Size and Share of Big Data Analytics Market In Energy Sector

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 10.62 Billion |

| Market Size (2030) | USD 17.95 Billion |

| Growth Rate (2025 - 2030) | 11.07% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Big Data Analytics Market In Energy Sector by Mordor Intelligence

The big data analytics market in energy sector stood at USD 10.62 billion in 2025 and is forecast to reach USD 17.95 billion by 2030, advancing at an 11.07% CAGR. The growth reflects a decisive pivot from reactive operations toward predictive intelligence as utilities and energy firms harness smart-grid, IoT, and distributed-asset data to optimize performance and curb cost. Falling cloud-computing prices, surging data volumes from advanced metering infrastructure, and regulatory requirements for grid monitoring together create a compelling business case. Vendors are increasingly bundling data-management platforms with domain-specific analytics, enabling customers to address grid reliability, renewable integration, and trading strategies with a single integrated stack. Emerging revenue streams from peer-to-peer trading, dynamic pricing, and demand response add further momentum as companies monetize analytical insights rather than focus solely on internal efficiency.

Key Report Takeaways

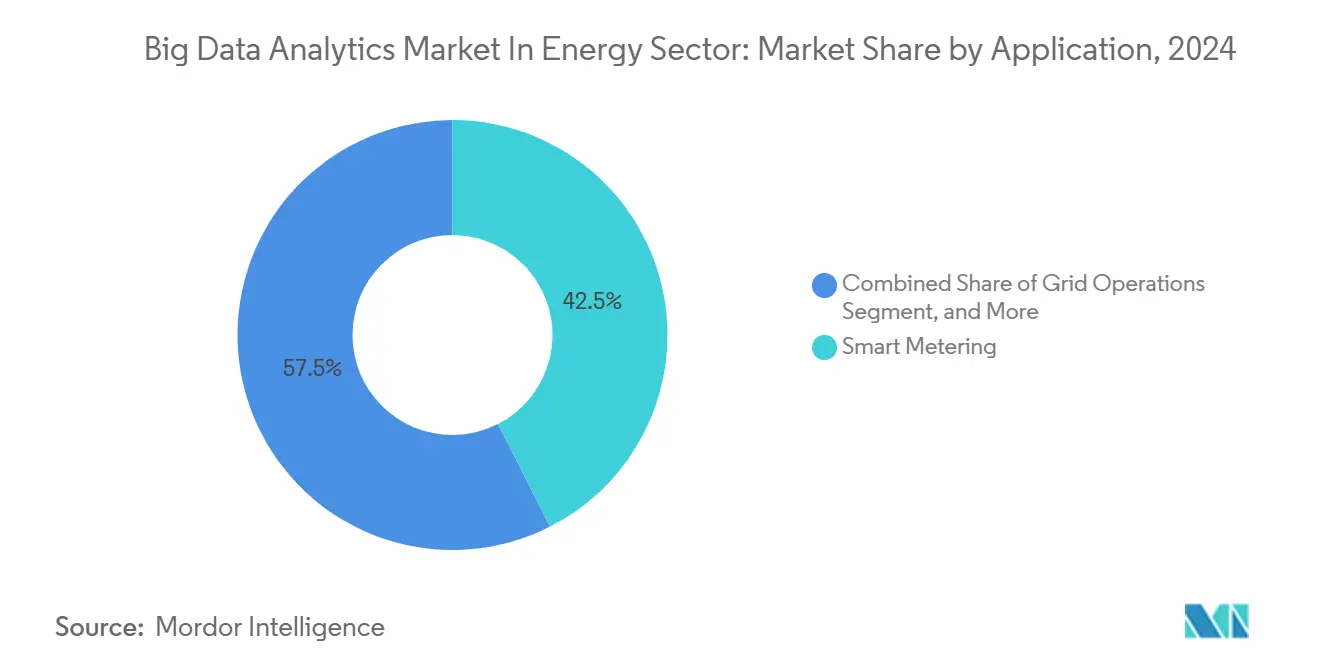

- By application, smart metering held a 42.5% share of the big data analytics market in energy sector in 2024, while predictive maintenance and asset performance management is projected to post a 28.7% CAGR through 2030.

- By component, software commanded a 61% share of the big data analytics market in the energy sector in 2024; services are poised for a 27.5% CAGR through 2030.

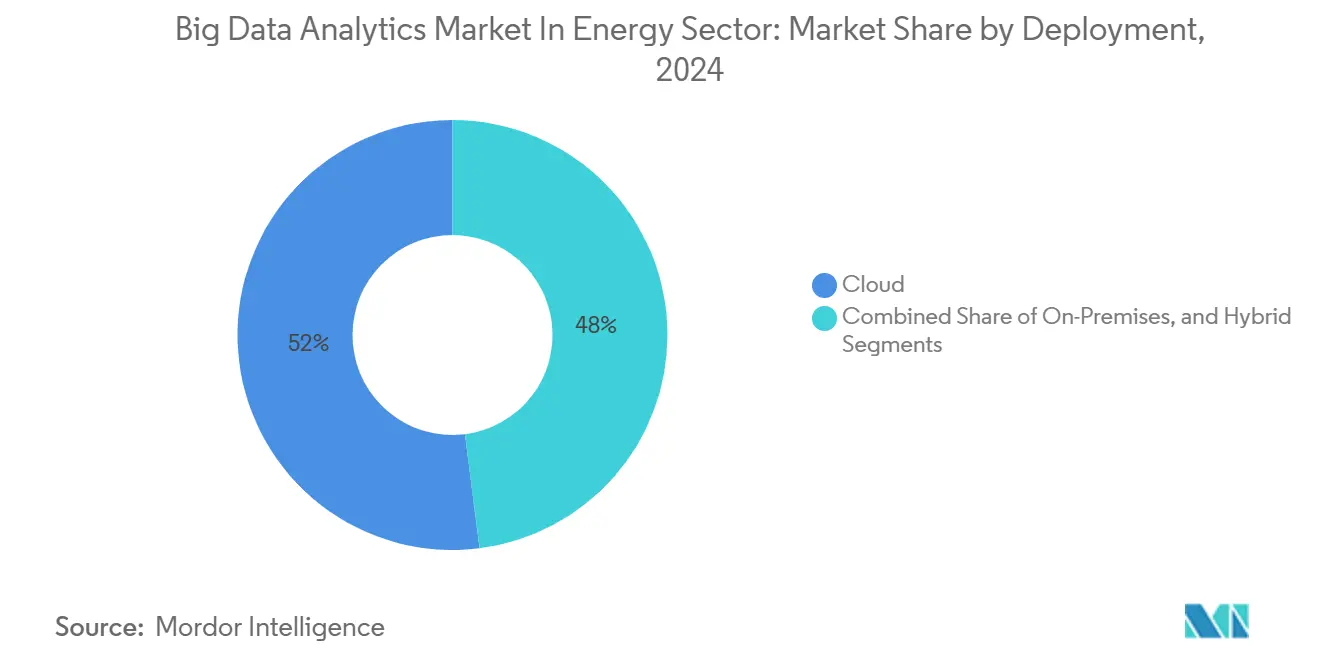

- By deployment, cloud models captured a 52% share of the big data analytics market in the energy sector in 2024 and are set to expand at a 28.13% CAGR through 2030.

- By end user, power utilities led the big data analytics market in the energy sector with a 43% share in 2024, whereas midstream and refining operators represented the fastest-growing segment, expanding at a 24% CAGR through 2030.

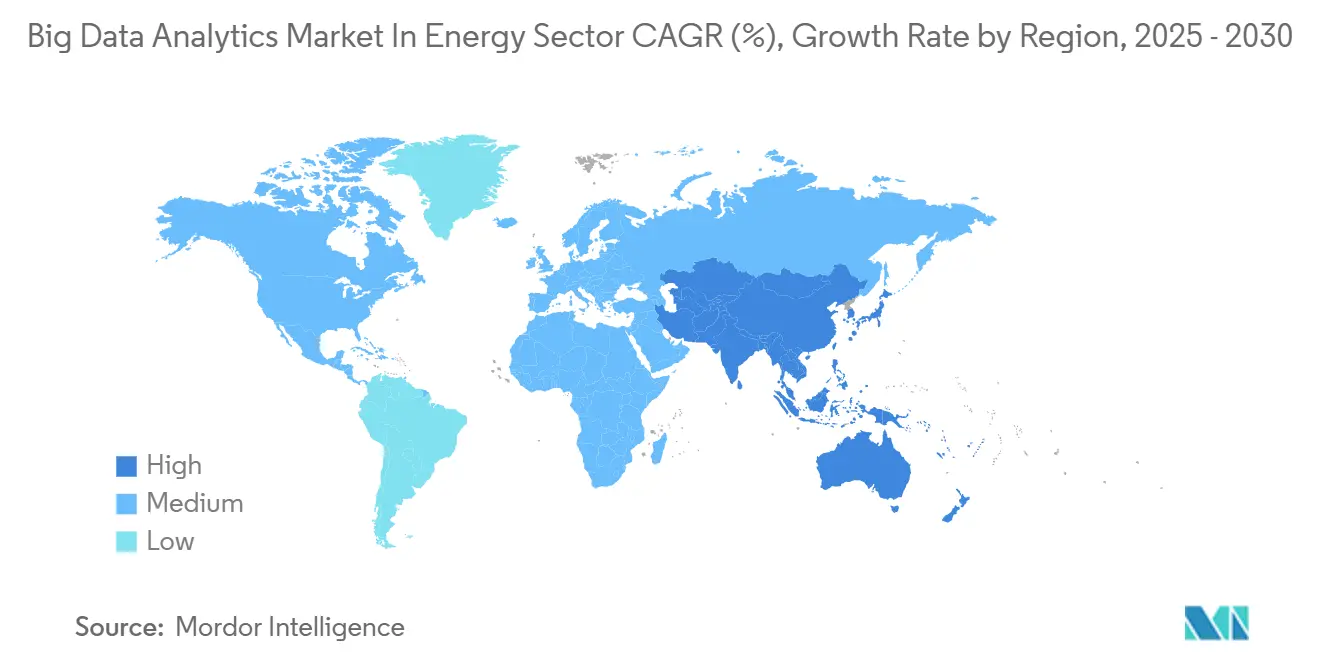

- By geography, North America accounted for a 35% share of the big data analytics market in energy sector in 2024; the Asia-Pacific region is forecast to accelerate at a 27.4% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Insights and Trends of Big Data Analytics Market In Energy Sector

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exponential smart-grid and IoT data growth | +2.8% | Global, with early gains in North America and Europe | Medium term (2-4 years) |

| Asset-performance optimization pressure | +2.1% | Global, concentrated in Asia-Pacific and North America | Short term (≤ 2 years) |

| Renewable-integration complexity | +1.9% | Global, spill-over from EU to Asia-Pacific | Long term (≥ 4 years) |

| Post-pandemic digital-transformation spend | +1.6% | North America and EU core, expansion to MEA | Medium term (2-4 years) |

| Peer-to-peer energy trading analytics need | +1.3% | EU and Australia leading, Asia-Pacific following | Long term (≥ 4 years) |

| Falling cloud and edge analytics costs | +1.2% | Global, with cost advantages in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Exponential Smart-Grid and IoT Data Growth

Utilities now process terabytes of grid telemetry every day, a drastic leap from the megabytes handled by legacy SCADA systems. Granular 15-minute interval data from smart meters exposes demand anomalies in near real time, letting operators fine-tune load allocation. Oracle’s March 2025 enhancements to its Advanced Distribution Management System illustrate how 7-day hourly forecasting supports companies such as Austin Energy and Tata Power in orchestrating distributed resources more effectively. IoT sensors across transmission lines yield feedback loops for predictive maintenance that have cut unplanned outages by up to 25% in recent deployments.[1]GE Vernova, “Benefits of Utilities Analytics and Automation Software for Energy Savings and Efficiency,” gevernova.com Mandatory frameworks such as NERC CIP reinforce adoption by requiring continuous grid-data surveillance across North American utilities.

Asset-Performance Optimization Pressure

Aging infrastructure meets volatile, renewable-driven demand, forcing operators to squeeze more output from legacy assets. Predictive maintenance lets firms shift from time-based to condition-based schedules, generating double-digit energy savings in year one, according to GE Vernova case studies. Unplanned downtime can exceed USD 1 million per hour for critical generation assets, so analytics rapidly pay for themselves. Schneider Electric’s work with Glencore shows how digital twins reduce CO₂ intensity in mining while maximizing throughput. Oil and gas majors such as ExxonMobil apply similar models to drilling, leak detection, and seismic imaging, extending optimization principles across the energy value chain.

Renewable-Integration Complexity

Variable wind and solar output demand high-resolution forecasting that legacy grid-management tools cannot supply. Cloud analytics blends weather, historical generation, and real-time sensor data to dispatch storage and demand response efficiently. Microsoft’s Azure partnerships provide utilities with scalable compute for multi-terabyte weather datasets that sharpen production forecasts. As rooftop PV, batteries, and electric-vehicle chargers introduce bidirectional flows, analytics must orchestrate thousands of distributed endpoints to maintain frequency and voltage. Compliance regimes in Europe and California push operators to verify renewable-portfolio targets through data-driven reporting, sustaining investment in advanced forecasting engines.

Post-Pandemic Digital-Transformation Spend

COVID-19 cemented the value of remote monitoring and automated decision support across energy facilities. Infosys research shows generative-AI outlays in energy, mining, and utilities doubling to more than USD 1 billion between 2023 and 2024.[2]Infosys Knowledge Institute, “Energy Industry Outlook 2024,” infosys.com Hybrid-cloud architectures now underpin redundant analytics stacks that sustain operations during disruptions. Supply-chain shocks exposed the need for granular vendor-risk analytics, driving uptake of demand-planning modules. Customer-engagement portals enriched with data-science models help utilities enroll households in demand-response and distributed-generation programs, extending transformation beyond plant walls.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Domain-specific data-science talent gap | -1.8% | Global, acute in Asia Pacific and MEA | Long term (≥ 4 years) |

| OT/IT cyber-security and privacy risks | -1.4% | Global, regulatory focus in North America and EU | Medium term (2-4 years) |

| Legacy systems and data silos | -1.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| High upfront analytics CAPEX in emerging regions | -0.9% | MEA and Latin America core, spill-over to Asia-pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Domain-Specific Data-Science Talent Gap

Energy analytics requires skill sets that straddle power-system engineering and data science, a combination scarce in today’s labor market. Universities seldom teach load-flow modeling or thermodynamic optimization alongside machine-learning theory, so graduates need lengthy on-the-job training. Consulting rates for such hybrid specialists remain elevated, stretching project timelines and budgets. The shortage is acute in fast-growing regions such as Asia-Pacific, where infrastructure build-outs outpace workforce development. Utilities are teaming with academic programs and launching internal boot camps, yet near-term supply still lags demand.

OT/IT Cyber-Security and Privacy Risks

Blending operational-technology feeds with enterprise IT expands the attack surface across energy networks. NERC CIP rules force North American operators to isolate critical-asset traffic or adopt expensive monitoring stacks. European GDPR constraints limit the use of high-granularity consumption data unless utilities obtain explicit consent, stalling some customer analytics pilots. Real-time analytics that straddle OT and IT domains create potential pathways for threat actors to reach grid-control layers, prompting conservative rollouts. Vendors now bundle zero-trust architectures and encrypted data-exchange frameworks, but security concerns still temper adoption speed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Smart Metering Drives Current Revenue

Smart Metering claimed 42.5% share of the Big Data Analytics Market in Energy Sector in 2024 as regulators in North America and Europe mandated advanced metering roll-outs. Utilities rely on the segment to collect 15-minute interval data, enabling theft detection, outage management, and time-of-use pricing. Grid operations and demand-response modules then reuse the data lake, amplifying return on infrastructure spending. Predictive Maintenance and Asset Performance Management is set to log a 28.7% CAGR through 2030, propelled by the need to cut downtime in aging thermal plants and renewables alike. Oracle’s 2025 ADMS update integrates distributed-resource models, showing how platforms bundle multiple applications under one interface. As cloud capacity expands, even smaller cooperatives can run AI models that once required enterprise budgets, widening the addressable base for application vendors.

The Big Data Analytics Market in Energy Sector benefits from utility appetite for multi-tenant subscription pricing that aligns cost with meter count. Energy-trading desks now tap grid-data feeds to drive algorithmic bids in hourly markets, extending analytical reach beyond operations. Customer-engagement platforms leverage smart-meter insights to recommend energy-efficiency retrofits, spawning ancillary service revenue. Over the forecast horizon, regulators plan sharper price-signal granularity, which will raise data density and further entrench analytics across metering-led workflows. As peer-to-peer trading pilots gain traction in Europe and Australia, application vendors will embed digital-ledger functions into existing analytics suites to track transaction provenance.

By Component: Software Dominance Faces Services Challenge

Software retained a 61% share of the Big Data Analytics Market in the Energy Sector in 2024, a testament to the platform-centric procurement model that utilities historically prefer. The feature breadth from ingestion and cleansing to model orchestration and visualization makes integrated suites attractive relative to point solutions. Yet the Services category will accelerate at a 27.5% CAGR through 2030, signaling a pivot toward outcome-based engagements. Schneider Electric’s Private Equity and Financial Services practice illustrates how consultancy plus toolset delivers measurable decarbonization returns for asset managers.[3]Schneider Electric, “Schneider Electric Expands Global Private Equity and Financial Services Practice,” perspectives.se.com Utilities increasingly outsource data-science and model-maintenance tasks, freeing resources for grid-modernization strategy. Managed analytics contracts tie vendor compensation to performance metrics such as loss-factor reduction, pushing suppliers to absorb technology risk. Vendors able to blend domain expertise with AI toolchains will outpace pure-software rivals. As regulatory reporting grows complex, auditability requirements favor service providers who maintain end-to-end data lineage. The interplay of software modularity and service customization thus shapes competitive moats over the outlook period.

By Deployment: Cloud Accelerates Despite Security Concerns

Cloud accounted for a 52% share of the Big Data Analytics Market in the Energy Sector in 2024 and will post the fastest 28.13% CAGR through 2030. The allure is clear: elastic compute handles surging data volumes without heavy capital outlay. Microsoft Azure and Oracle Cloud now offer utility-grade security blueprints, easing fears around critical infrastructure exposure. Hybrid models notch momentum as operators split workloads between on-premise OT environments and public-cloud AI processing, balancing latency, sovereignty, and cost.

On-premise installations persist for transmission control centers that require deterministic response and air-gap assurances. Edge analytics nodes complement both models, preprocessing high-frequency sensor data locally to cut bandwidth bills. Over time, standardized API gateways will let utilities shift workloads fluidly across environments, diminishing the binary cloud versus on-premise debate. Vendors investing in encryption and zero-trust frameworks will capture share as security assurances rise to procurement table stakes.

By End-User: Utilities Lead While Midstream Accelerates

Power Utilities held a 43% share of the Big Data Analytics Market in the Energy Sector in 2024 because smart-grid mandates and outage-management imperatives made analytics indispensable. Investments span load-forecasting, voltage-optimization, and customer-experience dashboards. Midstream and Refining Operators, however, are slated for a 24% CAGR as energy-price volatility and emissions regulations drive demand for supply-chain transparency. The Williams Companies’ Oracle Cloud ERP adoption shows how pipeline firms leverage unified datasets to standardize workflows and feed real-time dashboards.

Exploration and production entities deploy subsurface analytics to maximize recovery rates while managing methane leakage. Renewable-energy developers depend on high-precision weather and performance models to attain target capacity factors and secure financing. Energy-service companies use analytics to guarantee outcomes under energy-as-a-service contracts, reinforcing demand for continuous monitoring. As carbon accounting becomes mandatory, each end-user group will integrate sustainability metrics into operational dashboards, broadening analytical footprints.

Geography Analysis

North America captured a 35% share of the Big Data Analytics Market in Energy Sector in 2024 on the back of NERC CIP rules that require granular grid-monitoring and established utility procurement processes. Early adoption of advanced metering, competitive retail markets, and a mature vendor ecosystem support sustained analytics budgets. Canadian cross-border trade further elevates the need for predictive congestion management tools. Federal incentives for renewable integration plus state-level decarbonization targets will keep data volumes rising, cementing analytics as a core utility competency.

Asia-Pacific is the fastest-growing region with a 27.4% CAGR through 2030, driven by multibillion-dollar grid-modernization and renewable-expansion programs in China and India. China’s state-grid deployment of AI-enabled fault-location sensors reduces outage duration and showcases the scale benefit of data-driven operations. India’s smart-city and solar-park initiatives feed terabytes of telemetry into nascent cloud platforms, catalyzing vendor partnerships. Japan and South Korea pursue energy-efficiency mandates that depend on IoT sensor integration, while Australia’s market reforms elevate algorithmic trading use cases.

Europe maintains steady growth as utilities comply with renewable-portfolio and carbon-reduction mandates that require high-resolution forecasting and optimization. Peer-to-peer energy-trading pilots in Germany and the Netherlands spur analytics for settlement and provenance tracking. The Middle East and Africa offer emerging potential where oil-exporting economies diversify generation mixes and introduce smart-grid pilots. Though capital and talent constraints restrain uptake, targeted government programs and international partnerships hint at future acceleration.

Competitive Landscape

The Big Data Analytics Market in the Energy Sector is moderately fragmented. Enterprise software titans such as IBM, SAP, Microsoft, and Oracle leverage horizontal data platforms while tailoring modules for utility workflows. Operational-technology specialists Schneider Electric, Siemens, and GE Vernova bridge plant-level sensors with cloud analytics, creating defensible positions rooted in equipment domain know-how. Vertical integration is accelerating as vendors acquire niche AI startups to fold forecasting, anomaly detection, or cybersecurity functions into core suites; Oracle's Energy and Water Data Exchange highlights this end-to-end ambition.

Competitive edge now hinges on outcome-based service models and regulatory literacy rather than raw technology. Utilities favor vendors capable of guaranteeing loss-factor reductions or renewable-forecast accuracy, shifting risk from the buyer to the supplier. Cybersecurity credentials are a second pillar: providers embed zero-trust architectures and real-time threat analytics to calm infrastructure-protection worries. Emerging challengers such as C3.ai and Palantir pre-package use cases like transformer-failure prediction, gaining quick wins in pilot projects, while incumbents counter with broad product portfolios and deep channel relationships.

Market consolidation is likely as scale economies in data-ingestion pipelines, AI-model libraries, and compliance tooling reward larger players. Still, white-space remains in edge analytics for microgrids, AI co-pilots for control-room operators, and tokenized energy-trading platforms. Partnerships among cloud hyperscalers, equipment OEMs, and regional integrators will shape go-to-market dynamics, making ecosystem orchestration a key differentiator through 2030.

Leaders of Big Data Analytics Market In Energy Sector

International Business Machines Corporation

SAP SE

Microsoft Corporation

Siemens Aktiengesellschaft

Accenture plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Schneider Electric, ETAP, and NVIDIA introduced a digital-twin solution that simulates AI-factory power needs from grid to chip level using NVIDIA Omniverse, letting utilities model dynamic data-center loads that can exceed traditional rack ratings by 165%.

- March 2025: Oracle launched Energy and Water Data Exchange, a cloud platform that harmonizes utility and third-party data using IEEE and IEC standards to accelerate AI projects.

- March 2025: Oracle added 7-day hourly forecasting and expanded battery models to its Advanced Distribution Management System, now serving 61 million customer endpoints across six top U.S. utilities.

- May 2024: Oracle introduced grid-modernization solutions that blend real-time analytics with cloud platforms to manage demand volatility.

Scope of Report on Big Data Analytics Market In Energy Sector

The Big Data Analytics Market In Energy Sector Report is Segmented by Application (Grid Operations, Smart Metering, Asset and Workforce Management, Predictive Maintenance and APM, Demand Response and Load Forecasting, Energy Trading and Risk Management), Component (Software, and Services), Deployment Model (On-Premise, Cloud, and Hybrid), End-User (Power Utilities, Oil Exploration and Production, Midstream and Refining Operators, Renewable Energy Developers, Energy Service Companies (ESCOs), Other End-Users), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Grid Operations |

| Smart Metering |

| Asset and Workforce Management |

| Predictive Maintenance and APM |

| Demand Response and Load Forecasting |

| Energy Trading and Risk Management |

| Software |

| Services |

| On-Premise |

| Cloud |

| Hybrid |

| Power Utilities |

| Oil Exploration and Production |

| Midstream and Refining Operators |

| Renewable Energy Developers |

| Energy Service Companies (ESCOs) |

| Other End-Users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Application | Grid Operations | ||

| Smart Metering | |||

| Asset and Workforce Management | |||

| Predictive Maintenance and APM | |||

| Demand Response and Load Forecasting | |||

| Energy Trading and Risk Management | |||

| By Component | Software | ||

| Services | |||

| By Deployment Model | On-Premise | ||

| Cloud | |||

| Hybrid | |||

| By End-User | Power Utilities | ||

| Oil Exploration and Production | |||

| Midstream and Refining Operators | |||

| Renewable Energy Developers | |||

| Energy Service Companies (ESCOs) | |||

| Other End-Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and growth outlook for Big Data analytics market in the energy space?

The Big Data Analytics Market in Energy Sector is valued at USD 10.62 billion in 2025 and is set to reach USD 17.95 billion by 2030, reflecting an 11.07% CAGR.

Which application generates the most revenue for energy analytics vendors?

Smart Metering dominates with 42.5% market share in 2024 as utilities roll out advanced meters under regulatory mandates.

Which deployment model is expanding fastest among energy companies?

Cloud deployments are growing at a 28.13% CAGR because scalable compute absorbs surging smart-grid and IoT data without heavy capital spends.

Which region will add the most incremental analytics spending by 2030?

Asia-Pacific is projected to lead incremental growth at a 27.4% CAGR, fueled by large-scale grid-modernization projects in China and India.

What is the leading restraint on wider analytics adoption in energy?

A shortage of data scientists versed in both analytics and energy-system engineering slows project timelines and raises implementation costs.

How fragmented is competition among analytics providers to utilities?

The market is moderately fragmented; the top five vendors hold roughly 45% combined share, so no single player exercises dominant control.

Page last updated on: