Idiopathic Pulmonary Fibrosis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.68 Billion |

| Market Size (2031) | USD 6.43 Billion |

| Growth Rate (2026 - 2031) | 6.55% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Idiopathic Pulmonary Fibrosis Market Analysis by Mordor Intelligence

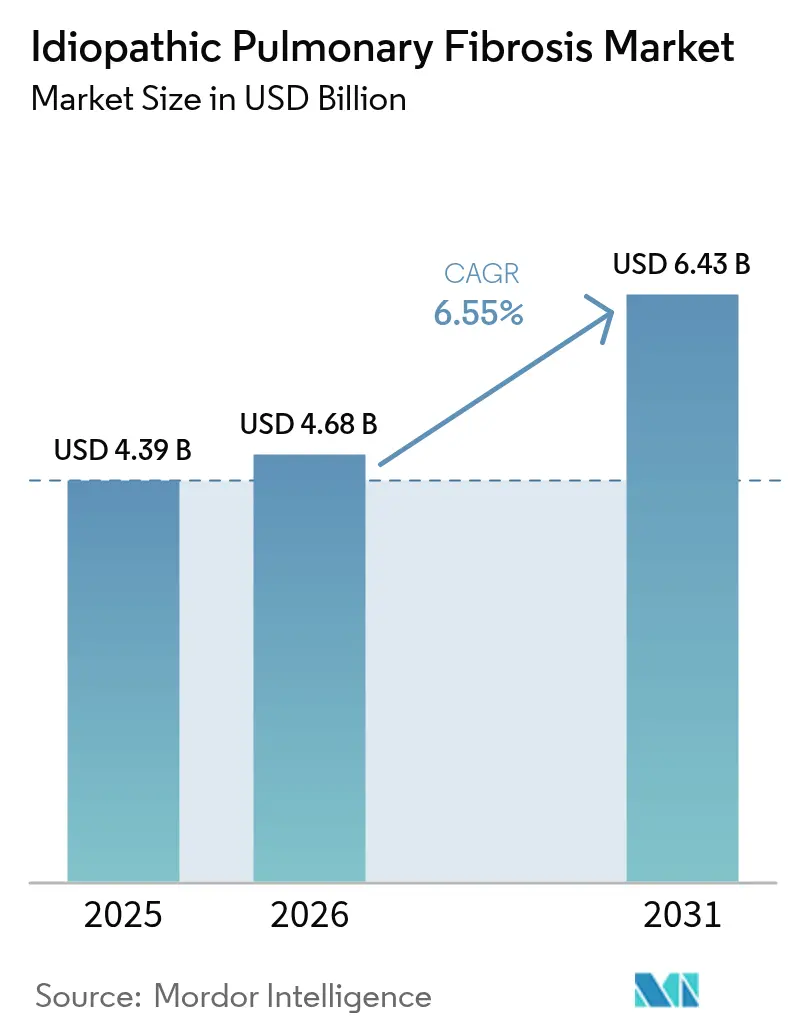

The Idiopathic Pulmonary Fibrosis market size is expected to grow from USD 4.39 billion in 2025 to USD 4.68 billion in 2026 and is forecast to reach USD 6.43 billion by 2031 at 6.55% CAGR over 2026-2031.

This upward path is sustained by accelerated diagnostic adoption, an expanding elderly population, and a deep pipeline of next-generation antifibrotic agents. Inhaled delivery platforms that curb systemic exposure are reshaping therapeutic positioning, while biomarker-driven precision medicine is pushing clinical trials toward smaller, better-targeted cohorts. Asia-Pacific is moving quickly from a peripheral participant to a central growth engine, aided by regional clinical-trial density and rapidly improving reimbursement frameworks. At the same time, North America’s large diagnosed pool, advanced specialty-center network, and supportive regulatory climate keep it as the primary commercial theater of the idiopathic pulmonary fibrosis market.

Key Report Takeaways

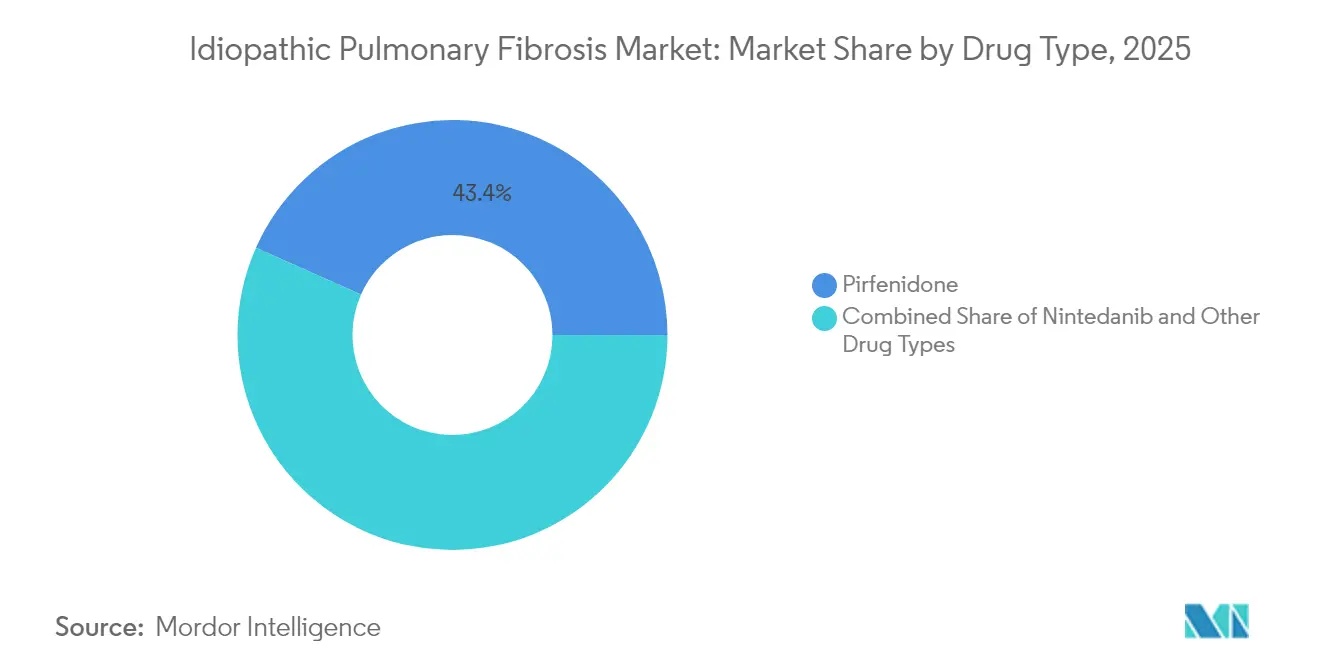

- By drug type, pirfenidone secured 43.35% of the idiopathic pulmonary fibrosis market share in 2025, whereas nintedanib is projected to expand at a 7.52% CAGR through 2031.

- By mode of action, antifibrotic agents commanded 82.05% revenue share in 2025; tyrosine kinase inhibitors are on track for the fastest rise with a 9.12% CAGR.

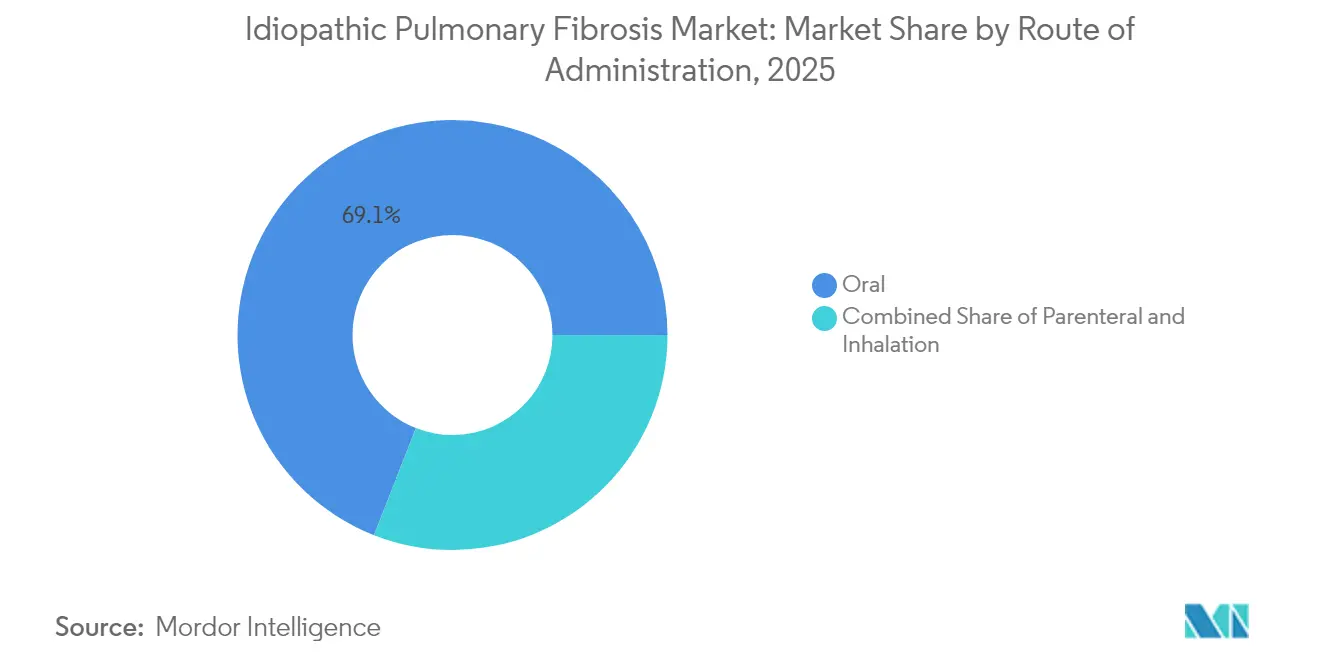

- By route of administration, oral therapies accounted for 69.05% of the idiopathic pulmonary fibrosis market size in 2025, yet inhalation is advancing at a 9.85% CAGR across 2026-2031.

- By end user, hospitals and clinics held 57.05% of revenue in 2025, while home-care settings are forecast to post a 8.78% CAGR to 2031.

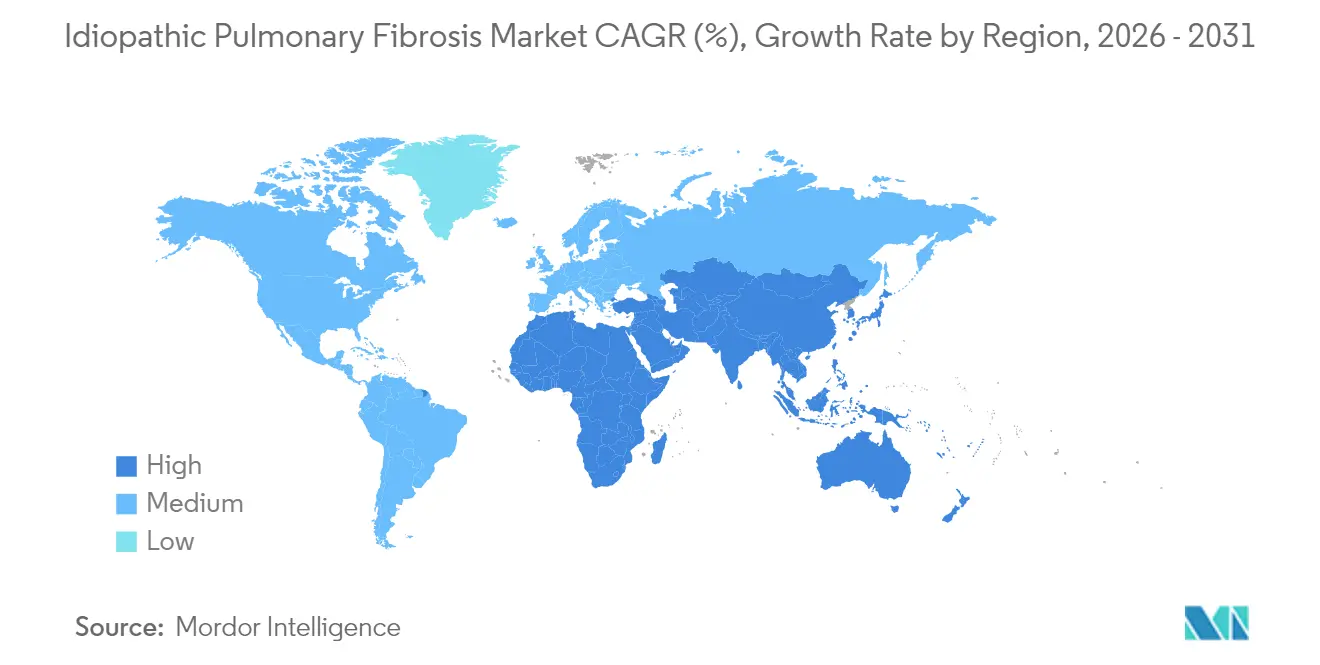

- By geography, North America dominated with 41.05% share in 2025; Asia-Pacific is projected to register the quickest 8.62% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Idiopathic Pulmonary Fibrosis Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of IPF coupled with aging demographics | +2.1% | Global (North America, Europe, East Asia) | Long term (≥ 4 years) |

| Expansion of diagnostic capabilities and early detection programs | +1.6% | North America, Europe, developed Asia-Pacific | Medium term (2–4 years) |

| Advancements in antifibrotic therapies and robust pipeline momentum | +2.3% | Global (initial impact in North America, Europe) | Medium term (2–4 years) |

| Strategic collaborations & investments in fibrosis research | +1.4% | North America, Europe, China, Japan | Medium term (2–4 years) |

| Increased use of artificial intelligence for radiological screening & disease-progression monitoring | +1.1% | Developed markets worldwide | Medium term (2–4 years) |

| Rising patient advocacy and awareness campaigns worldwide | +0.9% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of IPF Coupled with Aging Demographics

Incidence continues to rise in tandem with global population aging, placing sustained pressure on healthcare systems and pushing demand for novel medicines. Europe diagnoses about 40,000 new cases annually, and prevalence in South Korea tops 4.5 per 10,000 persons, nearly double North American rates.[1]Frontiers Editorial Office, “Global Epidemiology of Idiopathic Pulmonary Fibrosis,” frontiersin.org Care costs run 2.5-to-3.5 times higher than for non-IPF patients, incentivizing pharmaceutical investment and stimulating development of geriatric-adapted formulations.

Expansion of Diagnostic Capabilities and Early Detection Programs

High-resolution computed tomography remains foundational, yet 2024 FDA clearance of an AI-enabled algorithm signaled a step-change in radiology workflows.[2]Respiratory Therapy Editorial Team, “FDA Clears AI Tool for IPF Diagnosis,” respiratorytherapy.ca Parallel progress in circulating and exhaled-breath biomarkers such as the PROLIFIC multi-analyte panel supports earlier confirmatory testing and stratifies patients more effectively for therapy selection. Earlier intervention strengthens treatment response durability, expanding the addressable idiopathic pulmonary fibrosis market.

Advancements in Antifibrotic Therapies and Robust Pipeline Momentum

More than 100 assets from over 80 companies are active in clinical development, underscoring mounting competitive intensity. Boehringer Ingelheim’s PDE4B inhibitor nerandomilast reduced FVC decline in Phase III, positioning it to join or eclipse the long-standing duopoly of nintedanib and pirfenidone.[3]Boehringer Ingelheim Press Office, “Nerandomilast Phase III Topline Results,” boehringer-ingelheim.com Bristol Myers Squibb’s LPA1 antagonist admilparant also demonstrated a hazard ratio of 0.54 on disease progression endpoints.

Strategic Collaborations & Investments in Fibrosis Research

Endeavor BioMedicines raised USD 132.5 million Series C to advance Hedgehog-pathway inhibitor ENV-101. REMAP-ILD’s adaptive global protocol enhances trial efficiency and gathers multicountry evidence simultaneously. Asia-Pacific’s 44% share of global IPF trials reflects CRO specialization and streamlined ethics processes, shortening development timelines.

Restraints Impact Analysis of Idiopathic Pulmonary Fibrosis Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost and limited accessibility of antifibrotic drugs | -1.2% | Global (greater impact in emerging markets) | Medium term (2–4 years) |

| Adverse side-effect profile leading to treatment discontinuation | -0.8% | Global | Short term (≤ 2 years) |

| Limited therapeutic options beyond antifibrotics | -0.6% | Global | Long term (≥ 4 years) |

| Low diagnosis rates in primary care settings | -0.5% | Global (particularly rural regions) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Cost and Limited Accessibility of Antifibrotic Drugs

Annual treatment bills consume a sizable share of respiratory-care budgets, constraining uptake in lower-income regions. With only 25% of eligible patients started on therapy, manufacturers are exploring value-based pricing and co-pay assistance programs. Generic pirfenidone, available since 2021, offers near-term relief but broad commercial impact hinges on further price erosion once additional patents lapse.

Adverse Side-Effect Profile Leading to Treatment Discontinuation

Real-world evidence shows discontinuation rates of 61.22% for nintedanib and 32.68% for pirfenidone, largely from gastrointestinal events. Surveys reveal fatigue and breathlessness persist in 78% and 86% of treated patients, respectively. Reduced-dose regimens and inhaled delivery platforms aim to mitigate intolerance, positioning tolerability as a primary differentiation axis in forthcoming launches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Idiopathic Pulmonary Fibrosis Market Segment Analysis

Drug Type:

Pirfenidone Dominates Despite Nintedanib's MomentumPirfenidone captured 43.35% idiopathic pulmonary fibrosis market share in 2025 through wider prescriber familiarity and earlier commercial rollout. Nintedanib’s broader label covering progressive fibrosing interstitial lung diseases underpins its 7.52% CAGR forecast. Comparative cohort studies report similar survival benefit yet divergent AE profiles that directly shape physician choice. Next-wave candidates such as PDE4B and LPA1 modulators—could recalibrate share distribution by offering organ-specific targeting and lower discontinuation risk.

The introduction of deupirfenidone (LYT-100) lowered gastrointestinal events by 50% versus reference pirfenidone, signaling that reformulations can stretch product lifecycles and sustain pirfenidone’s franchise. Combination regimens under investigation could embed pirfenidone or nintedanib as backbone therapy, anchoring their commercial relevance even as new agents arrive.

Mode of Action:

Antifibrotics Lead While Kinase Inhibitors AccelerateAntifibrotic agents controlled 82.05% of 2025 revenue, highlighting their foundational role in dampening extracellular-matrix deposition. Tyrosine kinase inhibitors contribute the sharpest growth trajectory at 9.12% CAGR, thanks to nintedanib’s multi-receptor blockade. Dual-pathway drugs such as nerandomilast combine anti-inflammatory and antifibrotic effects, mirroring evolving scientific consensus that parallel pathway modulation affords superior lung-function preservation.

Early-stage programs are exploring senolytics, integrin blockers, and TGF-β signaling disruptors. Shanghai Ark Biopharmaceutical’s AK3280 illustrated significant lung-function gains by modulating multiple fibrosis-linked pathways across 31 Chinese trial sites. Sophisticated biomarker panels guide endotype selection, supporting differentiated regulatory filings and payer negotiations.

Route of Administration:

Oral Dominance Challenged by Inhalation InnovationIn 2025, oral formulations contributed 69.05% of the idiopathic pulmonary fibrosis market size. However, inhalation is scaling fastest at a 9.85% CAGR, energised by United Therapeutics’ treprostinil and Avalyn Pharma’s inhaled IPF franchise. Direct pulmonary deposition curtails systemic exposure and improves tolerability, particularly pertinent to patients intolerant to high-dose oral nintedanib.

Avalyn’s AP02 delivered nintedanib directly to alveolar surfaces with minimal plasma levels, potentially slashing gastrointestinal AEs while preserving efficacy. Parenteral routes remain restricted to acute care and investigational combination strategies, yet may augment chronic therapies as fibrosis-reversal targets emerge.

End User:

Hospitals Lead While Home-Care Settings ExpandSpecialist hospitals and academic clinics retained 57.05% revenue share in 2025 through multidisciplinary expertise and access to lung-transplant infrastructure. Home-care, supported by remote spirometry and telehealth, is on course for a 8.78% CAGR, partly reflecting pandemic-driven decentralization and payer preference for lower-cost settings. Specialty pulmonary clinics bridge these models, offering advanced imaging and trial enrollment outside major hospitals.

The shift supports adherence by reducing travel burden on elderly populations while generating granular real-world data streams that enrich payer dossiers. Portable inhalation devices and app-based symptom tracking further anchor chronic management in community environments.

Geography Analysis

North America Idiopathic Pulmonary Fibrosis Market

North America held 41.05% of 2025 revenue, supported by deep reimbursement coverage, a dense network of ILD centers, and rapid incorporation of AI diagnostics into radiology suites. Venture capital continues to sponsor late-stage programs, and adaptive trial designs pioneered in United States academic consortia are accelerating regulatory timetables. Precision-medicine approaches, bolstered by payer acceptance of biomarker testing, are widening specialist adoption and stabilizing patient retention on therapy.

APAC Idiopathic Pulmonary Fibrosis Market

Asia-Pacific is the fastest-expanding region, posting an 8.62% CAGR across 2026-2031. China and Japan dominate commercial potential owing to large diagnosed populations, while South Korea records the highest prevalence globally at 4.5 per 10,000 persons. The idiopathic pulmonary fibrosis market benefits from regional trial-site density 44% of current IPF studies are run in Asia-Pacific, strengthening early physician familiarity with investigational agents and shortening launch ramp-up times. Domestic innovators such as Shanghai Ark are further stimulating local competition.

Europe Idiopathic Pulmonary Fibrosis Market

Europe remains a pivotal market with strong regulatory incentives for rare-disease therapeutics. National reimbursement expansion exemplified by Belgium’s 2024 update broadens antifibrotic accessibility, while pan-EU Horizon funding underwrites translational projects. Specialist ILD centers exhibit 91% antifibrotic access versus 60% in non-specialist facilities, underlining the benefits of concentrated expertise. Harmonized clinical-practice guidelines support consistent uptake across major economies, sustaining Europe’s contribution to global revenue.

Competitive Landscape

The idiopathic pulmonary fibrosis market displays moderate concentration: Boehringer Ingelheim and Roche collectively account for a sizable but not overwhelming proportion of global sales through nintedanib and pirfenidone franchises. Competitive dynamics are reshaped by biotech disruptors advancing novel mechanisms Pliant Therapeutics’ bexotegrast targets integrins pivotal to TGF-β activation and is now in Phase 2b/3. PureTech Health’s deupirfenidone achieved 50% lower GI-event incidence, emphasizing tolerability as strategic white space.

Artificial-intelligence-assisted discovery has quickened candidate generation cycles. Insilico Medicine’s INS018_055, designed via AI to inhibit TGF-β1/Smad3, underscores computational chemistry’s growing role. On the diagnostic front, 2024 FDA clearance of an AI algorithm improves early detection accuracy, indirectly enlarging the treatable pool and incentivizing new entrants.

Strategic alliances and option-to-acquire deals increasingly populate the transaction pipeline, spreading risk and broadening portfolios. Large pharma seeks externally sourced assets that bypass legacy tolerability constraints, while smaller firms gain commercialization muscle and global trial infrastructure. As generics erode early-generation revenues, incumbents pivot toward combination-therapy strategies and lifecycle-extension dosing studies.

Idiopathic Pulmonary Fibrosis Industry Leaders

Boehringer Ingelheim International GmbH

F. Hoffmann-La Roche Ltd

Horizon Therapeutics plc

Cipla Ltd

FibroGen Inc.

- *Disclaimer: Major Players sorted in no particular order

Idiopathic Pulmonary Fibrosis Market Companies Covered in this Report

- Roche

- Boehringer Ingelheim

- Cipla

- Merck

- Bristol-Myers Squibb

- United Therapeutics Corp.

- FibroGen Inc.

- Horizon Therapeutics

- Avalyn Pharma Inc.

- MediciNova Inc.

- Gyre Therapeutics Inc.

- AstraZeneca

- Vicore Pharma

- Novartis

- Tvardi Therapeutics

- Pliant Therapeutics

- Galapagos NV

- Gyre Therapeutics

- AdAlta Ltd

Recent Industry Developments in Idiopathic Pulmonary Fibrosis Market

- May 2025: Boehringer Ingelheim announced positive Phase III results for nerandomilast in both IPF and progressive pulmonary fibrosis, demonstrating significant reduction in forced vital capacity decline compared to placebo, positioning it as a potential new standard of care.

- May 2025: Vicore Pharma presented new data on buloxibutid (C21) at the ATS International Conference, showing superior anti-fibrotic activity compared to existing treatments, with potent inhibition of PRO-C3, a biomarker for fibrotic progression.

- May 2025: Avalyn Pharma showcased positive clinical data for its inhaled therapies AP01 (pirfenidone) and AP02 (nintedanib) at the ATS 2025 conference, demonstrating improved safety and tolerability compared to oral formulations.

- May 2025: GRI Bio presented positive pre-clinical data for GRI-0621, showing resolution of inflammation and fibrosis in a bleomycin-induced fibrosis model, along with promising preliminary Phase 2a clinical results.

Global Idiopathic Pulmonary Fibrosis Market Report Scope

As per the scope of the report, idiopathic pulmonary fibrosis (IPF) refers to a type of lung disease that causes scarring (fibrosis) of the lungs for an unknown reason. As time passes, this scarring gets worse, and it becomes hard to take deep breaths, and the lungs cannot take in enough oxygen. IPF involves the interstitium (the tissue and space around the air sacs of the lungs) and not directly involve the airways or blood vessels.

The idiopathic pulmonary fibrosis market is segmented by drug type, mode of action, end user, and geography. Based on drug type the market is segmented as nintedanib, pirfenidone, and other drug types. Based on mode of action the market is segmented as antifibrotic agents, tyrosine kinase inhibitors, and other modes of action. Based on end users the market is segmented as hospitals and clinics, pharmacies, and other end users. Based on geography the market is segmented by North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value in USD for the above segments.

Segmentation Overview

| Nintedanib |

| Pirfenidone |

| Other Drug Types |

| Antifibrotic Agents |

| Tyrosine Kinase Inhibitors |

| Other Modes of Action |

| Oral |

| Parenteral |

| Inhalation |

| Hospitals & Clinics |

| Specialty Clinics |

| Home-Care Settings |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Type | Nintedanib | |

| Pirfenidone | ||

| Other Drug Types | ||

| By Mode of Action | Antifibrotic Agents | |

| Tyrosine Kinase Inhibitors | ||

| Other Modes of Action | ||

| By Route of Administration | Oral | |

| Parenteral | ||

| Inhalation | ||

| By End User | Hospitals & Clinics | |

| Specialty Clinics | ||

| Home-Care Settings | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current idiopathic pulmonary fibrosis market size and growth outlook?

The idiopathic pulmonary fibrosis market size is USD 4.68 billion in 2026 and is projected to reach USD 6.43 billion by 2031, growing at a 6.55% CAGR.

Which region is expanding fastest in the idiopathic pulmonary fibrosis market?

Asia-Pacific is forecast to grow at an 8.62% CAGR between 2026 and 2031 due to rising diagnosis rates, robust clinical-trial activity, and improving reimbursement.

Why are inhaled therapies gaining traction?

Inhalation delivers drugs directly to lung tissue, significantly lowering systemic exposure and gastrointestinal side effects that drive high discontinuation with oral formulations.

Which drug type currently leads market share?

Pirfenidone held 43.35% idiopathic pulmonary fibrosis market share in 2025, although nintedanib is advancing rapidly because of its broader fibrosing-ILD label.

How are high therapy costs being addressed?

Manufacturers are exploring value-based pricing, generic launches post-patent expiry, and patient assistance programs to expand accessibility, especially in emerging economies.

What pipeline therapies could reshape the competitive landscape?

Boehringer Ingelheim’s nerandomilast, Bristol Myers Squibb’s admilparant, and integrin inhibitor bexotegrast from Pliant Therapeutics are among the late-stage agents that may redefine standard of care if approved.

Page last updated on: