Austria Data Center Power Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

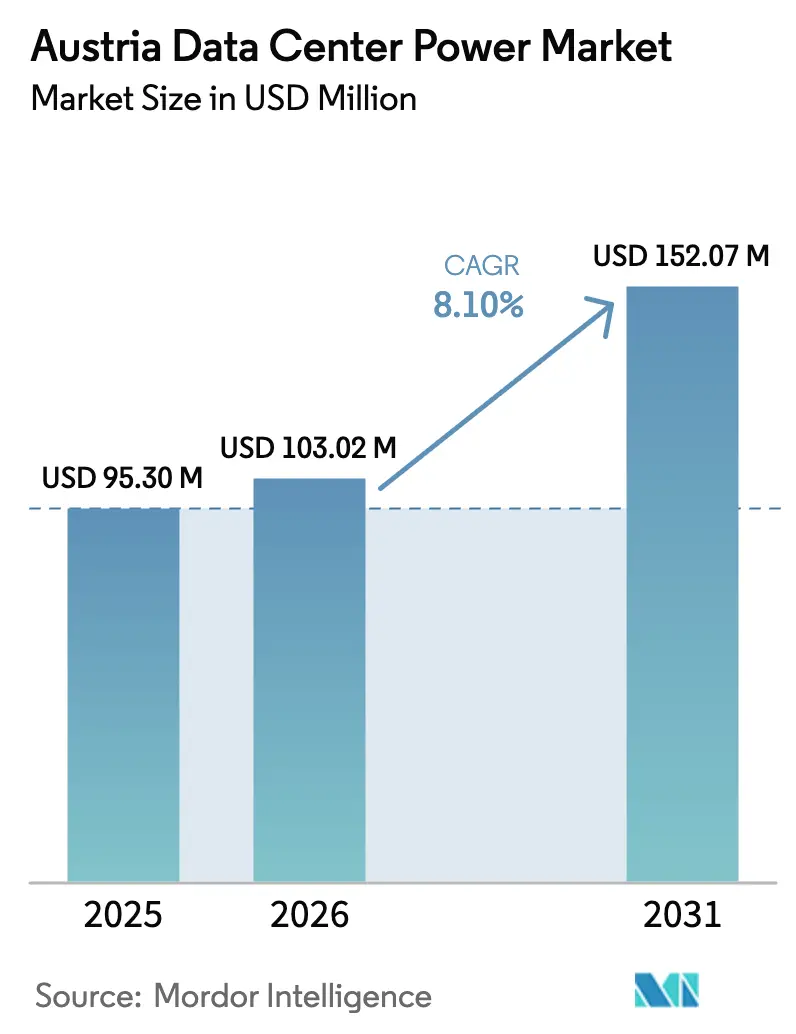

| Base Year Market Size (2025) | USD 95.3 Million |

| Market Size (2026) | USD 103.02 Million |

| Market Size (2031) | USD 152.07 Million |

| Growth Rate (2026 - 2031) | 8.10% CAGR |

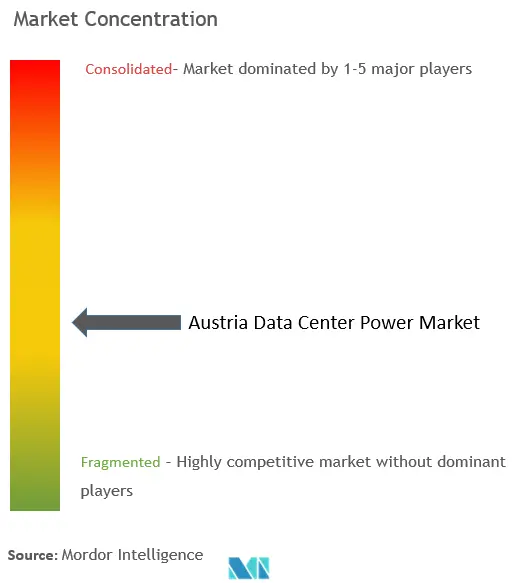

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Austria Data Center Power Market Analysis by Mordor Intelligence

Austria data center power market size in 2026 is estimated at USD 103.02 million, growing from 2025 value of USD 95.3 million with 2031 projections showing USD 152.07 million, growing at 8.10% CAGR over 2026-2031. Investments in grid upgrades, the country’s 92% renewable-electricity mix reached in 2023, and Austria’s legal target of 100% renewable electricity by 2030 combine to create an expanding addressable base of sustainable power infrastructure. Robust capital programs such as the Austrian Power Grid’s decade-long EUR 3.5 billion modernization plan are lifting transmission reliability, which supports higher rack-density deployments in both Vienna and Upper Austria. Hyperscale interest is rising after Google purchased 185 acres in Kronstorf near hydropower sources, signalling a pivot toward mega-scale campuses that can draw on low-carbon electricity at competitive tariffs. Meanwhile, federal procurement rules that mandate 100% green power for public IT workloads by 2027 are pulling demand for efficient switchgear, UPS and battery energy-storage solutions across the country’s public-sector data estates

Key Report Takeaways

- By component, UPS systems led with 27.65% of the Austria data center power market share in 2025, while power distribution units post the fastest 9.78% CAGR through 2031.

- By data-center type, colocation providers held 57.60% of 2025 revenue; hyperscale and cloud sites post the highest 10.72% CAGR to 2031.

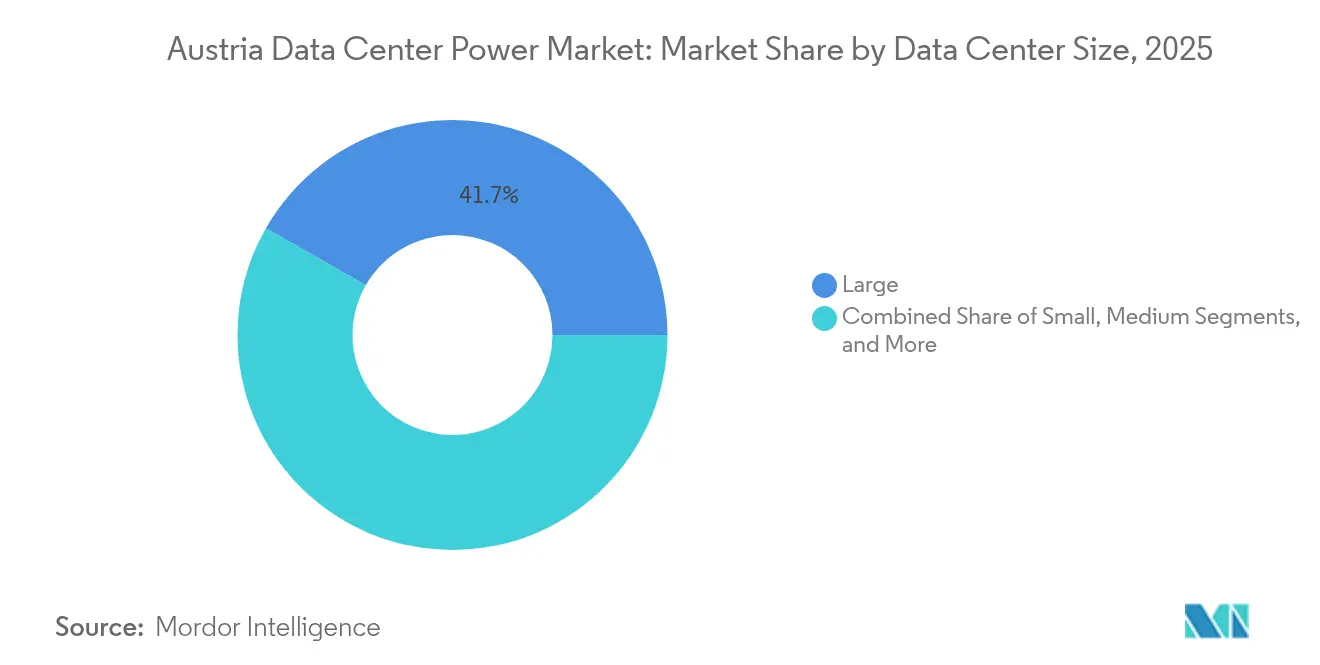

- By size band, large facilities accounted for 41.73% of the Austria data center power market size in 2025; massive facilities expand at a 11.94% CAGR through 2031.

- By tier, Tier III sites dominated with 50.60% share in 2025; Tier IV postings accelerate at 9.05% CAGR across the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Austria Data Center Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale and cloud site adoption | +2.1% | Vienna & Upper Austria | Medium term (2-4 years) |

| Pressure to curb energy-related OPEX | +1.8% | Nationwide | Short term (≤ 2 years) |

| Subsidies for renewable-powered IT loads | +1.5% | Nationwide | Long term (≥ 4 years) |

| Grid-modernisation-led backup upgrades | +1.2% | Vienna, Upper Austria, Styria | Medium term (2-4 years) |

| Federal green procurement mandate (2027) | +0.9% | Nationwide | Short term (≤ 2 years) |

| AI/HPC lab demand for micro-grid capacity | +0.6% | Vienna, Linz, Innsbruck | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Hyperscale and Cloud Facilities

Hyperscale operators are reshaping the Austria data center power market by placing large-footprint campuses close to hydropower plants. Google’s Kronstorf land purchase exemplifies this trend and is expected to stimulate auxiliary build-outs by power-electronics suppliers and local utilities.[1]Kronstorf Substation Expansion Project, Publisher: SPIE, URL: spie.com The hyperscale segment’s forecast 11.2% CAGR aligns with Austria’s electricity mix, where 85% already comes from renewables, mostly hydro and biomass. Vantage Data Centers’ EUR 1.4 billion EMEA expansion, announced in February 2025, includes capacity earmarked for the Austrian node of its regional platform vantage-dc.com. The Renewable Energy Expansion Act, seeking an extra 27 TWh of clean power by 2030, underpins these operators’ carbon-neutral roadmaps. Local districts and utilities view such projects as anchor loads that justify additional sub-station work and multi-MW grid interconnects

Pressure to Lower Energy-Related OPEX

Removal of temporary power subsidies in January 2025 pushed household electricity bills up 45%, signaling wider tariff inflation for commercial users.[2] Energy in Austria 2024, Publisher: Austrian Energy Regulator, URL: e-control. at To protect margins, operators within the Austria data center power market are adopting battery energy-storage as a service solutions that enable peak-shaving and demand-charge reduction. The nationwide smart-meter roll-out makes flexible tariff procurement feasible, further lowering cost per kWh for facilities that can modulate loads. Partnerships such as Wien Energie’s spare-parts digitisation project show how operational-efficiency tools complement power-cost mitigation partium.io. Government schemes allocating EUR 940 million to transition heating systems indicate a policy environment that generally rewards lower fossil-energy dependency, indirectly benefitting data-center PUE optimisation

Government Subsidies for Renewable-Powered IT Loads

Austria’s Renewable Energy Expansion Act provides about EUR 1 billion yearly in premiums and grants, an incentive pool that improves payback periods for on-site solar, small hydro tie-ins and heat-recovery systems in data centers.[3]Integrated National Energy and Climate Plan, Publisher: Federal Ministry for Climate Action, URL: bmk.gv.at The integrated national energy and climate plan charts a path to climate neutrality by 2040, giving operators long-term policy clarity. Practical examples include Austrian facilities channeling waste heat to hospitals, which qualifies projects for additional environmental subsidies. Regional utilities, such as Energy AG Oberösterreich, intend to add 630 GWh of new renewables by 2030, helping operators secure green-power purchase agreements at stable rates.

Grid Modernisation Investments Accelerating Backup Upgrades

Austrian Power Grid’s EUR 9 billion 2024-2034 network plan includes a 220-kV ring that replaces aging 110-kV circuits around Upper Austria, directly boosting short-circuit fault levels and power quality for new data-center feeders. The Kronstorf sub-station expansion, executed by SPIE, illustrates how modern switchgear design is influencing UPS bypass and generator synchronisation architectures. Pumped-storage plants such as Reisseck II+ add 45 MW of fast-ramping capacity, a boon for facilities that require millisecond-level frequency support. Austria temporarily became a net electricity importer in December 2024, underscoring the need for resilient on-site generation during grid works. Emergency gas-plant dispatch costing EUR 500 million in 2024 revealed budget pressures, prompting operators to upgrade gensets and controllers for more efficient fast-start cycles

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront installation and maintenance costs | -1.4% | Nationwide | Short term (≤ 2 years) |

| Limited land & grid head-room in Vienna | -1.1% | Vienna metro | Medium term (2-4 years) |

| 18-month lead time for MV transformers | -0.8% | Nationwide | Medium term (2-4 years) |

| Strict noise limits for diesel gensets | -0.5% | Urban areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Installation and Maintenance Costs

Budget-consolidation targets of EUR 6.4 billion in 2025 and EUR 8.7 billion in 2026 could curb some subsidy envelopes and shift more capex risk onto investors bmf.gv.at. The EUR 400 million Reisseck II pumped-storage example highlights the ticket size of hybrid renewable-backup projects that many mid-tier operators cannot match alone. Schneider Electric’s USD 140 million factory expansion, aimed at scaling power equipment output, confirms that cost curves remain high but volumes are climbing. New EU reporting rules for energy and water metrics raise ongoing compliance cost, a heavier burden for small colocation sites. Additionally, Austria’s multi-vector renewable mix requires multidisciplinary maintenance teams, lifting opex for facilities that integrate hydro, wind and solar tie-ins

Limited Land and Grid Head-Room Around Vienna Metro

Eastern grid bottlenecks compel Vienna sites to draw on thermal plants rather than cheaper renewables, squeezing carbon targets and expansion room. Digital Realty’s 338,000 ft² hub already maxes out available adjacent parcels, pointing emerging entrants toward outer districts or other provinces. The Austrian Data Center Association has publicly warned that suitable plots inside the capital are scarce, which incentivises hyperscale developers to select secondary cities. Google’s Kronstorf choice illustrates this shift to locations with easier zoning and stronger hydropower links. Delays on Salzburg’s 380-kV line further demonstrate how transmission constraints ripple through site-selection strategies well beyond Vienna.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: UPS Systems Lead Market Share

UPS equipment commanded 27.65% of the Austria data center power market share in 2025, underpinned by the path to a 100% renewable grid that necessitates ride-through and voltage-support capabilities for public and private clouds. The Austria data center power market size for UPS is projected to expand steadily as operators adopt lithium-ion and flywheel hybrids that shave maintenance cycles while supporting grid services. Growing penetration of battery energy-storage enables operators to enroll in frequency-response programs, unlocking new revenue streams that defray capital costs.

Power distribution units are the fastest-expanding component, tracking a 9.78% CAGR to 2031. Rising rack-density and mixed AC-DC layouts require intelligent PDUs that gather branch-circuit telemetry in real time. Generator adoption stays resilient; however, city-centre sites face tougher acoustic ceilings, pushing vendors toward hydrogen ready and gas micro-turbine models. Switchgear demand benefits from the EUR 3.5 billion grid-upgrade program, with arc-resistant MV panels and static transfer switches gaining share in the Austria data center power market

By Data Center Type: Colocation Providers Dominate Market

Colocation vendors retained 57.60% revenue in 2025 as enterprise and public-sector tenants looked for ISO-certified, renewables-powered footprints without bearing full capex. The Austria data center power market size for colocation continues to grow as operators sign 10-year green PPAs to satisfy sustainability audits. Hyperscale sites, although just emerging, post the top 10.72% CAGR because platform giants lock in low-carbon electricity at scale, catalysing regional supply-chain spend.

Enterprise and edge facilities leverage the 2027 federal procurement mandate, installing compact power skids and modular UPS blocks to service latency-sensitive government workloads bmk.gv.at. Cloud-sovereignty projects such as STACKIT’s Austrian zone encourage locally domiciled workloads, further widening colocation hall builds in Salzburg and Graz.

By Data Center Size: Large Facilities Lead Current Market

Large data centers captured 41.73% of 2025 spend owing to economies of scale that lower renewable energy levellised costs. The Austria data center power market size linked to large campuses benefits from hydropower’s baseload profile that pairs well with high-density halls. Massive facilities log a 11.94% CAGR as grid-connected sites outside Vienna gain traction after completion of the 220-kV Upper Austria ring.

Medium and small halls serve branch finance, healthcare and academia, taking advantage of Austria’s 85% renewable mix to keep PUE below 1.4 without exotic cooling systems. The MUSICA HPC initiative, spanning Vienna, Linz and Innsbruck, demonstrates how multi-site clusters depend on reliable mid-sized facilities to share AI loads

By Tier Level: Tier III Facilities Dominate Infrastructure

Tier III environments held 50.60% share in 2025 by balancing resiliency with cost. Operators adopt N+1 topologies that integrate renewable grid feeds with battery energy-storage to ride through disturbance events at minimal capex uplift ntt-data-centers.com. Tier IV footprints grow 9.05% CAGR as critical finance and federal workloads demand 2N architectures ahead of new cyber-resilience requirements.

Lower-tier halls, often at the edge, capitalise on Austria’s high renewable penetration, allowing relaxed generator hours while maintaining SLA compliance. Power-protection vendors like Piller Power Systems supply medium-voltage UPS trains that enable Tier IV uptime without large diesel footprints, aligning with strict urban noise codes

Geography Analysis

Austria’s small geographic footprint belies pronounced regional contrasts in grid head-room, land pricing and renewable mix. Vienna still houses the bulk of installed IT load thanks to dense enterprise demand, with Digital Realty’s 338,000 ft² campus and NTT’s 15.2 MW facility anchoring the hub . Yet land scarcity and limited feeder capacity push new entrants toward Upper Austria and Styria, where hydropower corridors and affordable plots shorten build schedules.

Upper Austria’s visibility surged after Google secured farmland in Kronstorf, roughly 40 km from the provincial hydropower cascade, a siting move that demonstrates how river basins influence megawatt economics for the Austria data center power market. Carinthia and Salzburg are also candidates for future builds as the pumped-storage fleet provides grid-balancing services that appeal to Tier IV designers.

Austria re-imported electricity in December 2024 for the first time in years, highlighting the need for regional diversity in supply chains and backup assets. The country’s link-up to neighbouring transmission systems via 220-kV connectors into Germany, Italy, and Switzerland offers path diversity but adds complexity for power-quality management during seasonal hydro swings e-control . ContourGlobal’s 162 MW wind fleet, operated across seven farms, points to evolving renewables depth that rural data centers can tap through corporate PPAs `

Competitive Landscape

The Austria data center power market is moderately concentrated. Global electrical majors such as ABB, Schneider Electric, and Vertiv pair scale manufacturing with Austrian-specific product tweaks, from cold-weather lithium-ion strings to hydro-compatible rotor designs. Schneider Electric broadened its cooling portfolio by acquiring Motivair in October 2024, bolstering end-to-end power-and-thermal offerings for domestic operators focused on PUE targets.

Service-based models are gaining ground. ABB’s battery energy storage as a service reduces upfront charge and improves uptake among smaller colo halls. Hydrogen and advanced gas genset suppliers, led by INNIO Group in concert with RAG Austria, pioneer low-carbon backup options that suit urban sites constrained by diesel noise limits. VoltaGrid’s mobile gas platform, co-developed with Jenbacher engines, highlights innovation in modular standby power that can bridge 18-month transformer lead-times

Local collaboration also intensifies. The Austrian Data Center Association, created in 2023, counts more than 100 European facilities and pushes unified procurement for high-efficiency electrical components, improving bargaining power versus OEMs heise.de. This bloc, together with the Climate Neutral Data Centre Pact, drives demand away from legacy diesel and toward grid-interactive UPS topologies, sharpening vendor competition around sustainability credentials

Austria Data Center Power Industry Leaders

ABB Ltd.

Eaton Corporation.

Legrand Group

Vertiv Group Corp.

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: OMV opened Austria’s largest green-hydrogen plant, offering an alternative fuel stream for data-center backup power systems

- February 2025: Vantage Data Centers confirmed EUR 1.4 billion for its EMEA platform, with capacity earmarked for Austrian expansion

- January 2025: VoltaGrid and Jenbacher partnered to introduce mobile gas power modules for data-center standby applications.

- November 2024: SPIE began the Kronstorf sub-station expansion that will loop a new 220-kV ring into Upper Austria by 2030

- October 2024: Schneider Electric acquired Motivair, boosting liquid-cooling expertise for domestic data-center clients

- June 2024: Google purchased 185 acres in Kronstorf for a potential hyperscale campus near hydropower facilities

Austria Data Center Power Market Report Scope

Data center power refers to the power infrastructure, including electrical components and electrical distribution systems, that provide the power necessary to operate and support the devices and servers within the data center. It includes various components and technologies designed to ensure a reliable, uninterruptible power supply for data center IT equipment, including uninterruptible power supplies (UPS), power distribution units (PDU), backup generators, and other power management solutions tailored to the specific needs of data centers. Data center operators achieve data center redundancy through duplicated components to maintain uninterrupted operations in the event of failure of some components and to maintain uptime during maintenance.

The Austrian data center power market is segmented by power infrastructure (electrical solution (UPS system, generators, power distribution solutions (PDU, switchgear, critical power distribution, transfer switches, remote power panels, others)), and service), by End User (IT & telecommunication, BFSI, government, media & entertainment, and other end users). The market sizes and forecasts are provided in terms of value (USD Million) for all the above segments.

| Electrical Solutions | UPS Systems | |

| Generators | Diesel Generators | |

| Gas Generators | ||

| Hydrogen Fuel-cell Generators | ||

| Power Distribution Units | ||

| Switchgear | ||

| Transfer Switches | ||

| Remote Power Panels | ||

| Energy-storage Systems | ||

| Service | Installation and Commissioning | |

| Maintenance and Support | ||

| Training and Consulting | ||

| Hyperscaler/Cloud Service Providers |

| Colocation Providers |

| Enterprise and Edge Data Center |

| Small Size Data Centers |

| Medium Size Data Centers |

| Large Size Data Centers |

| Massive Size Data Centers |

| Mega Size Data Centers |

| Tier I and II |

| Tier III |

| Tier IV |

| By Component | Electrical Solutions | UPS Systems | |

| Generators | Diesel Generators | ||

| Gas Generators | |||

| Hydrogen Fuel-cell Generators | |||

| Power Distribution Units | |||

| Switchgear | |||

| Transfer Switches | |||

| Remote Power Panels | |||

| Energy-storage Systems | |||

| Service | Installation and Commissioning | ||

| Maintenance and Support | |||

| Training and Consulting | |||

| By Data Center Type | Hyperscaler/Cloud Service Providers | ||

| Colocation Providers | |||

| Enterprise and Edge Data Center | |||

| By Data Center Size | Small Size Data Centers | ||

| Medium Size Data Centers | |||

| Large Size Data Centers | |||

| Massive Size Data Centers | |||

| Mega Size Data Centers | |||

| By Tier Level | Tier I and II | ||

| Tier III | |||

| Tier IV | |||

Key Questions Answered in the Report

What is the current value of the Austria data center power market?

The market is valued at USD 103.02 million in 2026 and is forecast to grow to USD 152.07 million by 2031.

How fast is the market growing?

It is expanding at an 8.10% compound annual growth rate between 2026 and 2031.

Which component segment holds the largest share?

UPS systems lead with 27.65% of revenue in 2025 due to their critical role in absorbing renewable-driven grid fluctuations.

Why are hyperscale operators interested in Austria?

High renewable penetration, supportive subsidies and grid-modernisation projects provide clean, reliable electricity that meets hyperscale carbon commitments.

What regional hotspots exist beyond Vienna?

Upper Austria, especially around Kronstorf, is emerging because of land availability and proximity to hydropower assets.

How strict are Austria’s sustainability requirements for data centers?

Public IT must run on 100% renewable electricity by 2027, and more than 100 facilities have pledged climate neutrality under the Climate Neutral Data Centre Pact.

Page last updated on: