Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

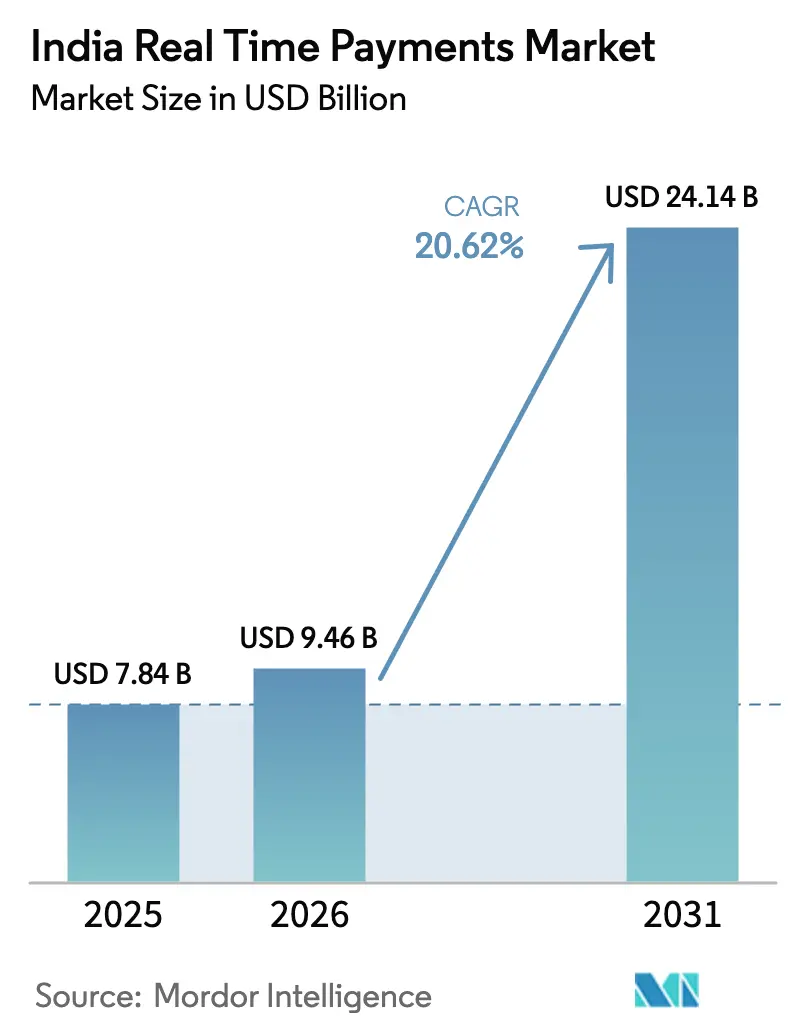

| Base Year Market Size (2025) | USD 7.84 Billion |

| Market Size (2026) | USD 9.46 Billion |

| Market Size (2031) | USD 24.14 Billion |

| Growth Rate (2026 - 2031) | 20.62% CAGR |

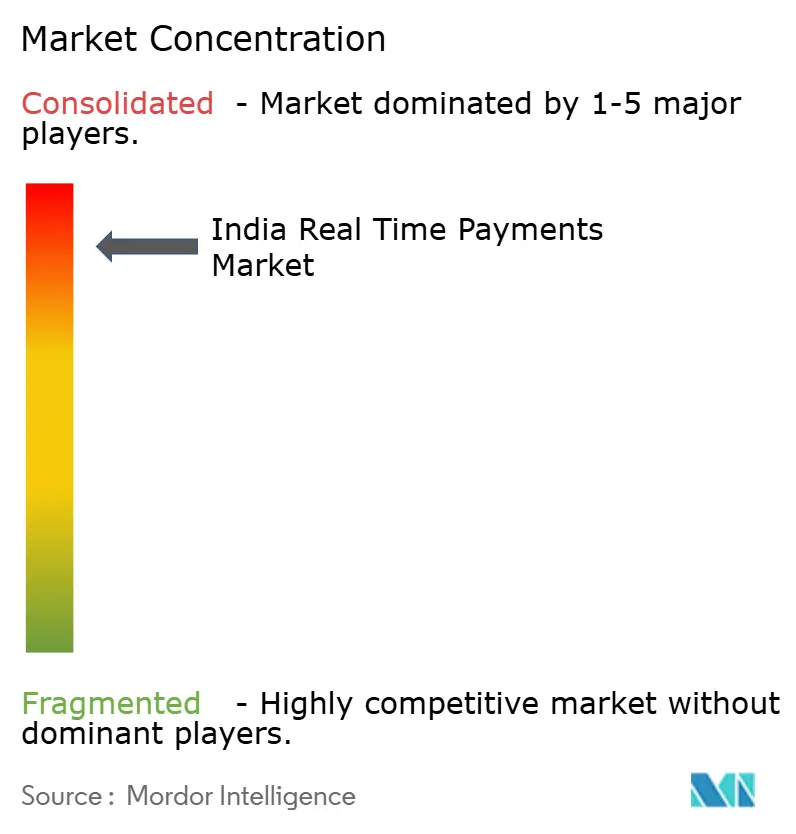

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Real Time Payments Market Analysis by Mordor Intelligence

The India real-time payments market size was valued at USD 7.84 billion in 2025 and estimated to grow from USD 9.46 billion in 2026 to reach USD 24.14 billion by 2031, at a CAGR of 20.62% during the forecast period (2026-2031). Exceptional transaction velocity on the Unified Payments Interface (UPI) platform, supportive government incentives, and rapid merchant onboarding continue to reshape the competitive order. Interoperable innovations such as UPI-123PAY and the recent linkage of RuPay credit cards to UPI have expanded addressable demand across device categories and income segments. The National Payments Corporation of India’s (NPCI) target of 1 billion daily UPI transactions, already eclipsing Visa’s global volumes, underscores the structural shift away from card rails toward instant account-to-account payments.[1]Press Information Bureau, “Government Extends Incentive Scheme for Low-Value UPI Transactions,” pib.gov.in Intensifying rivalry among payment service providers (PSPs) is evident in aggressive cash-back programs, ubiquitous QR-code roll-outs, and an escalating race to embed lending, insurance, and wealth products within day-to-day payment flows, further broadening revenue opportunities for ecosystem participants.

Key Report Takeaways

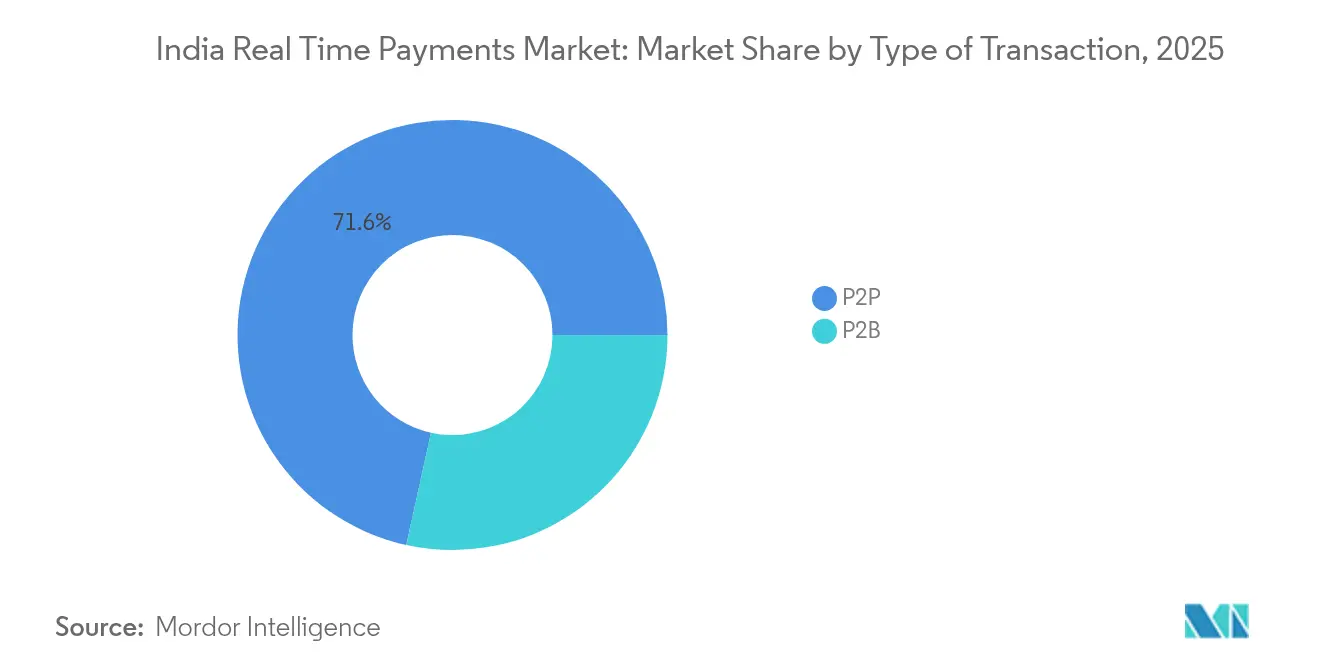

- By transaction type, peer-to-peer (P2P) transfers led with 71.55% of India real-time payments market share in 2025, whereas peer-to-business (P2B) transactions are poised for the fastest 23.85% CAGR through 2031.

- By component, platform/solution offerings captured 63.20% of the 2025 India real-time payments market size, while value-added services are forecast to expand at a 28.05% CAGR.

- By deployment mode, cloud implementations commanded 77.90% share of the India real-time payments market size in 2025 and remain central to scaling spikes in daily volumes; on-premise solutions record the highest projected 21.7% CAGR to 2031.

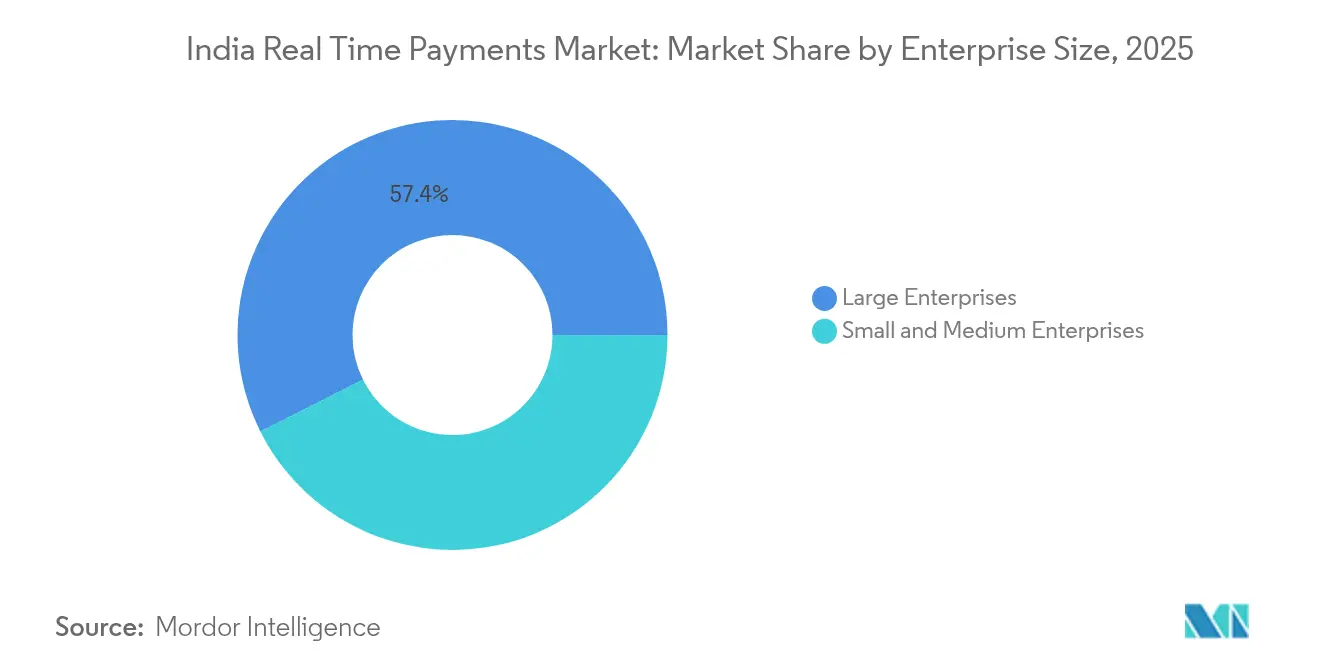

- By enterprise size, large organizations retained 57.40% revenue share in 2025, yet small and medium enterprises (SMEs) are accelerating at 25.5% CAGR on the back of zero merchant discount-rate policies.

- By end-user industry, retail & e-commerce accounted for 32.10% revenue in 2025, while the government and public-sector vertical is expected to advance at 27.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Real Time Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in UPI adoption driven by NPCI incentives and merchant cash-backs | +4.2% | National, with higher impact in tier-2/3 cities | Medium term (2-4 years) |

| Government-mandated interoperability via UPI-123PAY | +3.8% | National, focused on rural and semi-urban areas | Long term (≥ 4 years) |

| Instant settlement demand from gig-economy platforms drives the market | +2.9% | Urban centers, expanding to tier-2 cities | Short term (≤ 2 years) |

| QR-based offline payments growth in Tier-3/4 towns drives the market | +3.5% | Tier-3/4 cities and rural areas | Medium term (2-4 years) |

| RuPay credit-card linkage on UPI boosts ticket size | +2.1% | Urban and semi-urban areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in UPI adoption driven by NPCI incentives and merchant cash-backs

Cash-back programs funded by the government’s INR 1,500 crore incentive pool for FY 2024-25 have pushed transaction counts in smaller cities to new highs, with 80% of new UPI users emerging outside metros. The subsidy on sub-INR 2,000 tickets sustains a zero merchant discount rate, motivating kirana stores and street vendors to display QR codes prominently and creating a network-effect flywheel as consumer convenience rises. P2B volumes have consequently grown faster than P2P volumes, and PSPs have lowered customer-acquisition costs by leveraging expanded merchant footprints. NPCI reports a 126% surge in active QR codes during 2H 2024, supplying the physical infrastructure for omnipresent quick-response payments.

Government-mandated interoperability via UPI-123PAY

UPI-123PAY allows India’s 400 million feature-phone users to initiate real-time payments through dual-tone multi-frequency (DTMF) prompts, closing the device-gap that had restricted digital participation in rural districts. Monthly volumes have already exceeded 10 million transactions in early 2025, concentrated in states with sub-40% smartphone penetration. Telecom alliances with BSNL and Airtel ensure unbroken USSD messaging, while NPCI’s common library enables cross-network routing, preventing vendor lock-in and guaranteeing a consistent user experience regardless of PSP brand.

Instant settlement demand from gig-economy platforms drives the market

Food-delivery and ride-hailing platforms have migrated to UPI pay-outs to shrink settlement cycles from weekly batches to real time, cutting working-capital needs by up to 20% and improving driver retention metrics. More than 85% of gig-workers on leading apps now request earnings via instant transfer rails, and embedded micro-credit products layered on these flows are opening fresh revenue lines for PSPs.[2]Reserve Bank of India, “Payment and Settlement Systems in India: Vision 2025,” rbi.org.in

QR-based offline payments growth in tier-3/4 towns

QR adoption in small towns is expanding 175% faster than in metros, as the absence of point-of-sale hardware costs eliminates the final barrier for merchants unwilling to rent traditional terminals.[3]National Payments Corporation of India, “UPI Product Statistics,” npci.org.in RBI-backed pilots using sound-wave tokens and batch upload capabilities allow transactions to clear even when data networks are patchy, broadening the utility of QR for agri-mandi traders and rural provision stores.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rural network latency hitting transaction success rates | -2.8% | Rural and remote areas | Medium term (2-4 years) |

| Fraud via UPI collect requests & screen-scraping apps hinders the market | -1.9% | National, higher impact in urban areas | Short term (≤ 2 years) |

| Interchange disputes curbing PSP monetisation | -1.4% | National, affecting all payment service providers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rural network latency hitting transaction success rates

Peak-season failure rates exceed 15% in villages where 4G coverage remains inconsistent, compared to 2-3% in metros. BharatNet’s optical-fiber roll-out, currently 60% complete, promises eventual relief, yet delay-sensitive sectors including agriculture payments continue to experience timeout errors. PSPs are testing edge-computing caches that queue transactions for later synchronization, though the upfront capital is substantial for low-ticket rural traffic.

Fraud via UPI collect requests & screen-scraping apps hinders the market

UPI fraud losses grew 85% year-on-year in FY 25, reaching INR 485 crore, undermining trust among first-time users. From June 2025 NPCI mandates that payer apps display the bank-registered beneficiary name before transfer confirmation. Simultaneously, RBI’s Central Payments Fraud Information Registry offers real-time incident feeds to PSPs, enabling rules-based interdiction of suspected mule accounts within seconds of an alert.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Transaction Type: P2B Segment Drives Commercial Transformation

P2B accounted for 28.45% of total UPI volume in January 2025 and is sprinting ahead at a 23.85% CAGR. The India real-time payments market size for P2B payments is on track to expand faster than remittance-oriented P2P flows, reflecting new consumer habits such as paying for public transport, street food, and utilities with a single scan. Average P2B ticket value stands at INR 1,471, confirming deeper penetration into micro-transactions. RuPay credit-card integration will add revolving-credit elasticity to P2B spend while maintaining instant confirmation.

P2P nevertheless preserves a dominant 71.55% share of 2025 transactions, illustrating entrenched use cases like salary advances, rent, and family support. Transcontinental remittances facilitated by UPI ties with Nepal and Singapore are set to sustain core P2P relevance, even as the segment’s growth rate normalizes. Rural off-grid households rely on P2P to move harvest proceeds rapidly, underlining the social-inclusion mandate built into the India real-time payments market.

By Component: Services Segment Capitalizes on Platform Maturity

The services layer, forecast to rise at 28.05% CAGR, now comprises fraud analytics, unified reconciliation, and lending APIs. PSPs such as Razorpay launched 40 new service lines in FY 24, showcasing how the zero merchant discount-rate environment is pushing providers up the value pyramid. The India real-time payments market benefits from AI-driven risk models that can score transactions within milliseconds and throttle suspicious flows before they hit settlement.

Platform/solution revenues still contribute 63.20% of the 2025 base and remain the gateway for onboarding newly digital merchants. Modular SDKs and low-code integration kits reduce time-to-market for retailers, creating a funnel from basic acceptance tools to premium SaaS subscriptions. This stacking effect is central to long-term monetization within the India real-time payments industry.

By Deployment Mode: Cloud Infrastructure Dominates Scalability Requirements

With 77.90% share in 2025, cloud environments support daily peaks that often cross 600 million transactions. Public-cloud providers have opened India-specific regions to comply with RBI data-localization norms, encouraging banks to lift-and-shift middleware workloads. During festival periods the elasticity of autoscaling clusters prevents brownouts that would otherwise occur on fixed on-premise servers, safeguarding the reputation of the India real-time payments market.

On-premise deployments grow at 21.7% CAGR, powered by public-sector banks and electricity boards that must retain citizen data within government-owned facilities. Hybrid architectures use cloud bursting for compute-intensive fraud detection while holding personally identifiable information on private racks, combining compliance with cost efficiency.

By Enterprise Size: SMEs Drive Democratization of Digital Payments

SMEs process more than 200 monthly digital transactions today versus fewer than 50 in 2020. Their 25.5% CAGR mirrors a behavioural reset as customers switch from cash to scan-and-pay for groceries and services. Government training camps and zero-fee QR kits lower onboarding friction, making the India real-time payments market central to micro-enterprise formalization.

Large enterprises still hold 57.40% of 2025 value due to high-ticket electric-utility, telecom, and e-commerce payments. They lean on advanced dashboards that reconcile thousands of sub-merchant accounts in real time, optimising treasury operations and cash forecasting. The widening availability of those dashboards to midsize firms will further equalise competitive capabilities across tiers within the India real-time payments market.

By End-User Industry: Government Sector Emerges as Growth Leader

Digital public-finance reforms are propelling a 27.75% CAGR in government usage. Real-time settlement of taxes, fines, and welfare remittances reduces leakage and enhances audit trails, positioning India as a frontrunner in public-sector fintech adoption. Smart metering schemes in electricity distribution companies now default to instant UPI payment links, cementing public-sector volumes in the India real-time payments market.

Retail & e-commerce maintains the largest 32.10% slice of 2025 spend. Seamless checkout flows and contextual embedded credit at the moment of purchase maintain momentum, while BFSI continues integrating programmable payment messaging into core banking stacks. Healthcare, education, and transport corridors such as metro rail are next in line to embed real-time payment triggers, expanding the industry’s surface area.

Geography Analysis

Metropolitan hubs, Mumbai, Delhi, Bengaluru, and Chennai, generated 44.20% of aggregate transaction value in 2025, yet their dominance is tapering as tier-2 and tier-3 cities produce the bulk of new customer sign-ups. The India real-time payments market is therefore pivoting from value concentration in metros toward volume leadership in smaller cities where QR density has crossed 1,000 per square kilometre in dense commercial pockets. State-level initiatives have accelerated rollout; Karnataka and Tamil Nadu sponsor municipal-tax rebates for merchants adopting digital collections, further lifting penetration.

Rural districts registered a leap to 65% digital-payment penetration from less than 20% in 2020. RBI pilots enabling offline UPI through sound-wave tokens and near-field communication have unlocked commerce in network-dark zones. Northern states, Uttar Pradesh, Bihar, Rajasthan, demonstrate the highest latent potential, with agricultural procurement moving toward same-day wallet credit. The India real-time payments market size attributed to these regions is expected to expand rapidly once fibre backhaul under BharatNet approaches full reach.

Cross-border extensions now permit Indian tourists to scan UPI codes in Nepal, Bhutan, and Singapore, broadening foreign-currency inflows for domestic PSPs. Such linkages introduce new settlement complexities but solidify India’s ambition to export its home-grown protocol. Divergent regional preferences persist; southern consumers lean on wallet overlays, whereas northern users prefer direct bank payments. PSPs therefore adapt interface vernacular, settlement windows, and promotional structures to local expectations, a hallmark of geographic granularity within the India real-time payments market.

Competitive Landscape

PhonePe’s 48% grip derives from a two-sided merchant-and-consumer acquisition blitz deploying more than 15 million QR stickers nationwide and embedding insurance as well as investment options inside its super-app. Google Pay’s 37% share benefits from Android pre-installation, voice search integration, and a gamified rewards engine. The NPCI has postponed its 30% share-cap enforcement until December 2026, enabling both incumbents to consolidate scale economics before ceding ground to challengers.

Strategic differentiation has shifted toward AI risk-scoring, conversational interfaces, and contextual credit. Amazon Pay streams order-level data from its marketplace into a proprietary decision engine that offers micro-loans at checkout, tightening its surface area across commerce and finance. Meanwhile, Razorpay and Juspay position themselves as infrastructure specialists, white-labelling APIs for banks and emerging fintechs. These partnerships accelerate embedded-finance proliferation without requiring each PSP to build a full stack.

Zero merchant discount‐rate economics compress traditional fee revenue, so players monetise through subscription-based reconciliation dashboards, premium APIs, and cross-sell of investment products. Barriers to entry remain formidable given the liquidity support, cyber-risk defences, and compliance budgets required to operate at 600 million-plus daily transactions. Nonetheless niche upstarts exploit white spaces in healthcare, education, and public utilities where domain depth can offset scale deficits. Overall, the India real-time payments industry demonstrates a classic duopolistic core with a ring of specialised adjacencies.

India Real Time Payments Industry Leaders

PhonePe Private Limited

Google LLC (Alphabet Inc.)

NPCI (National Payments Corporation of India)

Paytm Payments Bank Ltd

PayPal Payments Private Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Juspay raised USD 60 million in Series D funding led by Kedaara Capital to expand rule-based fraud-mitigation engines, sharpening its positioning as an infrastructure layer for banks and fintechs.

- April 2025: Easebuzz secured USD 30 million from Bessemer Venture Partners, directing proceeds toward plug-and-play payment modules for midsize merchants, an attractive white-space as SME volumes surge.

- March 2025: Pine Labs announced plans for a USD 1 billion IPO in 2H 2025 while unveiling Pay-by-Link for offline merchants, highlighting a pivot from card-terminal heritage toward omnichannel real-time payments.

- January 2025: BharatPe detailed a two-year IPO roadmap centred on EBITDA-positive operations and planned co-branded credit-card launches, emphasising diversification beyond QR code acceptance.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the India real-time payments market as the total value of domestic account-to-account transfers that clear, settle, and provide irrevocable confirmation in sixty seconds or less on 24 x 7 rails such as the Unified Payments Interface (UPI) and Immediate Payment Service (IMPS). Transactions routed through card networks, deferred-net settlement batches, or cross-border corridors fall outside this boundary.

Scope Exclusions: Wallet top-ups, card-based fast-payment programs, and crypto rails are excluded.

Segmentation Overview

- By Transaction Type

- Peer-to-Peer (P2P)

- Peer-to-Business (P2B)

- By Component

- Platform / Solution

- Services

- By Deployment Mode

- Cloud

- On-Premise

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By End-User Industry

- Retail and E-Commerce

- BFSI

- Utilities and Telecom

- Healthcare

- Government and Public Sector

- Other End-user Industries

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed payment-system architects, bank digital heads, and large as well as mid-size merchants across Tier 1-3 cities. These conversations clarified merchant discount-rate economics, real-time refund use cases, and likely uptake of credit-on-UPI, allowing us to stress-test desk assumptions and finetune segment shares.

Desk Research

We first mined publicly available data from tier-one sources such as the Reserve Bank of India's monthly payments bulletin, National Payments Corporation of India's UPI and IMPS dashboards, the Ministry of Electronics & IT's Digital Payments reports, and trade bodies like Payments Council of India. Company filings, investor presentations, and reputable business press added adoption metrics, fee structures, and policy updates. Subscription databases, D&B Hoovers for operator financials and Dow Jones Factiva for deal flow, supplied supplemental benchmarks on platform revenues and user counts. These references anchor historical baselines and inform elasticity checks; however, many other secondary sources were also reviewed for cross-validation and context.

Market-Sizing & Forecasting

A top-down and bottom-up hybrid model is employed. We rebuild annual transaction value from RBI clearing statistics, adjust for duplicate routing, and then corroborate totals with sampled acquirer roll-ups and average ticket size x volume checks. Key model drivers include smartphone penetration, active UPI VPA count, merchant QR density, MDR policy direction, and payroll digitization rates, each projected through multivariate regression. Forecast years integrate scenario analysis that flexes QR expansion and credit overlay adoption. Gaps in merchant data are bridged with channel checks before finalizing outputs.

Data Validation & Update Cycle

Outputs undergo variance scans against external indicators, followed by peer review and supervisory sign-off. Models refresh every twelve months, while material policy moves, such as MDR revisions, trigger interim updates, ensuring clients always receive the most current view.

Why Mordor's India Real-Time Payments Baseline Commands Reliability

Published estimates often diverge because firms treat payment scope, settlement speed, and unit pricing in very different ways.

Our disciplined perimeter selection, variable hygiene, and annual refresh mean figures stay traceable and up to date.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.84 B (2025) | Mordor Intelligence | - |

| USD 82.4 B (2024) | Industry Analytics Provider A | Bundles all digital payments, inflating base |

| USD 7.84 B (2024) | Regional Consultancy B | Uses processor revenue proxies, not transfer value |

In sum, the Mordor baseline balances transparent scope, validated indicators, and a repeatable update cadence, giving decision-makers a dependable starting point while spotlighting exactly why competing numbers stray higher or lower.

Key Questions Answered in the Report

What is the current value of the India real-time payments market?

The market stands at USD 9.46 billion in 2026 and is projected to reach USD 24.14 billion by 2031.

Which transaction type is expanding fastest?

Peer-to-business (P2B) payments are advancing at a 23.85% CAGR as QR-code acceptance among small merchants rises.

Why are SMEs adopting real-time payments so quickly?

Zero merchant discount-rate policies and free QR kits have removed entry barriers, leading to a 25.5% CAGR in SME payment volumes.

How do cloud deployments support transaction spikes?

Elastic cloud clusters scale automatically to handle festival surges when volumes climb 300-400%, maintaining system uptime.

What are the main threats to sustained growth?

Fraud via spoof apps and rural network latency can erode user trust and raise failure rates, marginally dampening the market’s CAGR.

Page last updated on: