Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.31 Billion |

| Market Size (2026) | USD 1.38 Billion |

| Market Size (2031) | USD 1.82 Billion |

| Growth Rate (2026 - 2031) | 5.58% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Brazil Diagnostic Imaging Equipment Market Analysis by Mordor Intelligence

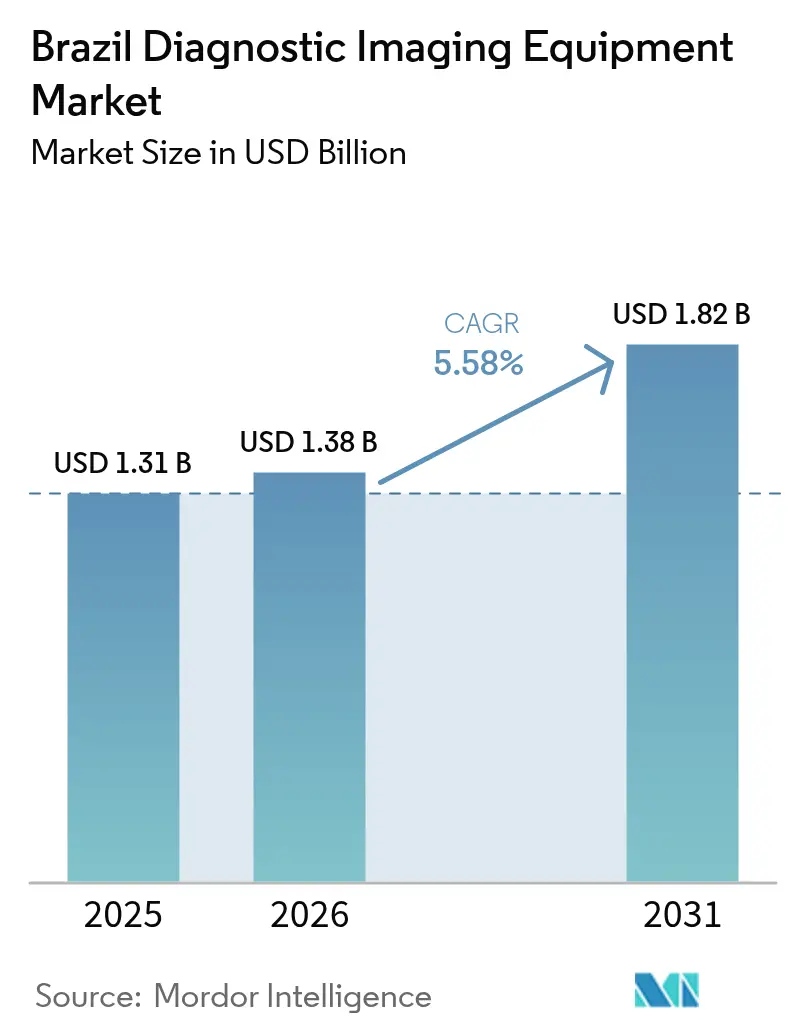

The Brazil Diagnostic Imaging Equipment Market size is expected to grow from USD 1.31 billion in 2025 to USD 1.38 billion in 2026 and is forecast to reach USD 1.82 billion by 2031 at 5.58% CAGR over 2026-2031.

The healthcare market is undergoing a significant transformation, driven by the shift toward high-complexity modalities, an aging installed base in public hospitals, and ANVISA’s pro-innovation reforms. Private hospital chains and diagnostic networks are expediting procurement processes to comply with federal mandates for faster oncology and stroke diagnostics. Simultaneously, municipal entities are preparing to capitalize on the September 2025 procurement reform, which will enable direct equipment purchases. The rapid adoption of teleradiology is facilitating the deployment of mobile ultrasound and X-ray units in underserved interior regions. Furthermore, AI-enabled software retrofits are extending the operational lifespan of older CT and MRI scanners. Local manufacturing incentives, such as Rota 2030 and PADIS, are helping global vendors mitigate import tariffs, ensuring stable unit sales despite currency fluctuations.

Key Report Takeaways

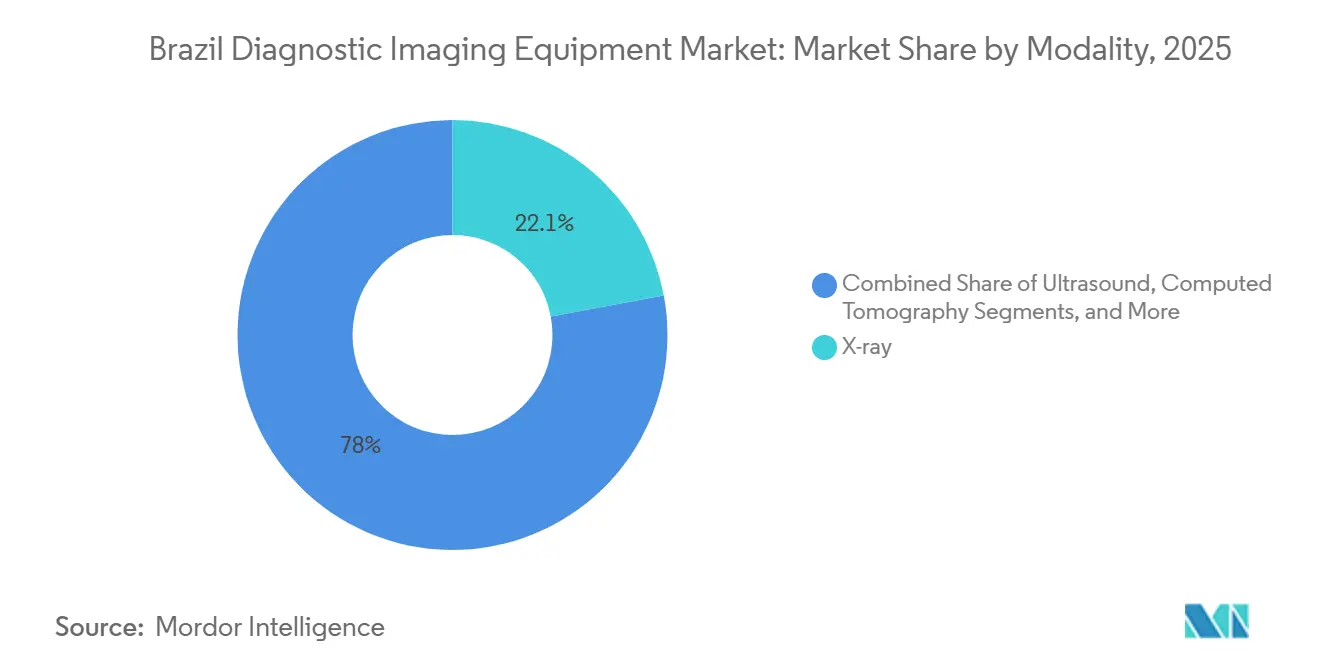

- By modality, X-ray systems led with 22.05% of the Brazil diagnostic imaging equipment market share in 2025, while MRI is advancing at a 7.54% CAGR through 2031.

- By portability, fixed installations commanded 81.62% of 2025 revenue, whereas mobile and hand-held systems are projected to post a 7.86% CAGR to 2031.

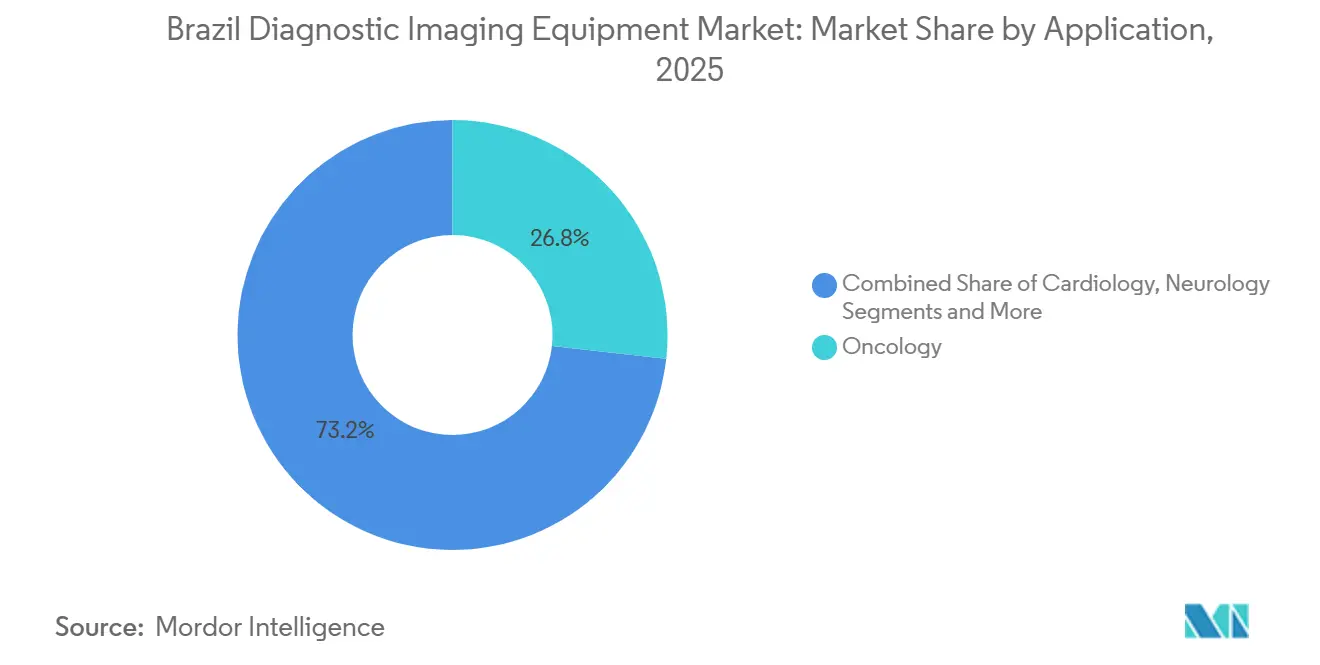

- By application, oncology accounted for 26.76% of overall spending in 2025; neurology imaging is forecast to expand at a 8.21% CAGR during 2026-2031.

- By end-user, hospitals accounted for 58.54% of total sales in 2025, yet diagnostic imaging centers are on track for a faster 6.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Diagnostic Imaging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden Of Chronic And Lifestyle Diseases | +1.2% | National, with concentration in Southeast and South regions | Long term (≥ 4 years) |

| Accelerating Population Aging And Imaging Utilization | +0.9% | National, acute in Southeast and South; emerging pressure in Central-West | Medium term (2-4 years) |

| Ongoing Digital Transformation And Modalities Upgrade Cycles | +1.1% | National, led by private hospital chains in São Paulo, Rio de Janeiro, and Belo Horizonte | Medium term (2-4 years) |

| Expanding Public-Private Healthcare Investment Programs | +1.4% | National, flagship projects in São Paulo; spillover to Northeast via federal programs | Short term (≤ 2 years) |

| Rapid Growth Of Teleradiology Start-Ups Enabling Rural Market Penetration | +0.6% | North and Northeast regions, rural municipalities >50 km from tertiary centers | Medium term (2-4 years) |

| Local Manufacturing Incentives Under Brazil's Rota 2030 And PADIS Programs | +0.4% | National, manufacturing hubs in Contagem (Minas Gerais) and Campinas (São Paulo) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic and Lifestyle Diseases

Brazil’s National Cancer Institute projects more than 704,000 new cancer cases each year between 2023 and 2025, and a Harvard study forecasts a 68% jump in incidence by 2040[1]National Cancer Institute, “Estimativa 2023–2025 Incidência de Câncer no Brasil,” inca.gov.br. Law 12.732/2012 obliges hospitals to begin cancer treatment within 60 days of diagnosis, yet 42.1% of colorectal patients breached that limit from 2013-2019, exposing facilities to penalties. Providers, therefore, race to add CT, PET/CT, and MRI capacity to compress diagnostic cycles. Cardiovascular disease and diabetes also propel uptake of cardiac CT angiography and vascular ultrasound. Equipment leasing and pay-per-scan contracts are emerging because public budgets cannot finance outright purchases, creating white space for vendors willing to assume asset risk.

Accelerating Population Aging and Imaging Utilization

Brazil’s population over 65 will climb from 10.8 million in 2025 to 14.7 million in 2031, creating disproportionate demand for orthopedic, neurology, and breast imaging. Mammography density stands at 13 units per million residents versus the OECD average of 24, underscoring a supply gap. The Atlas of Variation documented a 133.9-fold spread in mammography rates across health regions, indicating misallocated capacity. The New Development Bank’s USD 320 million Smart Hospital loan cites an 8,600-bed shortfall in metropolitan São Paulo as justification. Suppliers focusing on mobile mammography vans and point-of-care ultrasound can reach municipalities more than 50 km from tertiary sites, where fixed installations remain under-utilized.

Ongoing Digital Transformation and Modalities Upgrade Cycles

More than 66% of the MRI fleet is over 6 years old, so hospitals are prioritizing AI software that increases throughput without replacing the magnet. Philips’ Vue PACS now embeds Carpl.ai algorithms at flagship sites such as Hospital Israelita Albert Einstein and DASA, binding hardware refreshes to long-term software subscriptions. Fujifilm’s helium-free ECHELON Smart 1.5T MRI, previewed at Hospitalar 2025, eliminates recurring gas costs that plague remote sites with unreliable logistics. ANVISA’s AnvisAI program recruited 102 specialists in 2025 to streamline SaMD reviews under RDC 657/2022, yet forthcoming Bill 2,338/2023 will hard-wire liability rules that favor multinationals with deep compliance benches. Collectively, these factors are tilting capital budgets toward upgrade-ready platforms that support AI workflows out of the box.

Expanding Public-Private Healthcare Investment Programs

Rede D'Or has allocated R$7.5 billion (USD 1.5 billion) to expand its operations by adding 5,400 beds and has already installed three sealed-magnet MRI units in newly established facilities across Greater São Paulo. The network further strengthened its position by acquiring 11 Richet imaging centers, creating a unified procurement platform for vendors offering bundled solutions, including hardware, software, and maintenance. A procurement reform, effective September 2025, enables SUS hospitals to directly purchase capital equipment, bypassing delays associated with federal grants. Additionally, the New Development Bank is financing an 800-bed AI-enabled complex at Hospital das Clínicas through its Smart Hospital loan, with plans to integrate imaging data into Brazil’s RNDS health-data grid. Private equity investors are also aligning with this trend, channeling funds into mid-sized diagnostic chains that offer faster returns compared to traditional brick-and-mortar hospitals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Expenditure And Total Cost Of Ownership | -0.8% | National, acute in public sector and municipalities with limited fiscal capacity | Short term (≤ 2 years) |

| Shortage Of Skilled Radiology Workforce | -0.6% | National, severe in North and Northeast regions; São Paulo 10/100k, North <3/100k | Medium term (2-4 years) |

| Persistent Logistics Bottlenecks In Northern & Interior Regions | -0.3% | North and remote municipalities in Northeast and Central-West | Long term (≥ 4 years) |

| Regulatory Approval Delays For AI-Enabled Imaging Software | -0.2% | National, affecting multinational vendors and local AI start-ups | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure and Total Cost of Ownership

Only 1.9% of National Health Fund transfers flowed into the Investment block between 2019-2022, sharply limiting SUS purchases of CT and MRI units[2]Frontiers in Public Health, “Fiscal Space for Health Investment in Brazil,” frontiersin.org. Constitutional Amendment 95 further caps federal outlays, shifting financing to states that grapple with volatile tax receipts. Municipal tenders, such as the BRL 252,000 digital X-ray order from Anchietense Hospital, reveal how piecemeal and under-funded procurement can be. Total cost of ownership—including helium top-ups, training, and service contracts—often exceeds the purchase price over the course of a decade. Consequently, vendors marketing equipment-as-a-service or pay-per-scan packages, such as the IAEA-facilitated SPECT lease in Niterói, gain traction in markets with tight capital budgets.

Shortage of Skilled Radiology Workforce

Radiology density ranges from 10 per 100,000 residents in São Paulo to fewer than 3 per 100,000 in the North, depressing utilization even where scanners exist. The Atlas of Variation shows thrombolysis is absent in 270 of 450 health regions because no specialist can interpret emergency CT scans in time. While Siemens and Galileu Health launched a teleradiology backbone for São Paulo in 2025, only two-thirds of Basic Health Units reported reliable internet in the latest national audit. Public training budgets prioritize primary-care physicians under the More Doctors program, leaving specialist shortages unresolved. Vendors bundling remote-reading services and on-site training, therefore, enjoy a strategic edge when pitching advanced modalities to understaffed hospitals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: MRI’s Rapid Ascendancy in Oncology Protocols

In 2025, X-ray captured a 22.05% share of Brazil's diagnostic imaging equipment market, reinforcing its critical role in emergency departments. Meanwhile, MRI is projected to achieve a 7.54% CAGR through 2031, representing the fastest growth within Brazil's diagnostic imaging market. The increasing prevalence of oncology cases and rising neurology workloads are driving the adoption of AI-enabled 1.5 T and 3 T systems, which significantly enhance efficiency by reducing scan times. Hospitals are increasingly adopting helium-free magnets, such as the ECHELON Smart platform, citing benefits like lower lifecycle costs and improved supply-chain resilience in remote areas. While CT maintains a large installed base, over 66% of its units are more than six years old. Consequently, many facilities are implementing dose-optimization software like SubtleHD™ instead of investing in new scanners. Ultrasound continues to dominate obstetrics and rural care, supported by battery-powered Mindray models that enable seamless image uploads when connectivity is available. Although nuclear medicine remains a niche segment, it is highly profitable; for example, United Imaging’s total-body PET/CT at the Portuguese Charity of São Paulo delivers unmatched oncology throughput compared to partial-body systems.

The growing prominence of MRI is reshaping procurement strategies. Rede D'Or's deployment of sealed magnets highlights the willingness of private healthcare chains to invest in advanced technology that minimizes downtime and mitigates helium supply risks. Compliance with Law 12.732/2012, which mandates timely malignancy confirmation, is driving hospitals to rely on multiparametric MRI for precise biopsy planning. X-ray manufacturers are differentiating their offerings with dose-tracking dashboards that meet the stringent IEC 60601-2-54 standard, a key requirement in municipal tenders. CT vendors are partnering with AI firms to introduce retrofits that reduce radiation exposure by up to 40% while extending the lifespan of existing assets, a critical advantage for budget-constrained SUS hospitals. Mammography vendors are addressing the market's low penetration rate by offering turnkey screening solutions funded through public-private partnerships. As a result, the market is shifting towards high-field MRI and AI-enhanced CT, while value-tier mobile X-ray and ultrasound systems continue to sustain unit volumes in primary care settings.

By Portability: Mobile Systems Extend Care Beyond Megacities

In Brazil's diagnostic imaging equipment market, hospital-based imaging hubs dominated, contributing 81.62% of the revenue in 2025. However, with the increasing adoption of teleradiology, mobile and handheld units are projected to grow at a CAGR of 7.86% through 2031. Rural municipalities in the North, constrained by limited road infrastructure, rely on riverboats and aeromedical teams equipped with battery-powered ultrasound and X-ray devices. A study conducted in the Legal Amazon demonstrated the effectiveness of portable scanners, showing that equipping medevac helicopters expanded emergency service coverage to 71% of the population from nine operational bases. As a result, the mobile platform segment within Brazil's diagnostic imaging market is expected to witness the fastest growth in the North and Northeast, where workforce and infrastructure gaps are most pronounced.

Urban hospitals are also shifting toward mobility for bedside imaging, optimizing the utilization of fixed CT and MRI suites. The New Development Bank's "Smart Hospital" initiative incorporates Wi-Fi-enabled imaging carts for remote wards, enabling radiologists to analyze scans without relocating fragile patients. Vendors such as Fujifilm are leveraging INMETRO-certified lithium batteries that provide full-shift power while adhering to infection-control standards by eliminating power cables. Additionally, AI-enabled edge processing integrated into probes now delivers preliminary interpretations, reducing the workload on the limited pool of specialists. With private insurers reimbursing portable scans at rates comparable to fixed-site imaging, the adoption of mobile solutions is further incentivized. Consequently, the demand for portable imaging solutions is expanding from remote river docks to advanced tertiary ICUs, creating a new layer of growth alongside the established dominance of fixed-site imaging.

By Application: Oncology Leadership Reflects Disease Burden

In 2025, oncology accounted for 26.76% of total spending, maintaining its dominant position. However, neurology is projected to experience the fastest growth, with an 8.21% CAGR through 2031, as Brazil focuses on addressing its stroke-care gap. Thrombolysis usage remains below 1% across 394 health regions, prompting federal authorities to allocate funds for CT and MRI units capable of executing stroke protocols within the therapeutic window. Bracco’s AiMIFY™ software, which received ANVISA clearance in November 2025, enhances lesion-contrast sensitivity, a development that physicians regard as critical for accelerating ischemia mapping. Cardiology is leveraging DASA’s extensive network of 521 facilities to standardize cardiac CT angiography, while orthopedics increasingly relies on MRI for cartilage assessments to meet the needs of an aging population. Obstetrics is also expanding, driven by the adoption of handheld ultrasound devices that reduce barriers to prenatal care.

Oncology’s leadership is underpinned by INCA’s cancer incidence forecasts and the statutory 60-day treatment rule, which mandates capacity expansion even in budget-constrained public healthcare centers. PET/CT upgrades are eligible for PADIS tax incentives if vendors incorporate local content, directing demand toward manufacturers with Brazilian assembly operations. Neurology’s robust growth is fueled by the Ministry of Health’s efforts to reduce the 2.3 million disability-adjusted life years lost to strokes in 2025. Diagnostic chains are strategically positioning neurology suites near emergency departments to capture time-sensitive referrals. Additionally, AI-enhanced MRI technology is gradually entering the dementia screening market, which holds significant potential given Brazil’s forecast of 5.1 million Alzheimer’s patients by 2035. While oncology continues to lead in revenue, neurology is emerging as the key growth driver in Brazil’s diagnostic imaging equipment market.

By End-User: Diagnostic Centers Accelerate on Vertical Integration

In Brazil's diagnostic imaging equipment market, hospitals accounted for 58.54% of expenditures in 2025. However, diagnostic imaging centers are projected to grow at a 6.54% CAGR, outpacing the growth of inpatient facilities. Rede D'Or’s acquisition of Richet highlights a strategic move, as chains increasingly integrate outpatient scanners into hospital operations to capture a larger share of imaging revenues. DASA, managing over 200 million exams annually—35% of which are imaging—leverages its scale to negotiate bulk discounts on multi-scanner roll-outs, effectively reducing per-scan costs. Diagnostic centers, with streamlined compliance procedures, are adopting AI software like Philips’ chest-X-ray algorithm suite at a faster pace. Meanwhile, specialty clinics, though smaller in scale, cater to affluent urban patients who pay cash for immediate services such as breast MRIs or musculoskeletal scans.

Hospitals remain critical for emergency and interventional imaging, with initiatives like the Smart Hospital project set to strengthen São Paulo’s public network. This project will add 800 beds and advanced imaging modalities, integrating AI scheduling with tele-ICU coverage. The September 2025 procurement reform granted SUS entities greater flexibility, but limited federal transfers to capital budgets continue to constrain public hospitals, forcing many to rely on leasing or vendor credit for scanner financing. In contrast, diagnostic centers are leveraging private equity and insurer partnerships to expand capacity beyond the limitations of public budgets. Specialty clinics are thriving by offering personalized care; for example, breast centers combine mammography, ultrasound, and MRI services under one roof, utilizing compact equipment suited to their limited space. While hospitals retain their position as revenue leaders, outpatient chains are driving the fastest growth in Brazil's diagnostic imaging equipment market.

Competitive Landscape

The diagnostic imaging equipment market in Brazil is moderately concentrated, with key players such as GE Healthcare, Siemens Healthineers, and Philips leveraging localized production under Rota 2030 to avoid high import tariffs. GE operates a remanufacturing facility in Contagem, extending the lifecycle of X-ray and mammography equipment to cater to cost-sensitive public sector buyers. Siemens utilizes PADIS credits to ensure rapid delivery of CT scanners from its Joinville logistics hub, guaranteeing shipment to any Southeast client within 48 hours. Philips strengthens customer retention by offering multi-year AI and PACS subscription packages, which combine software updates with hardware refresh cycles, effectively increasing switching costs.

Chinese competitors, including United Imaging and Mindray, are disrupting price points by importing sub-assemblies for final testing in São Paulo's free-trade zones. United Imaging’s subsidiary, launched in July 2025, introduced total-body PET/CT systems capable of completing full-body scans in under 20 minutes, addressing the needs of high-volume oncology centers. Mindray, with a 16-year presence in the region, reports its ultrasound systems are installed in 80% of Latin American medical institutions, with sales increasing by 25% year-on-year in 2024. Canon Medical and Fujifilm compete in helium-free MRI and enterprise imaging IT, respectively, while Esaote and Neusoft focus on niche segments such as low-field MRI and compact CT systems.

Market players are transitioning from unit sales to lifetime-value business models. Siemens, through a February 2025 partnership with Galileu Health, has integrated cloud teleradiology services in rural São Paulo, enabling revenue generation through per-study billing. Philips, via its Vue-Carpl.ai integration, offers algorithm-as-a-service, tying customers to annual licenses indexed to exam volumes. Regulatory advancements, such as ANVISA’s AnvisAI fast-track, have reduced software approval timelines from 180 days to under 90 for compliant dossiers, favoring companies with robust regulatory capabilities and creating challenges for smaller AI startups. Additionally, the anticipated passage of Bill 2,338/2023, which aims to codify algorithm liability, is expected to consolidate market power among the top six vendors capable of managing associated legal costs.

Brazil Diagnostic Imaging Equipment Industry Leaders

-

GE Healthcare

-

Siemens Healthineers

-

Koninklijke Philips N.V.

-

Canon Medical Systems

-

Fujifilm Holdings Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Bracco Imaging secured ANVISA clearance for AiMIFY, an AI-powered MRI brain package that doubles contrast sensitivity for stroke and dementia protocols.

- August 2025: Subtle Medical won ANVISA approval for SubtleHD MRI software, claiming up to 80% quicker scans and partnering with Hospiline for distribution.

- July 2025: United Imaging inaugurated its Brazilian subsidiary to market total-body PET/CT and AI-embedded workflows targeted at oncology centers.

Brazil Diagnostic Imaging Equipment Market Report Scope

As per the scope of the report, diagnostic imaging equipment refers to medical devices used to create visual representations of the interior of the body for diagnosis and treatment planning. Examples include MRI, CT scans, X-ray, and ultrasound machines.

The Brazil Diagnostic Imaging Equipment Market Report is Segmented by Modality (X-Ray, Ultrasound, Computed Tomography, MRI, Nuclear Imaging, Fluoroscopy & C-Arms, and Mammography), Portability (Fixed Systems and Mobile & Hand-Held Systems), Application (Oncology, Cardiology, Neurology, Orthopedics, Obstetrics & Gynecology, and Other Applications), and End-User (Hospitals, Diagnostic Imaging Centers, and Specialty Clinics). The report offers the value (in USD million) for the above segments.

By Modality

| X-Ray |

| Ultrasound |

| Computed Tomography |

| MRI |

| Nuclear Imaging (PET/SPECT) |

| Fluoroscopy & C-Arms |

| Mammography |

By Portability

| Fixed Systems |

| Mobile & Hand-Held Systems |

By Application

| Oncology |

| Cardiology |

| Neurology |

| Orthopedics |

| Obstetrics & Gynecology |

| Other Applications |

By End-User

| Hospitals |

| Diagnostic Imaging Centers |

| Specialty Clinics |

| By Modality | X-Ray |

| Ultrasound | |

| Computed Tomography | |

| MRI | |

| Nuclear Imaging (PET/SPECT) | |

| Fluoroscopy & C-Arms | |

| Mammography | |

| By Portability | Fixed Systems |

| Mobile & Hand-Held Systems | |

| By Application | Oncology |

| Cardiology | |

| Neurology | |

| Orthopedics | |

| Obstetrics & Gynecology | |

| Other Applications | |

| By End-User | Hospitals |

| Diagnostic Imaging Centers | |

| Specialty Clinics |

Key Questions Answered in the Report

What is the projected value of the Brazil diagnostic imaging equipment market by 2031?

It is forecast to reach USD 1.81 billion, growing at a 5.58% CAGR between 2026 and 2031.

Which modality is expected to grow fastest through 2031 in Brazil?

MRI is projected to rise at a 7.54% CAGR, driven by oncology and neurology protocols.

Why are mobile imaging systems gaining popularity in Brazil?

Teleradiology start-ups and rural health programs need portable equipment that works in areas lacking fixed infrastructure and specialist coverage.

How will the new procurement law affect public hospitals?

The September 2025 amendment lets SUS facilities buy scanners directly, freeing them from federal grant delays and possibly speeding up equipment replacement.

Which companies dominate Brazil's diagnostic imaging space?

GE Healthcare, Siemens Healthineers, and Philips hold the largest combined share, with United Imaging and Mindray expanding rapidly.

Page last updated on: