Brazil Small Arms Ammunition Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

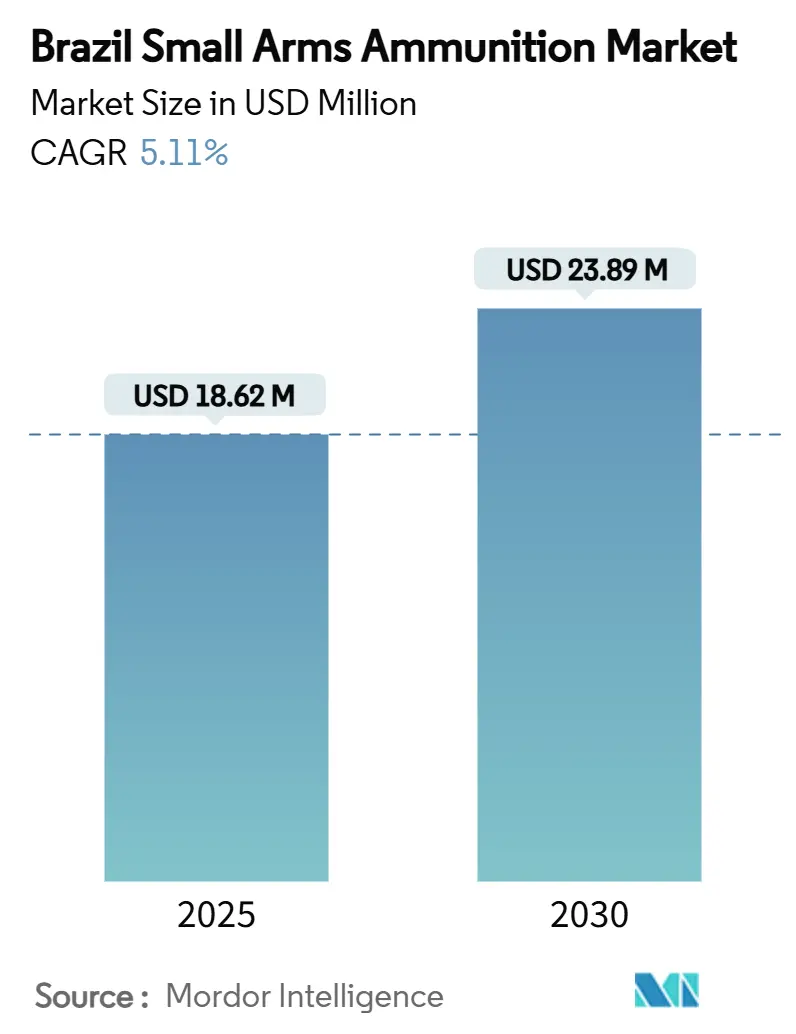

| Market Size (2025) | USD 18.62 Million |

| Market Size (2030) | USD 23.89 Million |

| Growth Rate (2025 - 2030) | 5.11% CAGR |

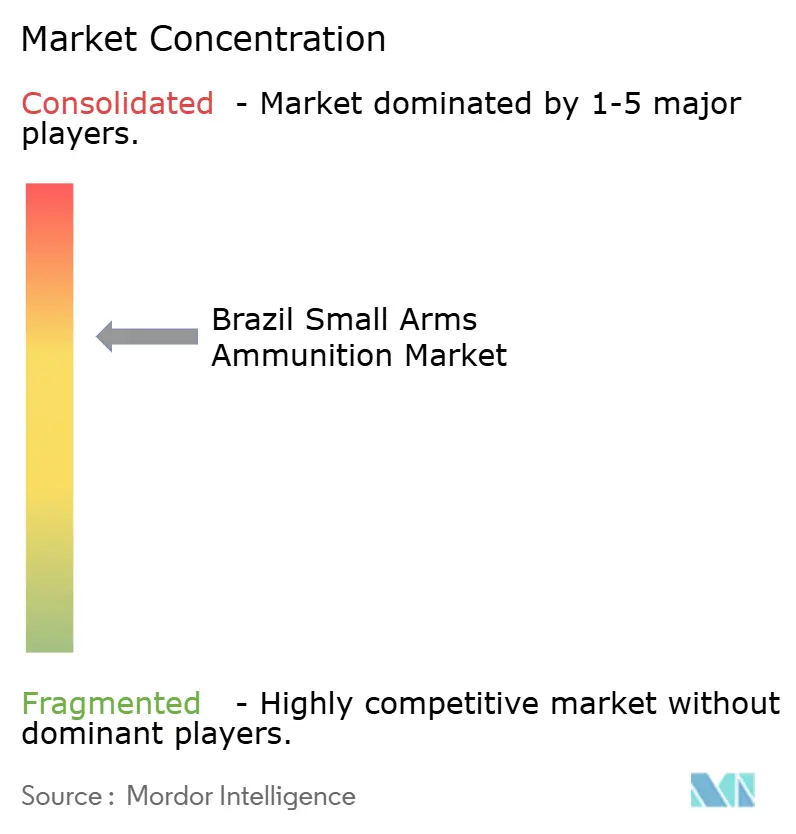

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Small Arms Ammunition Market Analysis by Mordor Intelligence

The Brazilian small arms ammunition market size stands at USD 18.62 million in 2025 and is forecasted to reach USD 23.89 million in 2030, advancing at a 5.11% CAGR from 2025 to 2030. Robust domestic demand, a sizeable installed base of legally owned firearms, and steady export momentum underpin this upward trajectory even as the regulatory environment tightens. Handgun rounds remain the volume anchor, while 9×19 mm retains leadership thanks to military standardization and civilian versatility. Stepped-up defense modernization, exemplified by the Brazilian Army’s 155 mm self-propelled howitzer program and mandatory local ammunition offsets, broadens industrial know-how. Parallel investments—such as CBC Global Ammunition’s USD 300 million US manufacturing unit—illustrate how local manufacturers hedge domestic uncertainty through foreign capacity and currency diversification. Supply-chain vulnerabilities in nitrocellulose and antimony continue to present cost and scheduling risks, but Brazil’s ability to process deteriorated propellants into spherical powders partly cushions the shock.

Key Report Takeaways

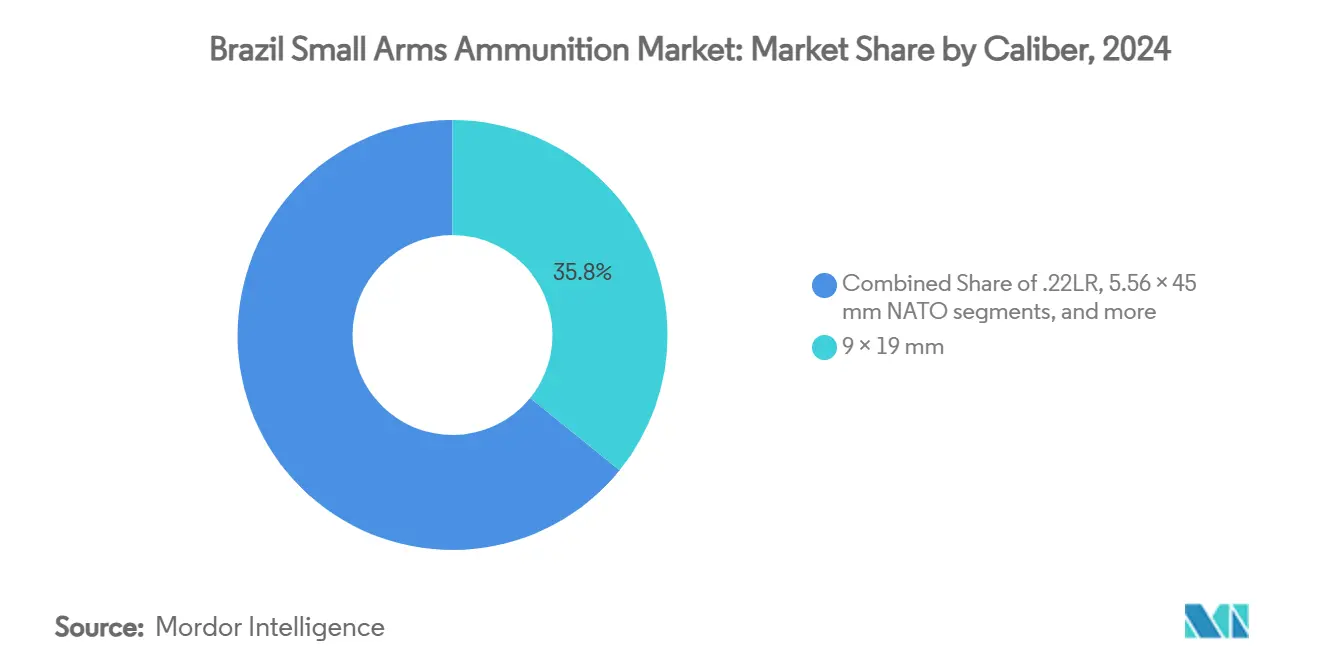

- By caliber, 9×19 mm claimed 35.84% of the Brazilian small arms ammunition market in 2024; the combined “Others” group is poised to advance at a 5.76% CAGR between 2025 and 2030.

- By end user, civilians accounted for 58.59% of the Brazilian small arms ammunition market share in 2024, while the military segment is projected to register the fastest 5.88% CAGR to 2030.

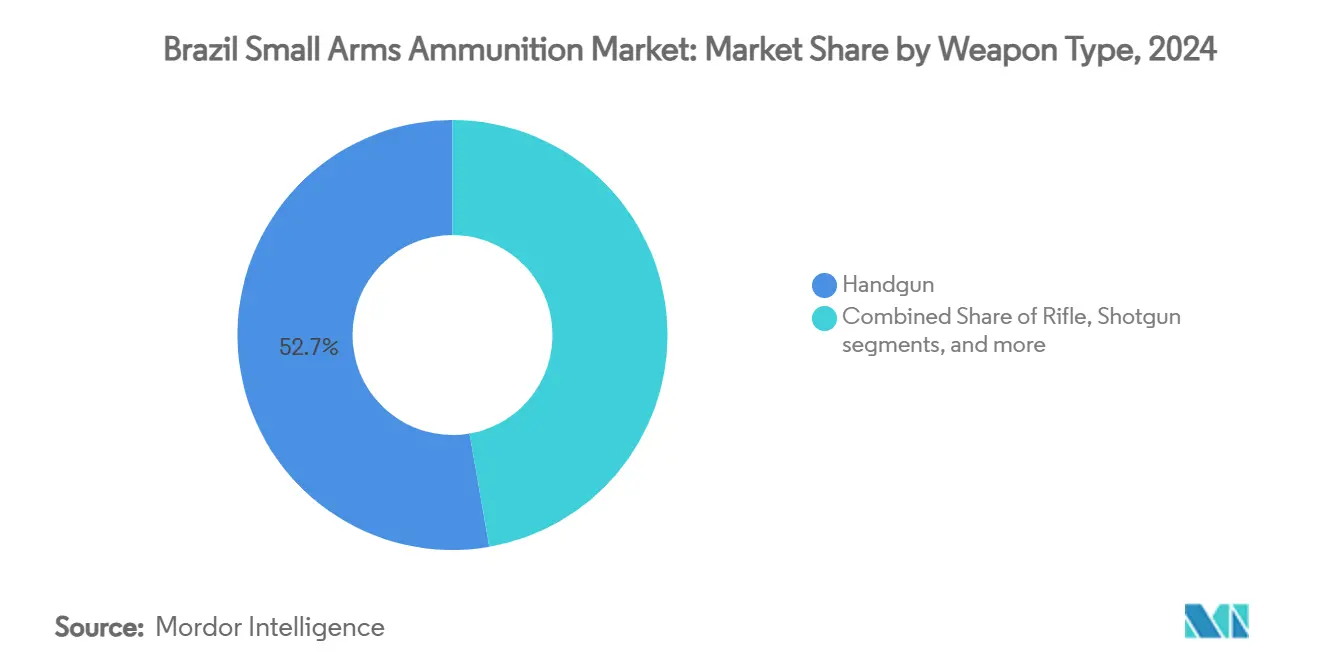

- By weapon type, handgun ammunition led with 52.73% revenue share in 2024; sub-machine gun and pistol-caliber carbine rounds are forecasted to expand at a 6.19% CAGR through 2030.

- By lethality, lethal cartridges dominated with a 98.74% share in 2024, while non-lethal rounds remain a niche and are poised to grow at a 4.90% CAGR during the forecast window.

Brazil Small Arms Ammunition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising civilian firearm ownership post-loosening of regulations | +1.2% | Urban centers nationwide | Medium term (2-4 years) |

| Modernization programs of Brazilian armed forces and police | +0.8% | National defense hubs | Long term (≥ 4 years) |

| Expansion of CBC’s export capacity and foreign demand | +1.0% | North and Latin America | Medium term (2-4 years) |

| Shift toward lead-free ammo driven by state environmental rules | +0.4% | Environmentally sensitive states | Long term (≥ 4 years) |

| Surge in competitive sport-shooting events boosting demand | +0.3% | Large metropolitan areas | Short term (≤ 2 years) |

| Offset-driven foreign OEM technology transfer | +0.6% | Defense-industry clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Civilian Firearm Ownership Post-Loosening of Regulations

During 2019-2022, permissive rules doubled legal civilian firearm holdings, lifting the installed base to roughly 1.5 million weapons among 980,000 CAC registrants. Even after stricter decrees in 2023 limited fresh gun purchases, the earlier surge preserved an entrenched cohort that consumes ammunition regularly. Current caps of 50 cartridges per gun—up to 600 for collectors—provide a stable minimum demand. The regulatory pendulum, therefore, creates a counter-cyclical effect: lower new gun sales coincide with steady ammunition replenishment, cushioning volume swings for manufacturers. Established brands benefit most, as compliance hurdles deter casual new entrants. The Brazilian small arms ammunition market continues to receive predictable civilian orders that underpin factory utilization.

Modernization Programs of Brazilian Armed Forces and Police

Defense procurement adds a structural growth layer. The army’s plan to buy 36 self-propelled 155 mm howitzers carries a USD 180 million budget and mandatory technology-transfer clauses to create the nation’s first domestic 155 mm shell line. Similar offset rules apply to projects exceeding USD 50 million, accelerating know-how diffusion into local firms. Police agencies are upgrading squad small-arms inventories and designated marksman gear, demanding match-grade rounds tailored for urban engagements. Military and law-enforcement frameworks, therefore, guarantee multiyear contracts that stabilize the Brazilian small arms ammunition market during times of civilian uncertainty.

Expansion of CBC’s Export Capacity and Foreign Demand

CBC Global Ammunition ships to more than 100 nations and has raised global output by nearly 2 billion rounds per year, thanks to plants in Brazil, Germany, and now the United States. The USD 300 million Oklahoma investment enlarges center-fire cartridge volume from 9 mm to 12.7 mm and links directly to US federal and state agency demand. The facility complements Brazilian lines, freeing domestic capacity for regional orders across Latin America and Africa. Because exports reached USD 590 million in 2023—a 33% jump year on year—foreign sales hedge domestic cycles and inject scale efficiencies into the Brazilian small arms ammunition market.[1]“Brazil | Imports and Exports | World | Arms and ammunition…,” TrendEconomy, trendeconomy.com

Shift Toward Lead-Free Ammo Driven by State Environmental Rules

In 2025, Brazil’s Chemical Management Law 15.022 began requiring registration of chemicals above one ton, pushing ammunition makers to review lead-bearing primer and projectile inputs. Environmental agency IBAMA has intensified inspections in sensitive biomes, highlighting lead contamination risks. Early-adopter states back non-toxic bullet initiatives for hunting reserves, nudging manufacturers toward copper or bismuth cores. These adaptations raise R&D spending and open premium sustainability niches inside the Brazilian small arms ammunition market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Potential tightening of gun laws (regulatory uncertainty) | -0.9% | Nationwide, uneven state enforcement | Short term (≤ 2 years) |

| Volatile prices of brass, lead and propellant chemicals | -0.4% | Global inputs, national plants | Medium term (2-4 years) |

| Crackdown on illegal trade and mandatory ammo traceability | -0.3% | Borders and urban hubs | Medium term (2-4 years) |

| Dependence on imported nitrocellulose/antimony supply chains | -0.5% | Global supply networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Potential Tightening of Gun Laws (Regulatory Uncertainty)

New registrations dropped 82% in 2023 after decrees capped personal defense ownership at three weapons. Portaria 299 now obliges all post-2019 firearms to re-register under SINARM, exposing owners to seizure risks if non-compliant. These shifts can suppress short-term purchases and unsettle production forecasts. Yet existing firearm owners still require ammunition, muting the adverse effect on the Brazilian small arms ammunition market. Makers favor flexible lines and export channels to hedge domestic volatility.

Volatile Prices of Brass, Lead and Propellant Chemicals

Copper and zinc price swings inflate cartridge-case costs, while global lead-smelting curbs tighten supply. Propellant inputs such as nitrocellulose track geopolitical disruptions, raising working-capital needs. Producers negotiate long-term supply contracts and explore alloy substitutions to keep the Brazilian small arms ammunition market price-competitive without eroding margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Caliber: NATO Standards Drive Market Concentration

The 9 × 19 mm segment represented 35.84% of the Brazilian small arms ammunition market share in 2024 and continues to anchor institutional and civilian demand through 2030. Military adoption of NATO specifications, widespread police standardization, and sport-shooting popularity give this caliber unmatched volume. Standardization also compresses per-unit production cost because tooling changes are minimal. Larger-bore 5.56 × 45 mm and 7.62 × 51 mm rounds enjoy stable orders from security forces and export clients, yet they trail 9 mm in absolute terms. Niche cartridges such as .40 S&W and .45 ACP rally when agencies refresh sidearm fleets, pushing the “Others” category toward a 5.76% CAGR. Emerging requirements for domestic 155 mm shells to support howitzer programs point to eventual diversification beyond small-caliber dominance. As technology transfer advances, heavier-caliber production lines may shift market composition in the late forecast window.

The Brazilian small arms ammunition market producers exploit economies of scale in 9 mm by synchronizing local and export batches, aligning Brazilian runs with US demand curves. That synchronicity keeps machinery utilization high and dampens cost inflation. The Brazilian small arms ammunition market size linked to 9 mm is expected to stay above USD 8 million by 2030, even as alternative calibers climb faster. Standard NATO-compatible rounds also bolster export credibility, making caliber choice a strategic commercial lever.

By End User: Civilian Dominance Despite Regulatory Headwinds

Civilian consumers held 58.59% of the Brazilian small arms ammunition market in 2024, underlining the importance of CAC members and security-conscious homeowners. Their forecasted 5.88% CAGR stems from replenishment rather than fresh gun purchases. The military accounts for the second-largest slice, propelled by artillery, infantry rifle, and crew-served-weapon upgrades. Police purchases, while smaller, command premium specifications such as barrier-blind performance and reduced ricochet risk, supporting higher unit pricing.

Regulatory tightening may lower casual hobbyist entry and disincentivize gray-market reloads, channeling volume toward compliant factories. Institutional buyers synchronize with budget cycles, adding predictability. As ammunition traceability systems mature, registered users become stickier customers, reinforcing a demand core that undergirds Brazil small arms ammunition market revenue.

By Weapon Type: Handgun Preference Reflects Urban Security Concerns

Handgun ammunition contributed 52.73% of total revenue in 2024 due to urban self-defense needs and sidearm prevalence in police forces. The market size for handgun rounds in Brazil will be USD 12 million by 2030. Sub-machine gun and pistol-caliber carbine rounds are forecasted to post a 6.19% CAGR thanks to law-enforcement tactical shifts toward compact, controllable platforms. Rifles and shotguns retain steady demand: rifles for military patrols and hunting, rural protection, and sporting clays.

High urban crime visibility sustains steady replenishment of personal-defense calibers, and police modernization reinforces official cycle purchases. Thus, manufacturers allocate the bulk of tooling capacity to 9 mm and .40 S&W handgun loads. Even so, incremental rifle ammunition demand from border patrol units ensures balanced product portfolios within the Brazilian small arms ammunition market.

By Lethality: Lethal Ammunition Dominance with Niche Non-Lethal Growth

Lethal cartridges occupied 98.74% of 2024 revenue and will grow at a 5.15% CAGR. Institutional doctrines prioritize proven terminal ballistics, leaving non-lethal offerings largely confined to rubber bullets and bean-bag rounds for riot control. These specialized items enjoy stable but modest volumes. Training environments adopt frangible or reduced-range loads to meet safety mandates, yet lethal ball and jacketed hollow-point rounds remain indispensable across user groups.

Export customers likewise prioritize lethal performance, reinforcing product-development focus. Environmental directives may stimulate lead-free lethal designs sooner than broad non-lethal adoption. Consequently, lethal lines dominate capital investment plans, and non-lethal extensions remain ancillary in the Brazilian small arms ammunition market.

Geography Analysis

Domestic consumption anchors roughly 70% of the Brazil small arms ammunition market, fed by an installed base of 4.4 million privately held guns and routine military demand. Urban agglomerations such as São Paulo, Rio de Janeiro, and Brasília account for the bulk of handgun cartridge turnover. At the same time, rural North and Central-West regions absorb rifle and shotgun loads for pest control and subsistence hunting. Federal Police oversight of at least 4.8 million firearms from 2025 onward is expected to improve compliance and data clarity, supporting long-term market forecasting.

Export channels diversify revenue and cushion domestic cyclicality. In 2023, Brazil shipped USD 590 million worth of arms and ammunition, of which 55% went to the United States. Strong US retail demand and federal purchases explain CBC’s decision to establish its third plant in Oklahoma. Latin America absorbs calibers standard to regional police inventories, while Africa and Asia buy bulk military lots through government-to-government agreements.

Production clusters in Rio Grande do Sul and São Paulo benefit from skilled labor and supportive sub-national policies to attract defense contractors.[2]Christiano Cruz Ambros, “Experiências Subnacionais…,” ufrgs.br Proximity to Santos and Rio Grande ports streamlines outbound logistics, enhancing export competitiveness. Border states confront illicit trafficking that diverts legal ammunition, prompting joint operations between IBAMA and federal police that temporarily depress grey-market leakage.[3]Ibama, “Ibama e PRF embargam…,” ibama.gov.br Over time, tighter controls should channel wary buyers toward licensed outlets, indirectly aiding legitimate sales.

Competitive Landscape

The Brazil small arms ammunition market is moderately concentrated. CBC Global Ammunition commands the most significant share through a two billion-round annual capacity spread across plants in Brazil, Germany, and the United States. Its USD 300 million Oklahoma site gives logistical proximity to key buyers and demonstrates strategic hedging against domestic regulatory shifts. State-owned IMBEL secures military tenders for rifle and machine-gun calibers, ensuring internal competition that encourages price discipline.

Smaller specialists occupy niches such as lead-free match ammo, leveraging agile lines and quicker regulatory approvals. Offset clauses lure foreign OEMs into co-producing artillery shells, gradually increasing technological diffusion into local firms.

Traceability mandates confer advantage on established players with robust ERP systems capable of granular lot reporting. Commodity swings squeeze low-scale reloaders, while environmental rules amplify capex requirements, nudging the competitive field toward well-capitalized manufacturers. Export accreditation remains a soft barrier, as decades-old import protocols favor incumbents already approved by the US BATFE and NATO maintenance agencies.

Brazil Small Arms Ammunition Industry Leaders

CBC Global Ammunition

BAE Systems plc

Aguila Ammunition

Nammo AS

Sellier & Bellot a.s.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Fonte Segura reported the police oversight expansion to at least 4.8 million firearms by 2025.

- December 2024: Taurus Armas secured a contract through an international bidding process initiated by the Ministry of Justice and Public Security. The contract involves supplying 37,102 Taurus TS9 9mm caliber semi-automatic pistols to 14 Brazilian states participating in the National Security Force.

- May 2024: The Brazilian House of Representatives signed a contract with Companhia Brasileira de Cartuchos (CBC) to supply ammunition to its Legislative Police. The Legislative Police is the internal security force responsible for protecting lawmakers and congressional premises. The procurement aims to enhance operational readiness, support regular training, and ensure ammunition compatibility with the force's existing firearms.

- March 2022: Brazil's IMBEL completed and delivered the first batch of new 7.62x51mm IA2 rifles to the Brazilian Army's Army Evaluation Center (CAEx) for extensive testing. The batch consisted of 50 rifles. This development is expected to drive the growth of Brazil's small arms ammunition market, supported by increasing military modernization efforts and domestic defense manufacturing capabilities.

Brazil Small Arms Ammunition Market Report Scope

| .22 LR |

| 9×19 mm |

| 5.56×45 mm NATO |

| 7.62×51 mm NATO |

| Others (.40S&W, .45 ACP, .38 Special) |

| Military |

| Government |

| Civilian |

| Handgun |

| Rifle |

| Shotgun |

| Sub-Machine Gun/Pistol-Caliber Carbine |

| Lethal |

| Non-Lethal |

| By Caliber | .22 LR |

| 9×19 mm | |

| 5.56×45 mm NATO | |

| 7.62×51 mm NATO | |

| Others (.40S&W, .45 ACP, .38 Special) | |

| By End-User | Military |

| Government | |

| Civilian | |

| By Weapon Type | Handgun |

| Rifle | |

| Shotgun | |

| Sub-Machine Gun/Pistol-Caliber Carbine | |

| By Lethality | Lethal |

| Non-Lethal |

Key Questions Answered in the Report

What is the current value of the Brazil small arms ammunition market?

The market is valued at USD 18.62 million in 2025.

How fast will the market grow by 2030?

It is forecasted to expand at a 5.11% CAGR, reaching USD 23.89 million.

Which caliber dominates sales?

The 9×19 mm round holds the largest 35.84% share because of its broad civilian and military use.

Who is the leading manufacturer?

CBC Global Ammunition leads with around 60% domestic revenue and global output near 2 billion rounds per year.

How is environmental regulation influencing product trends?

Brazil REACH and IBAMA enforcement are pushing producers toward lead-free alternatives, creating a premium niche while raising compliance costs.

What supply-chain risk is most significant?

Dependence on imported nitrocellulose and antimony exposes producers to price spikes and shortages, affecting powder and primer availability.

Page last updated on: