Bronchial Hyperreactivity Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 14.60 Billion |

| Market Size (2030) | USD 17.60 Billion |

| Growth Rate (2025 - 2030) | 4.90% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bronchial Hyperreactivity Market Analysis by Mordor Intelligence

The bronchial hyperreactivity market size reached USD 14.6 billion in 2025 and is forecast to climb to USD 17.6 billion by 2030, reflecting a 4.9% CAGR over the period. Patent expirations for inhaled steroids are tempering top-line growth. Yet, rising air-pollution exposure, a deepening biologics pipeline, and guideline-backed early diagnosis initiatives continue to widen the treatable population. Biologic approvals for COPD—led by Dupixent and Nucala—are redefining care algorithms and raising the average revenue per patient. Meanwhile, connected inhaler ecosystems are improving adherence and generating real-world evidence that accelerates reimbursement. The bronchial hyperreactivity market, therefore, balances the maturity of legacy inhaled corticosteroid franchises with the disruptive promise of precision biologics, telehealth-enabled distribution, and consolidation-driven portfolio breadth.

Key Report Takeaways

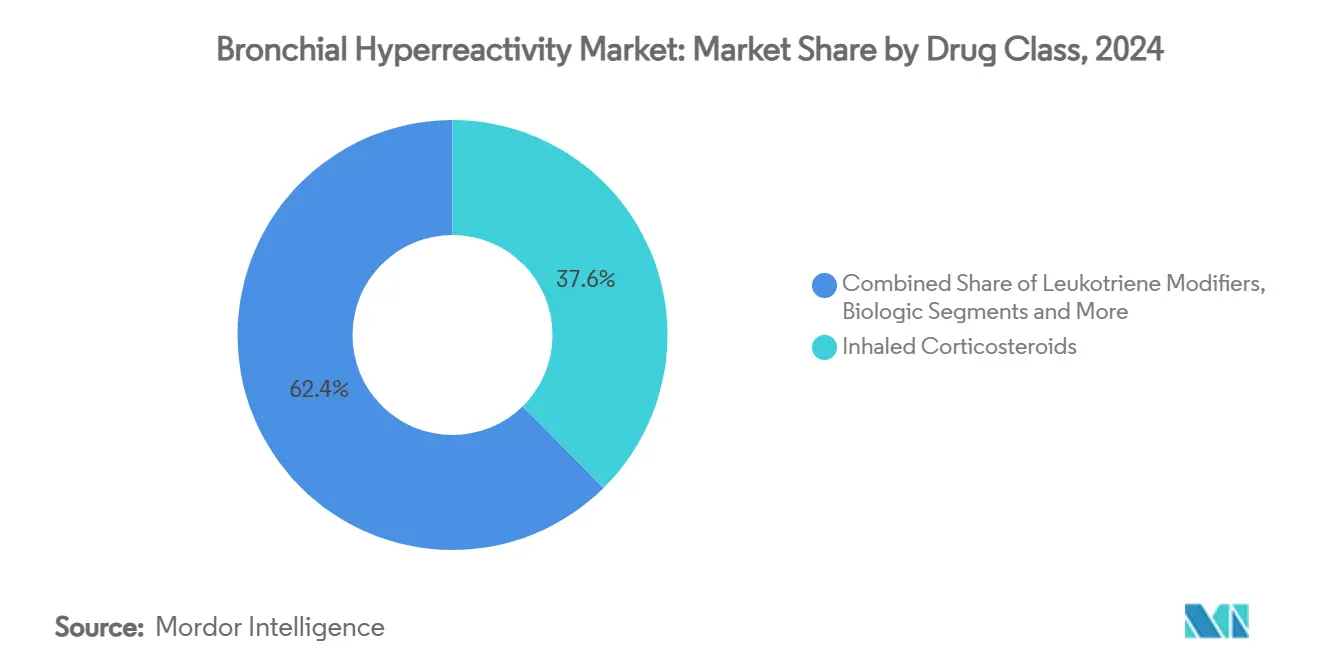

- By drug class, inhaled corticosteroids led with 37.6% revenue share in 2024, whereas biologic therapies are advancing at a 5.6% CAGR through 2030.

- By route, inhalation commanded 71.4% of the bronchial hyperreactivity market share in 2024; parenteral delivery is projected to expand at a 4.2% CAGR.

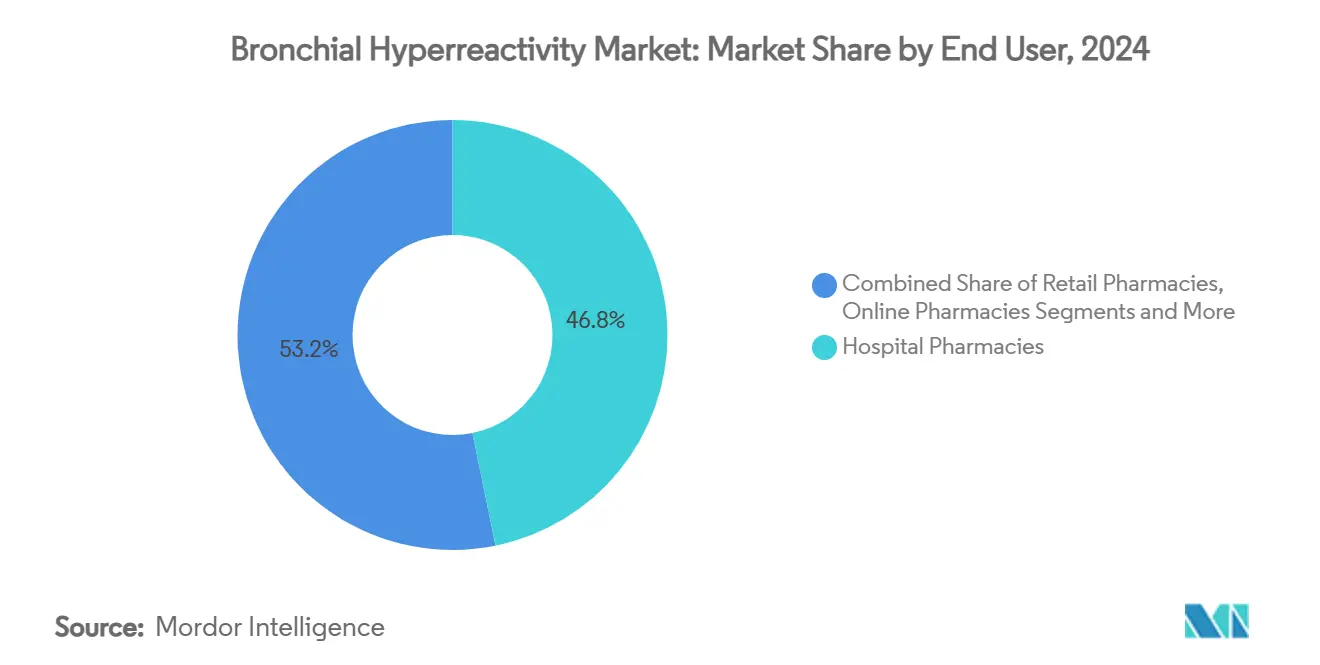

- By end user, hospital pharmacies held a 46.8% share in 2024, while online pharmacies represent the fastest-growing channel at 5.7% CAGR.

- By geography, North America accounted for 45.3% of the bronchial hyperreactivity market size in 2024; Asia Pacific is poised to grow at a 6.8% CAGR to 2030.

Global Bronchial Hyperreactivity Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of asthma & COPD | +1.20% | Global, highest in Asia Pacific & Sub-Saharan Africa | Long term (≥ 4 years) |

| Expansion of biologic therapies pipeline | +0.80% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Guideline-driven early diagnosis programs | +0.60% | Global, led by developed markets | Medium term (2-4 years) |

| Increasing adoption of digital inhalers | +0.40% | North America, EU, urban APAC | Short term (≤ 2 years) |

| Air-pollution-induced pediatric BHR surge | +0.70% | APAC core, spill-over to MEA & Latin America | Long term (≥ 4 years) |

| Long-COVID airway hypersensitivity | +0.30% | Global, higher in high-infection regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Asthma & COPD

Asthma now affects 339 million people worldwide, while COPD ranked third among global killers in 2024, creating an enduring patient funnel for the bronchial hyperreactivity market.[1]Frontiers Researchers, “Temporal Trends and Future Projections of Asthma in China,” Frontiers, frontiersin.orgAbsolute case numbers keep rising even where incidence rates decline because aging populations live longer with chronic disease, resulting in older, more comorbid cohorts that consume costlier biologic and combination therapies. Low- and middle-income countries shoulder more than 80% of COPD deaths, yet limited reimbursement infrastructures heighten unmet need and promote generic penetration. The net effect adds volume growth in emerging regions and value growth in high-income markets, anchoring a dual-speed expansion pattern for the bronchial hyperreactivity market.

Expansion of Biologic Therapies Pipeline

Dupixent’s landmark 2024 COPD approval signaled regulatory validation for biologics beyond severe asthma and could generate USD 6.5 billion in pulmonary revenue within a decade. Pipeline depth broadened rapidly: GSK’s depemokimab offers twice-yearly dosing, Sanofi’s amlitelimab targets OX40-Ligand, and AstraZeneca’s tozorakimab blocks IL-33 signaling, highlighting a pivot toward precision immunology. As biomarker-guided prescribing becomes mainstream, payers weigh higher upfront costs against documented exacerbation reductions, reinforcing premium pricing headroom for advanced biologics. These dynamics elevate the biologic share of bronchial hyperreactivity market revenues even while inhaled corticosteroids hold volumetric dominance.

Air-Pollution-Induced Pediatric BHR Surge

Ninety-three percent of children inhale PM2.5 above World Health Organization guidelines, embedding bronchial hyperreactivity risk from infancy and lengthening lifetime therapy duration.[2]MDPI Contributors, “Oxidative Stress, Environmental Pollution, and Lifestyle as Determinants of Asthma in Children,” MDPI, mdpi.com Traffic-related particulates intensify autumn asthma peaks, while oxidative stress pathways dampen steroid responsiveness, forcing clinicians to escalate to leukotriene modifiers or biologics sooner. Asia Pacific urban centers such as Delhi, Beijing, and Jakarta, therefore, add disproportionate pediatric volume that feeds long-run growth, positioning the region as the fastest-growing slice of the bronchial hyperreactivity market. Governments are responding with pollution curbs, but infrastructure lag implies a multi-year demand tailwind for pediatric formulations and antioxidant-enhanced combination inhalers.

Long-COVID Airway Hypersensitivity

Post-COVID children frequently present with dyspnea despite normal spirometry, yet impulse oscillometry reveals peripheral airway obstruction that reverses with inhaled corticosteroids. This novel phenotype broadens the treatable universe beyond allergic inflammation and is driving specialist clinic referral surges in the United States and Europe. Early data suggest that combination bronchodilator–steroid regimens outperform monotherapy, a finding that may influence formularies and propel fixed-dose innovation. Because SARS-CoV-2 exposure is worldwide, this incremental cohort introduces a durable demand layer that compounds core asthma and COPD volumes, further energizing the bronchial hyperreactivity market through the decade.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patent cliffs for key inhaled steroids | −0.9% | North America & EU | Short term (≤ 2 years) |

| Stringent inhaler-device regulatory hurdles | −0.5% | Global | Medium term (2-4 years) |

| Biologic therapy cost–access gap | −1.1% | Global, highest in emerging markets | Long term (≥ 4 years) |

| Inhalation-technique error in the elderly | −0.3% | Developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Patent Cliffs for Key Inhaled Steroids

Trelegy Ellipta and Breo Ellipta lose exclusivity in 2031, while Tudorza Pressair and Duaklir Pressair already faced generic entry in 2025. The abrupt withdrawal of Flovent in 2024 revealed systemic fragility when pediatric hospitalizations jumped 17.5% within three months. Generic waves depress price pools, yet innovators are counter-programming with device patents and ultra-long-acting biologics, cushioning revenue erosion. The overall impact shaves 0.9 percentage points off forecast CAGR yet simultaneously stimulates consolidation as firms seek scale to absorb pricing pressure.

Biologic Therapy Cost–Access Gap

A single biologic course can exceed USD 35,000 per year in the United States, placing treatments well above conventional cost-effectiveness thresholds and fueling discontinuation in 29.8% of patients, 20.3% for financial reasons. European models show that prescribing through specialist asthma units can achieve cost-efficiency, but emerging markets struggle as payers cap reimbursement. Pharmacy benefit manager consolidation layers additional mark-ups that widen patient copays and delay therapy initiation. Although discount biosimilars promise relief, regulatory complexity has slowed their arrival, prolonging the access divide that subtracts 1.1 percentage points from projected CAGR for the bronchial hyperreactivity market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Biologics Gain Traction While ICS Retain Scale

In 2024, inhaled corticosteroids generated 37.6% of bronchial hyperreactivity market revenue, underscoring their enduring first-line status for chronic control despite mounting generic erosion. Flovent's discontinuation exposed supply shortage vulnerabilities and forced rapid therapeutic substitution, reinforcing the clinical reliance on this class. Biologic agents, though starting from a smaller base, are projected to climb at a 5.6% CAGR through 2030 as expanded COPD indications enlarge the addressable pool. Dupixent's swift uptake, Nucala's eosinophilic COPD label, and depemokimab's twice-yearly regimen are resetting clinician expectations for durability and convenience, accelerating share migration toward antibody-based solutions.

Combination products that unite inhaled corticosteroids with LABA or LAMA bronchodilators act as a buffer, sustaining adherence and extending lifecycle protection. Leukotriene modifiers continue to serve exercise-induced bronchospasm and aspirin-intolerant cohorts, maintaining predictable demand curves. Triple-therapy formulations such as Trelegy Ellipta, now in late-life patent defense, still outperform dual combinations in the exacerbation reduction metric. Yet, their long-term role depends on competitive biologic pricing. The therapeutic mix therefore reflects coexistence rather than displacement, with biologics capturing value and inhaled steroids safeguarding volume in the bronchial hyperreactivity market.

By Route of Administration: Inhalation Dominates, Parenteral Accelerates

The inhalation route accounted for 71.4% of the bronchial hyperreactivity market size in 2024, thanks to direct airway deposition, fast relief, and favorable safety profiles.[3]PubMed Reviewers, “Pulmonary Route of Administration Is Instrumental,” National Library of Medicine, pubmed.ncbi.nlm.nih.gov Dry-powder inhalers are gaining ground in environmentally regulated markets because they eliminate propellants, while vibrating-mesh nebulizers have revived interest by enabling stable monoclonal antibody delivery. Propellant migration from HFA to low-GWP solutions also supports regulatory compliance without sacrificing performance.

Parenteral delivery, although representing a minority today, is expanding at 4.2% CAGR as subcutaneous autoinjectors and on-body pumps reduce clinic-visit burdens. Depemokimab’s twice-yearly injection epitomizes convenience-led adoption, lowering adherence barriers and encouraging payers to cover premium biologics for high-risk cohorts. Novel microneedle patches and long-acting depot technologies are under study, seeking to blend systemic exposure control with patient self-administration. Collectively, these innovations diversify delivery options and reinforce competitive differentiation in the bronchial hyperreactivity market.

By End User: Digital Dispensing Redraws Supply Chains

Hospital pharmacies captured 46.8% of dispensing value in 2024, leveraging integrated specialty-pharmacy services to initiate biologics, manage adverse events, and navigate insurance approvals. Their roles have broadened to include telehealth triage and electronic prior-authorization processing, bolstering revenue resilience even as outpatient volumes migrate online.

Online pharmacies, growing at 5.7% CAGR, benefit from telemedicine’s explosive shift from 15.4% to 87% utilization during the pandemic. Real-time prescription transmission, doorstep cold-chain delivery, and AI-powered adherence reminders appeal to digitally native patients and working parents. Regulatory gray zones around remote physiologic monitoring reimbursement persist, yet CMS pilot programs are testing new fee structures that could unlock further volume. Retail chains, facing thinning margins, have turned to medication-therapy-management and point-of-care spirometry to retain customer loyalty. Specialty clinics specializing in severe asthma and COPD round out the channel mix, often operating within academic hospitals to ensure biomarker-guided biologic optimization, thereby sustaining a premium service niche across the bronchial hyperreactivity market.

Geography Analysis

North America held 45.3% of bronchial hyperreactivity market size in 2024 on the back of early biologic adoption, robust payer coverage, and rapid FDA approvals for innovative mechanisms such as IL-4/IL-13 and IL-5 inhibition. Declining mortality among chronic lower respiratory disease patients reflects widespread controller usage, yet rural populations continue to endure care disparities, sustaining opportunity for remote dispensing and connected inhaler platforms. Canada’s unified drug assessment process accelerates national reimbursement decisions, enabling equitable biologic deployment, whereas the United States struggles with PBM mark-ups that inflate patient out-of-pocket costs.

Asia Pacific is forecast to post the fastest 6.8% CAGR, buoyed by rising urban pollution and broadening insurance coverage in markets such as China and India. Despite a dip in age-standardized incidence, China still projects 4.5 million asthma cases by 2046, reinforcing volume momentum. Pediatric exposures to PM2.5 above WHO thresholds feed constant treatment initiation, while Japan and South Korea front-load regional biologic penetration under single-payer reimbursement models. India’s dual embrace of allopathic and traditional medicine yields hybrid therapeutic pathways that could spur novel combination formulations. The net result positions Asia Pacific as the principal incremental contributor to bronchial hyperreactivity market growth this decade.

Europe delivers steady expansion on the strength of harmonized EMA pathways and centralized health technology assessments that facilitate guideline uptake. Early EMA clearance of Dupixent for COPD granted clinicians earlier access than their US counterparts, underscoring regulatory agility. Specialized asthma units in Spain illustrate how multidisciplinary care can render high-cost biologics cost-effective, a model now under review in Germany and the United Kingdom. Brexit-related supply-chain friction has moderated but continues to prompt dual licensing filings, marginally increasing administrative overhead. Eastern European countries lag on biologic reimbursement, defining a tiered adoption landscape within the continent’s overall mature bronchial hyperreactivity market.

Competitive Landscape

The bronchial hyperreactivity market shows moderate concentration with the top five manufacturers controlling nearly 60% of global prescription value. Merck’s USD 10 billion Verona Pharma purchase added first-in-class ensifentrine, reflecting a pivot toward inhaled dual PDE-3/4 inhibition and signaling appetite for late-stage respiratory assets. GSK spent USD 1 billion on Aiolos for TSLP biology and partnered with Hengrui in a USD 12 billion framework to accelerate Asian pipeline access, spreading portfolio and geographic risk. AstraZeneca bolstered its respiratory footprint via a USD 2 billion Almirall franchise acquisition, filling pipeline gaps as Trelegy Ellipta nears expiry.

Digital inhaler ecosystems have become a battleground: sensor-equipped devices now feed adherence data to cloud algorithms that predict exacerbations days in advance, a capability that underpins risk-based contracting with payers. Device patents thus serve as lifecycle-extension levers when molecule exclusivity wanes. Companies unwilling to integrate software have opted to license platforms from med-tech specialists, creating a web of cross-sector alliances that blur traditional industry boundaries.

Competitive strategy also circles around pediatric gaps revealed by Flovent’s exit; several firms have accelerated low-dose HFA-free steroid development aimed at children under five. In parallel, pipeline biologics are exploring dual or triple cytokine blockade to surpass existing efficacy ceilings. Collectively these moves tilt the bronchial hyperreactivity market toward fewer, more diversified players wielding both molecule and technology assets to defend share and expand addressable patient segments.

Bronchial Hyperreactivity Industry Leaders

GlaxoSmithKline plc

AstraZeneca plc

Novartis AG

Teva Pharmaceutical Industries Ltd.

Boehringer Ingelheim Int’l GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Merck completed its USD 10 billion acquisition of Verona Pharma, adding Ohtuvayre as the first novel inhaled COPD maintenance therapy in two decades.

- July 2025: GSK and Hengrui announced a USD 12 billion respiratory collaboration, including USD 500 million upfront for late-stage assets.

- April 2025: Sanofi reported positive phase 2 data for OX40-Ligand inhibitor amlitelimab in heterogeneous inflammatory asthma.

Global Bronchial Hyperreactivity Market Report Scope

| Inhaled Corticosteroids (ICS) |

| Long-Acting ?2-Agonists (LABA) |

| Leukotriene Modifiers |

| Biologic Therapies (Anti-IgE, Anti-IL-5/13, etc.) |

| Combination Drugs (ICS/LABA, Triple, etc.) |

| Inhalation (pMDI, DPI, Nebuliser) |

| Oral |

| Parenteral |

| Transdermal & Others |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Specialty Clinics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Inhaled Corticosteroids (ICS) | |

| Long-Acting ?2-Agonists (LABA) | ||

| Leukotriene Modifiers | ||

| Biologic Therapies (Anti-IgE, Anti-IL-5/13, etc.) | ||

| Combination Drugs (ICS/LABA, Triple, etc.) | ||

| By Route of Administration | Inhalation (pMDI, DPI, Nebuliser) | |

| Oral | ||

| Parenteral | ||

| Transdermal & Others | ||

| By End User | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Specialty Clinics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the bronchial hyperreactivity market?

The bronchial hyperreactivity market size stands at USD 14.6 billion in 2025 and is projected to reach USD 17.6 billion by 2030.

How fast is the market expected to grow?

The market is forecast to register a 4.9% CAGR from 2025 to 2030.

Which therapy class leads revenue today?

Inhaled corticosteroids hold the largest 37.6% revenue share, reflecting continued first-line positioning.

Which route of administration is gaining momentum?

Parenteral delivery is the fastest-growing route at a 4.2% CAGR thanks to convenient subcutaneous biologic injections.

Which region will expand the quickest?

Asia Pacific is set to post the highest 6.8% CAGR, propelled by pollution-driven pediatric volumes and improving healthcare access.

What is driving industry consolidation?

Approaching patent cliffs for inhaled steroids and the need for biologic portfolio depth have spurred multi-billion-dollar acquisitions among the top players.

Page last updated on: