Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.61 Billion |

| Market Size (2026) | USD 4.85 Billion |

| Market Size (2031) | USD 6.26 Billion |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Personal Care Packaging Market Analysis by Mordor Intelligence

The US Personal Care Packaging Market size was valued at USD 4.61 billion in 2025 and estimated to grow from USD 4.85 billion in 2026 to reach USD 6.26 billion by 2031, at a CAGR of 5.24% during the forecast period (2026-2031). Persistent PFAS phase-outs, mounting sustainability mandates and the social-media driven quest for eye-catching packs are reshaping material selection and design philosophies. Tight state rules Minnesota’s 2025 ban on intentionally added PFAS in cosmetics among them push converters to explore new barrier chemistries and upgrade recycling infrastructure.[1]Minnesota Pollution Control Agency, “2025 PFAS Prohibitions,” pca.state.mn.us Regional spending patterns amplify these shifts: households in the West devote USD 1,038 each year to personal-care items, well above the USD 908 national average, which explains the region’s early uptake of premium, sustainable formats. Brand owners also intensify vertical integration to lock in packaging innovation capacity, a trend underscored by Amcor’s all-stock combination with Berry Global in April 2025, expected to generate USD 650 million in synergies and more than USD 3 billion in cash flow by 2028. Together, these forces support steady value growth, SKU proliferation and rising demand for refill-ready designs across the US personal care packaging market.

Key Report Takeaways

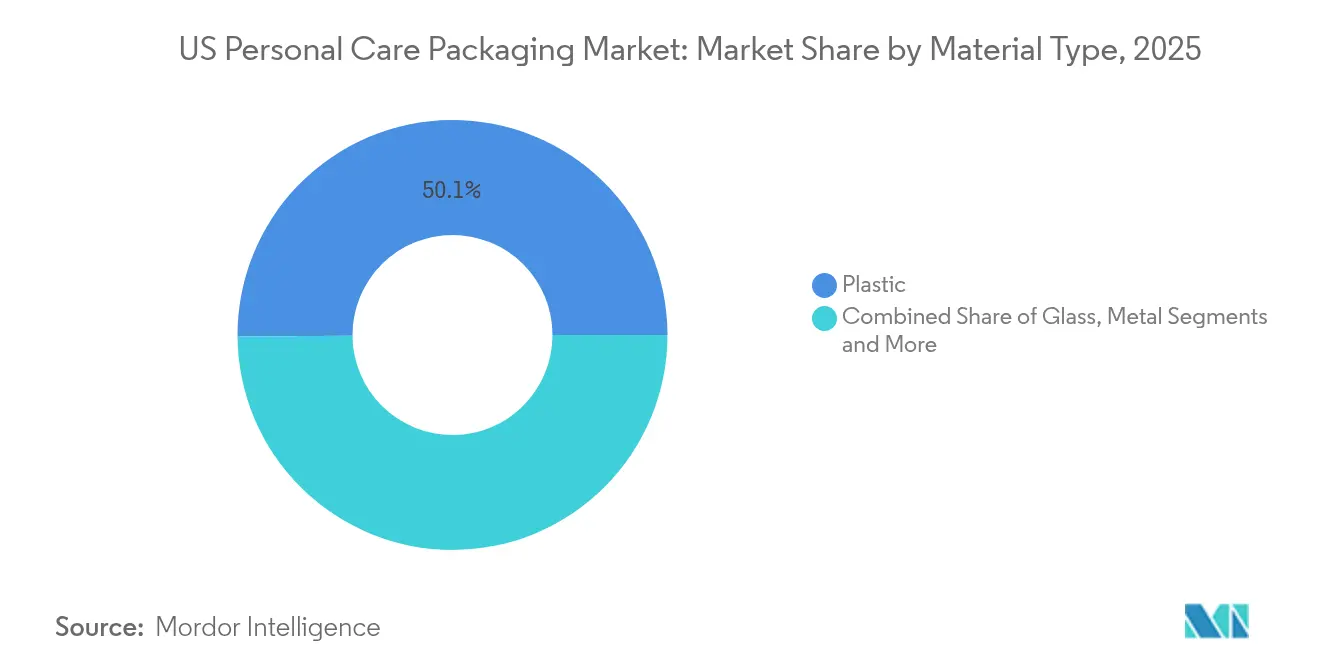

- By material type, plastic held 50.12% US personal care packaging market share in 2025; paper and paperboard is projected to rise at a 9.12% CAGR through 2031.

- By product type, bottles captured 37.65% of the US personal care packaging market size in 2025, while pouches are expected to climb at an 10.78% CAGR.

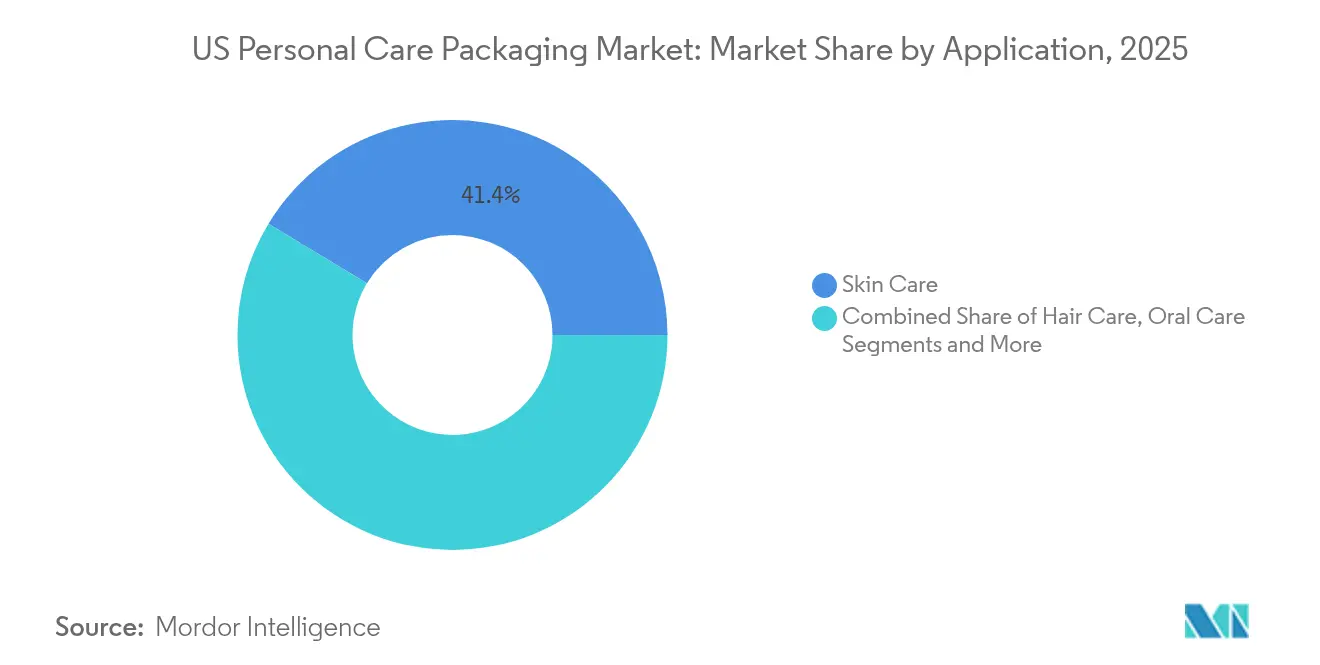

- By application, skin care accounted for 41.35% of the US personal care packaging market size in 2025; sun care is advancing at a 8.66% CAGR between 2026 and 2031.

- By sustainability attribute, recyclable mono-material packs represented 46.42% of the market in 2025; refillable/reusable systems are forecast to post a 12.35% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Personal Care Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Disposable Income Fuels Pack Demand | +1.2% | National, most pronounced in the West and Northeast | Medium term (2-4 years) |

| Instagram-Ready Aesthetics Accelerate Premiumization | +0.8% | Nationwide, especially in large urban centers | Short term (≤ 2 years) |

| E-commerce Drives Ship-Ready Protective Formats | +1.0% | Country-wide, with early traction in the West and South | Short term (≤ 2 years) |

| Subscription and Refill Models Favor Durable Solutions | +0.6% | National, led by premium-price segments | Long term (≥ 4 years) |

| Growth in TSA-size travel packs for on-the-go consumers | +0.4% | Nationwide, strongest around major airports | Medium term (2-4 years) |

| Smart/IoT-enabled packs enhance engagement and traceability | +0.3% | Nationwide, skewed toward tech-savvy demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income Fuels Pack Demand

Personal-care outlays reached USD 908 per household in 2024 and climb even higher in the West, where annual spending averaged USD 1,038.[2]U.S. Bureau of Labor Statistics, “Consumer Expenditures Selected Areas, 2022–23,” bls.gov Steady wage gains translate into greater SKU variety, premium pack finishes and niche formulations, which in turn boost unit-volume requirements across the US personal care packaging market. Glass and metal formats benefit the most because consumers associate them with quality and sustainability.

Instagram-Ready Aesthetics Accelerate Premiumization

Design now doubles as a marketing channel, prompting brands to invest in striking shapes, embossing and custom colorways that photograph well. Glass jars and brushed-aluminum aerosols outperform conventional HDPE bottles because they align with eco-messaging and visual storytelling on social platforms. L’Oréal’s partnership with IBM to train AI on sustainable formulations underscores how tech convergence supports both look and function.[3]Beauty Packaging Staff, “L’Oréal & IBM to Build First AI Model for Sustainable Cosmetics,” beautypackaging.com

E-commerce Drives Ship-Ready Protective Formats

Direct-to-consumer channels require packs that survive long parcel journeys yet deliver an engaging unboxing moment. Reinforced pouches, inverted tubes and tamper-evident pumps address leak, crush and pilfer concerns without inflating freight costs. Brands that master tight cube utilization and mono-material secondary packs cut emissions and shipping fees while winning repeat purchases.

Subscription and Refill Models Favor Durable Solutions

Recurring delivery programs encourage investment in sturdier containers, notably aluminum and glass, which withstand repeated cycles. Ball Corporation’s collaboration with Meadow on fully recyclable aluminum cans highlights the pivot toward closed-loop durability.[4]Ball Corporation, “Ball and Meadow to Produce Fully Recyclable Aluminium Cans,” packagingeurope.com Smart tags embedded in refill cartridges also trigger automatic reorders, deepening brand loyalty.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High R&D and Tooling Costs Limit Innovation | -0.9% | Nationwide, hitting smaller producers hardest | Medium term (2-4 years) |

| State-Level PFAS Rules Add Compliance Burden | -0.7% | Nationwide, but rules vary by state | Short term (≤ 2 years) |

| Fluctuating recycled-resin prices and inconsistent quality | -0.5% | Nationwide, with manufacturing hubs most exposed | Short term (≤ 2 years) |

| Reverse-logistics hurdles for refill and return programs | -0.4% | Nationwide, eased somewhat in dense urban areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High R&D and Tooling Costs Limit Innovation

Developing a new blow-mold or precision pump can exceed USD 1 million per line. Small converters struggle to fund multiple trials, particularly when bio-based resins demand specialized machinery and extended qualification. Patent filings for collapsible applicators illustrate the complexity as well as the capital intensity behind differentiated dispensing technology.

State-Level PFAS Rules Add Compliance Burden

California’s SB682 bans PFAS in many consumer products beginning in 2027. In parallel, the FDA withdrew 35 food-contact PFAS notifications in 2025, raising uncertainty for analogous personal-care uses. Maintaining multiple resin blends and barrier coatings for each state erodes supply-chain efficiency and inflates testing costs, slowing the overall growth of the US personal care packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Plastic Holds Ground as Paper Gains Pace

Plastic retained 50.12% US personal care packaging market share in 2025 thanks to low cost, design flexibility and well-established supply chains. Yet the paper and paperboard segment is projected to log a 9.12% CAGR through 2031, buoyed by PFAS crackdowns and consumer favor for renewable substrates. Brands experiment with barrier-coated cartons and molded-fiber jars that pass moisture tests without compromising shelf appeal. Recycled PET integration and pilot chemical recycling plants help plastics defend their lead by easing circularity concerns.

Circular-economy policies push converters to raise post-consumer-resin (PCR) content and build take-back schemes. Simultaneously, glass and metal profit from luxury positioning: prestige skin-care labels deploy heavy-walled flacons and brushed-aluminum sticks to justify price premiums while touting infinite recyclability. Material innovation is also spurred by vertical integration, exemplified by Amcor’s resin-sourcing investments that safeguard PCR supply for the expanding US personal care packaging market.

By Product Type: Bottles Rule but Pouches Accelerate

Bottles commanded 37.65% of the US personal care packaging market size in 2025 due to familiarity, shelf impact and versatility across lotions, shampoos and body washes. However, flexible pouches are projected to log an 10.78% CAGR, propelled by e-commerce cube-efficiency and lower material usage. Reclosable spouts and stand-up formats bolster consumer convenience, while ultra-thin films curb shipping weight.

Tubes, sticks and precision pumps cater to targeted applications think SPF sticks for sun-care or airless pumps for retinol serums where dosing accuracy matters more than unit cost. Folding cartons gain ground as brands migrate to mono-material paper solutions that simplify curbside recycling. Across all formats, NFC chips and QR codes elevate packs into engagement hubs, a key differentiator in the crowded US personal care packaging market.

By Application: Skin Care Dominant, Sun Care Fastest

Skin-care lines accounted for 41.35% of the US personal care packaging market size in 2025, reflecting category maturity, regimen layering and broad age appeal. Jar-in-box sets, UV-protective frosted glass and airless pumps maintain high throughput across co-packers. Meanwhile, sun-care is forecast to grow at a 8.66% CAGR as outdoor recreation rebounds and broad-spectrum claims proliferate. Lightweight, sachet-style minis also fuel trial purchases.

Hair-care holds steady with pouch-based refill programs and oversized pump bottles, both designed to cut plastic intensity per use. Oral-care and color cosmetics innovate through recyclable tube-heads and refillable palettes, respectively. Each niche spurs bespoke barrier and dispensing needs, keeping the US personal care packaging market diversified.

By Sustainability Attribute: Recyclable Leads, Refillable Surges

Recyclable mono-materials held a 46.42% share in 2025 as extended-producer-responsibility laws reward designs that flow into existing MRFs. Converters chase drop-in barriers that omit PFAS yet preserve shelf life, ensuring these solutions scale quickly. In parallel, refillable systems are poised for a 12.35% CAGR. Aluminum deodorant shells and glass serum bottles paired with PCR PET refill pods illustrate how luxury aesthetics mesh with waste-reduction goals.

Post-consumer-recycled content faces feedstock gaps, but chemical depolymerization projects around the Gulf Coast promise future supply security. Compostable PLA or PHA films remain niche, mainly due to cost and limited municipal infrastructure, yet ongoing R&D hints at broader adoption post-2030. Such momentum underlines the long-term evolution trajectory of the US personal care packaging market.

Geography Analysis

The South accounted for 35.74% of US personal care packaging market share in 2025, supported by favorable labor costs, robust resin supply lines along the Gulf Coast and a sprawling consumer base stretching from Texas to Florida. Migration into Sun Belt metros sustains household formation and, by extension, demand for value-priced personal-care SKUs, reinforcing high-volume bottle and closure demand in the region.

The West is the fastest-growing regional cluster with a 7.45% CAGR through 2031. Elevated household incomes, averaging USD 1,038 spent annually on personal-care products, fuel willingness to pay for low-impact packs, including molded-fiber jars and elegantly frosted glass bottles. California’s sweeping EPR statutes and PFAS bans further nudge brands toward advanced mono-material laminates and chemical-free barrier layers. Silicon Valley’s tech culture also accelerates adoption of QR-enabled recycling guidance and refill-tracking apps that sync seamlessly with subscription models, magnifying the region’s influence on nationwide packaging trends.

The Northeast and Midwest maintain steady but moderate expansion. Affluent coastal cities such as New York and Boston underpin demand for prestige packs, whereas the Midwest leverages cost-competitive land and a skilled workforce to attract large-scale capital projects like Kimberly-Clark’s USD 2 billion manufacturing upgrade across Ohio and South Carolina. Both regions benefit from logistical proximity to key FMCG brand owners, streamlining package-to-shelf times and tempering freight emissions for the broader US personal care packaging market.

Competitive Landscape

The market exhibits moderate consolidation, with the combined Amcor–Berry Global entity now commanding a formidable footprint across bottles, closures and flexible laminates. Synergy capture of USD 650 million over three years will enhance its bargaining power with resin suppliers and technology licensors. Meanwhile, TricorBraun’s 2025 purchase of Veritiv Containers broadened its North American distribution network and fortified service levels for mid-sized beauty brands.

Technology adoption stands out as a differentiator. AptarGroup deploys AI-enabled vision systems to certify 100% closure integrity, while Silgan’s smart-dispense pumps embed RFID tags to monitor fill volumes and authenticate refills at point of sale. Smaller specialists such as Virospack leverage niche expertise in droppers and luxury glass to win high-margin orders following its January 2025 stake in Eurovetrocap.

Sustainability credentials also dictate share gains. Amcor has pledged to incorporate 30% recycled content across global operations by 2030 and published a detailed decarbonization roadmap outlining scope-1, -2 and -3 targets. Localized PCR sourcing, bio-based varnishes and lightweighting programs are now table stakes rather than differentiators, pressuring laggards and energizing innovators throughout the US personal care packaging market.

US Personal Care Packaging Industry Leaders

HCP Packaging Co. Ltd

Silgan Holdings Inc.

Berry Global Group, Inc.

Albea Services SA

APC Packaging

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Unilever acquired Dr. Squatch to deepen its men’s grooming footprint and scale a high-growth direct-to-consumer model.

- May 2025: Kimberly-Clark unveiled a USD 2 billion US manufacturing expansion featuring AI-powered robotics and logistics upgrades.

- April 2025: Amcor finalized its all-stock merger with Berry Global, forecasting USD 3 billion in annual cash flow.

- March 2025: TricorBraun agreed to buy Veritiv Containers, adding rigid-pack distribution scale across the continent.

US Personal Care Packaging Market Report Scope

Personal care packaging plays an essential role in product marketing as it adds to the visual appeal and displays relevant information regarding the product. The report studies primary materials like plastic, paper, etc. The packaging is done for various products, such as cosmetics, shampoos, etc., where rigid plastics dominate the market due to their low price, non-corrosive, and lightweight properties.

The US personal care packaging is segmented by material type (plastic, glass, metal, and paper and paperboard), product type (bottles, tubes and sticks, pumps and dispensers, pouches, and other product types), and application (skin care, hair care, oral care, makeup products, deodorants and fragrances, and other applications). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Material Type

| Plastic |

| Glass |

| Metal |

| Paper and Paperboard |

By Product Type

| Bottles |

| Tubes and Sticks |

| Pumps and Dispensers |

| Pouches |

| Folding Cartons |

| Others |

By Application

| Skin Care |

| Hair Care |

| Oral Care |

| Makeup and Color Cosmetics |

| Deodorants and Fragrances |

| Depilatories |

| Others |

By Sustainability Attribute

| Recyclable (mono-material) |

| Post-consumer-recycled (PCR) Content |

| Refillable / Reusable |

| Compostable / Bio-based |

| By Material Type | Plastic |

| Glass | |

| Metal | |

| Paper and Paperboard | |

| By Product Type | Bottles |

| Tubes and Sticks | |

| Pumps and Dispensers | |

| Pouches | |

| Folding Cartons | |

| Others | |

| By Application | Skin Care |

| Hair Care | |

| Oral Care | |

| Makeup and Color Cosmetics | |

| Deodorants and Fragrances | |

| Depilatories | |

| Others | |

| By Sustainability Attribute | Recyclable (mono-material) |

| Post-consumer-recycled (PCR) Content | |

| Refillable / Reusable | |

| Compostable / Bio-based |

Key Questions Answered in the Report

What is the current value of the US personal care packaging market?

The market is valued at USD 4.85 billion in 2026 and is projected to grow to USD 6.26 billion by 2031.

Which material is gaining the most ground against conventional plastics?

Paper and paperboard solutions are registering a 9.12% CAGR, outpacing every other substrate due to rising PFAS bans and consumer demand for recyclable fiber packs.

Why are pouches growing faster than bottles?

Pouches optimize shipping space, use less material and fit e-commerce logistics, which drives their 10.78% CAGR through 2031.

How will state PFAS regulations influence future packaging choices?

Bans in states such as Minnesota and California are accelerating the shift toward PFAS-free barrier chemistries, forcing brands to reformulate and adopt alternative substrates sooner than planned.

What role does e-commerce play in the sector’s growth?

Online sales amplify the need for ship-ready, protective and right-sized packs, adding roughly 1 percentage point to the overall market CAGR.

Which sustainability attribute is expanding fastest?

Refillable and reusable systems are advancing at a 12.35% CAGR as subscription services and premium positioning make durable containers financially viable.

Page last updated on: