extend coverage through personal belongings and business equipment endorsements, which broadens options beyond standalone plans. Telco offerings differentiate on multi-device eligibility, claim caps, and annual claim counts, as shown by EE’s Multi Tech Cover pricing tiers for damage-only and full loss and theft, with up to five claims per year. For households, the ability to cover phones, laptops, and accessories under one policy resonates with preferences for administrative simplicity and predictable outcomes. For students and budget-minded buyers, clear acceptance criteria and transparent pricing in laptop and phone policies support uptake where repair speed matters. These dynamics favor providers that balance price, settlement speed, and device eligibility across the UK electronic gadgets insurance market.

Technology upgrades support operational efficiency and service quality. Aviva’s rollout of a generative AI summarization tool demonstrates how automation can reduce processing times in complex underwriting workflows and inform similar approaches in claims triage and communications. Likewize benefits from expanded investment capacity following Genstar Capital’s majority stake, supporting AI-driven claims handling and premium technical support across a large volume of device issues. SME-focused intermediaries emphasize speed and clarity, positioning rapid decisions and dependable repair logistics as differentiators for device-reliant businesses. Together, these moves set higher service benchmarks in the UK electronic gadgets insurance market.

Partnership models extend reach at checkout and across verticals. AXA Partners and bolttech announced a long-term collaboration to deliver embedded insurance and assistance solutions across the European Union, the United Kingdom, and Switzerland, targeting carriers, MGAs, reinsurers, and distribution partners in telco, financial services, OEM, and retail segments. Contents providers continue to raise limits and broaden eligible devices to align with modern usage that blends home, school, and work contexts. As Consumer Duty guides clearer disclosures and outcomes measurement, transparency on acceptance, evidence needs, and repair options will remain central to competitive positioning in the UK electronic gadgets insurance market.

UK Electronic Gadgets Insurance Industry Leaders

Axa (Inter Partner Assistance SA)

Aviva Insurance Ltd

Assurant General Insurance Limited

AmTrust Europe Limited

American International Group UK Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: EE launched Multi Tech Cover with Chubb, offering protection for unlimited eligible devices at GBP 15.99 monthly for damage-only and GBP 22.99 for full cover including loss and theft, with up to five claims permitted in any 12-month period. The plan includes phones, tablets, laptops, headphones, smartwatches, e-readers, home security accessories, fitness trackers, gaming consoles, controllers, and VR headsets, aligning with household device mixes.

- September 2025: AXA Partners and bolttech unveiled a long-term strategic partnership to deliver embedded insurance and assistance solutions across the European Union, the United Kingdom, and Switzerland. The collaboration targets carriers, MGAs, reinsurers, and distribution partners spanning telcos, financial services, OEMs, and retail to broaden access to device protection offers at point of sale

- July 2025: AXA UK launched a GBP 2 million academic-industry partnership called AI2: Assurance and Insurance for Artificial Intelligence, in collaboration with the University of Edinburgh, WMG at the University of Warwick, the University of Oxford, and UKRI Prosperity Partnership funding. The project aims to develop novel methods to understand, measure, and insure risks associated with AI in sectors such as transport and healthcare.

- March 2024: Aviva enhanced its Direct Home insurance for new business and renewal by increasing personal belongings cover to GBP 50,000 and business equipment cover to GBP 15,000, with explicit protection for mobile phones and student devices at term-time addresses. The update also raised theft limits from locked outbuildings and student contents limits away from home to better match modern usage patterns.

UK Electronic Gadgets Insurance Market Report Scope

Electronic Gadget insurance covers various gadgets' accidental damage, liquid or water damage, theft, burglary, and fire damage. This insurance covers cell phones, laptops, digital cameras, and other electronic devices. Furthermore, when a customer's gadget is stolen, damaged, or lost, insurance providers pay them. However, the amount varies by coverage. UK Electronic Gadgets Insurance Market segmented by Coverage Type (Physical Damage, Electronic Damage, Data Protection, Virus Protection, and Theft Protection), Device Type (Laptops, Computers, Cameras, Mobile Devices, and Tablets), and End User (Corporate and Individual).

| Accidental Damage |

| Theft and Loss |

| Laptops |

| Computers |

| Cameras |

| Mobile Devices |

| Drones |

| Corporate |

| Individual |

| By Coverage Type | Accidental Damage |

| Theft and Loss | |

| By Device Type | Laptops |

| Computers | |

| Cameras | |

| Mobile Devices | |

| Drones | |

| By End Users | Corporate |

| Individual |

Key Questions Answered in the Report

What is the size and growth outlook for the UK electronic gadgets insurance market by 2031?

The UK electronics gadgets insurance market size is USD 0.71 billion in 2026 and is projected to reach USD 1.07 billion by 2031 at a 9.17% CAGR.

Which coverage options are leading and growing fastest in the United Kingdom?

Accidental damage leads with a 78.57% share in 2025, while theft and loss is the fastest-growing coverage, advancing at a 10.04% CAGR through 2031.

Which device types most influence demand in the United Kingdom?

Mobile devices account for 46.83% in 2025, while drones record the fastest projected growth at a 12.82% CAGR through 2031, supported by contents-based cover and multi-device plans that fit mixed-use settings.

How do regulations shape device protection offerings in 2026?

Consumer Duty requirements emphasize fair value, customer understanding, and outcomes testing, which guide product design, disclosure clarity, and claims governance across providers.

What innovations are most visible across protection products today?

Multi-device plans with defined claim caps and AI-enabled operations in underwriting and claims are prominent, reflected in EE's bundled cover and Aviva's document summarization tool.

How is SME demand evolving across the United Kingdom?

SMEs are adopting equipment endorsements and considering bundled cyber options as half of UK businesses report incidents, with average breach costs that make combined protection paths attractive.

Page last updated on: