Battery Testing And Inspection Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

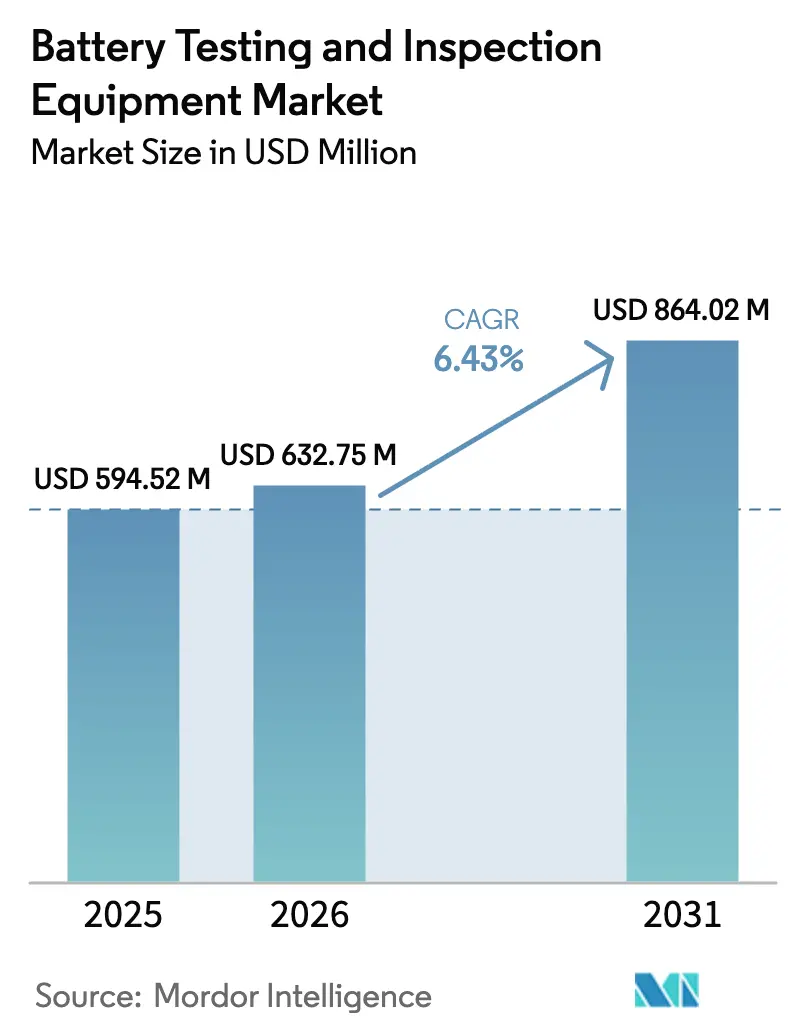

| Market Size (2026) | USD 632.75 Million |

| Market Size (2031) | USD 864.02 Million |

| Growth Rate (2026 - 2031) | 6.43% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

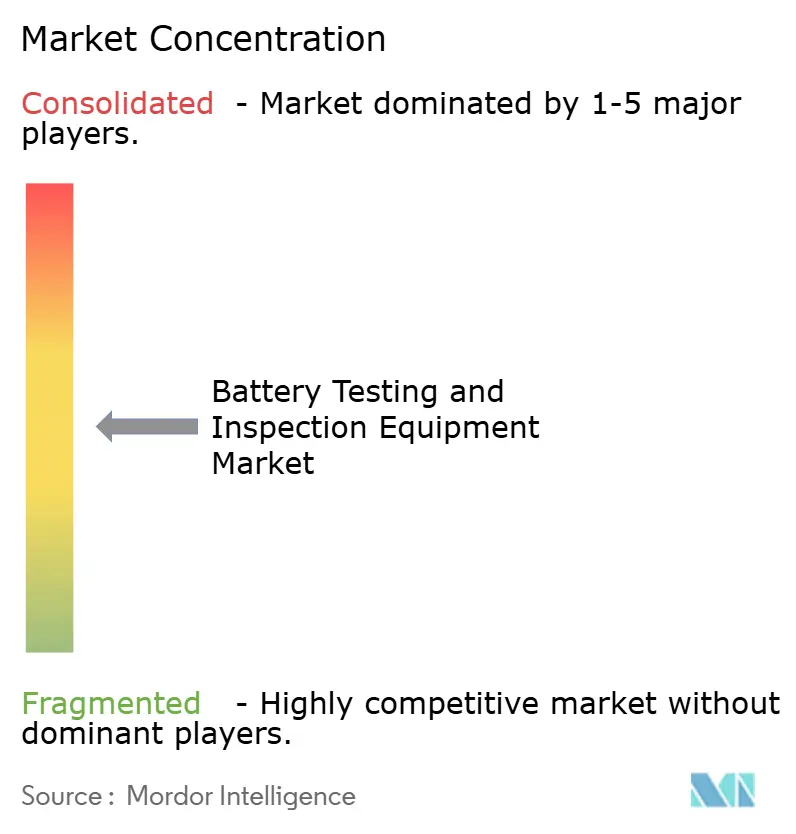

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Battery Testing And Inspection Equipment Market Analysis by Mordor Intelligence

The Battery testing & inspection equipment market size is expected to grow from USD 594.52 million in 2025 to USD 632.75 million in 2026 and is forecast to reach USD 864.02 million by 2031 at 6.43% CAGR over 2026-2031. The upward trajectory of the Battery testing & inspection equipment market reflects converging safety regulations, the scale-up of gigafactories, and the rapid commercialization of next-generation chemistries. UNECE R100 Rev. 4, FMVSS 305a, and China’s GB38031-2025 collectively extend testing scope from cell abuse to full-pack thermal-propagation analysis, creating demand for multi-parameter platforms that combine electrical, mechanical, and environmental stress testing.[1]United Nations, “Battery Testing in Accordance with UN Regulation 100 Rev. 3,” revivebatts.com Asia-Pacific leads procurement as regional firms bring more than 250 GWh of fresh capacity online between 2025-2027, while Europe’s battery-passport mandate shifts customer preferences toward testers with embedded traceability functions.[2]Battery Pass consortium, “Content Guidance for the EU Battery Passport,” thebatterypass.euSystem vendors differentiate by integrating electrochemical-impedance-spectroscopy (EIS) modules derived from automotive BMS technology, transforming test labs into data-rich hubs that feed real-time health metrics back to design teams.

Key Report Takeaways

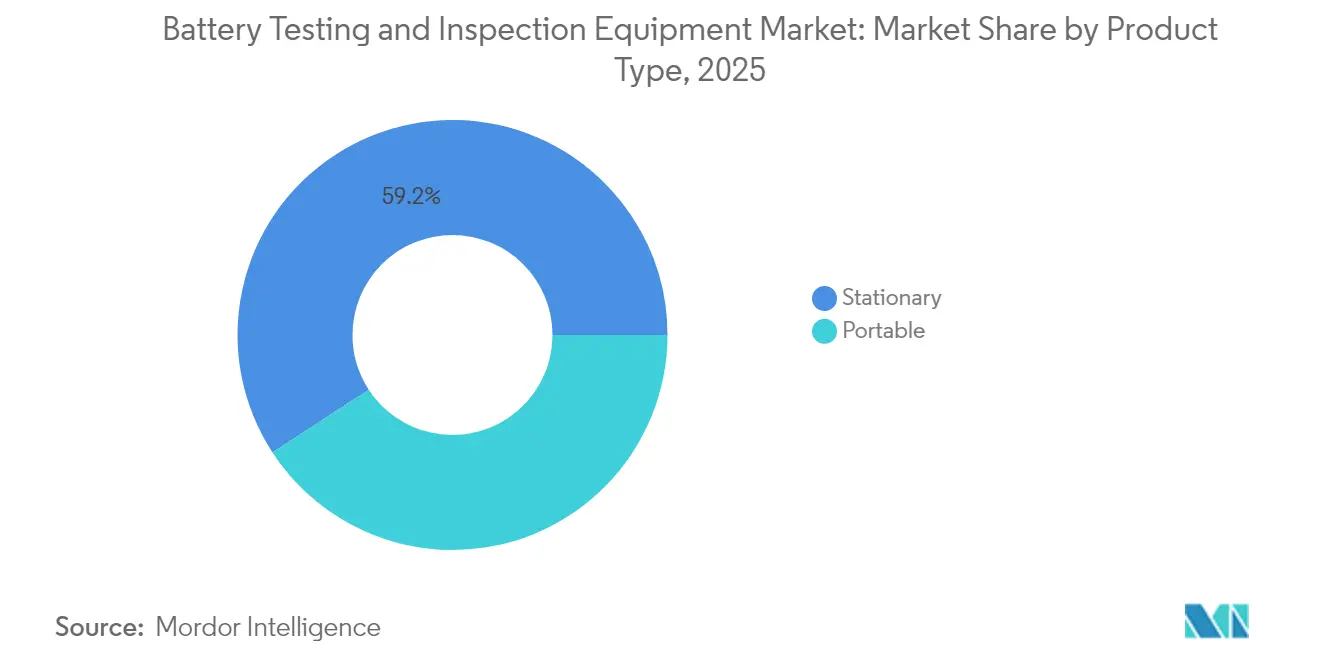

- By product type, stationary systems retained 59.20% revenue share of the Battery testing & inspection equipment market in 2025, while portable platforms are forecast to expand at an 8.35% CAGR to 2031.

- By application, pack-level testers captured 45.40% of the Battery testing & inspection equipment market size in 2025 and are projected to grow at 7.18% CAGR.

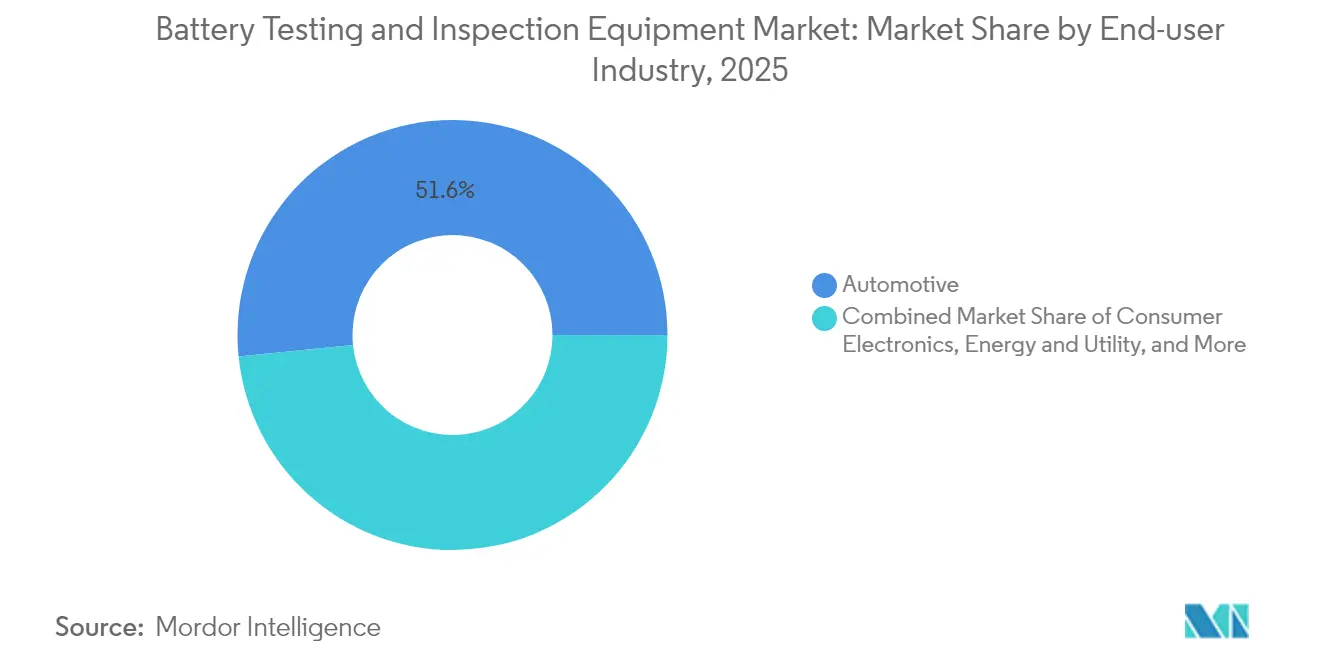

- By end-user, the automotive sector held 51.60% Battery testing & inspection equipment market share in 2025, whereas the energy-and-utility segment records the fastest 7.05% CAGR through 2031.

- By chemistry, lithium-ion commanded 80.30% share of the Battery testing & inspection equipment market size in 2025; solid-state testers deliver the highest 7.29% CAGR.

- By geography, Asia-Pacific led with 44.80% revenue share in 2025; North America is strengthening capacity behind new FMVSS 305a rules at a robust pace.

- BioLogic, Hioki and National Instruments together accounted for 18% share of global installed channels in 2024, underscoring an unconcentrated playing field.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Battery Testing And Inspection Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV crash-safe regulations tighten (UNECE-R100 Rev. 4) | +1.2% | Global with EU & North America lead | Medium term (2-4 years) |

| Surge in gigafactory commissioning (≥250 GWh 2025-27) | +1.8% | APAC core, spill-over to NA & EU | Short term (≤ 2 years) |

| Adoption of “battery passport” in EU | +0.9% | Primarily EU | Medium term (2-4 years) |

| Embedded EIS analytics in testers | +1.1% | Worldwide, automotive first mover | Long term (≥ 4 years) |

| Solid-state pilot lines need high-voltage rigs | +0.7% | APAC & North America | Long term (≥ 4 years) |

| Second-life mandates require pack screening | +0.6% | EU & North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EV crash-safe regulations tighten (UNECE-R100 Rev. 4)

Global roll-out of UNECE-R100 Rev. 4 obliges every electric-vehicle battery to pass thermal-shock, mechanical deformation, and fire-exposure protocols, elevating hardware specifications across the Battery testing & inspection equipment market. Test benches must log simultaneous voltage, temperature, and pressure signals under sub-second synchronization, prompting labs to invest in high-speed DAQ systems with optical-fiber networking. The rule pushes buyers toward turnkey rigs that incorporate thermal-propagation chambers, thereby converting single-purpose cycler budgets into multi-discipline capital projects

Surge in gigafactory commissioning (≥250 GWh added 2025-27)

Proliferation of gigafactories accelerates volume purchasing of channel-dense cyclers that validate thousands of cells in parallel. BMW’s Wackersdorf center, a EUR 100 million (USD 109 million) flagship, demonstrates how automakers internalize testing to compress design-to-launch cycles.[3]BMW Group, “Green light for Wackersdorf battery testing centre,” press.bmwgroup.comVendors supplying modular, rack-mountable cyclers gain a logistical edge as facility managers replicate identical blocks line after line.

Adoption of “battery passport” in EU 2024/2025

The passport forces each production lot to carry traceable performance, carbon-footprint and recycled-content data, migrating compliance tasks from spreadsheets to tester firmware. Instruments that auto-export secure JSON files to blockchain ledgers become procurement favorites among European OEMs.

Integration of embedded EIS analytics in testers

EIS modules shrink into plug-in cards, letting pack cyclers deliver impedance spectra every cycle without halting the charge-discharge loop. Real-time detection of lithium plating or SEI build-up shifts maintenance from reactive pack recalls to predictive interventions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-current cycler cap-ex inflation (Cu & Si costs) | -0.8% | Global with NA & EU acute | Short term (≤ 2 years) |

| Restricted lab talent & safety-certified facilities | -0.5% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High-current cycler cap-ex inflation (Cu & Si costs)

Copper busbars and silicon carbide MOSFETs, critical to 1,000-A testers, face 2025 commodity spikes, inflating unit prices. Some U.S. labs postpone upgrades, raising utilization rates on legacy racks. Vendors respond with leasing models that spread cap-ex pain over five-year OPEX horizons.

Restricted lab talent & safety-certified facilities

Battery test chambers handling runaway events above 3 MJ require ISO 17025 accreditation and fire-suppression retrofits that smaller firms struggle to fund. The resulting scarcity of certified slots slows validation timelines for start-ups, marginally curbing orders for additional equipment in North America and Europe.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Stationary dominance with portable acceleration

Stationary systems generated 59.20% of 2025 revenue within the Battery testing & inspection equipment market, a lead upheld by stringent abuse-test protocols that demand inert-gas chambers and explosion vents. Portable testers, though small, post an 8.35% CAGR as utilities deploy field-grade analyzers to screen repurposed EV packs on site. Portable rigs often piggyback on standard 19-inch rack controllers so spare parts stay common across both fleets. Stationary lines migrate toward robot-loaded trays to offset labor scarcity, a shift that magnifies software integration expenditures above hardware costs.

In the second half of the decade, the Battery testing & inspection equipment market size for portable units is projected to top USD 389.6 million, reflecting new inspection mandates for residential-storage packs. Automation vendors partner with cycler OEMs to embed robotic arms that swap trays every 10 minutes, trimming cycle-time variance across shifts. Stationary labs, in contrast, focus on high-current headroom; 1 MW DC channels enable simultaneous testing of eight 130 kWh bus packs, aligning with FMVSS 305a soak-test requirements.

By Application Type: Pack-level validation leads integration push

Pack testers held a 45.40% share of the Battery testing & inspection equipment market size in 2025, as automakers prioritize end-system integrity over isolated cell metrics. Heat-shrink ovens, crush plates, and vibration tables integrate into single lines so engineers run mechanical and electrical tests without repalletizing. Module-level rigs remain relevant for mid-stream quality gates inside gigafactories, while cell cyclers underpin supplier qualification.

Pack-level dominance intensifies as regulators demand whole-pack safety data for type approval. Embedded EIS sensors in harness wiring shortcut diagnostics during endurance cycles, raising ASPs per channel. Module testers evolve into hybrid rigs that toggle between CC-CV cycling and 30 Hz impedance sweeps, thereby extending utility into R&D labs seeking flexible assets.

By End-user Industry: Automotive leads while grid storage surges

Automotive OEMs purchased more than half of all channels shipped in 2025, locking down 51.60% Battery testing & inspection equipment market share. Their demand profile emphasizes fast-ramp construction schedules and 24/7 automation. Energy-and-utility buyers, however, post the briskest 7.05% CAGR. Long-duration storage finalists in U.S. Department of Energy solicitations must experimentally validate 6,000-cycle life at 100% depth of discharge, a test that ties up cyclers for 18 months.

Telecom back-up modules, medical-device packs, and aerospace batteries round out the customer mix, driving niche testers certified for RTCA DO-160 thermal-altitude profiles. Oil-and-gas robotics batteries create micro-opportunities for high-pressure submersible chambers.

By Battery Chemistry: Lithium-ion dominance with solid-state momentum

Lithium-ion retained 80.30% share in 2025, yet vendors already quote 850 V solid-state platforms for pilot lines slated to open in 2027. These units replace liquid-cooling loops with dielectric-fluid sprays to evacuate heat from densified ceramic stacks. Lead-acid persists in telecom UPS niches that require cold-crank metrics, while nickel-metal hydride rides on hybrid-bus retrofits in Japan.

The Battery testing & inspection equipment market anticipates dual-chemistry labs where software auto-detects cell type and switches compliance scripts. Fraunhofer ISI projects solid-state production at scale from 2030, and early validation contracts drive instrument revenue.

Geography Analysis

Asia-Pacific remains the epicenter of the Battery testing & inspection equipment market with a 44.80% share in 2025, driven by concentrated cell manufacturing clusters in China, South Korea, and Japan. Chinese integrators such as Xian Dao Intelligent deliver turnkey pack cyclers with 98% domestic parts content, aligning with Beijing’s localization push. Government subsidies in the Yangtze River Delta finance lab expansions inside regional innovation parks, accelerating orders for environmental chambers and high-speed DAQ boards. India’s PLI scheme for advanced-chemistry cells fosters a nascent market built around sub-100 kWh telecom and two-wheeler batteries, broadening the vendor base.

North America registers double-digit shipment growth as automakers localize supply chains to qualify for clean-vehicle tax credits. The Battery testing & inspection equipment market size for U.S. and Canadian buyers will reach USD 223.4 million by 2031, lifted by gigafactory hubs in the Southeast. UL Solutions’ Michigan laboratory serves as a regional reference site for FMVSS 305a readiness, and its open-access model lets Tier 2 suppliers verify modules without building in-house facilities. Canadian miners exploring sodium-ion cathodes partner with university labs to co-develop test scripts targeting sub-zero cycle life.

Europe concentrates on purchasing around compliance with Regulation (EU) 2023/1542. German OEMs demand instruments that auto-calculate carbon intensity per cycle and push encrypted data to cloud dashboards, turning testers into traceability nodes. The Battery testing & inspection equipment market share for EU-27 is expected to stay near 22.90% through 2031 as local manufacturers integrate solid-state pilot lines. Poland and Hungary emerge as cost-competitive lab-services hubs, offering third-party certification to smaller e-mobility start-ups.

Competitive Landscape

The Battery testing & inspection equipment market displays moderate fragmentation: the top five players command roughly 35% of installed global channel capacity. Multinationals such as BioLogic, Hioki, and Chroma pursue platform breadth, bundling cyclers with impedance analyzers and climate chambers in single purchase frameworks. BioLogic’s 2024 launch of the BCS-900 added 10 A/6 V modules optimized for research benches, yet its scalable backplane caters to high-volume pack lines, illustrating a multi-segment strategy. Hioki leverages proprietary four-terminal sensing to cut lead loss errors below 5 µΩ, appealing to solid-state developers who evaluate dendrite growth at high frequencies.

New entrants emphasize software as a differentiator. Californian start-up ReJoule embeds machine-learning models inside portable graders that predict SOH within 3 minutes, reducing screening costs for second-life operators. Asian robotics integrators bolt collaborative arms onto cyclers, automating pouch-cell insertion and thermocouple placement, thus lowering labor intensity. Strategic alliances grow: Chroma partners with AVL to co-market powertrain-test rigs, while National Instruments aligns its PXI instrumentation with power-rack OEMs, targeting open-architecture buyers.

Patent analysis highlights a shift toward on-board impedance measurement; Lithium Balance patents covering real-time EIS in BMS narrow options for latecomers. Suppliers respond by negotiating cross-licenses or investing in galvanostatic EIS alternatives. As solid-state pilot lines multiply, specialty vendors offering 10 kV isolation testers gain mindshare. Meanwhile, price competition intensifies in commodity cell-cycler SKUs, prompting tier-one brands to bundle condition-based maintenance services that lock in annuity revenue.

Battery Testing And Inspection Equipment Industry Leaders

Arbin Instruments

Hioki USA

Neware Battery Testers

Keysight Technologies

Chroma Systems Solutions, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: EVTank reported the global lithium-ion battery-equipment market contracted 28.8% year-over-year to CNY 1,331.4 billion (USD 183.4 billion), signaling inventory correction and tighter capital allocation among Chinese cell makers

- February 2025: California Energy Commission awarded USD 2.5 million to ReJoule to demonstrate a 2 MWh second-life EV battery system, validating field-grade screening economics in multi-family housing

- January 2025: NOVONIX received a conditional USD 754 million DOE-ATVM loan to build synthetic-graphite capacity in Tennessee, bolstering domestic anode supply for future U.S. gigafactories

- December 2024: NHTSA finalized FMVSS 305a, mandating thermal-runaway resistance, water-immersion endurance and unified emergency-response guides for EV batteries sold in the United States

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global battery testing and inspection equipment market as the sale of dedicated portable and stationary instruments, fixtures, and software used to evaluate cell, module, or pack performance across electrical, mechanical, and safety criteria throughout a battery's life cycle. According to Mordor Intelligence, devices such as cyclers, impedance testers, leak detectors, and end-of-line inspection stations are in scope.

Scope Exclusion: Certification services, generic multimeters, and full battery production machinery fall outside this study.

Segmentation Overview

- By Product Type

- Portable

- Stationary

- By Application Type

- Cell Testing Equipment

- Module Testing Equipment

- Pack Testing Equipment

- By End-user Industry

- Automotive

- Consumer Electronics

- Energy and Utility

- Telecom and Data Communication

- Healthcare

- Aerospace and Defence

- Oil and Gas

- Factory Automation and Industrial Equipment

- By Battery Chemistry

- Lithium-ion

- Lead-acid

- Nickel-based

- Solid-state / Next-Gen

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with battery lab managers, quality engineers at EV makers, and distributors in Asia, Europe, and North America. These interviews confirmed selling prices, utilization rates, and replacement cycles, closing gaps left by desktop findings and shaping model assumptions.

Desk Research

We leaned on tier-1 public sources such as UNECE R100 and IEC 62660 dockets, IEA battery deployment data, UN Comtrade shipment codes, and trade association white papers to frame demand and pricing. Company 10-Ks, investor decks, and reputable press added cost and channel detail, while paid repositories like D&B Hoovers and Dow Jones Factiva clarified vendor revenue splits. This source list is indicative; many additional references informed our desk analysis.

Market-Sizing & Forecasting

One top-down build starts with global lithium-ion cell output in gigawatt hours, applies an average test channel per GWh ratio, and multiplies by blended ASPs to derive demand, which is then balanced against regional replacement curves. Select bottom-up checks, supplier revenue roll-ups and sampled pack tester shipments, keep totals within a five percent band. Key variables include gigafactory commissioning schedules, mandated EV safety tests, ASP drift by feature set, chemistry share shifts, and pack energy density trends. A multivariate regression with ARIMA overlays handles interaction effects and short-term shocks. When vendor data are partial, we interpolate using channel counts verified during primary calls.

Data Validation & Update Cycle

Outputs pass anomaly filters, multi-analyst review, and senior sign-off. Reports refresh yearly, with interim updates triggered by policy shifts, major plant expansions, or material recall events.

Why Our Battery Testing And Inspection Equipment Baseline Commands Reliability

Published estimates often diverge because providers select different scopes, metrics, and refresh cadences.

Mordor Intelligence anchors its baseline in clearly bounded equipment definitions and a mixed modeling approach that tempers extremes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 594.52 million (2025) | Mordor Intelligence | - |

| USD 1.20 billion (2024) | Regional Consultancy A | Includes calibration benches and TIC services; relies mostly on revenue roll-ups |

| USD 575.1 million (2025) | Global Consultancy B | Omits inspection rigs and narrows end-user coverage |

| USD 634.31 million (2025) | Trade Journal C | Projects straight-line growth from a 2022 base; limited primary validation |

The comparison shows that, once scope and input rigor are aligned, Mordor's moderated figure offers decision-makers a transparent, repeatable baseline they can trust.

Key Questions Answered in the Report

What is driving growth in the Battery testing & inspection equipment market?

Tighter global safety regulations, rapid gigafactory build-outs and the EU battery-passport mandate collectively lift demand for advanced multi-parameter test platforms.

Which region buys the most testing equipment today?

Asia-Pacific accounts for 44.80% of 2025 revenue thanks to China’s dominant cell-manufacturing base and aggressive storage deployments.

How fast is portable battery test equipment growing?

Portable systems log an 8.35% CAGR through 2031 as utilities and second-life operators need field-ready graders.

Why is pack-level testing gaining share?

Regulators require system-level safety validation, and OEMs want integrated thermal-propagation and BMS diagnostics, bringing pack testers to 45.40% market share in 2025.

Will solid-state batteries change equipment demand?

Yes, pilot lines need 10 kV isolation and ceramic-interface diagnostics, pushing vendors to launch new high-voltage cyclers and impedance analyzers.

How fragmented is the competitive landscape?

With the top five firms holding about 35% of global capacity, competition hinges on software and analytics capabilities rather than sheer scale.

Page last updated on: