Autologous Matrix-induced Chondrogenesis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

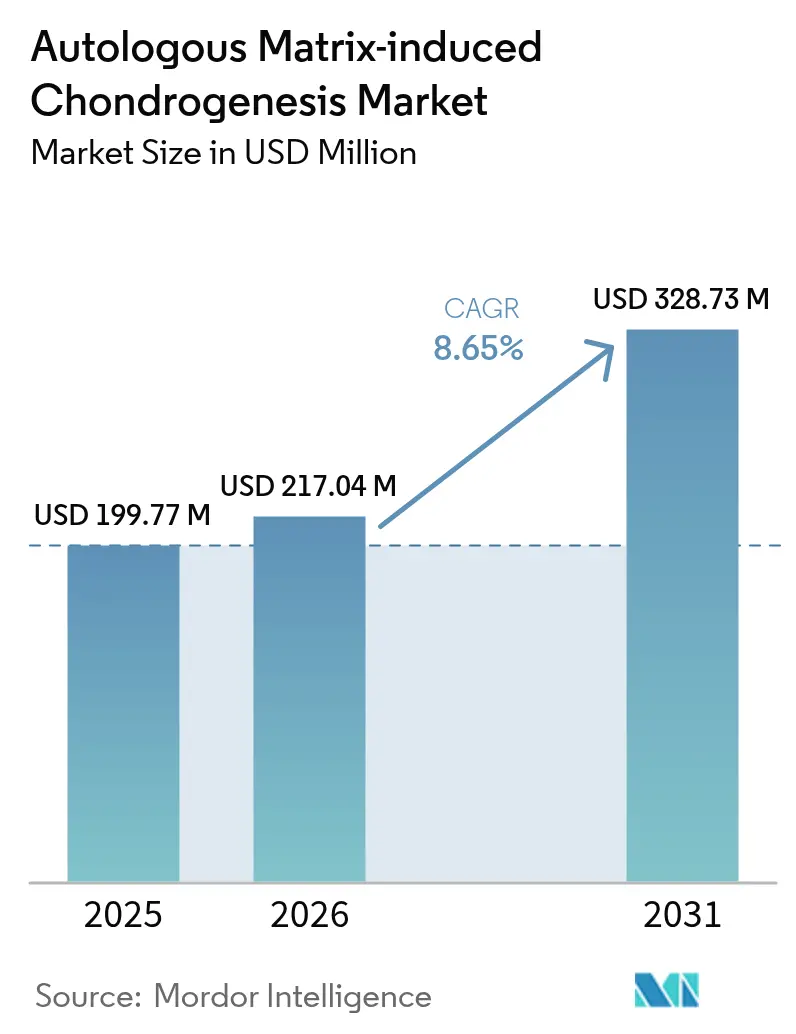

| Market Size (2026) | USD 217.04 Million |

| Market Size (2031) | USD 328.73 Million |

| Growth Rate (2026 - 2031) | 8.65% CAGR |

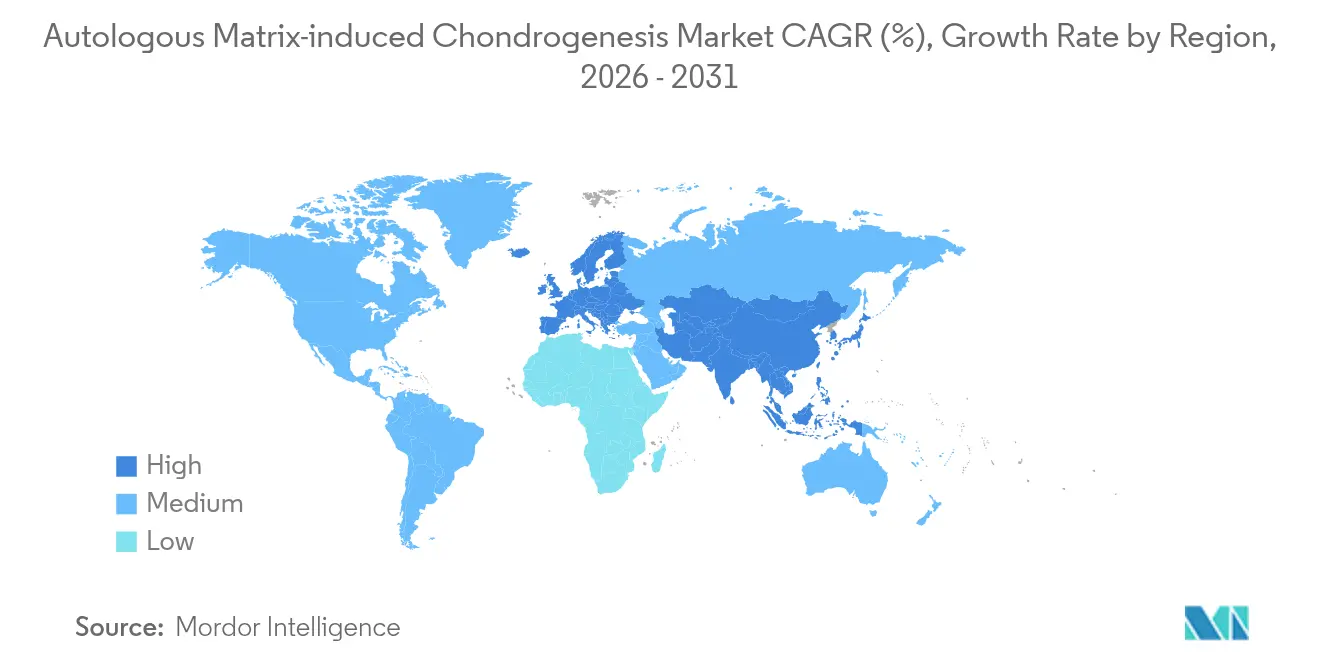

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

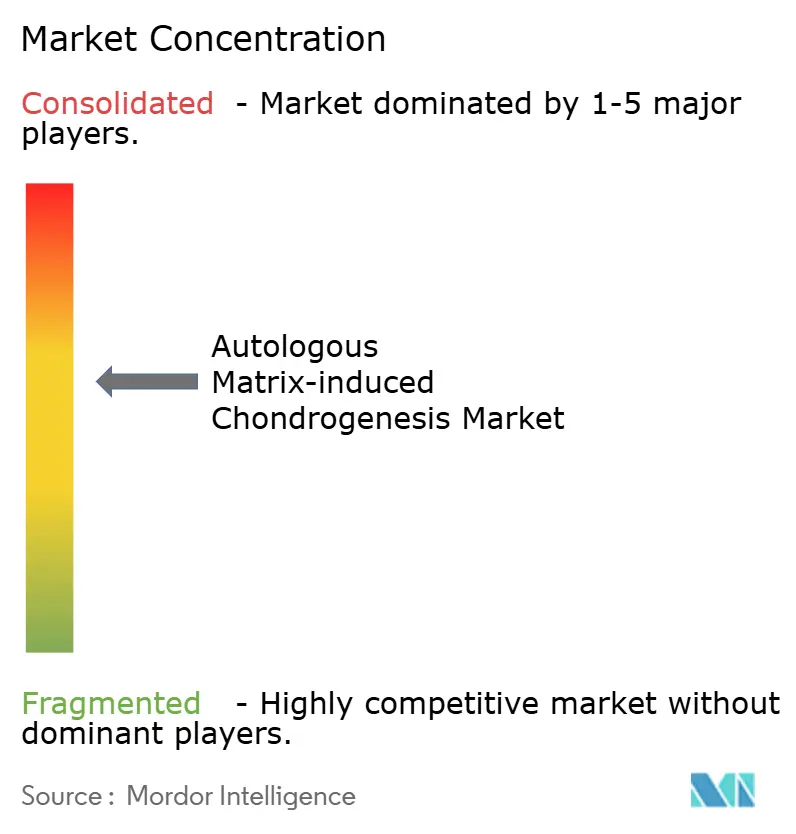

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Autologous Matrix-induced Chondrogenesis Market Analysis by Mordor Intelligence

The Autologous Matrix-induced Chondrogenesis market size is expected to grow from USD 199.77 million in 2025 to USD 217.04 million in 2026 and is forecast to reach USD 328.73 million by 2031 at 8.65% CAGR over 2026-2031. Momentum comes from surgeons seeking a single-stage bridge between conventional microfracture and complex cell-based implants, a niche that AMIC fills by pairing bone-marrow stimulation with a protective scaffold. Rapid uptake of minimally invasive orthopedic techniques, rising outpatient surgery volumes, and continuing FDA clearances sustain demand. Hyaluronic-acid scaffolds remain the preferred material, but chitosan platforms are outpacing rivals as innovation unlocks bioactive, drug-delivering hydrogels. North America retains leadership thanks to reimbursement alignment and strong clinical evidence, while Asia-Pacific records the fastest expansion on the back of infrastructure investments and growing sports participation.

Key Report Takeaways

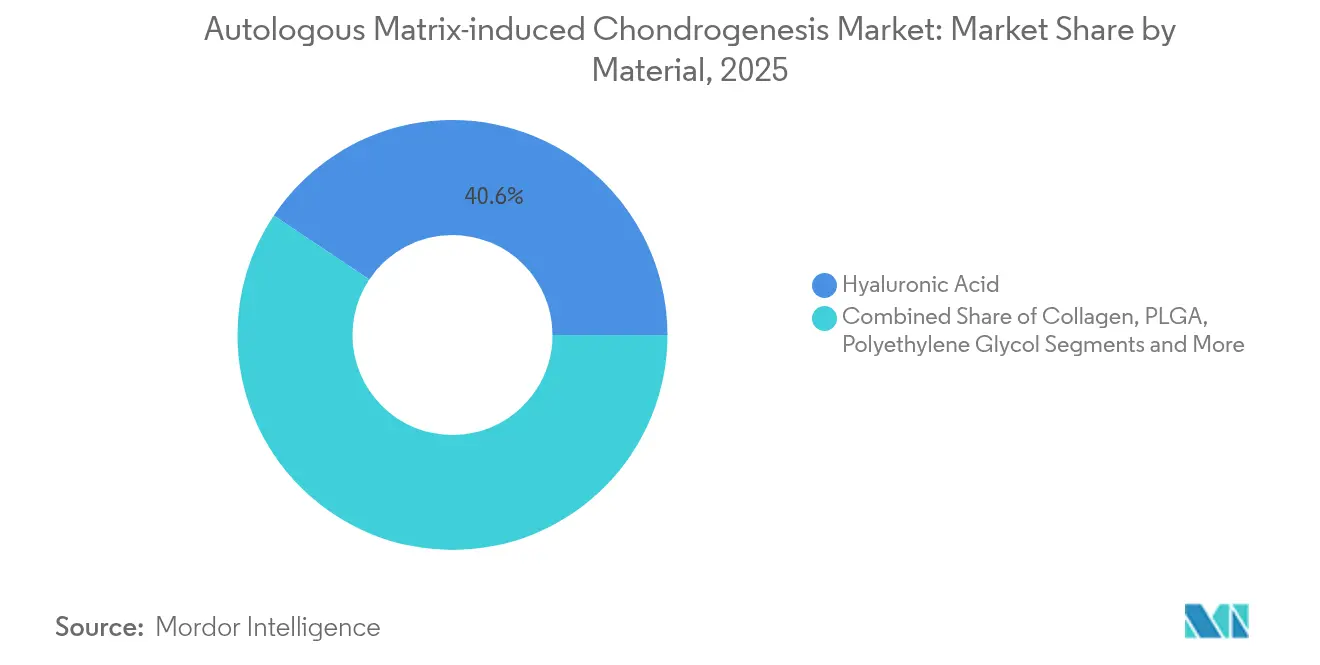

- By material, hyaluronic acid captured 40.62% of Autologous Matrix-induced Chondrogenesis market share in 2025, while chitosan and other novel biomaterials are projected to grow at an 11.35% CAGR through 2031.

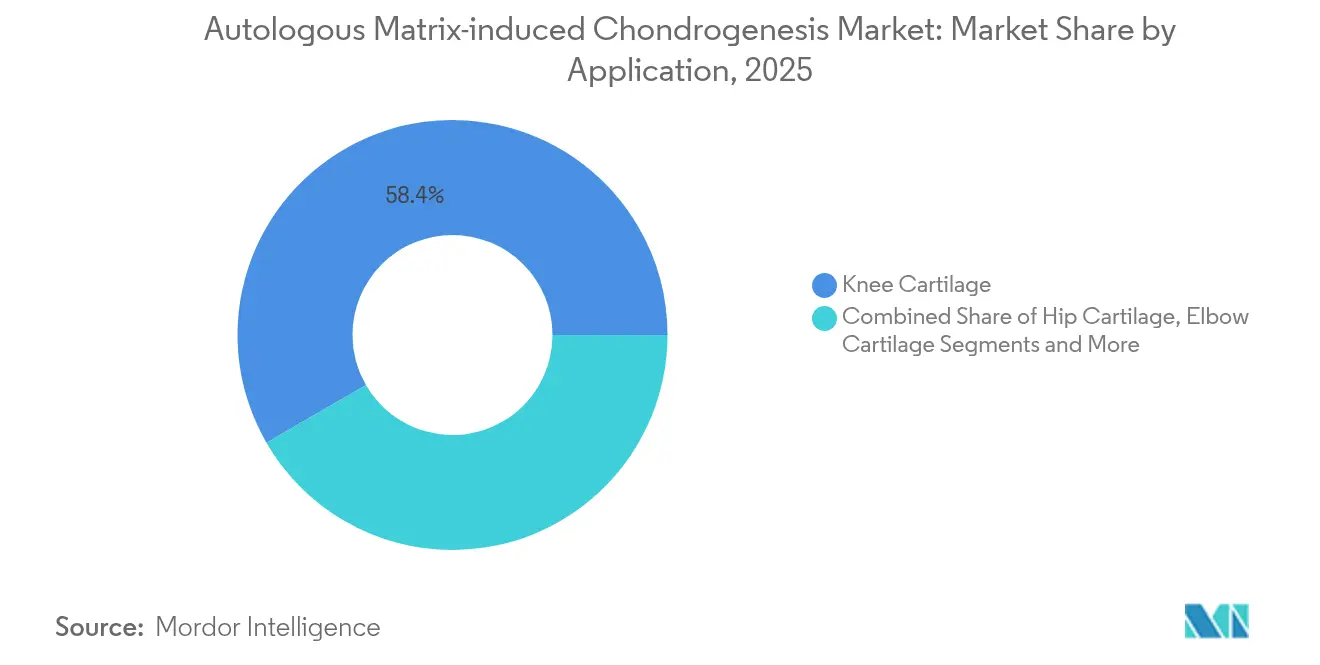

- By application, knee cartilage held 58.35% of the Autologous Matrix-induced Chondrogenesis market size in 2025; hip cartilage is forecast to expand at a 12.02% CAGR to 2031.

- By end user, hospitals led with 52.67% revenue share in 2025, whereas ambulatory surgery centers are advancing at an 10.78% CAGR through 2031.

- By geography, North America commanded 36.20% share of the Autologous Matrix-induced Chondrogenesis market in 2025, while Asia-Pacific is poised for a 10.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Autologous Matrix-induced Chondrogenesis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Osteoarthritis & Cartilage Injuries | +2.1% | Global, with highest impact in North America and Europe | Medium term (2-4 years) |

| Growing Sports‐Related Trauma Cases Worldwide | +1.8% | Global, particularly Asia-Pacific and North America | Short term (≤ 2 years) |

| Accelerating Demand For Minimally-Invasive Orthopedic Procedures | +2.3% | Global, led by developed markets | Medium term (2-4 years) |

| Expanded Reimbursement For Knee Cartilage Repair | +1.2% | North America and Europe primarily | Long term (≥ 4 years) |

| Surge In Outpatient Ambulatory Surgery Centers Adopting AMIC | +1.9% | North America, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Development Of Next-Gen Photo-Cross-Linked HA Scaffolds Enabling Single-Stage Repair | +1.4% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Osteoarthritis & Cartilage Injuries

Global life expectancy is rising, and with it the number of people living long enough to develop degenerative joint disease. Osteoarthritis now affects 27 million Americans, and post-traumatic cases represent another 10-12% of the total, underscoring the unmet clinical need for durable cartilage repair options.[1]Mahammad Gardashli, “Mechanical Loading and Orthobiologic Therapies in the Treatment of Post-Traumatic Osteoarthritis,” Frontiers in Bioengineering and Biotechnology, frontiersin.orgAgainst this backdrop, single-stage AMIC procedures appeal to surgeons because they avoid expensive cell-expansion steps while still improving tissue quality. Mid-term evidence shows patients treated with advanced implants experience an 87% lower risk of total knee arthroplasty within four years, strengthening the procedure’s value-based argument. Health systems facing budget pressure see AMIC as a way to delay or even avert joint replacements, which carry higher downstream costs. As populations continue to age and remain active, the steady flow of cartilage lesions should keep demand for single-stage solutions on an upward trajectory.

Growing Sports-Related Trauma Cases Worldwide

Participation in organized sports is rising across youth, amateur, and professional levels, creating a wider injury funnel for orthopedic care. Between 2014 and 2023, U.S. emergency departments recorded more than 843,000 soccer-related lower-extremity injuries, of which ankle issues accounted for 36.39%. Professional basketball mirrors that burden, with musculoskeletal problems making up 65.54% of all health events and the knee alone representing nearly one quarter.[2]Vangelis Sarlis, “Injury Patterns and Impact on Performance in the NBA League Using Sports Analytics,” Computation, mdpi.com AMIC’s minimally invasive approach returns 80.8% of talus-lesion athletes to sport within roughly 43 months, a statistic that resonates with players and teams focused on rehabilitation speed.[3]Riccardo D’Ambrosi, “Return to Sport After Arthroscopic Autologous Matrix-Induced Chondrogenesis for Osteochondral Lesion of the Talus,” Clinical Journal of Sport Medicine, journals.lww.com Surgeons therefore view AMIC as a pragmatic bridge between conservative management and joint-replacement extremes. Continued growth in global sports participation—especially in Asia-Pacific—will enlarge the candidate pool for cartilage-preserving technologies.

Accelerating Demand for Minimally Invasive Orthopedic Procedures

Health-care delivery is shifting rapidly from inpatient wards to outpatient suites, driven by payer mandates and patient preference. Ambulatory surgery centers already conduct 72% of U.S. operations and can operate at 45-60% lower cost than hospital outpatient departments. The Centers for Medicare & Medicaid Services has amplified this migration by adding new orthopedic codes to the ASC list and boosting reimbursement by 3.1% for qualifying facilities. Technological enablers such as AI-guided needle arthroscopy make it possible to perform single-stage cartilage repair through portals barely wider than a biopsy needle, which reduces soft-tissue trauma and shortens recovery time.[4]Alex B. Walinga, “Needle Arthroscopy for Osteochondral Lesions of the First Metatarsophalangeal Joint: A Standardized Approach,” PubMed, pubmed.ncbi.nlm.nih.gov With patient-reported satisfaction hitting 92% in ASC settings and wait times falling by one-fifth, the outpatient model provides fertile ground for AMIC adoption.

Development of Next-Gen Photo-Cross-Linked HA Scaffolds Enabling Single-Stage Repair

Material science is pushing hyaluronic-acid scaffolds far beyond simple viscoelastic fillers. Injectable HA hydrogels that carry transforming growth factor-beta 3 stimulate robust chondrogenesis, leading to thicker and more organized cartilage repair in preclinical models. Photo-cross-linking further stabilizes these constructs, allowing surgeons to shape and cure the scaffold directly inside the defect during arthroscopy, which simplifies workflow and cuts operating time. Commercial systems such as HyaloFAST have entered routine clinical use, validating the regulatory path for bioactive, single-stage implants. Early clinical programs report faster functional recovery and reduced donor-site morbidity compared with two-stage cell therapies. As manufacturing platforms mature and costs decline, these advanced HA scaffolds are expected to widen AMIC’s addressable market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Uncertain Long-Term Clinical Outcomes Beyond 10 Years | -1.8% | Global, particularly in evidence-based healthcare systems | Long term (≥ 4 years) |

| Limited Surgeon Proficiency Outside Tier-1 Orthopedic Hubs | -1.2% | Emerging markets and rural areas globally | Medium term (2-4 years) |

| High Procedure & Scaffold Costs Vs. Microfracture | -1.5% | Cost-sensitive markets, particularly emerging economies | Short term (≤ 2 years) |

| Regulatory Lag For Novel Biomaterials | -0.9% | Global, with varying impact by regulatory jurisdiction | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Uncertain Long-Term Clinical Outcomes Beyond 10 Years

Five-year survivorship for AMIC reaches 85% in the knee and 89% in the ankle, yet most payers and guideline panels demand 15-year durability before revising standard-of-care recommendations. Younger, highly active patients may therefore be steered toward treatments with longer historical datasets even if early AMIC outcomes appear superior. Technique heterogeneity—ranging from scaffold composition to fixation strategy—complicates pooled analysis and blunts the power of meta-studies. Inconsistent rehabilitation protocols add further variability, making it harder for insurers to model lifetime cost-effectiveness. Until long-term registries mature, conservative reimbursement policies will continue to cap procedure volumes.

Limited Surgeon Proficiency Outside Tier-1 Orthopedic Hubs

AMIC demands precise defect debridement, subchondral micro-perforation, and scaffold handling skills that are rarely mastered during general residency. Surgeons in rural hospitals or emerging markets often lack structured training pathways and may default to microfracture, which is simple and instrument-light. Insufficient hands-on exposure also raises complication risks, discouraging early adopters and fueling skepticism among referral networks. Device makers run cadaver labs and virtual modules, but high travel and equipment costs limit uptake in low-resource settings. The skills gap thus slows equitable geographic diffusion of AMIC, confining volumes to high-volume centers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Hyaluronic Acid Sustains Leadership While Chitosan Gains Pace

Hyaluronic-acid constructs held 40.62% of Autologous Matrix-induced Chondrogenesis market share in 2025. Their innate presence in synovial fluid supports cellular adhesion and protects against degradation, a blend of benefits that keeps surgeons loyal. The segment has also produced the highest volume of peer-reviewed evidence, reducing regulatory friction in key markets. Nevertheless, chitosan’s 11.35% CAGR shows buyers value its antimicrobial traits, mesenchymal-cell compatibility, and tunable degradation. Novel formulations embed mesoporous silica nanoparticles to drive chondrogenesis, positioning chitosan as the likely next frontier. Manufacturers are scaling multizonal constructs that mirror cartilage-subchondral gradients, a development that broadens indications.

In parallel, collagen membranes retain a substantial installed base thanks to long clinical familiarity and versatile handling. PEG and PLGA designs meet niche needs where mechanical strength or slow resorption is mandatory. The Autologous Matrix-induced Chondrogenesis market size for hyaluronic-acid products is forecast to reach USD 133.6 million by 2031, whereas chitosan is set to deliver the fastest absolute gains. As cost pressures rise, suppliers capable of lowering unit prices without sacrificing bioactivity will secure a decisive foothold.

By Application: Knee Dominance Faces Hip-Segment Upswing

Knee cases accounted for 58.35% of the Autologous Matrix-induced Chondrogenesis market size in 2025, reflecting high injury incidence and arthroscopic accessibility. Surgeons deploy AMIC for focal defects, osteochondritis dissecans, and combined meniscal lesions, confident in workflows refined over two decades. However, hip procedures now show the sharpest growth, clocking a 12.02% CAGR as nanosurgery and cartilage-engineering protocols move from trials to operating rooms. Visual Analog pain scores have fallen from 7.8 to 0.2 in recent randomized studies, encouraging conservative surgeons to adopt the technique.

The ankle & talus segment benefits from promising return-to-sport data, while shoulder, elbow, and smaller joints fill out the specialty pipeline. As robotics and imaging innovations shrink portal sizes and boost precision, more surgeons will expand indications beyond the knee, diluting historical concentration. The emerging evidence base suggests hip outcomes may quickly rival knee benchmarks, driving up procedure volumes.

By End User: Ambulatory Surgery Centers Reshape Delivery Economics

Hospitals retained 52.67% revenue share in 2025, leveraging integrated imaging, anesthetic support, and the ability to handle complex revisions. Yet the growth axis has pivoted to ambulatory surgery centers, which are adding operating rooms, imaging pods, and sterilization suites tailored for single-stage orthopedics. The segment’s 10.78% forecast CAGR reflects payer preference for lower-cost sites that still meet quality targets. Autologous Matrix-induced Chondrogenesis market participants now bundle implants, instruments, and digital-workflow tools to help ASCs meet accreditation and inventory requirements.

Orthopedic and sports-medicine clinics occupy a middle ground, functioning as referral hubs that capture pre-operative evaluation and post-operative rehabilitation. Their procedural share will remain steady as they deepen expertise and play a central role in training surgeons new to AMIC.

Geography Analysis

North America led the Autologous Matrix-induced Chondrogenesis market with a 36.20% share in 2025. The region benefits from clear FDA pathways, growing ASC penetration, and outcome-based payment models rewarding joint-preservation strategies. Recent MACI Arthro and RejuvaKnee approvals further validate the technology pipeline, giving surgeons confidence to broaden indications. Commercial payers increasingly bundle reimbursement for single-stage repairs, reducing the financial uncertainty once tied to scaffold use.

Europe follows closely, propelled by strong university–industry collaboration and a tradition of regenerative-medicine research. CE-marked scaffolds such as Chondro-Gide maintain wide adoption, and national health systems evaluate AMIC in cost-utility studies that may unlock broader coverage. Meanwhile, Latin America continues to invest in sports-injury clinics and public-private orthopedic centers, presenting growth opportunities for suppliers willing to offer tiered pricing and onsite training.

Asia-Pacific is the fastest-expanding territory at a 10.62% CAGR. Governments are channeling resources into hospital build-outs, while aging populations push elective-joint workloads higher. China champions domestic scaffold manufacturing and has begun reimbursing select cartilage procedures, lowering entry barriers for global brands through joint ventures. Japan leverages its robotics ecosystem to refine hip and ankle arthroscopy, while India’s National Medical Devices Policy supports local production of cost-effective implants. Southeast Asian nations, once reliant on medical tourism, are installing ASC networks that favor single-stage cartilage repair. Rising youth-sports injury rates—37.5% knee injuries among school footballers in some regions—underscore latent demand.

Collectively, these dynamics will lift regional contributions and diversify revenue streams, reducing the Autologous Matrix-induced Chondrogenesis market’s historical reliance on mature Western economies.

Competitive Landscape

The Autologous Matrix-induced Chondrogenesis market features moderate concentration. Multinational orthopedic groups pursue strategic acquisitions and organic R&D to integrate AMIC into broader sports-medicine portfolios. Smith+Nephew completed a USD 180 million purchase of CartiHeal, adding a coral-based implant that addresses early osteoarthritis and expanding its value proposition beyond microfracture adjuncts. Zimmer Biomet pairs its biologics catalog with AI-enabled imaging through the OrthoGrid buyout, while simultaneously rolling out a cementless partial-knee platform that simplifies conversion to joint replacement if cartilage repair fails.

Geistlich capitalizes on decades of collagen-membrane research, positioning Chondro-Gide as the trusted backbone for bone-marrow stimulation. Vericel breaks new ground with MACI Arthro, the first FDA-cleared cellularized scaffold deployable via arthroscopy, opening AMIC to a wider surgeon cohort. Competitive edges increasingly hinge on ecosystem support—robot-compatible instruments, cloud-based outcome tracking, and surgeon-education portals—rather than stand-alone implant performance.

White-space opportunities reside in emerging markets where price sensitivity is acute. Vendors focused on cost-optimized chitosan or hybrid scaffolds that require minimal capital equipment stand to expand access. Regulatory convergence and fast-track pathways for breakthrough biomaterials may cut commercialization timelines, intensifying rivalry but also accelerating technology diffusion.

Autologous Matrix-induced Chondrogenesis Industry Leaders

Anika Therapeutics, Inc.

B. Braun SE

Smith+Nephew

Zimmer Biomet Holdings

Geistlich Pharma AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Smith+Nephew showcased advanced robotic-ready knee, hip, and shoulder reconstruction technologies at AAOS 2025, reinforcing its commitment to precision surgery

- January 2025: CartiHeal’s Agili-C implant gained momentum as surgeons highlighted real-world outcomes for cartilage lesions.

- October 2024: Anika set plans to divest Arthrosurface and Parcus Medical, sharpening its focus on core regenerative platforms.

- October 2024: Regenity Biosciences secured FDA 510(k) clearance for the RejuvaKnee meniscus implant, marking its 60th regulatory milestone.

Global Autologous Matrix-induced Chondrogenesis Market Report Scope

As per the scope of the report, AMIC is a single-stage cartilage regeneration approach in which a cell-free collagen matrix is implanted into a defective cartilage, combined with microfracture. These treatments have proven better outcomes as compared to conventional techniques.

The autologous matrix-induced chondrogenesis market is segmented by material (hyaluronic acid, collagen, polyethylene glycol (PEG), poly lactic-co-glycolic acid (PLGA), and other materials), application (knee cartilage, elbow cartilage, and other applications), and geography (North America, Europe, Asia-Pacific, Middle East, and Africa, South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally.

The report offers the value (in USD) for the above segments.

| Hyaluronic Acid |

| Collagen |

| Polyethylene Glycol (PEG) |

| Poly Lactic-co-glycolic Acid (PLGA) |

| Chitosan & Other Materials |

| Knee Cartilage |

| Hip Cartilage |

| Elbow Cartilage |

| Ankle & Talus Cartilage |

| Other Joints |

| Hospitals |

| Ambulatory Surgery Centers |

| Orthopedic & Sports Medicine Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material | Hyaluronic Acid | |

| Collagen | ||

| Polyethylene Glycol (PEG) | ||

| Poly Lactic-co-glycolic Acid (PLGA) | ||

| Chitosan & Other Materials | ||

| By Application | Knee Cartilage | |

| Hip Cartilage | ||

| Elbow Cartilage | ||

| Ankle & Talus Cartilage | ||

| Other Joints | ||

| By End User | Hospitals | |

| Ambulatory Surgery Centers | ||

| Orthopedic & Sports Medicine Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the Autologous Matrix-induced Chondrogenesis market?

The Autologous Matrix-induced Chondrogenesis market is valued at USD 217.04 million in 2026.

How fast is the Autologous Matrix-induced Chondrogenesis market expected to grow?

It is projected to expand at an 8.65% CAGR, reaching USD 328.73 million by 2031.

Which material segment leads the Autologous Matrix-induced Chondrogenesis market?

Hyaluronic-acid scaffolds command the largest share at 40.62%, thanks to strong biocompatibility data.

Which region is growing the fastest in the Autologous Matrix-induced Chondrogenesis market?

Asia-Pacific shows the highest growth, forecasting a 10.62% CAGR through 2031.

Why are ambulatory surgery centers important for AMIC adoption?

ASCs offer lower costs and shorter wait times, and their outpatient setting fits the single-stage AMIC workflow, propelling an 10.78% CAGR for this end-user segment.o forecasts the Autologous Matrix-induced Chondrogenesis Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

What is the main challenge limiting wider AMIC uptake?

A limited pool of long-term (>10 years) clinical data raises payer and surgeon concerns about durability compared with established microfracture techniques.

Page last updated on: