Bio-based Polypropylene Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

| Market Volume (2025) | 41.43 kilotons |

| Market Volume (2030) | 104.59 kilotons |

| Growth Rate (2025 - 2030) | 20.35% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bio-based Polypropylene Market Analysis by Mordor Intelligence

The bio-based polypropylene market is measured at 41.43 kilotons in 2025 and is forecast to reach 104.59 kilotons by 2030, advancing at a 20.35% CAGR during 2025-2030. Demand is expanding as consumer-facing industries translate net-zero promises into concrete material substitutions and as brand owners take advantage of drop-in processing compatibility to accelerate time-to-market for low-carbon products. Injection molding remains the fulcrum of volume growth because it combines geometric freedom with tight dimensional control, enabling automotive, appliance, and consumer goods producers to switch to low-footprint resins without retooling. Feedstock diversification, especially the commercialization of cellulosic biomass pathways, is narrowing cost differentials with fossil-based polypropylene, while mass-balance certification is unlocking capacity expansion by allowing producers to co-process bio-attributed and conventional propylene in existing assets. Headwinds stem from the 85-90% price premium over petro-derived polypropylene, tempered only when rising carbon-pricing schemes amplify the implicit cost of conventional plastics.

Key Report Takeaways

- By feedstock, sugarcane contributed 61% share of the bio-based polypropylene market size in 2024, whereas cellulosic biomass is set to expand at 24.63% CAGR between 2025-2030.

- By product type, homopolymer commanded 57% share in 2024, yet impact copolymer is poised for 23.22% CAGR growth through 2030.

- By application, injection molding held 65% of the bio-based polypropylene market share in 2024 and is forecast to grow at 22.01% CAGR through 2030.

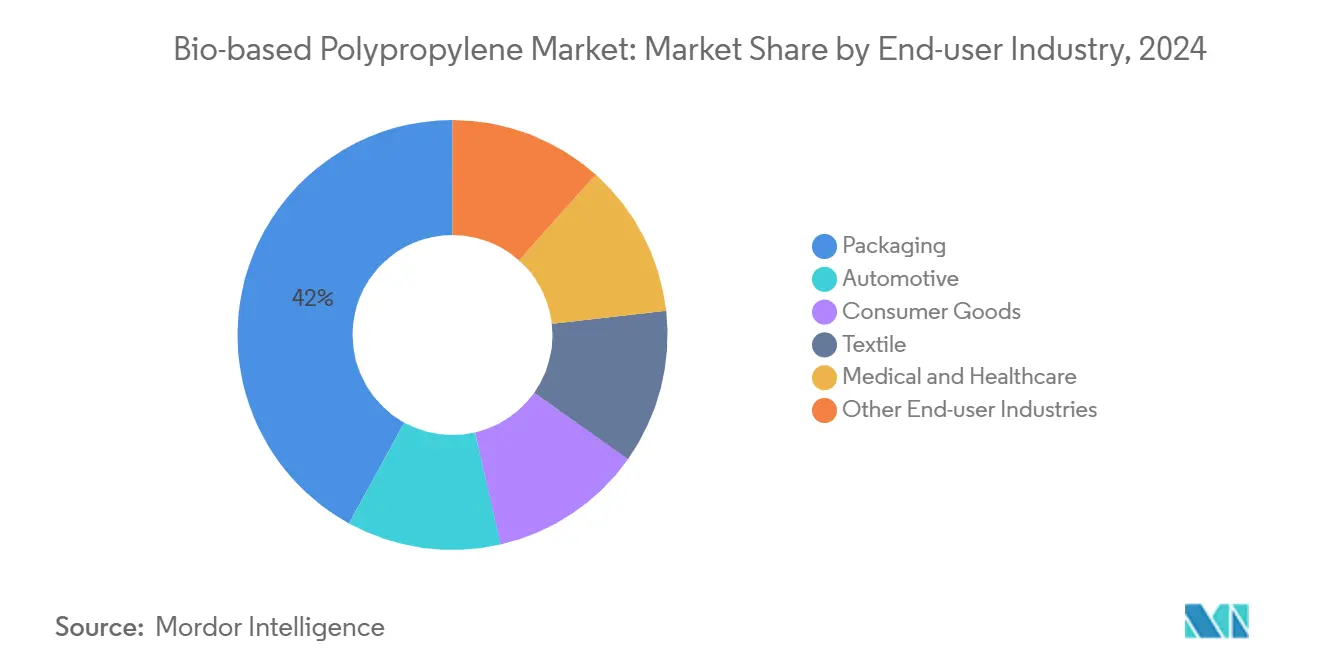

- By end-user industry, packaging accounted for 42% revenue share in 2024, while automotive is projected to advance at 23.05% CAGR to 2030.

- By geography, Asia-Pacific led with 41% market share in 2024 and is expected to post the fastest regional CAGR of 24.56% during 2025-2030.

Global Bio-based Polypropylene Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU packaging laws | +5.2% | Europe, export markets | Medium term (2-4 years) |

| Automotive lightweighting targets | +4.8% | Global, Europe, and North America focus | Medium term (2-4 years) |

| FMCG net-zero packaging commitments | +3.5% | Global, led by Europe and North America | Medium term (2-4 years) |

| Sustainable textile momentum | +2.9% | Global, early adoption in Europe | Medium term (2-4 years) |

| Compostable filaments in medical prototyping | +1.2% | North America and Europe | Long term (≥4 years) |

Source: Mordor Intelligence

European Union’s Packaging Laws Drive Bio-based Polypropylene Adoption

The 2025 introduction of the Packaging and Packaging Waste Regulation forces every packaging format sold in the bloc to be recyclable by 2030, with staged recycled-content thresholds that begin affecting procurement plans immediately. Brand owners see bio-based polypropylene as a straight drop-in that ensures compliance because the polymer retains the same recycling code as its fossil-based counterpart while cutting cradle-to-gate carbon intensity. Multinational consumer-goods players have already instructed converting partners to earmark volumes of bio-attributed PP, and converters are retrofitting lines for mono-material designs compatible with mechanical recycling. Packaging groups exporting into the EU are mirroring these moves to avoid trade frictions, creating a global reverberation that stimulates demand across Asia-Pacific and the Americas[1]Hazel O'Keeffe, “The New EU Packaging and Packaging Waste Regulation – Highlights and Challenges Ahead,” PackagingLaw.com, packaginglaw.com.

Automotive OEM Lightweighting Targets Drive Bio-based Polypropylene Demand

Vehicle programs entering series production in 2026-2028 incorporate material budgets explicitly tied to gram-per-kilometer CO₂ savings. Bio-based polypropylene compounds reinforced with kenaf or sisal fibers help designers deliver up to 20% mass reduction while preserving impact strength, providing an offset that would otherwise require expensive aluminum or magnesium substitutions. Lifecycle assessments demonstrate further gains because bio-PP stores biogenic carbon, allowing automakers to publicize sustainable content without sacrificing throughput or part complexity. Accessibility through existing molding presses lowers capital hurdles and accelerates platform-wide roll-out, particularly for dashboards, door cards, and seat backs.

Net-zero Packaging Commitments Influence Flexible Bio-based Polypropylene Film Demand

Leading fast-moving consumer goods companies with 2040 net-zero pledges translate Scope 3 obligations into revamped packaging scorecards that value renewable carbon and mass-balance attribution. Film extruders, therefore, contract certified bio-attributed feedstock to satisfy buyers’ carbon accounting rules without relinquishing optics, sealability, or barrier performance. Because the mass-balance chain of custody lets producers blend bio- and fossil-derived propylene in the same crackers, asset utilization stays high and incremental costs decline as volumes scale. These attributes explain the recent wave of purchase agreements locking in a multi-year supply of bio-PP film grades for snack-food and personal-care brands.

Growing Emphasis on Sustainable Textiles Drives Bio-based Polypropylene Demand

Rising scrutiny of microfiber shedding, water intensity, and end-of-life disposal in the textile value chain has propelled mills and converters to look beyond recycled polyester. Bio-based polypropylene fibers offer weight savings, hydrophobicity, and a 25% lower carbon footprint relative to standard PP fibers, positioning them well in hygiene, geotextile, and carpet backings. ISCC PLUS-certified fiber streams allow apparel and flooring brands to label renewable content while utilizing conventional spun-bond or melt-blown equipment, minimizing changeover downtime. Commercial launches of negative-carbon MONO-PP yarns underscore how the material can broaden sustainability narratives across fashion, automotive upholstery, and filtration media.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost | −4.5% | Global | Short term (≤2 years) |

| Lower heat-distortion temperature | −2.8% | Global automotive | Medium term (2-4 years) |

| Lack of harmonized biomass-balance certification | −2.1% | Middle East, global supply chains | Short term (≤2 years) |

Source: Mordor Intelligence

High Production Cost Limits Bio-based Polypropylene Adoption

The most credible techno-economic studies put the manufacturing cost of bio-PP at nearly double that of petro-based grades, primarily due to smaller plant scales, feedstock processing steps, and longer campaign times. The premium constrains penetration in mass-market food packaging or commodity household goods, where pennies per kilogram decide material selection. Producers are betting on cellulosic sugar platforms, energy-integration retrofits, and carbon-credit valorization to chip away at the delta, yet most analysts expect meaningful parity only once installed capacity surpasses 1 million tons per year globally[2]Pedro Gerber Machado et al., “Bio-based Propylene Production in a Sugarcane Biorefinery,” Wiley Online Library, onlinelibrary.wiley.com.

Lower Heat-Distortion Temperature Limits Under-hood Automotive Applications

Conventional polypropylene already sits at the lower end of heat-distortion thresholds for power-train proximity, and bio-based variants often register slightly reduced crystallinity, nudging thermal limits down by several degrees Celsius. As a result, Tier-1 suppliers restrict bio-PP to interior, trunk, and fascia components, leaving higher-temperature housings to glass-filled nylons or polyphenylene sulfide. Ongoing compound development focuses on nucleating agents and fiber reinforcement to lift heat performance, but each additive step up cost, accentuating price challenges.

Segment Analysis

By Feedstock: Sugarcane Dominates While Cellulosic Biomass Accelerates

Sugarcane retains 61% feedstock share in 2024 thanks to mature fermentation infrastructure converting sucrose to ethanol and onward to bio-propylene. Geographical proximity of cane plantations to Brazilian and Thai production hubs underpins supply reliability and anchors a competitive cost base despite feedstock seasonality. The bio-based polypropylene industry now channels learnings from sugarcane process integration to other biomass routes.

Cellulosic biomass, encompassing corn stover, wheat straw, and bagasse, is the fastest riser and set to grow at 24.63% CAGR through 2030. Technological leaps in enzymatic hydrolysis and catalytic dehydration unlock carbohydrates once considered intractable, broadening the feedstock basket and dampening the risk of food-versus-fuel debates.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Homopolymer Foundations, Support Impact Copolymer Growth

Homopolymer grades contributed 57% of global volume in 2024, mainly because they run trouble-free on legacy extrusion, molding, and thermoforming lines. These grades serve mainstream applications such as beverage caps, yogurt cups, and storage bins where rigidity and clarity matter. Producers leverage well-characterized property profiles to shorten qualification cycles, a decisive advantage for converters juggling tight project timelines.

Impact copolymers are on pace to register a 23.22% CAGR between 2025-2030 as automakers and appliance makers request tougher, low-temperature-resistant parts. The bio-based polypropylene market size for impact copolymers stands to benefit from TPO bumper fascia and luggage-compartment liners, applications where ductility at −20 °C prevents brittle failure. Random copolymers bridge the gap by offering improved clarity and flexibility, nurturing adoption in squeeze bottles, medical syringes, and clear hinged-lid packs. Collectively, the diversification allows buyers to select tailored mechanical and optical attributes while staying inside the renewable-carbon envelope.

By Application: Injection Molding Sustains Versatility Across Industries

Injection molding captured 65% of the bio-based polypropylene market in 2024, owing to its suitability for complex, thin-wall parts that demand dimensional accuracy. During 2025-2030, this application is projected to widen its lead with a 22.01% CAGR as automotive interior, consumer electronics casings, and appliance housings transition to renewable resins that require no mold redesign.

Films continue to gain traction in snack-food wraps, stand-up pouches, and personal-care overwraps. Producers exploit bio-PP’s barrier parity with fossil-derived PP, enabling downgauging without compromising moisture or aroma retention. The segment benefits from the mass-balance approach, where bio-attributed feedstock is assigned to high-visibility SKUs, allowing brand owners to promote renewable content while keeping plant run rates stable.

By End-user Industry: Packaging Leads Circular Economy Transition

The packaging sector accounted for 42% of the bio-based polypropylene market share in 2024, anchored by mono-material rigid containers, lidding films, and thin-wall tubs. Multinationals are specifying renewable grades to inch closer to publicized 2030 carbon-reduction trajectories, leveraging bio-PP’s compatibility with mechanical recycling streams.

Automotive is projected to be the fastest-growing end-use, with a CAGR of 23.05%. Sector players value the resin’s capacity to achieve component mass reduction without triggering new tooling investments, a decisive factor amid tight model-cycle calendars.

Consumer goods maintain a steady pull for bio-PP in houseware, toys, and personal-care packaging, where renewable content claims resonate with eco-conscious shoppers. Textile use cases, particularly spun-bond and needle-punched nonwovens, represent an incremental yet strategic avenue because the negative-carbon potential of certain fiber variants supports brand storytelling in high-volume markets like carpet backing. Medical and healthcare demand is embryonic but influential; ISO-certified grades for diagnostic disposables and sterilizable trays signal future scalability if price points converge.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific commanded 41% of global demand in 2024 and is projected to outpace all regions with a 24.56% CAGR over 2025-2030. The region’s policy frameworks, notably Japan’s Bio-strategy Roadmap and China’s Five-Year Plan provisions for green materials, drive capital deployment into bio-attributed propylene assets. Domestic converters benefit from ready access to agricultural residues, particularly in Southeast Asia, lowering outbound logistics costs for feedstock and improving plant utilization rates.

Europe is energized by binding waste-reduction directives and sector-specific recycled-content targets. Automotive component suppliers headquartered in Germany, France, and Italy are rolling out renewable resin specifications across global subsidiaries to maintain harmonized material numbers, thereby lifting transregional demand for bio-PP compounds. \

North America shows accelerating uptake as brand owners align with Science-Based Targets initiatives and as announcements like Braskem’s evaluation of a U.S. bio-based polypropylene plant create domestic supply visibility. The Middle East and Africa hold a smaller baseline today, yet recent ISCC certifications at integrated refinery-petrochemical complexes suggest a strategic pivot toward renewable olefins to diversify revenue streams beyond crude exports.

Competitive Landscape

The bio-based polypropylene market is moderately concentrated and consists of established petrochemical incumbents, specialized biopolymer pioneers, and integrated feedstock-to-resin platforms. Strategic alliances dominate new capacity announcements because no single actor controls the entire renewable value chain. Upstream feedstock specialists secure offtake agreements with polymer producers, while converters sign multi-year supply contracts to lock in assured volumes under mass-balance certification.

Bio-based Polypropylene Industry Leaders

-

Braskem

-

SABIC

-

LyondellBasell Industries Holdings B.V.

-

Borealis GmbH

-

Mitsui Chemicals, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Braskem introduced bio-circular polypropylene WENEW derived from used cooking oil, targeting restaurant and snack-food packaging.

- September 2023: SABIC and Taghleef partnered with two Greek firms to produce mono-PP thin-wall containers using certified renewable polymers for in-mould labeling food applications.

Global Bio-based Polypropylene Market Report Scope

Bio-based polypropylene is a polymer created using natural resources such as sugarcane, maize, vegetable oil, and other biomass. These polymers are progressively replacing traditional plastics. The bio-based polypropylene market report is segmented by application and geography. The market is segmented into injection molding, textiles, films, and other applications based on application. The report also covers the market size and forecast in 11 countries across major regions. The report offers market size and forecast for bio-based polypropylene in terms of volume (Kilotons) for all the above segments.

| By Feedstock | Sugarcane | ||

| Corn | |||

| Cellulosic Biomass | |||

| Waste Cooking Oil and Used Oils | |||

| Others (Algae, Lignin, Etc.) | |||

| By Product Type | Homopolymer | ||

| Random Copolymer | |||

| Impact Copolymer | |||

| By Application | Injection Molding | ||

| Films | |||

| Textiles | |||

| Other Applications (Foams, Blow Molding, Extrusion Coating) | |||

| By End-user Industry | Packaging | ||

| Automotive | |||

| Consumer Goods | |||

| Textile | |||

| Medical and Healthcare | |||

| Other End-user Industries (Electronics, Building and Construction and Agriculture) | |||

| By Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN Countries | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle-East and Africa | |||

| Sugarcane |

| Corn |

| Cellulosic Biomass |

| Waste Cooking Oil and Used Oils |

| Others (Algae, Lignin, Etc.) |

| Homopolymer |

| Random Copolymer |

| Impact Copolymer |

| Injection Molding |

| Films |

| Textiles |

| Other Applications (Foams, Blow Molding, Extrusion Coating) |

| Packaging |

| Automotive |

| Consumer Goods |

| Textile |

| Medical and Healthcare |

| Other End-user Industries (Electronics, Building and Construction and Agriculture) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

Key Questions Answered in the Report

What is the current size of the bio-based polypropylene market?

The bio-based polypropylene market stands at 41.43 kilotons in 2025 and is projected to grow rapidly through 2030.

Which application dominates demand for bio-based polypropylene?

Injection molding commands 65% of demand in 2024 because its processing flexibility allows quick substitution without tooling changes.

Why is Asia-Pacific the leading regional market?

Asia-Pacific benefits from abundant agricultural residues, government bioeconomy initiatives, and accelerated investment in renewable propylene capacity, giving it 41% share in 2024.

How much more expensive is bio-based polypropylene than conventional polypropylene?

Production cost analyses indicate an 85-90% premium, driven by smaller scale plants and more complex conversion steps.

Which end-use industry is forecast to grow fastest?

Automotive applications are expected to expand at a 23.05% CAGR between 2025-2030 as OEMs pursue weight reduction and sustainability targets.