Calcium Stearate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

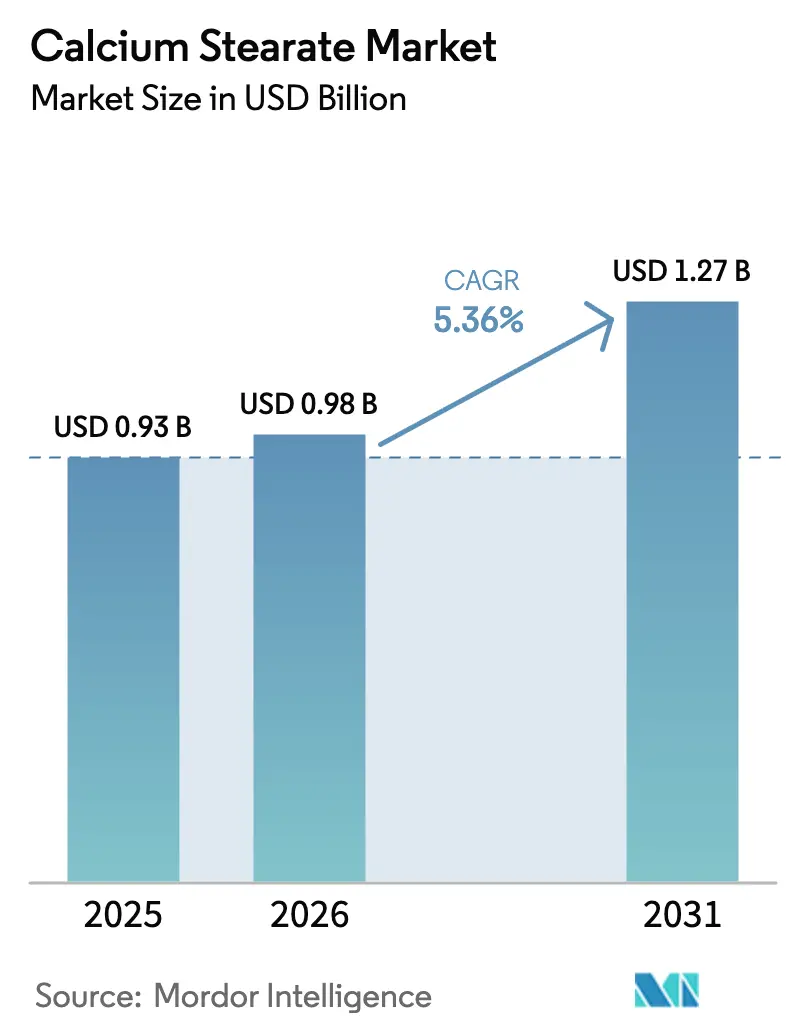

| Market Size (2026) | USD 0.98 Billion |

| Market Size (2031) | USD 1.27 Billion |

| Growth Rate (2026 - 2031) | 5.36% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Calcium Stearate Market Analysis by Mordor Intelligence

The Calcium Stearate Market size was valued at USD 0.93 billion in 2025 and is estimated to grow from USD 0.98 billion in 2026 to reach USD 1.27 billion by 2031, at a CAGR of 5.36% during the forecast period (2026-2031). This growth path is anchored in the transition from toxic-metal stabilizers toward calcium-based systems, stronger demand for moisture-resistant concrete additives in humid regions, and a gradual pivot to vegetable-oil feedstocks to meet brand-owner sustainability pledges. Regulatory ceilings on lead in polyvinyl chloride (PVC), published under Regulation (EU) 923/2023 and effective November 2024, dismantled the economic case for lead stabilizers in Europe, triggering rapid reformulation activity that amplifies demand for calcium stearate, which simultaneously behaves as a heat stabilizer and a lubricant during PVC extrusion. Parallel growth stems from Asia-Pacific infrastructure projects where concrete admixture formulators rely on calcium stearate at 0.5-1.5% cement loading to block capillary pores and fight chloride intrusion, especially in coastal megacities vulnerable to monsoon cycles. In North America, sustainability-conscious brand owners now specify non-palm vegetable derivatives, adding price resilience as buyers accept 10-15% premiums to de-risk supply chains from deforestation exposure.

Key Report Takeaways

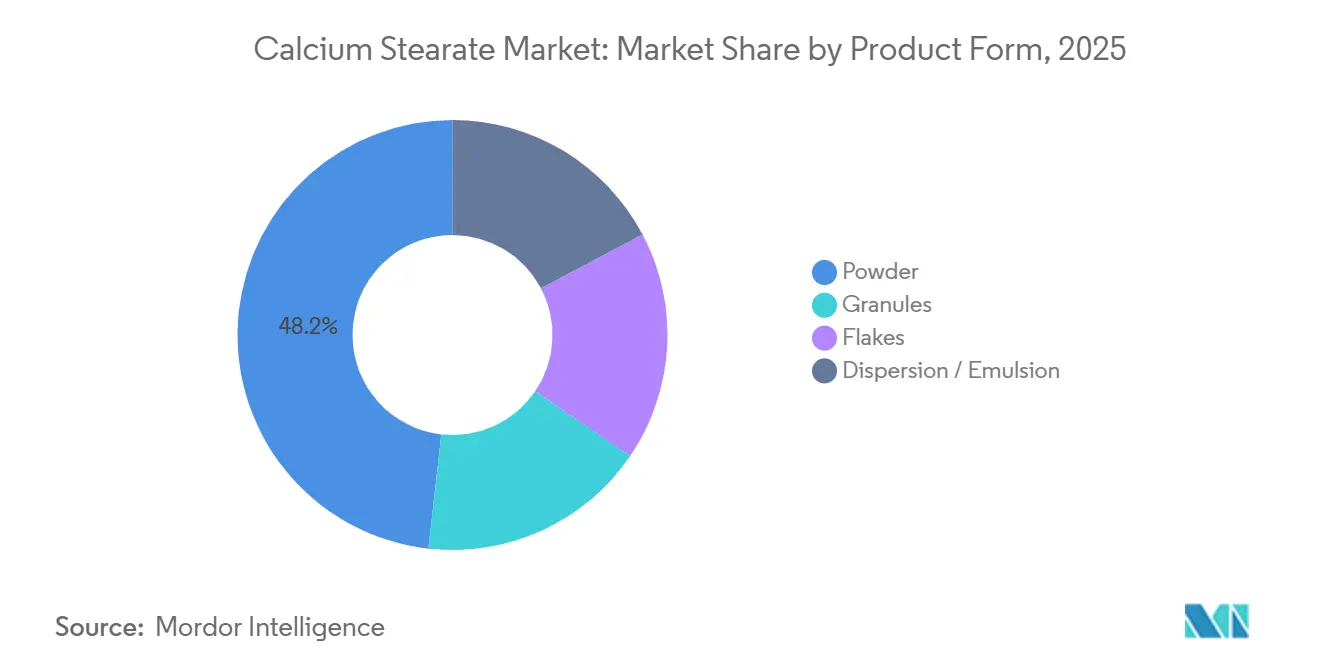

- By product form, powder commanded 48.22% of the Calcium Stearate market share in 2025, whereas granules are advancing at a 5.87% CAGR during the forecast period (2026-2031).

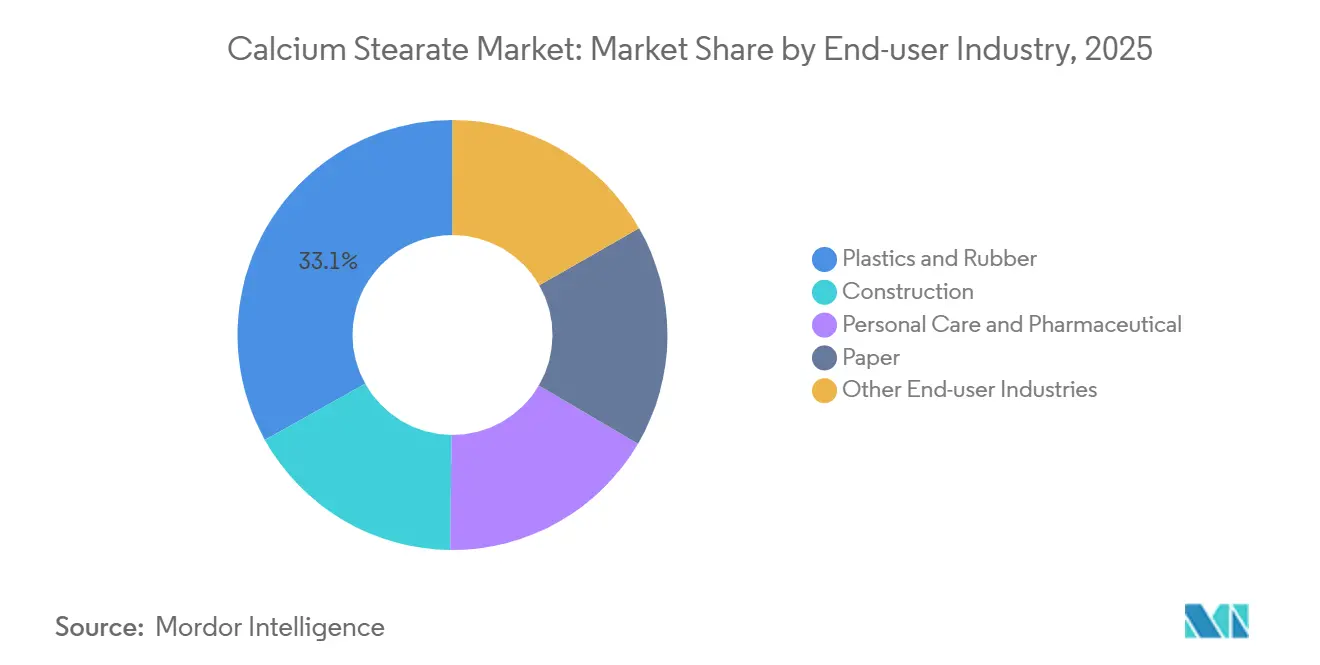

- By end-user industry, plastics and rubber led with 33.11% of the Calcium Stearate market share in 2025, while personal care and pharmaceuticals record the fastest growth at 6.31% CAGR during the forecast period (2026-2031).

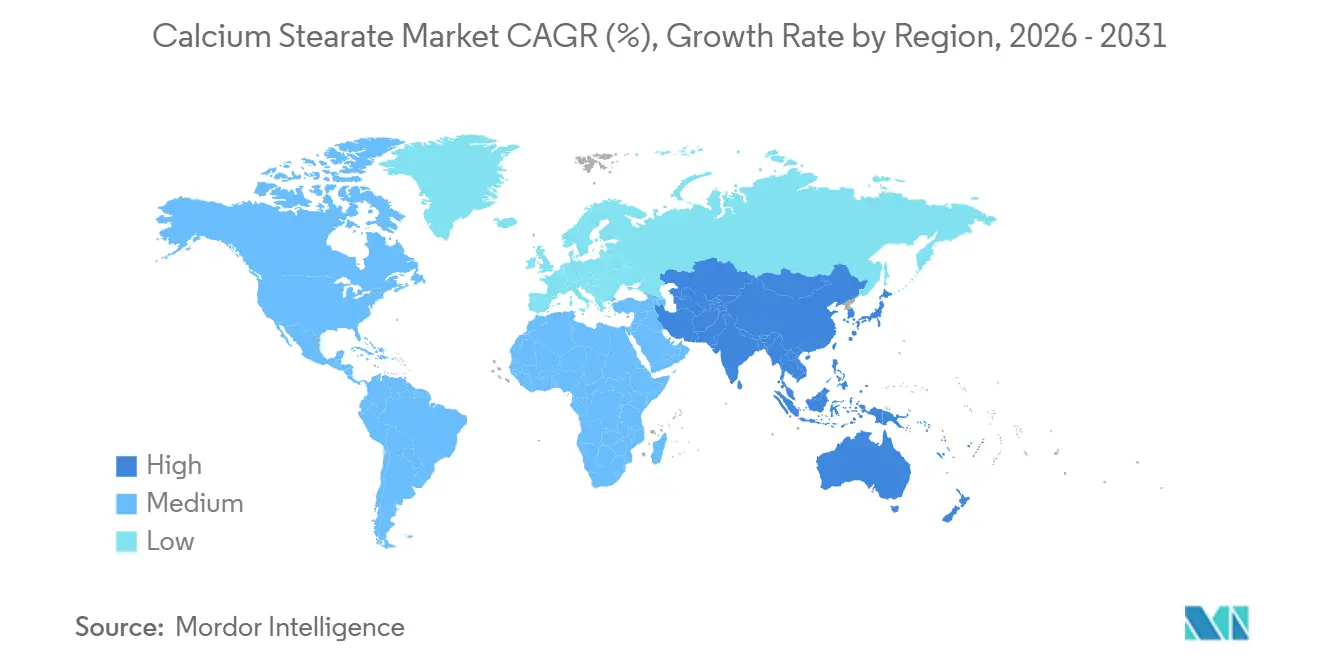

- By geography, Asia Pacific accounted for 44.57% of the Calcium Stearate market share in 2025; the region is projected to expand at a 5.63% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Calcium Stearate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of construction chemicals and concrete additives | +0.8% | Asia-Pacific (China, India, ASEAN), Middle East | Medium term (2-4 years) |

| Switch from lead-based to Ca-based stabilizers | +0.7% | Europe, North America, APAC (regulatory spill-over) | Short term (≤ 2 years) |

| OEM push for dust-free pelletised additives to improve shopfloor health and automation | +0.6% | Global (concentrated in EU, North America, Japan) | Medium term (2-4 years) |

| Growth in solvent-free dispersions for water-borne coatings | +0.5% | North America, Europe, China | Medium term (2-4 years) |

| Food-contact packaging shift to vegetable-oil-derived calcium stearate grades | +0.4% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Construction Chemicals and Concrete Additives

Calcium stearate acts as a hydrophobic pore blocker in concrete. Laboratory trials in South Korea demonstrated that 1 % dosage by cement weight lowered water absorption by 23 % and chloride penetration by 31% after 28 days of curing, benefits that resonate in coastal projects from Jakarta to Chennai[1]Seung-Woo Park, “Hydrophobic Performance of Calcium Stearate in High-Humidity Concrete,” Korea University Journal, korea.ac.kr. Demand intensifies as ASEAN governments channel stimulus into port expansions and elevated highways, creating a virtuous loop between cement manufacturers and admixture blenders. Although the additive’s upfront cost is higher than conventional water-reducers, dual functionality, water repellency, and lubricity shrink total admixture recipes, supporting long-term adoption once ASTM C494 requalification is complete.

Switch from Lead-Based to Calcium-Based Stabilizers

The 0.1 % lead threshold in PVC under Regulation (EU) 923/2023 renders historical lead stabilizers unusable at the loadings necessary for color retention and heat stability. European converters have little buffer inventory and must certify new formulations immediately, propelling calcium-zinc systems with calcium stearate at their core. Major stabilizer vendors have responded: Baerlocher commissioned a low-carbon plant in Dewas, India, during 2023, while its United Kingdom site lifted capacity by over 50% earlier. Spill-over is evident in Mexico and Vietnam, where global OEMs (Original Equipment Manufacturers) unify recipes to streamline procurement audits, raising global calcium stearate uptake.

OEM Push for Dust-Free Pelletized Additives

Automotive and appliance producers aim to curb respirable dust (less than 10 µm) below OSHA’s 5 mg/m³ limit. Granular calcium stearate, spray-dried into 0.4-1.0 mm pellets, exhibits bulk densities around 0.7 g/cm³, improving gravimetric-feeder accuracy to within ±0.5%[2]Occupational Safety and Health Administration, “Permissible Exposure Limits,” osha.gov. Plants shifting from powder to granules report 15-20 % additive waste reduction and 30-40 % quicker color-change cycles, cutting labor downtime and underpinning payback periods of 12-18 months for silo-feeder retrofits.

Growth in Solvent-Free Dispersions for Water-Borne Coatings

VOCs face shrinking thresholds under EPA Method 24 and EU Directive 2004/42/EC. Water-borne coating formulators now adopt 50%-solids calcium stearate emulsions, eliminating the milling step once required for powder soaps. PPG’s CALSAN range has commercialized this path; laboratory benchmarks show equal matting efficiency at 30% lower dosage than solvent-based metallic soaps, trimming raw-material intensity even before rebate credits for VOC compliance. Coating makers, however, need at least 18 months of accelerated weathering before widespread spec-in, hence the medium-term designation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile stearic-acid feedstock pricing | -0.6% | Global (acute in Asia-Pacific, Europe) | Short term (≤ 2 years) |

| Tightening trace-metal limits in high-potency pharma excipients | -0.5% | North America, Europe, Japan | Medium term (2-4 years) |

| ESG-linked loans penalising palm-oil-based supply chains | -0.4% | Global (concentrated in EU, North America) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Stearic-Acid Feedstock Pricing

Palm oil rallied from CNY 7,481 per ton in January 2024 to CNY 10,070 per ton by December, feeding directly into stearic-acid prices with a two-month lag. Given that stearic acid forms about 68% of calcium stearate’s cash cost, gross margins for spot sellers compressed markedly, prompting short production stoppages among small independents in Shandong and Jiangsu. Hedging adoption remains uneven, and many producers lack the credit lines required for long-dated palm-oil futures, heightening earnings volatility.

Tightening Trace-Metal Limits in Pharma Excipients

ICH (International Council for Harmonisation) Q3D places arsenic, cadmium, and lead limits of 1.5, 0.5, and 5 µg/g, respectively, in oral excipients. Meeting these specs obliges producers to add activated-carbon polishing and ion-exchange columns, raising conversion cost by USD 0.50-0.80 per kg. Larger excipient makers can amortize the upgrade, but smaller toll manufacturers struggle, losing bids to vertically integrated suppliers with in-house ICP-MS (Inductively Coupled Plasma Mass Spectrometry) analytics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Granules Gain Ground on Automation Mandates

Roughly 48.22% of the 2025 volume remained powder, reflecting entrenched infrastructure in legacy PVC lines. Yet lights-out molding cells in Germany and Japan now specify pellets to meet ISO 45001 audits. Granular product forms are expected to capture a 5.87% CAGR during the forecast period (2026-2031), overtaking powders, as the calcium stearate market transitions to automated dosing. Flakes persist in rubber internal-mixers but remain niche. Water-dispersions command roughly 25% price premiums thanks to their plug-and-spray convenience for water-borne coatings.

The calcium stearate market share of pelletized forms will therefore climb as OEMs chase dust-free benchmarks. Early adopters confirm 15-20% savings in additive waste, converting directly into lower scrap rates. Equipment suppliers report brisk orders for 40-m³ stainless silos fitted with loss-in-weight screws, evidence that the commercial case is accepted across thermoplastic value chains.

By End-User Industry: Pharma Outpaces Plastics on Purity Demands

Plastics and rubber retained a 33.11% hold on the Calcium Stearate market size in 2025, fueled by PVC window frames and tire inner-liners. Yet the segment’s CAGR settles low as some formulators pivot to zinc stearate or synthetic waxes. By contrast, personal care and pharma will lift their combined share by 2031 on a 6.31% CAGR during the forecast period (2026-2031), sustained by USP-NF (United States Pharmacopeia and the National Formulary) calcium and fatty-acid ratios plus ICH Q3D metal caps. At USD 5-6 /kg, pharmaceutical grades furnish a value pool double that of commodity plastics grades, helping suppliers offset feedstock shocks.

Calcium stearate market share gains also stem from tablet-press makers adopting high-lubricity direct-compress blends. These blends cut punch sticking and raise throughput by 8-10%, a critical metric for continuous-processing lines. Cosmetic formulators likewise favor low-color (less than 2 Lovibond) grades for pressed powders and lipsticks, aligning with dermatological safety dossiers that exclude talc.

Geography Analysis

Asia Pacific dominated the Calcium Stearate market in 2025 at 44.57% and should keep momentum with a 5.63% CAGR during the forecast period (2026-2031). Proximity to Indonesian palm plantations secures stearic feedstock, while India’s National Infrastructure Pipeline advances PVC pipe intakes. Japanese coastal codes mandate admixtures that limit chloride ingress, prompting high-grade calcium stearate admixture usage despite the region’s modest overall construction volume.

Europe’s immediate spike is linked to Regulation 923/2023 lead bans. Over the horizon, PVC substitution by cross-linked polyethylene could temper growth, though food-contact and pharma purity niches reinforce price resilience. North America’s tilt toward soybean-based derivatives alleviates RSPO (Roundtable on Sustainable Palm Oil) penalties and aligns with the United States retailer deforestation pledges.

Latin America and the Middle East each advance at a similar CAGR, paced by civil-works pipelines and nascent pharma clusters. Baerlocher’s Brazil site, expanded in phases since 2013, now exports metal stearates to neighboring countries, showing how a single hub can shape regional supply.

Competitive Landscape

The Calcium Stearate market is highly fragmented. Western leadership lies with Baerlocher, Valtris, and Peter Greven, all backward-integrated into stearic production. Regulatory credentials turn into hard entry barriers. FDA (Food and Drug Administration) GRAS (Generally Recognized As Safe) status, REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) dossiers, and RSPO (Roundtable on Sustainable Palm Oil) supply-chain audits demand rigorous analytical labs.

Calcium Stearate Industry Leaders

Baerlocher GmbH

Valtris Specialty Chemicals

FACI Corporate S.p.A.

PMC Biogenix, Inc.

Peter Greven GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Univar Solutions LLC formed an exclusive North American distribution agreement with Syensqo for beauty care ingredients, expanding its specialty chemicals portfolio. The partnership strengthens its position in personal care markets by enabling integrated solutions that combine calcium stearate with other cosmetic ingredients.

- May 2024: Norac Additives, a Peter Greven GmbH & Co. KG subsidiary, launched a new production line for LIGAFLUID brand calcium stearate dispersions. The company now supplies customers with dispersion grades matching those from its production facilities in Germany and Malaysia.

Global Calcium Stearate Market Report Scope

Calcium stearate is a carboxylate of calcium salt. It is used as a component of some lubricants and surfactants. Calcium stearate is largely utilized in the plastics sector as an acid scavenger, releasing agent, lubricant, waterproofing agent in construction, and anti-caking additive in pharmaceuticals and cosmetics.

The Calcium Stearate market is segmented by product form, end-user industry, and geography. By product form, the market is segmented into powder, granules, flakes, and dispersion/emulsion. By end-user industries, the market is segmented into plastic and rubber, construction, personal care and pharmaceutical, paper, and other end-user industries (food, automotive, paints and coatings, and petrochemicals). The report also covers the market size and forecasts in 16 countries across major regions. For each segment, market sizing and forecasts were made on the basis of value (USD).

| Powder |

| Granules |

| Flakes |

| Dispersion / Emulsion |

| Plastics and Rubber |

| Construction |

| Personal Care and Pharmaceutical |

| Paper |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Form | Powder | |

| Granules | ||

| Flakes | ||

| Dispersion / Emulsion | ||

| By End-user Industry | Plastics and Rubber | |

| Construction | ||

| Personal Care and Pharmaceutical | ||

| Paper | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the calcium stearate market be by 2031?

It is forecast to reach about USD 1.27 billion, advancing at a 5.36 % CAGR from 2026.

Which region leads calcium stearate consumption?

Asia-Pacific accounts for roughly 45 % of global demand, benefiting from stearic-acid feedstock proximity and expanding PVC construction use.

Why are granules growing faster than powder in additive form?

Granules satisfy OEM mandates for dust-free handling, improve feeder accuracy, and reduce waste, driving a 5.87 % CAGR through 2031.

What is the key regulatory trigger for demand in Europe?

Regulation (EU) 923/2023 caps lead in PVC at 0.1 %, compelling a switch to calcium-based stabilizers that rely on calcium stearate.

How does feedstock volatility affect calcium stearate producers?

Stearic-acid price swings, linked to palm-oil markets, compress margins and can prompt smaller converters to idle capacity during spikes.

Page last updated on: