Brazil Big Data Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

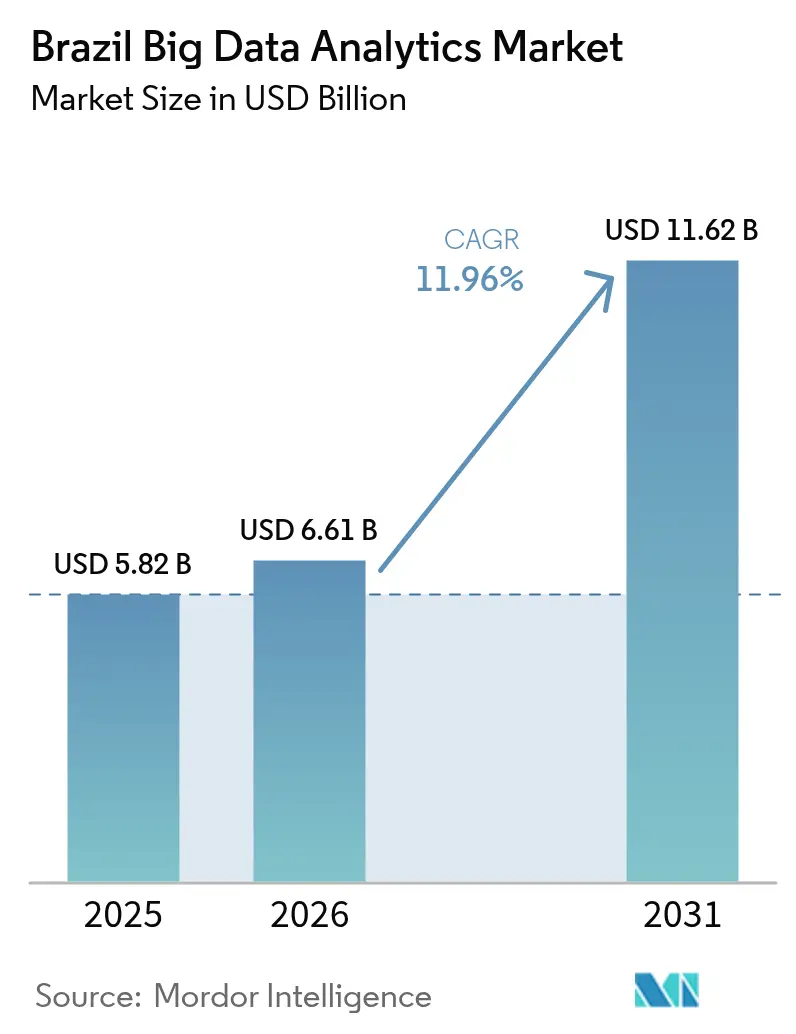

| Base Year Market Size (2025) | USD 5.82 Billion |

| Market Size (2026) | USD 6.61 Billion |

| Market Size (2031) | USD 11.62 Billion |

| Growth Rate (2026 - 2031) | 11.96% CAGR |

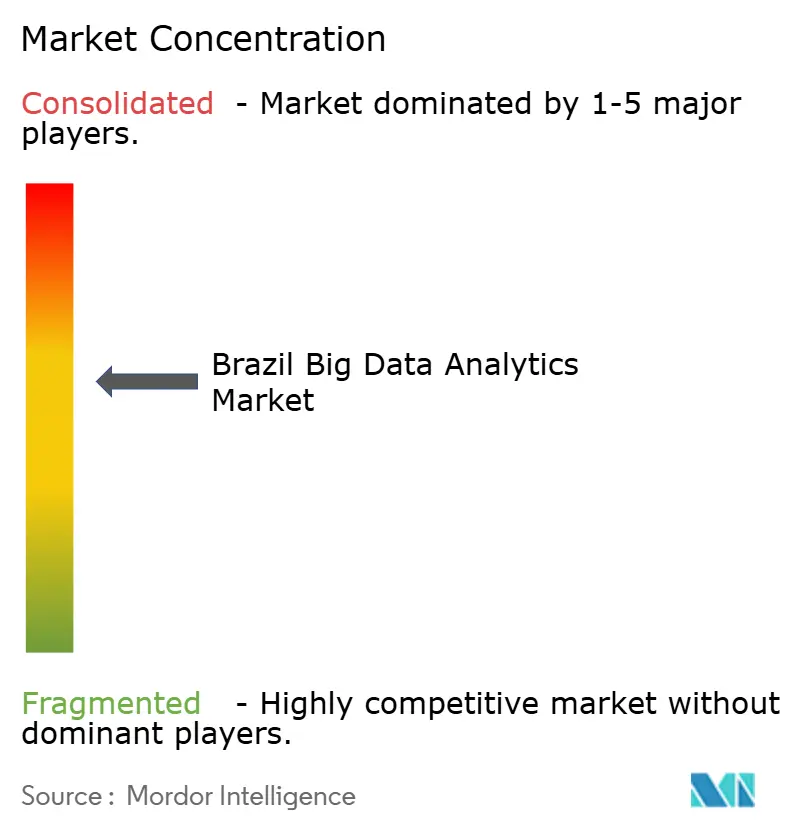

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Big Data Analytics Market Analysis by Mordor Intelligence

The Brazil big data analytics market size is expected to grow from USD 6.61 billion in 2026 to USD 11.62 billion by 2031, advancing at an 11.94% CAGR over 2026-2031. Recent regulatory mandates that force high-volume data sharing, a USD 4 billion hyperscale datacenter wave, and subsidized credit for Industry 4.0 have made real-time analytics both technically feasible and financially attractive to firms of all sizes. Financial institutions rapidly opening application-programming-interface (API) gateways, manufacturers retrofitting plants with internet-of-things (IoT) sensors, and health providers sending telemedicine streams to the cloud are expanding the addressable workload for the Brazil big data analytics market. Intensifying competition among hyperscalers has compressed per-terabyte storage prices by nearly 40% since 2024, while managed service specialists pick up demand from companies lacking in-house data talent. At the same time, exchange-rate swings that inflate dollar-denominated cloud invoices and a persistent shortage of data scientists temper spending velocity but do not derail the long-term growth trajectory.

Key Report Takeaways

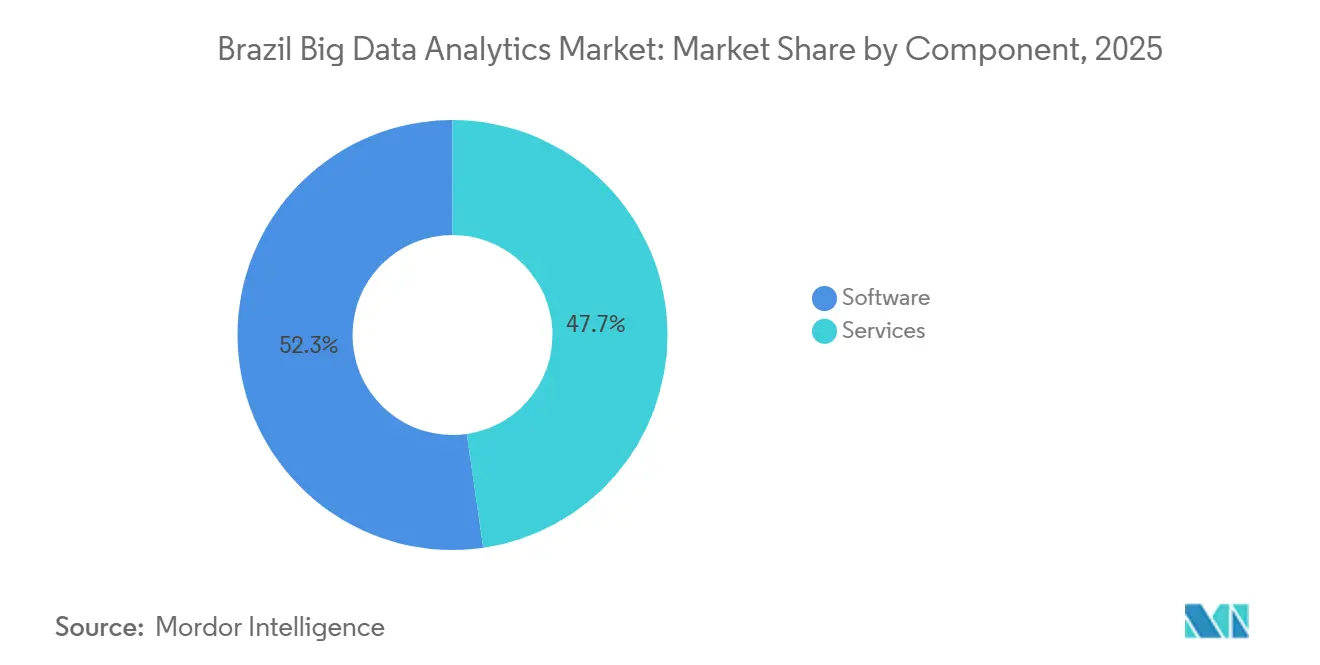

- By component, software captured 52.29% of Brazil big data analytics market share in 2025, whereas services are projected to post the strongest growth at a 12.55% CAGR through 2031.

- By deployment mode, cloud commanded 63.48% of the Brazil big data analytics market size in 2025 and is forecast to expand at a 12.86% CAGR to 2031.

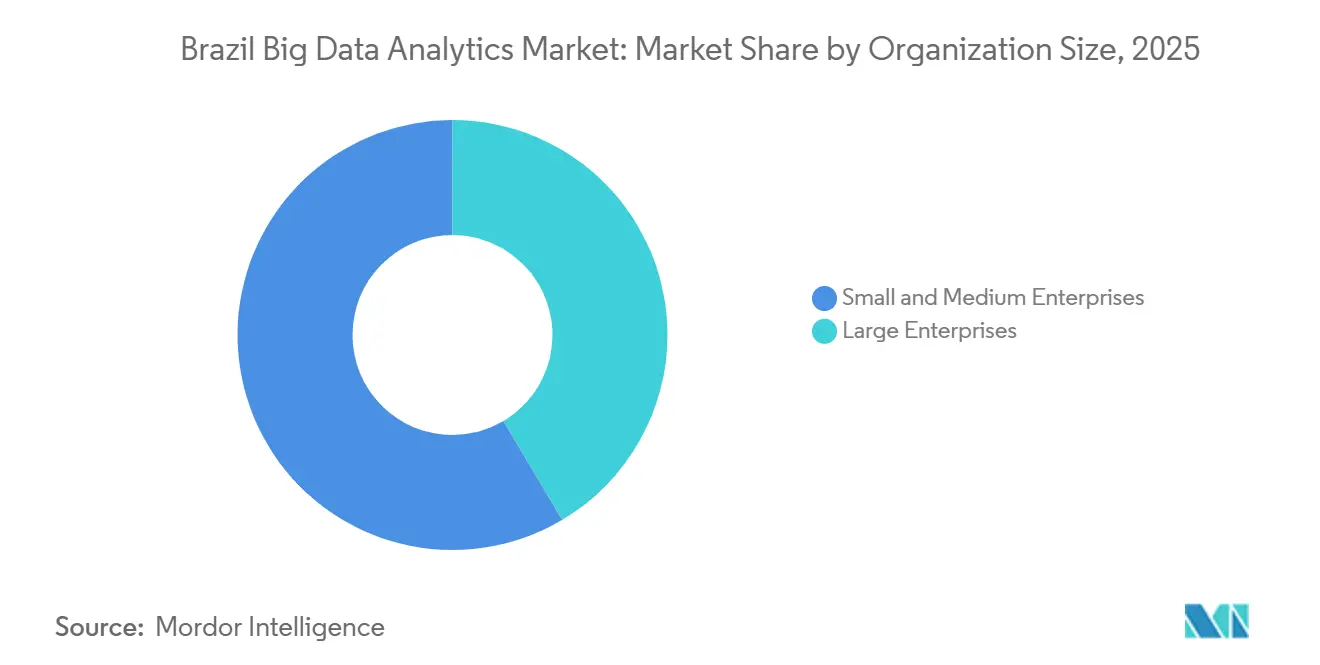

- By organization size, large enterprises accounted for 58.53% of spending in 2025, yet small and medium enterprises are poised to grow at a 12.91% CAGR during 2026-2031.

- By end-user vertical, banking, financial services, and insurance led with 27.31% revenue share in 2025, while healthcare and life sciences are advancing at a 12.57% CAGR to 2031.

- By geography, Southeast Brazil held 43.19% of revenue in 2025, whereas the North region is the fastest climber with a 12.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Big Data Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first analytics adoption among large enterprises | +2.30% | National, concentrated in Southeast (São Paulo, Rio de Janeiro) | Medium term (2-4 years) |

| Exponential data growth from IoT-enabled digital transformation | +2.10% | National, with early gains in agriculture (Center-West, South) and manufacturing (Southeast) | Long term (≥ 4 years) |

| Government Open Finance and e-Financeira mandates enlarge data pools | +2.00% | National, mandatory for institutions with >5M customers | Short term (≤ 2 years) |

| Public-sector AI and Industry 4.0 funding for SMEs | +1.80% | National, targeted support for North, Northeast, Center-West | Medium term (2-4 years) |

| Hyperscale datacenter build-out lowers latency and cost of analytics | +1.70% | Southeast (São Paulo primary), spillover to South and Center-West | Medium term (2-4 years) |

| Embedded Pix payments data fuels real-time analytics demand | +1.50% | National, urban concentration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cloud-First Analytics Adoption Among Large Enterprises

Five hyperscale build-outs since 2024 trimmed storage and compute unit costs by 30-40%, enabling banks, telcos, and exchanges to spin up elastic Spark clusters for regulatory reporting without locking capital into on-premises hardware. Multicloud contracts signed by major incumbents moved over 80% of mission-critical workloads into Brazilian availability zones, satisfying data-residency under the General Data Protection Law (LGPD) and compressing provisioning cycles from months to minutes.[1]Microsoft Corporation, “Microsoft anuncia investimento de R$ 14,7 bilhões no Brasil,” microsoft.com SAP, Qli,k and Oracle responded with local cloud regions so customers can run analytics stacks alongside core enterprise-resource-planning (ERP) data, eliminating cross-border latency penalties. Growing elasticity has shifted budgeting from capital to operating expense, favouring subscription-based software that scales with query volume and cementing cloud as the default for the Brazil big data analytics market.

Exponential Data Growth from IoT-Enabled Digital Transformation

Brazil registered 30 million IoT connections in 2024, with precision-farming probes, industrial accelerometers and smart-city cameras each adding terabytes of sensor streams daily.[2]Agência Nacional de Telecomunicações, “IoT Connections Brazil,” anatel.gov.br Predictive-maintenance pilots in automotive plants cut unplanned downtime by up to 50%, while agritech platforms used soil-moisture telemetry to trim fertilizer bills by nearly 20%.[3]Empresa Brasileira de Pesquisa Agropecuária, “Precision Agriculture in Brazil,” embrapa.br The Nova Indústria Brasil action plan earmarked USD 9.8 million in non-reimbursable grants for 100 factory digitalization pilots, guaranteeing an on-ramp of data-hungry workloads through 2026. Retailers equipped with computer-vision shelves reduced stockouts by 25%, proving that even low-margin sectors recoup sensor and analytics spend quickly. The sheer breadth of connected assets ensures a self-reinforcing data flywheel for the Brazil big data analytics market.

Open Finance and e-Financeira Mandates Enlarge Data Pools

Brazil’s Open Finance platform logged peaks of 4 billion API calls per week in 2025 as mandatory participation kicked in for institutions serving over 5 million customers. Normative Instruction 2 278 further compelled fintech to deliver transaction files electronically to tax authorities, expanding structured datasets used for anti-money-laundering and credit scoring. Compliance pressures forced mid-tier banks to license consent-lifecycle engines and data-quality monitors, widening demand for governance modules bundled with analytics suites. The regulatory push unlocks previously siloed credit, investment and payment records, broadening the foundation on which Brazil big data analytics market applications are built.

AI and Industry 4.0 Funding for SMEs

A USD 2.1 billion BNDES and Finep credit line launched in August 2025 capped interest at 8.5%, roughly six points below commercial rates, making edge-analytics gear affordable to small and medium enterprises. Finep set aside USD 350 million for firms in underserved northern states, while BNDES and SENAI introduced Smart Factory grants that co-fund up to 100 AI pilots. Vendor roadmaps now include packaged dashboards tuned for aquaculture, textiles and food processing, accelerating vertical expansion of the Brazil big data analytics market. Workforce programs from Microsoft and SAP plan to train over 5.5 million Brazilians in cloud and AI skills by 2027, easing a talent bottleneck that previously slowed SME adoption.

Advanced Analytics Talent Scarcity

Brazil counted only 53,000 data scientists in 2024 against a projected need of 530,000, driving annual wage inflation of up to 20% for mid-level roles. Recruitment cycles now average six months, pushing enterprises to rely on external consultancies and managed services, which in turn lifts delivery costs for Brazil big data analytics market projects. Although ConectAI and other upskilling drives pledge to certify millions, the 12-to-18-month learning curve means shortages will linger through 2027. Vendors are responding with low-code model builders and automated feature stores that curb dependence on scarce machine-learning specialists.

Legacy Data Silos and Low Data-Sharing Trust

Roughly 60% of large Brazilian firms juggle ten or more disconnected systems, forcing analytics teams to spend most project hours on data wrangling rather than insight generation. Only 30% run unified lakes or lake houses, and high-profile breaches erode willingness to exchange information with suppliers or peers, hampering cross-enterprise visibility initiatives. ERP incumbents such as TOTVS now bundle migration toolkits with embedded analytics, yet heavy customizations accrued over decades make cloud moves slow and risky. These obstacles cut directly into time-to-value and weigh on expansion of the Brazil big data analytics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Outpace Software as Complexity Rises

Software accounted for 52.29% of Brazil big data analytics market share in 2025 thanks to cloud-native platforms that fuse SQL, streaming and machine learning in one environment. Yet services revenue is set to climb at a 12.55% CAGR because companies lacking talent outsource model tuning, LGPD audits and Open Finance integrations. The Brazil big data analytics market size for services is projected to widen sharply as mergers such as Semantix-Atos add 2,800 consultants and deepen cybersecurity and SAP expertise.

Customers also lean on professional services to retrofit sensors, cleanse decades of ERP data and embed dashboards in line-of-business workflows. Consulting attach rates are highest in heavily regulated verticals where compliance failures carry financial penalties. Meanwhile, software vendors keep releasing auto-ML and vector-database modules, but configuration still demands architects fluent in Portuguese tax rules and LGPD clauses, anchoring demand for human services well into the forecast horizon.

By Deployment Mode: Cloud Continues Its Ascendancy

Cloud deployments commanded 63.48% of the Brazil big data analytics market size in 2025 and are on track for a 12.86% CAGR because fintech must file real-time reports via electronic pipelines. Hyperscale investments totalling USD 4 billion have pushed storage latency into single-digit milliseconds for users across the Southeast, while on-demand GPUs enable training of transformer models without local clusters.

On-premises estates persist where data sovereignty intersects with legacy mainframes, but hybrid setups let retailers burst seasonal analytics loads to the cloud. Cost predictability clauses baked into multiyear contracts have eased CFO concerns over foreign-exchange volatility, further cementing cloud as the foundation of the Brazil big data analytics market. Vendors now ship FinOps dashboards that reconcile usage, spot anomalies, and forecast spend, buffering enterprises against price shocks.

By Organization Size: SMEs Narrow the Gap

Large enterprises held a 58.53% revenue slice in 2025, yet small and medium enterprises are projected to post a brisk 12.91% CAGR as subsidized credit removes capital hurdles. The Brazil big data analytics industry’s playbook for SMEs blends turnkey ERP-embedded dashboards, fixed-fee implementation and pay-as-you-grow cloud tiers. North and Northeast firms tap Finep’s USD 350 million earmark, bringing first-time buyers into the funnel and spreading vendor footprints beyond São Paulo.

Meanwhile, fintech platforms embed predictive credit scoring and cash-flow analytics directly inside payment rails, letting micro-merchants harness insights without purchasing standalone tools. This embedded-analytics wave increases total addressable accounts and diversifies revenue streams for the Brazil big data analytics market.

By End-User Vertical: Healthcare Surges Ahead

Banking, financial services and insurance dominated spending with 27.31% in 2025, but healthcare and life sciences will lead growth at a 12.57% CAGR. The National Health Data Network now unifies 160 million patient records, feeding triage algorithms that flag chronic-disease risk and detect prescription fraud. Real-world evidence from Conecte SUS trims clinical-trial recruitment costs for pharmaceutical firms, bolstering demand for HIPAA-aligned analytics sandboxes.

Pix real-time payments supply billions of monthly transaction rows that banks mine for customer segmentation, while retail chains exploit RFID feeds to optimize shelf layouts. Government units run anomaly detectors on tax filings and traffic sensors, widening civic use cases. Each domain injects new data modalities, sustaining the Brazil big data analytics market expansion.

Geography Analysis

Southeast Brazil generated 43.19% of 2025 revenue, propelled by São Paulo’s 670 megawatts of live datacenter capacity and an imminent 770-megawatt expansion. Projects such as a planned 4.75-gigawatt AI campus and an Oracle-Nvidia-Elea megacomplex in Rio de Janeiro further compress compute latency for enterprises clustered in the region. The presence of Itaú, Bradesco, Ambev, and Petrobras supplies a dense pipeline of petabyte-scale workloads that anchors most service providers.

The North region is the fastest climber with a 12.51% CAGR because a USD 350 million Finep allocation subsidizes Industry 4.0 projects, drawing vendors to Manaus Free Trade Zone factories and aquaculture farms along the Amazon.

Precise-agriculture suites that fuse satellite imagery, soil sensors, and weather data help soybean growers in the Center-West cut input costs by nearly 20%. The Northeast’s textile and renewable-energy clusters adopt predictive-maintenance dashboards, while the South leverages proximity to Mercosur to integrate export-compliance analytics across automotive and food-processing supply chains. Together, these shifts diversify the Brazil big data analytics market beyond its historical Southeast locus.

Competitive Landscape

The vendor arena consists of global hyperscalers, regional system integrators, and niche AI start-ups. Cloud titans exploit USD billion-scale investments to offer localized AI accelerators, data-sovereignty certifications, and integrated compliance frameworks, thereby tightening customer lock-in. Brazilian incumbents such as TOTVS and Semantix leverage vertical knowledge, Portuguese support, and local sales channels to defend market space.

Domain-specific offerings targeting agribusiness and energy verticals gain traction, as regulatory nuances favor localized solutions. Talent scarcity intensifies merger and acquisitions activity, with well-funded firms acquiring boutique analytics consultancies to secure scarce skills.

Over the forecast horizon, platform convergence will accelerate, heightening barriers for point-solution providers unless they pivot to deep specialization. Firms able to embed governance, observability, and performance optimization into turnkey offerings will gain customer loyalty. Competitive differentiation will revolve around delivering measurable ROI while guaranteeing compliance, a prerequisite across the Brazil Big Data Analytics market.

Brazil Big Data Analytics Industry Leaders

IBM Corporation

Microsoft Corporation

Amazon Web Services, Inc.

QlikTech International AB

Splunk Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Polícia Federal initiated Operação Carbono Oculto, scrutinizing BRL 52 billion in suspicious transactions and prompting stricter analytics reporting for fintechs.

- May 2025: The Ministry of Science, Technology, and Innovation launched Nova Indústria Brasil, allocating BRL 10 billion for Northeast industry digitalization.

- March 2025: The National AI Plan 2024-2028 earmarked BRL 23 billion for compute infrastructure, including a supercomputer projected to rank in the global top five.

Brazil Big Data Analytics Market Report Scope

The Brazil Big Data Analytics Market Report is Segmented by Component (Software, Services), Deployment Mode (On-premise, Cloud, Hybrid), Organization Size (Small and Medium Enterprises, Large Enterprises), End-user Vertical (IT and Telecom, BFSI, Retail and Consumer Goods, Manufacturing, Healthcare and Life Sciences, Government, Energy and Utilities, Transportation and Logistics, Other End-user Verticals), and Geography (Southeast, South, North, Northeast, Center-West). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| On-premise |

| Cloud |

| Hybrid |

| Small and Medium Enterprises |

| Large Enterprises |

| IT and Telecom |

| BFSI |

| Retail and Consumer Goods |

| Manufacturing |

| Healthcare and Life Sciences |

| Government |

| Energy and Utilities |

| Transportation and Logistics |

| Other End-user Verticals |

| By Component | Software |

| Services | |

| By Deployment Mode | On-premise |

| Cloud | |

| Hybrid | |

| By Organization Size | Small and Medium Enterprises |

| Large Enterprises | |

| By End-user Vertical | IT and Telecom |

| BFSI | |

| Retail and Consumer Goods | |

| Manufacturing | |

| Healthcare and Life Sciences | |

| Government | |

| Energy and Utilities | |

| Transportation and Logistics | |

| Other End-user Verticals |

Key Questions Answered in the Report

How large will Brazil's big data analytics revenue pool be by 2031?

Forecasts place the Brazil big data analytics market at USD 11.62 billion in 2031, reflecting an 11.94% CAGR from 2026.

Which component is growing fastest?

Services are projected to expand at a 12.55% CAGR as firms outsource model tuning, LGPD compliance and API integration.

What is driving cloud dominance in analytics workloads?

Regulatory e-Financeira reporting, USD 4 billion in new datacenters and multicloud cost guarantees have pushed cloud to 63.48% of 2025 spend.

Why is healthcare the vertical to watch?

A unified National Health Data Network covering 160 million Brazilians fuels AI models that cut fraud and manage chronic disease, propelling a 12.57% CAGR.

Which region offers the quickest growth upside?

The North is set for a 12.51% CAGR through 2031 as Finep credit subsidizes Industry 4.0 rollouts in Manaus and surrounding states.

How competitive is the supplier landscape?

Moderate fragmentation prevails, with hyperscalers, ERP giants and lakehouse specialists all vying for share, giving a market-concentration score of 5.

Page last updated on: