Cable Glands Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

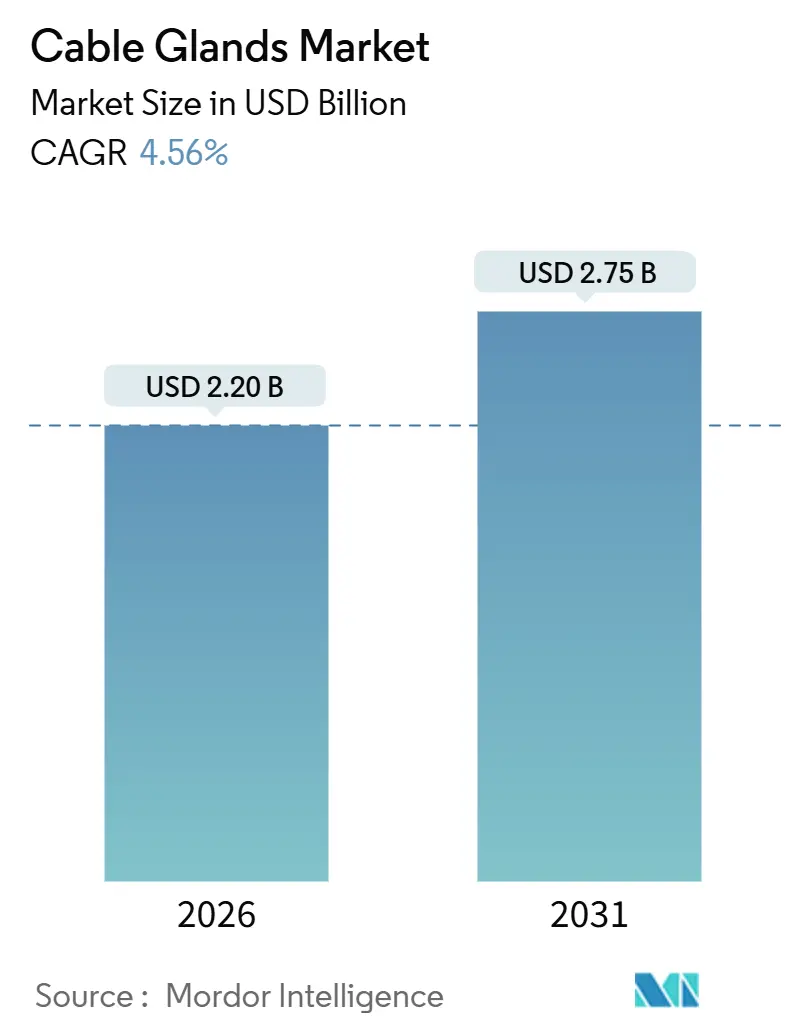

| Market Size (2026) | USD 2.20 Billion |

| Market Size (2031) | USD 2.75 Billion |

| Growth Rate (2026 - 2031) | 4.56% CAGR |

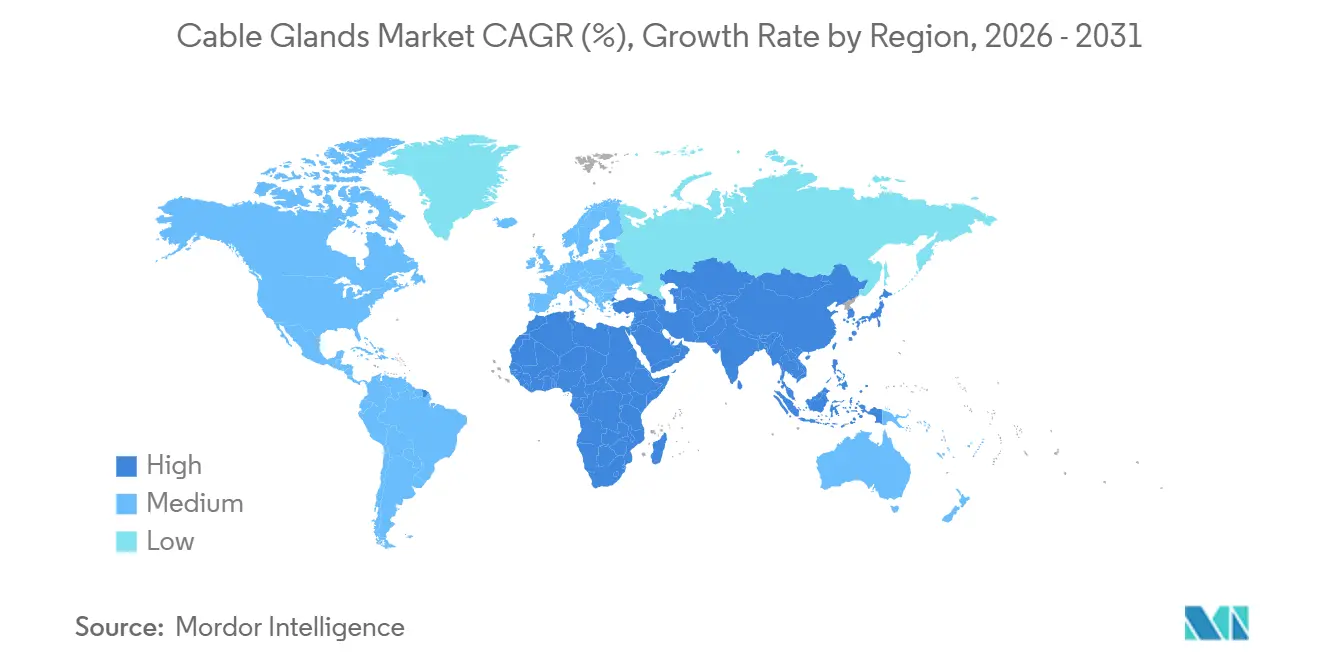

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

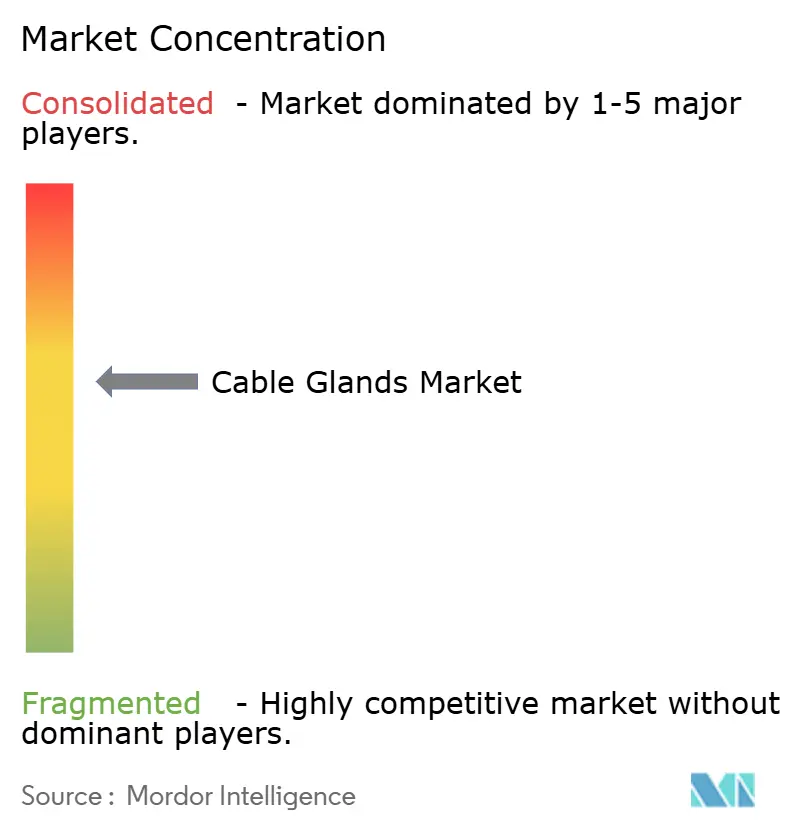

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cable Glands Market Analysis by Mordor Intelligence

The cable glands market size reached USD 2.20 billion in 2026 and is forecast to climb to USD 2.75 billion by 2031, registering a 4.56% CAGR during the period. Grid modernization budgets in North America and Europe, fast-moving manufacturing investments in the Asia-Pacific region, and the rollout of offshore renewable projects are expanding the demand base for certified termination hardware. Utilities are specifying flameproof and increased-safety variants for new transmission lines, while data-center builders are turning to compact multi-cable designs that save rack space and simplify electromagnetic-compatibility compliance. Petrochemical chains in the Middle East and China are adopting dual ATEX and IECEx approvals to align with corporate risk policies, which boosts the revenue mix toward high-margin stainless-steel assemblies. At the same time, tightening ingress-protection rules in food and pharmaceutical plants are accelerating the shift from IP68 to IP69K, opening room for premium-priced, wash-down-ready glands. Competitive intensity remains moderate, yet localized supply, breadth of certification, and rapid prototyping are decisive differentiators in large framework contracts.

Key Report Takeaways

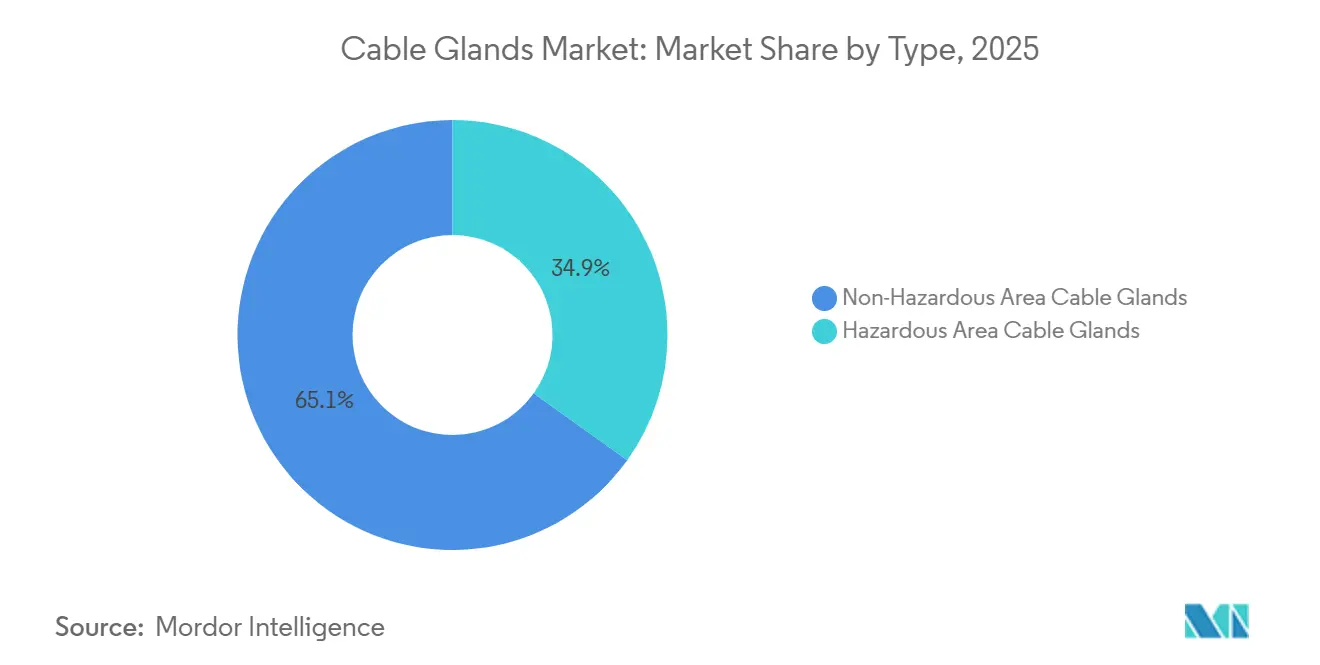

- By type, non-hazardous-area products dominated with 65.10% of 2025 revenue, whereas hazardous-area variants are set to post a 6.30% CAGR to 2031.

- By cable type, armored designs secured 54.20% of 2025 value, while unarmored variants will deliver the fastest 6.10% CAGR thanks to data-center retrofits.

- By material, brass retained 48.30% of 2025 sales, yet stainless steel leads growth at a 4.90% CAGR on offshore wind and marine demand.

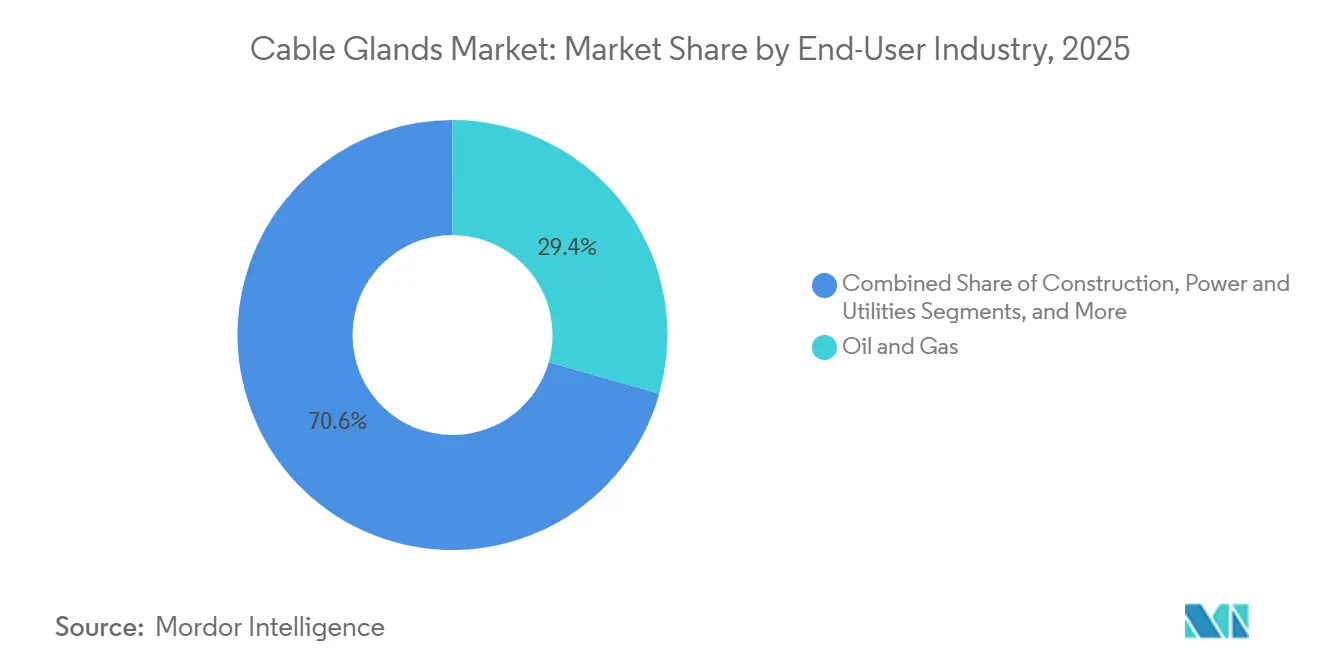

- By end-user industry, oil and gas commanded 29.40% share in 2025, whereas chemicals is projected to expand at a 4.70% CAGR on new petrochemical complexes.

- By ingress-protection rating, IP68 held 36.00% of 2025 turnover, but IP69/IP69K products are poised for a 5.80% CAGR on stringent hygiene codes.

- By thread type, metric threads captured 42.70% of 2025 revenue, while PG threads are on track for a 5.60% CAGR amid Central European machinery exports.

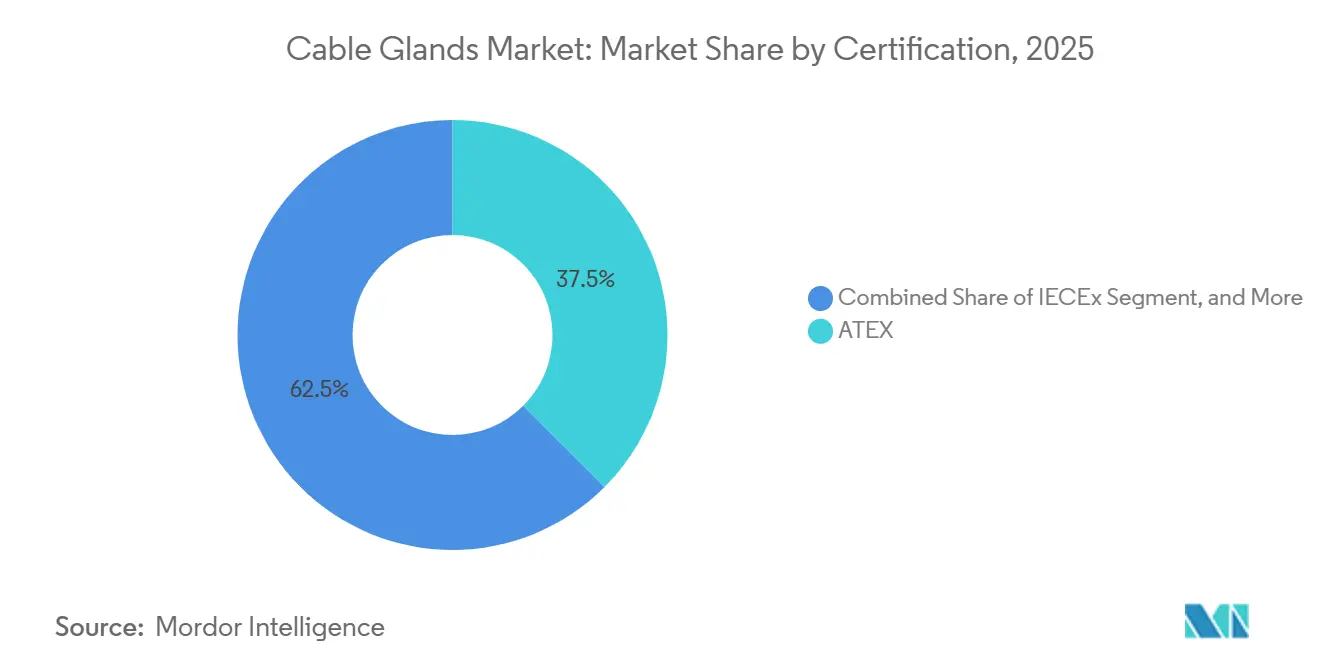

- By certification, ATEX accounted for 37.50% of 2025 revenue, yet IECEx certificates will progress at a 5.20% CAGR as multinationals favor mutual recognition.

- By installation technique, industrial panel mounting delivered 58.00% of 2025 sales, whereas bulkhead and barrier systems will advance at a 6.00% CAGR in modular data centers and offshore platforms.

- By geography, Asia-Pacific led with 38.90% of 2025 revenue and is forecast to grow at a 5.00% CAGR on strong manufacturing FDI inflows.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cable Glands Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Upgrading and Renewal of Legacy Power Networks | +1.2% | North America, Europe, Asia-Pacific urban grids | Long term (≥ 4 years) |

| Surge in Global Construction Activity | +0.9% | Asia-Pacific, Middle East, South America | Medium term (2-4 years) |

| Expansion of Offshore Renewable Energy Installations | +0.8% | Europe, Asia-Pacific, North America | Long term (≥ 4 years) |

| Growth in Manufacturing Investments in Emerging Economies | +0.7% | India, Vietnam, Indonesia, Mexico, Egypt | Medium term (2-4 years) |

| Miniaturization Driven High-Density Data-Center Cabling | +0.6% | Early adoption in North America and Europe | Short term (≤ 2 years) |

| Hydrogen Economy Demands Explosion-Proof Glands | +0.4% | Germany, Netherlands, Saudi Arabia, UAE, Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Upgrading and Renewal of Legacy Power Networks

Transmission and distribution operators are now channeling record budgets into underground cable replacement, substation digitization, and wildfire-mitigation programs. The International Energy Agency values the global grid-renewal requirement at USD 600 billion per year through 2030, and every project specification includes hundreds of glands for circuit entry.[1]International Energy Agency, “World Energy Investment 2024,” iea.org The European Union’s grid action plan earmarks EUR 584 billion for cross-border interconnectors, which mandates ATEX Zone 1 approvals in many switching stations. In the United States, the Department of Energy’s Transmission Facilitation Program provides USD 2.5 billion in loans that call for UL-listed flameproof terminations. Urban utilities are also burying feeders to cut outage risk, a choice that multiplies the number of cable entries per vault and elevates demand for IP69K ingress protection. Prefabricated, skid-mounted substations further streamline supply chains, favoring vendors that can deliver factory-installed glands with full traceability to ISO 9001 standards.

Surge in Global Construction Activity

Rebounding infrastructure spending in emerging economies is driving orders for termination hardware in HVAC panels, elevator drives, and building automation racks. World Bank data show project starts returning to pre-pandemic levels in South and East Asia. India’s National Infrastructure Pipeline schedules massive metro and airport additions, each embedding hundreds of cable entries that must adhere to IEC 60331 fire-survival standards. In Mexico, nearshoring is driving the expansion of industrial real estate, prompting contractors to specify IP66 and IP67 brass glands for use in dusty production halls. Revised European and Gulf building codes now require outdoor-grade ingress protection in indoor wash-down zones, which drives the adoption of stainless-steel IP69K variants. Higher fire-safety expectations also favor glands with integral sealing elements that hold integrity during high-temperature events, nudging buyers toward premium designs despite cost sensitivity.

Expansion of Offshore Renewable Energy Installations

Global offshore wind capacity reached 83 GW in 2024 and is projected to quintuple by 2034, resulting in significant demand for stainless-steel glands that can withstand salt spray, vibration, and UV aging. Germany awarded 7 GW of new leases in the North and Baltic Seas in 2024, specifying IEC 61892 compliance for all electrical penetrations. The United Kingdom’s seabed round in 2025 added 8 GW, stipulating ATEX Zone 1 protections in turbine nacelles. In the Asia-Pacific region, Taiwan’s 20-GW program requires vendors to localize stainless-steel machining in order to meet the lead-time targets set by the Bureau of Energy. Floating platforms destined for water depths beyond 60 m introduce cyclic bending stresses at the entry point, prompting innovation in dynamic-seal technologies that legacy compression fittings cannot match.

Growth in Manufacturing Investments in Emerging Economies

Foreign direct investment of USD 71 billion in India and USD 36.6 billion in Vietnam in 2024 is translating into fresh demand for motor-control centers, programmable logic controller panels, and clean-energy converters. India’s Production-Linked Incentive scheme triggered 32 electronics plants that require both IP68 and ATEX Zone 2 terminations in solvent-handling sections. Multinational battery-cell manufacturers are requesting IECEx-certified IIC glands in cathode-mixing rooms to meet global insurance requirements. As modern factories pursue zero-downtime targets, operators are increasingly specifying modular glands that facilitate rapid field replacement without disrupting neighboring circuits. These orders favor suppliers capable of shipping mixed material lots, brass for dry zones and stainless steel for corrosive work cells, from a single regional warehouse.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmentation of Regional Supplier Base | -0.5% | Asia-Pacific and Africa | Medium term (2-4 years) |

| Volatility in Non-Ferrous Metal Prices | -0.8% | Global | Short term (≤ 2 years) |

| Environmental Rules on Leaded Brass Alloys | -0.3% | North America, Europe | Long term (≥ 4 years) |

| Shift Toward Wireless Sensor Networks | -0.2% | Mining, oil and gas, process industries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmentation of Regional Supplier Base

End users often juggle divergent certification labels, screw threads, and material codes when sourcing glands across multi-country projects. The Asia-Pacific and African markets are especially fragmented, with hundreds of small machine shops supplying unbranded hardware that often lacks cross-border documentation. Engineering, procurement, and construction contractors lose schedule certainty when identical part numbers carry different seismic or flameproof ratings, forcing costly requalification. The absence of universal interchangeability compounds the complexity of maintenance in global asset portfolios.

Volatility in Non-Ferrous Metal Prices

Metal price swings compress margins in product lines where brass, copper, and aluminum account for more than half of the manufacturing cost. International Monetary Fund data showed copper jumping 8.1% between February and August 2024 before moderating. Low-lead brass alloys that meet drinking-water rules trade at a 15-20% premium over C36000, and the premium widens when smelters curtail output during energy spikes. Suppliers are adopting surcharge clauses and bigger hedge books, yet sharp quarterly moves still derail fixed-price framework agreements and slow project award cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hazardous-Area Variants Capture High-Value Hydrogen Projects

Hazardous-area glands are poised to erode the 65.10% share held by non-hazardous designs in 2025, as the cable glands market shifts toward hydrogen electrolyzers, floating LNG units, and advanced refineries that require wide footprints to be classified as Zone 1 or Zone 2.

Demand for non-hazardous glands will continue to grow in absolute volume; however, average selling prices will erode under pressure from plastic substitutes and simplified compression fittings. Original-equipment manufacturers lean on large-volume brass catalogs to shave bill-of-materials costs in low-risk environments. Nevertheless, the emergence of new fire-survival and hygiene codes prompts some specifiers to jump directly from basic IP66 brass to IP69K stainless steel, bypassing mid-tier options and challenging legacy pricing ladders in the cable glands market.

By Cable Type: Unarmored Demand Surges in Space-Constrained Racks

Armored glands preserved 54.20% of 2025 sales, driven by oil, gas, and mining circuits that need armor termination for earth continuity. Yet unarmored devices will log a 6.10% CAGR, fueled by hyperscale data halls where every millimeter of rack space counts. Miniaturized cast-metal bodies with integral EMI gaskets slot neatly into overhead tray layouts, and installers appreciate the quicker torque cycle compared with armor clamping. Data-center builders also value the lower weight of unarmored cable bundles, which reduces the need for ladder-rack reinforcement. These factors collectively swing procurement policies toward compact unarmored SKUs without compromising shielding effectiveness against high-frequency switching noise.

Heavy-industry operators remain loyal to armored glands, notably in the Middle East, where 30-year design lives and sand-storm exposure justify steel-wire or aluminum-tape armor. In these sites, utility crews prefer double-seal designs that maintain ingress protection even after repeated torque checks. The bifurcation thus pits high-volume, low-margin unarmored orders in commercial technology sectors against high-spec, high-margin armored projects in greenfield hydrocarbon complexes, keeping the overall cable glands market balanced but competitive.

By Material: Stainless Steel Climbs on Offshore and Desalination Growth

Brass led materials revenue in 2025, yet stainless steel is outpacing at a 4.90% CAGR as developers pursue corrosion-proof solutions in offshore wind substations, subsea umbilical terminations, and Middle Eastern desalination lines. Grade 316L and duplex alloys withstand chloride attack and stress corrosion cracking, delivering a lower life-cycle cost than brass, despite a higher upfront investment. Additionally, new European recyclability directives favor stainless steel due to its high scrap recovery rate, which provides a sustainability credit in project bids.

Brass persists in indoor switchgear and machine tools due to its unparalleled machinability, which keeps part pricing low in high-volume runs. Nickel-plated aluminum remains a niche option in weight-sensitive rail and aerospace cabins, while plastic glands serve low-voltage sensor loops that have no grounding requirements. Growing environmental pressure to eliminate lead pigments in C36000 brass may further increase machining costs, nudging even conservative buyers toward stainless steel sooner than previously forecast, and reinforcing the premium tier within the cable glands market.

By End-User Industry: Chemicals Segment Accelerates on New Complexes

Oil and gas dominated demand with 29.40% share in 2025, but chemicals plants stand out with a projected 4.70% CAGR. Integrated ethylene-to-polyethylene complexes in Saudi Arabia, the UAE, and coastal China require thousands of stainless-steel glands approved for hydrogen sulfide and high-temperature solvents. The weight of capital is shifting toward value-added intermediates and specialty derivatives, each of which demands Zone 1 flameproof equipment. Insurers often insist on dual ATEX and IECEx marks, a requirement that filters out low-tier suppliers and supports higher margins.

Utility, mining, marine, and aerospace orders remain steady, though each follows unique specification dialects that limit part commonality. Power utilities are retrofitting flood-prone substations with IP69K stainless-steel entries, whereas aircraft builders favor anodized-aluminum bodies meeting AS85049. As the chemicals boom plays out, it reconfigures the regional sales mix, anchoring an enlarged premium segment within the cable glands market.

By Ingress Protection Rating: IP69K Becomes the Hygiene Benchmark

IP68 dominated 36.00% of 2025 turnover, yet IP69/IP69K will post a 5.80% CAGR as regulators and brand owners tighten sanitation protocols in food and pharma packaging halls. DIN 40050-9 water-jet tests at 80 °C validate glands for caustic-foam clean-downs, cutting microbial risk. Equipment exporters to the European Union and the United States embed IP69K glands to streamline market access, and Asian producers emulate the requirement to win co-packing contracts from multinational brands. Modular seal inserts now enable field upgrades from IP66 to IP69K, reducing installer inventory but increasing unit price.

Traditional IP66 and IP67 brass bodies will maintain a foothold in indoor industrial cabinets, although some specifiers skip directly to IP69K once they factor in the total cost of cleaning downtime. That leap further enlarges the premium layer of the cable glands market and encourages suppliers to refine machining tolerances that deliver repeatable jet-spray resistance.

By Thread Type: PG Retains Foothold in Central Europe

Metric threads anchored 42.70% of 2025 revenue through ISO standardization across Asia, Southern Europe, and much of South America. PG threads nevertheless secure a 5.60% CAGR, driven by Germany’s vast installed base. Machine builders in Baden-Württemberg and Bavaria ship equipment with DIN 40430 knockouts, obliging maintenance crews worldwide to stock matching glands. Export momentum in plastic extrusion, packaging, and automotive assembly lines keeps PG specifications alive.

Meanwhile, ANSI NPT threads dominate U.S. and Canadian oilfield hardware, and BSP threads persist in the United Kingdom and Australia. Multinational vendors answer this diversity by machining multi-thread inventory from shared billet stock, encouraging economies of scale even amid SKU proliferation in the cable glands market.

By Certification: IECEx Emerges as the Preferred Global Passport

ATEX accounted for 37.50% of 2025 turnover within the European Economic Area, but IECEx certificates are expected to grow at 5.20% as project owners seek a single test suite that unlocks multiple regions. The publicly searchable IECEx database of equipment and manufacturing sites streamlines due diligence checks for engineering firms. Suppliers achieve cost savings by running a single destructive test program and then layering on regional label printing for UL or CSA, where required by law.

North American buyers still demand UL 1203 or CSA C22.2 approvals; however, they often accept an IECEx test report as evidence of baseline conformity. As more regulators reference IEC standards directly, the gravitational pull toward IECEx gathers pace, positioning it as the default baseline for new product development within the cable glands market.

By Installation Technique: Bulkhead Systems Win in Modular Builds

Industrial panel mounting captured 58.00% of the 2025 value, but bulkhead and barrier systems are expected to rise at a 6.00% CAGR, as modular data-center containers and offshore platforms increasingly favor pre-certified multi-cable transits. These frames seal multiple conductors through a single opening while maintaining fire, smoke, and water integrity in accordance with UL 2225 or IEC 60092-101. Factory integration slashes on-site labor and eliminates the risk of field mis-torque.

Direct equipment entry remains popular for pumps, motors, and instruments where a junction box would add cost and volume. Even so, the push for compartmentalized fire zones in lithium-ion battery plants and floating LNG hulls steers engineers toward bulkhead modules, reinforcing the premium diversification inside the cable glands market.

Geography Analysis

The Asia-Pacific region generated 38.90% of 2025 revenue and is tracking a 5.00% CAGR, as India, Vietnam, and Indonesia welcome record electronics and automotive investments. India’s Production-Linked Incentive scheme alone triggered 32 new factories that rely on metric-thread stainless-steel IP68 glands in solvent areas. China is adding over 10 million t per year of ethylene equivalent on the coast, requiring dual-certified flameproof terminations compliant with GB 3836 guidelines. Japan and South Korea are rolling out hydrogen refueling corridors that specify IECEx-listed equipment, further raising Asia-Pacific’s premium mix in the cable glands market.

Europe benefits from a strong offshore wind pipeline and stringent ATEX enforcement. The European Commission’s EUR 584 billion grid plan funnels stainless-steel orders into Baltic interconnectors, while Germany’s 7-GW auction in 2024 codified IEC 61892 ingress rules for all turbine decks.[2]European Commission, “EU Grid Action Plan,” europa.eu The United Kingdom’s Crown Estate adds to momentum with 8 GW of new seabed leases slated for completion after 2028. These developments secure long visibility for explosion-proof gland suppliers and boost average selling prices across the region.

North America rides a dual narrative: data-center megaprojects in Virginia, Texas, and Quebec order compact multi-cable glands with EMI shielding, while grid resilience funds support UL-listed flameproof entries in high-voltage rebuilds. Mexico’s nearshoring wave spurs PG and metric demand in assembly corridors along the Bajío region. The Middle East commands outsized project values in petrochemicals, notably the Jafurah gas complex and Ghasha sour-gas field, each specifying stainless-steel, dual-certified glands for Zone 1 areas. Africa and South America exhibit smaller bases but demonstrate healthy growth tied to mining and renewable energy concessions, underscoring a diversified geographic runway for the cable glands market.

Competitive Landscape

The top 10 suppliers account for roughly 45-50% of global revenue, positioning the cable glands market in a moderately concentrated tier. Multinationals such as ABB, Eaton, and Amphenol leverage broad certification portfolios, regional machining hubs, and digital configurators to win multi-country tenders. Eaton’s 2024 acquisition of Cobham Mission Systems enhances its aerospace cable-management expertise, which may cross-pollinate industrial gland innovation.[3]Eaton Corporation, “Cobham Mission Systems Acquisition,” eaton.com Amphenol reported a 16% year-over-year sales increase in Q3 2024, capturing high-density data center projects that favor miniaturized, EMI-screened glands.

Regional specialists, CMP Products, Hummel, Warom Technology, and Roxtec, differentiate through rapid certification cycles and customization. Roxtec’s additive-manufactured prototypes cut lead time for bespoke bulkhead seals to days, a decisive advantage in offshore retrofits. Meanwhile, Chinese producers offer cost-competitive metric brass glands but face acceptance barriers in ATEX projects due to limited audit trails. Sustainability credentials are emerging as a tender differentiator, pushing suppliers to report recycled-metal content and to substitute low-lead alloys in drinking-water zones. Integrated condition-monitoring sensors and one-turn installation mechanisms represent white-space opportunities as end-users seek predictive maintenance and lower field labor costs.

Supply chain resilience remains under scrutiny following 2024 freight disruptions; vendors with dual-continent machining backups captured a share when transit times from East Asia spiked. Given the mix of premium offshore orders and commoditized commercial demand, strategic partnerships between stainless-steel foundries and global distributors are expected to intensify over the forecast window.

Cable Glands Industry Leaders

CMP Products Limited

ABB Ltd

Eaton Corporation plc (Cooper Crouse-Hinds)

Hubbell Incorporated

Amphenol Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: ABB launched the BW Series modular stainless-steel IP68 and IP69K glands, claiming 30% faster installation for cleanroom machinery.

- November 2025: ABB released ATEX Zone 1 and IECEx IIC glands with integral pressure-relief to mitigate hydrogen embrittlement at refueling stations.

- August 2025: ABB rolled out miniaturized, EMI-screened cable glands for hyperscale data halls, delivering 30% size savings compared to legacy housings.

- June 2025: Amphenol introduced the GuardXcel stainless-steel IP69K gland family for offshore wind and marine deployments.

Global Cable Glands Market Report Scope

Cable glands can broadly be defined as mechanical fittings that form a part of electrical installation systems. They enable high levels of barrier protection and insulation. These systems are used in conjunction with power cables, wires, and probes. The primary purpose of these systems is to seal cables and maintain the ingress protection of enclosures. The Cable Glands Market Report is Segmented by Type (Non-Hazardous Area Cable Glands, Hazardous Area Cable Glands), Cable Type (Armored Cable Glands, and More), Material (Brass, and More), End-User Industry (Mining, and More), Ingress Protection Rating (IP66, and More), Thread Type (PG, and More), Certification (UL, and More), Installation Technique, and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Non-Hazardous Area Cable Glands |

| Hazardous Area Cable Glands |

| Armored Cable Glands |

| Unarmored Cable Glands |

| Brass |

| Aluminium |

| Stainless Steel |

| Plastic |

| Rest of Materials |

| Oil and Gas |

| Power and Utilities |

| Manufacturing and Processing |

| Construction |

| Aerospace |

| Marine |

| Mining |

| Chemicals |

| IP66 |

| IP67 |

| IP68 |

| IP69/IP69K |

| Metric |

| PG |

| NPT |

| BSP |

| ATEX |

| IECEx |

| UL |

| CSA |

| Other Certifications |

| Industrial Panel Mounting |

| Direct Equipment Entry |

| Bulkhead and Barrier Systems |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Type | Non-Hazardous Area Cable Glands | |

| Hazardous Area Cable Glands | ||

| By Cable Type | Armored Cable Glands | |

| Unarmored Cable Glands | ||

| By Material | Brass | |

| Aluminium | ||

| Stainless Steel | ||

| Plastic | ||

| Rest of Materials | ||

| By End-User Industry | Oil and Gas | |

| Power and Utilities | ||

| Manufacturing and Processing | ||

| Construction | ||

| Aerospace | ||

| Marine | ||

| Mining | ||

| Chemicals | ||

| By Ingress Protection Rating | IP66 | |

| IP67 | ||

| IP68 | ||

| IP69/IP69K | ||

| By Thread Type | Metric | |

| PG | ||

| NPT | ||

| BSP | ||

| By Certification | ATEX | |

| IECEx | ||

| UL | ||

| CSA | ||

| Other Certifications | ||

| By Installation Technique | Industrial Panel Mounting | |

| Direct Equipment Entry | ||

| Bulkhead and Barrier Systems | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What value will cable gland sales reach by 2031?

Global revenue is projected to rise to USD 2.75 billion by 2031, up from USD 2.20 billion in 2026.

Which geographic region currently buys the largest share of cable glands?

Asia-Pacific generated 38.90% of global 2025 revenue and is forecast to advance at a 5.00% CAGR through 2031.

Why are IP69K-rated products becoming popular in food and pharma facilities?

High-pressure wash-down rules under DIN 40050-9 require equipment to survive 80 °C jets at 80–100 bar, so engineers favor stainless-steel IP69K glands that resist water ingress and chemicals.

How do hazardous-area products compare in price to standard non-hazardous units?

Explosion-proof or increased-safety designs typically command 50–100% premiums because of dual ATEX and IECEx testing, flame-path machining, and stainless-steel construction.

Which material segment is expanding fastest?

Stainless steel is growing at a 4.90% CAGR thanks to offshore wind, marine, and desalination projects that demand superior corrosion resistance.

What makes IECEx certification attractive to multinational EPC contractors?

A single IECEx test report unlocks access to 37 member economies, reducing duplicate testing costs while still allowing local labeling for UL or CSA where required.

Page last updated on: