Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

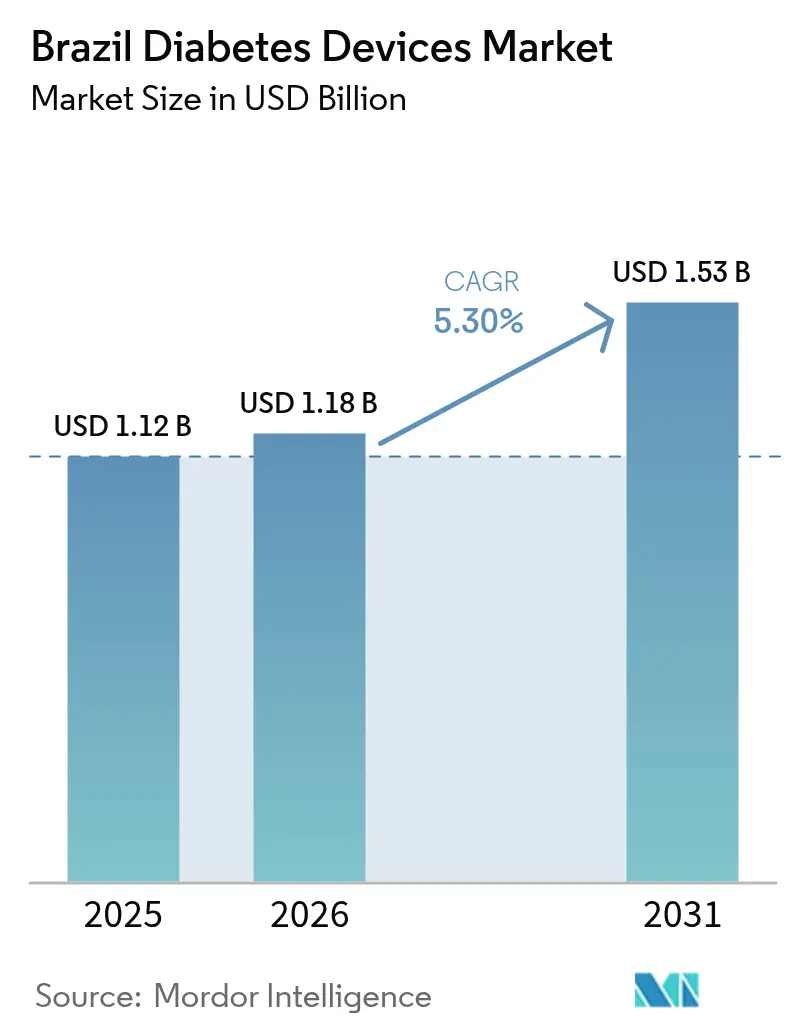

| Base Year Market Size (2025) | USD 1.12 Billion |

| Market Size (2026) | USD 1.18 Billion |

| Market Size (2031) | USD 1.53 Billion |

| Growth Rate (2026 - 2031) | 5.30% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Brazil Diabetes Devices Market Analysis by Mordor Intelligence

The Brazil diabetes devices market size is expected to grow from USD 1.12 billion in 2025 to USD 1.18 billion in 2026 and is forecast to reach USD 1.53 billion by 2031 at 5.3% CAGR over 2026-2031. Growth is propelled by a rising diabetic population of 16.8 million people in 2024, broader national screening programs, and rapid adoption of digital health tools that streamline patient engagement and data sharing. Device manufacturers are localizing production to comply with domestic regulation while meeting increasing demand for innovative glucose monitors and insulin delivery systems. At the same time, government subsidy schemes are expanding reimbursement, improving affordability in lower-income regions, and boosting volume sales. Competitive pressure is sharpening as multinationals and domestic firms pursue hybrid solutions that blend affordability with advanced functionality, a combination well suited to varied Brazilian income levels and care settings.

Key Report Takeaways

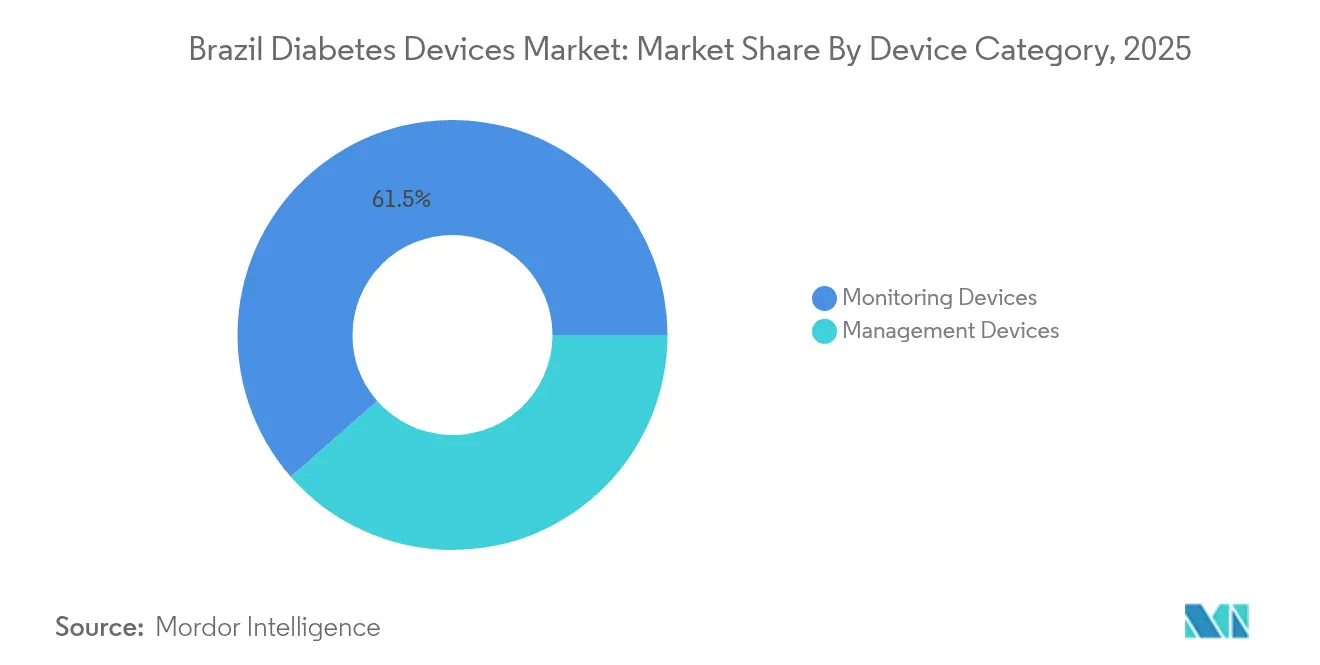

- By device category, SMBG products led with 61.45% of Brazil diabetes devices market share in 2025, whereas CGM systems are advancing at a 6.12% CAGR to 2031.

- By management device, disposable insulin pens captured 44.32% share of the Brazil diabetes devices market size in 2025, while insulin pumps record the fastest 5.57% CAGR through 2031.

- By end user, hospitals and clinics held 54.38% revenue share in 2025; home-care settings are projected to grow at 5.78% CAGR between 2026 and 2031.

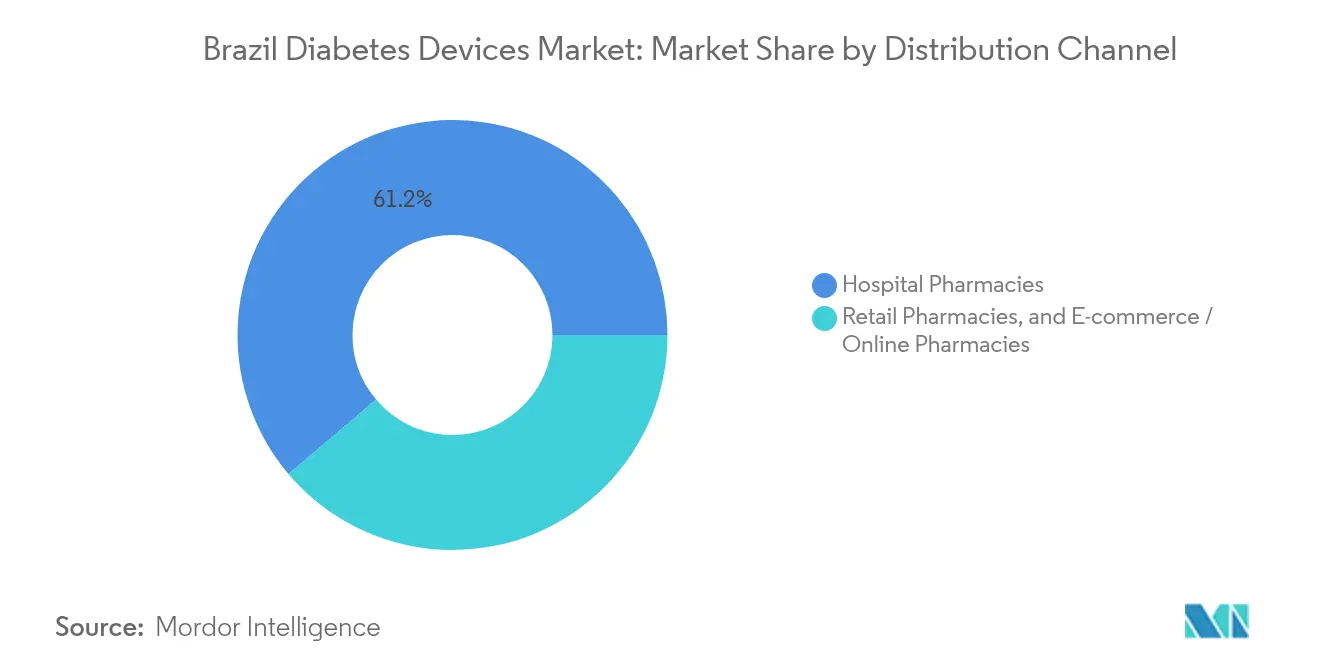

- By distribution channel, hospital pharmacies accounted for 61.18% share of the Brazil diabetes devices market size in 2025, whereas e-commerce is expanding at 6.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Diabetes Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of obesity and diabetes | +0.9% | Southeast and South | Long term (≥ 4 years) |

| Rising geriatric population | +1.2% | Urban centers nationwide | Long term (≥ 4 years) |

| Integration of digital health solutions | +1.4% | Urban, expanding inland | Medium term (2-4 years) |

| Rapid CGM adoption after ANVISA reimbursement inclusion (SUS & private) | +1.0% | Nationwide | Short term (≤ 2 years) |

| Surge in Brazilian e-pharmacy platforms enabling D-to-C device sales | +0.7% | Major cities and metropolitan belts | Medium term (2-4 years) |

| National diabetes screening expansion | +0.8% | State capitals nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Obesity and Diabetes

Brazil’s adult obesity rate is projected to reach 48% by 2044, climbing from 28.2% in 2022 [1]Eduardo Augusto F. Nilson, “Almost Half of Brazilian Adults Will Be Living With Obesity Within 20 Years,” World Obesity Federation, worldobesity.org. This trend is closely tied to a modeled surge in type 2 diabetes prevalence from 9.2% to 27.0% by 2036. Rising disease burden is translating into stronger demand for sophisticated monitoring devices, especially CGM systems that integrate with weight-management apps and offer continuous insights. Younger adults now face earlier diagnoses, creating a consumer segment that values mobility, connectivity, and preventative analytics. Manufacturers are responding with integrated platforms that link glucose tracking to lifestyle coaching, a product-mix shift that boosts average device value. The driver’s influence is amplified in more industrialized Southeast and South regions where obesity rates and disposable incomes are highest.

Rising Geriatric Population

Brazil’s population aged 65 plus is forecast to double by 2050, with current studies showing diabetes prevalence of 18.5% in seniors versus 6.4% nationally. [2]Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov This demographic demands devices with larger displays, simplified interfaces, and caregiver-friendly data sharing. Older users often prefer hybrid monitoring—combining manual logging with digital dashboards—prompting suppliers to redesign CGM receivers and SMBG meters for clarity and tactile feedback. Extended life expectancy means longer treatment horizons, thus enlarging cumulative device consumption. Urban centers see the greatest impact because specialist clinics and telehealth infrastructure simplify elderly onboarding. Over the long term, device makers that cater to ergonomic and usability needs will consolidate share among this expanding cohort.

Integration of Digital Health Solutions

Regulatory endorsement of telemedicine in 2022 accelerated remote management platforms such as GlucoTrends, which report 85% consultation resolution rates. Seamless pairing of CGM alerts with mobile apps lets clinicians adjust therapy without in-person visits, a capability valued in Brazil’s geographically dispersed interior. Digital therapeutics also create premium pricing opportunities: connected meters and smart pens sell at roughly 30% above basic devices yet benefit from quicker therapy optimizations. Supply-chain data show hospitals and private insurers leaning toward integrated ecosystems, encouraging vendors to bundle hardware, cloud analytics, and coaching services. As infrastructure gaps in rural zones close over the medium term, digital health is set to be the largest incremental contributor to Brazil diabetes devices market growth.

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of obesity and diabetes | +0.9% | Southeast and South | Long term (≥ 4 years) |

| Rising geriatric population | +1.2% | Urban centers nationwide | Long term (≥ 4 years) |

| Integration of digital health solutions | +1.4% | Urban, expanding inland | Medium term (2-4 years) |

| National diabetes screening expansion | +0.8% | State capitals nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

National Diabetes Screening Expansion

Brazil’s Ministry of Health is standardizing high-risk patient protocols to improve early detection, addressing the fact that only 36.5% of professionals now use uniform criteria. Broader screening is lifting diagnosis rates and guiding patients directly into the subsidized Farmácia Popular channel, where 53.6% of oral medication users already source supplies. Early diagnosis increases lifetime device spending, particularly for SMBG starter kits and entry-level glucometers. Uptake is fastest in state capitals that host centralized labs and public-sector purchasing hubs. Over the next four years, screening will lift baseline unit volumes more predictably, enabling producers to refine demand forecasts and inventory strategies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulations | -0.7% | Nationwide; stronger on imports | Short term (≤ 2 years) |

| Low endocrinologist density | -0.6% | North, Northeast interiors | Medium term (2-4 years) |

| High costs | -0.4% | Lower-income regions | Medium term (2-4 years) |

| Import tariffs (14–16%) on CGM transmitters | -0.5% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Low Endocrinologist Density

Specialist scarcity limits advanced device adoption in interior municipalities; many complex CGM or pump systems require prescription and follow-up from endocrinologists. Tele-consult pilots such as UBS+Digital achieved an 85% resolution rate across 6,312 sessions, indicating partial relief [3].Celina de Almeida Lamas, “Telehealth Initiative to Enhance Primary Care Access in Brazil,” Journal of Medical Internet Research, jmir.orgNonetheless, inconsistent broadband and digital literacy temper results, leaving uptake uneven outside large cities. Manufacturers are partnering with nursing networks and primary-care physicians to widen training reach, yet rollout speed remains tied to professional capacity.

Stringent Regulations

ANVISA’s rigorous approval process extends device launch timelines by up to 18 months; its 2024 technical note barred non-invasive SmartWatch glucose sensors over safety concerns. Overseas entrants must appoint local representatives and often build domestic assembly lines, raising first-year costs. While reforms aim for greater mutual recognition with foreign regulators by 2029, current bottlenecks favor established multinationals that hold Brazilian Good Manufacturing Practice certificates. Smaller innovators face capital strain as they navigate documentation, clinical validation, and language requirements. These hurdles slow the refresh cycle of high-end technologies, curbing short-term market acceleration.

High Costs

Premium CGM kits and insulin pumps retail at 3-4 times the price of basic SMBG bundles, outpacing budgets of patients reliant on the Unified Health System. Although Farmácia Popular broadens access to strips and syringes, coverage for real-time CGM remains limited. Device firms are introducing value-engineered models with reusable sensors and extended wear periods to lower per-day cost, but subsidy expansion remains key. Until reimbursement widens, price sensitivity will cap penetration in Brazil diabetes devices market segments serving low-income users.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Category – Monitoring Devices: CGM Gains Traction

Self-monitoring blood glucose still dominated with 6 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov0 Years,” World Obesity Federation, worldobesity.org"> 1Eduardo Augusto F. Nilson, “Almost Half of Brazilian Adults Will Be Living With Obesity Within 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov0 Years,” World Obesity Federation, worldobesity.org. 4International Trade Administration, “Brazil – Healthcare,” trade.gov5% revenue share of the Brazil diabetes devices market in 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov0 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov5. The segment’s consumable test strips generate steady sales, while glucometers and lancets have slower replacement cycles. CGM systems, however, are projected to register a 6. 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov0 Years,” World Obesity Federation, worldobesity.org"> 1Eduardo Augusto F. Nilson, “Almost Half of Brazilian Adults Will Be Living With Obesity Within 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov0 Years,” World Obesity Federation, worldobesity.org 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov% CAGR through 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov0 3Celina de Almeida Lamas, “Telehealth Initiative to Enhance Primary Care Access in Brazil,” Journal of Medical Internet Research, jmir.org 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov0 Years,” World Obesity Federation, worldobesity.org"> 1Eduardo Augusto F. Nilson, “Almost Half of Brazilian Adults Will Be Living With Obesity Within 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov0 Years,” World Obesity Federation, worldobesity.org, reshaping the monitoring mix. Brazil diabetes devices market size for CGM is forecast to expand alongside demand for round-the-clock insights that connect to physician dashboards, a feature valued by both public and private insurers for its potential to lower complication-related costs.

SMBG remains indispensable where Farmácia Popular covers strips and meters, driving high penetration across income brackets. Suppliers now embed Bluetooth in affordable meters so that data integrate with mobile apps, narrowing functionality gaps with CGM. As a result, hybrid products are emerging: fingerstick meters that prompt automated coaching via smartphones, offering an accessible entry point for patients phased into continuous sensing over time. This staged upgrade path supports gradual revenue lift while keeping initial out-of-pocket expense modest.

Disposable insulin pens captured 4International Trade Administration, “Brazil – Healthcare,” trade.gov 4International Trade Administration, “Brazil – Healthcare,” trade.gov. 3Celina de Almeida Lamas, “Telehealth Initiative to Enhance Primary Care Access in Brazil,” Journal of Medical Internet Research, jmir.org 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov% share of the Brazil diabetes devices market in 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov0 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov5 thanks to their dosing accuracy and broad reimbursement. Insulin pumps, although a smaller base, are forecast to grow 5.57% CAGR by 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov0 3Celina de Almeida Lamas, “Telehealth Initiative to Enhance Primary Care Access in Brazil,” Journal of Medical Internet Research, jmir.org 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov0 Years,” World Obesity Federation, worldobesity.org"> 1Eduardo Augusto F. Nilson, “Almost Half of Brazilian Adults Will Be Living With Obesity Within 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov0 Years,” World Obesity Federation, worldobesity.org as closed-loop algorithms and simplified user interfaces improve patient acceptance. Brazil diabetes devices market share for pumps is bolstered by partnerships that integrate Abbott sensors with Medtronic delivery hardware, creating near-automated glycemic control.

Reusable pens using insulin cartridges appeal to environmentally conscious users and institutions seeking waste reduction. Syringes and jet injectors, once predominant, now serve cost-constrained settings. Across categories, convergence is under way: manufacturers bundle pen devices with cloud apps that record injections and combine the logs with glucose data, supporting physician titration decisions and adherence reporting.

By End User – Home-Care Settings Reshape Delivery

Hospitals and clinics retained 5 4International Trade Administration, “Brazil – Healthcare,” trade.gov. 3Celina de Almeida Lamas, “Telehealth Initiative to Enhance Primary Care Access in Brazil,” Journal of Medical Internet Research, jmir.org8% of device revenue in 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov0 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov5 as they remain the entry point for diagnosis, acute management, and advanced technology initiation. Home-care settings, however, are growing at a 5.78% CAGR, propelled by telemedicine regulations that enable remote follow-up and electronic prescriptions. The Brazil diabetes devices market size for home-care is expanding fastest in metropolitan areas where internet infrastructure supports real-time data transmission from CGM sensors to care teams.

Retail pharmacies and dedicated diabetes centers act as intermediate hubs by offering device training without hospital overhead. Studies of FreeStyle Libre users under Brazil’s public system show that education programs delivered through these centers significantly improve time-in-range metrics, underlining the importance of accessible support. Over time, device data flowing from homes to clinics will facilitate population-level analytics that inform public health strategies.

By Distribution Channel – E-commerce Disrupts Legacy Supply

Hospital pharmacies accounted for 6 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov0 Years,” World Obesity Federation, worldobesity.org"> 1Eduardo Augusto F. Nilson, “Almost Half of Brazilian Adults Will Be Living With Obesity Within 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov0 Years,” World Obesity Federation, worldobesity.org. 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov0 Years,” World Obesity Federation, worldobesity.org"> 1Eduardo Augusto F. Nilson, “Almost Half of Brazilian Adults Will Be Living With Obesity Within 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov0 Years,” World Obesity Federation, worldobesity.org8% of the Brazil diabetes devices market size in 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov0 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov5 on the strength of integrated discharge protocols and reimbursement links. Online channels are advancing at 6. 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov 4International Trade Administration, “Brazil – Healthcare,” trade.gov% CAGR, fueled by younger patient preferences and a USD 2Adriana Amorim de Farias Leal, “Access to Medicines for Hypertension and Type 2 Diabetes in Brazil,” Cad Saude Publica, pubmed.ncbi.nlm.nih.gov00 million federal digitalization program that supports electronic prescriptions. Urban consumers value doorstep delivery, especially for monthly test-strip replenishment and sensor replacements.

Retail chains remain a key brick-and-mortar option, particularly where Farmácia Popular subsidies apply. They serve as pick-up points for subsidized supplies, streamlining last-mile access in mid-sized cities. For manufacturers, omnichannel coherence—consistent pricing, authentication, and after-sale support across physical and digital outlets—is becoming a competitive differentiator.

Geography Analysis

Southeast Brazil commands the largest regional slice of the Brazil diabetes devices market due to higher household income, dense specialist networks, and 68% of national device manufacturing capacity in São Paulo.The region’s hospitals spearhead adoption of CGM-pump integrations and participate in pilot reimbursement schemes, setting benchmarks later replicated elsewhere. Telemedicine platforms such as Sírio-Libanês Hospital’s service further enrich the region’s ecosystem, enabling data-driven care that amplifies device value.

The South enjoys strong public health expenditure and thus posts higher CGM penetration than the national average. Conversely, the Northeast exhibits lower baseline use but the fastest regional growth as targeted federal projects address historical under-investment. Subsidy expansion through Farmácia Popular, coupled with educational campaigns, is narrowing access gaps, though endocrinologist scarcity still constrains high-tech device rollout in rural zones.

North and Central-West areas represent early-stage opportunities with double-digit growth off a small base. Geographic barriers hamper logistics, and internet coverage is patchy, but telehealth pilots like UBS+Digital reveal latent demand; 85% of consultations closed without referral, indicating effective remote management potential. As infrastructure improves, suppliers focused on rugged devices that tolerate heat and humidity may find receptive markets.

Regulatory Landscape

Brazil diabetes devices are regulated by ANVISA under a risk-based framework led by RDC No. 751/2022 for medical devices, with specific pathways for in vitro diagnostic self-testing systems such as glucometers and strip-based test systems governed under the IVD framework (RDC No. 830/2023). In March 2024, ANVISA issued RDC No. 848/2024, which set essential safety and performance requirements across medical devices and strengthened expectations around clinical evidence when design, raw materials, or intended use are innovative, raising the bar for next-generation CGM and connected insulin delivery submissions.

Traceability and public-sector purchasing requirements tightened in 2026. ANVISA Normative Instruction No. 426/2026 operationalized the Unique Device Identification (UDI) system (SIUD), effective March 1, 2026, adding ongoing data governance duties for registration holders. Separately, the Ministry of Health issued Portaria GM/MS No. 11.694 on June 23, 2026, standardizing planning and orientation for SUS acquisition of diagnostic and therapeutic equipment and requiring purchase registration on the BPS (Banco de Precos em Saude) platform. This increases the weight of compliant labeling, documentation, and life-cycle records for suppliers selling through public procurement.

Value Chain Analysis

The value chain for diabetes devices in Brazil starts with imported and domestic inputs (sensor components, plastics, electronics, and reagents), moves through local assembly or manufacturing, and then passes through ANVISA registration and quality compliance before distribution via hospital pharmacies, retail pharmacy chains, and fast-growing e-commerce or online pharmacies. Public-sector demand is strongly influenced by SUS purchasing and programs such as Farmacia Popular, shaping volumes of SMBG consumables (test strips, lancets) and basic delivery supplies, while private insurers and specialist clinics tend to drive uptake of connected CGM ecosystems and higher-end insulin delivery devices that integrate with digital platforms.

Regulatory and trade frictions remain key bottlenecks across the chain. Glucose monitoring systems must meet analytical performance requirements aligned with ISO 15197:2013 for registration, and ANVISA scrutiny has been visible in areas such as non-invasive smartwatch glucose claims (Technical Note 12/2024/SEI/GQUIP/GGTPS/DIRE3/ANVISA). This reinforced that such software claims require registration and that no non-invasive glucose monitoring device has been regulated under that route. On the supply side, Brazil recorded a medical device trade deficit of USD 8.62 billion in 2024 (imports USD 9.79 billion vs exports USD 1.17 billion), underscoring reliance on external supply and foreign exchange exposure for complex components used in CGM and pump systems. Trade policy volatility also affects upstream planning and export-linked scale economics, contributing to a greater focus on localized production, distributor partnerships, and after-sales service networks that can support training, sensor adherence, and device maintenance.

Competitive Landscape

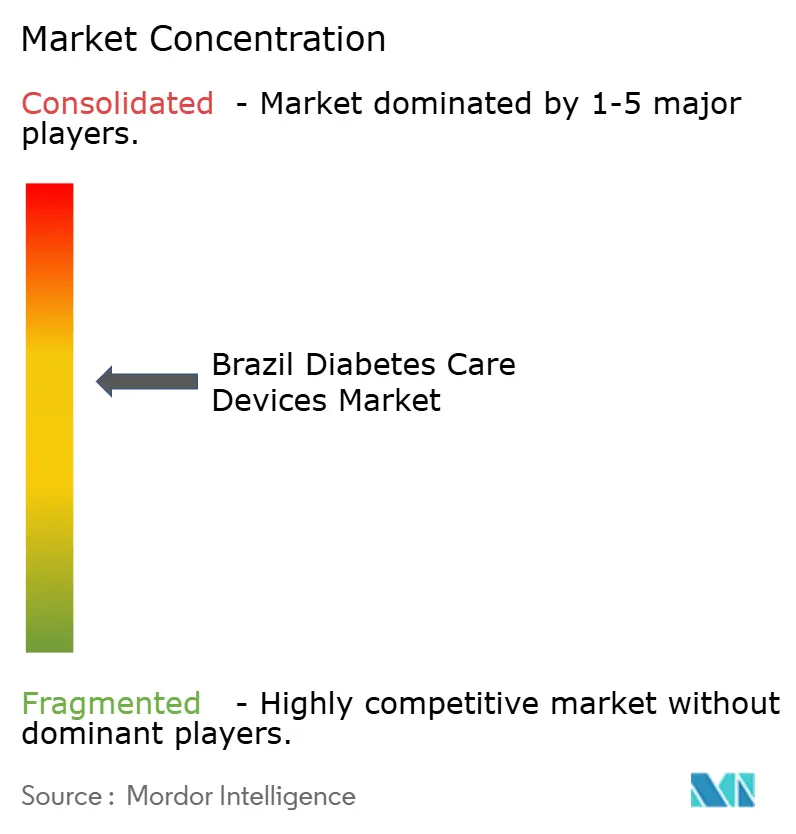

Brazil diabetes devices market competition is moderate, led by Abbott, Roche, and Medtronic, which leverage global R&D and local assembly sites. Medtronic controls about 20.5% of the insulin pump niche, while Abbott’s FreeStyle Libre dominates flash CGM supply to public clinics. Localization strategies include Novo Nordisk’s USD 6.4 billion expansion of the Montes Claros plant, aligning with the government’s Productive Development Partnership to secure technology transfer.

Digital ecosystem builders are emerging as competitive wildcards. Platforms such as GlucoTrends aggregate data from meters, sensors, and pens, then feed insights to clinicians, boosting stickiness of whichever hardware the patient uses. Multinationals invest in open APIs, while domestic firms pursue lower-price hybrids that bridge basic monitoring and full-time sensing. Regulation shapes rivalry: ANVISA’s stringent reviews advantage companies with in-country regulatory teams, a barrier that newcomers must surmount through partnerships or contract manufacturing.

White-space remains in mid-priced connected SMBG meters and entry-level pumps packaged with training modules in Portuguese. Firms that embed reimbursement coding and clinician education into product launches gain acceleration. Over the forecast horizon, portfolio breadth, supply-chain resilience, and integration with telehealth portals will dictate share shifts.

Brazil Diabetes Devices Industry Leaders

-

Abbott Diabetes Care

-

Medtronic PLC

-

Eli Lilly and Company

-

Roche Diabetes Care

-

LifeScan Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Tighter traceability, quality, and self-test oversight is creating a clearer near-term pull aligned with broader digitization of care delivery and procurement. The SIUD UDI operationalization under ANVISA Normative Instruction No. 426/2026 (effective March 1, 2026) raises demand for compliant labeling, data exchange, and master-data management, favoring suppliers that can connect product identifiers with inventory controls, recall readiness, and post-market surveillance across hospital and e-commerce channels. In parallel, ANVISA signaling of 2026-2027 priorities, including review requirements for self-testing blood glucose systems, supports product refresh and compliance-led upgrades in glucometers, test strips, and calibrators. This combination creates room for mid-priced connected SMBG systems that meet accuracy requirements while fitting telehealth workflows.

Localization is also a practical route to capture volume tied to public programs and stabilize supply. Brazil restarted national insulin manufacturing after 20 years through Ministry of Health-backed technology transfer with partners such as Biomm and Funed, with deliveries that include pen formats for SUS in 2025-2026. This reinforces a broader policy direction toward domestic production capacity and structured procurement. For device makers, the shift supports partnerships around insulin delivery hardware, Portuguese-language training modules, and distribution models that align with SUS purchasing and Farmacia Popular replenishment patterns, while also addressing private-sector demand for integrated monitoring and adherence solutions.

Recent Industry Developments

- June 2026: The Ministry of Health issued Portaria GM/MS No. 11.694, setting mandatory planning and orientation rules for SUS acquisition of diagnostic and therapeutic equipment and requiring purchase registration on the BPS platform. This strengthens the role of centralized procurement processes and increases the importance of documentation, traceability, and compliant product master data for diabetes device suppliers selling into public channels.

- July 2025: The Ministry of Health and partners Biomm and Funed received the first batch of domestically produced insulin, resuming national insulin manufacturing after 20 years via technology transfer. Deliveries include vials and pen formats for the SUS across 2025 and 2026, reinforcing local supply security and creating a more favorable environment for insulin delivery device ecosystems aligned to public distribution.

- October 2024: Brazil broadened Farmacia Popular coverage of diabetes supplies, widening subsidized access through retail pharmacy networks. The change supported higher-throughput dispensing of core monitoring consumables and basic delivery supplies, which can shift volume toward standardized SKUs and strengthen pharmacy-led distribution models.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the Brazil diabetes devices market is defined as the value of diabetes monitoring and insulin delivery devices sold for human diabetes management in Brazil, measured in current USD across institutional and home-use settings.

Scope exclusions: We exclude veterinary use, research-only analyzers, and informal or gray-market import kits that are not reliably tracked in channel data.

Segmentation Overview

-

By Device Category

-

Monitoring Devices

-

Self-Monitoring Blood Glucose (SMBG) Devices

- Glucometers

- Test Strips

- Lancets

-

Continuous Glucose Monitoring (CGM) Devices

- Sensors

- Durables (Receivers & Transmitters)

-

Self-Monitoring Blood Glucose (SMBG) Devices

-

Management Devices

-

Insulin Delivery Devices

- Insulin Pump Devices

- Insulin Disposable Pens

- Insulin Cartridges in Re-usable Pens

- Insulin Syringes & Jet Injectors

-

Insulin Delivery Devices

-

Monitoring Devices

-

By End User

- Hospitals & Clinics

- Home-Care Settings

- Retail Pharmacies & Diabetes Centers

-

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- E-commerce / Online Pharmacies

-

By Region (Brazil)

- Southeast

- South

- Northeast

- North

- Central-West

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the starting structure for the model and to anchor it with real Brazil health and trade signals. We typically refer to sources such as the Brazilian Ministry of Health data releases, IBGE demographic tables, and ANVISA regulatory and product registration information to understand what is approved and actively marketed.

To stress-test volumes and imports, we also review public trade statistics (such as Comex Stat) and customs-linked category trends, followed by diabetes burden and care-pathway references from sources like the WHO and peer-reviewed clinical journals. Company annual reports, investor presentations, and credible press coverage were used to understand product mix shifts (for example, sensors versus strips) and channel strategy changes. Where available, paid subscriptions for company financials and shipment-level import and export records are used to speed up cross-checks. These are illustrative examples only, and many other public and paid sources were consulted during data collection and validation.

Primary Interviews and Surveys

Primary work was used to confirm what desk sources cannot clearly show, especially adoption rates, pricing movement, and channel splits across Brazil. We speak with manufacturers, distributors, clinicians, diabetes educators, pharmacy stakeholders, and procurement roles, so assumptions like refill behavior for strips and sensor replacement cycles can be corrected.

Feedback is also collected across Brazil to reflect differences in access and reimbursement patterns between major urban centers and the rest of the country. The model is then adjusted when multiple respondents point in the same direction.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 16% | |

| Mid tier: 43% | Functional/Unit leaders: 24% | |

| Smaller Players: 20% | Managers: 60% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the Brazil demand pool using diabetes population signals, treated patient mix, and typical device usage patterns that translate patients into annual consumable and durable needs. Results are then compared against selective bottom-up checks, such as sampled average selling price (ASP) times implied volumes by channel and a reasonableness roll-up using publicly discussed supplier revenue exposure to Brazil. This helps us adjust totals where the first pass looks off.

Inputs that matter in this market include the share of patients on insulin, the split between SMBG and CGM usage, strip consumption per active user, sensor replacement frequency, pump penetration, and local pricing differences across retail pharmacies versus institutional buying. Since reimbursement and affordability can swing demand, we also track public health program signals and the pace of new product registrations as practical indicators of access and availability.

For forecasting, scenario analysis is used so base case growth can be flexed based on realistic adoption paths for CGM, inflation-led ASP movement, and channel expansion in online pharmacy. When data is thin for a sub-area, the gap is handled by anchoring it to a better-observed proxy (for example, using monitoring device user counts to frame consumable demand), and then re-checked in follow-up calls before locking the final time series.

Data Validation & Update Cycle

Validation is done through several layers so the final numbers are not driven by a single assumption. We compare modeled outputs against independent signals like import trend direction, estimated active user pools, and what multiple channel participants describe as year-on-year movement in volumes and pricing.

Outliers are reviewed, and if a large variance shows up, assumptions are revisited and respondents are re-contacted to clarify what changed (for example, a reimbursement policy shift or a supply disruption). Before sign-off, the work goes through multi-step analyst reviews that focus on logic checks and internal consistency across device categories and channels. The report is refreshed annually, and interim updates are made when a material event can change the near-term trajectory, followed by a final pre-delivery review pass so clients receive the latest view.

Mordor Intelligence's Brazil Diabetes Devices Market Size Compared Against Other Published Estimates

Published market values for Brazil diabetes devices can vary because the included product basket is not always the same, and because pricing and usage assumptions are updated at different times. Differences also show up when one estimate is closer to a shipment view while another leans more on patient counts and replacement cycles.

The benchmark table shows a spread that is largely explained by scope and counting rules. In Mordor Intelligence's model, diabetes management software is not added into the devices total, and CGM value is tied to sensor and durable replacement patterns observed in Brazil rather than a single blended per-patient annual spend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.12 B (2025) | |

| Industry Publisher A | USD 1.20 B (2025) | Often uses a slightly wider product scope and can apply more generalized ASP uplift across channels, which tends to pull the 2025 total upward versus a device-only count. |

| Advisory Firm B | USD 1.00 B (2023) | Uses an earlier base year and may blend devices with adjacent categories, and the implied pricing and adoption path can lag current CGM mix changes, which can keep the starting value lower. |

Taken together, the comparison suggests that the most consistent way to read the market is to start from a clear device-only definition, then tie each category to observable usage rates, replacement cycles, and channel pricing. That approach keeps the final market number traceable to a few practical levers, which can be rechecked and updated as the Brazil care pathway evolves.

Key Questions Answered in the Report

How big is the Brazil Diabetes Devices Market?

The Brazil Diabetes Devices Market size is expected to reach USD 1.18 billion in 2026 and grow at a CAGR of 5.30% to reach USD 1.53 billion by 2031.

Which monitoring device segment is growing fastest?

Continuous glucose monitoring systems are expanding at a 6.12% CAGR between 2026 and 2031.

How significant is the role of hospital pharmacies in device distribution?

Hospital pharmacies account for 61.18% of total revenue, although e-commerce is gaining momentum at a 6.24% CAGR.

What government initiative most improves affordability?

The Farmácia Popular program subsidizes strips, syringes, and medications, with 53.6% of oral diabetes drug users sourcing supplies through this channel.

Page last updated on: