Axial Flow Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

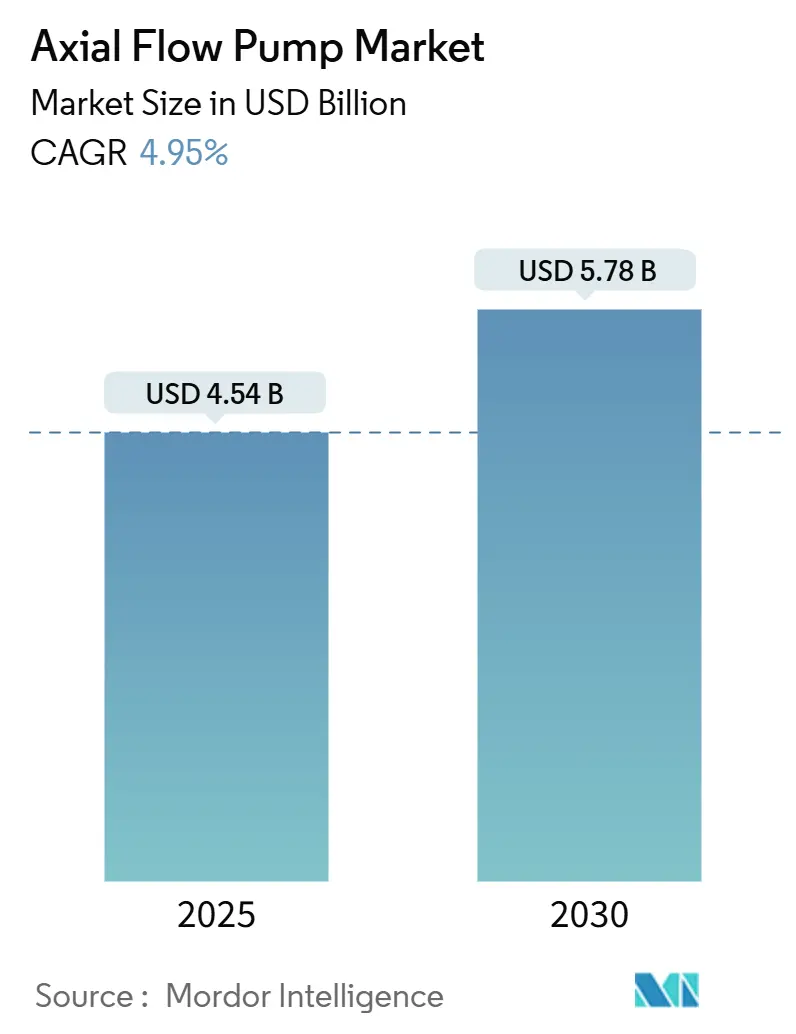

| Market Size (2025) | USD 4.54 Billion |

| Market Size (2030) | USD 5.78 Billion |

| Growth Rate (2025 - 2030) | 4.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Axial Flow Pump Market Analysis by Mordor Intelligence

The Axial Flow Pump Market size is estimated at USD 4.54 billion in 2025, and is expected to reach USD 5.78 billion by 2030, at a CAGR of 4.95% during the forecast period (2025-2030).

This healthy trajectory reflects the pump’s unique ability to move very large water volumes against low heads, which keeps demand strong from municipal water utilities, irrigated agriculture, and flood-control agencies. Governments are channeling unprecedented capital into climate-resilient water infrastructure, and most of those projects specify large-bore axial units because alternative designs struggle to match the required flow rates. Ongoing retrofits also favor the axial flow pump market as utilities pursue energy-saving upgrades that pair variable-frequency drives with real-time monitoring. Competitive intensity is rising, but established manufacturers continue to leverage materials science and digital services to protect margins in a value-driven procurement environment.

Key Report Takeaways

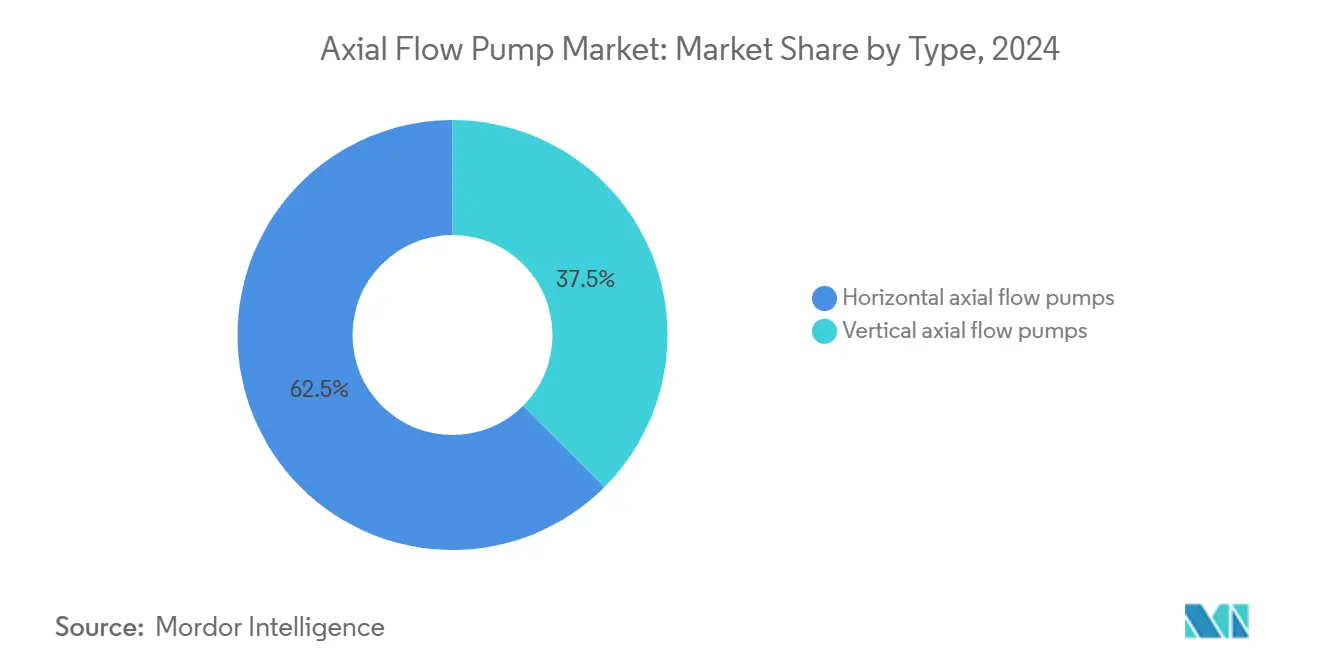

- By pump configuration, vertical units held 62.5% of the 2024 axial flow pump market share, while horizontal variants are forecast to post a 5.7% CAGR through 2030.

- By material, cast iron captured 48.0% of the 2024 axial flow pump market size, whereas stainless steel is projected to grow at a 6.0% CAGR to 2030.

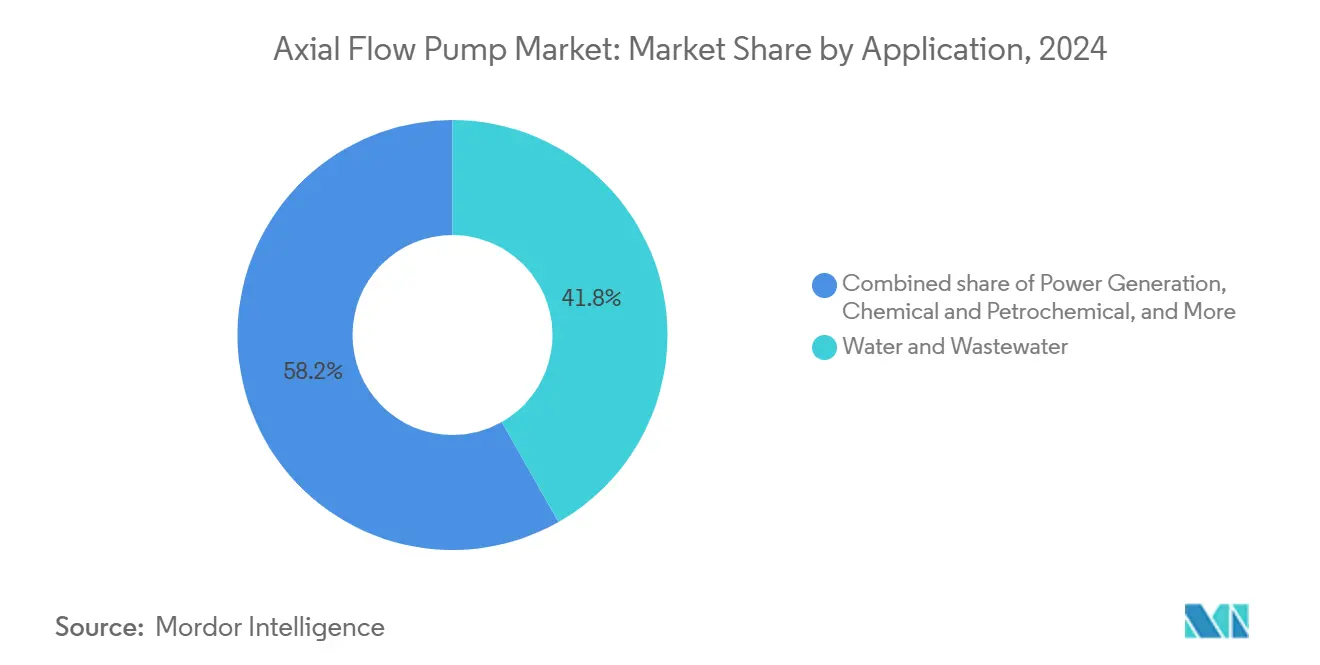

- By application, water and wastewater treatment accounted for 41.8% of the revenue in 2024; power generation is expected to expand at a 6.3% CAGR through 2030.

- By end-user, municipal buyers accounted for 55.1% of demand in 2024, while industrial facilities are projected to grow at a 5.9% CAGR through 2030.

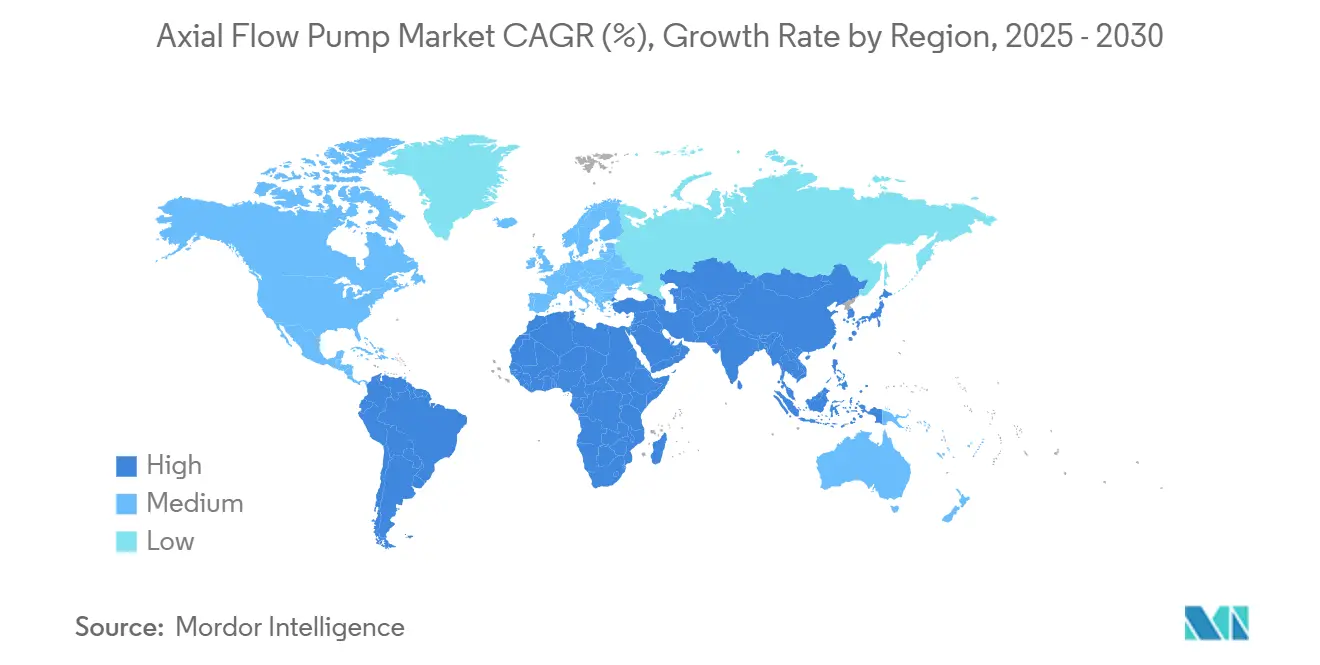

- By geography, Asia-Pacific led with 46.4% of global revenue in 2024 and is pacing for a 6.2% CAGR during the forecast period

Global Axial Flow Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating investments in water & wastewater infrastructure | 0.70% | North America, Asia-Pacific | Long term (≥ 4 years) |

| Expansion of agricultural irrigation in emerging economies | 0.60% | Asia-Pacific, MEA, South America | Medium term (2-4 years) |

| Rising demand for energy-efficient pump retrofits | 0.50% | North America, EU, Asia-Pacific | Short term (≤ 2 years) |

| Urban flood-control projects under climate-resilience programs | 0.40% | Coastal APAC & North America | Medium term (2-4 years) |

| Low-head small-hydro retrofits using axial turbines | 0.30% | North America, EU, South America | Long term (≥ 4 years) |

| Cooling loops for modular green-hydrogen electrolyzers | 0.20% | EU, North America, pilot APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Investments in Water & Wastewater Infrastructure

Municipal utilities worldwide are accelerating their capital programs, prioritizing treatment-plant upgrades and new trunk conveyance corridors. The American Water Works Association estimates that U.S. systems alone will need more than USD 1 trillion over the next two decades, a sum that directly drives large orders for high-capacity axial pumps.[1]American Water Works Association, “Buried No Longer: Confronting America’s Water Infrastructure Challenge,” awwa.org Seattle Public Utilities, for example, has earmarked USD 10 billion for modernization that incorporates hundreds of digitally monitored axial machines.[2]Seattle Public Utilities, “2024 – 2030 Capital Improvement Program,” seattle.gov Energy optimization is another catalyst, as utilities can trim their electricity bills by up to 30% when legacy pumps are replaced with variable-speed axial designs. Tighter water-quality regulations are accelerating the retirement of 1980s-era pump stations that lack the efficiency features of today. These factors combine to keep the axial flow pump market on a secular growth path through 2030.

Expansion of Agricultural Irrigation in Emerging Economies

India plans to expand irrigation coverage by 15 million ha before 2030, and similar programs are unfolding in Indonesia and Brazil.[3]Ministry of Water Resources, India, “Pradhan Mantri Krishi Sinchayee Yojana Progress Report 2025,” mowr.gov.in The axial flow pump market benefits because high-volume, low-head units are well-suited to lift canal water across sprawling command areas. Government subsidies offset upfront costs, while precision irrigation trends encourage the deployment of variable-frequency drives that allow growers to match flow to crop evapotranspiration rates. Manufacturers that pre-engineer solar-ready motor controls enjoy an advantage as farms look to integrate renewable power on remote pivots. Climate-adaptation funding further supports robust order pipelines, as resilient irrigation networks are central to national food security strategies.

Expansion of Agricultural Irrigation in Emerging Economies

India plans to expand irrigation coverage by 15 million ha before 2030, and similar programs are unfolding in Indonesia and Brazil.[4]Sulzer Ltd., “Energy Efficiency in Industrial Pumping,” sulzer.com The axial flow pump market benefits because high-volume, low-head units are well-suited to lift canal water across sprawling command areas. Government subsidies offset upfront costs, while precision irrigation trends encourage the deployment of variable-frequency drives that allow growers to match flow to crop evapotranspiration rates. Manufacturers that pre-engineer solar-ready motor controls enjoy an advantage as farms look to integrate renewable power on remote pivots. Climate-adaptation funding further supports robust order pipelines, as resilient irrigation networks are central to national food security strategies.

Rising Demand for Energy-Efficient Pump Retrofits

Industrial pumping accounts for roughly 20% of global electricity use, and energy costs are intensifying board-level focus on retrofit programs. U.S. Department of Energy rules now mandate minimum efficiency standards for most commercial and industrial pump types, and compliance deadlines are pushing forward the replacement of aging axial units. Modern designs with integrated sensors routinely cut kWh consumption by up to half, yielding payback periods of 18-36 months for plants in high-tariff regions. Utility rebate schemes—some covering 40% of upgrade costs—tilt the ROI calculation further in favor of new purchases. Because retrofits also unlock predictive-maintenance contracts, suppliers capture annuity-like service revenue that enhances lifetime customer value.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High lifecycle maintenance & corrosion costs | -0.40% | Global marine & chemical | Short term (≤ 2 years) |

| Unsuitability for high-pressure offshore duties | -0.20% | North Sea, Gulf of Mexico | Medium term (2-4 years) |

| Limited global sand-casting capacity for large SS bowls | -0.20% | Concentrated foundries | Short term (≤ 2 years) |

| Digital-twin interoperability gaps with legacy SCADA | -0.10% | North America, EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Lifecycle Maintenance & Corrosion Costs

Total cost of ownership analyses indicate that energy and maintenance account for approximately 65% of a pump’s 12-year lifecycle costs. In seawater or aggressive chemical service, corrosion can necessitate impeller replacement after just five years, and repairs often require factory refurbishment, which can cost up to 60% of the original purchase price. Remote sites compound the challenge because skilled technicians and replacement parts are scarce, lengthening downtime. Although condition-monitoring sensors help predict failures, smaller operators hesitate to invest in the necessary analytics platforms. These financial pressures can prompt buyers to consider alternative pump types or delay procurement cycles, thereby tempering near-term growth for the axial flow pump market.

Unsuitability for High-Pressure Offshore Duties

Axial hydraulics lose efficiency at pressures above roughly 70 psi, limiting applicability on deepwater platforms where process requirements exceed 1,000 psi. Subsea production systems therefore choose centrifugal or positive-displacement pumps, constraining axial sales in the lucrative offshore segment. Emerging offshore wind farms likewise require high-pressure hydraulic units for pitch control, another niche where axial designs cannot compete. As the energy transition reallocates capital toward deepwater carbon capture and CO₂ injection, axial vendors face an opportunity cost as they are sidelined from these high-value projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Horizontal Variants Gain Urban Traction

Vertical units dominated the 2024 demand, accounting for 62.5% of the axial flow pump market share, thanks to their deep-sump installation advantage in irrigation lift schemes and municipal intake towers. The configuration eliminates long suction headers, cutting civil works costs on new greenfield plants. Yet horizontal layouts are scaling rapidly at a 5.7% CAGR, particularly in retrofits where operators can slide a compact skid into an existing basement without excavating new wells. In many Asia-Pacific megacities, land scarcity favors shallow horizontal stations that tuck beneath roadways or transit lines.

Horizontal packages are increasingly shipped with factory-mounted variable-frequency drives, which simplify commissioning and ensure DOE compliance. Service crews appreciate ground-level motor access, which reduces the need for confined-space permits and turnaround time. Conversely, vertical pumps still enjoy a reliability halo in flood-control projects because their column design tolerates debris better during storm surges. As manufacturers refine hybrid semi-axial hydraulics, buyers can match performance curves more precisely to duty points, ensuring both geometries will coexist across the axial flow pump market through 2030.

By Material: Stainless Steel Rises on Corrosion Concerns

Price-competitive cast iron retained 48.0% of 2024 revenue, cementing its role in chlorinated but otherwise benign municipal water duties. Stainless steel, however, is advancing at a 6.0% CAGR on the strength of desalination, chemical, and ultra-pure water systems. Grade 316L is now the default for marine intakes because its molybdenum content resists chloride pitting, while duplex alloys are selected for high-stress hydrogen cooling loops. Bronze usage continues to shrink as alloy prices converge and procurement teams prioritize lifecycle economics over acquisition cost.

Advanced composites, such as glass-fiber-reinforced bowls, address both weight and corrosion simultaneously, but remain a small slice of the axial flow pump market because production cycles are long and field familiarity is limited. Material decisions are increasingly relying on total-cost-of-ownership models that factor in downtime, coating schedules, and energy efficiency. As hydrogen electrolyzer OEMs specify ultra-low-carbon stainless chemistries to prevent embrittlement, suppliers with metallurgical depth are positioned to command premium margins.

By Application: Power Generation Accelerates Growth

Water and wastewater treatment accounted for 41.8% of 2024 spending, yet turbine-condenser and hydrogen-cooling duties are driving the power segment at a 6.3% CAGR. Combined-cycle gas plants upgrading once-through cooling loops adopt large axial units paired with VFDs to modulate flow as ambient temperatures fluctuate. Grid-balancing pumped-storage projects double-count pumps as reversible turbines, giving the axial flow pump market a gateway into renewable capacity additions. Petrochemical operators still favor axial designs for low-head circulation in fractionation columns; however, energy-intensity targets are forcing investments in high-efficiency runners.

Agricultural irrigation maintains a sizable absolute volume, bolstered by subsidy-driven modernization in India and Vietnam. Flood-control budgets are climbing on every continent, though irregular project cycles complicate supplier forecasting. Mining retains a niche share for pit dewatering at shallow heads, where rugged construction takes precedence over peak efficiency. Across applications, buyers value life-cycle efficiency gains over headline purchase price, steering specifications toward premium designs that integrate digital diagnostics.

By End-User: Industrial Automation Drives Efficiency

Municipal authorities accounted for 55.1% of the volume in 2024, reflecting their statutory obligations to secure potable water and manage sewage systems. Procurement protocols favor qualified vendor lists, granting incumbents visible pipelines but exposing them to budget cycles. Industrial customers, growing at a 5.9% CAGR, offer higher margin potential because they purchase integrated packages that embed drives, sensors, and analytics dashboards. Process engineers in the food & beverage and specialty chemicals industries value repeatability and downtime avoidance, which aligns with predictive maintenance service plans.

Commercial buildings form a smaller slice, yet high-rise developments in the Middle East request compact horizontal axial skids for fire-water and HVAC condenser loops. OEM system integrators are also important because they bundle pumps into turnkey water-treatment containers for off-grid deployment. Across all buyer types, energy-efficiency legislation and ESG reporting frameworks are pushing total-cost-of-ownership to the forefront of decision-making, a trend that favors suppliers with digital-enabled portfolios.

Geography Analysis

The Asia-Pacific region led the global axial flow pump market with 46.4% of the market share in 2024, and is forecasted to advance at a 6.2% CAGR to 2030, as China, India, and Southeast Asia invest heavily in irrigation canals, smart city drainage schemes, and green hydrogen clusters. Large hydropower retrofits in Japan and Korea also specify axial turbines because they fit existing dam bays without major civil modifications. While the regional supply chain delivers cost advantages, stainless steel casting capacity remains tight, elongating lead times for premium projects.

North America represents a mature yet resilient demand base, anchored by USD 1 trillion in forecasted water-utility spending over the next 20 years. The axial flow pump market benefits when cities like Seattle allocate multi-billion-dollar budgets to reservoir tunnels and treatment-plant upgrades. Retrofits targeting DOE efficiency compliance keep industrial order books full, and coastal flood-control installations continue to specify super-capacity axial units.

Europe emphasizes decarbonization and circular economy objectives, spurring the replacement of legacy units with ISO 14414-certified, high-efficiency designs. Germany’s industrial sector often realizes 30-50% electricity savings after pump swaps, proving the business case. EU Green Deal financing also supports the expansion of pumped-storage hydro facilities that utilize reversible axial turbines. Digital-twin adoption leads global trends, though cybersecurity mandates extend project timelines.

Emerging prospects in South America and the Middle East & Africa revolve around agriculture, desalination, and power-plant cooling. Brazil’s irrigation expansion and Gulf desalination megaprojects prefer corrosion-resistant stainless pumps, driving above-average unit values. African water-access projects funded by multilateral banks focus on rugged, low-maintenance designs that can operate on intermittent power, creating opportunities for solar-powered axial packages.

Mordor Intelligence provides coverage of the axial flow pump market across other key regional markets, including North America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The axial flow pump market remains moderately fragmented, although recent acquisitions suggest a gradual concentration trend. Veolia’s USD 1.75 billion purchase of the remaining 30% stake in Water Technologies & Solutions accelerates its vertical-integration strategy and adds scale to its North American installed base. Xylem continues to differentiate through smart-water platforms that couple pumps with predictive analytics, reporting double-digit service revenue growth in 2024. Sulzer invested USD 10 million to expand U.S. manufacturing capacity, underscoring the strategic value of localized production when public projects stipulate domestic content.

Materials innovation is a parallel battleground. KSB’s USD 25 million Virginia expansion brings additional stainless casting furnaces online to alleviate bowl bottlenecks. Flowserve, meanwhile, secured a marquee carbon-capture contract with ADNOC, demonstrating competence in emerging energy-transition segments that demand corrosion-resistant metallurgy and stringent cleanliness. Smaller specialists exploit niches such as fish-friendly runners or hydrogen-ready alloys, while broader portfolios from ITT Goulds and WILO emphasize packaged solutions that bundle drives and controls.

Service models are evolving from break-fix toward outcome-based contracts. OEMs now guarantee uptime percentages measured by cloud dashboards, deepening customer lock-in. Because public tenders increasingly weigh total-life cost over acquisition price, suppliers that demonstrate measurable kWh savings and lower chemical dosing gain scoring advantages. Cyber-secure connectivity, backed by ISO 27001 certification, is emerging as a new differentiator in digitally mature geographies.

Axial Flow Pump Industry Leaders

Xylem Inc.

Sulzer Ltd.

KSB SE & Co. KGaA

Grundfos Holding A/S

Flowserve Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Veolia acquired CDPQ’s 30% stake in Water Technologies and Solutions for USD 1.75 billion, targeting EUR 90 million in additional cost synergies by 2027.

- January 2025: Flowserve won a contract with ADNOC to supply flow-control technology for a flagship carbon capture project, underscoring the expanding environmental role of pumps.

- January 2025: Frontier-Kemper Constructors secured a USD 1.1 billion award for New York City’s Kensico-Eastview tunnel, which will transport 2.6 billion gallons per day of water and require multiple axial pump stations.

- January 2025: A global pump OEM announced a USD 85 million U.S. manufacturing expansion to meet rising domestic demand.

Global Axial Flow Pump Market Report Scope

| Horizontal axial flow pumps |

| Vertical axial flow pumps |

| Cast Iron |

| Stainless Steel |

| Bronze |

| Others |

| Water and Wastewater |

| Agriculture and Irrigation |

| Power Generation |

| Chemical and Petrochemical |

| Oil and Gas |

| Others |

| Municipal |

| Industrial |

| Commercial |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Horizontal axial flow pumps | |

| Vertical axial flow pumps | ||

| By Material | Cast Iron | |

| Stainless Steel | ||

| Bronze | ||

| Others | ||

| By Application | Water and Wastewater | |

| Agriculture and Irrigation | ||

| Power Generation | ||

| Chemical and Petrochemical | ||

| Oil and Gas | ||

| Others | ||

| By End-user | Municipal | |

| Industrial | ||

| Commercial | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What CAGR is projected for the global axial flow pump market to 2030?

The market is expected to grow at 4.95% annually through 2030.

Which region currently leads demand for axial flow pumps?

Asia-Pacific accounts for the largest share, with 46.4% of global revenue in 2024.

Why are horizontal axial pumps gaining popularity in cities?

Their compact footprint fits existing basements, reducing excavation costs and easing maintenance access.

What material segment is growing fastest in axial pump manufacturing?

Stainless steel is expanding at a 6.0% CAGR due to its corrosion resistance in desalination and chemical duties.

How do utilities justify replacing older axial pumps?

Modern variable-speed units can cut energy use by 30-50%, yielding attractive payback periods and compliance with new efficiency standards.

Which emerging application offers new demand for axial flow designs?

Cooling loops for green-hydrogen electrolyzers require compact, corrosion-resistant axial pumps.

Page last updated on: