Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

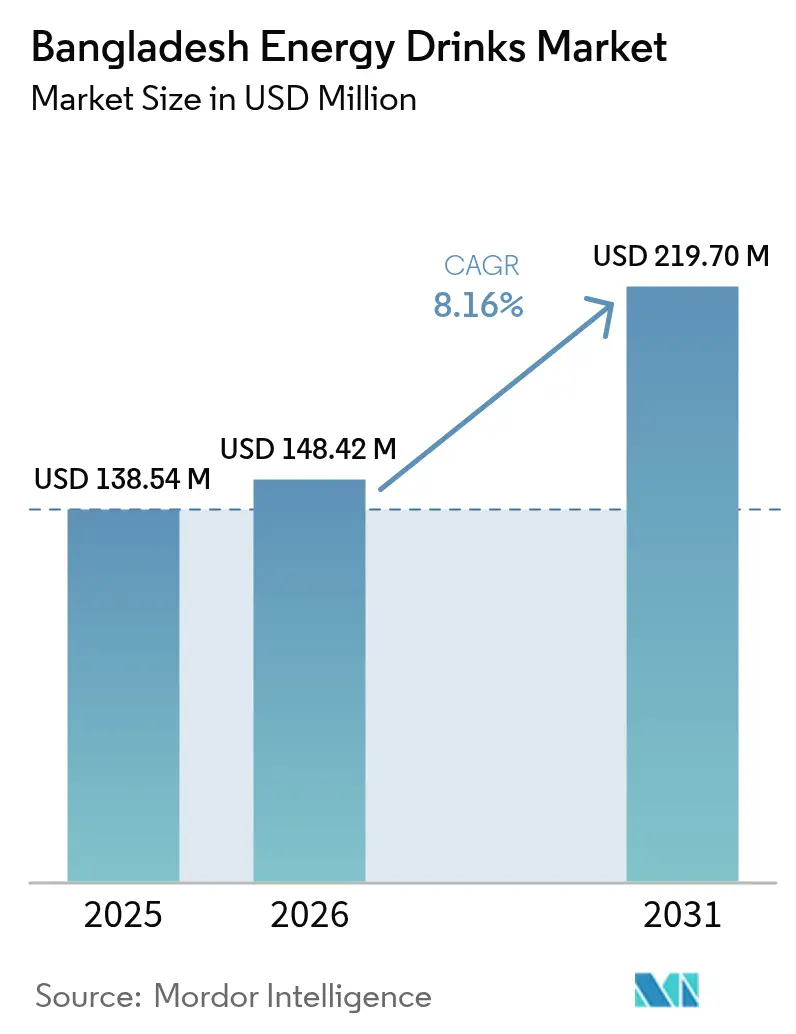

| Base Year Market Size (2025) | USD 138.54 Million |

| Market Size (2026) | USD 148.42 Million |

| Market Size (2031) | USD 219.70 Million |

| Growth Rate (2026 - 2031) | 8.16% CAGR |

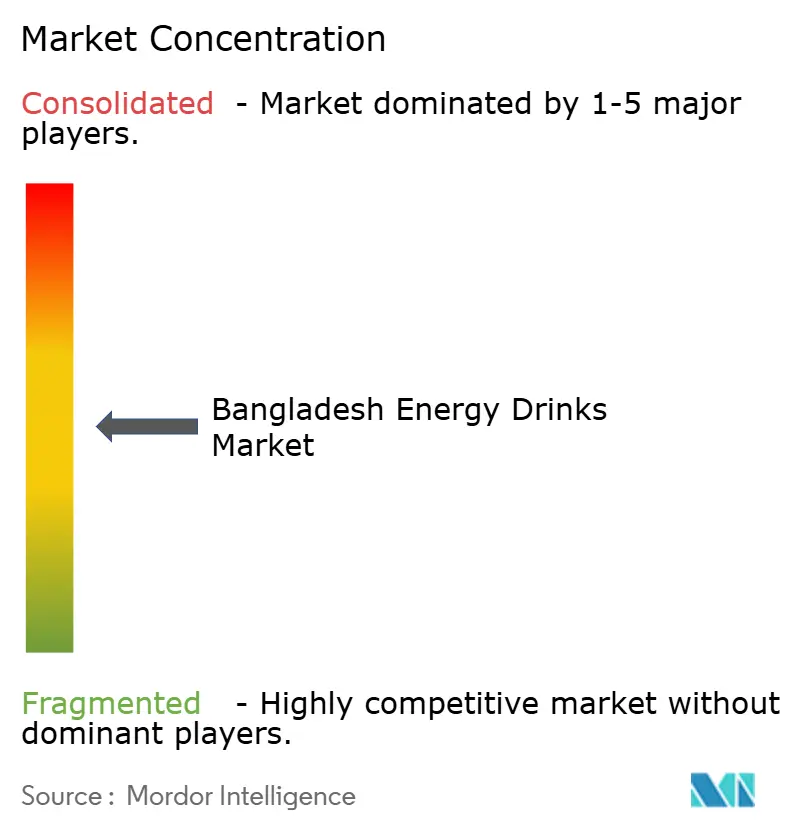

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bangladesh Energy Drinks Market Analysis by Mordor Intelligence

The Bangladesh energy drinks market size is expected to grow from USD 138.54 million in 2025 and USD 148.42 million in 2026 to USD 219.70 million by 2031, registering a CAGR of 8.16% between 2026 and 2031. Bangladesh’s energy drink market is expanding rapidly, driven by urban concentration in Dhaka and stricter food safety and halal compliance regulations. Longer commute times and growth in gig-based employment are increasing demand for convenient caffeine boosts, particularly among young consumers. Despite a high overall tax burden on beverages, brands are using organized retail and e-commerce channels to reduce supply chain layers and keep prices competitive. Multinationals like PepsiCo and Red Bull are strengthening their premium positioning through cricket sponsorships and digital influencer campaigns. Meanwhile, local players such as PRAN-RFL Group and Akij Group are defending share through aggressive pricing and in-store promotions.

Key Report Takeaways

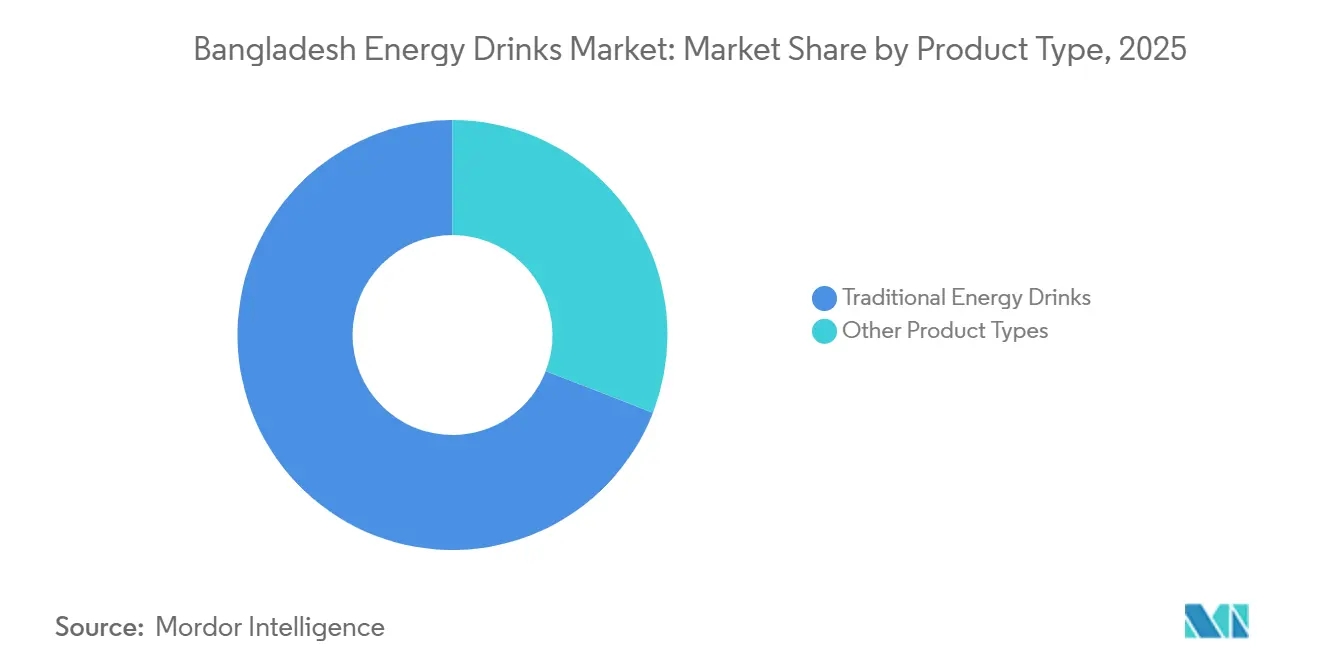

- By product type, traditional energy drinks held 69.12% of the Bangladesh energy drinks market share in 2025, whereas other product types are projected to register the quickest 8.57% CAGR through 2031.

- By packaging type, cans accounted for 42.05% of the Bangladesh energy drinks market size in 2025, while bottles represent the fastest-growing format at an 9.07% CAGR to 2031.

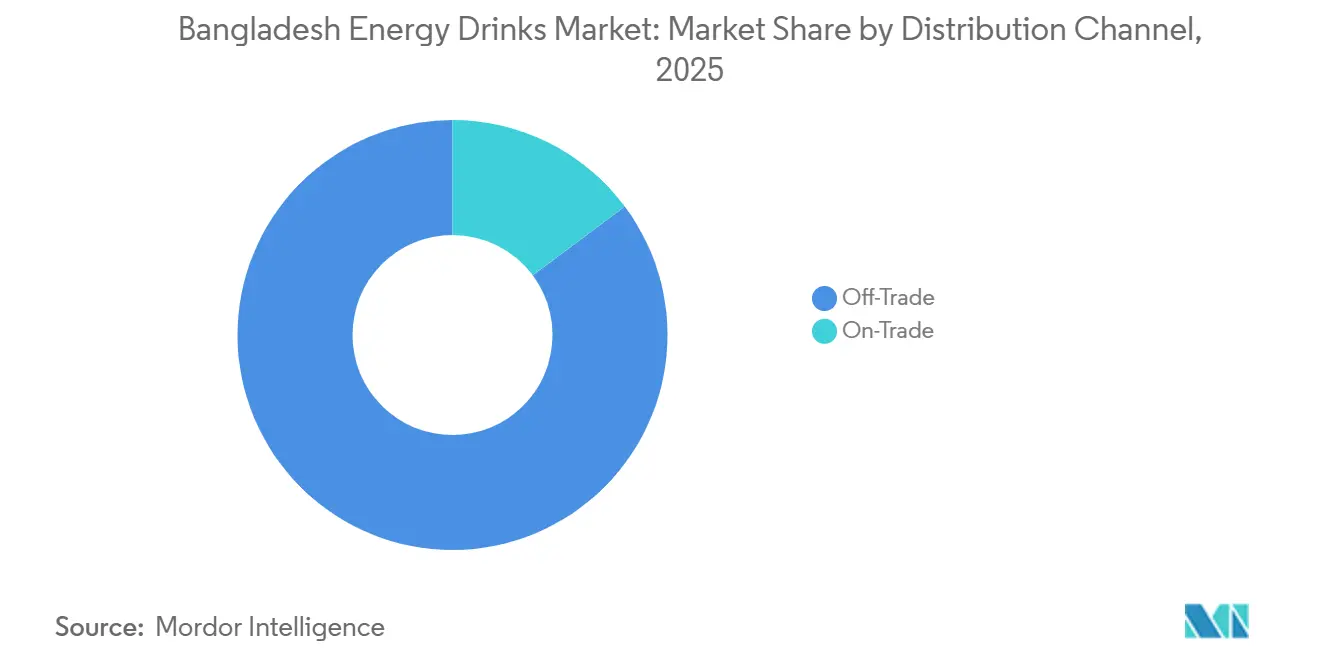

- By distribution channel, off-trade outlets commanded 85.20% of revenue in 2025, while on-trade venues are set to grow the fastest, advancing at a 8.95% CAGR to 2031.

- By geography, Dhaka dominated with 36.95% value share in 2025 and is projected to grow at 9.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bangladesh Energy Drinks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fast-paced urban lifestyles driving demand for convenient consumption options | +1.80% | Dhaka and Chittagong urban cores, spill-over to secondary cities | Medium term (2–4 years) |

| Growth of modern retail channels and expansion of cold-chain infrastructure | +1.50% | National, with early gains in Dhaka metro accounting for expanding Shwapno outlets | Long term (≥4 years) |

| Rising premiumization trend with increasing preference for healthier ingredients | +1.20% | Dhaka, Chittagong affluent segments; limited rural penetration | Medium term (2–4 years) |

| Strong promotional push through intensive advertising and event sponsorships | +1.00% | National, concentrated in cricket-heavy metros | Short term (≤2 years) |

| Introduction of sugar-free variants catering to health-conscious consumers | +0.90% | Urban Dhaka, Chittagong middle-class households | Medium term (2–4 years) |

| Halal certification enhancing consumer trust and strengthening demand | +0.70% | National, with export spillover to Middle East and Africa | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Fast-paced urban lifestyles driving demand for convenient consumption options

Rapid urban expansion in cities such as Dhaka and Chittagong is reshaping beverage preferences, as longer commutes, dense living conditions, and demanding service-sector jobs push consumers toward convenient, ready-to-drink energy options. With commute times often stretching beyond 90 minutes and inflation tightening discretionary spending, single-serve, affordable energy drink formats have gained traction among office workers, students, delivery riders, and night-shift employees. The gradual rise of modern retail and quick-commerce platforms has further strengthened impulse and repeat purchases, embedding functional beverages into daily routines. For instance, a study from PLOS Global Public Health highlights that 44.4% of adolescents now consume carbonated beverages daily, signaling a growing acceptance of Western-style energy products [1]Source: Munmun Shabnam Bipasha et al., “Sugar Sweetened Beverages Consumption among University Students of Bangladesh,” International Journal of Public Health Science, iaescore.com. University populations, particularly those balancing academic and part-time work commitments, represent a strong consumer base, but demand is equally visible among garment factory staff, IT professionals, and gig-economy couriers seeking sustained alertness. Together, these structural urban and employment shifts are steadily expanding the baseline consumption of energy drinks across Bangladesh’s metropolitan centers.

Growth of modern retail channels and expansion of cold-chain infrastructure

Bangladesh’s retail ecosystem is rapidly modernizing, strengthening the reach of energy drinks across urban and emerging semi-urban centers. Organized chains such as Shwapno, now operating hundreds of outlets nationwide, and Agora are streamlining procurement through direct-sourcing models, reducing intermediary mark-ups and enabling more competitive pricing for popular PET bottle formats. Policy support, including the withdrawal of VAT on supermarket purchases, has further stimulated store traffic and improved affordability for cost-sensitive shoppers. Meanwhile, online marketplaces like Chaldal and Daraz are enhancing convenience through doorstep delivery, particularly appealing to time-constrained consumers. On the supply side, major investments in temperature-controlled warehousing and high-capacity aseptic production lines are strengthening cold-chain efficiency and ensuring consistent product quality. Collectively, these advancements are improving shelf availability, maintaining optimal chill conditions, and reinforcing repeat consumption patterns within Bangladesh’s energy drink segment.

Rising premiumization trend with increasing preference for healthier ingredients

Increasing scrutiny over sugar and caffeine levels is redefining Bangladesh’s energy drink category, pushing brands to reformulate with lower sugar, balanced caffeine, and added functional ingredients such as vitamins and electrolytes. In 2025, ACME expanded its presence with ION positioned firmly within the energy drink segment, aligning with compliance standards set by the Bangladesh Standards and Testing Institution following tighter regulatory oversight. Similarly, Bruvana Sports+ entered the market as a performance-oriented energy drink, highlighting clean-label claims and the absence of artificial colors or sweeteners to attract health-aware urban consumers. Laboratory findings revealing elevated caffeine concentrations in certain products further accelerated reformulation and premium positioning strategies. Middle-class professionals are increasingly willing to pay more for energy drinks perceived as safer and functionally superior. Despite tax pressures, manufacturers are broadening sugar-free and fortified energy drink portfolios, transforming the category from a purely stimulant-based offering into a more lifestyle-driven segment.

Strong promotional push through intensive advertising and event sponsorships

As product differentiation narrows, competition in Bangladesh’s energy drink sector is increasingly driven by emotionally resonant branding rather than functional claims. Companies are investing heavily in cricket tie-ups, celebrity ambassadors, and hyper-local influencer campaigns to deepen youth engagement. Globe Soft Drinks has accelerated Royal Tiger’s growth through widespread television placements and large-format outdoor advertising that appeal to both metropolitan and semi-urban audiences. Global players such as PepsiCo (via Sting) and Red Bull are channeling substantial budgets into YouTube and Facebook video promotions to capture Bangladesh’s rapidly expanding digital population. Periods of geopolitical sensitivity have further reshaped market dynamics, enabling domestic brands to adopt patriotic positioning and gain traction when multinational sentiment weakens. Collectively, these strategies have shifted energy drinks from niche stimulants to culturally embedded lifestyle beverages within a relatively short span.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer concerns about excessive sugar and caffeine intake | -1.3% | National, with heightened scrutiny in Dhaka medical/academic circles | Medium term (2–4 years) |

| Increasing presence of counterfeit products disrupting market pricing | -1.1% | Dhaka, Chittagong, and peri-urban wholesale hubs | Short term (≤2 years) |

| Higher price sensitivity among consumers | -0.8% | Rural Bangladesh and lower-income urban segments | Short term (≤2 years) |

| Higher excise duties on carbonated soft drinks and energy drinks | -0.6% | National, affecting all formal-sector producers | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing consumer concerns about excessive sugar and caffeine intake

Growing clinical scrutiny is reshaping perceptions of energy drinks in Bangladesh, particularly among informed urban consumers. Independent academic assessments have identified caffeine content in leading 250 ml packs ranging roughly between 22 mg and 65 mg, while other laboratory reviews have flagged levels surpassing international reference thresholds, alongside sugar quantities that can approach or exceed recommended daily intake limits in a single serving. Healthcare practitioners, including specialists at BIRDEM General Hospital, have also cautioned against frequent consumption of electrolyte-style beverages due to elevated sodium levels and potential blood pressure risks, an important concern in a country with millions of diabetes patients. In response to mounting health concerns, the Bangladesh Food Safety Authority has taken enforcement actions against non-compliant manufacturers, while authorities have emphasized stricter labeling transparency for sugar and caffeine content. This evolving regulatory and medical narrative is encouraging a gradual shift toward moderated intake and sugar-free alternatives, slightly constraining projected category growth.

Higher excise duties on carbonated soft drinks and energy drinks

Raids conducted in March 2025 exposed an underground manufacturing network supplying imitation products to wholesale markets, where they are sold at prices up to 40% lower than authentic brands. This parallel supply chain significantly undermines legitimate players and results in substantial fiscal losses for the government. Recent crackdowns uncovered an informal supply network distributing imitation products across wholesale markets, where they are sold at significantly lower prices than established brands, resulting in notable revenue losses for the government. Despite multiple enforcement drives and legal actions in recent months, regulatory efforts have lacked consistency. Counterfeit energy drinks continue to reappear in retail channels, undermining consumer confidence in official quality certifications. This ongoing grey-market activity disrupts fair competition and challenges the stability of the organized segment. This persistent informal activity compresses margins for organized brands, limits their ability to pass on high excise costs, and ultimately constrains premiumization in the Bangladesh energy drinks sector.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Traditional Formulations Drive Market Leadership

Traditional Energy Drinks remain the backbone of the Bangladesh energy drinks market, accounting for a dominant 69.12% share in 2025. Their strength lies in strong brand familiarity, affordable pricing, and expansive distribution reach across urban and semi-urban retail networks. Local brands such as Akij Food & Beverage Ltd. (Speed) and Globe Soft Drinks Ltd. (Royal Tiger) have strategically positioned themselves as cost-effective alternatives to international players, appealing to price-sensitive consumers. Competitive price points reinforce their accessibility among mass-market buyers. Established equity and deep retailer penetration continue to drive high-volume sales. However, increasing regulatory scrutiny and quality compliance requirements may gradually influence cost structures within this volume-driven segment.

Other Energy Drinks are emerging as the fastest-growing category, projected to expand at a CAGR of 8.57% through 2031. This segment includes electrolyte-infused, vitamin-enriched, sugar-free, and low-calorie formulations tailored to evolving consumer preferences. Rising health awareness, coupled with Bangladesh’s growing diabetic population, is accelerating demand for reduced-sugar and functional energy options. Urban professionals, particularly within the 26–35 age group, are increasingly drawn to compact, functional beverages that deliver targeted benefits beyond caffeine stimulation. Portfolio diversification by major players such as PRAN-RFL Group reflects a strategic shift toward premium and niche offerings. Supported by regulatory oversight from the Bangladesh Standards and Testing Institution, the segment is benefiting from rising consumer trust and gradual premiumization trends.

By Packaging Type: Cans Dominate While Bottles Surge

Cans remain the largest packaging segment, accounting for 42.05% of total sales in 2025, reflecting their strong association with premium quality and international standards. The aluminum format offers superior protection against light and oxygen, helping extend shelf life beyond six months in Bangladesh’s tropical climate. This preservation advantage supports taste consistency, a factor highly valued by urban consumers. Premium global brands such as Red Bull continue to leverage cans to reinforce aspirational positioning and justify higher price points. Despite higher unit costs, the format sustains demand due to its perceived authenticity and superior product integrity. While sustainability conversations are emerging, purchasing decisions remain primarily influenced by brand image and quality cues.

Bottles, particularly PET formats, represent the fastest-growing segment, projected to expand at a 9.07% CAGR, steadily narrowing the gap with cans. PET packaging offers 30–40% savings in raw material costs and reduces breakage risks during transportation across congested distribution routes. Its lighter weight and stackability improve logistics efficiency, especially for e-commerce and micro-warehouse deliveries. Manufacturers favor bottles for balancing affordability with product visibility, a key purchase driver in traditional retail. The format’s flexibility also enables varied pack sizes, supporting both urban convenience and rural price sensitivity. As affordability and distribution efficiency gain priority, bottles are increasingly becoming the operational backbone of Bangladesh’s energy drinks packaging landscape.

By Distribution Channel: Off-Trade Supremacy with On-Trade Growth

The off-trade segment emerged as the largest distribution channel in 2025, accounting for 85.20% of total market volume, reflecting Bangladesh’s strong reliance on retail-led beverage sales. Supermarkets, convenience outlets, and traditional grocery stores continue to anchor energy drink distribution across urban and semi-urban areas, while online grocery platforms such as Chaldal and Daraz drive a shift toward digital purchasing. According to the World Bank, internet usage in Bangladesh rose by 6% over the past two years to reach 45% in 2023, accelerating online grocery adoption and e-commerce-led beverage sales [2]Source: World Bank, "World Bank Database", data.worldbank.org. Modern trade players are further strengthening their position through app-based ordering, home delivery, and click-and-collect models, enabling brands to optimize visibility, promotions, and consumer engagement, reinforcing off-trade dominance.

In contrast, on-trade represents the fastest-growing segment, projected to expand at a CAGR of 8.95% through the forecast period. Although comparatively smaller in share, cafés, quick-service restaurants, hotels, and entertainment venues are increasingly positioning energy drinks as premium, high-margin offerings. Growth in co-working hubs, e-sports lounges, sports clubs, and corporate dining facilities, particularly in major cities such as Dhaka and Chittagong, is expected to gradually elevate on-premise consumption. As disposable incomes rise and lifestyle-oriented spending gains momentum, on-trade channels are becoming critical for brand visibility, experiential marketing, and premium product placements within Bangladesh’s evolving beverage landscape.

Geography Analysis

Dhaka, accounting for 36.95% of the 2025 market value and projected to expand at a robust 9.12% CAGR through 2031, remains the anchor of Bangladesh’s energy drinks market. As the country’s economic and administrative hub, it concentrates the highest disposable incomes and a dense urban workforce. Demanding work schedules, academic pressure, and prolonged commute times sustain steady consumption among students, professionals, and service workers. Organized retail presence, led by chains such as Shwapno and Agora, ensures strong product visibility and cold-chain access across income segments. Premium variants gain traction among corporate employees, while affordable local brands continue to drive high-volume sales. The division also serves as a strategic launchpad for new product introductions and premium SKU testing.

Chittagong Division continues to benefit from its role as Bangladesh’s primary port and industrial corridor. Export-oriented manufacturing, shipbreaking yards, and logistics operations generate consistent demand from industrial workers and shift-based employees seeking convenient energy solutions. Rising trade activity and industrial wages are strengthening household purchasing power, gradually narrowing the consumption gap with Dhaka. The region’s expanding urban base and retail modernization are supporting wider brand penetration. However, infrastructure bottlenecks and port-related congestion still pose operational challenges that can affect distribution efficiency and inventory cycles.

The Rest of Bangladesh, including rural and semi-urban areas across other divisions, remains comparatively underpenetrated but presents significant long-term headroom. According to the World Bank, urban population accounted for approximately 33% of Bangladesh’s total population in 2024, highlighting substantial rural consumption potential as infrastructure and retail access continue to expand [3]Source: World Bank, "World Bank Database", data.worldbank.org. Expanding road networks, rural electrification, and mobile connectivity are enabling deeper last-mile distribution. Remittance inflows are improving disposable incomes, encouraging trial of affordable, small-pack energy drink formats. Domestic conglomerates such as PRAN-RFL Group demonstrate how strong nationwide distribution can unlock demand beyond metropolitan centers. With continued infrastructure upgrades and retail formalization, these regions are positioned to become the next growth frontier for Bangladesh’s energy drinks industry.

Competitive Landscape

Competitive intensity in the Bangladesh energy drinks market remains moderate, as leading domestic groups command significant share while smaller and informal players fragment overall value capture. Established local companies such as PRAN-RFL Group, Globe Soft Drinks, Osotspa Co. Ltd, Red Bull GmbH, and Akij Food & Beverage, among others leverage deep-rooted distribution networks, cost-efficient production, and strong retailer relationships to protect their mass-market strongholds. Their scale advantages allow them to compete effectively on pricing while maintaining consistent nationwide availability across urban and semi-urban centers.

At the same time, competition is evolving beyond traditional carbonated energy drinks toward diversified functional beverage portfolios. Companies are extending into product portfolio into other performance-oriented formulations to tap emerging lifestyle trends and niche consumer segments. Premiumization is gradually gaining traction, particularly in urban areas, where higher-income consumers show interest in improved formulations and international-quality standards. This shift reflects a dual-track strategy, volume-led penetration in price-sensitive segments alongside selective premium positioning.

On the supply side, investments in automation, quality control technologies, and supply chain optimization are strengthening manufacturing efficiency and regulatory compliance. Certifications such as halal accreditation from BSTI reinforce credibility in both domestic and potential export markets, especially in Middle Eastern corridors. However, the regulatory framework governed by the Bangladesh Standards and Testing Institution (BSTI) and the Bangladesh Food Safety Authority (BFSA) raises entry barriers, favoring well-capitalized incumbents with the resources to meet evolving compliance and quality mandates.

Bangladesh Energy Drinks Industry Leaders

-

PRAN-RFL Group Ltd

-

Osotspa Co. Ltd

-

Red Bull GmbH

-

Globe Soft Drinks & AST Beverage Ltd.

-

Akij Food & Beverage Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: PepsiCo Bangladesh, in a bid to capture the youthful market, rolled out its Sting energy drink in a 200ml PET bottle, retailing at Tk 30. The launch was bolstered by an extensive "Shock Lagbei" marketing blitz, spanning television, digital, and outdoor platforms.

- March 2025: ACME Consumer Products Ltd has launched its ION hydration drink, responding to the rising demand for electrolyte replenishment beverages and making a notable foray into the functional beverage market.

- December 2024: PRAN-RFL Group announced comprehensive sustainability plans, including a 20% energy usage reduction with 25% from renewable sources by 2030, alongside a commitment to recycle all plastics and use 90% local ingredients.

Bangladesh Energy Drinks Market Report Scope

Energy drinks contain a high concentration of stimulants, majorly caffeine, taurine, ginseng, guarana, and others. It enhances physical performance along with mental alertness. The Bangladesh energy drinks market is segmented by packaging and distribution channels. Based on packaging, the market is segmented into cans and PET bottles. Furthermore, based on distribution channels, the market is segmented into supermarkets/hypermarkets, convenience/grocery stores, online stores, and others. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Traditional Energy Drinks |

| Other Energy Drinks |

By Packaging Type

| Cans |

| Bottles |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Off-Trade Channels |

By Region

| Dhaka |

| Chittagong |

| Rest of Bangladesh |

| By Product Type | Traditional Energy Drinks | |

| Other Energy Drinks | ||

| By Packaging Type | Cans | |

| Bottles | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Off-Trade Channels | ||

| By Region | Dhaka | |

| Chittagong | ||

| Rest of Bangladesh | ||

Key Questions Answered in the Report

How large will the Bangladesh energy drinks market be by 2031?

It is projected to reach USD 219.70 million by 2031, advancing at a 8.16% CAGR from 2026.

Which product type grows fastest inside Bangladesh’s energy-drink space?

Other Product Types are expected to post the quickest 8.57% CAGR as consumers are exploring new product offerings.

What packaging trends should suppliers watch?

Cans still dominate with 42.05% share in 2025, but bottles are gaining traction at an 9.07% CAGR.

Why region shows the highest market growth?

Dhaka witnessed the highest market share of 36.95% in 2025, while also being the fastest-growing segment with 9.12% CAGR through 2031.

Page last updated on: