Baby Care Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

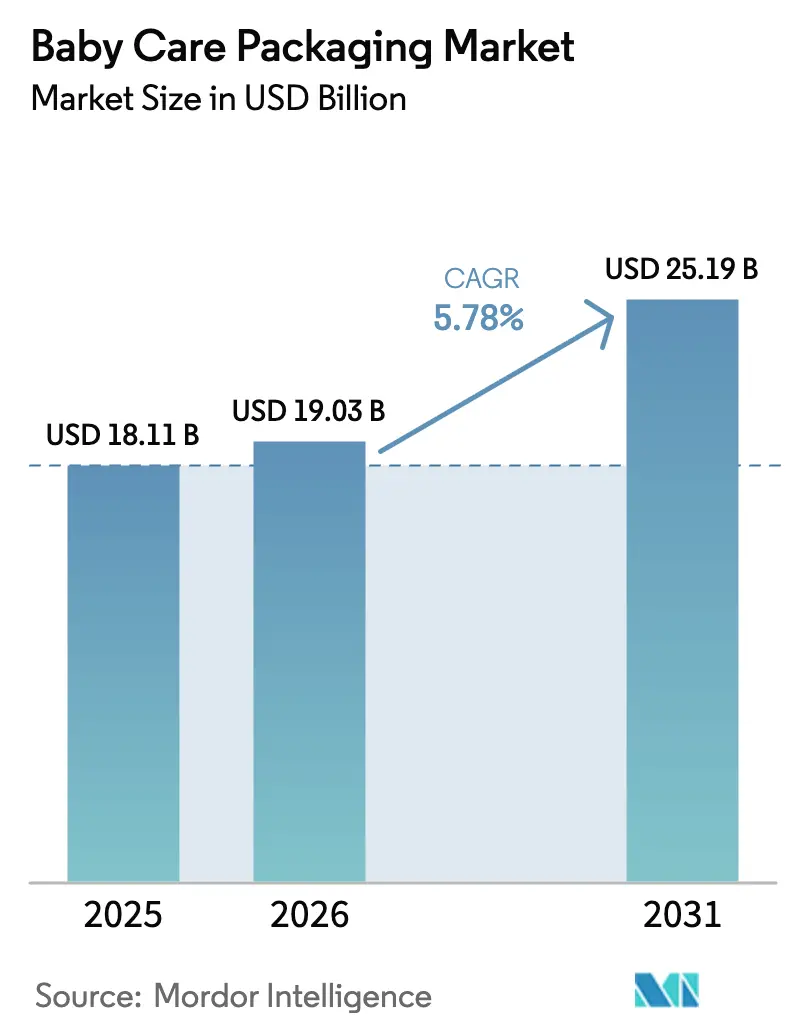

| Market Size (2026) | USD 19.03 Billion |

| Market Size (2031) | USD 25.19 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

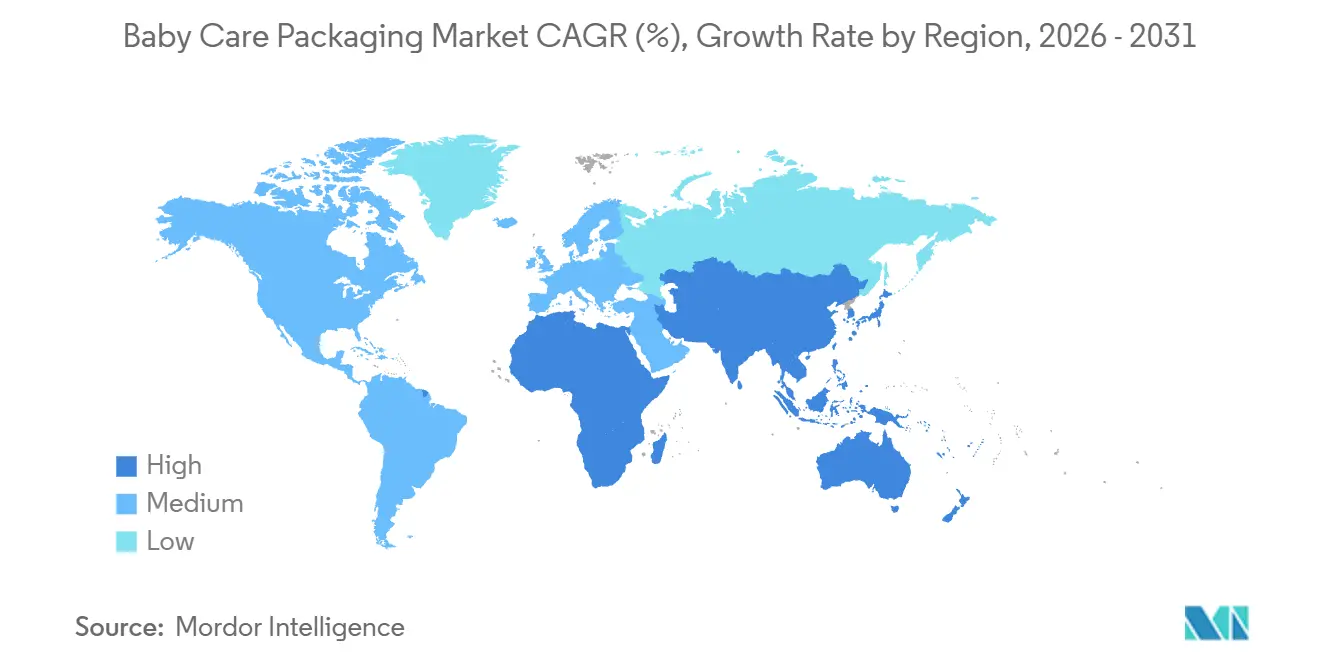

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Baby Care Packaging Market Analysis by Mordor Intelligence

The baby care packaging market size is projected to expand from USD 18.11 billion in 2025 and USD 19.03 billion in 2026 to USD 25.19 billion by 2031, registering a CAGR of 5.78% between 2026 to 2031. Accelerating e-commerce penetration, regulatory moves restricting bisphenol compounds in food-contact plastics, and premiumization in emerging economies are widening the addressable market for tamper-evident, child-safe packs. Structural shifts toward on-the-go consumption, smartphone-enabled subscription buying, and middle-class trading-up are steering converters toward spout pouches, lightweight mono-material films, and refill-ready dispensers. Brand owners are prioritizing formats that survive last-mile delivery tests, photograph well for thumbnail merchandising, and comply with tightening Extended Producer Responsibility targets. Competitive focus is therefore tilting toward value-added closures, barrier innovations that remove bisphenols, and supply-chain resilience for food-grade bio-resins.

Key Report Takeaways

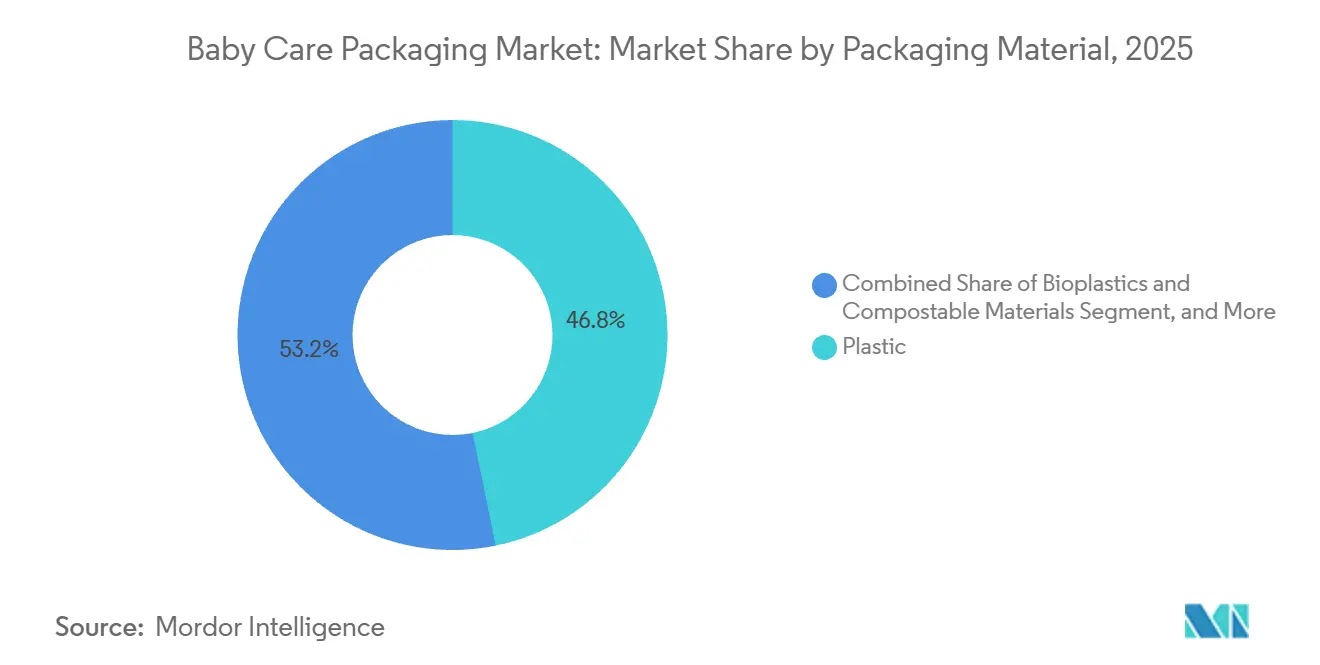

- By packaging material, plastic led with 46.78% of baby care packaging market share in 2025, while bioplastics and compostable materials are projected to expand at 7.11% CAGR through 2031.

- By packaging format, pouches and sachets accounted for 34.42% of the baby care packaging market size in 2025 and are growing at 6.35% annually.

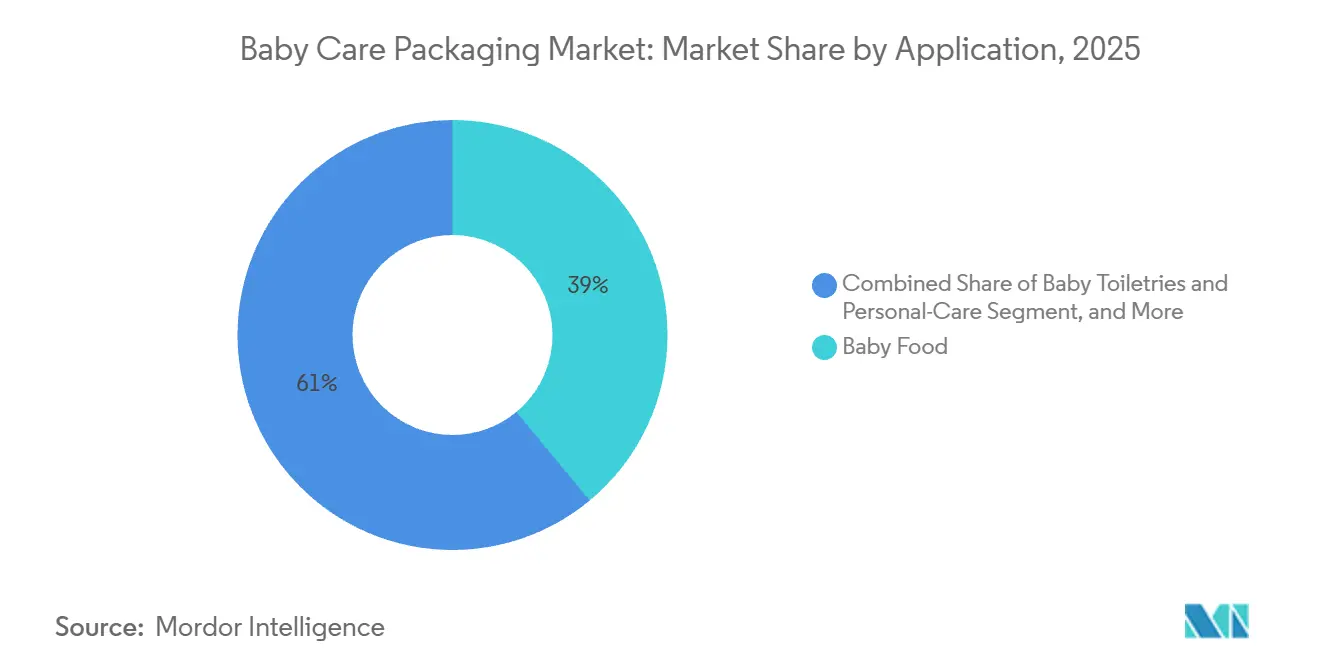

- By application, baby toiletries and personal care registered the highest projected growth, advancing at 6.72% CAGR to 2031, whereas baby food retained the largest 38.98% revenue share in 2025.

- By packaging type, flexible packaging captured 56.87% share of the baby care packaging market size in 2025 and is set to rise at 6.49% CAGR.

- By geography, Asia-Pacific dominated with 39.89% revenue share in 2025, yet the Middle East and Africa region is forecast to log the fastest 7.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Baby Care Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Convenient On-The-Go Packs | +1.2% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Growth in E-Commerce Distribution for Baby Products | +1.4% | Global, led by North America, Europe, China, and India | Short term (≤ 2 years) |

| Increasing Birth Rates and Middle-Class Spending in Emerging Economies | +1.1% | Asia-Pacific (India, Southeast Asia), Middle East and Africa, South America | Long term (≥ 4 years) |

| Regulatory Push for Tamper-Evident and Safety Features | +0.9% | North America and Europe, with spillover to Asia-Pacific and Middle East | Medium term (2-4 years) |

| Adoption of Spout-Cap Pouches Enabling Infant Self-Feeding | +0.7% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Integration of Smart Inks and QR Codes for Caregiver Education | +0.5% | North America, Europe, and premium segments in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Convenient On-The-Go Packs

Caregiver time scarcity has turned single-serve, resealable packs into necessities rather than luxuries. A 2024 consumer survey showed that convenience-oriented baby products grew 2.7 times faster than standard equivalents despite 15-30% price premiums. Spout pouches with tamper bands and flip-top closures now outperform rigid jars because they weigh less, survive drops, and slip into diaper bags. Aptar’s Quick Flip fitment, launched in October 2025, added a self-sealing valve that prevents product buildup, resolving hygiene concerns that once limited pouch uptake.[1]“Quick Flip Flexible Fitment Closure,” Aptar, aptar.com Airless pump dispensers for lotions echo the trend by allowing caregivers to dispense with one hand while keeping formulas preservative-free. Collectively, these designs reinforce portability, dosing precision, and product integrity, expanding repeat sales through parental loyalty.

Growth in E-Commerce Distribution for Baby Products

Online channels already account for about 20% of baby-product retail sales across ASEAN, aided by 88% smartphone penetration that will reach 90% by 2026. E-commerce shipping stresses packaging; ISTA-6 drop tests, leak-proof closures, and thumbnail-ready graphics are new baselines. Aptar’s Future disc-top closure, launched in February 2024, locks during transit yet remains fully recyclable, cutting damage claims in beauty and baby toiletries. QR codes embedded on labels drive caregivers to ingredient transparency portals and how-to videos, converting packs into interactive brand tools. Digital-first millennial parents thus reward converters that merge durability, convenience, and data connectivity.

Increasing Birth Rates and Middle-Class Spending in Emerging Economies

Demographic and income tailwinds in India, Southeast Asia, and the Gulf raise demand for premium, branded packages that assure hygiene and authenticity. India’s organized retail boom in tier-2 and tier-3 cities is pushing tamper-evident, shelf-stable packs compliant with national food safety codes. China’s three-child policy, supported by tax incentives through 2025, stabilized infant-formula volume despite broader aging trends. Gulf Cooperation Council grants and retail-modernization projects shift consumption from open souks to climate-controlled malls, elevating expectations for branded, tamper-proof packs that convey quality. Rising disposable income lets households trade up from bulk formats to single-serve pouches and refillable pump systems, compounding volume and value growth.

Regulatory Push for Tamper-Evident and Safety Features

Regulators have tightened chemical limits and mandated child-resistant, tamper-evident closures. EFSA slashed the tolerable daily intake for bisphenol A in April 2023, effective January 2025, forcing reformulation of polycarbonate bottles and epoxy can linings.[2]“Bisphenol A: EFSA updates risk assessment,” European Food Safety Authority, efsa.europa.eu The U.S. FDA’s 2024 guidance expanded migration testing to cover nanomaterials and PFAS in barrier coatings. Virospack’s ISO-certified push-and-turn dropper for baby healthcare demonstrates how converters blend adult usability with child-resistant features. Tamper-band tear strips and induction seals are now non-negotiable in infant formula and baby food, ensuring both compliance and caregiver confidence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Plastic Resin and Paperboard Prices | -0.8% | Global, with acute pressure in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Stringent Bans and Taxes on Single-Use Plastics | -0.6% | Europe, North America, and select Asia-Pacific markets (India, Thailand) | Medium term (2-4 years) |

| Rise of Refillable / Reusable Baby-Care Containers | -0.4% | North America and Europe, with early trials in urban Asia-Pacific | Long term (≥ 4 years) |

| Supply-Chain Instability for Food-Grade Bio-Resins | -0.3% | Global, with bottlenecks in Asia-Pacific and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Plastic Resin and Paperboard Prices

Double-digit swings in polyethylene and polypropylene spot prices during early 2026 squeezed converter margins and forced annual contract renegotiations.[3]“Packaging Materials Update Q1 2026,” Berlin Packaging, berlinpackaging.com Paperboard pricing also remained elevated due to pulp scarcity and high European energy costs. Smaller converters lack hedging tools, leading to exits or consolidations that tighten supply options for brands. Baby care packs can account for up to 25% of landed product cost, so resin shocks can compress brand margins or raise shelf prices, eroding volume in price-sensitive segments. The uncertainty complicates inventory planning, especially for brands juggling multiple regional SKUs to meet varying safety regulations.

Stringent Bans and Taxes on Single-Use Plastics

Extended Producer Responsibility laws in six U.S. states levy eco-modulation fees on multilayer pouches, pushing converters toward mono-material polyethylene or recyclable paper-based laminates. The European Union widened its Single-Use Plastics Directive in 2024 to demand that real-world recycling exist at scale, not just technical recyclability. India’s 2024 Plastic Waste Management Rules added recycled-content quotas and format bans, forcing multinationals to manage fragmented SKUs. These overlapping mandates restrict design latitude, elevating compliance costs and occasionally downgrading barrier performance, especially for moisture-sensitive infant formula. Brands that cannot reconcile safety, functionality, and recyclability fall back on exemptions or pay higher fees, undercutting sustainability claims.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Material: Bioplastics Gain Despite Barrier Challenges

Plastic retained 46.78% revenue share in 2025, reflecting its cost-to-performance edge for bottles, closures, and films across the baby care packaging market. Polyethylene and polypropylene dominate spout pouches, while PET suits transparent bottles that showcase product color. Nonetheless, bioplastics, especially polylactic acid and polyhydroxyalkanoate, are on track for 7.11% CAGR through 2031 as brands chase fossil-carbon reductions and align with single-use plastic taxes. Supply scarcity and weaker moisture barriers slow adoption, yet early commercial runs in baby wipes overwraps hint at future scaling. Paperboard stands in the mid-20s share, buoyed by formula cartons and diaper boxes that now sport water-based barrier coatings to resist grease. Glass remains niche, signaling purity in premium organic puree jars, whereas metal tubes persist in ointments that need 100% light and oxygen exclusion. Material choices are fragmenting as converters juggle inventory for fossil, bio, and fiber substrates, raising qualification workloads for regulatory testing.

Second-generation enzymes that depolymerize PET into monomers and large-scale mechanical recycling streams for high-density polyethylene closures are lowering life-cycle emissions, but certification costs remain high. Brands are piloting closed-loop take-back schemes to secure post-consumer feedstock, anchoring the baby care packaging market in circular-economy narratives. The tension between performance, cost, and recyclability continues to drive co-development between resin suppliers and converters.

By Packaging Type: Pouches Dominate Flexible Growth

Pouches and sachets commanded 34.42% of baby care packaging market share in 2025 and will ride a 6.35% CAGR as spout-cap technology makes toddler self-feeding spill-safe. Their lighter weight slashes freight emissions by up to 70% compared with glass jars, resonating with carbon-reporting targets. Rigid bottles and jars still account for a high-20s share because parents equate solidity with safety, especially in powdered formula canisters that need high moisture and oxygen barriers. Yet EPR fees and lightweighting targets erode their cost advantages. Aerosol cans and collapsible metal tubes stay niche, reserved for diaper-rash sprays and targeted creams where dosing accuracy commands a premium. Caps and closures, once an afterthought, now anchor differentiation; Aptar’s NEO closure blends tamper bands, precise dosing, and post-consumer recycled resin, condensing multipiece assemblies into a single mould.

Fast-cure water-based inks enable high-definition graphics that survive retort, vital for thumbnail imagery on e-commerce storefronts. Meanwhile, soluble barrier-coating breakthroughs point toward paper-based pouches that could encroach on flexible plastic volumes, although migration testing for fatty foods remains unresolved. Format convergence is unlikely; instead, brands will deploy a mix of rigid and flexible packs, each tuned to channel and product requirements within the baby care packaging market.

By Application: Toiletries Outpace Food on Refill Momentum

Baby food delivered 38.98% of market share in 2025 thanks to high purchase frequency and strict traceability rules that mandate tamper evidence. Growth, however, is tempering as birth rates plateau in developed economies and private-label purees proliferate. Baby drinks and formula maintain a mid-20s share anchored by moisture-sensitive powders and shelf-stable liquid bottles that demand multilayer foil laminates, adding complexity under recyclability rules. Baby toiletries and personal care are projected to be the fastest-growing category, with a 6.72% CAGR, propelled by refill stations and airless pumps that prolong formulation life without preservatives. Lifecycle assessments show 40% pack-weight cuts after the first refill, allowing brands to meet carbon pledges with minimal consumer behavior change. Baby healthcare packets, OTC drops, oral rehydration sachets, and dermal ointment tubes occupy a low-teens niche yet require ISO-8 cleanroom production, creating higher entry barriers.

Apparel and accessory packaging is pivoting from polybags to compostable mailers in response to fashion industry pledges. Refill adoption brings reverse logistics headaches and hygiene verification tasks, but loyalty benefits appear to offset the complexity. For food products, spout-pouch safety pins technology and UV-cured inside coatings aim to extend shelf life in ambient conditions, hinting at future cross-pollination between food and personal-care package designs.

By Packaging Format: Flexible Formats Lead Lightweighting

Flexible packs held 56.87% of the baby care packaging market size in 2025 and will march forward at a 6.49% CAGR as lightweighting economics and e-commerce compatibility trump the recyclability challenges of multilayer films. Brands are rapidly shifting from polyethylene-aluminum structures to mono-material polyethylene pouches that pass How2Recycle Store Drop-Off protocols, sacrificing some oxygen barrier but dodging EPR fees. Rigid formats cling to a 43% share by leveraging thin-wall injection molding and blow-fill-seal bottle technology that removes caps entirely for ready-to-feed formulas. Rigid’s heft conveys premium cues and withstands thermal abuse in hot climates, a selling point in emerging markets with limited cold chains.

Hybrid solutions, such as stand-up pouch refills coupled with reusable PET dispensers, blur type boundaries while optimizing total material use. Automated filling lines now switch between flexible and rigid SKUs with minimal downtime, letting converters hedge against demand swings. Future gains in chemical recycling could equalize end-of-life outcomes, but today the strategic calculus still favors flexibles for freight-intensive e-commerce channels within the baby care packaging market.

Geography Analysis

Asia-Pacific, with 39.89% of the baby care packaging market share in 2025, benefits from large birth cohorts, expanding middle classes, and modern trade penetration. China’s three-child incentives and India’s tier-2 city retail boom both call for tamper-proof, shelf-stable packs that comply with local food-safety statutes. Smartphone-based subscription models in Indonesia, Vietnam, and the Philippines accelerate the adoption of flexible-pack products, while Japanese caregivers favor precision-dosing pumps that cut waste.

North America held a high-20s share, underpinned by premium positioning, high e-commerce penetration, and strict FDA guidance on child-resistant packaging, which favors converters with deep compliance labs. Brands rapidly test mono-material films to avoid EPR eco-fees, yet gaps in recycling infrastructure still challenge multilayer pouches. In Europe, a mid-20s share relies on leadership in fiber pouches and bio-resins, but stagnant birth rates and aggressive plastic levies squeeze margins, sparking joint ventures to pilot paper-based spout pouches that may reset format economics.

The Middle East and Africa region is forecast to post a 7.24% CAGR, the fastest globally. Gulf-natalist grants, retail modernization programs, and rapid urbanization drive demand for branded baby packs that signal safety in air-conditioned malls. Rural Africa remains price-sensitive, sustaining sachet economies, yet multinationals still introduce tamper-banded caps to build trust. South America commands a low-teens share; Brazil and Argentina lead but wrestle with currency volatility and import tariffs that buoy local converters. Refillable lotion dispensers and compostable wipes show early traction in São Paulo and Buenos Aires, aligning consumer eco-concerns with affordability.

Competitive Landscape

The market is fragmented, with Amcor, Mondi, Huhtamaki, Tetra Pak, and others operating. These incumbents pivot from volume to value by investing in child-resistant closures, tamper-bands, and mono-material pouches that satisfy EPR mandates without sacrificing barrier performance. Aptar exemplifies the move with its NEO closure, which fuses dosing precision and tamper evidence, trimming multi-part assemblies, and streamlining recycling.

Regional specialists exploit bio-resin niches, smart-packaging features, QR traceability, and embedded freshness indicators to win premium orders despite their smaller scale. Material recovery innovators such as Ridwell and Rabbit Recycling partner with brands to collect hard-to-recycle pouches, creating closed-loop stories that resonate with millennial parents. Supply-chain headaches for bio-resins, however, curb immediate scaling, compelling converters to dual-source fossil and bio substrates that complicate operations and messaging.

Regulatory compliance is emerging as a moat. EFSA’s severe bisphenol limits, effective 2025, advantaged players owning toxicology labs and in-house migration testing. Meanwhile, mid-tier firms lacking mono-material know-how or lightweighting capital saw their shares erode as EPR fees widened cost gaps. Machine-learning sortation lines at recycling facilities now capture small closures, making design-for-recycling certifications a future differentiator.

Baby Care Packaging Industry Leaders

Sonoco Products Company

Amcor PLC

Huhtamaki Oyj

Mondi plc

Tetra Laval International S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Aptar introduced the Future disc-top closure for baby toiletries, offering 100% polyethylene mono-material, ISTA-6 e-commerce compliance, and Class A RecyClass grading.

- December 2025: Aptar unveiled fully recyclable disc-top closures targeting circular beauty and baby-care lines, signaling an innovation focus on sustainability.

- October 2025: Aptar released Quick Flip pouch fitment integrating SimpliSqueeze valves and tamper-evident bands for controlled baby food dispensing.

- October 2025: Aptar debuted the Squeeze and Turn child-resistant cap, tested to ISTA-6 and compatible with post-consumer recycled resin.

Global Baby Care Packaging Market Report Scope

Baby care packaging is used for baby products. In the material, plastic is one of the most used packaging materials due to its lightweight nature, which makes it easy to carry products. The baby food industry accounts for a major share of the baby care packaging industry. Moreover, stand-up pouches with sprouts are also popular because they make it easy to squeeze the baby food and help avoid waste.

The Baby Care Packaging Market Report is Segmented by Packaging Material (Plastic, Paper and Paperboard, Glass, Metal, and Bioplastics and Compostable Materials), Packaging Type (Bottles and Jars, Pouches and Sachets, Cans, Tubes and Sticks, Caps, and Closures and Labels), Application (Baby Food, Baby Drinks and Formula, Baby Toiletries and Personal Care, Baby Healthcare/OTC, and Baby Apparel and Accessories), Packaging Format (Flexible, and Rigid), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Plastic |

| Paper and Paperboard |

| Glass |

| Metal |

| Bioplastics and Compostable Materials |

| Bottles and Jars |

| Pouches and Sachets |

| Cans |

| Tubes and Sticks |

| Caps, Closures and Labels |

| Baby Food |

| Baby Drinks and Formula |

| Baby Toiletries and Personal-Care |

| Baby Healthcare / OTC |

| Baby Apparel and Accessories |

| Flexible |

| Rigid |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Packaging Material | Plastic | ||

| Paper and Paperboard | |||

| Glass | |||

| Metal | |||

| Bioplastics and Compostable Materials | |||

| By Packaging Type | Bottles and Jars | ||

| Pouches and Sachets | |||

| Cans | |||

| Tubes and Sticks | |||

| Caps, Closures and Labels | |||

| By Application | Baby Food | ||

| Baby Drinks and Formula | |||

| Baby Toiletries and Personal-Care | |||

| Baby Healthcare / OTC | |||

| Baby Apparel and Accessories | |||

| By Packaging Format | Flexible | ||

| Rigid | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How fast is the baby care packaging market expected to grow through 2031?

It is projected to advance at 5.78% CAGR from 2026 to 2031, moving from USD 19.03 billion in 2026 to USD 25.19 billion by 2031.

Which packaging format is expanding the quickest?

Pouches and sachets are growing at 6.35% per year thanks to spout-cap innovations that support toddler self-feeding.

What material shift is most pronounced in baby packs?

Bioplastics such as polylactic acid and polyhydroxyalkanoate are forecast to grow at 7.11% CAGR, outpacing conventional plastics despite supply constraints.

Why is the Middle East and Africa region a focus market?

Natalist incentives, mall-based retail expansion, and urbanization are driving a robust 7.24% CAGR for baby care packaging demand in the region.

Which regulatory trend most influences design today?

Stricter bisphenol limits and EPR eco-fees are compelling converters to adopt mono-material, tamper-evident constructions that pass real-world recyclability tests.

Page last updated on: