Bioceramics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.49 Billion |

| Market Size (2031) | USD 6.5 Billion |

| Growth Rate (2026 - 2031) | 7.64% CAGR |

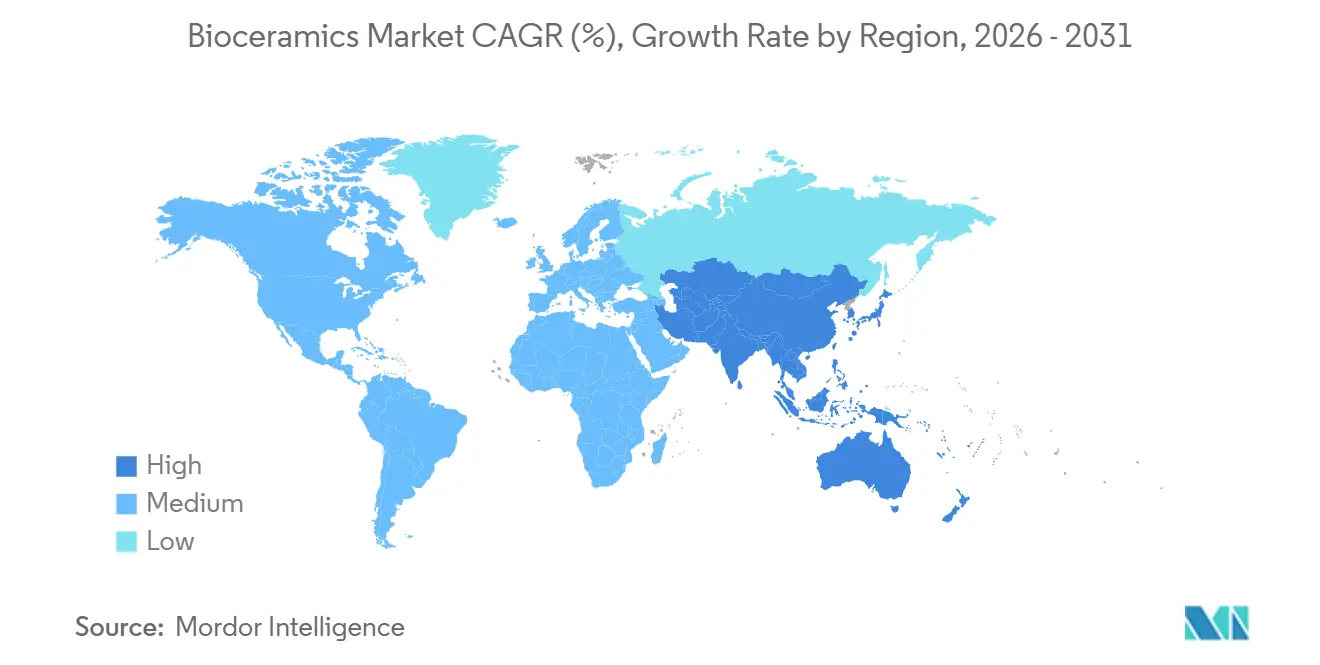

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

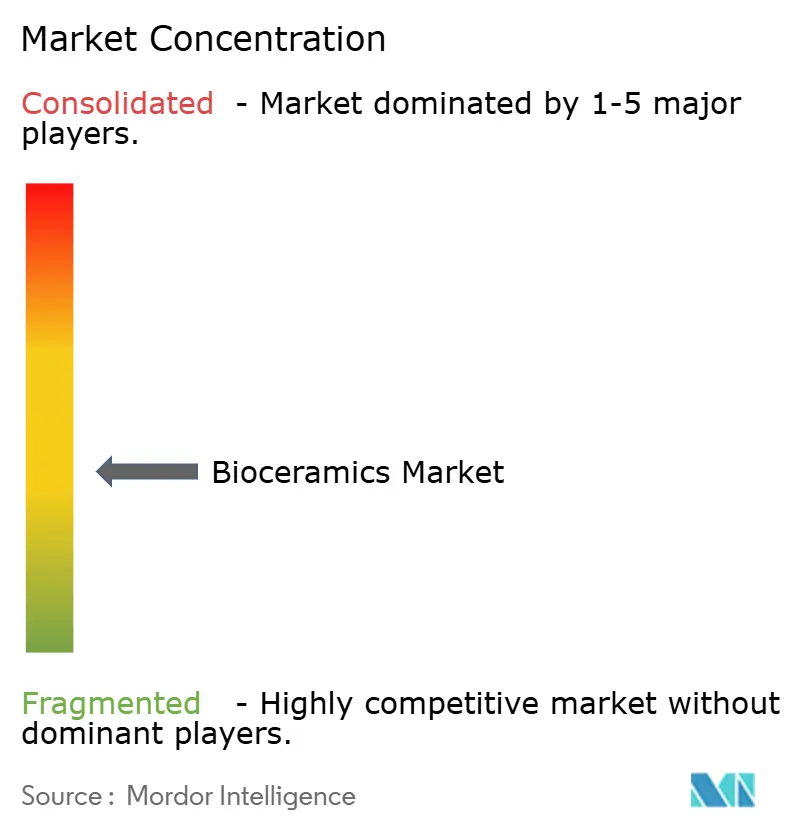

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bioceramics Market Analysis by Mordor Intelligence

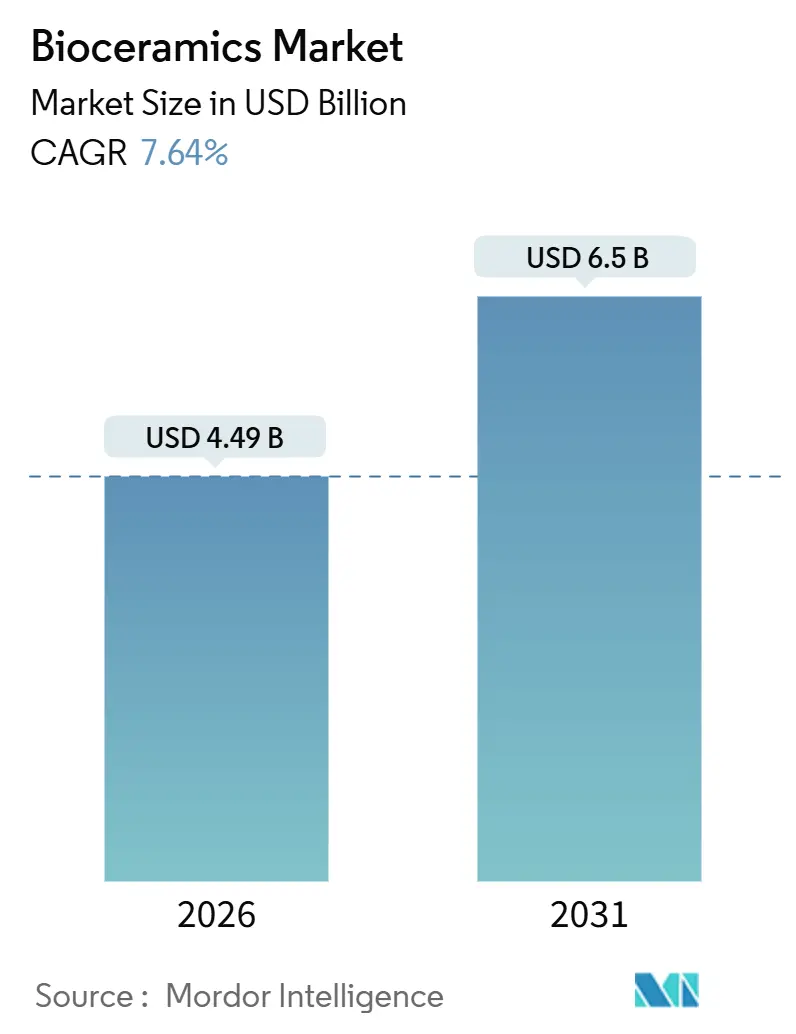

The Bioceramics Market size is estimated at USD 4.49 billion in 2026, and is expected to reach USD 6.5 billion by 2031, at a CAGR of 7.64% during the forecast period (2026-2031). Surging preference for bio-inert ceramic bearings in hip and knee arthroplasty, rapid uptake of 3D-printed patient-specific implants, and government programs that reimburse calcium-phosphate scaffolds over autografts in spine surgery are the principal growth engines. Aluminum oxide maintains a dominant presence owing to its outstanding compressive strength, yet zirconia is capturing dental-implant demand because practitioners value metal-free esthetics and lower peri-implantitis risk. Hospitals account for the largest share of bioceramic consumption, but adoption is accelerating in dental clinics as chairside milling shortens crown delivery to a single visit. Competitive intensity is increasing as original-equipment manufacturers integrate ceramic-bearing production to secure supply and retain margin.

Key Report Takeaways

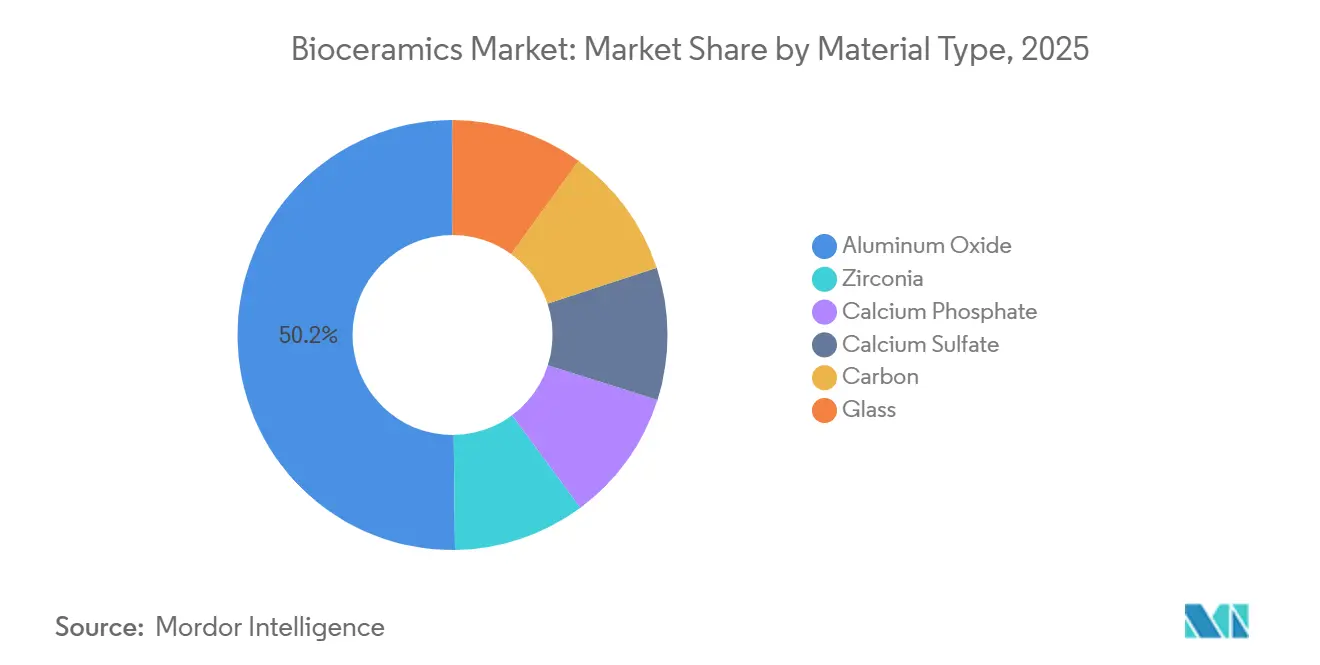

- By material type, aluminum oxide led with 50.18% revenue share in 2025 and is expected to post the fastest growth at a 7.91% CAGR for 2026-2031.

- By form, powder accounted for 48.45% of the bioceramics market share in 2025, while liquid (injectable) is projected to expand at a 7.88% CAGR through 2031.

- By type, bio-inert ceramics held 80.81% of the bioceramics market share in 2025, showing the highest projected CAGR at 7.96% through 2031.

- By application, dental solutions commanded 37.12% of the bioceramics market size in 2025, and biomedical is set to advance at a 7.70% CAGR to 2031.

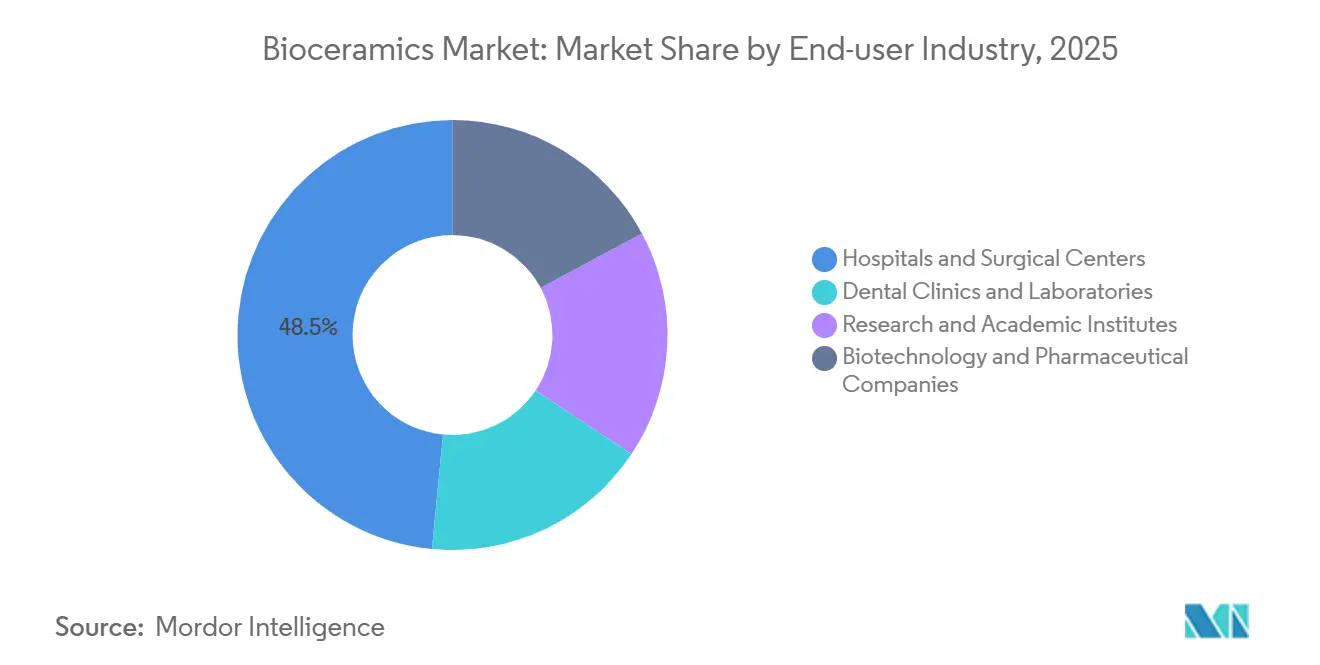

- By end-user industry, hospitals and surgical centers retained a 48.48% share of the bioceramics market in 2025, while dental clinics and laboratories are set to record the strongest 7.85% CAGR to 2031.

- By geography, Europe dominated with a 44.10% share of the bioceramics market in 2025; Asia Pacific exhibits the highest 8.04% CAGR forecast through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Bioceramics Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of 3D-printed custom implants | +1.2% | North America, Germany | Medium term (2-4 years) |

| Accelerated dental-implant penetration boosting zirconia | +1.5% | Europe, Asia Pacific | Short term (≤ 2 years) |

| Government spine-surgery programs fueling calcium-phosphate use | +0.8% | China, India, Brazil | Long term (≥ 4 years) |

| OEM shift from metal to bio-inert ceramic bearings | +1.1% | North America, Europe, Japan | Medium term (2-4 years) |

| Bioactive-glass coatings for antimicrobial screws | +0.7% | Global revision-surgery centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of 3D-Printed Custom Implants

Regulators in the United States now clear patient-specific bioceramic devices under the 510(k) pathway in as little as 12 months, down from 36 months in conventional filings[1]U.S. Food & Drug Administration, “510(k) Premarket Notification,” fda.gov. Stryker won clearance for a calcium-phosphate craniofacial implant that replicates native bone porosity and halves vascular ingrowth time. Surgeons prefer these lattice geometries in complex reconstructions because they eliminate intraoperative contouring and shorten anesthesia exposure. Germany’s Fraunhofer Institute reports that binder-jetting alumina slashes lead times to five days and material waste to 8%. Adoption is further helped by ISO/ASTM 52900, which standardizes layer thickness and post-processing, giving manufacturers a harmonized path toward CE-mark approval.

Accelerated Dental-Implant Penetration Boosting Zirconia

Five-year cohort studies show peri-implantitis in only 3.2% of zirconia abutments compared with 5.8% for titanium, nudging clinicians toward ceramic restorations. Straumann reported a 14% jump in zirconia-based revenue in 2025, well ahead of its overall implant line. Chairside systems such as the CEREC platform mill pre-sintered blanks in 12 minutes and allow same-day delivery, slicing laboratory overhead by 40%. The FDA categorizes zirconia ceramics as Class II devices, while the EU MDR imposes post-market fracture surveillance, an administrative cost that consolidates supply among vertically integrated firms.

Government Spine-Surgery Programs Fueling Calcium-Phosphate Use

China’s Healthy China 2030 mandate expanded lumbar-fusion reimbursement to over 300 prefecture-level cities, sending procedure volumes up 22% year-over-year. India’s Ayushman Bharat covers up to INR 500,000 (USD 6,000) per spinal case, prompting public hospitals to favor injectable calcium sulfate over autografts that lengthen operations. BoneSupport’s CERAMENT has gained approvals in 18 Asian and Latin American countries, positioning the company for government tenders that prioritize cost-effectiveness. Compliance challenges revolve around local clinical data requirements, yet cost advantages keep adoption on an upward path.

OEM Shift from Metal to Bio-Inert Ceramic Bearings

Zimmer Biomet states that ceramic-on-polyethylene constructs now represent 62% of primary hip systems in Europe, compared with 48% in 2022. FDA guidance on metal-on-metal hips and ISO 6474-2 standards for ceramics have convinced surgeons that alumina and zirconia femoral heads minimize metal-ion release and lower revision risk. KYOCERA supplies roughly 40% of global ceramic femoral heads with fracture toughness above 6 MPa·m½, winning approvals for younger, high-activity patients.

Restraints Impact Analysis of Bioceramics Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter FDA nanoceramic dispersion guidelines | -0.40% | North America, with ripple effects in markets seeking FDA recognition | Short term (≤ 2 years) |

| Threat of substitutes | -0.50% | Global, concentrated in orthopedics and dental segments | Medium term (2-4 years) |

| High sintering energy costs compressing margins | -0.60% | Europe, Japan, South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter FDA Nanoceramic Dispersion Guidelines

The FDA now requires particle-size testing by dynamic light scattering and electron microscopy for injectable ceramics and demands two-year biodistribution studies, adding roughly USD 1.2 million to preclinical costs. Smaller developers face 18-month submission delays while European regulators have not followed suit, prompting firms to seek CE marks first. CeramTec reformulated two product lines to comply, pushing launch dates into 2026.

High Sintering Energy Costs Compressing Margins

Firing alumina or zirconia at 1,600°C consumes up to 65 kWh per kilogram, and European gas prices averaged EUR 40 per MWh in 2025, double the 2019 baseline[2]Restraint (~) % Impact on CAGR Forecast Geographic Relevance Impact Timeline Stricter FDA nanoceramic dispersion guidelines -0.40% North America, with ripple effects in markets seeking FDA recognition Short term (≤ 2 years) Threat of substitutes -0.50% Global, concentrated in orthopedics and dental segments Medium term (2-4 years) High sintering energy costs compressing margins -0.60% Europe, Japan, South Korea Medium term (2-4 years) . Gross margins for German suppliers slid 4.8 percentage points, whereas KYOCERA and CoorsTek cushioned costs through captive power and waste-heat recovery. Subsidy programs in Japan cover up to 30% of energy-efficiency investments, but smaller Korean vendors face sustained pressure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Bioceramics Market Segment Analysis

By Material Type:

Alumina Anchors Share, Zirconia Gains in EstheticsAluminum oxide retained 50.18% of the bioceramics market share in 2025 and is projected to post a 7.91% CAGR through 2031, supported by compressive strength exceeding 4,000 MPa. Zirconia is growing faster in dental and craniofacial indications due to transformation toughening that boosts flexural strength beyond 1,200 MPa.

Alumina’s chemical inertness underpins long-term survival in hip and knee replacements, while zirconia’s tooth-colored appearance fuels its uptake in anterior restorations. Calcium-phosphate materials dominate bone-graft substitutes because they remodel into native bone within 12 months. Carbon-based bioceramics occupy specialized niches such as intervertebral discs, and bioactive glass is emerging in antimicrobial coatings that cut infection risk without systemic antibiotics.

By Form:

Powder Dominates, Injectables Surge in Minimally Invasive ProceduresPowder products captured 48.45% of the 2025 bioceramics market size thanks to economical press-and-sinter lines that hold tolerances within ±0.05 millimeters. Liquid injectables, however, are advancing at a 7.88% CAGR as vertebroplasty and kyphoplasty shift toward outpatient settings.

Injectables blend calcium phosphate or sulfate with viscosity modifiers to achieve 12-minute working windows, enabling delivery through 11-gauge needles under fluoroscopy. Granules and blocks remain relevant in maxillofacial surgery, where surgeons value manual contouring. Asia Pacific shows the highest injectable penetration because aging populations favor minimally invasive vertebral augmentation that trims hospital stays to a single day.

By Type:

Bio-Inert Leads, Bio-Resorbable Gains in PediatricsBio-inert ceramics accounted for 80.81% of 2025 revenue and are expanding at a 7.96% CAGR on the back of decades of clinical data supporting alumina and zirconia bearings. Bioactive ceramics bond directly to bone within 48 hours, accelerating osseointegration in coated stems and dental implants.

Bioresorbable ceramics, especially tricalcium phosphate, are gaining traction in pediatric craniofacial surgery because they disappear as the child’s bone matures, avoiding future removal operations. Stryker’s resorbable cranial system, cleared in 2024, resorbs fully within 24 months, demonstrating clinical feasibility.

By Application:

Dental Leads, Biomedical AcceleratesDental implants represented 37.12% of the 2025 bioceramics market. Straumann and Dentsply Sirona together command 48% of global placements through vertically integrated zirconia workflows. Orthopedics remains the backbone of alumina and zirconia demand, while biomedical uses, drug-eluting coatings, sensors, and tissue scaffolds are growing fastest at a 7.70% CAGR.

Bioactive-glass microspheres embedded in polymeric screws release antibiotics over 90 days, cutting surgical-site infections by 38% in a 240-patient trial. Regulatory pathways treat these as combination products, raising the bar for newcomers but solidifying the opportunity for established suppliers.

By End-User:

Hospitals Dominate, Dental Clinics GainHospitals and surgical centers absorbed 48.48% of 2025 sales as group-purchasing organizations negotiated discounts in exchange for formulary standardization. Dental clinics are advancing at a 7.85% CAGR because chairside milling systems now deliver zirconia crowns during a single appointment, boosting patient compliance.

Research institutes employ bioceramics in NIH-funded trials focused on bone regeneration, while pharmaceutical companies investigate calcium-phosphate microspheres for sustained bisphosphonate release. Varied compliance regimes, for example, Joint Commission traceability in hospitals versus state dental-board rules in clinics, complicate vendor strategies but also create tailored niches.

Geography Analysis

Europe Bioceramics Market

Europe generated 44.10% of 2025 revenue, anchored by Germany’s precision-machining clusters and France’s reimbursement that prefers ceramic bearings over polyethylene. Hip replacement incidence exceeds 280 per 100,000 population in Germany, securing a robust replacement cycle, yet revision cases use fewer ceramics due to fracture concerns in compromised bone. The United Kingdom extended zirconia-implant reimbursement in 2025, adding significant volumes in London and Southeast England, where private practice is dominant. Southern European health systems emphasize cost containment, confining premium ceramics to private clinics that serve medical tourists.

APAC Bioceramics Market

Asia Pacific is the fastest-growing region at an 8.04% CAGR through 2031, driven by China’s RMB 1.2 trillion Healthy China 2030 spending and India’s Ayushman Bharat insurance covering 500 million citizens. Japan’s Pharmaceuticals and Medical Devices Agency extends ceramic approvals to younger patients, recognizing their 30-year implant life. South Korea now reimburses bioactive-glass coatings in revision cases, aiming to cut infection-related readmissions by 18% and save KRW 240 billion annually. Regulatory timelines diverge: China requires in-country trials, while India often accepts FDA clearances, giving multinationals a speed advantage.

The Americas and MEA Bioceramics Market

North America, South America, and the Middle East & Africa collectively hold the remaining share. In the United States, Medicare DRG 470 reimburses ceramic hip bearings at USD 18,500 per procedure, supporting adoption in ambulatory centers that target active patients. Canada sees private-pay upgrades because provincial wait lists push patients toward faster options. Brazil reimburses bioactive ceramics for vertebral compression fractures, a change that adds 85,000 procedures yearly. Saudi Arabia’s Vision 2030 specifies ceramic hips for patients under 60 in flagship medical cities, fostering regional demand that favors suppliers with ISO 13356 certification.

Value Chain Analysis

The bioceramics value chain starts with upstream suppliers of high-purity alumina and zirconia powders, calcium phosphate and calcium sulfate precursors, and bioactive-glass inputs, followed by intermediate processing steps such as powder classification, slurry preparation, granulation, machining of pre-sintered blanks, high-temperature sintering, and increasingly additive manufacturing for patient-specific geometries. Downstream, medical device OEMs and dental system companies integrate these ceramics into bearings, implants, and bone graft substitutes, and then sell through direct channels and specialized distributors into hospitals, surgical centers, and dental clinics.

Bottlenecks cluster around capital equipment and qualification timelines. Lead times for specialized milling and classification equipment can run 6 to 12 months, and supplier qualification and validation under medical device quality systems commonly extend 12 to 18 months, which slows multi-source transitions. Supply tightness also shows up in ceramic dental implants, with the European Society for Ceramic Implantology citing 2025 market supply constraints, reinforcing the importance of vertically integrated players and long-term procurement planning. On the enabling side, Himed and Lithoz opened a Bioceramics Center of Excellence in New York in May 2024, combining lithography-based ceramic manufacturing with materials expertise to shorten iteration cycles for OEM prototyping and scale-up.

Competitive Landscape

The Bioceramics market is moderately fragmented. Vertical integration accelerated as Stryker bought a German zirconia machining plant and Zimmer Biomet installed in-house sintering, shrinking lead times to six weeks. Disruptors such as CAM Bioceramics deliver patient-matched implants 30% below incumbent prices by bypassing distributors. In response, Straumann and Dentsply Sirona promote end-to-end digital ecosystems that lock dentists into proprietary consumables carrying 65% gross margins.

Bioceramics Industry Leaders

CeramTec GmbH

KYOCERA Corporation

CoorsTek Inc.

Institut Straumann AG

Zimmer Biomet

- *Disclaimer: Major Players sorted in no particular order

Bioceramics Market Companies Covered in this Report

- Berkeley Advanced Biomaterials

- BoneSupport AB

- CAM Bioceramics

- CeramTec GmbH

- CGbio

- CoorsTek Inc.

- CTL Amedica

- Dentsply Sirona

- dsm-firmenich

- FKG Dentaire Sàrl

- Himed

- Institut Straumann AG

- Ivoclar Vivadent AG

- Jyoti Ceramic

- KYOCERA Corporation

- Medical Device Business Services, Inc.

- Morgan Advanced Materials

- Sagemax

- Shandong Sinocera Functional Materials Co., Ltd.

- Stryker

- TOSOH CERAMICS CO., LTD.

- Zimmer Biomet

Market Opportunities and Future Outlook

Opportunities are concentrated on expanding capacity and building regulatory-ready product platforms in bone graft substitutes, where injectable formats and putties are being adopted to support minimally invasive workflows. In South Korea, CGBio opened its NOVO Factory in Hwaseong in March 2026, stating capacity of 1 million syringes of Novosis Putty annually, and in May 2026 the company received a favorable MFDS re-examination decision for Novosis supported by a seven-year post-market surveillance study. That outcome supports continued tender participation and strengthens hospital purchasing confidence.

A second whitespace is contract manufacturing and analytical services that help OEMs address tighter characterization and validation expectations for ceramics and injectables. CaP Biomaterials completed an expansion of its East Troy, Wisconsin facility in June 2026, adding lab space and analytical equipment to support portfolio additions, aligning with the industry shift toward faster qualification and tighter particle and chemistry controls, including dual-sourcing. For dental and orthopedic implants, scaling high-throughput, consistent zirconia and alumina processing remains a practical gap, and that is reinforced by announced manufacturing investments such as Shinheung MSTs July 2026 investment MOU for a new facility in Wonju, aimed at increasing implant-set output over the longer term.

Recent Industry Developments in Bioceramics Market

- July 2026: Shinheung MSTs announced an investment MOU for a new facility in Wonju to materially increase implant-set output. The project points to a planned scale-up in zirconia and alumina processing capabilities, supported by a long-term supply contract with local suppliers. The update positions Shinheung MSTs as a regional manufacturing hub for next-generation dental and orthopedic implants.

- August 2025: Lionstead Applied Materials completed the acquisition of Ceramat, a bioceramics manufacturer. The deal expanded Lionstead's advanced materials footprint and set Ceramat up as a bioceramics platform asset for commercialization. It also supports expanded joint development programs and scales regional sales in Europe and North America.

- May 2024: Himed and Lithoz opened a Bioceramics Center of Excellence at Himed's New York headquarters to integrate additive manufacturing with bioceramics materials and analytical services. The facility supports rapid prototyping and development programs for medical device manufacturers, with the stated goal of shortening iteration cycles for patient-specific and complex-geometry ceramic implants.

Bioceramics Market Report Scope and Research Methodology

Market Definition and Coverage

In this methodology, the bioceramics market is defined as the revenue generated from medical-grade ceramic materials that are used inside the human body for implant, coating, or tissue repair uses, and it is sized at the manufacturer level in USD.

Scope exclusions: We exclude general industrial technical ceramics and non-ceramic implant materials. We also exclude routine dental consumables that are not counted as implant-grade bioceramic materials.

Segments Covered in This Report

- By Material Type

- Aluminum Oxide

- Zirconia

- Calcium Phosphate

- General Purpose

- Hydroxyapatite

- Calcium Sulfate

- Carbon

- Glass

- By Form

- Powder

- Liquid (Injectable)

- Other Forms

- By Type

- Bio-inert

- Bio-active

- Bio-resorbable

- By Application

- Orthopedics

- Dental

- Biomedical

- By End-user

- Hospitals and Surgical Centers

- Dental Clinics and Laboratories

- Research and Academic Institutes

- Biotechnology and Pharmaceutical Companies

- By Geography

- Asia Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle East and Africa

- Asia Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean fact base on procedure demand, material adoption, and trade flows that can be checked year over year. We mainly used public sources such as the US FDA device databases, OECD health statistics, World Health Organization health indicators, World Bank macro series, and trade statistics published through UN Comtrade, along with peer-reviewed journals covering orthopedic and dental biomaterials.

To convert those signals into usable sizing inputs, we also reviewed manufacturer annual reports, investor presentations, and medical association publications that discuss implant volumes, clinical trends, and reimbursement shifts. Where needed, we used paid subscriptions for company financials and news intelligence, plus patent databases to understand where new ceramic compositions and coatings are being developed and adopted. These desk research sources are illustrative only, and many more public references were also used for collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what gets counted as bioceramic revenue and what stays outside scope, since product mixes can vary widely by application. We spoke with a spread of implant supply chain participants, including material processors, component makers, and downstream medical device and distribution roles across major regions. The conversations helped us confirm adoption rates, pricing logic, and near-term demand signals.

The same discussions were used to pressure-test assumptions such as mix shift between alumina, zirconia, calcium phosphate, and bioactive glass. They were also used to confirm how much revenue sits in coatings versus bulk implant components.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 16% | APAC: 47% |

| Mid tier: 47% | Functional/Unit leaders: 25% | EMEA: 34% |

| Smaller Players: 16% | Managers: 59% | Americas: 19% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand pool that is reconstructed from procedure volumes and implant penetration, and then translated into material demand and value using application-level material intensity and pricing ranges. To keep the model grounded, we corroborate results through selective bottom-up checks, such as rolling up a sampled set of supplier revenues where disclosures exist, and cross-checking implied average selling prices against interview-confirmed ranges.

Key inputs used in the model include orthopedic and dental procedure volumes, age profile and joint replacement growth trends, implant mix shifts by material type, the split between bulk components and coatings, and typical pricing progression by grade and form factor. When bottom-up information is missing for smaller or private participants, gaps are handled using conservative share assumptions tied back to regional procedure demand and import-export signals, rather than simple straight-line scaling.

For forecasting, scenario analysis is used so the outlook can reflect realistic pathways for procedure growth, elective surgery normalization, and adoption of bioactive and resorbable ceramics in specific clinical uses. The variable paths are then aligned with what interviewees expect on timing for new product approvals and capacity additions, which helps avoid overstating short-term jumps.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, including procedure trends, disclosed revenue points, and implied pricing checks. We then compare results across regions to spot unit or currency inconsistencies. If a variance looks too large to be explained by mix or timing, we revisit assumptions and re-engage selected contacts to confirm what changed and why.

Before sign-off, the model goes through multi-step analyst review where calculations, conversions, and scope boundaries are rechecked. Outliers are documented or corrected. Reports are refreshed annually, and interim updates are made when material events occur, such as sharp procedure disruptions, meaningful regulatory changes, or major capacity shifts. Right before delivery, a final review pass is performed so clients receive the latest updated view.

Mordor Intelligence's Bioceramics Market Size Compared With Other Published Estimates

It is normal to see different bioceramics market values across public sources, even when they sound like they are talking about the same space. In most cases, the gap is created by how each publisher defines what is in scope, which year is treated as the base, and how pricing and adoption are projected forward.

By tracking procedure volumes, implant material mix, and manufacturer-level revenue recognition rules, Mordor Intelligence keeps the market total focused on medical-grade ceramic materials used in implanted applications, rather than folding in broader biomaterials or adjacent medical device revenue. Some estimates also lean on more aggressive adoption curves for newer bioactive and resorbable uses, or they convert currencies using different timing, which can widen the spread even when the growth rate looks similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.49 B (2026) | |

| Global Consultancy A | USD 19.60 B (2025) | Uses a broader revenue pool that appears to include wider medical device application coverage and potentially counts more downstream system value, which lifts the starting point versus a materials-only invoice view. |

| Industry Publisher B | USD 13.54 B (2024) | Anchors the estimate to an earlier base year and may apply wider material and end-use inclusions, which can blend implant-grade ceramics with adjacent biomedical categories and raise the reported total. |

The comparison shows that the biggest driver is not the math, it is the boundary around what revenue is counted and at which point in the value chain it is measured. When scope is kept tight to implant-grade ceramic materials and then validated with procedure-led demand signals and pricing checks, the resulting market size stays easier to reproduce and explain in a client review.

Key Questions Answered in the Report

What is the current value of the bioceramics market?

The bioceramics market size reached USD 4.49 billion in 2026 and is forecast to hit USD 6.5 billion by 2031.

Which material dominates global demand?

Aluminum oxide leads with 50.18% share, mainly in hip and knee replacements.

Why is zirconia gaining popularity in dentistry?

Zirconia abutments offer metal-free esthetics and show lower peri-implantitis rates than titanium.

Which region is growing the fastest?

Asia Pacific is projected to register an 8.04% CAGR through 2031 due to large public-health programs in China and India.

How are energy prices affecting ceramic manufacturers?

Elevated gas prices in Europe raise sintering costs, squeezing margins for producers without captive power.

Page last updated on: