Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

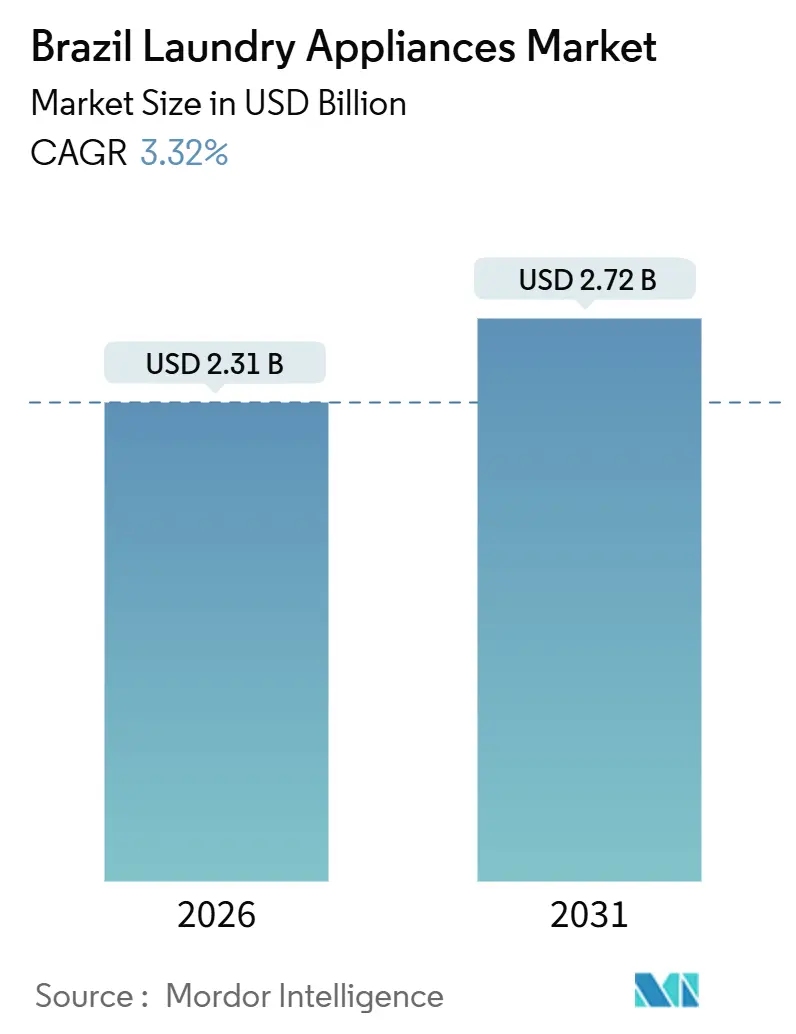

| Market Size (2026) | USD 2.31 Billion |

| Market Size (2031) | USD 2.72 Billion |

| Growth Rate (2026 - 2031) | 3.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Laundry Appliances Market Analysis by Mordor Intelligence

The Brazil laundry appliances market size stands at USD 2.31 billion in 2026 and is projected to reach USD 2.72 billion by 2031, reflecting a CAGR of 3.32%. Within the Brazil laundry appliances market, washing machines continue to anchor unit and value demand, while clothes dryers advance faster on the back of time-saving use cases and rising self-service laundry usage in large cities. Feature-led upgrades remain a visible swing factor as inverter motors, AI-based cycle selection, water reuse, and noise reduction influence replacement purchases among urban households living in compact apartments. The channel mix continues to rebalance as e-commerce adoption for durable goods rises and PIX instant payments reduce friction in installment-based transactions. Regional dynamics are mixed as the Southeast concentrates installed base and retail infrastructure while the Northeast grows faster on deeper coverage of financing, logistics, and franchise-led laundry access.

Key Report Takeaways

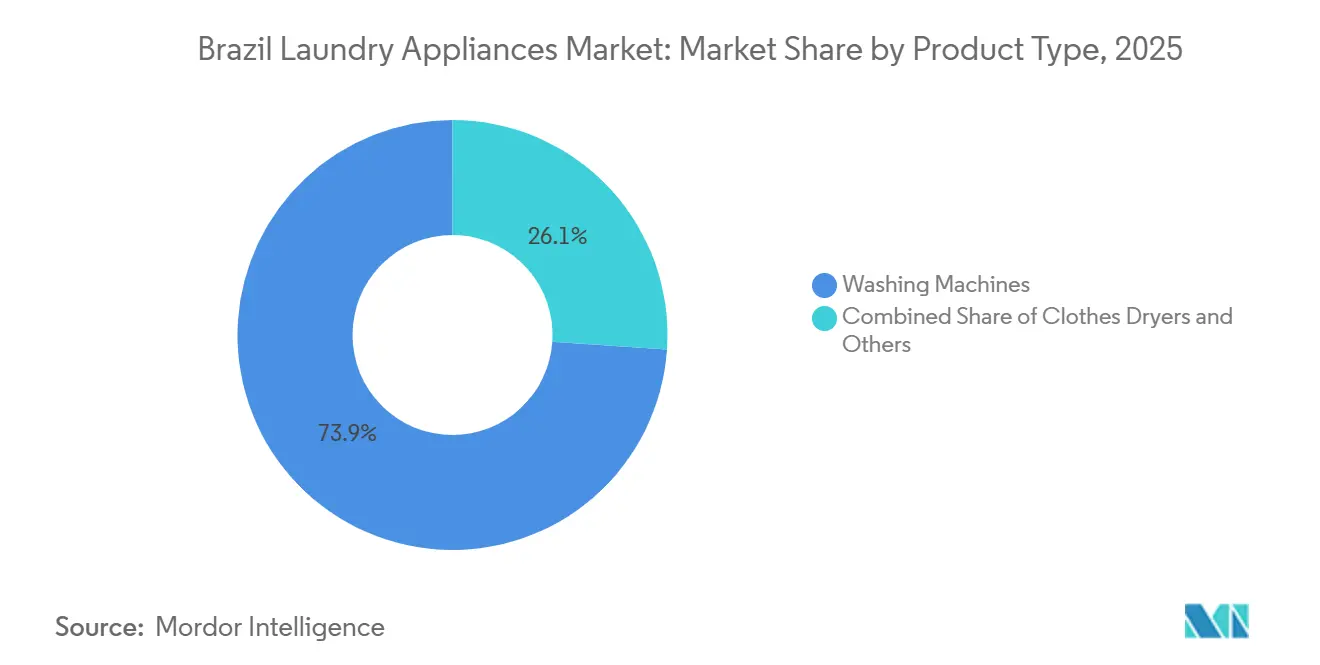

- By product type, washing machines led with 73.93% of the Brazil laundry appliances market share in 2025, while clothes dryers are forecast to expand at a 3.91% CAGR through 2031.

- By technology, fully automatic units accounted for 68.21% share in 2025 and are projected to advance at a 3.56% CAGR to 2031.

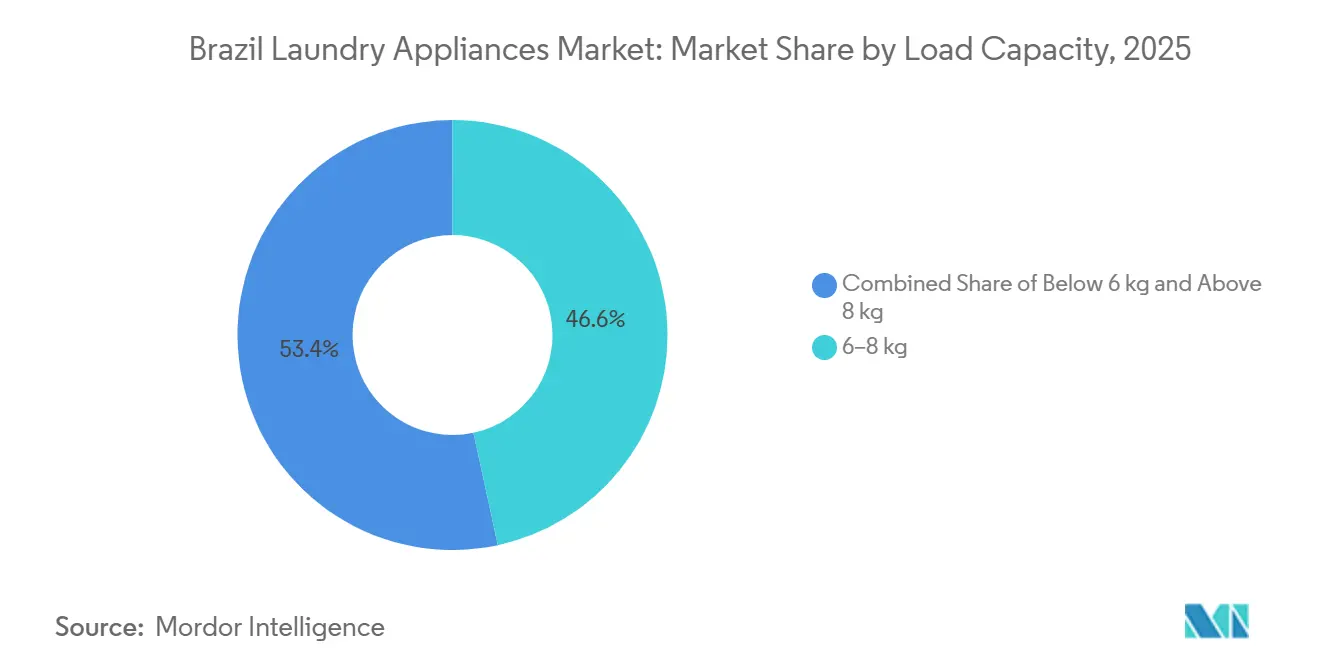

- By load capacity, 6–8 kg models captured 46.63% share in 2025, while units above 8 kg are set to grow at a 3.84% CAGR through 2031.

- By distribution channel, multi-brand stores held a 54.82% share in 2025, and online channels are expected to post a 4.12% CAGR through 2031.

- By geography, the Southeast accounted for a 46.91% share in 2025, while the Northeast is projected to grow at a 3.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Laundry Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feature-Led Upgrades Driven by Noise Reduction, Fabric Care, and Load Optimization Technologies | +0.9% | Global, with premium uptake concentrated in Southeast (São Paulo) and South | Medium term (2-4 years) |

| Expanding e-commerce penetration for appliances | +1.1% | National, spill-over acceleration in the Northeast as digital-payment infrastructure (PIX) deepens | Short term (≤ 2 years) |

| Energy-efficiency labeling programs | +0.6% | National, with PROCEL A compliance mandatory under INMETRO; utility-subsidized swap-out campaigns in Southeast | Long term (≥ 4 years) |

| Urban apartment living increases demand for compact dryers | +0.8% | São Paulo, Rio, with early gains in Curitiba, Porto Alegre | Medium term (2-4 years) |

| Growth of laundromat franchising networks | +0.7% | National, concentrated in Southeast (São Paulo state) and expanding to Northeast (Recife, Salvador) | Short term (≤ 2 years) |

| Water-scarcity regulations encouraging HE washers | +0.5% | Southeast (São Paulo basin) and Northeast (semi-arid regions) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Feature-Led Upgrades Driven by Noise Reduction, Fabric Care, and Load Optimization Technologies

Premium features are shaping replacement cycles in the Brazil laundry appliances market as consumers look for tangible performance gains that protect garments, reduce bills, and fit smaller apartments. AI-enabled fabric recognition and direct-drive or digital inverter motors support quieter operation in high-rise living and reduce energy draw compared with legacy belt-driven designs[1]Samsung Brazil, “Lavadoras e Secadoras,” Samsung Newsroom and Product Pages, samsung.com. Localized model lines emphasize water and detergent optimization, with brands highlighting water reuse and pre-dissolution systems that help avoid rewashes and detergent residue[2]Electrolux Brazil, “Smart Washers and Water Optimization,” Electrolux, electrolux.com.br. Panasonic and others position hygiene-led features, including anti-bacterial cycles and drum sanitization, for households with pets and allergy concerns. Adoption is strongest in the Southeast and South, where purchasing power, condo living, and service coverage support premium cycles and after-sales service.

Expanding E-Commerce Penetration for Appliances

Digital retail continues to take share in the Brazil laundry appliances market through broader payment options and easier product discovery for large-ticket items. PIX adoption improves checkout completion and helps buyers manage installments with lower friction and lower fraud risk across partnered platforms. Leading marketplaces and brand D2C stores are investing in rich content, AR viewing, and app-integrated support that reduces post-purchase calls and raises satisfaction. The share of durable goods sold online has risen since 2024, supported by logistics improvements and consumer familiarity with doorstep delivery for bulky items. Better last-mile routing, delivery lockers in residential buildings, and seller protections against cargo theft are gradually improving reliability in metro and Tier-2 cities. Online-led growth improves access for new entrants and value brands, sharpening competition on price-to-feature and pushing incumbents to expand D2C models with loyalty programs and bundle promotions.

Energy-Efficiency Labeling Programs

Brazil’s mandatory labeling under INMETRO’s PBE and PROCEL guides appliance choices toward higher-efficiency models and enforces a transparent comparison on energy and water use at the point of sale[3]INMETRO, “Programa Brasileiro de Etiquetagem,” Instituto Nacional de Metrologia, inmetro.gov.br. Manufacturers are responding with inverter-driven platforms, improved detergent dissolution, and water-level auto-adjustment to reduce utility bills over a product’s life. National updates to minimum performance standards since 2024 have tightened thresholds for top ratings, leading to more R&D and material improvements in premium and midrange tiers. Consumer education remains a priority, since energy efficiency often competes with price in buyer trade-offs in a context of pressure on living costs. Over time, labeling and utility-led swap programs are expected to stimulate accelerated replacement of legacy models in drought-prone regions that are sensitive to water and electricity usage.

Urban Apartment Living Increases Demand for Compact Dryers

Apartment footprints in large metros have trended smaller through 2024, reducing space for line drying and making compact dryers and washer-dryer combos more appealing for convenience and time savings. Dryer adoption also benefits from the spread of self-service laundries in dense neighborhoods where domestic drying is impractical or slow during rainy seasons. Heat-pump dryers are gaining visibility for energy efficiency, although price points mean they scale first in upper-middle-income households in the Southeast. Manufacturers are prioritizing noise reduction and more placement flexibility so that dryers can fit smaller laundry rooms without vibration or heat concerns. These dynamics support rising attachment rates for dryers over the next several years within the Brazil laundry appliances market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High import tariffs on finished appliances | -0.8% | National, with a disproportionate effect on premium dryer imports and component-heavy models | Medium term (2-4 years) |

| Price sensitivity amid economic volatility | -1.2% | National, most acute in the North and Northeast regions, where disposable income lags | Short term (≤ 2 years) |

| Underdeveloped after-sales service outside Tier-1 cities | -0.5% | Midwest, North, and interior Northeast (excludes capital cities) | Long term (≥ 4 years) |

| Persistent reliability issues with low-cost brands | -0.4% | National, with a higher incidence in entry-segment purchases (below BRL 1,500) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Import Tariffs on Finished Appliances

Brazil’s tariff structure keeps many finished home appliances at elevated duty rates, which raises shelf prices for imported dryers and complex washer platforms that rely on overseas components. To mitigate costs and currency exposure, new and incumbent brands continue to localize, evidenced by Midea’s Pouso Alegre complex and LG’s upcoming Paraná plant that will add white-line capacity and deepen local sourcing. Whirlpool reports a high local manufacturing ratio in Brazil, which helps reduce volatility from FX swings and lengthy import lead times. Tariffs have also slowed the path to wider dryer penetration compared with washers because initial premiums are harder to amortize for price-sensitive households. These conditions intensify the focus on localized production, supplier development, and tariff engineering to make midrange dryers viable in more ZIP codes.

Price Sensitivity Amid Economic Volatility

Household budgets remain careful on high-ticket purchases, which heightens the role of installment affordability and promotional financing in the Brazil laundry appliances market. Retail sales for furniture and appliances have shown month-to-month swings in recent cycles, reflecting clearance events and financing availability. Entrants compete with value-forward feature sets that narrow gaps in noise, AI cycles, and energy ratings, which places additional pricing pressure on legacy models. In response, brands highlight quantified consumer benefits such as longer motor warranties, remote diagnostics, and lower operating costs that justify premiums over entry options. As price remains the top criterion for many buyers, manufacturers will continue to calibrate configurations toward the strongest value-for-money bands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Washing Machines Lead, but Dryers Capture Aspirational Growth

Washing machines accounted for 73.93% of the 2025 value, while clothes dryers are set to grow at a 3.91% CAGR through 2031, indicating a multi-speed profile within the Brazil laundry appliances market. The Brazil laundry appliances market size for clothes dryers is poised to expand alongside dense urban living, smaller apartments, and the need to accelerate laundry turnaround during rainy seasons. Dryer penetration remains well below washer penetration, which leaves headroom for incremental units in upper-middle-income households that value convenience and noise control. Heat-pump dryers appeal to buyers who prioritize energy efficiency and fabric care, though price points delay mass adoption across regions. Self-service laundries influence behavior by familiarizing households with high-performance dryers that complete cycles quickly, which can later translate into home purchases.

Washer-dryer combos play a focused role in the Brazil laundry appliances industry, where space is constrained, and buyers prefer to consolidate footprints with front-load equipment and smart connectivity. Domestic product strategies emphasize hygiene cycles, AI fabric-care algorithms, and remote control through brand ecosystems to reduce support calls and improve lifetime value. Incremental capex by incumbents to lift dryer capacity reflects expectations that attachment rates will climb as financing and service coverage improve. Import duty structures and awareness gaps are still barriers for dryer scale, although these will moderate with localized production and targeted education on efficiency and care benefits.

By Technology: Fully Automatic Dominates, Yet Semi-Automatic Persists in Value Segments

Fully automatic units held 68.21% share in 2025 and are guided to a 3.56% CAGR through 2031 on the strength of inverter motors, smart dosing, and quieter operation favored in apartments. Front-load automatics deliver water savings and gentler fabric care, while top-load models remain strong in volumes because of the flexibility to add garments during a cycle and lower entry prices. Brands differentiate through drum geometry, AI-based soil and load sensing, and warranty length on the motor and key parts. Smart features strengthen D2C service loops through remote diagnostics and quick fixes, which lower service calls and costs for both customers and brands. These attributes keep fully automatic platforms at the center of the Brazil laundry appliances market.

Semi-automatic and manual models continue to serve specific contexts where plumbing constraints, budget limits, or maintenance simplicity are decisive. As labeling and awareness of life-cycle costs rise, value segments are also benefiting from cascaded technology advances, such as improved drum designs and better detergents. Production localization by international brands is intended to move more configurations into accessible price bands without compromising energy or water performance. Sustainability commitments by leaders, including zero waste-to-landfill and renewable energy in manufacturing, are also becoming visible points of differentiation. These changes keep both technology tiers relevant within the Brazil laundry appliances market as consumers move along income and infrastructure curves.

By Load Capacity: 6–8 kg Anchors Middle, Above 8 kg Races Ahead

The 6–8 kg band held 46.63% share in 2025 as it best matches the typical household size and available space in many urban apartments, while the above 8 kg units are projected to grow at a 3.84% CAGR through 2031. The Brazil laundry appliances market size for larger capacities is supported by buyers who want to reduce weekly loads and wash bulky items at home. Product designs have optimized cabinet dimensions to place higher capacity in standard-width footprints, which enables upgrades without space renovations. Water-level auto-adjustment, lint filtration improvements, and optimized detergent dissolution are now common even in mid-market offerings. These shifts keep load selection closely tied to household routines across regions within the Brazil laundry appliances market.

Units below 6 kg provide an entry path for singles and couples in compact homes and offer lower up-front costs in essential configurations. Intense competition in the 6–8 kg band keeps prices tight, which can compress margins as brands race to include premium-like features. Large-capacity machines remain a growth focus as families with more space aim to consolidate loads and reduce total time spent on laundry. Labeling, quality, and water savings matter more in drought-prone metros, which shape feature packs for larger washers. Capacity choices will stay diverse as household compositions evolve and apartment sizes remain tight in core cities.

By Distribution Channel: Multi-Brand Stores Dominate, Online Surges at Double-Digit Pace

Multi-brand stores held 54.82% of the 2025 value and remain the preferred path for shoppers who want to compare products, check build quality, and negotiate installments. The online channel is guided to a 4.12% CAGR to 2031, benefiting the Brazil laundry appliances market through richer content, better logistics, and safer payments. Marketplaces scale assortment and delivery reach, while brands invest in D2C, virtual showrooms, and AR visualization that clarifies fit and aesthetics. Payment diversity, including PIX and BNPL, lifts conversion among first-time online buyers of large durables. These advances ensure both channels will remain relevant and complementary in the Brazil laundry appliances market.

Brand stores and shop-in-shop formats provide curated experiences for premium segments, often linked with connected ecosystems and app support. Hypermarkets and direct sales play in more price-sensitive bands and in locations where comparison shopping is limited. Last-mile reliability has improved with lockers and better route planning, yet rural and interior cities still face longer delivery windows and higher risks. Better integration of payments, loyalty, and after-sales care across omnichannel journeys continues to be a differentiator. These dynamics keep channel strategy at the center of competitive execution within the Brazil laundry appliances market.

Geography Analysis

The Southeast accounted for 46.91% of 2025 demand and remains the anchor for installed base, premium adoption, and service depth. The region’s urban density, condo living, and retail infrastructure sustain a wide model mix across price bands for the Brazil laundry appliances market. The Brazil laundry appliances market size share for the Southeast aligns with stronger purchasing power and better logistics that support faster installation and service visits.

The Northeast is projected to expand at a 3.43% CAGR through 2031, supported by franchise laundries, digital payments, and improving logistics coverage. E-commerce helps reach more ZIP codes and supports installment affordability through PIX-enabled journeys. Water reuse and HE labeling resonate in semi-arid subregions, which shape demand for washers with efficient fill and rinse management. As coverage of after-sales service grows, interior cities should participate more in upgrades beyond essential configurations.

The South benefits from manufacturing investment and port proximity, which lowers logistics costs for select models and supports regional availability. The Midwest and North expand from a smaller base, where service coverage and delivery reliability shape adoption of premium models. This geographic mosaic calls for localized assortments, targeted financing, and flexible service to advance the Brazil laundry appliances market across varied household profiles.

Competitive Landscape

Market structure is moderately concentrated, with legacy leaders defending share through manufacturing depth, brand equity, and service coverage, while challengers scale through localization and online-led growth. Whirlpool invests in modernizing plants and raising dryer and washer capacity, linking Industry 4.0 initiatives to speed and quality improvements[4]Whirlpool Corporation, “Investimentos no Brasil,” Whirlpool Corporation, whirlpoolcorp.com. Electrolux continues to invest in Brazilian manufacturing with an emphasis on energy efficiency and lower operational emissions. These moves support a stable supply and consistent service, which matters across the Brazil laundry appliances market.

Global brands expand connected features, remote diagnostics, and longer part warranties to reinforce reliability and reduce the cost of ownership. Midea’s Pouso Alegre plant and ongoing local investments show a strategy focused on cost structure and price-to-feature positioning in washers, with roadmaps that add dryers over time. In commercial laundry, OEMs and partners launched stacked and high-efficiency models that shorten cycle times and reduce footprint for hospitality and healthcare customers. These product and footprint decisions define how brands meet varied budgets and space constraints within the Brazil laundry appliances market.

Sports and branding partnerships, franchise ecosystems, and legal clarity around trademarks also shape the competitive context. TCL’s global Olympic partnership signals a long-term branding platform that spans home appliances, including washers. Courts have reaffirmed territorial trademark rules in appliance disputes, ensuring brand rights in manufacturing and export. Franchise operators report network and revenue growth that raises consumer touchpoints for laundry services and complements household ownership. Together, these moves point to a market where scale, cost, service, and trust all drive competitive outcomes in the Brazil laundry appliances market.

Brazil Laundry Appliances Industry Leaders

Whirlpool

AB Electrolux

LG Electronics

Samsung

Midea Carrier

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Midea Group inaugurated its factory in Pouso Alegre, Minas Gerais, after a BRL 630 million investment, with capacity for 1.3 million units, including 600,000 washing machines, and targets for renewable energy, water reuse, and waste reduction.

- August 2024: LG Electronics started building a BRL 1.5 billion factory in Fazenda Rio Grande, Paraná, with opening planned for February 2026 and gradual expansion to washers and dryers.

- February 2024: Whirlpool announced BRL 550 million in investments across Brazilian units, including BRL 350 million to expand dryer and refrigerator capacity at Joinville and BRL 200 million at Rio Claro.

- February 2024: Electrolux announced a BRL 700 million factory in São José dos Pinhais, Paraná, powered by renewable energy.

Brazil Laundry Appliances Market Report Scope

Laundry appliances include traditional washing machines, as well as washer-dryer sets and portable machines. Brazil's laundry appliances market provides an in-depth analysis of the market along with current trends, which includes an assessment of the national accounts, economy, and emerging market trends by segments and significant changes in the market dynamics. The report also covers the competitive profile of major players in the market. Brazil laundry appliances are segmented by type, which includes freestanding laundry appliances and built-in laundry appliances; by product, which includes washing machines, dryers, electric smoothing irons, and others; and by technology, which includes automatic, semi-automatic/manual, and others; and by distribution channel which includes supermarkets and hypermarkets, specialty stores, online, and other distribution channels.

The report offers market size and forecasts for the Brazil laundry appliances market in terms of revenue (USD) for all the above segments.

By Product Type (value)

| Washing Machines |

| Clothes Dryers |

| Others (Garment Steamers, Electric Irons, Laundry Dehumidifiers) |

By Technology (value)

| Fully Automatic |

| Semi-Automatic / Manual |

By Load Capacity (value)

| Below 6 kg |

| 6-8 kg |

| Above 8 kg |

By Distribution Channel (value)

| Multi-brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Region (value)

| Southeast |

| South |

| Northeast |

| Midwest |

| North |

| By Product Type (value) | Washing Machines |

| Clothes Dryers | |

| Others (Garment Steamers, Electric Irons, Laundry Dehumidifiers) | |

| By Technology (value) | Fully Automatic |

| Semi-Automatic / Manual | |

| By Load Capacity (value) | Below 6 kg |

| 6-8 kg | |

| Above 8 kg | |

| By Distribution Channel (value) | Multi-brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| By Region (value) | Southeast |

| South | |

| Northeast | |

| Midwest | |

| North |

Key Questions Answered in the Report

What is the current size and growth outlook for the Brazil laundry appliances market?

The Brazil laundry appliances market size is USD 2.31 billion in 2026, and it is projected to reach USD 2.72 billion by 2031 at a 3.32% CAGR.

Which product category is growing fastest in Brazil, laundry appliances?

Which product category is growing fastest in Brazil's laundry appliances market?

Which regions lead demand for laundry appliances in Brazil?

The Southeast leads with 46.91% of 2025 demand, while the Northeast posts the fastest growth at a 3.43% CAGR through 2031.

What features are most influencing washer upgrades in Brazil?

Inverter motors, AI cycle selection, water reuse, and quieter operation are top upgrade drivers, reinforced by PROCEL and INMETRO energy labeling.

How is e-commerce changing sales of laundry appliances in Brazil?

E-commerce adoption is rising through PIX-enabled payments, richer product content, D2C service integration, and broader logistics coverage in Tier-2 cities.

Page last updated on: