Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 22.76 Billion |

| Market Size (2026) | USD 23.67 Billion |

| Market Size (2031) | USD 28.82 Billion |

| Growth Rate (2026 - 2031) | 4.01% CAGR |

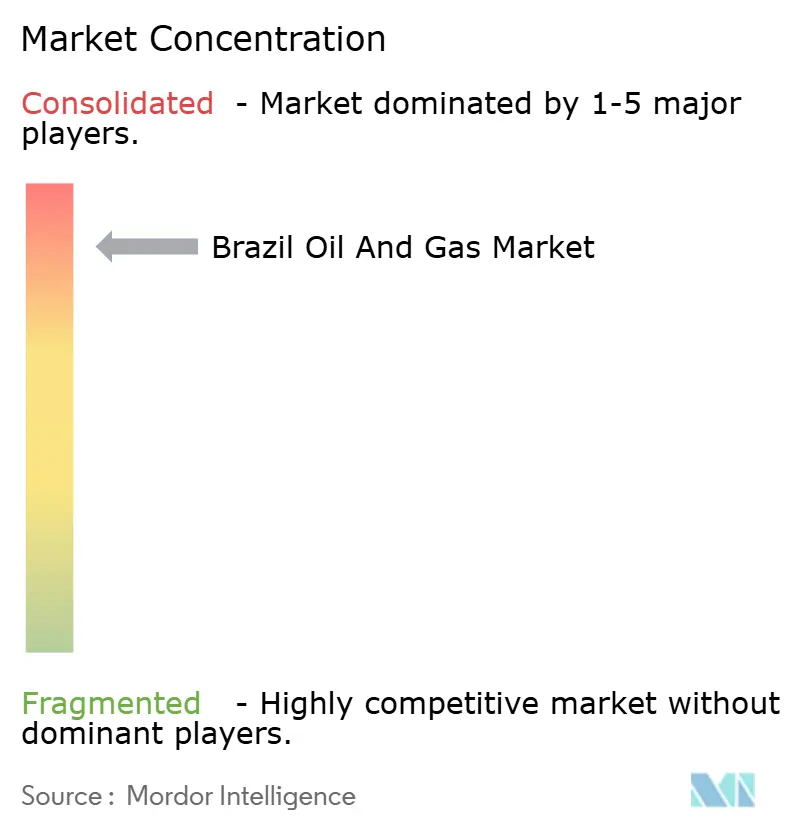

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Oil And Gas Market Analysis by Mordor Intelligence

The Brazil Oil And Gas Market size is expected to grow from USD 22.76 billion in 2025 to USD 23.67 billion in 2026 and is forecast to reach USD 28.82 billion by 2031 at 4.01% CAGR over 2026-2031.

Robust pre-salt output, steady midstream build-out, and fuel-switching policies keep demand resilient even as financing conditions tighten. Upstream activity dominates capital flows because pre-salt reservoirs offer record productivity and competitive lifting costs, while government auctions are unlocking new acreage for both state-owned and private operators. Midstream growth accelerates as new gas pipelines lower reinjection rates and feed rising gas-to-power projects, and downstream liberalization brings efficiency gains by allowing independent refiners to modernize assets. Private capital, advanced digital oilfield tools, and carbon-capture pilots support operational efficiency, whereas local-content rules and refining bottlenecks temper margins.

Key Report Takeaways

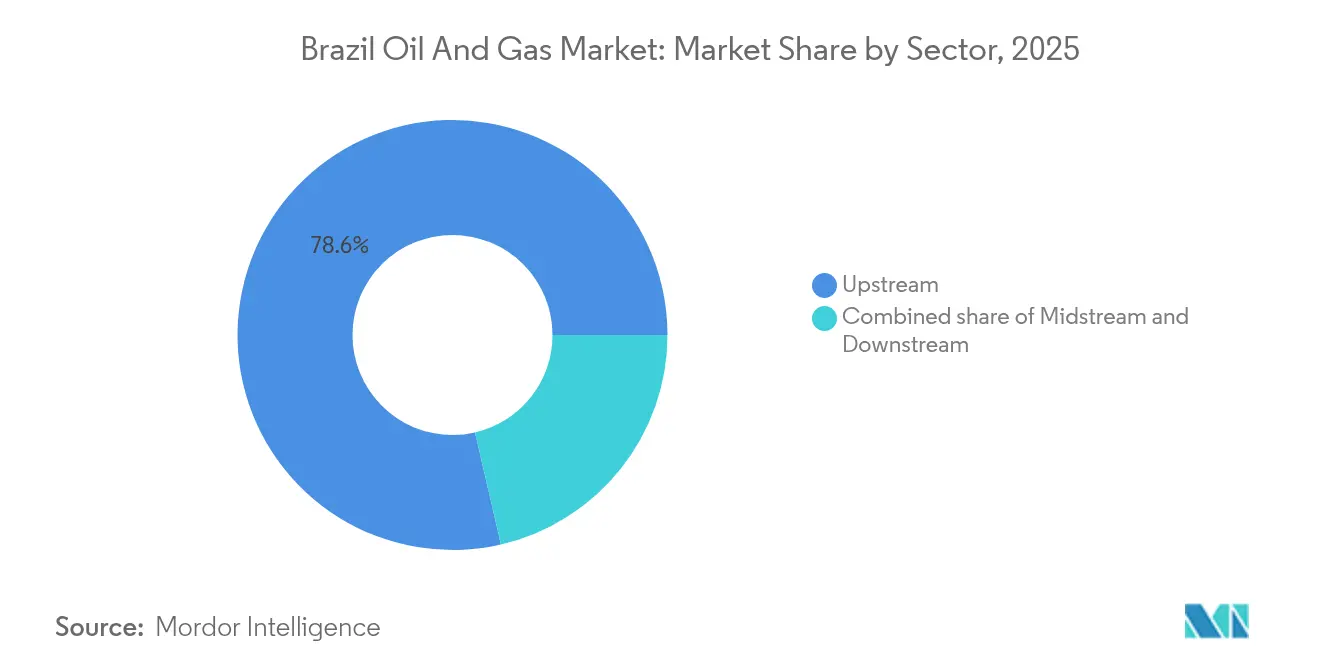

- By sector, the upstream sector accounted for 78.62% of Brazil's oil and gas market share in 2025 and is projected to post the fastest growth of 4.27% CAGR through 2031.

- By location, onshore fields captured 75.40% revenue share in 2025, while offshore operations are expected to rise at a 5.63% CAGR to 2031.

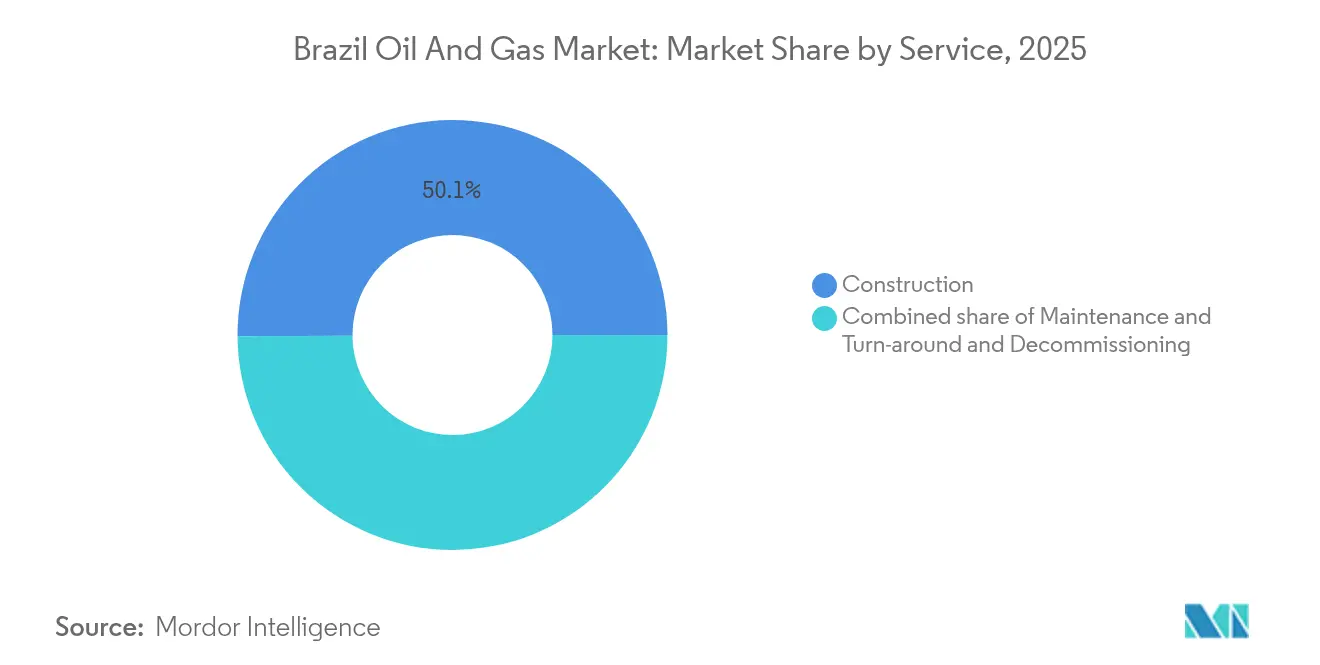

- By service, construction accounted for 50.10% of demand in 2025; decommissioning is the fastest-growing service, with a 6.44% CAGR to 2031.

- Petrobras produced 90.19% of the nation's hydrocarbons in 2024; however, ongoing divestments are widening the room for international majors and local independents.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Oil And Gas Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated pre-salt production ramp-up 2025-2029 | 1.20% | Santos and Campos Basins, offshore Brazil | Medium term (2-4 years) |

| 13th & 14th ANP bid rounds spurring E&P CapEx (2024+) | 0.80% | National, with concentration in equatorial margin | Short term (≤ 2 years) |

| Petrobras divestments opening mid/down-stream to private capital | 0.60% | National, with focus on Northeast refineries | Medium term (2-4 years) |

| Gas-to-Power build-out under New Gas Law | 0.40% | National, with emphasis on Northeast and Southeast | Long term (≥ 4 years) |

| Digital oilfield adoption (AI-driven well optimisation) | 0.30% | Offshore pre-salt and post-salt fields | Medium term (2-4 years) |

| Under-reported: CCS hubs linked to depleted Campos fields | 0.20% | Campos Basin, Rio de Janeiro state | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Pre-Salt Production Ramp-Up 2025-2029

Pre-salt wells delivered 71.5% of Brazil’s 36.9 million b/d output in 2024, and the Tupi field alone pumped 780,050 b/d in March 2025.[1]Agência Brasil, “Brazil Tops Soy Exports With Oil in 2024,” agenciabrasil.ebc.com.br Five FPSOs operating at Búzios have already reached a combined production of 600,000 b/d, and two additional units (P-84 and P-85) are expected to add a combined 450,000 b/d by 2030. Petrobras plans to channel USD 79 billion of its 2025-2029 budget to exploration and production, enabling Brazil to target a top-five global export slot before 2030. Thick evaporite layers at 5,500–6,500 m seal the reservoirs, allowing CO₂-injection pilots that may unlock 5.7 billion extra barrels and sequester 266 million t of CO₂ over two decades. Rising volumes underpin foreign-exchange inflows, helping Brazil overtake soybeans as its chief export in 2024.

13th & 14th ANP Bid Rounds Spurring E&P CapEx

The ANP’s recent licensing rounds offered 173 blocks, attracting Chevron, Shell, and others despite environmental scrutiny. The South Santos and Pelotas awards in 2024 deepened portfolio diversity, while the Foz do Amazonas basin made its debut on the permanent offer list with 47 offshore blocks. Brazil’s mixed model of concession and production-sharing contracts strikes a balance between investor flexibility and state revenue, with ANP estimating USD 428-474 billion of upstream spending through 2031. Early-stage seismic and appraisal work is accelerating as operators seek a stake in the next pre-salt analogue.[2]ANP, “13th & 14th Licensing Round Results,” anp.gov.br

Petrobras Divestments Opening Mid/Down-Stream to Private Capital

The USD 1.8 billion sale of RLAM to Mubadala Capital in 2024 signalled a structural downstream shift. TAG’s network integration with a private LNG terminal in October 2024 illustrated how new entrants are reshaping gas logistics. TAG targets BRL 5.2 billion in pipeline upgrades by 2028, while Petrobras continues to implement selective divestments to focus on its core ultra-deepwater acreage. Wider ownership encourages efficiency, lifts domestic refining utilisation, and diversifies funding channels.

Gas-to-Power Build-Out Under New Gas Law

Natural gas output climbed to 165.53 million m³/d in March 2025, a 15% year-over-year rise supported by Rota 3’s 44 million m³/d capacity. The 2021 New Gas Law fosters third-party access and caps reinjection volumes, ensuring molecules reach power plants when hydro reservoirs are depleted. Petrobras has already signed a BRL 6.4 billion, price-indexed supply deal with Compagas, effective 2025, and it has launched its first biomethane tender, which mandates 1% renewable content from January 2026. Competitive tariffs and increased supply security should stabilize electricity costs and catalyze further thermal capacity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Local-content rules raising project costs | -0.90% | National, with higher impact on offshore projects | Medium term (2-4 years) |

| Persistent refinery under-capacity & fuel import volatility | -0.60% | National, with concentration in Northeast | Short term (≤ 2 years) |

| Rising offshore ESG-driven financing hurdles | -0.40% | Offshore pre-salt and post-salt operations | Long term (≥ 4 years) |

| Under-reported: Congested port logistics for LNG & FPSO modules | -0.30% | Santos, Suape, and major coastal ports | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Local-Content Rules Raising Project Costs

Resolution 726 resets minimum targets but still obliges operators to source specialized goods locally, thereby lifting FPSO and drilling costs as high as 60% above global yard averages.[3]Columbia Center on Sustainable Investment, “Local-Content Rules in Brazilian O&G,” ccsi.columbia.edu Verification requires third-party auditors and imposes scheduling risks, so the industry body IBP advocates for more flexible bidding credits. Compliance burdens weigh heaviest on fast-track pre-salt tie-backs, where limited domestic capacity for high-spec subsea hardware lengthens lead times and reduces supplier competition.

Persistent Refinery Under-Capacity & Fuel Import Volatility

Petrobras is investing USD 892 million to double RNEST’s capacity to 260,000 b/d by 2028, yet demand for gasoline and diesel is forecast to grow 2-3% annually, sustaining import dependence. Utilisation at Brazil’s 11 refineries is near technical limits, forcing the export of crude and the import of pricier refined products, which compresses margins and creates FX exposure. Higher biofuel blend mandates mitigate part of the shortfall; however, sustained product imbalances are likely to persist until 2030.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Upstream Consolidates Market Leadership

The upstream segment accounted for a 78.62% share of the Brazilian oil and gas market in 2025 and is also set to expand at a 4.27% CAGR from 2026 to 2031, confirming its dual status as both a revenue anchor and growth engine of the Brazilian oil and gas market. Pre-salt productivity drives this dominance, with the zone contributing 79.8% of national output in March 2025 and logging a record 3.716 million barrels of oil equivalent (boe) per day, more than any other single source in Latin America. Petrobras has earmarked USD 77.3 billion for exploration and production in its 2025-2029 plan, underscoring how capital continues to flow toward reservoir delineation, new wells, and fresh FPSO capacity even as financing conditions tighten. Midstream and downstream activities remain structurally smaller, yet they benefit from pipeline build-outs and divestments that invite private refiners and gas shippers to modernize assets.

Upstream dynamism also reflects the ANP's projection of USD 428-474 billion in national E&P spending through 2031, as recent bid rounds have opened new acreage to global majors looking to replicate pre-salt success. SLB's USD 800 million integrated-services award across more than 100 Petrobras wells demonstrates how service companies are incorporating AI-driven formation testing and real-time fluid mapping to reduce drilling cycles and increase recovery factors. Such technological advancements, combined with reliable flow rates of 15,000-20,000 barrels per day (b/d) per well, position Brazil to reach approximately 4.9 million barrels per day (b/d) by 2032, a level that would place Brazil among the world's top five crude oil exporters. Continued upstream consolidation, therefore, remains pivotal for generating foreign exchange, fiscal receipts, and long-term supply security.

By Location: Onshore Dominance Faces Offshore Challenge

Onshore assets held a 75.40% share of the Brazilian oil and gas market in 2025, mirroring decades of infrastructure rollout across mature fields in the Recôncavo, Potiguar, and Solimões basins. These areas benefit from lower lifting costs, established gathering systems, and proximity to refineries, making them reliable cash generators even as output naturally declines. Offshore projects, however, are moving faster, with a 5.63% CAGR projected for 2026-2031 as ultra-deepwater technology taps thicker pay zones and higher pressures that onshore geology cannot match. The pre-salt Gato do Mato development, slated to produce 120,000 b/d from 2029, exemplifies how newer hubs in the Santos Basin are reshaping Brazil’s production map and shifting corporate capital seaward.

Petrobras’s commissioning of the P-84 and P-85 FPSOs, each rated for 225,000 b/d and scheduled for 2029-2030 start-up, further underlines the growing offshore pull on national capex. Frontier licensing reinforces this tilt: forty-seven blocks in the Foz do Amazonas basin entered the permanent offer cycle for the first time in 2025, drawing bids from Petrobras-Chevron consortia despite environmental headwinds. While onshore fields still supply steady volumes and quick cash flow, the long-run growth narrative now rests on offshore rigs, subsea tie-backs, and high-capacity FPSOs that can monetize multi-billion-barrel reservoirs at competitive breakevens.

By Service: Construction Dominates as Decommissioning Accelerates

Construction activities accounted for 50.10% of 2025 spending, reflecting the size of the Brazil oil and gas market required to finance refineries, gas pipelines, and next-generation FPSOs that anchor production growth. Flagship examples include the USD 4.8 billion Reduc-Boaventura integration, which adds 76,000 b/d of diesel throughput, and the USD 892 million project to double RNEST capacity to 260,000 b/d by 2028, both designed to increase domestic product output and reduce import reliance. FPSO orders, although smaller today, are the fastest-growing asset type, poised for a 6.44% CAGR between 2026 and 2031, as mature shallow-water fields reach the end of their life and new trunk lines keep engineering yards busy, ensuring construction remains the single largest value-chain slice.

Decommissioning, though smaller today, is the fastest-growing asset type, poised for a 6.44% CAGR between 2026-2031 as mature shallow-water fields reach end-of-life and regulators tighten site-restoration rules. The ANP recently approved BRL 72 billion in guarantees for Petrobras to retire 127 fields, creating a surge of work in well plugging, pipeline flushing, and topside dismantling that specialist contractors are eager to capture. This lifecycle balance—simultaneous greenfield builds and brownfield retirements—enriches Brazil’s oil-service portfolio, embeds higher environmental standards, and signals a sector that is maturing into full-spectrum asset stewardship rather than a pure expansion mode.

Geography Analysis

Pre-salt riches anchor production in the Santos and Campos Basins off Rio de Janeiro and São Paulo, together producing 79.8% of national output in March 2025. The Santos cluster hosts Búzios, Tupi, and Mero, each linked to high-capacity FPSOs that simplify tie-backs and share gas export routes. Campos provides mature backlog and future CCS hubs, while the expansion of the Route 3 pipeline channels gas to the Southeast industrial corridor.

The Northeast is emerging as a downstream and LNG node. RNEST’s doubling to 260,000 b/d and Suape’s multipurpose terminal will cut clean-product deficits and underwrite growth in Bahia and Pernambuco. TAG and gas-utilitiy deals are broadening pipeline interconnections, turning the region into a balancing point for domestic molecules and spot cargoes.

Attention is shifting north, where the equatorial margin’s Foz do Amazonas basin entered the permanent offer cycle in 2025, drawing interest from Petrobras and Chevron, despite environmental advocacy. Improved seismic imaging and potential analogues to Guyana’s Stabroek play are encouraging. If exploration success materialises, the Brazil oil and gas market could see a step change in geographic diversification and a mitigation of Southeast concentration risk.

Competitive Landscape

Petrobras still commands 90.19% of national crude, but its divestments have lowered downstream concentration, enabling independents such as Mubadala’s Acelen and PRIO to gain scale. International majors—Shell, TotalEnergies, Equinor—cooperate with FPSOs and hold sizeable stakes in frontier licences, leveraging global deepwater know-how and capital access.

Digitalisation and efficiency drive competitive advantage: SLB’s autonomous drilling cuts well time by 60%, while Baker Hughes delivers integrated subsea tie-backs that shrink pre-salt project cycles. White-space opportunities include midstream gas expander systems, modular refineries, and CCS hubs. ESG finance constraints raise the bar for transparency and methane management, rewarding firms that deploy flare-reduction kits and adopt measurement-verified reporting.

Recent deal flow highlights dynamism: PRIO’s USD 3.5 billion Peregrino acquisition from Equinor creates Brazil’s largest independent producer, while Shell’s commitment to Gato do Mato cements its rank as the leading IOC producer. Competitive intensity is therefore expected to rise as private capital backs both well-defined brownfield plays and frontier bids.

Brazil Oil And Gas Industry Leaders

Petrobras

Shell Brasil

Equinor ASA

TotalEnergies

Repsol Sinopec Brasil

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Petrobras confirmed a USD 4.8 billion plan to integrate Reduc and Boaventura, adding 76,000 barrels per day (b/d) of diesel output and expanding aviation kerosene streams.

- June 2025: Contracts worth USD 892 million were signed to double RNEST refinery capacity to 260,000 barrels per day (b/d) by 2028, including a SOx sulphur-reduction unit.

- June 2025: Petrobras-Chevron consortia secured multiple blocks in Foz do Amazonas, marking the basin’s first permanent-offer entry.

- March 2025: Shell sanctioned the Gato do Mato pre-salt project with Ecopetrol and TotalEnergies, targeting 120,000 barrels per day (b/d) from 2029.

Brazil Oil And Gas Market Report Scope

The Brazil oil and gas market report includes:

By Sector

| Upstream |

| Midstream |

| Downstream |

By Location

| Onshore |

| Offshore |

By Service

| Construction |

| Maintenance and Turn-around |

| Decommissioning |

| By Sector | Upstream |

| Midstream | |

| Downstream | |

| By Location | Onshore |

| Offshore | |

| By Service | Construction |

| Maintenance and Turn-around | |

| Decommissioning |

Key Questions Answered in the Report

How large is Brazil’s oil and gas market in 2026, and where is it headed by 2031?

The market stands at USD 23.67 billion in 2026 and is projected to climb to USD 28.82 billion by 2031, implying a 4.01% CAGR as pre-salt barrels underpin export growth.

Which part of the value chain brings in most revenue?

Upstream activity generates 78.62% of sector revenue in 2025 and is expected to expand at a 4.27% CAGR through 2031, thanks to sustained pre-salt investment and new bid-round acreage.

What is fueling the next leg of growth for Brazil’s producers?

Faster pre-salt ramp-ups, fresh exploration blocks from the 13th and 14th ANP rounds, and private money flowing into midstream assets after Petrobras divestments all push output and efficiency higher.

Where do the biggest hurdles lie?

Strict local-content quotas raise project costs, refinery shortfalls force costly product imports, and port congestion delays LNG and FPSO modules; together these factors trim margins and slow rollouts.

Who are the key players shaping the market?

Petrobras still pumps 90.19% of national volumes, but majors such as Shell, TotalEnergies and Chevron plus independents like PRIO are expanding stakes through new projects and asset deals.

How is technology changing field economics?

Operators are deploying AI-guided drilling, real-time formation testing and large-scale CO₂ reinjection, cutting well times, boosting recovery and opening a potential 950 million-ton storage market for CO₂ in depleted reservoirs.

Page last updated on: