Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

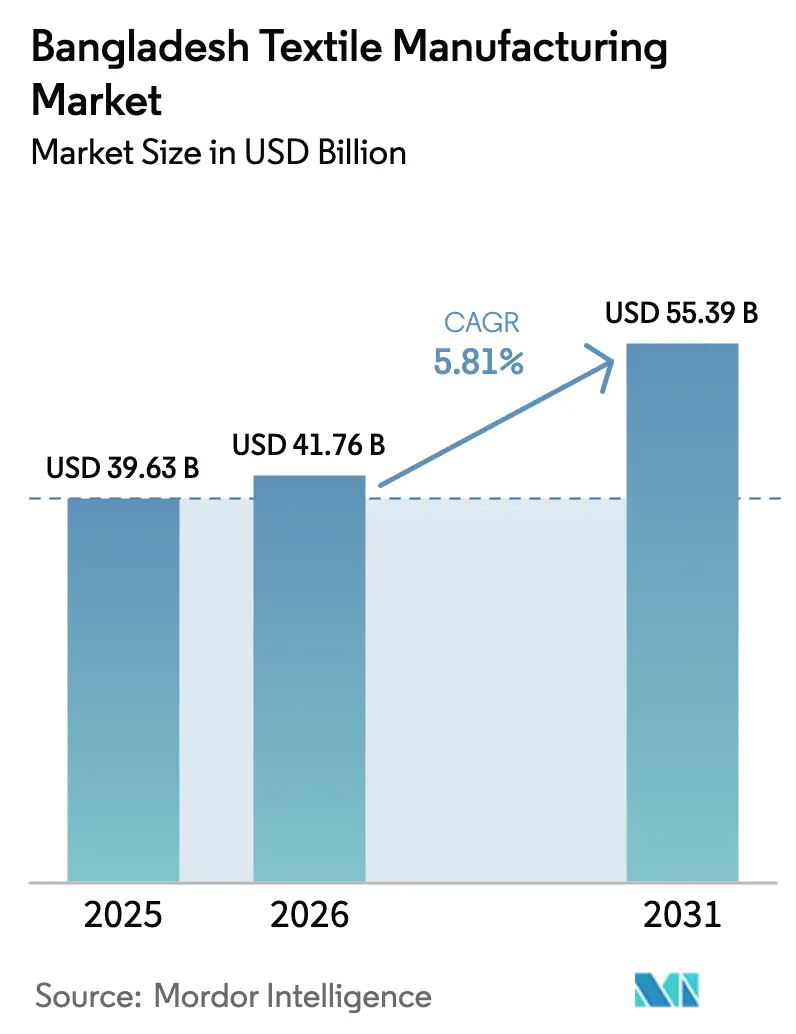

| Base Year Market Size (2025) | USD 39.63 Billion |

| Market Size (2026) | USD 41.76 Billion |

| Market Size (2031) | USD 55.39 Billion |

| Growth Rate (2026 - 2031) | 5.81% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bangladesh Textile Manufacturing Market Analysis by Mordor Intelligence

The Bangladesh Textile Manufacturing Market size is projected to expand from USD 39.63 billion in 2025 and USD 41.76 billion in 2026 to USD 55.39 billion by 2031, registering a CAGR of 5.81% between 2026 to 2031.

Continued duty-free access to the United Kingdom and the anticipated renewal of zero-tariff privileges in the European Union widen the customer base and reward mills that invested in verified environmental and social governance systems. Brand-mandated renewable-energy clauses, concessional green-finance windows, and real-time AI quality controls further lift productivity, although chronic gas shortages and volatile cotton prices challenge margin stability. Competitive momentum is shifting from pure cost arbitrage toward compliance-driven sourcing, technical-textile diversification, and speed-to-market capabilities. As a result, the Bangladesh textile manufacturing market is evolving into a mid-technology hub rather than a low-cost appendage, creating upside for mills that master traceability, recycled-fiber integration, and micro-lot production.

Key Report Takeaways

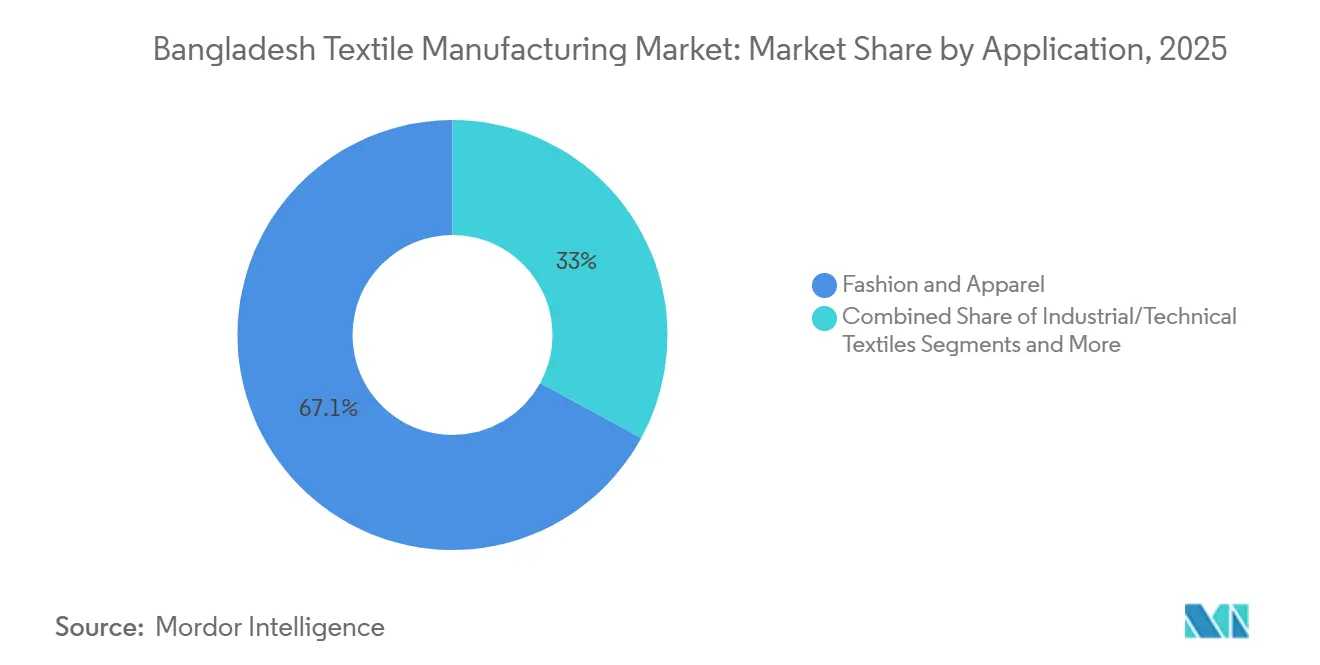

- By application, fashion and apparel commanded 67.05% of Bangladesh textile manufacturing market share in 2025, while industrial and technical textiles are forecast to expand at a 6.44% CAGR through 2031.

- By raw material, synthetic fibers led with a 36.99% share of the Bangladesh textile manufacturing market size in 2025, and polyester yarn is projected to grow at a 6.85% CAGR to 2031.

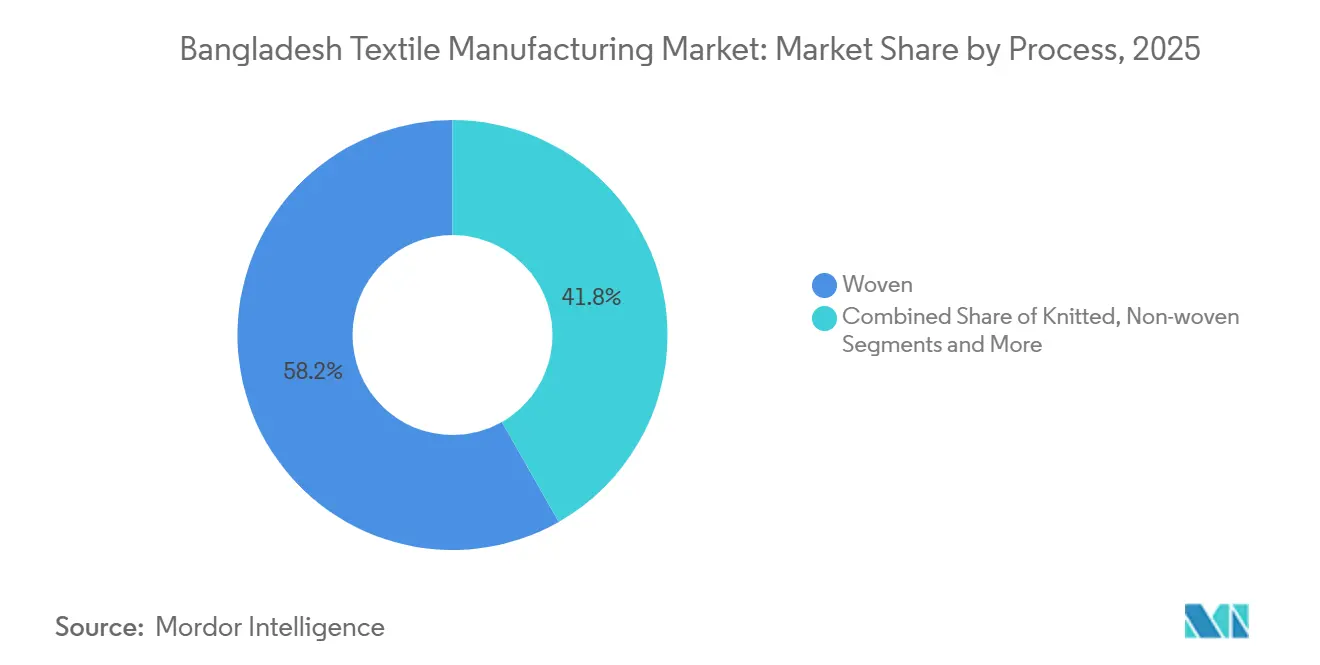

- By process, woven fabrics accounted for 58.23% of Bangladesh textile manufacturing market share in 2025, and non-woven lines will post the fastest 6.34% CAGR during the outlook period.

- By geography, Dhaka retained 52.42% capacity in 2025, whereas the Rest of the Bangladesh corridor, anchored by Bangabandhu Sheikh Mujib Shilpa Nagar, will accelerate at a 6.09% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Bangladesh Textile Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bangabandhu Sheikh Mujib Shilpa Nagar integrated hub | +0.9% | Mirsarai, Sitakunda, Sonagazi; Chittagong corridor | Long term (≥4 years) |

| Duty-free access extension under UK DCTS and expected EU GSP+ renewal | +0.8% | Dhaka, Gazipur, Chittagong export hubs | Medium term (2-4 years) |

| Compliance readiness for EU Corporate Sustainability Due-Diligence | +0.7% | EU-facing exporters nationwide | Medium term (2-4 years) |

| Brand-mandated renewable-energy projects cut Scope 2 emissions | +0.6% | Dhaka and Gazipur industrial clusters | Short term (≤2 years) |

| Green-finance window for zero-liquid-discharge dyeing lines | +0.5% | Gazipur and Narayanganj wet-processing belts | Medium term (2-4 years) |

| Gen-AI on-loom defect analytics enabling micro-lot orders | +0.4% | Pilot sites in Dhaka and Gazipur | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Duty-Free Access Extension Under UK DCTS and Expected EU GSP+ Renewal

The United Kingdom’s Developing Countries Trading Scheme locks in duty-free, quota-free entry for Bangladeshi apparel through 2029, shielding exporters from post-LDC graduation tariffs and relaxing rules of origin that once discouraged imported fabric content. Brussels is debating GSP+ admission that would reinstate zero duties in exchange for 27 international conventions, positioning compliant mills for uninterrupted EU access. Exporters hedged against safeguard ceilings by diversifying into technical textiles and automotive fabrics that carry separate tariff codes. These measures collectively lift buyer confidence and underpin volume commitments, adding clear tailwinds to the Bangladesh textile manufacturing market[1]UK Government, “Developing Countries Trading Scheme,” gov.uk .

Compliance Readiness for EU Corporate Sustainability Due-Diligence

The EU Corporate Sustainability Due Diligence Directive requires importers to audit tier-2 and tier-3 suppliers from 2027, imposing fines up to 5% of global revenue for lapses[2]European Parliament, “Corporate Sustainability Due Diligence: Deal on New Rules Approved,” europarl.europa.eu . Mills equipped with RFID roll tracking, blockchain batch records, and Higg Index reporting already moved up preferred-vendor lists in 2025. HSBC’s USD 65 million sustainability-linked loan to Viyellatex, tied to raw-material traceability targets, illustrates how compliance unlocks cheaper capital and stickier buyer relationships as European norms become de facto global baselines. Early adopters inside the Bangladesh textile manufacturing market secure multi-year volume pledges, while late movers risk margin-sapping remediation plans.

Brand-Mandated Renewable-Energy Projects Cut Scope 2 Emissions

Global retailers now require suppliers to cover at least 50% of electricity with renewables by 2027, prompting large Bangladeshi mills to install more than 200 megawatts of rooftop solar by end-2025. Pacific Jeans, Youngone, and Ha-Meem each activated arrays exceeding 8 megawatts, cushioning exposure to grid outages and lowering carbon footprints that factor directly into contract renewals. Import duties of 37–62% on photovoltaic hardware still deter smaller mills, yet concessional loans from IDCOL shorten payback periods to roughly four years. As green-power penetration rises, the Bangladesh textile manufacturing market gains differentiation based on verified emission cuts rather than headline wage costs.

Green-Finance Window for Zero-Liquid-Discharge Dyeing Lines

ADB and IFC blended capital now funds up to 70% of zero-liquid-discharge projects, shrinking payback windows for water-intensive dye houses. Envoy Textiles and DBL Group installed ZLD systems between 2023 and 2025, eliminating river effluent and meeting brand-level wastewater clauses[3]Asian Development Bank, “ADB Project 57005-001: Ananta Group Synthetic Knit Fabric Facility,” adb.org . Smaller processors face collateral hurdles, but the growing availability of sustainability-linked loans signals a path to scale environmental upgrades without cash-draining equity outlays. Enhanced water stewardship strengthens the Bangladesh textile manufacturing market’s license to operate amid tighter domestic enforcement.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic gas-supply shortfalls despite delayed LNG expansion | −0.9% | Dhaka, Gazipur, Narayanganj belts | Short term (≤2 years) |

| Climate-driven cotton price volatility | −0.6% | Spinning mills nationwide | Medium term (2-4 years) |

| Digitization gap among tier-3 subcontractors | −0.4% | Countrywide tier-3 suppliers | Medium term (2-4 years) |

| Rising IoT-linked cybersecurity breaches | −0.3% | Digitally advanced facilities | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Chronic Gas-Supply Shortfalls Despite Delayed LNG Expansion

Domestic gas output slipped to roughly 2,200 mmcfd in 2025 against industrial demand topping 2,800 mmcfd, forcing mills to burn diesel at costs 30–40% above piped gas. Summit LNG’s capacity-doubling plan slid to late-2026, prolonging rationing that shaved gross margins to single digits for mid-tier exporters. Uncertain allocation rules complicate production planning, dampening investment sentiment inside the Bangladesh textile manufacturing market.

Climate-Driven Cotton Price Volatility

Cotton peaked near 95 cents per pound in 2024 amid U.S. drought and Pakistani floods, then receded to 70 cents by early 2025. Mills locked into fixed-price apparel contracts absorbed inventory losses, tightening working capital as bank interest rates jumped above 11%. Producers blending polyester or viscose tempered exposure, yet sustained volatility underscores the importance of fiber diversification in the Bangladesh textile manufacturing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Fashion Dominance Drives Industrial Innovation

Fashion and apparel held a dominant 67.05% Bangladesh textile manufacturing market share in 2025, anchored by denim, knit tops, and value-priced fast-fashion orders. Industrial and technical textiles will accelerate at a 6.44% CAGR to 2031, supported by robust geotextile demand for road projects and steady hospital re-orders of medical gowns. Household textiles move roughly in line with the overall Bangladesh textile manufacturing market size, whereas automotive fabrics remain a white-space niche ripe for early movers.

Sustainability criteria reshape the mix: brands now stipulate 15–30% recycled polyester content, prompting Envoy Textiles to launch a USD 22 million waste-fabric recycling plant that closes the loop on cutting-room scraps. Medical-textile expansion hinges on ISO 13485 certification that fewer than 10 domestic mills presently hold. Protective and sportswear segments face tariff headwinds once LDC graduation occurs, underscoring the urgency of GSP+ status to preserve competitiveness.

By Raw Material: Synthetic Momentum Dominates

Synthetic fibers captured a 36.99% share of the Bangladesh textile manufacturing market size in 2025, with polyester yarn forecast to expand at a 6.85% CAGR through 2031. Price stability tied to crude derivatives and wrinkle-resistant properties make polyester the fiber of choice for quick-turn fashion. Domestic capacity additions by Energypac Fashions and Beximco Synthetics begin to trim import reliance on China and India.

Natural fibers remain essential for breathable garments, yet climate risk and water intensity inflate raw-cotton uncertainty. Recycled inputs gain traction: Ananta Group’s USD 70 million synthetic-knit project will blend recycled polyester chips with virgin feedstock, answering buyer mandates for circular sourcing. Specialty high-performance fibers stay niche due to capital barriers, but growing interest in military and industrial contracts may spark pilot lines later in the decade.

By Process/Technology: Woven Dominates, Non-Woven Accelerates

Woven fabrics commanded 58.23% of Bangladesh textile manufacturing market share in 2025, reflecting deep-rooted denim and shirting capabilities across Gazipur and Dhaka. Non-woven technologies, led by spunbond and melt-blown polypropylene, are on track to post a 6.34% CAGR to 2031 as hygiene and medical sectors localize supply. Knitting retains strategic importance for T-shirts and activewear, but loom-side AI upgrades position weaving plants to capture micro-lot premiums.

Investment patterns mirror demand: DBL Group evaluated needle-punched lines for geotextiles, while Youngone funds a training college to build 3D fabric skills. High-capital 3D weaving remains limited to fewer than five sites, yet rising automotive interest may justify additional imports of specialized looms. Overall, process diversification is broadening the Bangladesh textile manufacturing market beyond its legacy denim core.

Geography Analysis

Dhaka accounted for 52.42% of national capacity in 2025, offering proximity to banks and a skilled workforce but suffering from traffic-induced logistics costs and grid instability. Gazipur, just north of the capital, houses the largest spinning and dyeing clusters yet faces acute water stress during the dry season, driving adoption of zero-liquid-discharge plants by early movers such as Viyellatex and DBL. Chittagong’s share sits near 17%, and its port access trims lead times from factory floor to vessel to under two hours, although rising land prices narrow the cost gap.

The Rest of Bangladesh segment, including Narayanganj, Narsingdi, and emerging Cumilla and Feni zones, is projected to grow at a 6.09% CAGR to 2031, outpacing the overall Bangladesh textile manufacturing market. Bangabandhu Sheikh Mujib Shilpa Nagar spearheads this shift with LNG allocation, streamlined customs, and a decade-long tax holiday that already secured commitments from spinning, weaving, and garment groups. Better infrastructure disperses risk, relieving Dhaka congestion and diversifying power and water dependencies.

Environmental pressures differ by zone. Narayanganj dye houses received closure warnings in 2024 for river contamination, but compliant mills retained orders as brands pivoted away from non-certified facilities. Chittagong firms such as Youngone deploy large-scale solar arrays to meet Scope 2 targets amid soaring industrial tariffs. As capacity reallocates south and east, geographic competition intensifies inside the Bangladesh textile manufacturing market, stimulating investment in power reliability, waste management, and digital logistics.

Regulatory Landscape

Bangladesh textile manufacturing is governed through a mix of industrial policy, standards enforcement, and trade and tax administration. The Ministry of Textiles and Jute (MoTJ) is a primary policymaker for textiles and jute, including programs linked to the Jute Act 2017 and National Jute Policy 2018, while the National Board of Revenue (NBR) sets and administers customs duties, tariff lines, and bonded warehouse rules that shape input costs and backward-linkage competitiveness.

Product quality and conformity oversight sit with the Bangladesh Standards and Testing Institution (BSTI) under the Ministry of Industries, which issues product certification and runs laboratories accredited to ISO/IEC 17025. In the trade-policy pipeline, the draft Import Policy Order 2026-2029 includes proposals to raise minimum value-addition requirements across select garment categories, reinforcing the policy direction toward more domestic yarn and fabric use as Bangladesh navigates post-LDC trade conditions.

Value Chain Analysis

The Bangladesh textile manufacturing value chain starts with imported raw materials (notably cotton, and man-made fiber feedstocks), moves through spinning, weaving/knitting, dyeing and finishing, and then into garment manufacturing and export logistics. Industry coordination and capability-building are influenced by sector bodies such as the Bangladesh Textile Mills Association (BTMA) for primary textiles and BGMEA/BKMEA for garment and knitwear manufacturers, alongside export and investment facilitation through government entities such as the Export Promotion Bureau (EPB) and zone authorities (BEPZA/BEZA).

Key friction points in the chain remain energy and utilities reliability, working-capital costs, and dependence on imported cotton and selected yarn or fiber inputs. 2026 industry reports citing reduced utilization levels and a BTMA-referenced plan for spinning-mill shutdowns point to how gas and power constraints, combined with financial pressure, can disrupt upstream yarn supply and then propagate lead-time risk downstream. In response, larger groups emphasize vertical integration (spinning to fabric to apparel), renewable power additions such as rooftop solar, and compliance systems including traceability and wastewater management to stabilize throughput and meet buyer requirements.

Competitive Landscape

Competition remains moderately fragmented: the top 20 groups control roughly 35–40% of export volume, leaving considerable headroom for mid-tier entrants armed with niche capabilities. Vertical integration is the dominant strategy. DBL’s USD 390 million purchase of Glory Textile added 42 tonnes of daily yarn output, locking in denim feedstock and reinforcing single-vendor value propositions. Similar moves by Square Textile and Mohammadi align spinning, weaving, and garment stages to safeguard compliance visibility and capture margin at each node.

Technology adoption reinforces hierarchy. Leaders apply generative-AI vision, RFID roll tracking, and blockchain batch verification to win slots on EU sourcing lists governed by due diligence law. Mid-sized mills facing 10–12% gross margins often defer digital upgrades, risking exclusion as buyers trim vendor rosters. Foreign capital deepens the field; Destination Express International’s stake in Toyo Knitex highlights Chinese interest in the Bangladesh textile manufacturing market, driven by cost and duty advantages.

White-space potential centers on automotive and advanced technical textiles, areas where Bangladesh’s global share is below 1%. Polymer-extrusion know-how and weaving scale already exist, but certification gaps and just-in-time logistics networks require dedicated investment. As LDC graduation erodes tariff cushions after 2026, sustained relevance will depend on speed-to-market, innovation, and verifiable sustainability rather than baseline labor cost.

Bangladesh Textile Manufacturing Industry Leaders

Ha-meem Group

Noman Group

Beximco Textile Division Limited

Square Textile

DBL Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Policy and incentive levers are creating whitespace for deeper backward linkage and higher value-addition textiles. Bangladesh Bank raised the cash incentive for local textile exports to 5% for FY2026-27 (from 1.5%), directly rewarding domestic sourcing and local raw-material usage, while the draft Import Policy Order 2026-2029 proposes higher minimum value-addition thresholds in several garment categories. Together, these measures support investments that expand local yarn and fabric capacity, improve traceability, and reduce exposure to tariff and rule-of-origin constraints in key export markets.

Capital commitments in 2026 also point to expansion nodes around spinning, denim, and export-zone manufacturing platforms. Envoy Textiles disclosed a plan to invest about Tk179.15 crore to double open-end rotor spinning output at its Bhaluka facility to 50 tonnes per day, and new land leases in BEPZA and economic zones (for example, the Mirsharai and Jamalpur projects cited in 2026 announcements) signal continued use of zone infrastructure to scale capacity and shorten set-up times. Sustainability differentiation remains a commercial gateway: Bangladesh recorded 290 LEED-certified garment factories as of July 2026, aligning with brand compliance requirements and reinforcing demand for renewable energy, water recycling, and cleaner wet processing as part of upgrade roadmaps.

Recent Industry Developments

- June 2026: Ha-Meem Group commenced operations at a new garment accessories plant, targeting initial output of about 600,000 to 700,000 yards of fabric and accessories per month. The move strengthens backward linkage and helps reduce dependence on externally sourced trims and accessories that can extend lead times. It also improves the group’s ability to bundle products for buyers seeking tighter compliance control across inputs.

- May 2026: Square Textiles PLC inaugurated a 5.83 MW rooftop solar plant at its Gazipur facility. The installation supports energy-cost management during grid volatility and aligns production with buyer-driven decarbonization and ESG screening. It also signals that renewable power is becoming embedded in core textile operations, not limited to flagship garment units.

- November 2025: Ha-Meem Group signed a project agreement for a 16.9 MWp rooftop solar installation across its Textile Zone, covering units including Ha-Meem Denim Ltd., Ha-Meem Spinning Ltd., and Ha-Meem Textile Ltd. The project broadened the scale of captive renewable energy planning across upstream and midstream assets. Such multi-unit solar programs help stabilize electricity supply for spinning and denim lines that are sensitive to downtime.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as the value of textile manufacturing output generated within Bangladesh, covering fabric and textile production activities that supply apparel, home, and industrial end uses.

Scope exclusions: We exclude pure trading and distribution margins that are not linked to local manufacturing output.

Segmentation Overview

- By Application

- Fashion & Apparel

- Industrial/Technical Textiles

- Household & Home Textiles

- Medical & Healthcare Textiles

- Automotive & Transport Textiles

- Others (Protective, Sports Textiles, etc.)

- By Raw Material

- Natural Fibers

- Cotton

- Wool

- Silk

- Synthetic Fibers

- Polyester

- Nylon

- Rayon / Viscose

- Acrylic

- Polypropylene

- Recycled Fibers

- Others (Speciality High-Performance Fibers (Aramid, Carbon, UHMWPE))

- Natural Fibers

- By Process / Technology

- Woven

- Knitted

- Non-woven

- Spunlaid (Spunbond / Melt-blown)

- Dry-laid Hydro-entangled

- Wet-Laid

- Needle-punched

- 3-D Weaving & Spacer Fabrics

- By Geography

- Dhaka

- Gazipur

- Chittagong

- Rest of Bangladesh

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base on Bangladesh production, exports, and demand direction, before assumptions were shaped into a model. We relied on public sources such as Bangladesh Bank releases, the Bangladesh Bureau of Statistics, UN Comtrade trade data, ITC Trade Map style country export dashboards, and World Bank macro indicators to anchor units, price movement, and timing.

To avoid sizing the market on one data stream, export earnings were cross-checked with manufacturing output indicators, capacity expansion news, and policy signals that affect mills and processors. Company annual reports, exchange filings, investor presentations, and reputed press were used to validate revenue ranges and production footprints. Where needed, a paid subscription for company financials and a separate import-export shipment level database were used selectively to confirm volumes and mix, in a directionally consistent way. The desk sources listed here are illustrative only, and many other public references were also used for clarification and cross-verification.

Primary Interviews and Surveys

Primary work was done to pressure-test the desk assumptions, especially around capacity utilization, product mix shifts, and typical pricing for different textile processes. We spoke with manufacturers, sourcing and procurement teams, industry advisors, and logistics and trade-linked stakeholders across Bangladesh, and then used follow-up checks to close any wide ranges before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 18% | APAC: 38% |

| Mid tier: 40% | Functional/Unit leaders: 25% | EMEA: 36% |

| Smaller Players: 22% | Managers: 57% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts from a top-down reconstruction built from Bangladesh textile output signals and trade-linked demand, which are then translated into value using observed price ranges and mix. Our model was then corroborated with selective bottom-up approximations, such as supplier revenue bands, capacity-based rollups for key processes, and a basic ASP times volume logic for high-volume categories.

A few practical inputs did most of the work, even though we tracked more than these in the workbook. The most important ones included textile and apparel export earnings trends, yarn and fabric production direction, capacity additions and utilization at mills, shifts between woven and knit output, and fiber mix changes (cotton, man-made fibers, and jute) that affect achievable pricing. When partial information was available for smaller sites, gaps were handled using process-level utilization ranges and conservative throughput assumptions that were confirmed in interviews.

For forecasting, scenario analysis was used because export exposure, compliance costs, and input price swings can change outcomes quickly. These drivers were discussed in primary calls to set realistic bands. The final forecast line reflects the base scenario and is reviewed against trade growth signals, inflation assumptions, and the expected pace of capacity ramp-ups.

Data Validation & Update Cycle

Outputs are validated through triangulation across export signals, macro indicators, and manufacturing-side checks so no single data series drives the final number. Large variances trigger a second look at currency conversion timing, unit pricing, and mix assumptions, and then a targeted re-contact is done if the gap still stays wide.

Before sign-off, the model is reviewed in multiple analyst passes, and the assumptions table is checked for internal consistency across years. The report is refreshed annually, and interim updates are made when there are material events such as trade policy shifts, major capacity expansions, or sharp input price moves. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Bangladesh Textile Manufacturing Industry Study Market Estimate Compared With Other Published Estimates

It is normal to see different market size numbers for Bangladesh textiles because sources do not always measure the same thing, even when the report titles look similar. Differences usually come from what is counted as manufacturing value, the use of export-only proxies, and how pricing and exchange rates are applied in the base year.

Some published figures lean heavily on a narrow export-earnings view that tracks mostly garments shipped overseas, and then treat that as the total market. In Mordor Intelligence, the total is built to reflect textile manufacturing activity in-country, and it is counted across applications and processes rather than being limited to an export-only garment value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 39.63 B (2025) | |

| Industry Promotion Portal A | USD 38.48 B (2024) | Uses export earnings for textiles and apparel as the main yardstick, which can miss domestically consumed textiles and parts of upstream manufacturing value that do not ship as finished garments. |

| Market Aggregator B | USD 19.04 B (2024) | Likely reflects a narrower counted value pool or different value chain cut, and the base year conversion and pricing choices are not clearly shown, which can compress the reported total. |

Seen together, the spread is mainly explained by whether the estimate is export-led, manufacturing-led, or based on a limited value chain slice. Our approach stays traceable to observable output and trade signals, and it can be repeated year to year because the key variables and checks are explicitly tied back to Bangladesh-specific industry metrics.

Key Questions Answered in the Report

What is the current value of the Bangladesh textile manufacturing market?

The Bangladesh textile manufacturing market size reached USD 41.76 billion in 2026.

How fast will the sector grow over the next five years?

Industry revenue is projected to climb at a 5.81% CAGR, reaching USD 55.39 billion by 2031.

Which application segment is expanding the quickest?

Industrial and technical textiles are expected to post the fastest 6.44% CAGR through 2031.

Why are synthetic fibers gaining share?

Polyester offers stable pricing and wrinkle resistance, driving a 6.85% CAGR that outpaces natural fibers.

What geographic area will attract the most new investment?

The Rest of Bangladesh corridor led by Bangabandhu Sheikh Mujib Shilpa Nagar is set to expand at a 6.09% CAGR as infrastructure advantages pull capacity south and east.

How are mills addressing sustainability demands from global brands?

Leading firms install rooftop solar, adopt zero-liquid-discharge dyeing, and deploy blockchain traceability to secure contracts tied to environmental and social compliance targets.

Page last updated on: