Market Overview

| Study Period | 2019 - 2030 |

|---|---|

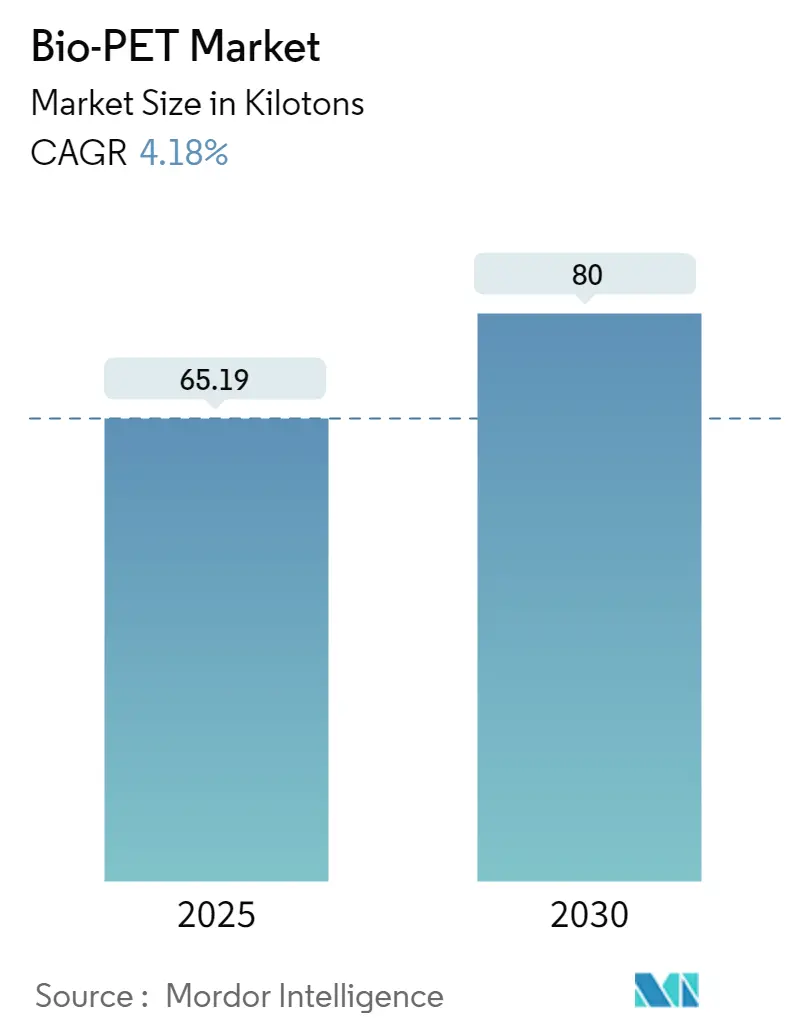

| Market Volume (2025) | 65.19 kilotons |

| Market Volume (2030) | 80 kilotons |

| Growth Rate (2025 - 2030) | 4.18% CAGR |

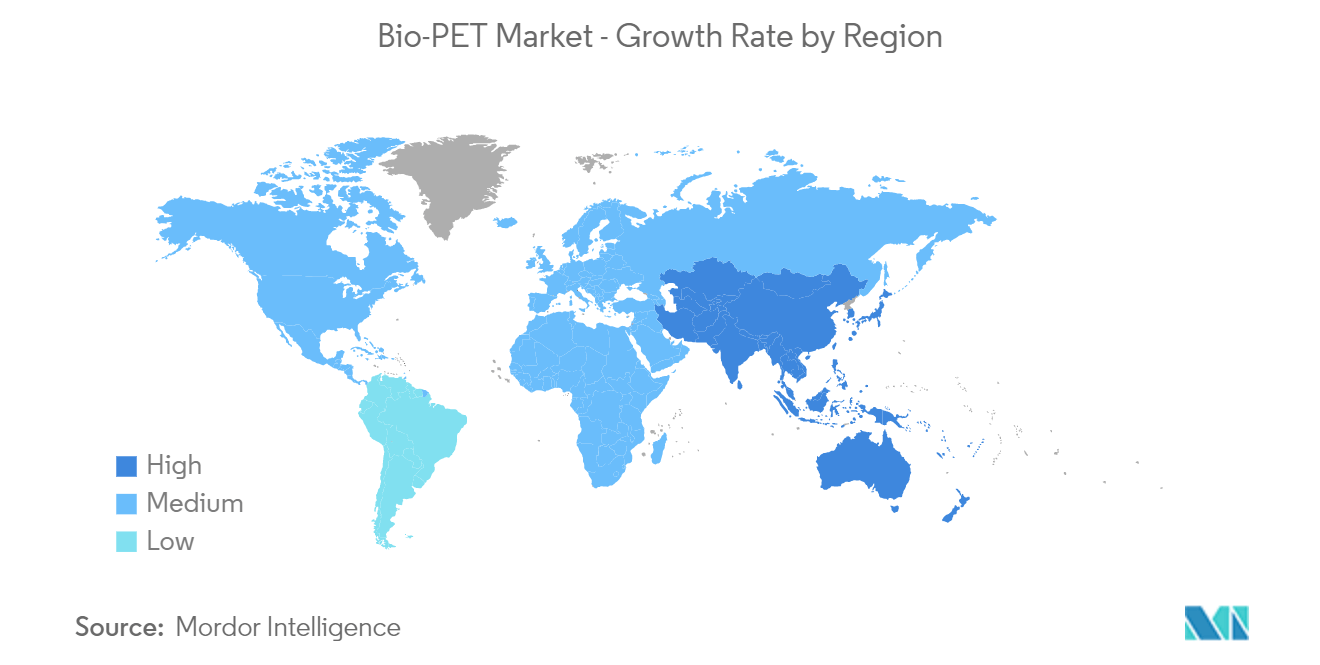

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bio-PET Market Analysis by Mordor Intelligence

The Bio-PET Market size is estimated at 65.19 kilotons in 2025, and is expected to reach 80.00 kilotons by 2030, at a CAGR of 4.18% during the forecast period (2025-2030).

Due to the COVID-19 outbreak, nationwide lockdowns worldwide, disruption in manufacturing activities and supply chains, and production halts negatively impacted the market in 2020. However, the conditions started recovering in 2021, restoring the market's growth trajectory.

- One of the major factors driving the market studied is the growing GHG (Greenhouse Gases) emission concerns.

- However, the development of PEF (Polyethylene Furanoate) and a low melting point of bio PET is likely to restrain the market.

- Environmental factors encouraging a paradigm shift will likely boost the demand for Bio-PET during the forecast period.

- Focus on renewable sources is likely to act as an opportunity for market growth in the future.

- Asia-Pacific dominated the market across the world, closely followed by North America. Asia-Pacific is likely to witness the highest growth rate during the forecast period.

Global Bio-PET Market Trends and Insights

Bottles Application to Dominate the Market

- Bio-PET is widely used in bottling applications. The demand for these is increasing rapidly worldwide as companies want to reduce their dependency on fossil-fuel-based products. In addition, the demand from consumers for bio-based products is also increasing.

- Bio-PET is a packaging material that helped advance the beverage industry by providing billions of people access to clean drinking water. The material offers safety and is lightweight, transparent, resealable, moldable, and 100% recyclable, with exceptional mechanical and barrier properties.

- Bio-PET is present in the market for many years. The plastic is made from 30% renewable and 70% petroleum-based raw materials. Bio-PET's mechanical and thermal properties are similar to other oil-based PET products, thus making it an ideal replacement for virgin PET.

- Bio-based PET (polyethylene terephthalate) is made from partially renewable raw materials. The benefits are clear. By using more renewable raw materials, fewer petroleum-based raw materials are required. Topics that consumers increasingly value and allow for differentiation. Bio-PET allows brand owners to highlight their position and draw attention to their products.

- As per the International Bottled Water Association (IBWA) reports, bottled water is the most consumed beverage product in the United States in terms of volume. A similar trend is being followed in the Asian-Pacific region, where the consumption of packaged drinking water is triggered in the past few years. Small-scale manufacturers flooded the market with vast production capacities for bottle production, thus positively supporting the bio-PET market.

- The bottle application will likely dominate the Bio-PET Market due to the abovementioned reasons.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region is home to half of the population in the world, and its consumption of PET bottles is high.

- This region is expected to play a prominent role in the growth of Bio-PET Market usage, as it massively helps the wide-scale acceptance of bio-PET in multiple applications, like textile, packaging, etc.

- The high cost of bio-PET is a deterrent to its wide acceptance in this region due to the cost-conscious nature of the consumer.

- Major manufacturers are focusing on lowering the price of bio-PET, and the success in lowering the prices massively affects the market shift toward bio-PET.

- In Asia-Pacific, the demand for packaged food is growing, owing to lifestyle changes, the growing disposable income of people, the increasing number of working professionals, and the growing preference for fast food. Consumers prefer ready-to-consume foods because they require considerably less time for cooking, are fresh, and include attractive and sturdy packaging, supporting the demand for the market studied.

- China is the world's largest packaging consumer globally owing to factors such as growing per capita income and rising e-commerce giants in the country. Due to the steady growth of its FMCG and packaging industries, China accounts for the highest market share in the Asia-Pacific region.

- Furthermore, the Chinese packaging industry grew rapidly and consistently in recent years, owing to the expanding economy and rising middle class with greater purchasing power. Food packaging is a major player in the packaging industry, accounting for roughly 60% of the total market share in China. According to Interpak, in China, total packaging in the foodstuff packaging category is expected to reach 447 billion units in 2023, indicating an increased demand for the studied market from the packaging industry.

- India's packaging industry is the fifth-largest in the world, growing at about 22-25% per year, as per the Plastics Industry Association of India. Packaging and processing food costs can be 40% lower than in Europe because of highly skilled labor and cheap labor costs. The growing population and increasing demand for packaging are expected to drive the market.

- According to the Packaging Industry Association of India (PIAI), the Indian packaging industry is expected to grow at 22% during the forecast period. Moreover, the Indian packaging market is expected to reach USD 204.81 billion by 2025, registering a CAGR of 26.7% between 2020 and 2025. Therefore, the Bio-PET market is expected to grow in the region.

- Hence, for the reasons above, Asia-Pacific will likely dominate the Bio-PET Market during the forecast period.

Competitive Landscape

The Bio-PET Market is partially consolidated. The majority of the market share is divided among a few players. Some of the key players in the bio-PET market include THE COCA-COLA COMPANY., Indorama Ventures Public Company Limited., Toyota Tsusho Corporation, TEIJIN LIMITED, and TORAY INDUSTRIES INC., among others (not in any particular order).

Bio-PET Industry Leaders

THE COCA-COLA COMPANY

Indorama Ventures Public Company Limited

Toyota Tsusho Corporation

TORAY INDUSTRIES INC.

TEIJIN LIMITED

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2022: Indorama Venturas announced the acquisition of UCY Polymers CZ s.r.o. (UCY) which is a Czech Republic-based PET plastic recycler.

Global Bio-PET Market Report Scope

Polyethylene terephthalate (PET) is a polymer used for different applications such as packaging, textiles, bottles, etc. The PET derived from natural compounds is called bio PET.

The Bio-PET Market report includes segmentation by application and geography. The market is segmented by application into bottles, packaging, consumer durables, furniture, films, and other applications. The report also covers the market size and forecasts for the bio PET market in 15 countries across major regions. The market sizing and forecasts for each segment are based on volume (Kilotons).

Application

| Bottles |

| Packaging |

| Consumer Durables |

| Furniture |

| Films |

| Other Applications |

Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Rest of the Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| Application | Bottles | |

| Packaging | ||

| Consumer Durables | ||

| Furniture | ||

| Films | ||

| Other Applications | ||

| Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Rest of the Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How big is the Bio-PET Market?

The Bio-PET Market size is expected to reach 65.19 kilotons in 2025 and grow at a CAGR of 4.18% to reach 80.00 kilotons by 2030.

What is the current Bio-PET Market size?

In 2025, the Bio-PET Market size is expected to reach 65.19 kilotons.

Who are the key players in Bio-PET Market?

THE COCA-COLA COMPANY, Indorama Ventures Public Company Limited, Toyota Tsusho Corporation, TORAY INDUSTRIES INC. and TEIJIN LIMITED are the major companies operating in the Bio-PET Market.

Which is the fastest growing region in Bio-PET Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Bio-PET Market?

In 2025, the Asia Pacific accounts for the largest market share in Bio-PET Market.

What years does this Bio-PET Market cover, and what was the market size in 2024?

In 2024, the Bio-PET Market size was estimated at 62.47 kilotons. The report covers the Bio-PET Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Bio-PET Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: