Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

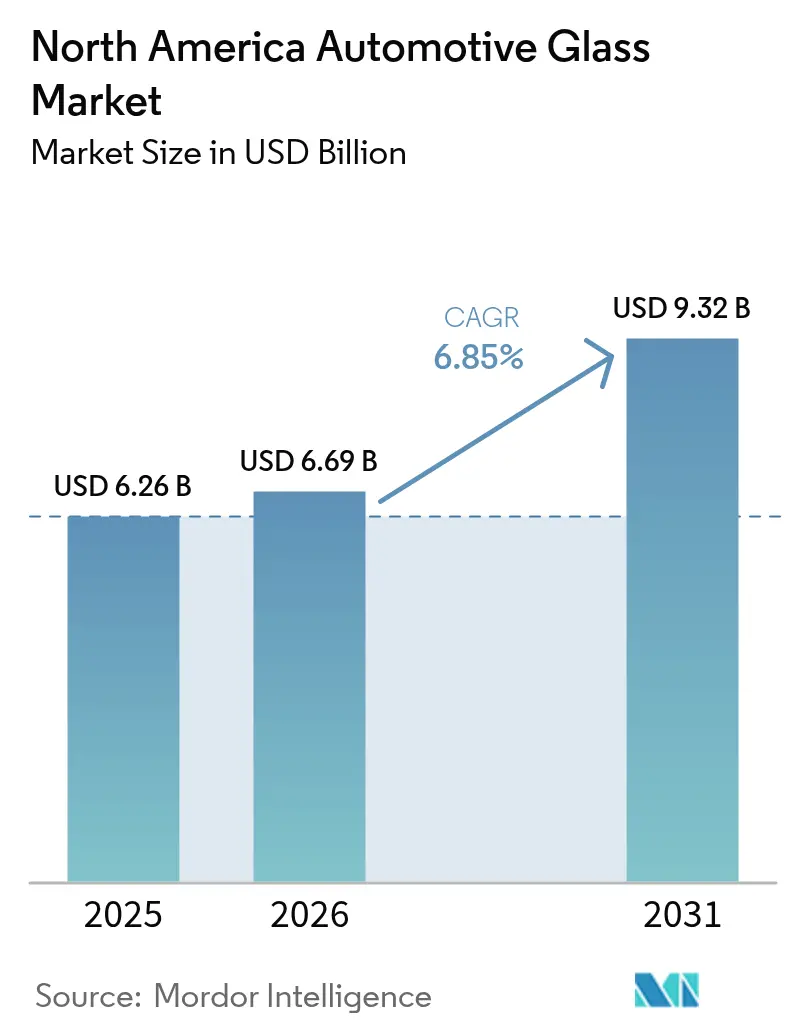

| Base Year Market Size (2025) | USD 6.26 Billion |

| Market Size (2026) | USD 6.69 Billion |

| Market Size (2031) | USD 9.32 Billion |

| Growth Rate (2026 - 2031) | 6.85% CAGR |

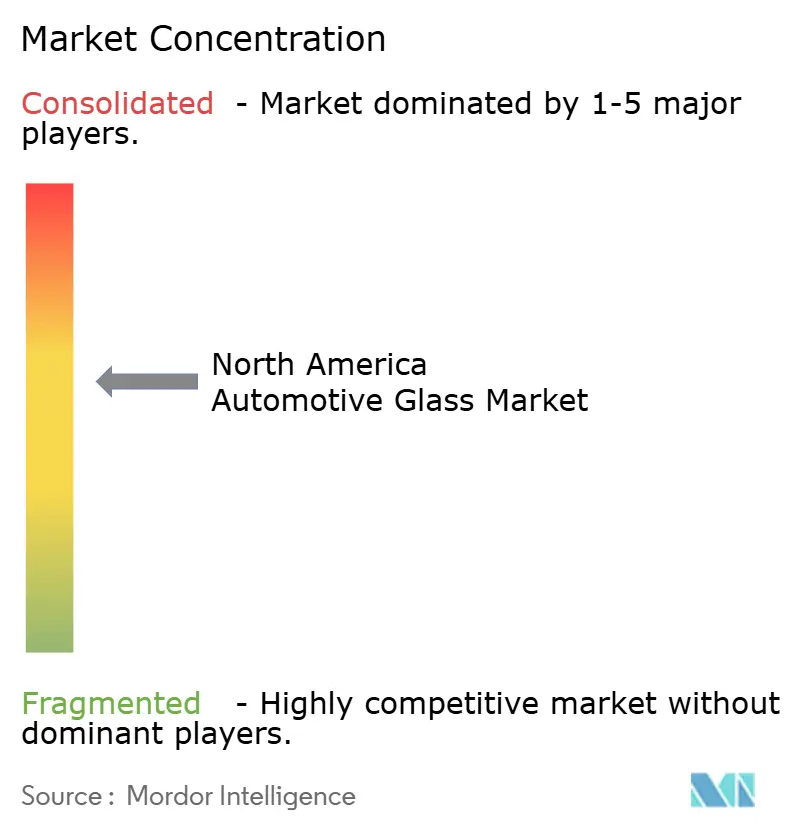

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Automotive Glass Market Analysis by Mordor Intelligence

The North America automotive glass market size is expected to grow from USD 6.26 billion in 2025 to USD 6.69 billion in 2026 and is forecast to reach USD 9.32 billion by 2031 at 6.85% CAGR over 2026-2031. The trajectory reflects a shift away from rounded glazing that meets tougher Federal Motor Vehicle replacement cycles toward value-added Safety Standards, supports the thermal and acoustic needs of battery-electric platforms, and aligns with OEM near-shoring strategies that limit Asia-Pacific supply risk.[1]National Highway Traffic Safety Administration, “Federal Motor Vehicle Safety Standards Overview,” nhtsa.gov Demand is sustained by bundled Advanced Driver Assistance Systems (ADAS) recalibration services, which turn every windshield replacement into a technical procedure and create new aftermarket revenue. Laminated glazing retains the largest position, yet smart or switchable glass gains traction as premium brands mainstream electrochromic features. Windshield units remain the primary volume driver, while panoramic roof innovations lift sunroof demand. Overall, the North America automotive glass market benefits from electrification mandates, regulatory harmonization, and an expanding network of localized float lines that shorten lead times.

Key Report Takeaways

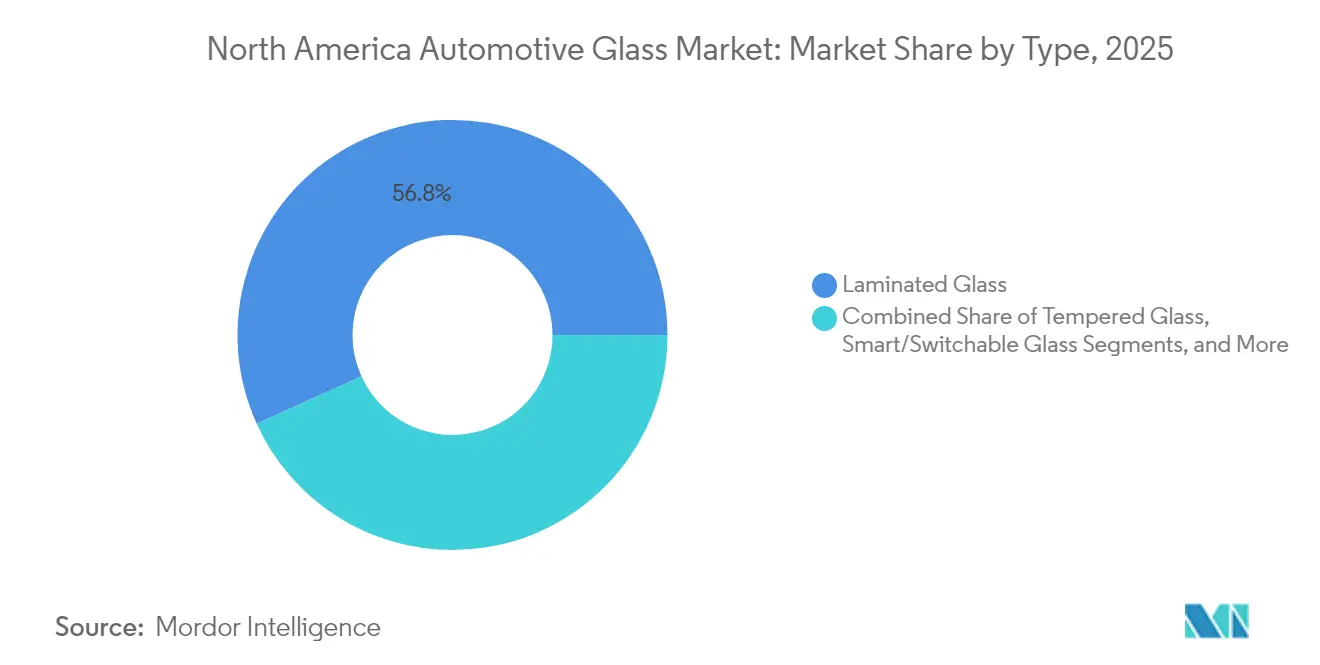

- By type, laminated glazing held 56.78% of the North America automotive glass market share in 2025; smart/switchable glass registers the fastest 8.28% CAGR through 2031.

- By application, windshields accounted for 48.10% share of the North America automotive glass market size in 2025, while sunroof and rooflite units are set to grow at 7.62% CAGR to 2031.

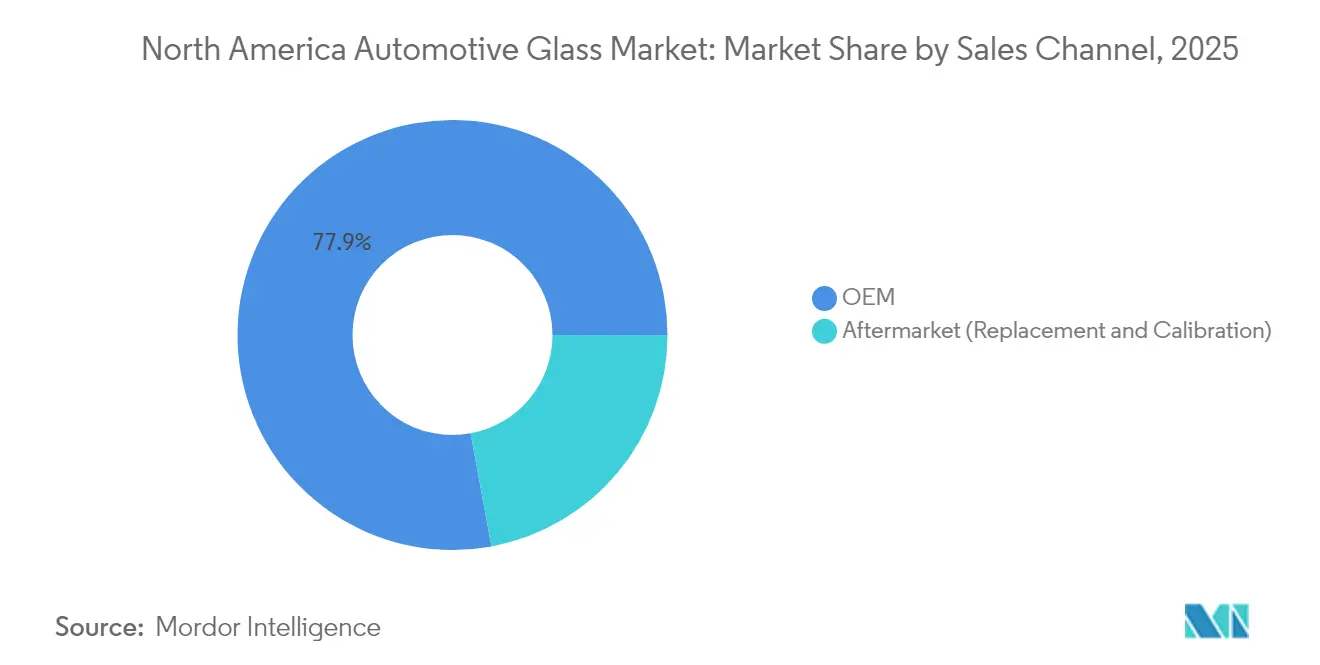

- By sales channel, OEM installations dominated with 77.90% share in 2025, yet the aftermarket is expanding at 8.78% CAGR on the back of ADAS recalibration needs.

- By vehicle type, passenger cars captured 64.60% of volume and are expected to grow at a 6.98% CAGR as electrification reshapes glazing specifications.

- By country, the United States supplied 74.80% of regional revenue in 2025; Canada represents the fastest-growing market with a 7.34% CAGR supported by large-scale EV investments.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Automotive Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart/Switchable Glass Adoption | +1.5% | Premium vehicle segments | Medium term (2-4 years) |

| Bundled ADAS Recalibration Services | +1.3% | Aftermarket channels | Short term (≤ 2 years) |

| Rising Light-Vehicle Production | +1.2% | United States, Canada, Mexico | Medium term (2-4 years) |

| Electrification Push for Lightweight Glass | +1.1% | EV manufacturing hubs | Long term (≥ 4 years) |

| OEM Near-shoring of Glass Supply | +0.9% | United States, Canada, Mexico | Medium term (2-4 years) |

| Stringent FMVSS and Transport Canada Rules | +0.8% | United States, Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid adoption of smart/switchable glass in premium trims

Electrochromic sunroofs, dimmable sidelites, and in-glass displays are crossing from luxury badges into upper-mid trims as OEMs seek cabin differentiation. Gentex ships more than 50 million dimmable devices annually, demonstrating manufacturing maturity that lowers cost barriers.[2]Gentex Corporation, “Dimmable Glass Technologies,” gentex.com Film-based electrochromic stacks trim weight compared with traditional glass-glass cell construction, aligning smart glazing with EV range targets. Added digital layers accommodate heads-up images and driver-monitoring sensors, letting manufacturers bundle safety and infotainment. As regulatory bodies encourage driver-monitoring technology, smart glass adoption rises in parallel, strengthening the North America automotive glass market.

Bundled ADAS recalibration services boosting replacement demand

Camera-based systems mounted on windshields must be recalibrated after glass replacement, turning a once-simple job into an electronics service visit. Insurers now require certified procedures, raising the skill floor for technicians and allowing chains that own calibration equipment to charge premiums. Windshield units grow in billable complexity, and complementary sensor modules on sidelites are also entering the aftermarket mix. The heightened technical barrier lifts revenue per job and helps sustain the North America automotive glass market beyond natural vehicle parc growth.

Rising light-vehicle production across North America

Production is stabilizing near 15.8 million units annually through 2030, reversing earlier trade-related volatility. Battery-electric models are forecast to account for 44.4% of regional output by 2029, up from 7.2% in 2023, while internal-combustion variants will fall below one-third of production. The move toward electric platforms requires thinner laminated assemblies that improve thermal management and reduce drag. Concentrated manufacturing corridors in the so-called auto alley create scale for just-in-time deliveries, further anchoring the North America automotive glass market to domestic output. Although tariffs still pose planning uncertainty, electrification mandates guarantee a long runway for advanced glazing demand.

Electrification push favoring lightweight laminated glazing

Every kilogram removed from an electric vehicle translates into higher usable range, driving OEMs to swap tempered sidelites for thin laminated alternatives that retain strength while cutting mass. Eastman’s Evoca interlayer example highlights how acoustic, solar, and impact performance can be combined in a single laminate aimed at battery-electric side windows. Solar-control coatings reduce HVAC loads that drain batteries, and acoustic layers compensate for the absence of engine noise. Suppliers able to co-extrude multi-function interlayers capture disproportionate growth as the North America automotive glass market shifts toward EV-specific designs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Soda Ash and Interlayer Prices | -0.9% | Global to North America | Short term (≤ 2 years) |

| High Incremental Cost of Smart Glass | -0.7% | Premium segments | Medium term (2-4 years) |

| Capacity Constraints in Low-Iron Float Lines | -0.6% | North America facilities | Medium term (2-4 years) |

| Insurance Preference for Low-cost Glass | -0.5% | United States, Canada aftermarket | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in soda ash, PVB, and EVA interlayer prices

Sekisui Chemical raised PVB prices by 6–15% in late 2024, citing energy and logistics inflation.[3]Sekisui Chemical Co. Ltd., “PVB Interlayer Price Revision,” sekisuichemical.com Sisecam’s acquisition of Ciner Group’s U.S. soda-ash assets concentrates supply at a time when demand is rising toward 83 million tons by 2030. Limited natural soda-ash mines and a small group of global PVB producers give upstream vendors pricing power, squeezing float margins and forcing processors to hedge or vertically integrate. Sudden cost spikes erode profitability across the North America automotive glass market when price pass-throughs lag.

High incremental cost of smart and coated glass solutions

Electrochromic and solar-control packages command price premiums that exceed mainstream willingness-to-pay outside luxury segments. Although film-based assemblies are cheaper than earlier vacuum devices, a panoramic roof equipped with dimmable layers can still add thousands of USD to a build sheet, slowing penetration rates in cost-sensitive trims. Suppliers must subsidize initial programs or bundle the glass with profitable feature packs to achieve scale. Until unit economics improve, the North America automotive glass market will see uneven smart glass adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Smart glass innovation drives premium segment transformation

Laminated glazing generated 56.78% of 2025 revenue in the North America automotive glass market, anchored by its indispensable role in windshields and the growing use of laminated sidelites for security and acoustic comfort. Smart or switchable glass leads to growth with an 8.28% CAGR as electrochromic sunroofs migrate into broader vehicle lines. Tempered panes, once dominant for cost reasons, are slowly being displaced in non-critical areas as manufacturers chase mass savings and higher thermal performance. Coated glass segments expand in parallel, propelled by EV programs that demand low solar heat gain to protect battery range.

Continuous innovation underpins segment momentum. Gentex’s film-based approach trims thickness while enabling large geometric freedom for roof modules. Integrated display technology merges glare control with infotainment, opening new revenue pools for glass makers. Laminated constructions now embed multiple interlayers—acoustic, solar, and structural—demonstrating how a single part can satisfy safety, comfort, and energy efficiency. As technology complexity climbs, suppliers with chemistry, coating, and electronics capabilities deepen their hold on the North America automotive glass market.

By Application: Sunroof innovation accelerates premium feature adoption

Windshields retained a 48.10% share of the North America automotive glass market in 2025, supported by mandatory fitment and strict impact regulations. Sunroof and rooflite modules, however, clock the fastest 7.62% CAGR through 2031 as panoramic roofs become a mainstream styling element. Laminated roof panels integrate electrochromic dimming, UV filtration, and heating grids, enhancing the cabin experience without adding opaque shades.

Sidelites transition from tempered to laminated formats in higher trims, providing burglary resistance and quieter cabins—attributes prized in near-silent EVs. Backlites remain stable in volume, yet see incremental smart features like integrated antennas and defog lines evolve. Exterior mirror glass migrates toward camera-based e-mirrors, reshaping the hardware stack but still relying on precision-polished substrates. Larger apertures and multi-functional coatings raise the engineering bar and reinforce OEM dependency on experienced glazing partners within the North America automotive glass market.

By Sales Channel: Aftermarket complexity drives service premiums

OEM installations delivered 77.90% of unit demand in 2025, a natural outcome of every new vehicle needing factory glass. Even so, the aftermarket’s 8.78% CAGR outpaces OEM growth because ADAS calibration turns replacements into high-ticket procedures. Calibration rigs, target boards, and software subscriptions create steep capital requirements, steering volume toward chains with nationwide footprints and insurance partnerships.

Specialty service packages bundle windshield replacement, camera recalibration, and sometimes wheel alignment, reflecting the interdependence of modern safety systems. Independent shops must invest or exit, accelerating consolidation. At the same time, e-commerce-enabled mobile installers thrive on convenience, but they must still subcontract calibration to licensed centers. The shift from commodity glass to integrated service explains why the North America automotive glass market commands higher average revenue per job than a decade ago.

By Vehicle Type: Passenger-car electrification drives glass innovation

Passenger cars captured 64.60% of the 2025 share and are forecast to advance at a 6.98% CAGR, steered by the rapid electrification of sedans, hatchbacks, and SUVs. The passenger cohort’s appetite for panoramic roofs and dimmable glass elevates value per vehicle. Sport-utility models, in particular, allocate more roof real estate to glass, rewarding suppliers able to laminate large, curved panels.

Light commercial vans benefit from fleet electrification and last-mile delivery growth, demanding thermal coatings that moderate cabin heat during frequent stops. Medium and heavy trucks follow regulatory upgrades requiring laminated side windows for rollover integrity. Across everybody styles, EV platforms impose new constraints on mass and thermal behavior, leading OEMs to specify advanced laminates with multi-function coatings. These shifts feed steady demand into the North America automotive glass market over the next five years.

Geography Analysis

The United States anchors the North America automotive glass market with 74.80% revenue in 2025. Domestic production is steady at roughly 15.8 million light vehicles per year, while regulatory rigor under FMVSS 205 nurtures continuous product upgrades. ADAS proliferation, high sunroof take-rates, and strong aftermarket networks enable premium glazing adoption. U.S. float lines also enjoy Buy America preference for federal fleet procurements, making them the go-to source for OEMs that want to avoid potential tariff exposure.

Canada records the fastest expansion at a 7.34% CAGR to 2031. Massive EV commitments—Honda’s CAD 15 billion value-chain build-out and Volkswagen’s CAD 7 billion battery plant—will lift local glass demand across windshields, roof modules, and sensor-ready sidelites. Transport Canada’s near-mirror alignment with FMVSS cuts duplicate testing costs, letting suppliers qualify parts once for sales in both countries. Provincial incentives for zero-emission vehicles further accelerate model launches, deepening the growth of the North America automotive glass market in Canada.

Mexico rounds out the region as a cost-competitive production base under the USMCA framework. Although its domestic sales are smaller, export-oriented assembly lines require synchronized glazing supply. Low labor costs attract additional lamination and back-lite lines, and proximity to U.S. distribution hubs reduces shipping lead times. As OEMs diversify supply chains, Mexico remains integral to the operational backbone of the North America automotive glass market.

Competitive Landscape

The North America automotive glass market displays moderate concentration. AGC Inc., Saint-Gobain Sekurit, Fuyao Glass, and NSG Group collectively control a majority of OEM volume, leveraging global scale and local float furnish. Technology specialists such as Gentex focus on smart‐glass niches, shipping electrochromic modules that command premium margins.

Capacity expansion underscores strategic intent. Fuyao’s USD 400 million upgrade in Illinois, announced in March 2025, adds 280,000 tons of float output, supporting both OEM and aftermarket customers. Gentex’s acquisition of VOXX International’s automotive assets, completed in April 2025, augments its roof-module and in-vehicle display capabilities, positioning it to bundle glass, electronics, and software in integrated offerings. AGC and Saint-Gobain invest heavily in solar-control and low-iron glass lines to capture EV demand.

Competition is evolving along two axes: cost leadership in commodity panes and technology leadership in multi-function laminates. Commodity suppliers chase throughput and yield, while tech leaders race to embed displays, antennas, and heating elements. OEM procurement increasingly values system integration expertise, favoring suppliers who can certify ADAS compatibility and provide data for digital vehicle-health platforms. This feature race defines the trajectory of the North America automotive glass market.

North America Automotive Glass Industry Leaders

AGC Inc.

Saint-Gobain Sekurit

Fuyao Glass Industry Group Co., Ltd.

Vitro S.A.B. de C.V.

Gentex Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Fuyao Glass committed USD 400 million to expand its Decatur, Illinois float plant, boosting premium auto-grade capacity by 280,000 tons.

- February 2025: PGW Auto Glass opened an advanced ADAS calibration center in Houston to enhance safety and service quality.

- January 2025: Gentex showcased film-based electrochromic sunroofs and display-enabled sun-visors at CES 2025, signaling next-level smart glass integration.

- September 2024: PGW Auto Glass acquired PH Vitres d’Autos, adding 22 Canadian locations and expanding its regional footprint.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the North America automotive glass market as all laminated, tempered, coated, and smart glazing that is factory-installed or sold for replacement on passenger cars and commercial vehicles across the United States, Canada, and Mexico. Glass for mirrors, sunroofs, and camera or sensor housings is counted when it is an integral pane or module.

Scope exclusion: building, appliance, and railway flat glass fall outside this assessment.

Segmentation Overview

- By Type

- Laminated Glass

- Tempered Glass

- Coated and Solar-Control Glass

- Smart/Switchable Glass

- By Application

- Windshield

- Sidelite

- Backlite

- Sunroof/Rooflite

- Rear-view and Exterior Mirrors

- By Sales Channel

- OEM

- Aftermarket (Replacement and Calibration)

- By Vehicle Type

- Passenger Cars

- Hatchback

- Sedan

- Sport Utility Vehicle

- Multi-purpose Vehicle

- Light Commercial Vehicles

- Medium and Heavy Commercial Vehicles

- Passenger Cars

- By Country

- United States

- Canada

- Rest of North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed manufacturing engineers at float-glass lines, OEM glazing buyers, and regional aftermarket chains in the U.S. Midwest, Ontario, and northern Mexico. These conversations clarified average selling prices, sensor-ready windshield share, and calibration labor attach rates, letting us reconcile secondary indications and adjust model coefficients.

Desk Research

We began with statutory data sets: U.S. Department of Transportation vehicle build, Statistics Canada motor-vehicle registrations, and Mexico's INEGI production outputs, which anchor unit volumes. Trade flows from UN Comtrade and U.S. International Trade Commission filings helped us observe cross-border movements of HS 700721 and 700729 items. Industry ratios were refined through safety-recall logs from NHTSA and loss-frequency tables published by the Insurance Institute for Highway Safety. Financial clues from SEC 10-Ks, Canadian SEDAR filings, and D&B Hoovers gave revenue guardrails, while technical adoption curves were traced through patents indexed on Questel. The sources listed are illustrative; additional public and subscription materials informed every datapoint used.

Market-Sizing & Forecasting

We constructed a top-down model that scales regional light-vehicle production and parc with vehicle-level glazing area, tempered-to-laminated mix, and replacement incidence. Results were cross-checked through selective bottom-up supplier roll-ups and channel checks. Key variables like SUV share of production, battery-electric penetration, tempered glass price inflation, collision frequency, and smart-glass option take rates feed a multivariate regression that projects values to 2030. Data gaps (e.g. Canada aftermarket volumes) were bridged by applying U.S. incidence ratios adjusted for fleet age.

Data Validation & Update Cycle

Outputs are stress-tested via variance checks against quarterly earnings from listed glass makers and customs trend breaks. Senior analysts review anomalies before sign-off. Reports refresh annually, with interim updates triggered by material events such as major capacity additions or new glazing mandates. Each release undergoes a fresh validation sweep.

Why Mordor's North America Automotive Glass Baseline Commands Confidence

Published figures often diverge because firms pick different service scopes, price mixes, and refresh cadences. Our approach, grounded in consistently reported regulatory, trade, and financial signals, keeps assumptions transparent for planners who need reproducible numbers.

Key gap drivers include: some publishers cap analysis at tempered panes or omit ADAS calibration revenue; others merge building and automotive glazing; several freeze currency at prior-year averages or model only OEM demand, overstating or understating totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.26 B (2025) | Mordor Intelligence | - |

| USD 5.42 B (2024) | Regional Consultancy A | Excludes aftermarket calibration and smart-glass premium; 2024 baseline year |

| USD 8.20 B (2024) | Trade Journal B | Counts tempered panes only yet adds full replacement volumes; ASP inflation assumption unvalidated |

Taken together, the comparison shows that when scope, valuation metrics, and update cadence are harmonized, Mordor's 2025 baseline offers a balanced midpoint and a traceable path forward for decision makers across the North American glazing value chain.

Key Questions Answered in the Report

What is the size of the North America automotive glass market in 2026?

The market is valued at USD 6.69 billion in 2026.

Which glass type is growing the fastest in this market?

Smart/switchable glass leads with an 8.28% CAGR through 2031.

Why is the aftermarket segment expanding quicker than OEM sales?

ADAS-equipped vehicles require precise calibration after glass replacement, boosting aftermarket service demand and driving a 8.78% CAGR.

Which country shows the highest growth rate in North America?

Canada records the fastest growth, advancing at a 7.34% CAGR due to major EV investments.

Page last updated on: