Automotive Catalytic Converter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 120.39 Billion |

| Market Size (2031) | USD 177.87 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Catalytic Converter Market Analysis by Mordor Intelligence

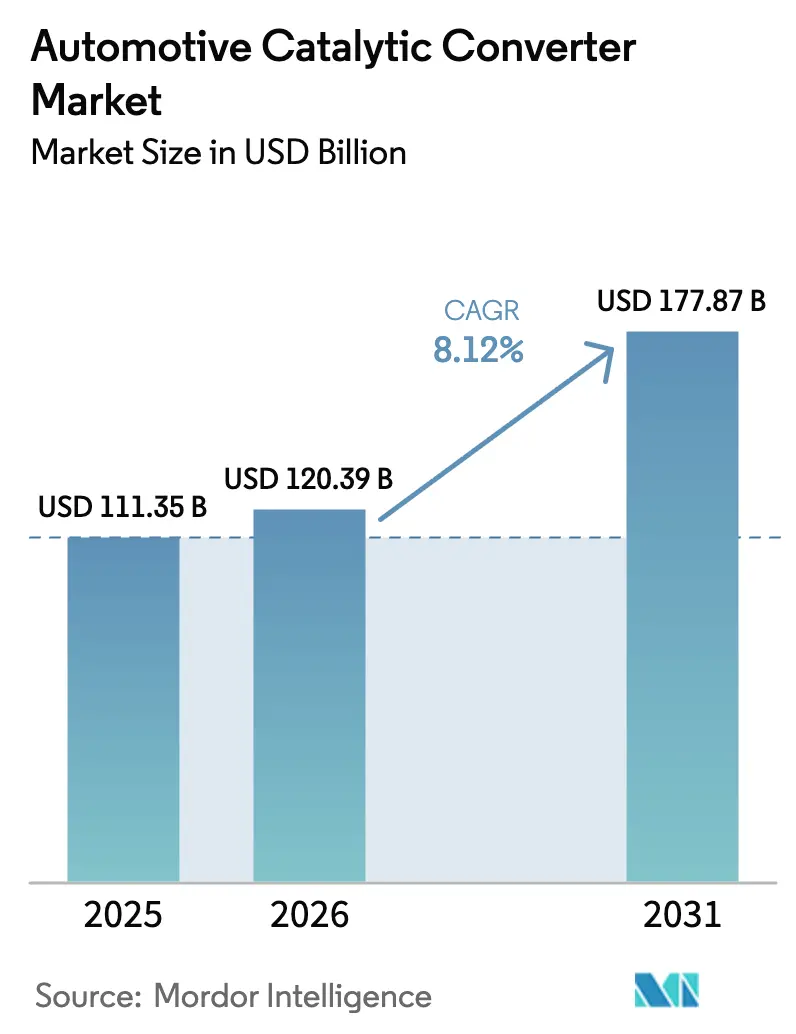

The catalytic converters market size is expected to grow from USD 111.35 billion in 2025 to USD 120.39 billion in 2026 and is forecast to reach USD 177.87 billion by 2031 at 8.12% CAGR over 2026-2031. The expansion reflects consistent regulatory tightening after 2025, including Euro 7, China 7, and updated United States standards, all of which mandate higher precious-metal loadings and advanced wash-coat chemistries. Further momentum comes from the rebound in global internal-combustion and hybrid vehicle production, precious-metal substitution strategies that cut cost risk, and retrofit activity in non-road machinery fleets. Supply chain resilience, new hydrogen internal-combustion projects, and promising single-material catalysts round out the opportunity set for the catalytic converters market.

Key Report Takeaways

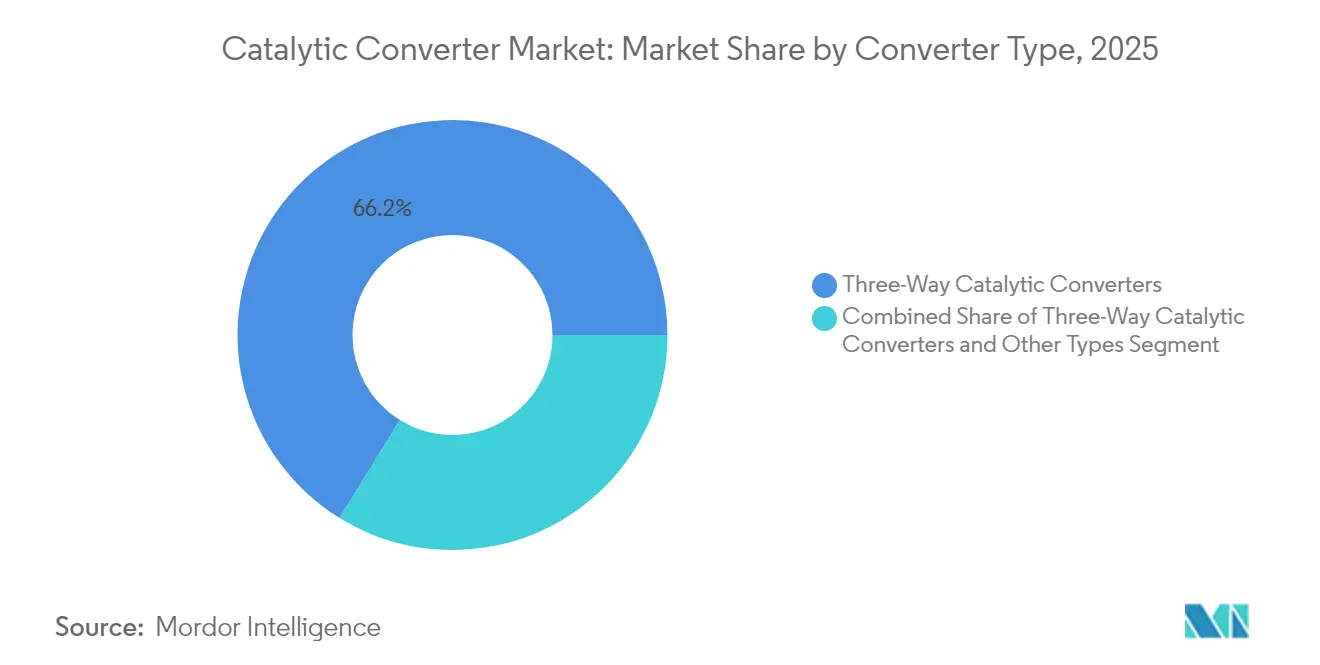

- By converter type, three-way systems held 66.20% of the catalytic converters market share in 2025, while the “other types” category is projected to grow at 11.59% CAGR through 2031.

- By vehicle type, passenger cars accounted for 63.05% of the catalytic converters market share in 2025; medium and heavy commercial vehicles are poised for the fastest 8.95% CAGR to 2031.

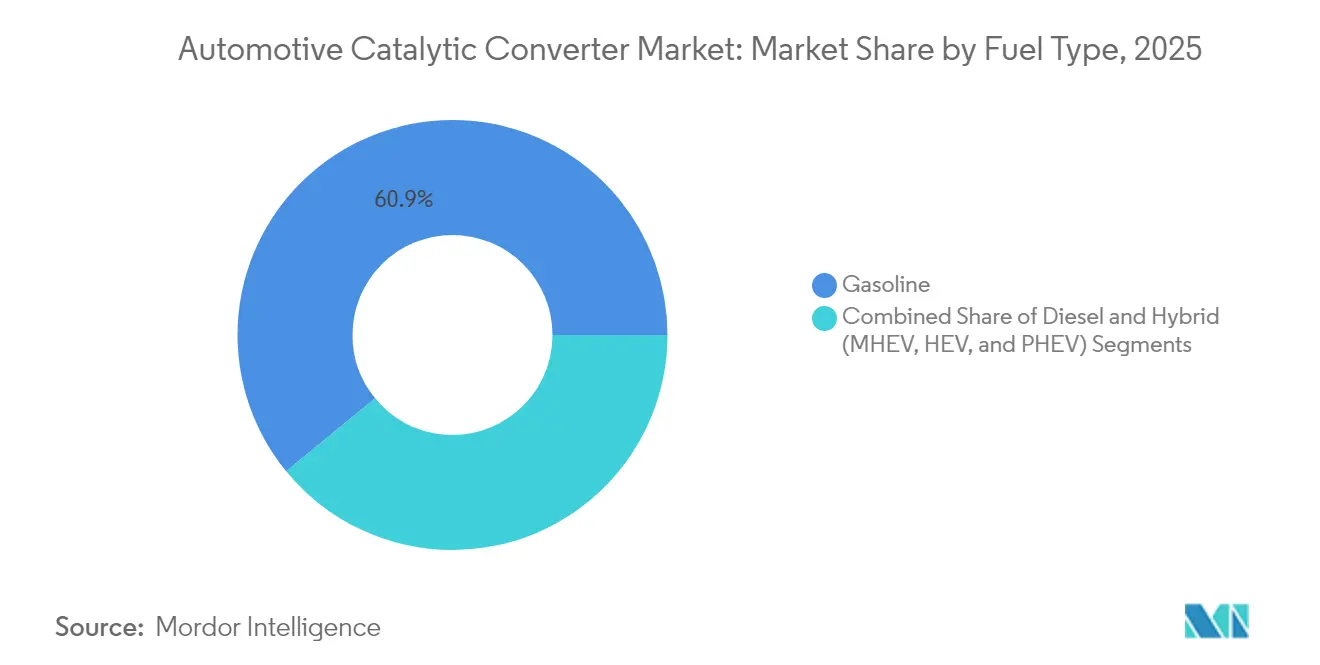

- By fuel type, gasoline powertrains captured 60.92% share of the catalytic converters market size in 2025, whereas hybrids are expected to expand at 9.01% CAGR during the forecast window.

- By substrate material, palladium substrates commanded 48.20% share of the catalytic converters market size in 2025; rhodium substrates led growth at a 6.48% CAGR.

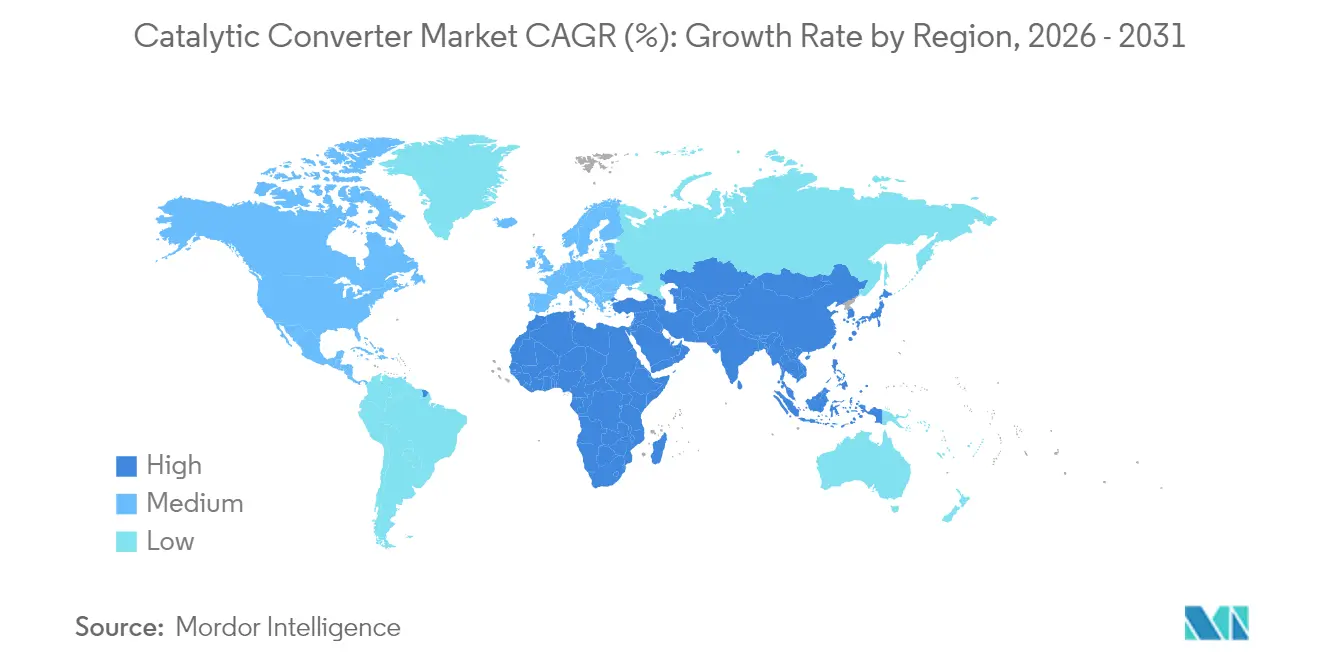

- By geography, Asia-Pacific dominated with 49.30% share of the catalytic converters market in 2025 and is also the fastest-growing region, advancing at 7.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Catalytic Converter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Post-2025 Emission Legislation | +2.8% | Global, with early implementation in EU and China | Medium term (2-4 years) |

| Rebounding Global ICE And Hybrid Production Volumes | +1.9% | Global, concentrated in APAC and North America | Short term (≤ 2 years) |

| Precious-Metal Loadings in GDI and Mild-Hybrids | +1.6% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| OEM Retrofit Demand from Non-Road/Mobile Machinery | +1.2% | EU Stage V, CARB Tier 5 regions, expanding globally | Long term (≥ 4 years) |

| Supply-Chain Gaps by Converter-Theft Recycling Boom | +0.8% | North America core, spill-over to EU | Short term (≤ 2 years) |

| Growing Incentives for Hydrogen-ICE Vehicles | +0.4% | EU and Japan early adoption, US emerging | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Post-2025 Emission Legislation Drives Technology Upgrades

Euro 7 begins phasing in from July 2025 and extends compliance durability to eight years/160,000 km, forcing automakers to specify thicker precious-metal layers and sophisticated gasoline particulate filters.[1]European Commission, “Regulation (EU) 2024/1257 on Type-Approval of Motor Vehicles and Engines with Respect to Their Emissions and Battery Durability (Euro 7),” eur-lex.europa.eu China 7 mirrors and, in several respects, exceeds Euro 7, requiring particulate-number limits and real-driving emissions testing across platforms. In the United States, tougher off-road and light-vehicle rules close historical regulatory gaps. Unified global thresholds remove the lag-time cushion OEMs once used, accelerating design cycles for advanced three- and four-way systems.

Rebound in Global ICE and Hybrid Production Volume Post-COVID

Worldwide light-vehicle output witnessed volume restoration across gasoline, diesel, and hybrid lines. Commercial trucks added volume on the back of logistics demand, while infrastructure stimulus in Asia-Pacific kept heavy-duty assembly lines active. Hybrids represented approximately 10% of production and need larger catalyst volumes to control cold-start emissions during frequent stop-start cycling. the China Association of Automobile Manufacturers is implementing a three-step development strategy targeting 20% carbon emissions reduction by 2035 through enhanced thermal efficiency and advanced emission control systems. Normalized factory utilization raises near-term unit shipments for the catalytic converters market despite longer-term electrification pressure.[2]Asian Clean Fuels Association, "The evolution of Internal Combustion Engines (ICE) and New Energy Vehicles (NEV) in China – A review and outlook for the industry," acfa.org

Higher Precious-Metal Loadings in GDI and Mild Hybrid Engines

Gasoline direct-injection powertrains reached 73% penetration in 2023 and emit finer particulates than port-fuel-injection designs, compelling automakers to integrate platinum-group metals and coated gasoline particulate filters. Turbocharging and mild-hybridization, both widespread in GDI applications, widen exhaust composition and temperature windows, demanding precise stoichiometric control and faster light-off. The resulting increase in PGM intensity strengthens revenue growth even as substitution initiatives seek cost neutrality.

OEM Retrofit Demand from Non-Road/Mobile Machinery ESG Pressure

Stage V and forthcoming Tier 5 rules require construction, agricultural and industrial equipment owners to retrofit legacy engines with advanced catalysts. Non-road engines frequently remain in service for two decades, creating incremental aftermarket demand extending well past 2030. Fleet operators adopt retrofit packages to satisfy corporate ESG pledges and municipal procurement criteria.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extreme PGM Price Volatility | -1.8% | Global, concentrated impact in cost-sensitive markets | Short term (≤ 2 years) |

| BEV Acceleration Reducing Long-Term Unit Demand | -1.4% | EU and China leading, North America following | Medium term (2-4 years) |

| Crack-Down on Illicit PGM Sourcing | -0.9% | Global supply chains, Africa-sourced materials focus | Medium term (2-4 years) |

| Commercialisation of Single-Material Catalysts | -0.6% | Research-intensive markets, Japan and Germany leading | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Extreme Platinum-Group-Metal Price Volatility

Palladium’s fall from more than USD 3,000/oz in 2022 to under USD 1,000/oz in early 2025, and platinum’s swings between USD 900–1,100/oz, complicate sourcing budgets and encourage substitution. Suppliers hedge, but small participants struggle to offset price moves, reducing short-term margin visibility and delaying orders when cost shocks hit. Planned reductions in South African mine capex threaten to tighten supply later in the decade..

Accelerated BEV Penetration Reducing Long-Term Unit Demand

Electric vehicle adoption accelerated significantly in 2024, creating a structural shift that reduces the addressable market for catalytic converters as battery electric vehicles require no emission control systems. BloombergNEF's Economic Transition Scenario forecasts even more aggressive adoption rates, projecting electric vehicles to capture 45% of global passenger-vehicle sales by 2030 and 73% by 2040, with global passenger EV sales expected to increase from 13.9 million in 2023 to over 30 million by 2027. The transition's geographic variation creates opportunities for catalyst manufacturers to optimize their regional strategies, as markets with slower EV adoption rates maintain stronger demand for advanced emission control technologies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Converter Type: Advanced Multi-Functional Systems Expand

Three-way converters retained a 66.20% share of the catalytic converters market in 2025, reflecting their universal fit for stoichiometric gasoline engines. Tightening particulate-number and durability rules keep this format central to compliance, though metal loading and wash-coat formulations continue to evolve. The catalytic converters market size for three-way units is forecast to rise in line with overall vehicle production through 2031, underpinned by hybridization that magnifies cold-start events.

A new wave of four-way converters, lean-NOx traps, and combined selective catalytic-reduction systems clusters in the “other types” category, which is projected to grow at 11.59% CAGR. Laboratory work at Washington State University shows that nano-scale ceria clustering induced by high exhaust heat boosts activity tenfold while using less precious metal, a discovery that may reshape cost curves. Parallel research into self-regenerating perovskite catalysts aims to cut PGM content by up to 90%, setting the stage for broader adoption once production scale and durability benchmarks are met.

By Vehicle Type: Commercial Fleets Accelerate Growth

Passenger cars dominated the 2025 volume with 63.05% catalytic converters market share, driven by their absolute production scale. Despite the portion declining modestly as electrification grows, passenger-car catalysts remain a staple due to long fleet lives, late-cycle hybrid launches, and emerging diesel-downsize gasoline strategies.

Medium and heavy commercial vehicles provide the fastest 8.95% CAGR. Logistics expansion, infrastructure spending, and stricter heavy-duty NOx ceilings push fleet managers toward higher-capacity catalyst bricks and longer warranties. Developers are already validating hydrogen-ICE systems for long-haul trucking, opening a fresh avenue for three-way catalysts that must tolerate 100% hydrogen streams at high exhaust temperatures while still curbing NOx. Off-road machinery, though niche, prolongs growth by tapping Stage V retrofit packages with bespoke pipe-fabricated housings.

By Fuel Type: Hybridization Alters Catalyst Duty Cycles

Gasoline engines delivered 60.92% of the 2025 catalytic converters market size, underlining their entrenched share across most passenger segments. High-compression and boosted GDI designs elevate particulate output, necessitating gasoline particulate filters coated with platinum-group metals that sustain efficiency at lean conditions.

Hybrids—mild, full, and plug-in- are the fastest 9.01% CAGR segment as automakers layer electrified drive modules onto conventional engines. Frequent shutdowns require catalysts that light off in seconds and regenerate quickly under transient load, stimulating demand for electrically heated bricks and low-mass substrates. Diesel remains indispensable for long-haul freight but faces a shrinking share in light vehicles. Research into electrically heated diesel catalysts claims 75% NOx removal during low-temperature cycles, indicating the technology’s resilience even as volumes ebb.

By Substrate Material: Substitution Strategies Shift PGM Mix

Palladium substrates led with a 48.20% share in 2025, but cost volatility encourages OEMs to specify platinum in new gasoline platforms where compatibility permits. Substitution reached 700 koz during 2024 and will likely persist over the entire seven-year vehicle cycles. Platinum thus captures incremental gasoline share while retaining diesel dominance as sulfur tolerance remains critical.

Rhodium, although used in smaller absolute volumes, is set for a 6.48% CAGR because no viable alternative exists for deep NOx reduction under high-oxygen exhaust. The “others” bucket, covering ceria-vanadia composites, advanced perovskites, and vanadium-oxide SCR formulations, remains exploratory yet strategically important for diversifying supply away from scarce PGMs. Early test cells show 10–14× faster ammonia-SCR reaction rates than classical vanadia/titania blends, hinting at sizeable, long-run displacement potential should scale-up succeed.

Geography Analysis

Asia-Pacific controlled 49.30% of the catalytic converters market revenue in 2025 and is expected to expand at a 7.72% CAGR through 2031. China anchors regional growth on the back of China 7 standards that embed particulate-number and real-driving protocols exceeding European thresholds. India adds volume as automotive production ramps up to meet both domestic mobility demand and export orders. Regional heavy-duty output benefits from infrastructure pipelines that stimulate truck and off-road equipment sales. Futures contracts for platinum and palladium listed on a new Guangzhou exchange further professionalize metal procurement, lessening price-shock exposure for local manufacturers.

North America is forecast to grow at 5.02% CAGR. Updated federal rules demand 50% NMOG + NOx cuts by 2032 and force gasoline particulate-filter adoption. Texas, Michigan, and Ontario remain key production clusters for light-vehicle converters, while Tier 5 off-road proposals in California pull through advanced SCR systems for construction machinery. Investments in hydrogen-ICE testing labs illustrate the region’s commitment to alternative propulsion while still relying on after-treatment for NOx abatement.

Europe’s 4.72% CAGR reflects a mature vehicle base under pressure from mandated zero-emission sales after 2035. Near-term catalyst demand rises as Euro 7 introduces eight-year durability and extended temperature compliance windows. Leading suppliers focus on higher density wash-coats, electrically heated bricks, and combined NOx/particulate regeneration algorithms to meet the stringent Euro 7 limits. Retrofit activity in non-road fleets sustains aftermarket volumes once new-car demand flattens.

Competitive Landscape

The market is moderately concentrated, with major players accounting for a prominent share. Scale economies in precious-metal recycling and sourcing deliver cost leverage while also creating barriers for smaller entrants. Technology differentiation is now the primary contest ground, with established players investing in hydrogen-ready converters, electro-thermal catalyst heaters, and machine-learning calibration models that optimize air-fuel ratios on the fly.

Regional specialization is evident. European groups emphasize deeply integrated exhaust modules for stringent legislative zones. Asian firms supply cost-effective systems for volume models, leveraging vertically integrated substrate production. North American producers concentrate on high-durability solutions for heavy trucks and off-road equipment. Closed-loop recycling schemes led by large refiners increasingly support OEM carbon-neutrality pledges by demonstrating full-life PGM traceability.

Innovation pipelines feature perovskite chemistries that slash PGM intensity, nano-structured wash-coats that regenerate in situ, and additive-manufactured honeycombs that cut weight without compromising surface area. Commercial rollout timelines hinge on scalable manufacturing and multi-year field durability validation, keeping traditional PGM catalysts dominant through most of the decade.

Automotive Catalytic Converter Industry Leaders

-

Tenneco Inc

-

Marelli Holdings Co., Ltd.

-

Eberspächer Group

-

Boysen Group

-

Futaba Industrial Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Tenneco confirmed a strategic investment agreement with Apollo Fund X to accelerate growth in its clean-air and powertrain divisions, transaction closing targeted for Q2 2025.

- October 2024: Tenneco opened new hydrogen-ICE testing facilities in Burscheid, Germany, and Ann Arbor, Michigan, along with a dedicated hydrogen materials lab in Nuremberg.

Global Automotive Catalytic Converter Market Report Scope

The toxic molecules from an engine's exhaust are converted into harmless gases, such as steam, by a catalytic converter, which uses a chamber called a catalyst. It works by breaking up the dangerous molecules in the gases produced by a car before they are released into the atmosphere. The catalytic converter is a huge metal box that is positioned on the underside of a car. It has two pipes protruding from it. During the process of making the gases safe to be released, the convertor makes use of these two pipelines as well as the catalyst.

The Automotive catalytic converter market is segmented by Type, Material Type, Vehicle Type, and Geography. By type, the market is segmented into the two-way catalytic converter, three-way catalytic converters, and other types. By Material type, the market is segmented into Platinum, Palladium, and Rhodium.

By Vehicle Type, the market is segmented into Passenger cars and commercial vehicles, and By Geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the world. For each segment, market sizing and forecast have been done on the basis of value (USD billion).

| Two-Way Catalytic Converters |

| Three-Way Catalytic Converters |

| Other Types |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Off-Road and Non-Road Equipment |

| Motorcycles and Powersports |

| Gasoline |

| Diesel |

| Hybrid (MHEV, HEV, and PHEV) |

| Platinum |

| Palladium |

| Rhodium |

| Others (Cerium, Vanadium, and Perovskites) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Converter Type | Two-Way Catalytic Converters | |

| Three-Way Catalytic Converters | ||

| Other Types | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| Off-Road and Non-Road Equipment | ||

| Motorcycles and Powersports | ||

| By Fuel Type | Gasoline | |

| Diesel | ||

| Hybrid (MHEV, HEV, and PHEV) | ||

| By Substrate Material | Platinum | |

| Palladium | ||

| Rhodium | ||

| Others (Cerium, Vanadium, and Perovskites) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the catalytic converters market?

The catalytic converters market generated USD 120.39 billion in 2026 and is on track to reach USD 177.87 billion by 2031.

How fast is the catalytic converter market growing?

From 2026 to 2031, the market expands at an 8.12% compound annual growth rate.

Which converter type leads the global share?

Three-way catalytic converters commanded 66.20% of global revenue in 2025.

Why is Asia-Pacific the largest regional market?

China’s stringent China 7 standards, combined with India’s expanding vehicle production, give Asia-Pacific a 49.30% share and the fastest 7.72% CAGR.

What role do hydrogen internal-combustion engines play?

Hydrogen-ICE platforms for heavy trucks still require three-way catalysts to control NOx, opening a fresh demand stream even as electrification advances.

Page last updated on: