Market Overview

| Study Period | 2020 - 2031 |

|---|---|

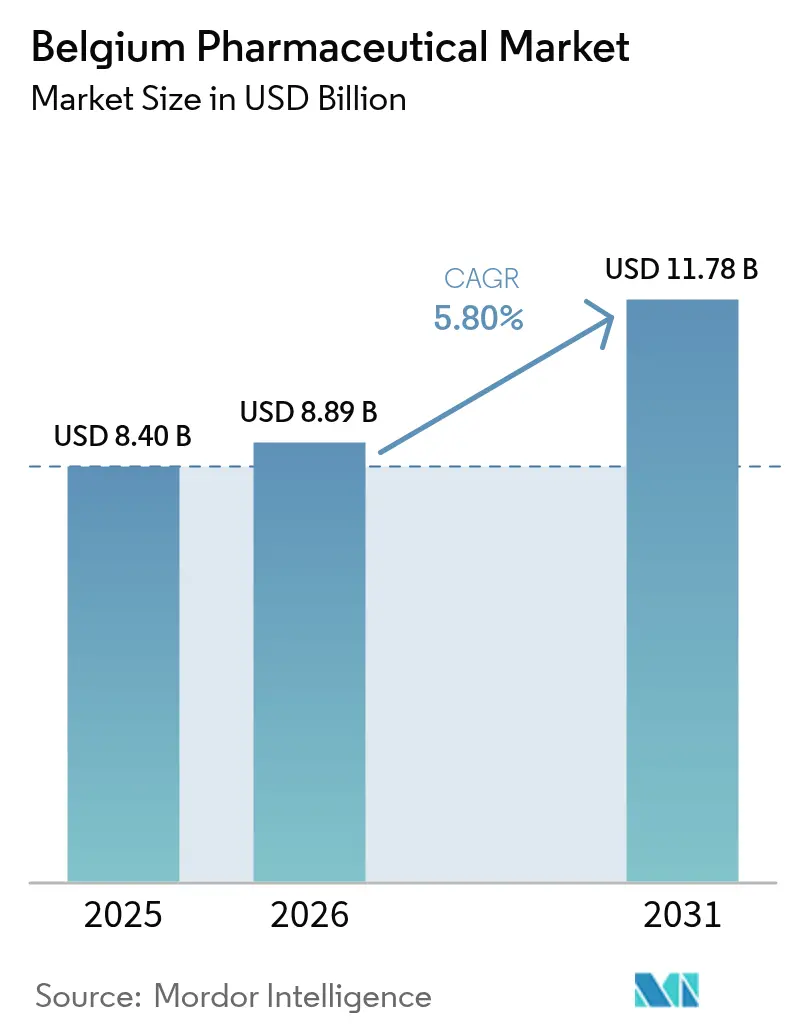

| Base Year Market Size (2025) | USD 8.40 Billion |

| Market Size (2026) | USD 8.89 Billion |

| Market Size (2031) | USD 11.78 Billion |

| Growth Rate (2026 - 2031) | 5.80% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Belgium Pharmaceutical Market Analysis by Mordor Intelligence

The Belgium Pharmaceutical Market size is expected to grow from USD 8.40 billion in 2025 to USD 8.89 billion in 2026 and is forecast to reach USD 11.78 billion by 2031 at 5.80% CAGR over 2026-2031.

Belgium’s export-led orientation, its EUR 79 billion shipment value in 2024, and R&D outlays equal to 19.3% of total EU pharmaceutical research collectively anchor a steady demand outlook. High per-capita health expenditure, a 100% national eHealth score, and policy support for fast-track reimbursement programs continue to lower barriers to access for breakthrough therapies. Mandatory post-exclusivity price cuts curb unit values but encourage large volumes by ensuring affordability, while manufacturer rebates under Managed Entry Agreements shift part of the budget burden away from public payers. Multinational subsidiaries dominate specialty segments yet growing online pharmacy penetration and a visible pipeline of biologics and advanced therapies signal widening opportunities for newer entrants.

Key Report Takeaways

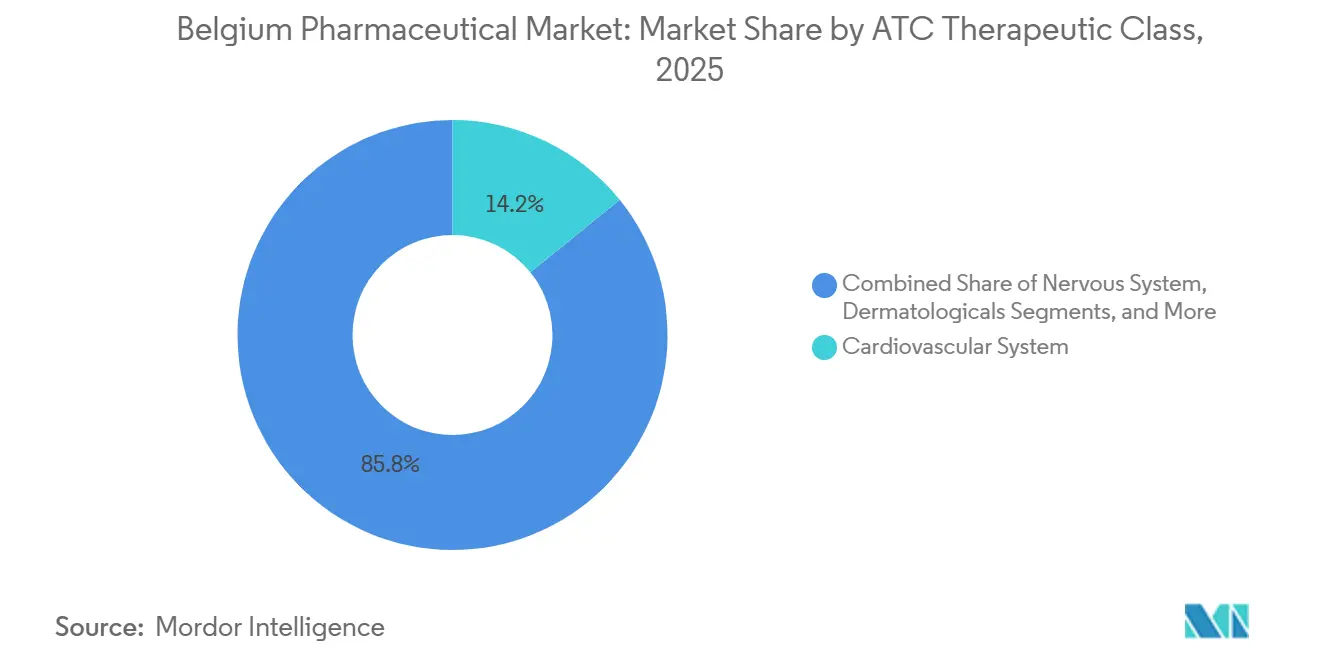

- By therapeutic class, the cardiovascular system segment held 14.18% of the Belgium pharmaceutical market share in 2025, while dermatologicals are projected to expand at a 7.54% CAGR through 2031.

- By drug type, prescription medicines accounted for 86.85% of the Belgium pharmaceutical market size in 2025; the over-the-counter category records the fastest 7.21% CAGR to 2031.

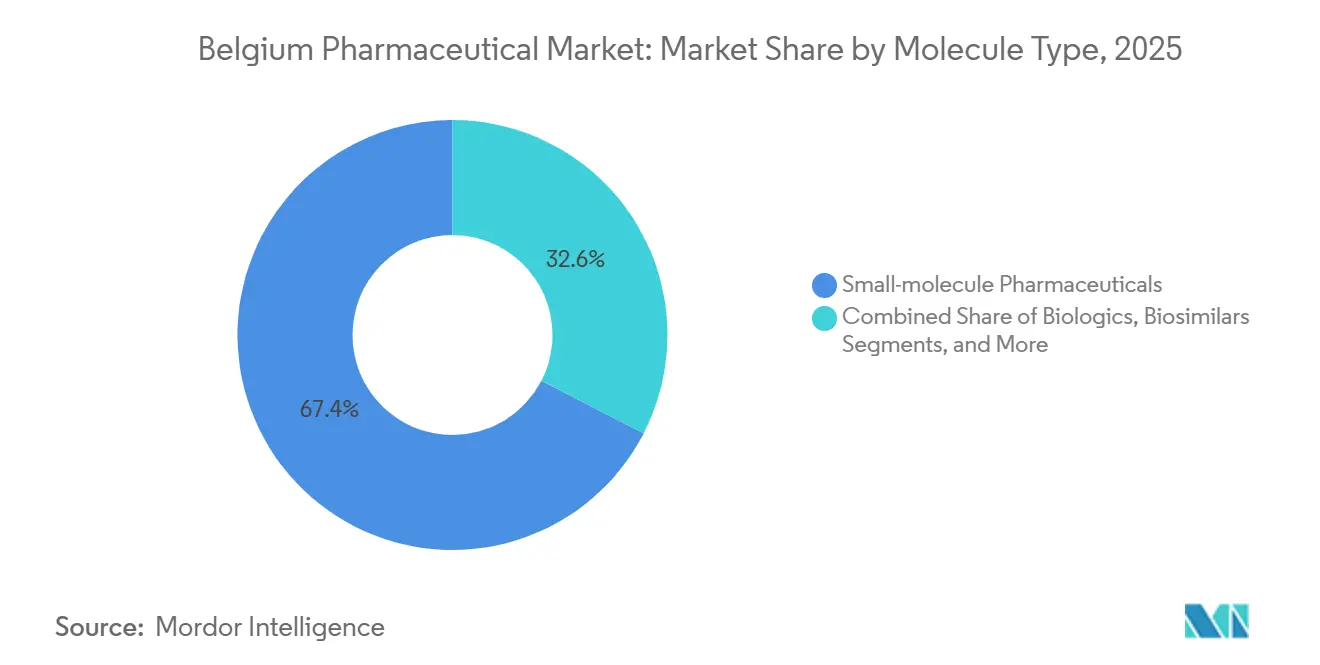

- By molecule type, small molecules represented 67.43% of the Belgium pharmaceutical market size in 2025, whereas biologics post the highest 6.78% CAGR between 2026-2031.

- By distribution channel, hospital pharmacies captured 45.73% of 2025 revenue, and online pharmacies are set to rise at a 7.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Belgium Pharmaceutical Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Health Expenditure Per Capita | +1.2% | National, concentrated in Brussels-Capital, Flemish and Walloon Brabant | Medium term (2-4 years) |

| High Burden of Chronic Diseases | +1.5% | National, aging clusters across Flanders and Wallonia | Long term (≥ 4 years) |

| Robust Biopharma Export Infrastructure | +1.0% | National, export hubs in Antwerp and Brussels Airport pharma corridor | Long term (≥ 4 years) |

| Government R&D Tax Incentives | +0.8% | National, strongest pull in biotech clusters around Leuven and Ghent | Medium term (2-4 years) |

| Digital Prescription and E-Pharmacy Adoption | +0.9% | National, early uptake in urban centers | Short term (≤ 2 years) |

| EU Critical Medicines Act Supply Resilience Programs | +0.7% | National, aligned with EU-wide rollout | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Health Expenditure Per Capita

Belgium’s per-capita health spend reached USD 6,022, outperforming the EU-14 average and freeing budget space for high-cost biologics. Public pharmaceutical outlays are forecast to rise from 8% of GDP in 2022 to 8.9% by 2027, translating into a 36.6% nominal increase. The 2026 federal budget earmarked EUR 25 million for the Early and Equitable Fast Access program, cutting reimbursement timelines for oncology and rare-disease drugs. Industry payrolls of 44,738 direct staff plus 140,835 across the value chain amplify tax receipts and voter interest in sector stability. Retail drug spending per capita sits 6% below the EU mean, indicating untapped volume potential as the population ages and discretionary income grows.

High Burden of Chronic Diseases

Cancer and circulatory disorders still account for roughly half of national mortality, coupled with an 82.6-year life expectancy. Mature cardiovascular categories face generic erosion, yet the obesity-linked surge in GLP-1 demand offers a new growth arc. Dermatological biologics for psoriasis and atopic dermatitis are outpacing systemic corticosteroids, lifting the segment’s growth curve for 2026-2031. Belgium’s 16% obesity prevalence accelerates uptake of oral GLP-1 candidates such as orforglipron once Lilly’s EUR 2.6 billion Netherlands plant goes live in 2027. Persistent supply constraints through 2025 create latent demand that is unlocked by capacity additions.

Digital Prescription and E-Pharmacy Adoption

A 100% eHealth indicator score and 91.8% e-prescription penetration lay the rails for seamless online fulfilment[1]European Commission, “EU Critical Medicines Act,” europa.eu. Belgium’s digital health turnover hit EUR 754.53 million in 2025 and should reach EUR 991.91 million by 2029 at a 7.09% CAGR. The upcoming EU Health Data Space and Digital Identity Wallet will support cross-border e-prescription redemption by 2027, pressuring domestic brick-and-mortar pharmacies to integrate home-delivery models. Current restrictions on the online sale of prescription medicines, shared with 18 other EU states, are expected to be softened under the Pharmaceutical Strategy for Europe. Over-the-counter lines, already web-enabled, benefit first from consumer preference shifts born during the pandemic.

EU Critical Medicines Act Supply Resilience Programs

Belgium registered 36 critical-impact shortage alerts in 2022—56% linked to immunoglobulins—highlighting dependence on a narrow manufacturing base. The EU Critical Medicines Act now compels diversified sourcing, strategic stockpiles and faster parallel-import clearances. Although Belgium exported EUR 79 billion worth of drugs in 2024, domestic inventories remain strained whenever global API flows falter. A January 2025 coalition pact placed shortages and biosimilar incentives high on the legislative agenda, while the EMA’s European Shortages Monitoring Platform allows earlier intervention when supply signals flash red.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory Post-Exclusivity Price Cuts | -0.8% | National, all reimbursed products | Short term (≤ 2 years) |

| Lengthy Reimbursement Timelines | -0.7% | National, affects innovative therapies | Medium term (2-4 years) |

| Hospital Financing Model Disincentivizing Biosimilar Uptake | -0.6% | National, public hospital networks | Medium term (2-4 years) |

| Increasing Sustainability Compliance Costs | -0.4% | National, energy-intensive plants in Flanders | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory Post-Exclusivity Price Cuts

Belgium slashes originator prices by up to 38% once generic or biosimilar competition appears, compressing margin runways and discouraging smaller line extensions[2]OECD, “Pharmaceutical Pricing and Reimbursement Policies 2025,” oecd.org. The 2026 budget further trims hospital invoice reimbursement to 78% and imposes EUR 1-2 patient co-pays, squeezing value-chain profits. Managed Entry Agreements, worth EUR 1.6 billion in 2019 rebates, cap upside whenever sales overshoot negotiated ceilings. Protracted reimbursement reviews—578 days on an EU average—plus reference pricing lower differentiation payoffs for formulation tweaks or adherence programs.

Hospital Financing Model Disincentivizing Biosimilar Uptake

Hospitals earn a fixed margin on invoiced drug costs, prompting them to favor costlier brands over cheaper biosimilars because revenue scales with unit price. The 2026 reimbursement cut compounds pressure yet leaves the perverse incentive intact. Despite a 2023 Royal Decree mandating competitive tenders, biosimilar penetration trails EU norms, confirming that tendering alone cannot offset structural financing biases. With hospital pharmacies holding 45.73% share of national purchases, any meaningful shift toward biosimilars hinges on financing reform. Coalition documents list biosimilar incentives as a priority, but operative details remain sketchy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By ATC/Therapeutic Class: Dermatologicals Lead Growth Amid Cardiovascular Maturity

Cardiovascular agents delivered 14.18% of the Belgium pharmaceutical market share in 2025 but confront generic-driven price ceilings as statins and ACE inhibitors mature. Dermatological products are projected to grow at a 7.54% CAGR through 2031, driven by monoclonal antibodies that offer superior remission rates in psoriasis and atopic dermatitis. Nervous-system drugs sustain volume via Belgium’s early adoption of disease-modifying therapies for multiple sclerosis and Alzheimer’s. Respiratory biologics that suppress IL-5 or IL-4/IL-13 pathways reduce exacerbations, while blood-forming agents face commoditization from direct oral anticoagulants. Insurance-backed fast-access funds tilt market mix in favor of oncology breakthroughs entering the residual “other” bucket.

Aging demographics and higher disposable incomes expand demand for osteoporosis, benign prostatic hyperplasia, and rheumatoid arthritis interventions. Patent filings totaling 417 in 2024 signal continued therapeutic diversification. GLP-1 therapies address metabolic conditions linked to the nation’s 16% obesity rate, with capacity expansion in neighboring the Netherlands set to clear supply bottlenecks beyond 2027. Belgium's pharmaceutical industry invests more in R&D toward immunology and rare diseases, fields with fewer entrenched generics.

By Drug Type: Prescription Dominance Persists as OTC Self-Care Accelerates

Prescription lines represented 86.85% of total 2025 value, reinforcing Belgium pharmaceutical market size dominance in specialty areas such as oncology and neurology. Branded molecules endure post-exclusivity reductions yet command volume in protected niches, while generics leverage automatic substitution rules to serve primary-care staples. Over-the-counter remedies expand at 7.21% CAGR as consumers retain self-care habits formed during pandemic mobility curbs.

Digital prescription ubiquity gives online pharmacies a friction-less path to scale, although regulatory gates still block remote dispensing of Rx products. European harmonization efforts suggest broader e-dispensing rights within this decade. Managed Entry rebates ensure public budgets stay on-course even when specialty volumes grow, permitting a balanced mix of high-value prescriptions and value-priced generics.

By Molecule Type: Biologics Surge as Small Molecules Retain Volume Base

Small molecules still anchor two-thirds of Belgium pharmaceutical market size thanks to oral convenience and optimized production footprints. Biologics, however, secure a 6.78% CAGR by answering unmet needs in oncology, immunology and ophthalmology. Biosimilar rollout remains lukewarm because hospital mark-up formulas reward originator usage, yet policy drafts call for financing realignment.

Advanced therapy medicinal products gain traction under fast-track reimbursement but reveal a manufacturing gap at home. GSK’s EUR 150 million vaccine expansion in Wavre and Lilly’s oral GLP-1 facility across the border illustrate the region’s pull for high-value plants. Rising R&D budgets increasingly favor cell, gene and RNA modalities, repositioning Belgium as a potential European launchpad once local capacity gaps close.

By Distribution Channel: Online Pharmacies Disrupt as Hospitals Retain Procurement Power

Hospital outlets held 45.73% of the 2025 turnover, dispensing most oncology and complex biologic regimens. The 2026 shift to a 78% reimbursement ceiling forces sharper tender strategies and may accelerate cross-hospital purchasing alliances. Online pharmacies, aided by 91.8% e-prescription usage, post a 7.65% CAGR through 2031 and will extend reach once EU Digital Identity wallets allow cross-border fills.

Retail pharmacists, roughly 2,000 nationwide, weather thinner margins because Belgium bans supermarket drug sales, preserving a professional, advice-centric model. The European Commission’s harmonization agenda foreshadows moderated restrictions on mail-order prescriptions, opening another lane for growth.

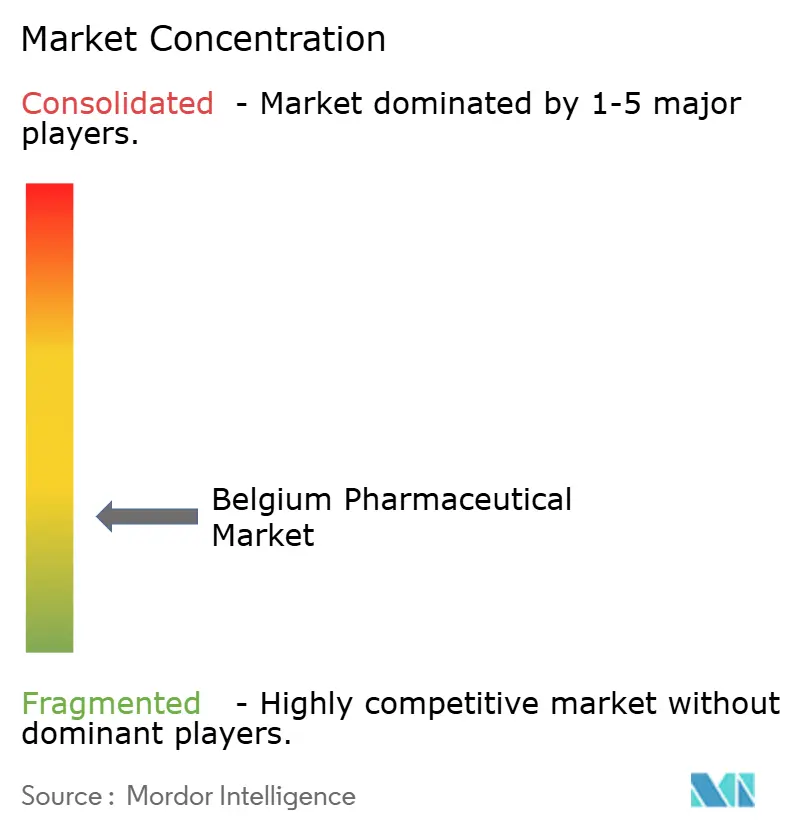

Competitive Landscape

Belgium pharmaceutical market competition centers on multinational subsidiaries, with Pfizer, Janssen, GSK, Novartis and AbbVie sharing scale with homegrown UCB, which alone absorbs 41% of national R&D spend. Strategy revolves around launching specialty biologics able to weather 38% post-patent price drops through clear clinical differentiation. Viatris and Zentiva chase hospital tenders for biosimilars but progress stalls against financing incentives that still reward originator price points.

Digital tools reshape selling models as e-prescription infrastructure enables direct-to-patient support programs, loyalty apps and data-driven adherence services. Divergent manufacturing bets sharpen contrasts: Pfizer shutters its Puurs site and cuts 1,200 roles, while GSK deploys EUR 150 million into Wavre and Lilly commits EUR 2.6 billion to a Netherlandic oral-solid plant. Belgium’s 417 patent filings in 2024 confirm fertile IP output, yet supply resilience dominates boardroom agendas after immunoglobulin shortages revealed logistical weak spots. Commercial alliances now blend R&D co-funding with risk-sharing reimbursement models to accelerate time-to-value.

Belgium Pharmaceutical Industry Leaders

AstraZeneca plc

AbbVie Inc.

Bayer AG

GlaxoSmithKline plc

Boehringer Ingelheim International GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Belgium announced its active participation in FAST-EU, a new EU initiative to streamline and accelerate multinational clinical trial approvals, aiming to modernize the process. This move positions Belgium as a test case for the EU’s efforts to enhance clinical research efficiency.

- November 2025: Eli Lilly committed EUR 2.6 billion to a greenfield oral-dose site in Katwijk, Netherlands, targeting orforglipron and other cardiometabolic assets, with ground-breaking slated for 2026.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Belgium pharmaceutical market as all human prescription and over-the-counter finished dosage forms, both small-molecule and biologic, that are manufactured in, imported into, and commercially invoiced within Belgium at ex-factory values.

Scope Exclusions

Veterinary medicines, stand-alone active pharmaceutical ingredients for export, medical devices, and food supplements fall outside this assessment.

Segmentation Overview

- By ATC / Therapeutic Class

- Alimentary Tract & Metabolism

- Blood & Blood-Forming Organs

- Cardiovascular System

- Dermatologicals

- Genito-Urinary System

- Systemic Hormonal Preparations

- Nervous System

- Musculoskeletal System

- Respiratory System

- Other Therapeutic Classes

- By Drug Type

- Prescription Drugs

- Branded

- Generics

- OTC Drugs

- Prescription Drugs

- By Molecule Type

- Small-Molecule Pharmaceuticals

- Biologics

- Biosimilars

- Advanced Therapy Medicinal Products (ATMPs)

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed regulators, hospital pharmacists, community-pharmacy leaders, and finance managers at Belgian producers across Flanders, Wallonia, and Brussels. Insights on channel mark-ups, parallel-trade patterns, and forthcoming therapeutic launches filled critical gaps and validated desk findings.

Desk Research

We extracted foundational volumes and values from Eurostat trade cubes, the National Institute for Health and Disability Insurance reimbursement files, EFPIA's annual "Pharma Figures," pharma.be economic briefs, and hospital procurement gazettes. Macro indicators such as population aging, GDP per capita, and health-outlay ratios came from Statbel and the World Bank. Paid resources, including D&B Hoovers for company splits and Dow Jones Factiva for deal flow, supplied additional context. These citations illustrate, but do not exhaust, the wider evidence pool consulted during desk work.

Market-Sizing & Forecasting

A top-down build reconciles national production plus imports minus exports, then adjusts for inventory swings. Select bottom-up checks, sampled ex-factory average selling prices multiplied by prescription and OTC pack volumes, calibrate therapeutic splits. Core variables powering the model include insured-resident counts, prevalence of oncology, cardiovascular, and diabetes cases, mean treatment duration, patent-expiry cadence, and co-payment rules. Forecasts to 2030 employ multivariate regression blended with ARIMA smoothing; scenario tests around parallel-trade volatility set outer bounds. Where pack data were missing, hospital invoice ratios benchmarked to community-pharmacy sell-out trends bridged gaps before final reconciliation.

Data Validation & Update Cycle

Outputs pass automated anomaly flags, peer-analyst cross-checks, and senior sign-off. Interviews are re-opened when variance breaches set thresholds. Models refresh annually, with interim updates for material policy or pricing shocks, so clients always receive the latest view.

Why Mordor's Belgium Pharmaceutical Baseline Commands Confidence

Estimates from different publishers often diverge because each applies distinct scopes, price points, and refresh cadences. Some exclude OTC drugs or rely on wholesale prices, while others freeze exchange rates for years. Mordor's disciplined annual update and mixed-method model offer a steadier, fully traceable benchmark.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.40 B | Mordor Intelligence | - |

| USD 8.10 B | Global Consultancy A | Older price base; hospital-only drugs excluded |

| USD 5.78 B (2024) | Regional Consultancy B | Wholesale pricing; OTC segment omitted |

Published figures differ, yet Mordor's balanced scope, transparent variables, and yearly refresh deliver a dependable baseline that decision-makers can recreate and trust.

Key Questions Answered in the Report

How large will Belgium's prescription segment be by 2031?

Prescription drugs, holding 86.85% of 2025 revenue, are projected to follow a 5.8% market CAGR, placing their 2031 value near USD 10.2 billion within the Belgium pharmaceutical market size.

Which therapeutic class is forecast to grow fastest to 2031?

Dermatologicals lead with a 7.54% CAGR as biologic treatments for psoriasis and atopic dermatitis gain reimbursement traction.

What drives online-pharmacy growth in Belgium?

A 91.8% e-prescription rate, a 100% eHealth indicator score and forthcoming EU cross-border e-prescription rules support a 7.65% CAGR for online channels.

Why do biosimilars gain ground slowly?

Hospital financing ties revenue to drug prices, so institutions favor higher-priced originators, muting biosimilar adoption until reimbursement reform occurs.

How big is BelgiumÕs pharmaceutical export surplus?

The sector generated a EUR 16.6 billion trade surplus in 2024, reflecting its role as a high-value production and export hub.

Which policy most eases patient access to innovative drugs?

The Early and Equitable Fast Access program, funded with EUR 25 million in the 2026 budget, cuts reimbursement timelines for breakthrough therapies.

Page last updated on: