Market Overview

| Study Period | 2023 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 114.56 Million |

| Market Size (2026) | USD 119.82 Million |

| Market Size (2031) | USD 149.96 Million |

| Growth Rate (2026 - 2031) | 4.59% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Bariatric Surgery Market Analysis by Mordor Intelligence

The Brazil bariatric surgery market size was valued at USD 114.56 million in 2025 and estimated to grow from USD 119.82 million in 2026 to reach USD 149.96 million by 2031, at a CAGR of 4.59% during the forecast period (2026-2031). Growing surgical eligibility, rapid uptake of minimally invasive platforms, and steady reimbursement expansion are the main engines lifting overall procedure volumes. Private hospitals dominate device purchases because 89% of the nation’s 291,731 bariatric operations completed between 2020 and 2024 took place outside the public SUS system. The May 2025 CFM rule that lowered the body-mass-index threshold to 30-35 for patients with comorbidities is expected to draw a much broader clinical pool into the Brazilian bariatric surgery market. Advanced stapling systems, endoscopic suturing solutions, and robotic platforms continue to command premium pricing, yet cost barriers inside the public sector limit nationwide technology penetration. Regional procedure rates remain uneven, with the North at 0.23% laparoscopic adoption versus 13.26% in the South, a gap that highlights infrastructure disparities holding back the Brazilian bariatric surgery market.

Key Report Takeaways

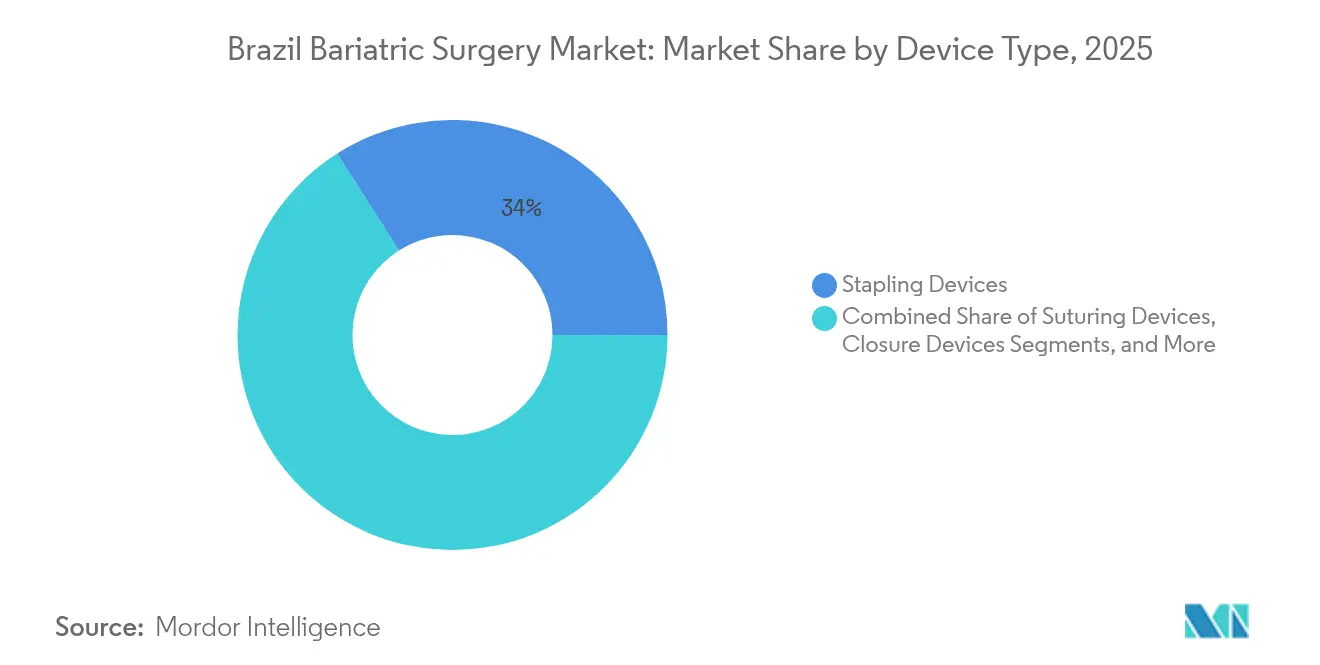

- By device type, stapling devices accounted for 34.01% revenue share in 2025, while gastric bands are projected to post a 5.44% CAGR through 2031.

- By procedure type, sleeve gastrectomy captured 75.02% of the Brazil bariatric surgery market size in 2025, whereas gastric bypass is forecast to register a 5.25% CAGR to 2031.

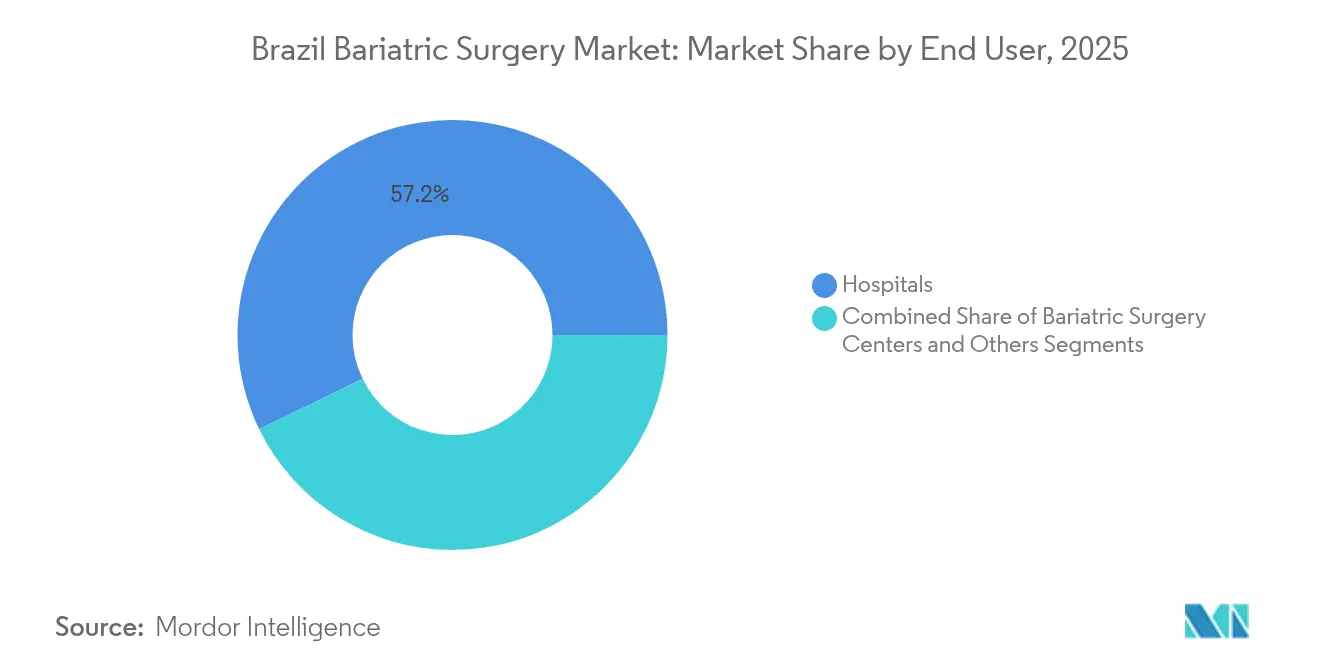

- By end user, hospitals held 57.22% of the Brazil bariatric surgery market size in 2025; specialized bariatric surgery clinics are expected to expand at a 5.61% CAGR during the same horizon

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Bariatric Surgery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising obesity prevalence & government anti-obesity programs | +1.2% | National, focused in São Paulo, Rio de Janeiro, Minas Gerais | Medium term (2-4 years) |

| Climb in T2DM & CVD comorbidities spurring surgical referrals | +0.9% | National, higher in urban centers | Long term (≥ 4 years) |

| Rapid adoption of minimally invasive & robotic techniques | +1.1% | South and Southeast, spreading to Northeast | Short term (≤ 2 years) |

| Expansion of private-payer DRG reimbursement | +0.8% | National, early uptake in metros | Medium term (2-4 years) |

| Uptake of endoscopic sleeve gastroplasty in premium clinics | +0.4% | São Paulo, Rio de Janeiro, Brasília | Short term (≤ 2 years) |

| AI-driven peri-operative monitoring | +0.3% | Major teaching hospitals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising obesity prevalence & government anti-obesity programs

Obesity prevalence climbed to 22.4% of Brazilian adults in 2025, a trend that fuels sustained demand for surgical intervention. The May 2025 CFM resolution broadened eligibility to patients with BMI 30-35 plus comorbidities, potentially doubling the national candidate pool[1]Giane Guerra, “CFM amplia acesso à cirurgia bariátrica ao reduzir IMC mínimo,” gauchazh.com.br. Federal investment of R$57 billion (USD 10.38 billion) targets domestic production of obesity therapies, complementing surgical pathways and supporting longer-term capacity building. Novo Nordisk’s R$6.4 billion (USD 1.17 billion) plant in Minas Gerais will supply injectables that may delay some procedures but should ultimately enlarge referral pipelines. The Brazil bariatric surgery market therefore benefits when surgery sits inside an integrated obesity-care framework that aligns pharmacotherapy and metabolic operations.

Climb in T2DM & CVD comorbidities spurring surgical referrals

Cardiologists and endocrinologists increasingly route patients toward metabolic surgery after evidence showed superior glycemic control relative to drug therapy alone. The CFM erased a prior rule that denied surgery to diabetics diagnosed more than 10 years, expanding the addressable base[2]Ministério da Saúde, “Brasil incorpora a prostatectomia robótica no SUS,” gov.br/saude. Hospital Metropolitano performed 1,100 surgeries in 2024 and logged 6,432 consultations, illustrating how systematic comorbidity screening amplifies demand. Device makers now emphasize instruments that optimize anatomic reconstruction and glucose outcomes. The Brazil bariatric surgery market thus gains momentum from its repositioning as a metabolic-disease solution.

Rapid adoption of minimally invasive & robotic techniques

Brazil installed 161 robotic systems by 2025, 120 of which sit in private hospitals, driving a 417% jump in bariatric robot cases since 2018. Robotic staplers coupled with 3-D visualization shorten learning curves and reduce complication rates. The public system’s August 2025 reimbursement of robotic prostatectomy sets a precedent that could unlock coverage for bariatric procedures in coming years. Manufacturer education programs and AI-guided simulators further ease surgeon adoption. These factors collectively lift technology penetration inside the Brazil bariatric surgery market.

Expansion of private-payer DRG reimbursement

The Superior Tribunal de Justiça ruled under Tema 1069 that private insurers must cover bariatric surgery and post-bariatric reconstruction when criteria are met. Structured authorization flows, such as Plan-Assist MPU’s pathway, minimize administrative bottlenecks. Legal certainty encourages providers to invest in capacity, while insulating patients against denial risk. The Brazil bariatric surgery market, therefore, strengthens as cost barriers for privately insured individuals erode.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure & device costs for SUS and patients | -1.8% | National, acute in North and Northeast | Long term (≥ 4 years) |

| Post-surgical complications & readmission burden | -0.7% | National, higher where infrastructure is limited | Medium term (2-4 years) |

| Regional shortage of trained laparoscopic/robotic surgeons | -0.5% | National | Medium term (2-4 years) |

| Infrastructure gaps in North & Northeast public hospitals | -0.3% | North and Northeast area | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High procedure & device costs for SUS and patients

Only 31,351 of the 291,731 bariatric surgeries performed from 2020–2024 were financed by SUS, highlighting affordability constraints in the public domain. Import dependence remains heavy, with a USD 8.62 billion medical-device trade deficit in 2024. Currency swings and tariffs inflate end-user prices, slowing uptake in lower-income regions. The government plans to raise domestic medical-device production from 45% to 70% by 2033, aiming to ease the burden, but it will mature beyond the forecast window. Cost pressure, therefore, tempers long-run growth for the Brazil bariatric surgery market.

Post-surgical complications & readmission burden

Nutritional deficiencies, leaks, and weight-regain episodes carry high management costs that stretch public budgets. Centers without multidisciplinary follow-up face higher readmission rates, discouraging program expansion. ANVISA demands robust post-market surveillance, elevating compliance expenses for suppliers. Hospital Metropolitano’s model, which blends 1,100 bariatric procedures with 1,132 endoscopies and 331 colonoscopies, shows the level of integrated care needed to mitigate complications. Limited diffusion of such models caps the Brazil bariatric surgery market’s pace in less-resourced areas.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Stapling Dominance Drives Innovation

Stapling platforms are expected to account for 34.01% of the Brazilian bariatric surgery market share in 2025, largely because sleeve gastrectomy remains the primary procedure nationwide. Johnson & Johnson’s ETHICON 4000 stapler introduced 3-D staple-line formation, which reduced leak interventions by 23% and gave hospitals a measurable outcome advantage. The company plans to pair the device with its forthcoming OTTAVA robotic system, strengthening ecosystem stickiness. Gastric bands are expected to record the fastest revenue growth, expanding at a 5.44% CAGR through 2031, supported by strong uptake in premium clinics. AI-enabled laparoscopic cameras and 4-K imaging towers fall under the “other devices” category and are gaining interest for their training and accuracy benefits within the Brazilian bariatric surgery market.

Surgeons’ preference for shorter operative times and lower leak risk reinforces the dominance of stapling platforms. Innovation focuses on real-time tissue-thickness feedback and auto-adjusting staple heights to manage vascular zones. Import tariffs of 24% on mechanical staplers are pushing suppliers to evaluate local assembly, aligning with the health-industrial-complex blueprint. Endoscopic sleeve gastroplasty disposables carry premium price tags but improve patient throughput by reducing the average stay by 2-4 days in private centers. These dynamics collectively shape the Brazil bariatric surgery market size trajectory at the device level.

By Procedure Type: Sleeve Gastrectomy Maintains Dominance

Sleeve gastrectomy is expected to account for 75.02% of total procedures in 2025, supported by a simpler, single-anastomosis workflow that delivers lower complication rates and shorter learning curves. Private insurers reimburse sleeve gastrectomy at 92% of billed charges, higher than the reimbursement rate for gastric bypass, further influencing surgeon preference. Although gastric bypass remains smaller in absolute procedure volume, it is forecast to grow at a CAGR of 5.25% through 2031, driven by its superior metabolic effects in patients with longstanding diabetes. ESG’s minimally invasive profile continues to attract cash-pay patients who prefer to avoid hospital stays. Revisional procedures are also increasing steadily as the early patient cohort ages, creating demand for advanced dissection tools and supporting equipment sales.

Technique evolution continues, with single-incision and robotic-assisted sleeve gastrectomy gaining visibility. National society guidelines prohibit adjustable gastric banding after outcome audits showed high explant rates, channeling demand toward more durable options. Fewer anastomoses reduce leak risk, which remains a critical factor in regions with limited intensive-care resources. Meanwhile, university hospitals are testing novel anastomosis configurations to optimize hormone modulation. Each innovation contributes incremental volume to the Brazilian bariatric surgery market.

By End User: Hospitals Lead While Clinics Accelerate

Hospitals are projected to account for 57.22% of the Brazil bariatric surgery market share in 2025, supported by significant capital investments in diagnostic imaging, intensive care, and multidisciplinary teams. A 208-bed reference facility in Mato Grosso includes 40 ICU beds, as well as endoscopy and radiology suites that support comprehensive perioperative care. Teaching hospitals also serve as innovation hubs by piloting robotic systems and AI dashboards. Their purchasing scale enables multi-year vendor contracts that bundle training and service.

Dedicated bariatric clinics are expected to record a 5.61% CAGR through 2031 as patients seek specialized centers with streamlined care pathways. High-volume concentration improves surgeon proficiency and supports pay-for-performance contracting with insurers. However, clinics depend on referral networks from internists and endocrinologists, making brand reputation critical. Ambulatory surgery centers manage only low-risk ESG cases due to regulatory limits on overnight stays. This provider mix preserves hospital dominance while creating new growth avenues, keeping the Brazilian bariatric surgery market dynamic.

Competitive Landscape

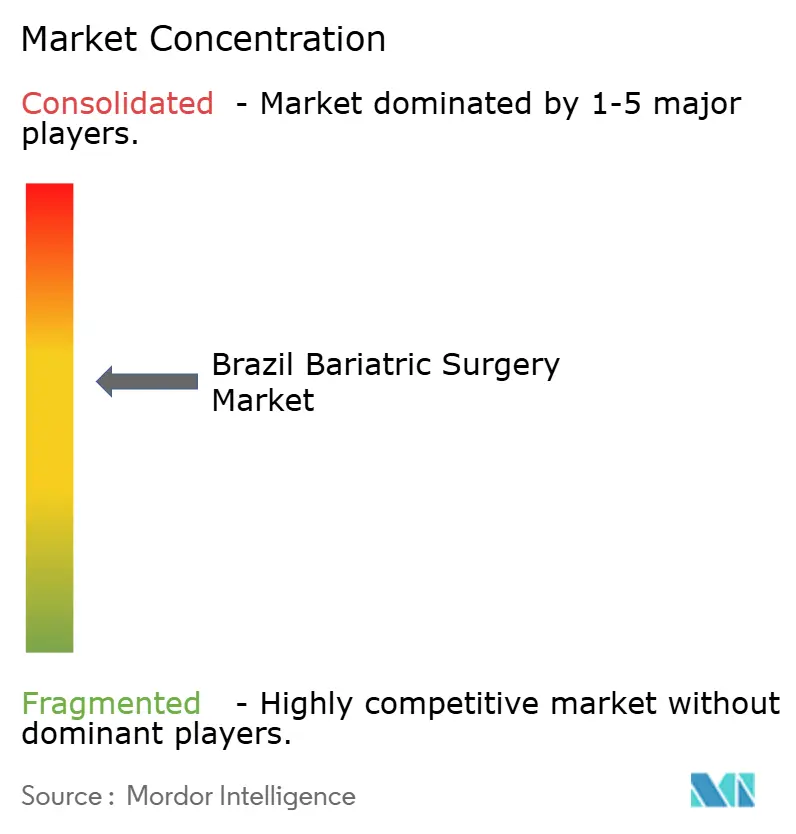

Multi-national suppliers hold moderate share, with Johnson & Johnson, Medtronic, and EziSurg competing on stapler performance, robotic integration, and cost-optimization. No single vendor exceeds 35%, yielding a moderately concentrated arena. Ethicon’s 3-D stapling paired with the future OTTAVA robot exemplifies ecosystem strategy by locking in disposables sales. Medtronic deploys GI Genius AI modules that overlay anatomical guidance onto laparoscopic views, enhancing training in lower-volume centers. EziSurg’s powered stapler, launched September 2024, targets cost-sensitive private clinics with value-driven technology.

Domestic manufacturing incentives under the industrial-complex plan create openings for joint ventures that can sidestep import tariffs. Novo Nordisk’s expansion in Minas Gerais signals foreign confidence in local capability scaling[3]Jornal do Brasil, “Indústria da saúde recebe R$57 bilhões em investimentos,” jb.com.br. Strattner distributes Intuitive Surgical robots and maintains a strong after-sales network that eases hospital adoption barriers. Compliance with ANVISA’s rigorous quality-system requirements favors incumbents that possess global regulatory infrastructure, curbing smaller foreign entrants. Competition therefore hinges on integrated platforms, local partnerships, and training investments, factors that will shape supplier standings inside the Brazil bariatric surgery market.

Brazil Bariatric Surgery Industry Leaders

Apollo Endosurgery Inc

B. Braun Melsungen AG

Medtronic

Johnson & Johnson Services, Inc. (Ethicon Inc)

Spatz FGIA Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: The Ministry of Health added robotic prostatectomy to SUS coverage, setting a precedent for future bariatric robot reimbursement.

- June 2025: The CFM lowered BMI thresholds to 30-35 for surgery candidates with comorbidities and removed age caps for diabetic patients.

- April 2025: The federal government confirmed R$57 billion (USD 10.38 billion) in health-industrial-complex spending, including Novo Nordisk’s R$6.4 billion (USD 1.17 billion) obesity-therapy facility in Minas Gerais.

- September 2024: EziSurg Medical introduced powered endoscopic staplers in Brazil to meet rising minimally invasive demand.

Brazil Bariatric Surgery Market Report Scope

As per the scope of the report, bariatric surgery or weight loss surgery is used as one of the significant treatment procedures for treating obesity. It is generally the last option for patients who have failed to lose weight by several other means. During this procedure, the stomach size is reduced by either removing some parts of the stomach or using a gastric band. The Brazil bariatric surgery market is segmented by device into assisting devices, implantable devices, and other devices. The assisting devices include suturing devices, closure devices, stapling devices, trocars, and other assisting devices. The report offers the value (in USD) for the above segments.

By Device

| Assisting Devices | Suturing Devices |

| Closure Devices | |

| Stapling Devices | |

| Other Assisting Devices | |

| Implantable Devices | Gastric Balloons |

| Gastric Bands | |

| Silastic Rings & Meshes | |

| Other Devices |

By Procedure Type

| Sleeve Gastrectomy |

| Gastric Bypass |

| Adjustable Gastric Banding |

| Endoscopic Sleeve Gastroplasty |

| Others |

By End User

| Hospitals |

| Bariatric Surgery Centers |

| Others |

| By Device | Assisting Devices | Suturing Devices |

| Closure Devices | ||

| Stapling Devices | ||

| Other Assisting Devices | ||

| Implantable Devices | Gastric Balloons | |

| Gastric Bands | ||

| Silastic Rings & Meshes | ||

| Other Devices | ||

| By Procedure Type | Sleeve Gastrectomy | |

| Gastric Bypass | ||

| Adjustable Gastric Banding | ||

| Endoscopic Sleeve Gastroplasty | ||

| Others | ||

| By End User | Hospitals | |

| Bariatric Surgery Centers | ||

| Others | ||

Key Questions Answered in the Report

How large is the Brazil bariatric surgery market in 2026?

It reached USD 119.82 million in 2026 and is projected to climb to USD 149.96 million by 2031.

Which procedure accounts for most surgeries in Brazil?

Sleeve gastrectomy dominates with 75.02% of all operations performed in 2025.

What is the fastest growing device segment?

Endoscopic sleeve gastroplasty kits are forecast to expand at a 5.44% CAGR through 2031.

Why do private hospitals lead adoption of robotic systems?

Eighty-nine percent of bariatric procedures occur in the private sector, which possesses the capital and reimbursement structures to fund 120 of the 161 robots installed nationwide.

What recent regulation broadened patient eligibility?

The CFM’s June 2025 resolution lowered the BMI threshold to 30-35 for patients with comorbidities and removed age limits for diabetics.

Which region shows the lowest minimally invasive adoption?

The North records just 0.23% laparoscopic surgery rates because of limited tertiary-care infrastructure.

Page last updated on: