Polyarylsulfone Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

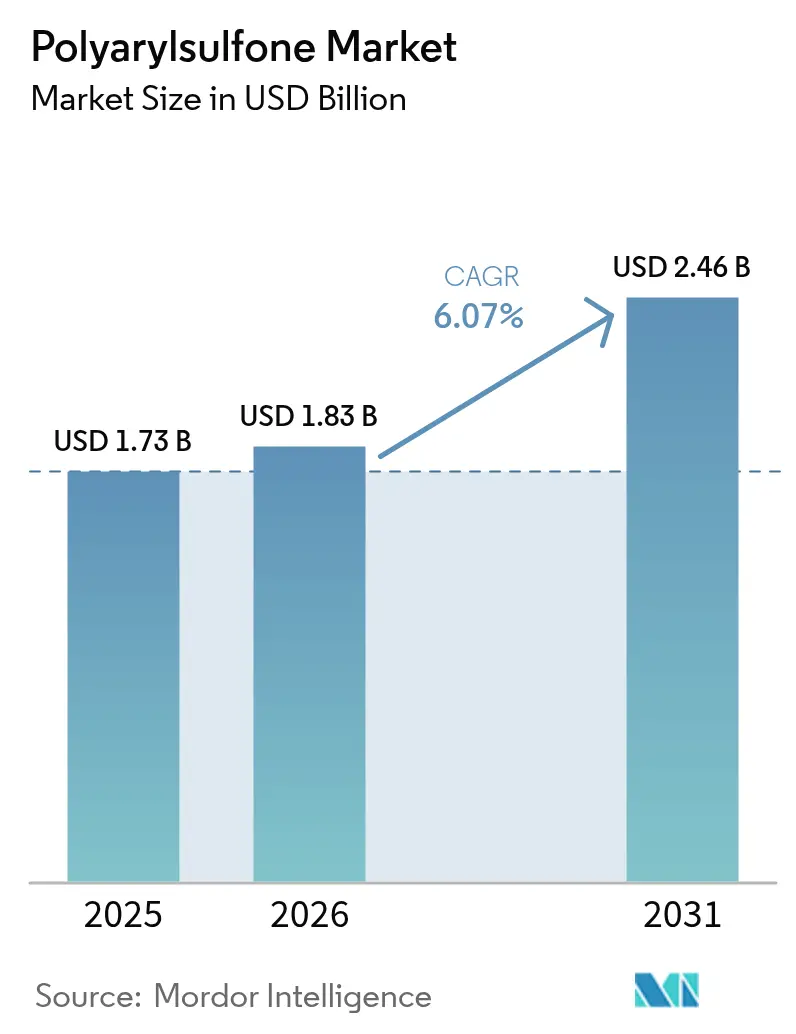

| Market Size (2026) | USD 1.83 Billion |

| Market Size (2031) | USD 2.46 Billion |

| Growth Rate (2026 - 2031) | 6.07% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyarylsulfone Market Analysis by Mordor Intelligence

Polyarylsulfone market size in 2026 is estimated at USD 1.83 billion, growing from 2025 value of USD 1.73 billion with 2031 projections showing USD 2.46 billion, growing at 6.07% CAGR over 2026-2031. Demand growth mirrors the wider shift toward lightweight, high-temperature polymers that substitute metals without sacrificing mechanical strength. Medical device makers are scaling adoption because the FDA’s 21 CFR 177.1560 regulation authorizes polyarylsulfone resins for food contact at normal baking temperatures, which validates their sterility and chemical inertness. In parallel, electric-vehicle suppliers favor the material’s dimensional stability for battery pack components, while semiconductor tool builders value its solvent resistance in plasma etching chambers. Leading producers leverage integrated petrochemical assets to offset bisphenol-A price swings, and most have announced ISCC Plus or mass-balance grades to satisfy sustainability audits. The polyarylsulfone market therefore occupies a strategic middle ground between commodity engineering polymers and ultra-exotic resins.

Key Report Takeaways

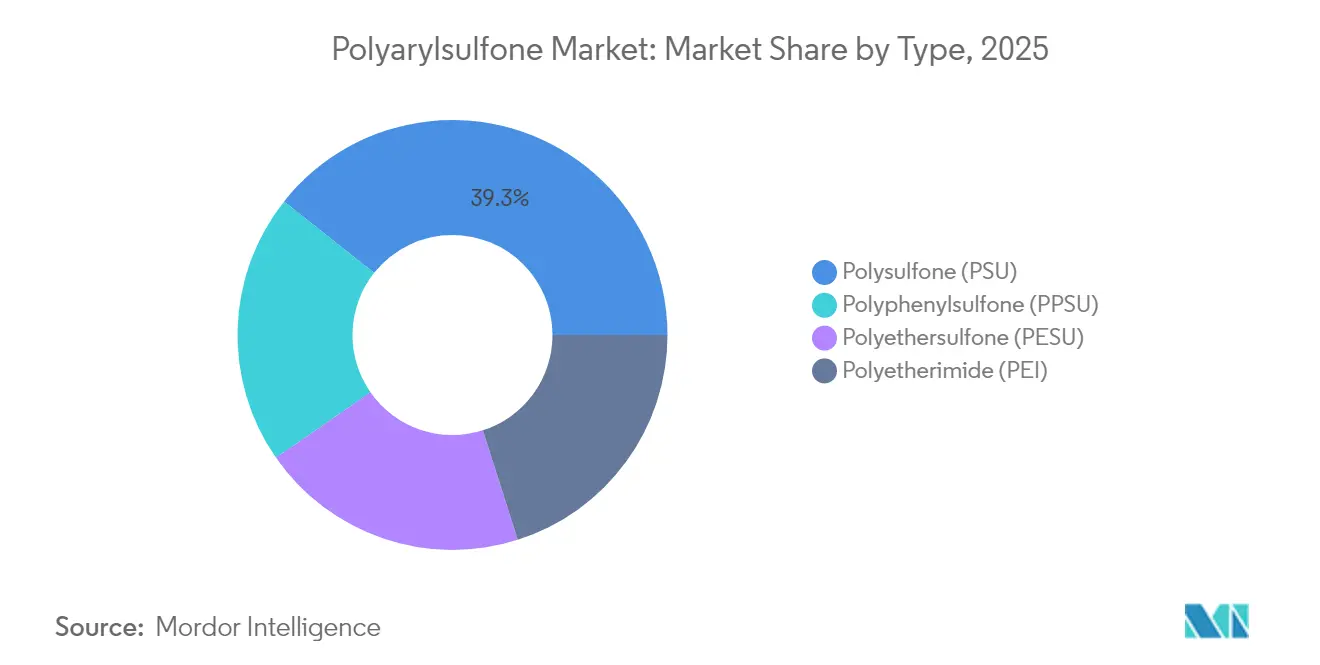

- By type, polysulfone led with 39.33% of the polyarylsulfone market share in 2025, whereas polyphenylsulfone is projected to expand at a 6.63% CAGR through 2031.

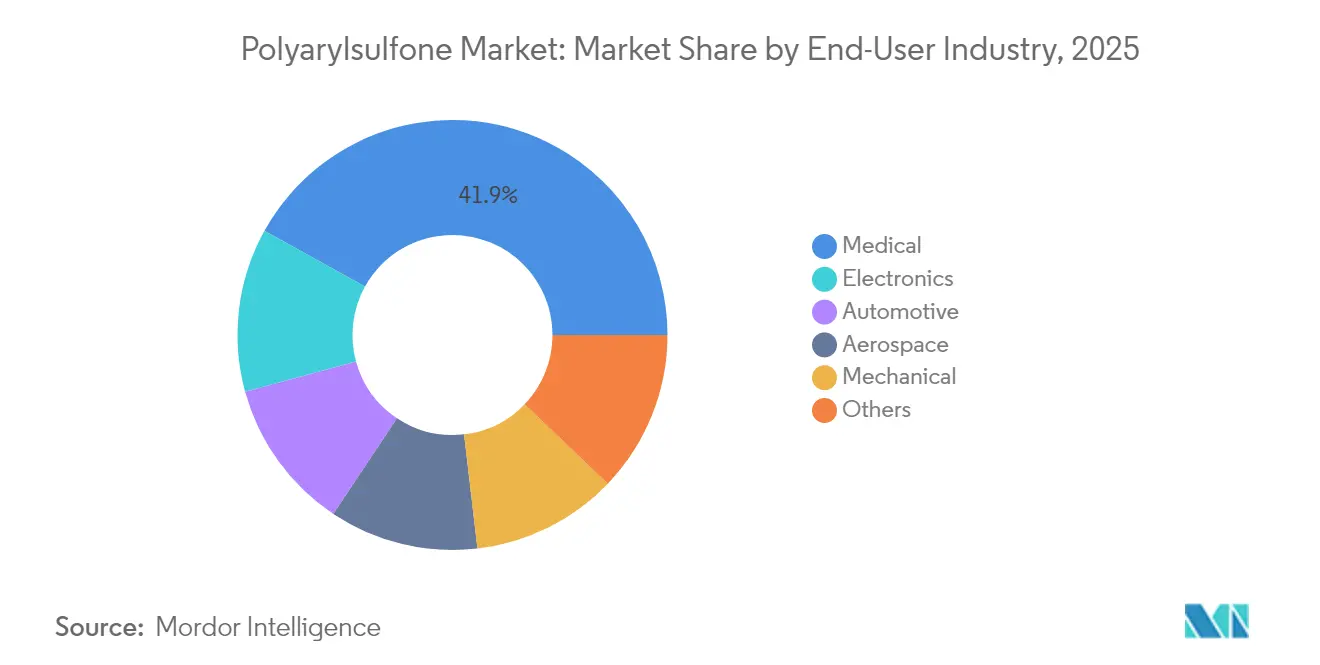

- By end-user industry, medical devices accounted for 41.95% of the polyarylsulfone market size in 2025, while electronics is poised to grow at a 6.52% CAGR to 2031.

- By geography, Asia Pacific captured 41.85% of global revenue in 2025; the region is expected to post the fastest 7.25% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polyarylsulfone Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid lightweight-ing push in EV & e-mobility platforms | +1.80% | Global, with early gains in China, Europe, North America | Medium term (2-4 years) |

| Medical OEM pivot toward reusable, steam-sterilizable components | +1.50% | Global, concentrated in North America & Europe | Short term (≤ 2 years) |

| Membrane retrofits in industrial & municipal water treatment | +1.20% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Mainstream shift from metals to high-performance polymers in aerospace interiors | +0.90% | North America & EU | Medium term (2-4 years) |

| Rising demand for solvent-resistant housings in next-gen semiconductor tools | +0.80% | APAC core, with expansion to North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Lightweighting Push in EV & E-mobility Platforms

Electric-vehicle producers are using polyarylsulfone in battery enclosures that demonstrate 20% weight reduction versus conventional aluminum housings, a milestone shown in SABIC’s multi-material pack program[1]SABIC, “Advanced Battery Pack Enclosures,” sabic.com . The polymer’s heat-deflection temperature allows thin-wall structures that survive thermal runaway events, while intrinsic chemical resistance shields components from electrolyte spills. Tier-1 suppliers highlight tooling productivity gains because complex geometries can be injection-molded in one shot, lowering assembly cost. Automakers also exploit the resin’s dielectric strength to design integrated cooling plates that double as electrical insulators. As pack energy density rises, these combined advantages translate into longer driving range, reinforcing adoption momentum.

Medical OEM Pivot Toward Reusable, Steam-Sterilizable Components

Hospitals are shifting from single-use to reusable surgical sets to reduce per-procedure expenditure by up to 60%, and polyarylsulfone meets repeated autoclave cycles without loss of clarity or toughness. ISO 10993-1 biocompatibility clearance for Udel PSU and Radel PPSU simplifies device registration in the United States and European Union. Instrument suppliers now specify transparent grades so clinicians can visually inspect internal channels, cutting downtime linked to hidden contamination. Pigmented variants for color-coded trays streamline workflow and lower identification errors in the operating room. With health systems pursuing both cost containment and sustainability, demand from surgical tools, sterilization cases, and dental equipment remains robust.

Membrane Retrofits in Industrial & Municipal Water Treatment

Ageing ultrafiltration lines are being upgraded with polyarylsulfone-based hollow fibers that hit 99% removal rates for selected PFAS contaminants. The material tolerates sodium hypochlorite and caustic cleans without cracking, stretching replacement intervals to five years in municipal service. Researchers have boosted flux by grafting hydrophilic nanomaterials onto the polymer backbone, generating composite membranes that water utilities can slot into legacy housings with minimal retrofit expense[2]Royal Society of Chemistry, “Nanocomposite Sulfone Membranes,” rsc.org . These performance gains arrive as APAC governments tighten discharge norms, unlocking a long-duration growth runway.

Mainstream Shift from Metals to High-Performance Polymers in Aerospace Interiors

Thermoplastic fuselage demonstrators under CleanSky 2 achieved 20–30% CO₂ reductions relative to today’s structures by substituting polyarylsulfone composites for aluminum frames. Airlines value cabin parts that satisfy FAR 25.853 fire-smoke-tox requirements while trimming weight and easing MRO inspections. The polymer’s fracture toughness resists fatigue over thousands of pressurization cycles, cutting life-cycle costs. Emerging conductive grades also provide electromagnetic interference shielding without metallic inserts, helping airframers meet next-generation avionics compatibility targets. These attributes align with aerospace electrification trends, placing the polymer on qualified material lists for interior monuments and cable conduits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile bisphenol-A & diphenylsulfone prices | -1.20% | Global, with acute impact in APAC | Short term (≤ 2 years) |

| Delayed regulatory approvals for food-contact grades | -0.80% | North America & EU | Medium term (2-4 years) |

| Recycling infrastructure gap for high-temperature thermoplastics | -0.60% | Global, most pronounced in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Bisphenol-A & Diphenylsulfone Prices

Feedstock volatility narrows producer margins because bisphenol-A spot prices swing with benzene and phenol supply cycles. California’s listing of bisphenol S as a reproductive toxicant adds uncertainty, prompting formulators to resource-shift or requalify grades at extra cost. Contract hedging only partially offsets price spikes, so processors push surcharges downstream, raising finished good pricing and dampening substitution in cost-sensitive sectors. Vertical integration helps majors absorb shocks; however, independent compounders face inventory-finance strain during up-cycles.

Delayed Regulatory Approvals for Food-Contact Grades

Although 21 CFR 177.1560 covers baseline resins, any colorant or recycled-content variant triggers fresh extractables testing that can extend to 24 months[3]U.S. Food & Drug Administration, “Food-Contact Notification Program,” fda.gov . Smaller suppliers lacking in-house toxicology teams must outsource dossiers, inflating development budgets. Multinational brand owners avoid unapproved materials to protect supply-chain continuity, so commercial roll-out lags technical readiness. This bottleneck especially restricts adoption in baby-care articles and industrial bakeware, where compliance evidence remains paramount.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Performance Differentiation Guides Purchasing Decisions

Polysulfone segment captured 39.33% of the global market share in 2025, emphasizing its significant contribution to overall revenue. Medical, filtration, and aerospace programs lean on PSU’s well-documented datasheets, which limit qualification time. Producers emphasize melt-flow consistency that supports multi-cavity tooling, and this reliability keeps cost-of-quality low for high-volume disposables. Meanwhile, supply-chain alliances between resin makers and compounders bring pre-colored PSU pellets directly to device molders, eliminating masterbatch steps.

Polyphenylsulfone commands premium pricing yet is on track to outpace every other grade at a 6.63% CAGR by 2031. PPSU’s impact strength allows thinner battery module frames than PEI or PEEK can deliver at comparable cost. Syensqo cites a 207 °C heat-deflection rating that safeguards under-hood brackets near turbochargers while absorbing vibration without micro-cracks. Polyethersulfone, in contrast, targets membrane casting and transparent lab ware, offering a cost-performance midpoint that appeals to price-sensitive Asian OEMs. Collectively, these differentiated value propositions lock in long-term offtake agreements and deter commoditization.

By End-User Industry: Healthcare Provides Scale; Electronics Delivers Momentum

Medical accounted for 41.95% of the polyarylsulfone market in 2025. Autoclave compatibility enables forceps, sterilization trays, and hemodialysis components that survive 1,000 steam cycles, giving hospitals confidence to amortize capital goods across multiple fiscal years. Transparency supports visual inspection and fosters photonic biosensors integrated into lab-on-chip devices, expanding addressable use cases. In orthopedics, radiolucent trial implants simplify intraoperative imaging, lowering radiation exposure for staff and patients alike.

Electronics are projected to achieve the highest growth, registering a notable 6.52% CAGR by 2031. Semiconductor OEMs specify PPSU and PESU housings for dry-etch chambers because the resins endure fluorine plasmas that etch metals within minutes. BASF’s new high-flow Ultrason D 1010 G6 U40 ensures consistent fiber-glass wet-out, allowing tight-tolerance flanges that seal against vacuum leaks. Consumer devices also embed polyarylsulfone into USB-C power adapters where thin walls must pass glow-wire tests at 850 °C. As IoT demand rises, enclosure suppliers appreciate the polymer’s inherent flame retardancy, eliminating halogenated additives and simplifying end-of-life recycling.

Geography Analysis

Asia Pacific held 41.85% of the polyarylsulfone market share in 2025, supported by China’s 5.48 million t/y bisphenol-A capacity and regional government incentives for high-tech plastics. Local converters integrate vertically from BPA to sulfone monomers, compressing conversion costs and shortening lead times to electronics and EV clusters. Japanese producers refine ultra-high-purity grades for surgical lighting lenses and semiconductor quartz replacements, reinforcing the region’s advanced-manufacturing pedigree. Supply-chain concentration, however, exposes Western OEMs to geopolitical risk, prompting dual-sourcing strategies with Korean and Indian suppliers.

North America remains a value-added hub focused on FDA-cleared medical disposables and FAA-certified aerospace interiors. Resin producers invest in compounding plants near major med-tech corridors in Minnesota and Massachusetts, cutting transit carbon. OEM preference for recycled content pushes suppliers to pilot solvent-based depolymerization that reclaims monomers at 95% yield. Federal procurement policies tied to Buy American clauses may accelerate localized capacity, cushioning the market from Asian supply disruptions.

Europe’s policy mix balances REACH chemical scrutiny with circular-economy targets. German automakers embed polyarylsulfone in thermal-management manifolds for battery electric vehicles, aiming to halve component weight versus aluminum. Continental water utilities retrofit hollow-fiber membranes to comply with the Drinking Water Directive’s stricter PFAS limits, and EU recovery funds earmarked for green infrastructure underpin volume growth. Eastern Europe offers cost-competitive molding, drawing inward investment from Western compounders seeking tariff-free access to the single market.

South America and the Middle East & Africa trail in volume but show double-digit demand in water treatment and oil-gas applications. Governments favor durable membranes to offset capital constraints, and climate-driven droughts make desalination capacity urgent. Gulf-region petrochemical majors evaluate backward-integration into sulfones, leveraging existing phenol production, which could shift global trade flows post-2027 if projects proceed.

Regulatory Landscape

Polyarylsulfone adoption in food-contact and adjacent medical processing applications is shaped by product-specific frameworks in the United States and a tightening compliance environment in Europe. In the United States, FDA regulation under 21 CFR 177.1560 authorizes qualifying polyarylsulfone resins for use in articles intended for food contact, anchored by extractives limits that brand owners and converters typically reference during material selection and qualification.

In Europe, REACH-driven compliance is extending beyond substance restrictions into more structured documentation and reporting. Regulation (EU) 2026/1168 (amending the EU synthetic polymer microparticle restriction) adds requirements around use and disposal instructions, plus annual reporting of emissions (for the prior calendar year) by May 31, which increases administrative workload for suppliers and downstream converters using polymeric materials and formulations. Separately, BASF highlighted portfolio actions in March 2026 to help processors re-qualify food-contact applications in line with EU Regulation 2024/3190, reinforcing how changes to food-contact compliance can trigger material re-qualification and re-testing cycles across the value chain.

Value Chain Analysis

The polyarylsulfone value chain begins with petrochemical feedstocks and intermediates that underpin monomers such as 4,4-dichlorodiphenyl sulfone and dihydroxy/biphenol building blocks, followed by polymerization commonly executed via nucleophilic substitution in high-boiling polar solvents (for example, sulfolane or N-methylpyrrolidone) with alkali bases, then washing and purification. Integrated producers and large-scale resin makers such as BASF, SABIC, and Solvay/Syensqo are advantaged by upstream access and by the ability to manage specification control for medical, electronics, and food-contact grades.

Midstream activities include compounding (glass-fiber reinforcement, high-flow and thin-wall molding grades, and customized coloration). Compounders and additive partners help shorten OEM qualification cycles by supplying pre-colored or application-ready pellets. Downstream, processors convert resins into injection-molded and machined components for medical devices, semiconductor and electronics equipment housings, EV battery-pack and thermal-management parts, and filtration membranes. Qualification and compliance run across the chain, with FDA 21 CFR 177.1560 shaping food-contact selections and EU documentation and reporting obligations adding data-management requirements. Sustainability audits are also influencing grade selection, reflected in the industry shift toward ISCC Plus, mass-balance, and circular-feedstock offerings from major suppliers.

Competitive Landscape

Industry structure skews toward moderately consolidated concentration. Solvay, BASF, and SABIC account for almost half of the installed capacity, benefiting from captive phenol, acetone, and sulfur trioxide streams. Their integrated models yield cost baselines 8–10% below independent compounders, permitting sustained R&D outlays in specialty grades. Solvay’s Fulcrum recycling pilot in Belgium converts post-industrial PSU waste into high-purity monomer, aligning with OEM decarbonization metrics. BASF partners with Encina Development Group to secure chemically recycled benzene, bolstering its circular feedstock pipeline.

Mid-tier players build regional presence through price leadership but face qualification gaps in medical and aerospace markets where documentation depth trumps cost. Custom compounders like RTP Company capture niches via rapid color matching and flame-retardant packages.

Innovation fronts center on fiber-reinforced pellets for structural auto parts, transparent grades with UV-blocking nanofillers for laboratory optics, and sulfone-carbon-nanotube blends that dissipate static in semiconductor fabs. Patent landscapes reveal a surge in surface-grafting techniques that improve hydrophilicity of filtration membranes without compromising chlorine resilience. Companies that commercialize these enhancements earliest will differentiate on lifecycle cost and ESG credentials.

Polyarylsulfone Industry Leaders

Solvay

BASF SE

SABIC

Sumitomo Chemical Co., Ltd.

Mitsubishi Chemical Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory-driven reformulation and documentation are exemplified by BASF's March 2026 expansion of Ultrason P to support manufacturers aligning with EU Regulation 2024/3190. Circularity and processing-enabling innovation are also moving ahead. Syensqo announced a chemical recycling route in October 2025 to depolymerize sulfone polymers back into purified monomers for closed-loop repolymerization, targeting recycled-content and audit requirements in high-performance applications. Solvay disclosed in May 2026 work on warpage-reduction technology for high-performance polymer blends, targeting dimensional stability needs in aerospace and advanced electronics manufacturing, which supports broader substitution of metals and legacy polymers.

Recent Industry Developments

- June 2026: BASF confirmed expanded production of Ultrason polyarylsulfones at its Yeosu, South Korea site is operational. The move strengthens regional supply for Asia Pacific converters serving electronics and e-mobility clusters, while also improving lead-time and continuity options for global OEMs that dual-source high-performance polymers.

- March 2026: BASF introduced six tailored Ultrason P polyphenylsulfone (PPSU) grades positioned to support manufacturers aligning food-contact materials with EU Regulation 2024/3190. By packaging application-specific compliance support into the resin portfolio, the launch reduces re-qualification friction for converters supplying regulated kitchenware and household food-contact applications.

- October 2025: Syensqo announced a chemical recycling route for depolymerizing polysulfone resins back into purified monomers for closed-loop repolymerization. The approach targets recycled-content and audit requirements in high-performance applications that are sensitive to property drift.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market is defined as the sales value of polyarylsulfone resins used in industrial processing and finished-part manufacturing, counted at the point of resin sale and tracked across major producing and consuming regions.

Scope exclusions: We exclude downstream parts fabrication value add, compounder service revenue, and finished medical device prices even when polyarylsulfone is the key material.

Segmentation Overview

- By Type

- Polysulfone (PSU)

- Polyethersulfone (PESU)

- Polyphenylsulfone (PPSU)

- Polyetherimide (PEI)

- By End-User Industry

- Automotive

- Aerospace

- Electronics

- Medical

- Mechanical

- Others

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

To build the first cut of the market, we started with public data that anchors polymer demand and supply signals. Sources reviewed include trade and industrial statistics such as US International Trade Commission data, UN Comtrade, Eurostat, and national statistical offices in large manufacturing countries, along with customs-based import and export classifications where high-performance polymers are visible.

We also used technical and adoption clues from ASTM and ISO material standards, US FDA public guidance related to polymer use in healthcare products, and peer-reviewed journals that discuss PSU, PESU, and PPSU processing and application trends. On the company side, annual reports, investor presentations, and press releases were screened to identify capacity moves, new grades, and end-use demand commentary. Where needed, we referenced paid subscriptions for company financials and patent databases to cross-check expansion timing and product introductions. The source list stated here is illustrative, and many other public and paid references were used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work was used to confirm what drives consumption and pricing after the desk model created the first estimate. We spoke with respondents across resin production, distribution, and high-temperature polymer processing, and then rechecked assumptions with buyers in automotive, aerospace, electronics, and medical value chains across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 13% | APAC: 47% |

| Mid tier: 52% | Functional/Unit leaders: 42% | EMEA: 30% |

| Smaller Players: 15% | Managers: 45% | Americas: 23% |

Market-Sizing & Forecasting

Sizing started from a top-down build where polymer consumption pools were reconstructed using high-performance thermoplastics demand by end-use, and then filtered using application fit and substitution ranges for polyarylsulfone. To keep this practical, we relied on a short set of repeatable inputs, such as capacity additions and utilization direction, import and export movements for specialty polymers, price ranges by grade, and end-use production indicators that pull material demand (for example, aircraft deliveries, vehicle output, and medical device manufacturing momentum).

The totals were then corroborated using selective bottom-up checks, mainly sampled volume by region multiplied by average selling prices, followed by distributor channel checks and spot validation from processors. Where direct data was thin, we handled gaps by using proxy grades and normalized spreads, then re-tested through expert feedback until the implied volumes and pricing stayed realistic.

For forecasting, scenario analysis was applied. Each scenario was anchored on how experts expect key drivers to move, including lightweighting demand, electrification-related thermal needs, membrane use trends, and medical-grade qualification timelines. Each scenario was converted into a yearly path for volumes and prices, and the final forecast was chosen only after it remained consistent with the demand indicators tracked in the historical period.

Data Validation & Update Cycle

To validate the model, we triangulated the output against independent signals, including trade flows, announced expansions, and the implied consumption intensity in key end uses. Outliers were flagged when a region showed a jump that did not match movement in production indicators or price bands, and those areas were reworked before internal sign-off.

A multi-step review is followed, where assumptions are checked by another analyst and any large variance is questioned with a clear reason logged. Reports are refreshed annually, and interim updates are made when material events happen, such as major capacity changes or sudden end-use shocks. Before delivery, a final pass is completed so clients receive the latest updated view available at that time.

Mordor Intelligence's Polyarylsulfone Market Size Compared Against Other Published Estimates

Published estimates for polyarylsulfone often do not match because the product boundary and the counting point can change from one study to another, and pricing assumptions can also move the value sharply. Differences are also created by the base year chosen, the way volume is inferred when public data is limited, and how frequently the model is refreshed.

Trade-flow direction, capacity announcements, and end-use production signals are the checks that keep Mordor Intelligence's 2026 estimate tied to resin sales value, rather than mixing in downstream fabricated part value or broader high-performance polymer baskets.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.83 B (2026) | |

| Global Consultancy A | USD 2.10 B (2024) | Uses a different base year and appears to group polyarylsulfone types with a wider application set, which can lift the value if adjacent specialty polymers or broader end-use baskets are included. |

| Industry Data Publisher B | USD 2.17 B (2024) | Reported on a 2024 base and blends shipment-led reporting with revenue, which can shift totals when regional price timing, currency conversion, or grade mix assumptions are not aligned to a single resin sales counting point. |

Looking across the figures, the spread is explained mainly by base-year timing and what is counted as in-scope material and revenue. By keeping the model anchored to observable demand and supply signals and then checking price and volume realism through interviews, the final number stays traceable to clear steps that can be repeated year to year.

Key Questions Answered in the Report

What is the current size of the polyarylsulfone market?

The market stands at USD 1.83 billion in 2026 and is projected to reach USD 2.46 billion by 2031.

Which end-use sector holds the largest share?

Medical devices lead with 41.95% of revenue because polyarylsulfone withstands repeated steam sterilization.

Why is Asia Pacific so dominant in the polyarylsulfone market?

The region integrates raw materials through to compounding, and its electronics and EV supply chains drive demand growth at a 7.25% CAGR.

What makes polyphenylsulfone the fastest-growing grade?

PPSU offers superior impact strength and chemical resistance, enabling new applications such as EV battery housings that justify its premium price.

How are suppliers addressing sustainability concerns?

Major producers have introduced ISCC Plus-certified and chemically recycled grades, and some are piloting depolymerization to reclaim sulfone monomers for reuse.

Page last updated on: