Cellulose Derivatives Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 7.85 Billion |

| Market Size (2031) | USD 10.17 Billion |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cellulose Derivatives Market Analysis by Mordor Intelligence

The Cellulose Derivatives Market size is projected to expand from USD 7.45 billion in 2025 and USD 7.85 billion in 2026 to USD 10.17 billion by 2031, registering a CAGR of 5.32% between 2026 to 2031. Heightened demand for hydroxypropyl methylcellulose (HPMC) in dry-mix mortars, stricter biodegradable-packaging mandates, rising lithium-ion battery production, and steady pharmaceutical excipient consumption collectively strengthen near-term growth prospects for the cellulose derivatives market. Construction, food, and battery manufacturers value cellulose ethers for water retention and clean-label attributes, while regenerated cellulose films gain traction on single-use plastics bans. Vertical integration into dissolving wood pulp shields leading suppliers from feedstock swings, yet European Union REACH Annex XVII solvent curbs and competition from polyvinylidene fluoride (PVDF) in premium anodes moderate upside potential. Across regions, China’s new ether capacity, India’s Production Linked Incentive (PLI) scheme, and the United States Food and Drug Administration’s Generally Recognized as Safe (GRAS) clearances expand the cellulose derivatives market footprint; compliance investments and competing synthetic binders remain the primary cost and substitution risks.

Key Report Takeaways

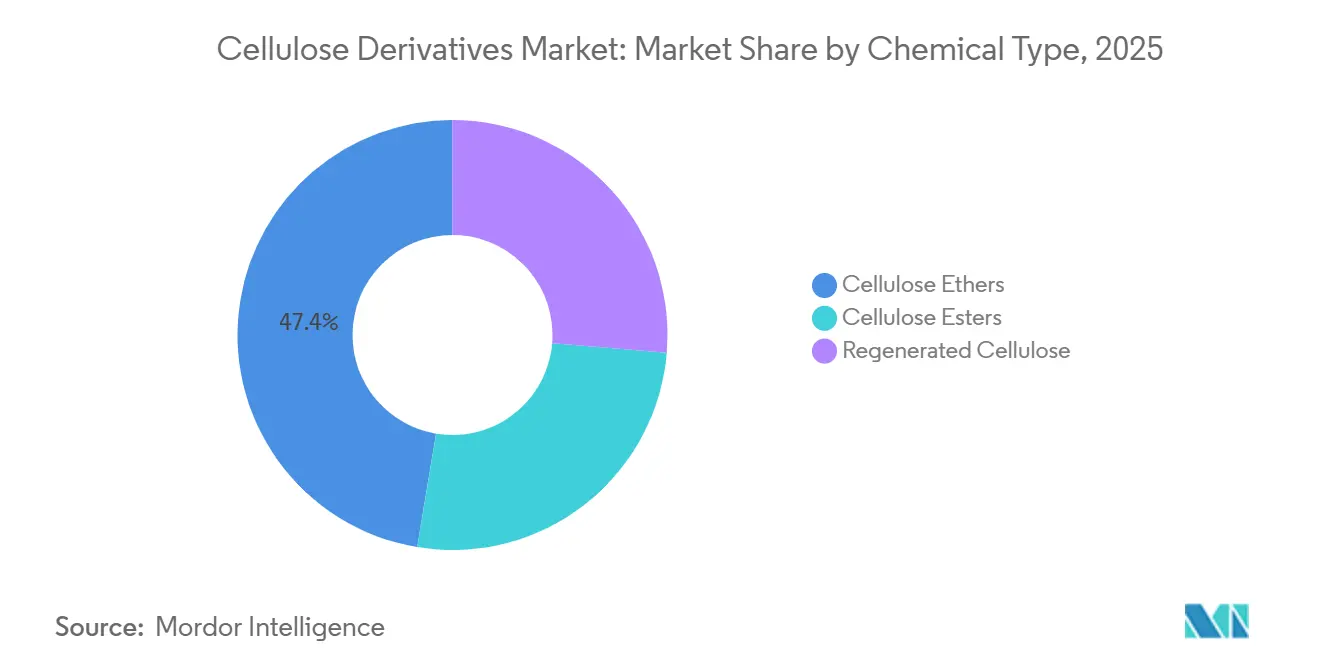

- Cellulose ethers led with 47.38% of cellulose derivatives market share in 2025, while regenerated cellulose is forecast to register the fastest 6.21% CAGR to 2031.

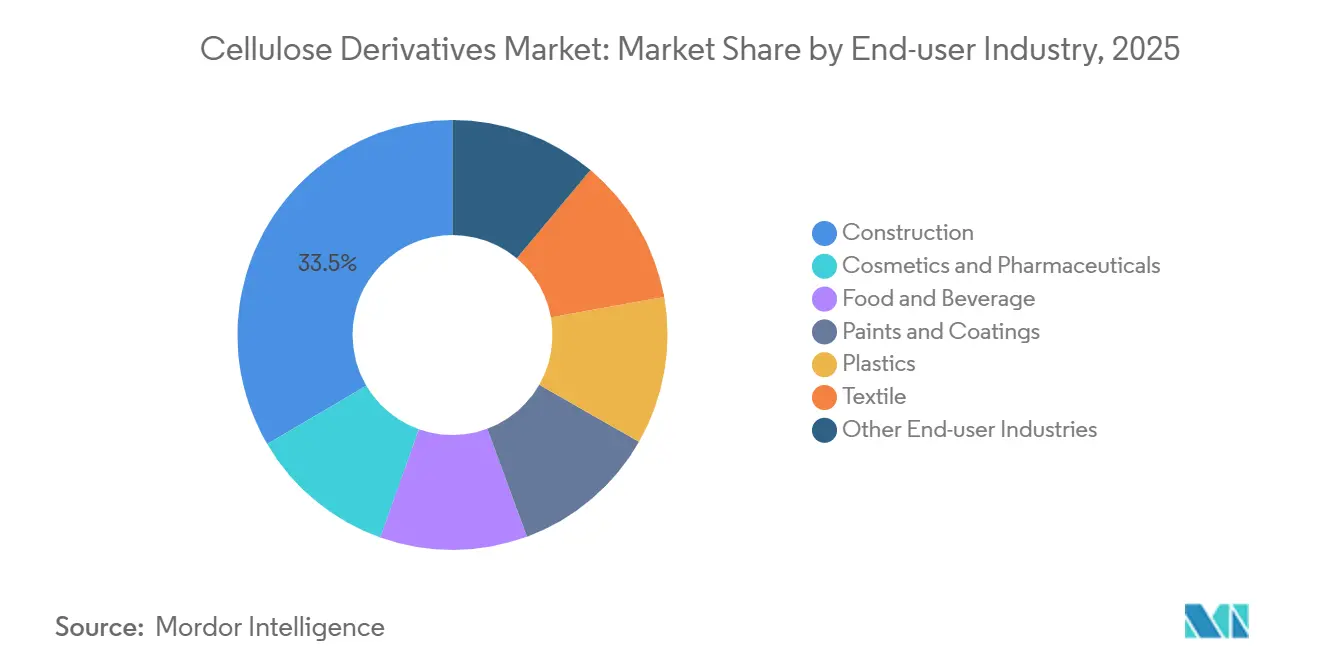

- Construction applications accounted for 33.46% of the cellulose derivatives market size in 2025; cosmetics and pharmaceuticals are set to advance at a 6.34% CAGR through 2031.

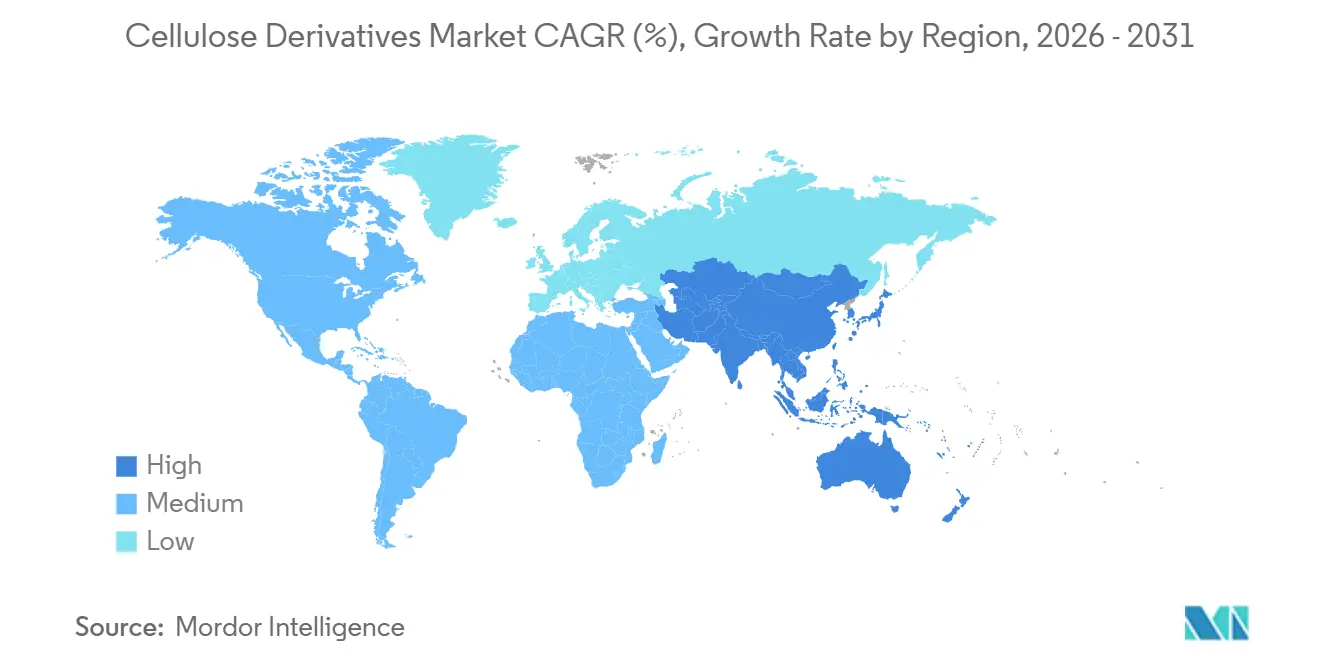

- Asia-Pacific dominated with 48.27% share of the cellulose derivatives market in 2025 and is projected to expand at a 5.92% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cellulose Derivatives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pharmaceutical-grade excipient demand | +1.20% | Global, with concentration in North America, Europe, and India | Medium term (2-4 years) |

| Growth in construction mortars and dry-mix products | +1.50% | APAC core, spill-over to Middle-East and North Africa | Short term (≤ 2 years) |

| Expanding food and beverage stabilizer usage | +0.80% | North America and EU, emerging in APAC urban centers | Medium term (2-4 years) |

| Sustainability push towards biodegradable substitutes | +0.70% | EU regulatory leadership, spreading to North America and APAC coastal markets | Long term (≥ 4 years) |

| Li-ion battery anode binder adoption | +0.90% | APAC manufacturing hubs (China, South Korea), North America EV corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Pharmaceutical-Grade Excipient Demand

United States Pharmacopeia monographs for hypromellose and cellulose acetate phthalate standardize viscosity grades, enabling manufacturers to streamline controlled-release tablet design and improve batch consistency[1]United States Pharmacopeia, “Hypromellose Monograph,” usp.org. India’s PLI incentives spur localized HPMC and carboxymethylcellulose (CMC-Na) production, cutting import lead times and aligning with International Council for Harmonisation Q3D elemental-impurity limits. Generic drug formulators continue to replace synthetic disintegrants with CMC-Na for rapid dissolution at competitive cost. The US Food and Drug Administration’s 21 CFR 182.1745 listing covering methylcellulose eases dual-use pathways in nutraceutical gummies and pediatric suspensions. Expanding biosimilar pipelines sustain double-digit excipient volume growth, allowing the cellulose derivatives market to capture incremental share in oral solid-dosage innovations.

Growth in Construction Mortars and Dry-Mix Products

HPMC grades dominate tile-adhesive, render, and exterior insulation finishing system (EIFS) mixes thanks to superior water retention and open-time extension. Dow’s WALOCEL and Shin-Etsu’s METOLOSE portfolios allow contractors to fine-tune viscosity for vertical applications and hot-weather curing. China’s mega-infrastructure pipeline anchors ether demand even as residential builds cool, while Saudi giga-projects specify specialty HPMC to combat premature water loss under 40 °C site conditions. In price-sensitive sub-segments, polyvinyl alcohol competes on cost, yet HPMC retains the premium niche where bond strength matters. Short delivery cycles for prefabricated housing further elevate demand for quick-setting mortars stabilized with cellulose ethers, underscoring near-term momentum for the cellulose derivatives market.

Expanding Food and Beverage Stabilizer Usage

Clean-label preferences propel formulators toward cellulose gums as emulsifiers and thickeners in plant-based meat, dairy alternatives, and ready-to-drink protein beverages. FDA GRAS Notices GRN 000498 and 000897 affirm the safety of methylcellulose and HPMC in food contact, accelerating deployment in North America. EFSA E-numbers E461 and E464 harmonize usage limits across Europe, simplifying multinational brand compliance[2]European Food Safety Authority, “Food Additives Database,” efsa.europa.eu. Beverage processors select low-viscosity CMC to keep cocoa or protein particulates in suspension during aseptic shelf life, reducing sedimentation rejects. Thermal-gelation of methylcellulose enables plant-based burgers to mimic animal fat melt and retain juiciness, reinforcing the cellulose derivatives market opportunity in texture design.

Li-ion Battery Anode Binder Adoption

Water-based CMC-SBR systems cut manufacturing costs up to 30% relative to PVDF/N-methyl-2-pyrrolidone lines while eliminating solvent recovery units flagged under California Proposition 65 and EU REACH Annex XVII. Ammonium-functionalized CMC improves silicon-anode adhesion, delivering 35% longer cycle life according to 2024 Journal of Power Sources data. Chinese and Korean gigafactories already integrate CMC binders in mid-range EV cells, capturing 25-30% of the anode-binder pool. IEC 62660 battery safety regulations remain chemistry-agnostic, allowing value-based binder selection. Viscosity and degree-of-substitution tuning let suppliers tailor flow for slot-die and doctor-blade coating, positioning the cellulose derivatives market for incremental battery share gains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from synthetic and protein-based fibers | -0.70% | Global, with intensity in North America premium battery and EU construction segments | Medium term (2-4 years) |

| Wood-pulp and cotton-linter price volatility | -0.50% | Global supply chain, acute in Asia-Pacific and South America sourcing regions | Short term (≤ 2 years) |

| Solvent-toxicity regulations for acetate grades | -0.60% | EU REACH jurisdiction, California Prop 65, spreading to APAC regulatory frameworks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Synthetic and Protein-Based Fibers

PVDF maintains ≥90% share in high-energy battery anodes, limiting CMC influence to cost-driven EV tiers despite sustainability mandates. In mortars, polyvinyl alcohol matches water retention at 15-20% lower price, siphoning volume in Southeast Asia where contractor margins are thin. Protein isolates such as soy and wheat gluten entice clean-label formulators but require allergen declarations and face supply fluctuations, tempering their advance. Synthetic polymer producers circumvent new REACH dossiers, avoiding the compliance fees levied on emerging cellulose ether entrants, producing a 3-5% cost edge. Technology breakthroughs in continuous etherification could shrink cellulose ether conversion cost by 8-12%, restoring competitiveness for the cellulose derivatives market against synthetics.

Wood-Pulp and Cotton-Linter Price Volatility

Dissolving pulp prices slid from USD 1,400 per ton in 2022 to USD 1,285 in Q3-2024, easing margin pressure yet underscoring cyclical risk. Cotton-linter supply swings with textile demand and seasonal yields, causing purity constraints for acetate tow used in cigarette filters and optical films. Bracell’s Q3-2024 quote of USD 1,250 per ton highlights regional disparities tied to freight and currency shifts. Vertical integration by Ashland and Lenzing stabilizes input flows but demands capital outlays above USD 100 million per site. Futures hedging blunts short spikes, yet structural viscose downturns or forestry policy changes can still trim cellulose derivatives market EBITDA margins by 200-300 basis points.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Chemical Type: Ethers Lead, Regenerated Cellulose Accelerates

Cellulose ethers captured 47.38% of the cellulose derivatives market share in 2025, anchored by HPMC and CMC usage in construction mortars, pharmaceuticals, and food stabilizers. Regenerated cellulose is forecast to post the quickest 6.21% CAGR, propelled by single-use plastics bans that favor compostable films for confectionery and tobacco packaging. Within the cellulose derivatives market size, esters such as cellulose acetate serve cigarette filters and optical films but face cost pressure from solvent compliance upgrades. Lenzing’s Ioncell process dissolves pulp in ionic liquids, eliminating carbon disulfide emissions and enabling closed-loop recovery that aligns with ISO 14001.

Hydroxypropyl methylcellulose reigns in ether demand owing to dual water-retention and film-forming traits valued by tile-adhesive formulators and controlled-release tablet developers. CMC’s water-based processing secures adoption in battery binders and ice-cream stabilization, while methylcellulose supports thermal-gel food systems such as plant-based meats. Ethyl cellulose remains a niche barrier-coating polymer. Regenerated cellulose films such as Futamura NatureFlex and Sappi Ultracast hold compostability certification under EN 13432, appealing to brand owners facing extended producer responsibility (EPR) rules in France and Germany.

By End-User Industry: Construction Dominates, Pharma Surges

Construction commanded 33.46% of the cellulose derivatives market size in 2025 as HPMC entrenched itself in dry-mix mortars. Cosmetics and pharmaceuticals are set to outpace the pack with a 6.34% CAGR, powered by film-coated generics, ophthalmic gels, and topical creams. Food and beverage categories leverage CMC and methylcellulose to meet clean-label viscosity and mouthfeel targets. Paints and coatings use hydroxyethyl cellulose for sag control in water-based architectural finishes, benefiting from VOC caps in California and the EU. Plastic applications such as acetate eyeglass frames grow more slowly due to polycarbonate incursions, yet acetate tow for cigarette filters continues to consume ester volumes.

Pharmaceutical uptake is strengthened by USP monographs that clarify purity thresholds, shrinking formulation risk, and expediting drug approvals. ISO 22000 food safety regimes further assure beverage brands that cellulose derivatives meet microbial limits in aseptic facilities. Together, these standards reinforce confidence among end users and support continued share gains for the cellulose derivatives market across premium applications.

Geography Analysis

Asia-Pacific held 48.27% share of the cellulose derivatives market in 2025 and is poised to expand at a 5.92% CAGR through 2031. China’s extra HPMC reactors feed both domestic construction and export channels, while India’s PLI inducements draw USD 200 million toward pharma-grade ether plants, shrinking reliance on European imports. Japanese and Korean battery giants employ CMC binders in EV cell lines within battery applications. Southeast Asia’s infrastructure boom and Indonesia’s nickel-battery ecosystem further underpin long-term uptake.

In North America, FDA GRAS listings ease functional-food launches, while the United States residential-repair cycle underpins HPMC demand in EIFS and joint compounds. Canada adapts cellulose ether mortars for cold-climate construction, and Mexico’s automotive hub draws CMC for battery and coating uses.

Europe’s share was tempered by mature construction but buoyed by pharmaceutical output in Germany, France, and Italy. REACH Annex XVII limits on N-methyl-2-pyrrolidone compel acetate plants to retrofit closed-loop acetylation, inflating specialty-grade costs yet spurring research into greener solvents. Eastern European builds adopt HPMC-enhanced renders for energy-efficient façades, providing a modest lift.

In South America and the Middle East & Africa, Brazil’s construction pipeline and pulp integration encourage cellulose ether consumption, whereas Saudi Arabia’s giga-projects specify high-temperature HPMC formulations. African ready-mix concrete markets remain early-stage but show promise as quality standards converge with international codes, offering incremental territory for the cellulose derivatives market.

Competitive Landscape

The Cellulose Derivatives market is moderately fragmented. Strategic moves concentrate on Asian expansions, closed-loop acetylation retrofits, and specialty film launches. For example, Lenzing invested USD 50 million in VEOCEL compostable packaging lines, while Futamura enhanced moisture-barrier NatureFlex to extend shelf life without aluminum laminates. Start-ups developing enzymatically modified cellulose rheology modifiers face scale barriers and regulatory clearance hurdles, limiting immediate disruption. Overall, margin defense hinges on feedstock integration, solvent-recovery efficiency, and rapid grade customization as the cellulose derivatives market matures.

Cellulose Derivatives Industry Leaders

Ashland

Eastman Chemical Company

Shin-Etsu Chemical Co., Ltd

Dow

Lenzing AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Eastman unveiled Eastman Esmeri CC1N10. This high-performance cellulose ester micropowder, readily biodegradable, is tailored for the color cosmetics industry. Sourced from sustainably managed forests, Esmeri aligns with stringent EU regulations, ensuring that its synthetic polymer microparticles fully biodegrade and leave no environmental trace.

- March 2025: DAICEL CORPORATION unveiled BELLOCEA's BS7, an eco-friendly cellulose acetate spherical particle that offers a soft touch. BELLOCEA BS7 could serve as a sustainable alternative to microplastic beads in cosmetics.

Global Cellulose Derivatives Market Report Scope

Cellulose derivatives are formed from the pulp produced after the separation of cellulose fibers from fiber crops, waste paper, or wood. Cellulose is a natural polymer and the most abundant polysaccharide that can be extracted from a vast number of sources, including wood and plants, some bacteria and algae, and also tunicates. Cellulose derivatives are extensively used in various industrial sectors, such as paint and coatings, textiles, food and beverage, etc.

The market is segmented by product type (cellulose esters, cellulose ethers, and regenerated cellulose), end-user industry (construction, cosmetics, and pharmaceuticals, food and beverage, paints and coatings, plastics, textiles, and other end-user industries), and geography (Asia-Pacific, North America, Europe, and the Rest of the World). The report also covers the market size and forecasts for the market in 18 countries across the globe. The report offers market size and forecasts for the cellulose derivatives market in value (USD) for all the above segments.

| Cellulose Esters |

| Cellulose Ethers |

| Regenerated Cellulose |

| Construction |

| Cosmetics and Pharmaceuticals |

| Food and Beverage |

| Paints and Coatings |

| Plastics |

| Textile |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Chemical Type | Cellulose Esters | |

| Cellulose Ethers | ||

| Regenerated Cellulose | ||

| By End-user Industry | Construction | |

| Cosmetics and Pharmaceuticals | ||

| Food and Beverage | ||

| Paints and Coatings | ||

| Plastics | ||

| Textile | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current global value of the cellulose derivatives market?

The cellulose derivatives market size reached USD 7.85 billion in 2026.

How fast is Asia-Pacific demand for cellulose derivatives growing?

Asia-Pacific consumption is forecast to rise at a 5.92% CAGR through 2031, driven by Chinese construction and Indian pharma ties.

Which chemical segment is expanding the quickest?

Regenerated cellulose is projected to grow at a 6.21% CAGR as global packaging policies favor compostable films.

Why is HPMC favored in dry-mix mortars?

HPMC provides superior water retention and open-time performance, essential for tile adhesives and EIFS applications.

How are cellulose derivatives used in lithium-ion batteries?

Carboxymethylcellulose serves as a water-based anode binder, lowering cost and avoiding toxic solvents found in PVDF systems.

Page last updated on: