Automotive Steering Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

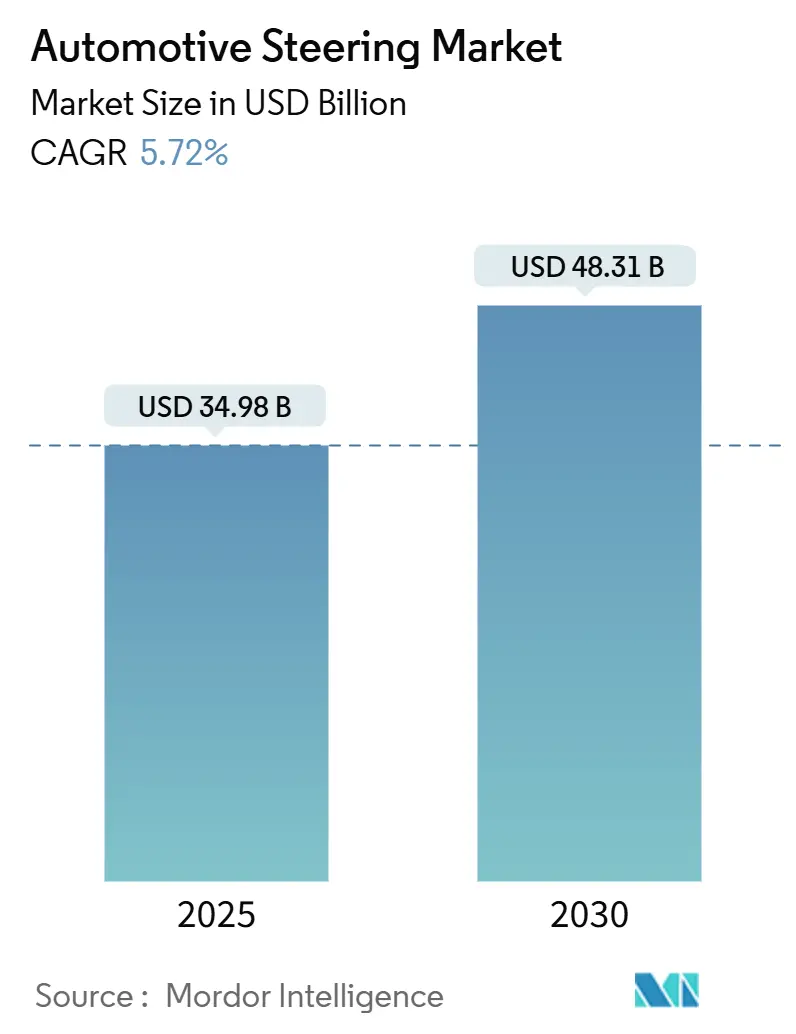

| Market Size (2025) | USD 34.98 Billion |

| Market Size (2030) | USD 48.31 Billion |

| Growth Rate (2025 - 2030) | 5.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Steering Market Analysis by Mordor Intelligence

The Automotive Steering System market is valued at USD 34.98 billion in 2025 and is forecast to reach USD 48.31 billion by 2030, reflecting a 5.72% CAGR. Growth is anchored in the rapid migration from hydraulic assistance to electronic power steering and the first commercial deployments of steer-by-wire. Tightening global emission limits and the rising share of battery-electric vehicles strengthen the business case for energy-efficient steering technologies, while cybersecurity rules under UNECE R155 accelerate demand for software-defined electronic control units[1]“Regulation No. 155 Cyber Security and Cyber Security Management Systems,”, United Nations Economic Commission for Europe, unece.org. Asia-Pacific retains a 48.67% revenue share, helped by China’s scale advantages and Japan’s specialization in high-precision components. Tier-1 suppliers are consolidating core technologies to secure intellectual property and to fund the high up-front investment needed for redundant, “fail-operational” architectures. Opportunities emerge for motor and sensor specialists that can remove rare-earth content, cut weight, and improve functional safety without inflating the bill-of-materials.

Key Report Takeaways

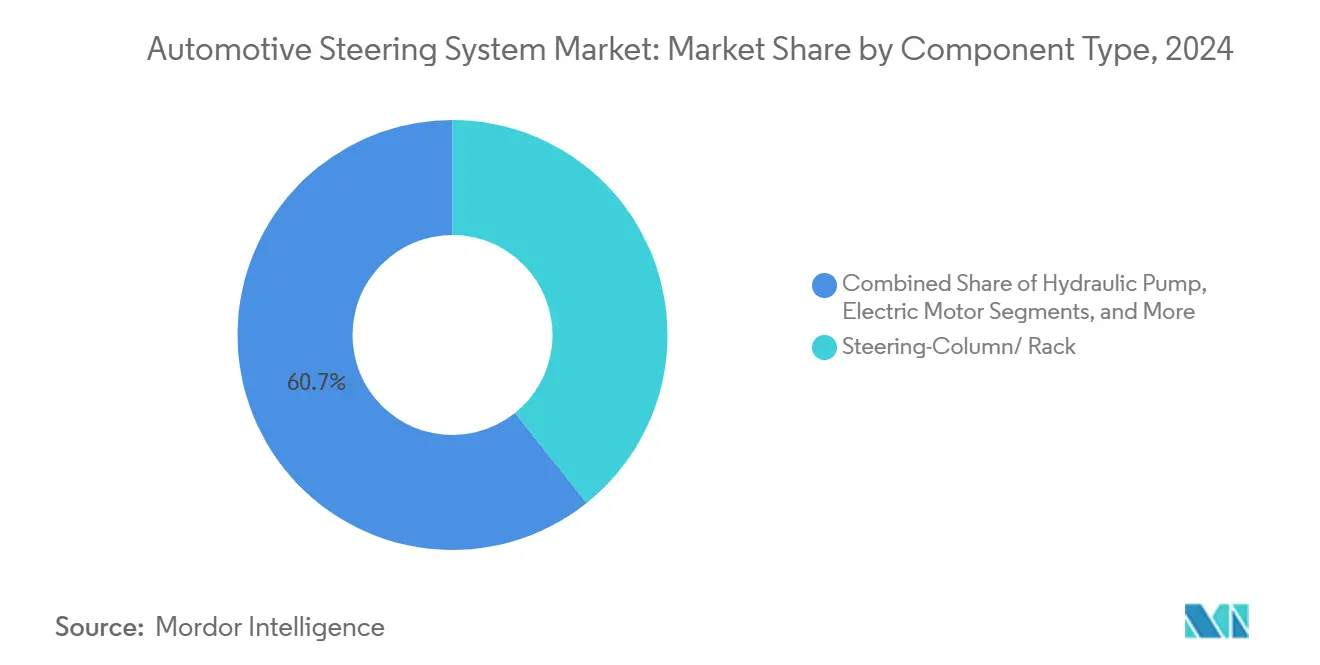

- By component, steering columns/racks led with 39.26% of the automotive steering system market share in 2024; electric motors are projected to expand at an 8.91% CAGR through 2030.

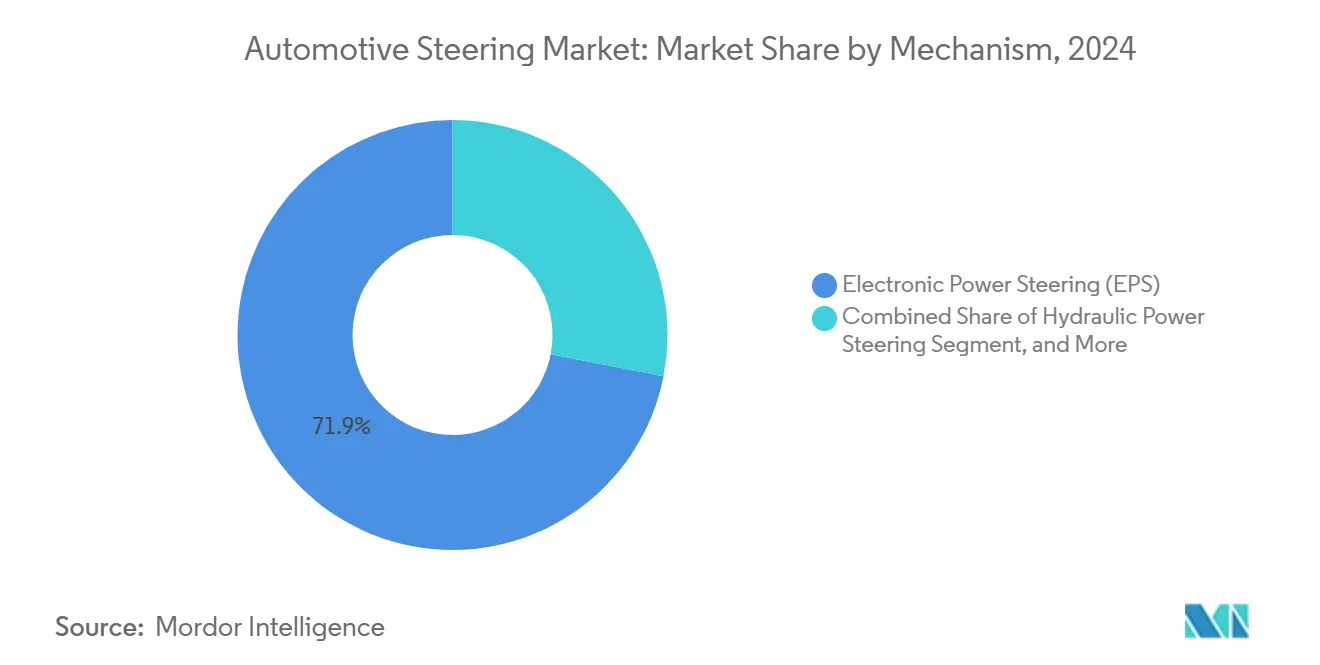

- By mechanism, electronic power steering commanded 71.95% share of the automotive steering system market size in 2024, while steer-by-wire is advancing at an 8.28% CAGR through 2030.

- By vehicle type, passenger cars held 63.28% of the automotive steering system market size in 2024; light commercial vehicles are forecast to post a 7.56% CAGR to 2030.

- By sales channel, OEMs dominated 87.23% of the automotive steering system market size in 2024; the aftermarket is set to grow at a 7.26% CAGR between 2025 and 2030.

- By geography, Asia-Pacific captured 48.67% of the automotive steering system market size in 2024 and is projected to expand at a 6.81% CAGR through 2030.

Global Automotive Steering Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid EPS penetration in ICE & xEV platforms | +1.8% | Global, led by Asia-Pacific | Medium term (2–4 years) |

| Steer-by-wire deployment in premium EVs | +0.9% | North America and Europe, expanding to China | Long term (≥ 4 years) |

| Lightweight steering columns | +1.2% | Europe and North America | Short term (≤ 2 years) |

| ADAS-ready “fail-operational” architectures | +1.4% | Global, premium segments first | Medium term (2–4 years) |

| Cyber-secure ECUs under UNECE R155 | +0.7% | Europe, rolling out globally | Short term (≤ 2 years) |

| OTA-upgradable torque-overlay software | +0.5% | Global, premium vehicles first | Long term (≥ 4 years |

Source: Mordor Intelligence

Rapid EPS Penetration in ICE & xEV Platforms

Electronic power steering is highly prevalent in China’s passenger-car industry and is approaching ubiquity in Europe and Japan. OEMs gain fuel-saving benefits while unlocking regenerative braking compatibility for electric drivetrains. The technology now scales from compact cars to Class 8 trucks, as ZF’s commercial-vehicle EPS delivers up to 8,000 Nm without hydraulic fluid. Column-assist units dominate the value B-segment, whereas rack-assist designs earn a share in premium cars that need higher precision and road feel. The accelerating shift keeps the automotive steering system market steadily growing.

Steer-by-wire Deployment in Premium EVs From 2025

Mercedes-Benz will introduce the first European production steer-by-wire system in 2026, following ZF’s 2025 launch on NIO’s ET9. Removing the mechanical shaft enables variable steering ratios that ease parking and enhance highway stability. Toyota’s “One Motion Grip” wheel shows how 200-degree input strokes can replace the traditional 540-degree turn, improving ergonomics and cabin packaging[2]“One Motion Grip Steering System Details,”, Toyota Motor Corporation, global.toyota. Redundant motors, power supplies, and haptic feedback maintain driver confidence, although consumer acceptance studies indicate a learning curve that may extend roll-out timelines beyond luxury nameplates.

Lightweight Steering Columns to Meet Euro 7/CAFÉ Norms

Suppliers switch from steel to aluminum or magnesium and exploit hollow shaft designs. JTEKT’s JIGB® integrated gear-bearing unit merges two functions, trimming space and cutting torque losses, while maintaining crash performance[3]“J-EPICS® Steer-by-Wire Platform Overview,”, JTEKT Corporation, jtekt.com. Every 10% weight reduction translates to a 0.3% fuel-efficiency gain, an outcome welcomed by electric brands keen to extend driving range. The competitive edge now lies in combining light metals with high-strength joining processes that protect energy-absorption paths.

OEM Demand for ADAS-ready “Fail-operational” Architectures

Level 3 hands-off driving regulations require a steering intervention within 200 milliseconds if the automated mode disengages. Dual-motor EPS layouts with isolated power and communication paths answer that need. Nexteer’s Quiet Wheel™ eliminates steering-wheel rotation during autonomous operation, while still handing back smooth control to the driver when requested[4]“Quiet Wheel™ Technology Briefing,”, Nexteer Automotive, nexteer.com. Such redundancy lifts unit prices by 40-60%, yet compliance requirements make the investment unavoidable for premium OEMs, locking in long-term content growth for suppliers.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rare-earth magnet price volatility | -1.1% | Global; most acute in Europe and North America | Short term (≤ 2 years) |

| Automotive MCU shortage through 2026 | -0.8% | Global; severe in Europe and North America | Medium term (2–4 years) |

| Steering-feel concerns in steer-by-wire | -0.4% | Premium segments worldwide | Long term (≥ 4 years) |

| Tier-1 consolidation lowers OEM bargaining power | -0.3% | Developed markets | Medium term (2–4 years) |

Source: Mordor Intelligence

Rare-earth Magnet Price Volatility Inflates EPS BOM

China controls roughly 70% of global rare-earth processing and has limited neodymium exports. Magnet costs already account for up to 25% of an EPS motor bill of materials. Ford’s temporary halt of Explorer production exposed the risk to OEM schedules. Suppliers respond by advancing rare-earth-free innovations such as ZF’s I2SM motor and Magna’s investment in Niron Magnetics’ iron-nitrogen Clean Earth Magnets.

Automotive MCU Shortage Through 2026

Safety-critical EPS controllers need high-reliability microcontrollers that few foundries can supply. Lead times remain in the 26-52-week range. Some suppliers now redesign boards around available chips, a strategy that increases qualification cost and slows new-feature deployment. Brands able to secure long-term wafer contracts gain an immediate competitive edge in the automotive steering system market.

Segment Analysis

By Component: Electric Motors Drive Electrification Shift

In 2024, steering columns and racks dominate the automotive steering system market, commanding a 39.26% revenue share. Integrated collapse mechanisms, multi-function switches, and driver-airbag modules keep the sub-segment essential across all platforms. In parallel, electric motors deliver the fastest expansion at an 8.91% CAGR through 2030 as brushless DC designs replace hydraulic pumps and belt-driven units. Cyber-secure electronic control units form the third-largest bucket, their content per vehicle climbing with every new over-the-air feature that UNECE R155 obliges manufacturers to secure.

Torque, angle, and position sensors advance in lockstep with steer-by-wire and ADAS features that depend on millisecond-accurate feedback. TDK’s four-mode HAL 39xy chip illustrates how single-package solutions cut wiring weight while resisting magnetic noise from high-voltage powertrains. Suppliers able to merge motor, sensor, and ECU functions inside compact, shielded housings improve system reliability and lower warranty exposure, reinforcing their standing in the automotive steering system market.

Note: Segment shares of all individual segments available upon report purchase

By Vehicle Type: Commercial Vehicles Accelerate EPS Adoption

In 2024, passenger cars dominated the global automotive steering system market, capturing 63.28% of the revenue. Meanwhile, light commercial vehicles emerged as the fastest-growing segment, boasting a robust 7.56% CAGR. E-commerce fleets value the precise low-speed maneuvering and lower maintenance that EPS provides, while autonomous delivery concepts lean on software-controlled steering for curb-side accuracy. Heavy commercial vehicles shift away from hydraulics as the latest rack-drive EPS units hit industrial torque outputs. Across classes, the automotive steering system market benefits from fleet owners' focus on fuel savings.

Within the passenger-car arena, battery electric models remove the engine vacuum source used by traditional hydraulics, making EPS mandatory. Sport utility vehicles secure a rising share as buyers favor higher ride positions, and their larger footprint translates into higher steering-system content. Multi-purpose vehicles and minivans leverage EPS packaging gains to offer flat-floor cabins. These combined shifts keep the automotive steering system industry on a stable path of unit and value growth.

By Mechanism: Steer-by-wire Disrupts Traditional Architecture

In 2024, electronic power steering dominates the automotive steering system market, holding a 71.95% share. Yet, the emerging frontrunner for future growth is steer-by-wire, projected to grow at an 8.28% CAGR to 2030. Early series projects by ZF for NIO and Mercedes-Benz sharpen interest among premium OEMs, particularly because variable-ratio logic can improve agility without compromising motorway stability. Eliminating the steering shaft opens fresh design latitude for retractable wheels and larger display zones.

Hydraulic steering lingers in niche high-load roles but shrinks yearly as cost parity improves for large electric drive units. Electro-hydraulic hybrids serve as a bridge technology, offering electronic command with existing hydraulic hardware. Over the forecast window, regulatory momentum behind automated-driving redundancy accelerates the pivot to pure-by-wire layouts, deepening the addressable pool for suppliers active in the automotive steering system market.

Note: Segment shares of all individual segments available upon report purchase

By Sales Channel: Aftermarket Gains From System Complexity

In 2024, OEM installations commanded a significant 87.23% share of the automotive steering system market, underscoring the importance of calibration and ISO 26262 validation on the assembly line. Meanwhile, the aftermarket segment is witnessing a robust growth, expanding at a 7.26% CAGR, driven by the aging of vehicles and the need for specialized diagnostics on intricate EPS units. Right-to-repair initiatives in Europe and selected U.S. states are widening access to service data, encouraging independent workshops to invest in programming tools.

The automotive steering system market size for the aftermarket stands to expand further as electric vehicles reach the secondary-owner phase, given that software updates, sensor recalibration, and cooling-loop maintenance are required throughout the life cycle. Suppliers that provide training, cloud-based diagnostics, and remanufactured assemblies position themselves to capture this emerging profit pool.

Geography Analysis

In 2024, Asia-Pacific commands a 48.67% share of the automotive steering system market and is set to achieve a robust 6.81% CAGR through 2030. China’s extensive electric-vehicle production base drives near-universal EPS fitment, while local challengers such as HIVE Steering undercut incumbent imports by bundling domestic silicon and magnet supply. Japan contributes specialized know-how, including JTEKT’s steer-by-wire tests and NSK’s low-friction bearing routes, even as NSK considers divesting its steering arm. Regional governments offer clear road maps for autonomous-driving certification, further enhancing demand for by-wire systems in the automotive steering system market.

Europe follows with high per-vehicle value as Euro 7 and UNECE cyber-rules reward advanced ECUs, lightweight columns, and redundant actuation. ZF and Bosch use local technical centers to tune steering feel for premium brands and are already shipping by-wire pilot volumes. OEMs, however, confront raw-material risks, which are highlighted when neodymium shortages force production pauses. That vulnerability fast-tracks research into rare-earth-free motor technology, allowing suppliers to raise content per vehicle without waiting for new model cycles.

North America sees steady take-up of EPS in pick-ups and sport utilities, the region’s largest segments by volume. Fleet operators closely monitor the total cost of ownership, and the 3-5% fuel-saving edge of EPS helps underpin adoption. The United States is also a development hub for alignment-free installation and secure over-the-air software to update steering logic during ownership. Meanwhile, South America, the Middle East and Africa adopt electronified steering as factories upgrade platforms. These markets often leapfrog directly to EPS on new models, creating incremental upside for the automotive steering system market over the long run.

Competitive Landscape

Leading suppliers are consolidating their resources in the automotive steering system market to prioritize the electronics and software developments essential for automated driving. JTEKT, Bosch, ZF, and Nexteer dominate the global landscape. Meanwhile, Schaeffler completed a merger with Vitesco, projects an annual EBIT of 600 million euros, and fully realizes its potential by 2029.

Technology differentiation now rests on by-wire readiness, rare-earth-free motor IP, and integrated safety stacks. ZF’s steer-by-wire won regulatory clearance on NIO’s ET9 in early 2025, giving the supplier a first-mover reference point. Bosch builds on its brake-by-wire competence to offer shared ECU platforms that lower integration complexity for OEMs. Nexteer pushes Quiet Wheel™ to align hand-off transitions with Level 3 guidelines. Smaller Chinese entrants leverage domestic chip capacity to serve local brands but face patent fences in mature regions.

Strategic investments extend into materials science. Magna’s stake in Niron Magnetics seeks to mitigate rare-earth dependency, while ZF’s I2SM programme targets 50% lower carbon emissions in motor production. Software monetization is a rising theme: suppliers sell torque-overlay functions and lane-keeping packages as over-the-air upgrades, opening recurring revenue streams across a vehicle’s life. The shifting profit pool keeps competitive intensity high, yet rewards those with end-to-end integration and global production footprints in the automotive steering system market.

Automotive Steering Industry Leaders

-

JTEKT Corporation

-

Robert Bosch GmbH

-

ZF Friedrichshafen AG

-

Nexteer Automotive Corporation

-

NSK Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Volvo Trucks has unveiled an enhanced version of its Volvo Dynamic Steering system, equipped with a feature that detects tire blowouts and swiftly maneuvers the truck to maintain safe road positioning.

- February 2025: Chinese manufacturer NIO has chosen ZF to equip its electric flagship, the ET9, with ZF's latest steer-by-wire system. ZF's technology group provides the steering wheel actuator, which enhances both steering control and feel, and a redundant steering gear actuator, complete with the necessary software.

Global Automotive Steering Market Report Scope

A steering wheel is primarily responsible for controlling the direction of a vehicle. It translates the driver's rotational commands into front-wheel swiveling motions. The joints and hydraulic lines of the steering system allow the driver's movement to eventually reach the tires as they make contact with the road.

The Automotive Steering Market is segmented by Vehicle Type (Passenger Cars and Commercial Vehicles), Mechanism (Electronic Power Steering (EPS), Hydraulic Power Steering (HPS), and Electrically Assisted Hydraulic Power Steering), Component (Hydraulic Pump, Steering/ Column/ Rack, Sensors, Electric Motor, and Other Components), and Geography (North America, Europe, Asia-Pacific, South America, and Middle-East and Africa). The report offers the market size in value (USD Billion) and forecasts for all the above segments.

| By Component | Hydraulic Pump | ||

| Electric Motor | |||

| Steering Column / Rack | |||

| Sensors (Torque, Angle, Position) | |||

| Electronic Control Unit (ECU) | |||

| Other Components | |||

| By Vehicle Type | Passenger Cars | Hatchback | |

| Sedan | |||

| Sport Utility Vehicle | |||

| Multi-Purpose Vehicle | |||

| Commercial Vehicles | Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicle | |||

| By Mechanism | Electronic Power Steering (EPS) | ||

| Hydraulic Power Steering (HPS) | |||

| Electro-hydraulic Power Steering (EHPS) | |||

| Steer-by-Wire | |||

| By Sales Channel | OEM | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Turkey | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| South Africa | |||

| Rest of Middle East and Africa | |||

| Hydraulic Pump |

| Electric Motor |

| Steering Column / Rack |

| Sensors (Torque, Angle, Position) |

| Electronic Control Unit (ECU) |

| Other Components |

| Passenger Cars | Hatchback |

| Sedan | |

| Sport Utility Vehicle | |

| Multi-Purpose Vehicle | |

| Commercial Vehicles | Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicle |

| Electronic Power Steering (EPS) |

| Hydraulic Power Steering (HPS) |

| Electro-hydraulic Power Steering (EHPS) |

| Steer-by-Wire |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Turkey |

| Saudi Arabia | |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the current size of the automotive steering system market?

The market is valued at USD 34.98 billion in 2025 and is expected to rise to USD 48.31 billion by 2030.

Which mechanism holds the largest share in the automotive steering system market?

Electronic power steering accounts for 71.95% of 2024 revenue, making it the dominant mechanism.

Why is steer-by-wire considered a disruptive technology?

It removes mechanical linkages, enables variable steering ratios and supports cabin re-designs, and it is projected to grow at an 8.28% CAGR through 2030.

How are raw-material constraints affecting suppliers?

Rare-earth magnet volatility increases costs and exposes production schedules, prompting investment in iron-nitrogen or induction motor alternatives.

What is driving growth in the aftermarket segment?

Rising vehicle complexity and right-to-repair regulations are boosting demand for specialized diagnostic and calibration services, supporting a 7.26% CAGR to 2030.