Biodegradable Mulch Film Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

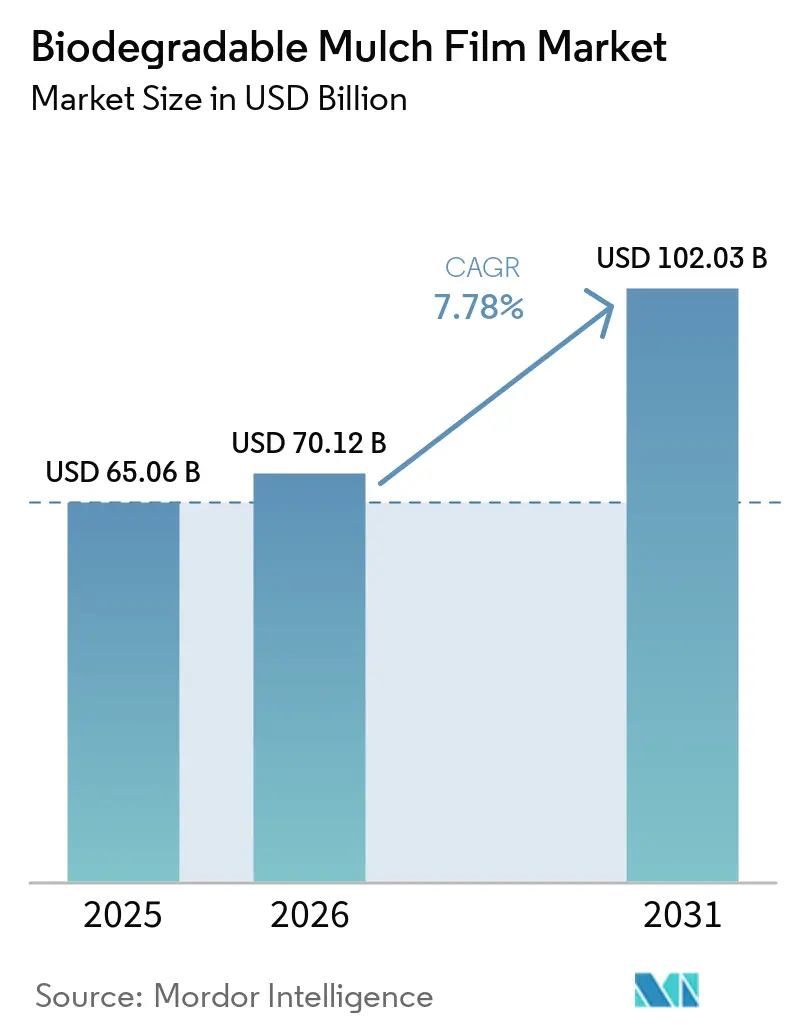

| Market Size (2026) | USD 70.12 Billion |

| Market Size (2031) | USD 102.03 Billion |

| Growth Rate (2026 - 2031) | 7.78% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Biodegradable Mulch Film Market Analysis by Mordor Intelligence

biodegradable mulch film market size in 2026 is estimated at USD 70.12 million, growing from 2025 value of USD 65.06 million with 2031 projections showing USD 102.03 million, growing at 7.78% CAGR over 2026-2031. Rising concerns over polyethylene waste, intensified greenhouse cultivation, and wider access to starch-based feedstocks continue to position soil-biodegradable films as a preferred solution across high-value horticulture systems. Farmers view the product’s elimination of film‐recovery labor as a direct operating-cost benefit, while regulators leverage landfill-avoidance targets to accelerate field adoption. Rapid expansion of protected cultivation in Asia–Pacific, sustained European regulatory pressure on single-use plastics, and emerging biochar-film combinations that open second-revenue streams through carbon credits further bolster uptake. Meanwhile, manufacturers are integrating vertically to secure cassava, potato, or corn starch and to refine proprietary hybrid blends that solve durability gaps in heavy-duty field conditions.

Key Report Takeaways

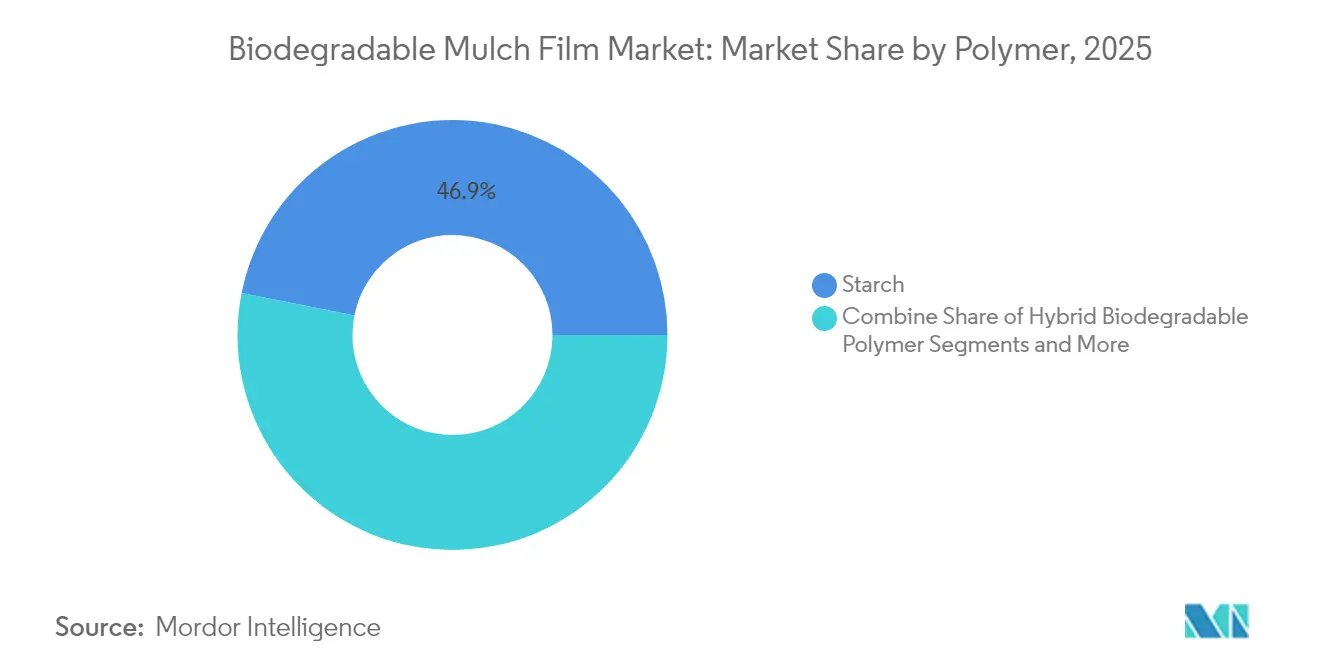

- By polymer category, starch-based films led with 46.88% of biodegradable mulch film market share in 2025; hybrid biodegradable polymers are projected to post the fastest 10.78% CAGR to 2031.

- By crop type, fruits and vegetables contributed 67.74% of the biodegradable mulch film market size in 2025, whereas flowers and ornamentals are forecast to expand at a 10.42% CAGR through 2031.

- By farming system, open-field cultivation accounted for 72.08% revenue in 2025; greenhouse and high-tunnel systems show the highest 9.02% CAGR over the outlook period.

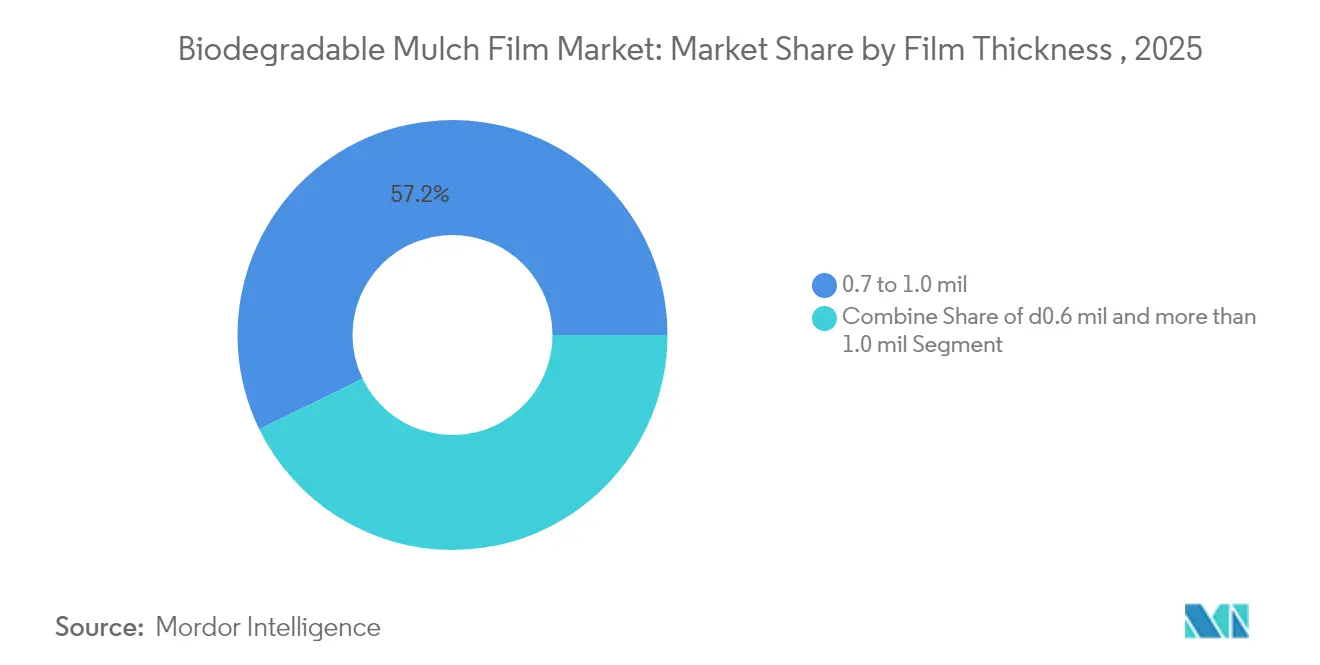

- By film thickness, 0.7-1.0 mil products occupied 57.22% of the biodegradable mulch film market in 2025; films above 1.0 mil thickness are poised for 11.15% CAGR growth to 2031.

- By sales channel, distributors and ag-dealer networks retained 82.45% share in 2025, while direct-to-farmer and e-commerce routes will climb at a 10.39% CAGR through 2031.

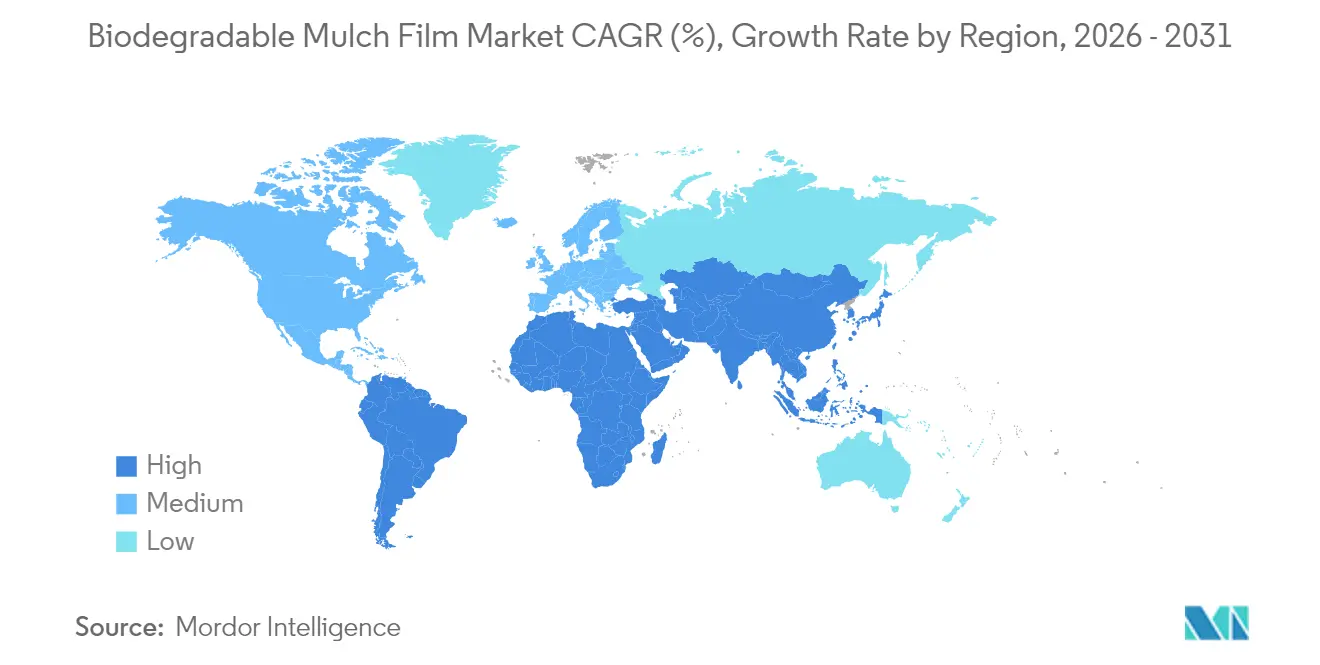

- By geograpghy, Asia-Pacific retained 41.02% share in 2025, and forecasted to grow at a 11.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biodegradable Mulch Film Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of greenhouse cultivation | +1.8% | Global, core in APAC & Europe | Medium term (2-4 years) |

| Government mandates and subsidies for soil-biodegradable films | +2.1% | Europe, North America & select APAC | Short term (≤ 2 years) |

| Rising disposal-cost penalties on polyethylene mulch | +1.5% | Europe & North America | Medium term (2-4 years) |

| Localization of low-cost cassava/potato starch feedstock | +1.3% | APAC focus, spill-over to South America | Long term (≥ 4 years) |

| Biochar-enriched films unlocking carbon-credit revenue | +0.9% | Global, early in Europe & North America | Long term (≥ 4 years) |

| GIS-based suitability mapping widens arable adoption zones | +0.6% | Global precision-ag markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Greenhouse Cultivation

Global greenhouse acreage keeps rising, creating a premium niche inside the biodegradable mulch film market where growers willingly absorb higher material costs to secure certification compliance and eliminate plastic-removal labor.[1]Government of Japan, “New Technology Makes Agriculture Possible on Barren Land,” japan.go.jp Controlled environments stabilize soil temperature and moisture, ensuring predictable degradation and strong crop-yield uplifts. European vegetable clusters now demand soil-biodegradable films to meet retailer sustainability scorecards, while high-tech greenhouse hubs in Japan employ film farming systems that integrate seamlessly with bio-based polymers. Reliable in-house monitoring of degradation data accelerates iterative formulation improvements, reinforcing manufacturer feedback loops and justifying premium price positions within the biodegradable mulch film market.

Government Mandates and Subsidies for Soil-Biodegradable Films

Subsidy programs and labeling rules are translating sustainability goals into near-term sales. California’s AB 1201 compels compostable products used in agriculture to satisfy USDA National Organic Program requirements by January 2026, effectively carving out an early-mover advantage for certified films.[2]Food Safety Magazine, “California Tightens Requirements for Labeling Products as ‘Compostable’,” food-safety.com Minnesota mirrors the approach with third-party certification deadlines in the same year. The European Union’s tighter migration thresholds for plastic materials from March 2025 raise compliance costs for polyethylene mulch, driving substitution. Inclusion of soil-biodegradable mulch films on the US National List of Approved Synthetic Substances further expands organic-farming addressable acreage. Collectively, these interventions inject clarity into return-on-investment calculations and spur R&D budgets across the biodegradable mulch film market.

Rising Disposal-Cost Penalties on Polyethylene Mulch

Field plastic recycling remains economically unviable owing to heavy soil contamination, with only 9% of farm plastics collected in the United States. Increasing landfill tipping fees, producer-responsibility levies, and stricter transport rules have made polyethylene-film disposal a line-item cost growers can no longer ignore. Biodegradable alternatives erase those post-harvest expenses while reducing the labor hours required for field cleanup, making the total-season economics more favorable, particularly for intensive horticulture operations in Europe and North America. This rising cost differential underpins expanded penetration across the biodegradable mulch film market.

Localization of Low-Cost Cassava and Potato Starch Feedstock

Starch supply chains anchored in Thailand, Indonesia, and Vietnam cut logistics overhead, buffer currency risk, and support rural incomes. Thai Wah’s ROSECO resin grades illustrate how vertically integrated starch processing underwrites cost parity strategies, enabling regional producers to capture share within the biodegradable mulch film market. Kazakhstan’s modified-starch research records tensile strengths rivaling PBAT while preserving full soil-degradation profiles.[3]MDPI, “The Use of Soil Surface Mulching on Melon (Cucumis melo L.) Production under Temperate Climate Conditions,” mdpi.comLower input volatility allows film suppliers to quote multi-season contracts that drive deeper distributor commitment and increase farmer confidence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High film and installation cost vs. PE alternatives | -2.3% | Global, higher in developing markets | Short term (≤ 2 years) |

| Inconsistent field-degradation and additive-leaching risks | -1.7% | Global, climate-variable regions | Medium term (2-4 years) |

| Impending microplastic rules on PBAT blends | -1.1% | Europe & North America | Medium term (2-4 years) |

| Competition from paper mulch and spray-on biopolymer coatings | -0.8% | North America & Europe, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Film and Installation Cost vs. PE Alternatives

At farm-gate, biodegradable rolls remain 2-3 times pricier than standard polyethylene, and specialized applicators may be needed to prevent premature tearing during laying. Lower-margin grain growers therefore hesitate, limiting rapid uptake outside premium crops. Although savings from avoided removal labor and landfill fees balance costs over multi-season horizons, financing hurdles persist for smallholder operations in Southeast Asia and Africa. Manufacturers must continue resin cost-down programs if the biodegradable mulch film market is to penetrate price-sensitive commodity segments.

Inconsistent Field-Degradation and Additive-Leaching Risks

Degradation speed swings with soil microbial density, moisture, and temperature, occasionally resulting in either premature film breakdown or residues that interfere with tillage schedules. Additive leachate concerns, particularly around plasticizers, raise buyer caution despite successful lab-scale compostability tests. Lack of harmonized global field-testing protocols deepens uncertainty, slowing standard-setting and retarding overall progress within the biodegradable mulch film market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Polymer: Starch Leads as Hybrids Gain Traction

Starch-based products held 46.88% of biodegradable mulch film market share in 2025, reflecting favorable feedstock economics and mature extrusion know-how. Hybrid blends that combine starch, PLA, and PBS are seeing 10.78% CAGR, propelled by durability in films thicker than 1.0 mil. BASF’s Ecovio M2351 demonstrates how tailored PBAT/PLA mixes meet mechanical-strength thresholds while passing soil-disintegration standards.

Advances in cassava- and potato-modified starch have narrowed moisture-barrier gaps, cutting defect rates in tropical field trials and improving mechanical performance relative to earlier starch films.The biodegradable mulch film market size for hybrids is forecast to climb once microplastic rules force incremental PBAT replacement, pushing demand toward fully mineralizable systems. Polylactic-acid volumes remain stable in premium greenhouse crops where predictable degradation outweighs cost concerns, while emerging PHA captures coastal acreage building on its marine-safe profile.

By Crop Type: High-Value Horticulture Sustains Momentum

Fruits and vegetables captured 67.74% of the biodegradable mulch film market size in 2025, underpinned by high per-acre revenue that justifies premium field inputs. Flowers and ornamentals, though smaller, will log 10.42% CAGR as consumer demand for sustainably produced blooms grows across Europe and North America.

Watermelon-specific Bio360 films exemplify crop-tailored design, offering heat management and wind resistance features valued in melon belts. Herbs and organic salad greens follow similar trajectories, leveraging yield lifts of 8-9% recorded in recent MDPI trials. Lower-margin grains remain tentative adopters as price gaps vs. polyethylene persist, but pilot projects integrating carbon-credit revenue are beginning to shift the calculus, broadening the biodegradable mulch film market.

By Farming System: Protected Cultivation Drives Premium Demand

Open-field systems represented 72.08% revenue in 2025 thanks to large land footprints, yet greenhouses and high tunnels show the strongest 9.02% CAGR on the back of controlled climate benefits that harmonize degradation with crop cycles. Studies confirm that biodegradable films stabilize soil temperature better than PE in greenhouse peppers, shortening maturation by up to six days.

High-tunnel growers appreciate simplified season transition: films degrade sufficiently ahead of replanting, saving labor otherwise spent on retrieval and disposal. Precision sensors increasingly alert growers to degradation milestones, ensuring that biodegradable mulch film market adoption in protected cultivation will keep rising across Asia, Europe, and North America.

By Film Thickness: Heavy-Duty Grades Outpace Mid-Gauge

Films between 0.7 and 1.0 mil accounted for 57.22% revenue in 2025, balancing material costs with acceptable life spans. Yet products above 1.0 mil register 11.15% CAGR, reflecting demand in mechanized farms that deploy heavier machinery and require stronger puncture resistance. Berry Hill data show 0.8 mil films lasting 5–6 months, a duration suiting two-cycle vegetable programs.

Ultra-thin gauges remain relegated to row crops with short seasons where price remains king. As hybrid resins strengthen tear resistance without sacrificing complete degradation, thick-film penetration will accelerate, elevating the premium tier inside the biodegradable mulch film market.

By Sales Channel: Direct-to-Farmer Platforms Accelerate

Traditional dealer networks still command 82.45% share given bundled agronomy services. However, direct-to-farmer and e-commerce routes carry a 10.39% CAGR as digitally savvy growers seek specialized advice and transparent pricing. Johnny’s Selected Seeds highlights this shift, offering online video guidance and agronomic chat support alongside biodegradable film SKUs.

Smaller film innovators leverage social-media marketing to bypass entrenched distribution, trimming channel costs and improving feedback loops. As data-literate farmers embrace on-farm trials, direct channels promise lasting influence over the biodegradable mulch film market’s route-to-market evolution.

Geography Analysis

Asia–Pacific commanded 41.02% of global revenue in 2025 and is expanding at 11.98% CAGR through 2031, buoyed by China’s vast protected-vegetable acreage and India’s subsidy schemes for bio-based farm inputs. Thailand’s cassava industry underpins local resin supply, trimming landed costs and enhancing competitiveness for domestic suppliers. Japanese material-evaluation breakthroughs shorten R&D cycles, ensuring regionally formulated films suit humid monsoon climates. Collectively, these factors cement Asia–Pacific as the centerpiece of the biodegradable mulch film market.

Europe ranks second by value, anchored by aggressive plastic-waste directives and large organic-farming footprints. German and Italian greenhouse hubs intensify demand, while EU migration-limit rules on food-contact plastics indirectly favor soil-biodegradable alternatives. Novamont collaborates with Bayer to integrate Mater-Bi clips and twine, extending system solutions beyond film alone. This holistic approach positions Europe as a technology and standards leader within the biodegradable mulch film market.

North America shows steady but policy-led growth. California’s compostability labeling law and extended-producer-responsibility schemes elevate compliance hurdles for polyethylene mulch, steering acreage toward certified soil-biodegradable alternatives. The United States processes only 9% of farm plastic waste, magnifying disposal cost savings when growers switch. Precision-ag mapping further supports regional expansion, identifying micro-zones of optimum degradation in the Corn Belt. Together, these levers sustain a healthy pipeline for the biodegradable mulch film market across the continent.

Competitive Landscape

Global supply remains fragmented, with suppliers controlling under one-quarter of revenue, though vertical integration is lifting entry barriers. BASF applies deep polymer-science capabilities to launch field-specific Ecovio grades, while Novamont’s cradle-to-cradle Mater-Bi platform pairs resins with agronomic accessories, offering growers a full suite of biodegradable inputs.

Equipment specialists such as Reifenhäuser contribute process know-how that lowers defect rates and substrate thinning, fostering multilayer architectures that elevate performance without raising material consumption. Emerging players exploit direct-to-farmer channels, promoting niche products like biochar-enriched films that secure premium positioning through carbon-credit eligibility. Intellectual-property portfolios around enzyme-accelerated degradation and robust starch modification are expected to widen competitive gaps as standardization pressure mounts across the biodegradable mulch film market.

Strategic partnerships are increasingly pivotal. Dow’s collaboration with New Energy Blue to derive bio-ethylene from corn stover signals rising interest from petrochemical majors in bio-feedstock back-integration. Likewise, Novamont’s European Biobased Solutions project aligns academic and industrial labs to speed commercialization. Such alliances combine supply security with brand equity, reinforcing the positions of early movers as market consolidation unfolds.

Biodegradable Mulch Film Industry Leaders

-

BASF SE

-

BioBag International AS

-

Organix A.G

-

Armando Alvarez Group

-

Novamont S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: TÜV Rheinland granted ISO 14064-1 verification to Kingfa Sci & Tech and entered a strategic cooperation pact to advance biodegradable plastics capabilities.

- June 2024: Novamont debuted the European Biobased Solutions project in Novara to accelerate sustainable agricultural films.

- June 2024: Bayer CropScience and Novamont started trials of Mater-Bi twine and clips in horticulture to slash on-farm plastic waste.

- May 2024: Japanese researchers unveiled a high-speed material-evaluation method that quickly compares hundreds of biodegradable candidates under identical soil conditions.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the biodegradable mulch film market as sales of soil-biodegradable plastic films, paper or starch-based sheets that are laid on cultivated land to suppress weeds, conserve moisture, and regulate temperature, with the film intentionally left in the field to decompose after harvest. The study covers fresh, factory-made films <= 2 mm thick that meet EN 17033, ISO 23517, or equivalent soil-degradation standards and are used in open-field as well as protected cultivation systems.

Scope exclusion: recycled polyethylene and photodegradable mulch films are outside our numbers.

Segmentation Overview

-

By Polymer

- Starch

- Polylactic Acid (PLA)

- Polyhydroxyalkanoates (PHA)

- Aliphatic-Aromatic Copolymers (AAC)

- Polybutylene Adipate-Terephthalate (PBAT)

- Polybutylene Succinate (PBS)

- Hybrid Biodegradable Polymer

-

By Crop Type

- Fruits and Vegetables

- Flowers and Ornamentals

- Grains and Oilseeds

- Other Specialty Crops

-

By Farming System

- Open-Field Cultivation

- Greenhouse / High Tunnel

-

By Film Thickness

- ≤0.6 mil

- 0.7-1.0 mil

- More than 1.0 mil (heavy-duty)

-

By Sales Channel

- B2B (Agricultural Dealers and Distributors)

- B2C (Direct-to-Farmer and E-commerce)

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacifc

-

Middle East and Africa

-

Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

-

Africa

- South Africa

- Kenya

- Rest of Africa

-

Middle East

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed agronomists, horticulture-input distributors, polymer compounders, and farm-equipment dealers across Asia-Pacific, Europe, and North America. Their insights on field-level degradation, subsidy uptake, and price premiums filled data gaps and let us validate acreage adoption rates derived from secondary sources.

Desk Research

Our analysts first screened public datasets such as FAO crop production statistics, Eurostat agri-environment indicators, USDA National Agricultural Statistics Service acreage reports, and China's Ministry of Agriculture plastic-film recovery bulletins. Trade association briefs from European Bioplastics and the Plasticulture Equipment & Supplies Dealers Association clarified polymer penetration trends. Company 10-K filings and investor decks helped benchmark average selling prices, while D&B Hoovers provided supplemental financials on regional converters. This list is illustrative; many more open and subscription sources informed our desk review.

Market-Sizing & Forecasting

A top-down acreage model begins with hectares under mulching-friendly crops, then applies region-specific penetration of biodegradable films derived from trade data reconstructions before multiplying by sampled film thickness and ASPs. Supplier roll-ups and channel checks serve as a light bottom-up cross-check. Key variables include: 1) protected-cultivation acreage, 2) subsidy value per hectare, 3) price gap versus polyethylene film, 4) average film life in crop cycles, and 5) disposable-income driven fresh-produce demand. A multivariate regression links these drivers to historical consumption; an ARIMA overlay projects short-term shocks. Missing bottom-up details are adjusted with weighted averages from confirmed interview ranges.

Data Validation & Update Cycle

Outputs pass variance checks against independent indicators such as polymer import volumes and farm-input spending. Senior analysts review anomalies, and peer review precedes sign-off. Reports refresh annually, with mid-cycle updates if material policy or price changes emerge.

Why Mordor's Biodegradable Mulch Film Baseline Commands Reliability

Published estimates often differ because each firm frames the market, base year, and adoption metrics uniquely.

Key gap drivers include divergent inclusion of compostable paper sheets, use of shipment weight rather than farm purchases, and single-country sampling. Mordor reports the market in value terms at the farm gate, applies uniform biodegradability criteria, and refreshes its base year every twelve months, reducing currency and inflation skews.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 65.06 million (2025) | Mordor Intelligence | - |

| USD 50.75 million (2024) | Global Consultancy A | Excludes greenhouse acreage and uses average film weight only |

| USD 68.0 million (2024) | Trade Journal B | Counts only starch films, omits PBAT blends |

| USD 82.82 million (2024) | Regional Consultancy C | Converts volumes at list prices without subsidy adjustments |

The comparison shows that market value shifts with scope, pricing, and refresh cadence.

By aligning on clearly stated degradation standards, triangulated acreage, and annually updated price decks, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can trace back to verifiable variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the biodegradable mulch film market?

The market stood at USD 70.12 million in 2026 and is projected to reach USD 102.03 million by 2031.

Which region leads global demand?

Asia–Pacific dominates with 41.02% revenue in 2025 and shows the fastest 11.98% CAGR through 2031.

Why are starch-based films so prominent?

Readily available cassava and potato feedstocks, coupled with mature processing, helped starch products secure 46.88% share in 2025.

How do biodegradable films offset higher purchase prices?

They eliminate plastic-removal labor and landfill fees, and in greenhouse systems they boost yield, improving whole-season economics.

What threatens future growth?

Cost gaps with polyethylene, inconsistent field degradation, and upcoming microplastic regulations on PBAT blends pose notable challenges.

Which farming systems offer the best fit?

Greenhouses and high tunnels deliver predictable degradation environments, driving a 9.02% CAGR for protected-cultivation demand.

Page last updated on: