Austria Data Center Storage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 180 Billion |

| Market Size (2026) | USD 189.27 Billion |

| Market Size (2031) | USD 243.33 Billion |

| Growth Rate (2026 - 2031) | 5.15% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Austria Data Center Storage Market Analysis by Mordor Intelligence

Austria data center storage market size in 2026 is estimated at USD 189.27 million, growing from 2025 value of USD 180 million with 2031 projections showing USD 243.33 million, growing at 5.15% CAGR over 2026-2031. Adoption progresses as enterprises balance strict EU data-sovereignty rules with pressures to cut energy use and carbon emissions. Vienna-based operators focus on high-density, energy-efficient storage because the country’s electricity tariff exceeds the EU average. Demand is amplified by the EU AI Regulation, which obliges organizations to maintain granular data lineage records for high-risk systems. Hyperscalers entering Austria are localizing infrastructure to satisfy residency mandates, increasing orders for compliant storage architectures. Vendors able to deliver low-power flash arrays, immersion-ready racks, and built-in audit capabilities gain an edge in this measured growth environment.

Key Report Takeaways

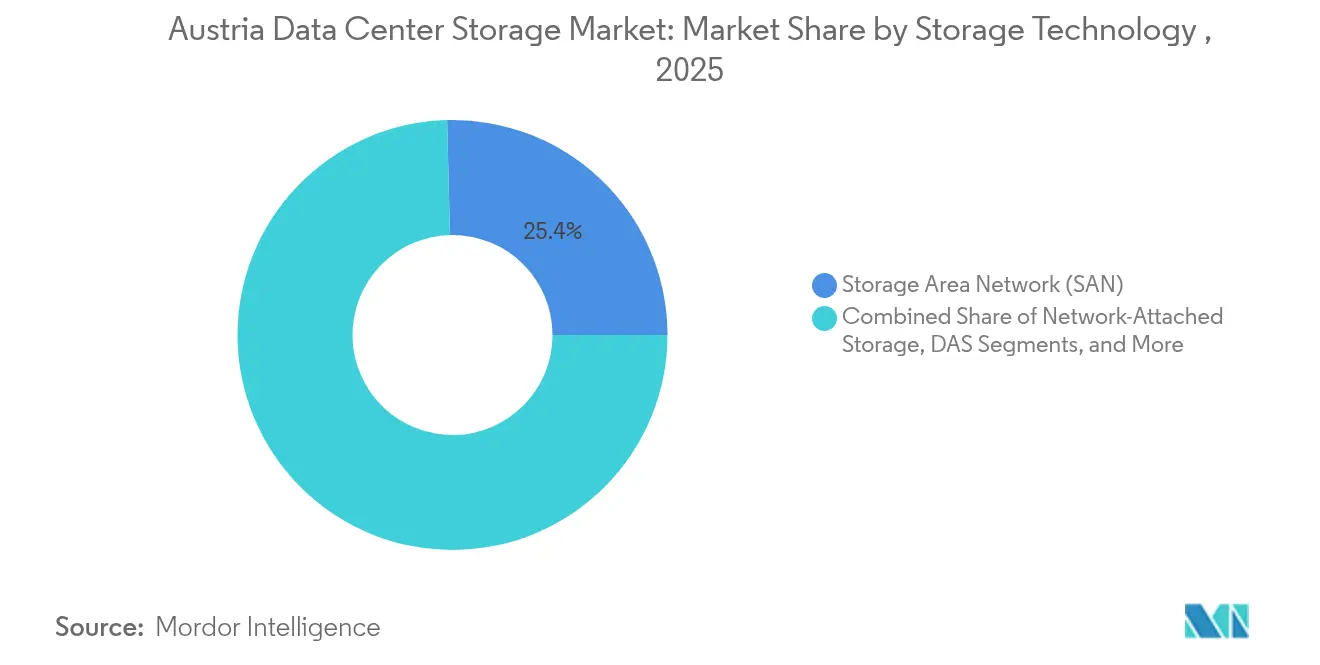

- By storage technology, SAN led with a 25.40% revenue share in 2025, while NAS is set to post the fastest 5.61% CAGR through 2031.

- By storage type, HDD arrays accounted for 42.30% of the Austria data center storage market share in 2025; all-flash arrays are projected to expand at a 6.09% CAGR to 2031.

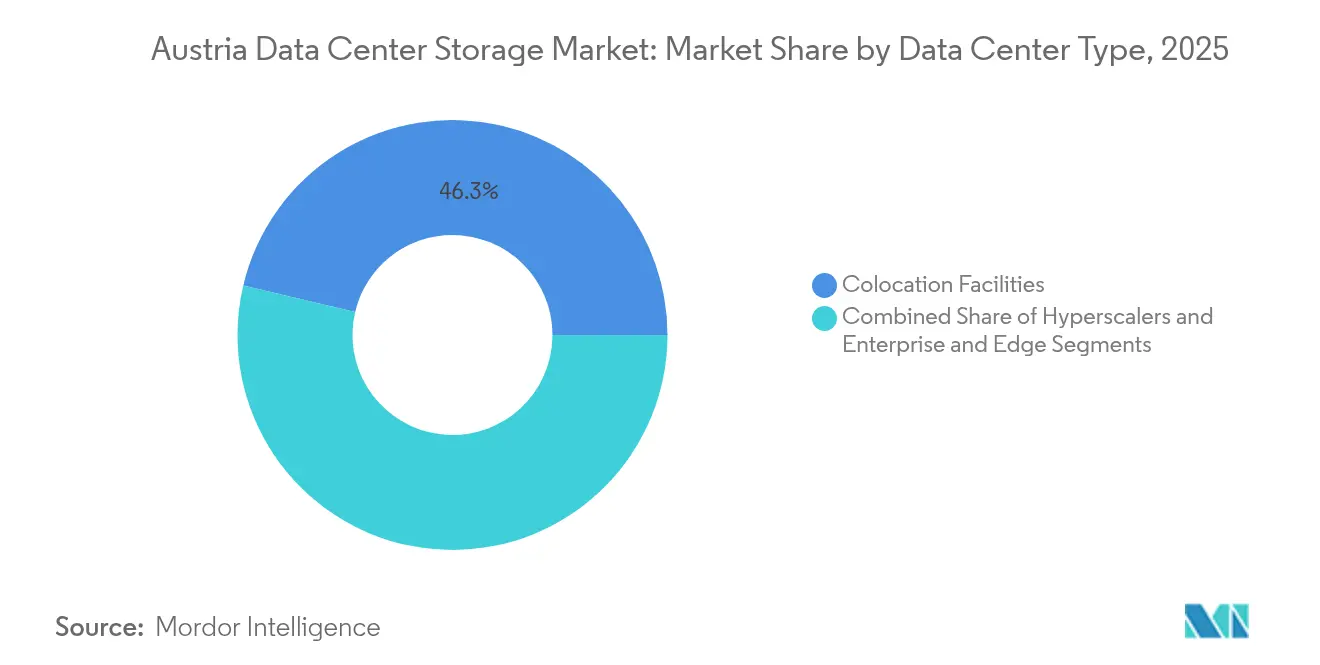

- By data-center type, colocation maintained 46.30% of the Austria data center storage market size in 2025, whereas hyperscaler facilities recorded the highest 6.98% CAGR through 2031.

- By end user, IT and telecommunications held 24.40% revenue share in 2025; BFSI shows the strongest 6.18% CAGR forecast to 2031.

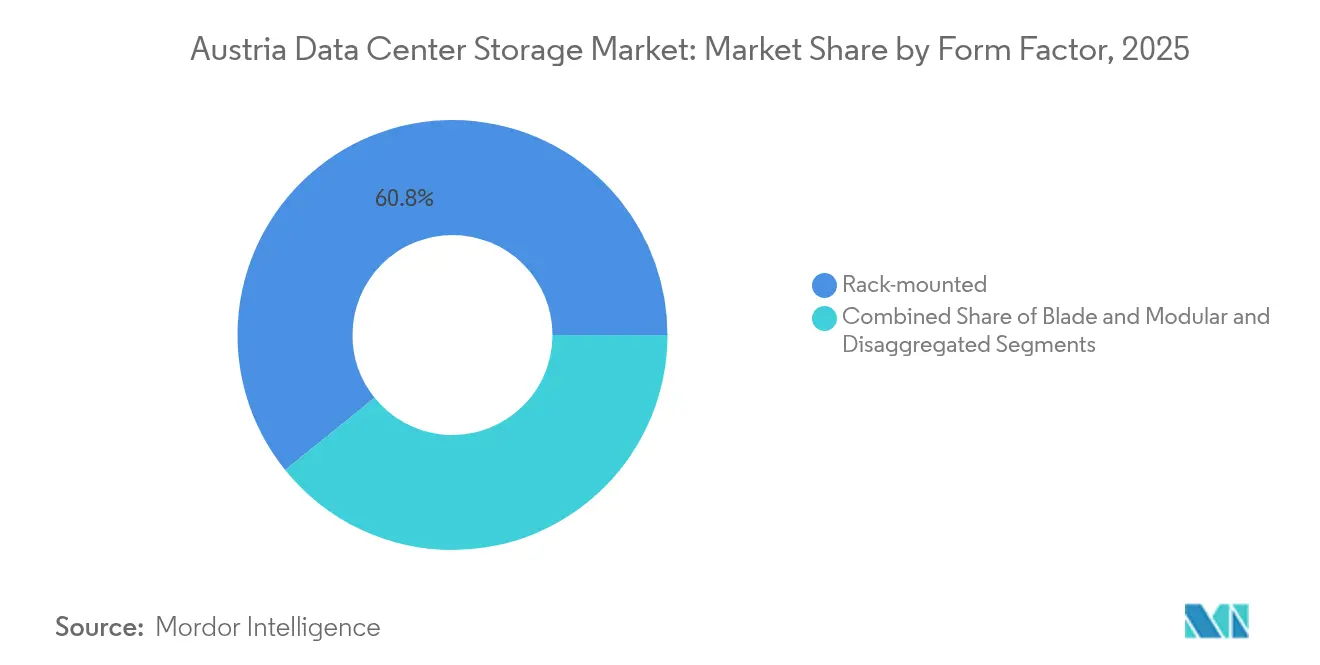

- By form factor, Rack-mounted held 60.80% revenue share in 2025; Disaggregated / Composable shows the strongest 6.79% CAGR forecast to 2031.

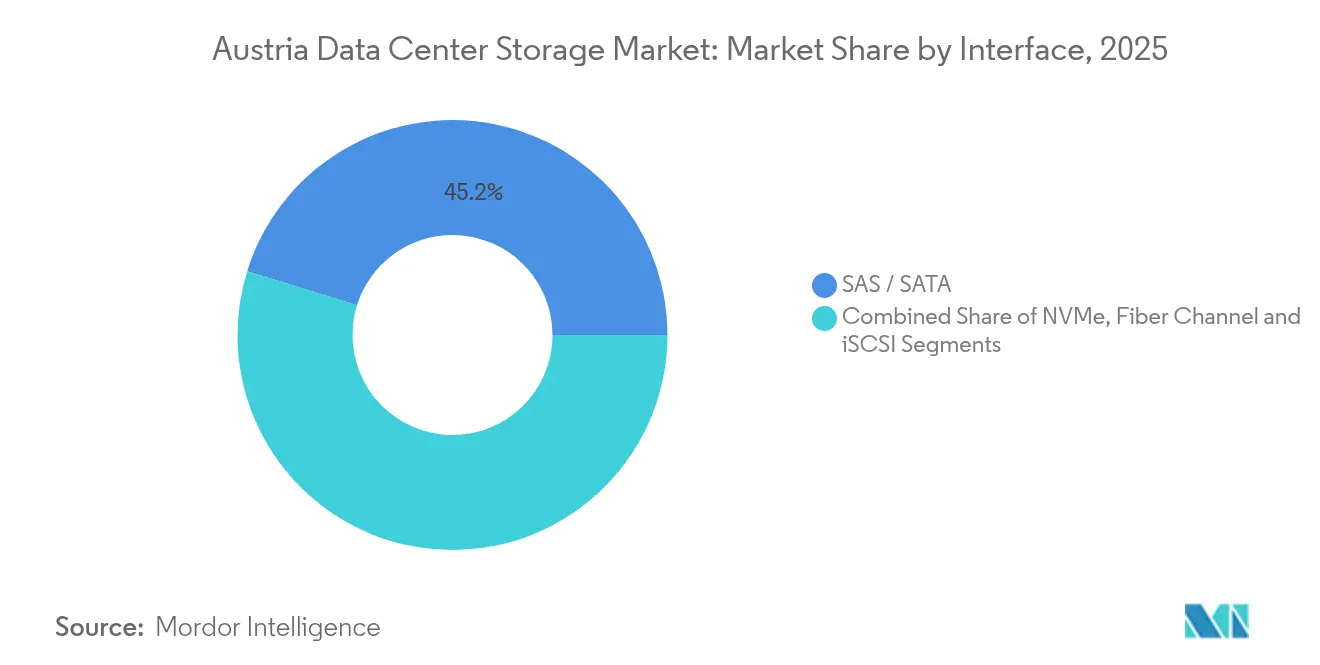

- By Interface, SAS / SATA held 45.20% revenue share in 2025; NVMe shows the strongest 5.19% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Austria Data Center Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-computing expansion & hyperscale investments | +1.2% | National, with concentration in Vienna metropolitan area | Medium term (2-4 years) |

| Energy-efficient & cost-optimized storage designs | +0.8% | National, with higher impact in urban centers | Long term (≥ 4 years) |

| Data-sovereignty compliance under EU regulations | +0.7% | National, with spillover effects to neighboring EU markets | Short term (≤ 2 years) |

| Government-funded digital-twin R&D programs | +0.4% | Regional, focused on Vienna and Graz technology clusters | Long term (≥ 4 years) |

| Edge-compute pilots in Vienna's smart-city grid | +0.3% | Local, with potential national expansion | Medium term (2-4 years) |

| Film-production tax incentive boosting object storage | +0.2% | Regional, concentrated in Vienna and Salzburg | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cloud-computing expansion & hyperscale investments

Global hyperscalers plan significant investments in infrastructure outlays during 2025, and a portion is earmarked for Austrian availability zones to meet data-residency needs.[1]Fierce Network Staff, “Hyperscalers Plan USD 215 Billion Data-Center Spend in 2025,” fierce-network.comVienna’s scarce real estate raises rack-density requirements, so buyers prioritize performance-per-rack over raw capacity. Local operators weigh commodity hardware favored by hyperscalers against compliance-focused systems preferred by domestic firms. This dual demand profile lifts shipments of software-defined NAS and flash arrays that support rapid, automated provisioning. Vendors with mature service ecosystems pivot quickly to meet both hyperscale and enterprise expectations.

Energy-efficient & cost-optimized storage designs

Electricity prices exceed the EU mean, incentivizing the adoption of low-power flash and advanced cooling. Incoming refrigerant rules cap GWP at 700 by 2027, making two-phase immersion a viable choice for high-density bays. Flash arrays deliver superior performance-per-watt, and lifecycle models now trump initial price in procurement decisions. Vendors differentiate through granular power-usage analytics and smart-throttling firmware that curbs peak loads. As operators chase carbon-neutral targets, storage hardware with verifiable energy-saving credentials commands premium margins.

Data-Sovereignty Compliance Under EU Regulations

The EU’s push for sovereign cloud raises storage decisions to board-level priorities, and Austria is an early proving ground for GDPR-aligned architectures. Enterprises demand arrays that can enforce granular access controls and automate audit logs, spurring interest in platforms with native policy-based tiering. IKARUS Security’s GDPR-focused mobile-device management hosted in ISO-certified Vienna facilities embodies this compliance-first mindset. [2]Microsoft, “Microsoft announces first cloud region in Austria,” microsoft.comAs cross-border data flows expand to CEE, Austria’s central location drives regional replication requirements, thereby lifting capacity demand within the Austria data center storage market.

Government-Funded Digital-Twin R&D Programs

Austria earmarked EUR 16.64 billion for R&D in 2024, targeting digital twins for smart-city and industrial use cases.[3]IKARUS Security, “ISO-certified data centers in Vienna,” ikarussecurity.com These workloads involve continuous sensor ingestion and real-time analytics, stressing write endurance and metadata handling. The Aspern Urban Lakeside project’s live energy-grid twin illustrates multi-petabyte growth trajectories. Funding under the EU’s IPCEI further channels capital toward advanced storage controllers and in-memory databases. Vendors that align with these initiatives secure early-stage pilots, reinforcing the Austria data center storage market’s pivot to performance-dense solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited storage-security talent pool & cyber-risks | −0.9% | Nationwide shortages, acute in Vienna & Salzburg | Short term (≤ 2 years) |

| Austria’s above-EU-average electricity prices | −0.6% | National, sharpest in major cities | Medium term (2-4 years) |

| Scarce urban real estate for new builds | −0.4% | Vienna metropolitan area | Long term (≥ 4 years) |

| Planned carbon-pricing scheme on DC operations | −0.3% | Countrywide, phase-in starts 2026 | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Storage-Security Talent Pool & Cyber-Risks

Enterprises struggle to hire specialists who blend deep storage know-how with cyber-resilience skills, delaying modernization roadmaps. BFSI and pharma firms, bound by strict audit trails, feel this pinch most acutely. Wüstenrot Gruppe’s decision to outsource mainframe modernization to Kyndryl underscores reliance on external expertise for complex data migrations. Ransomware attacks further elevate skill requirements, forcing companies to invest in immutable snapshot technologies. The scarcity inflates wages and elongates deployment cycles, tempering near-term growth in the Austria data center storage market.

Austria’s Above-EU-Average Electricity Prices

While 87% of Austria’s power mix is renewable, tariffs remain high, adding persistent OPEX pressure. Operators therefore defer non-critical capacity expansions or demand steep efficiency gains from vendors. The forthcoming carbon-pricing mechanism promises to magnify cost differentials between legacy spinning media and flash. Some organizations relocate DR sites to neighboring countries with cheaper energy, trimming incremental spend inside the Austria data center storage market over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Storage Technology: SAN leadership meets fast NAS gains

SAN retained the largest slice at 25.40% in 2025, anchoring mission-critical databases within the Austria data center storage market. Enterprises trust SAN for deterministic latency and mature zoning features. NAS, growing at 5.61% CAGR, aligns better with file-level audit mandates set by GDPR and the AI Regulation. Vendors embed policy engines that tag files for retention, easing compliance audits. In the second half of the period, NAS adoptions accelerate inside hyperscale annexes where micro-services need shareable file pools. Expanding AI workloads also lift object storage though volumes remain niche. Tape enjoys a renaissance for cold archives linked to long retention statutes.

Shift dynamics favor software-defined stacks that abstract hardware. Austrian buyers migrate workloads from legacy Fibre-Channel SAN to Ethernet-based NAS clusters to cut licensing and maintenance bills. The Austria data center storage market size for NAS solutions is expected to widen as cloud providers standardize on NFS variants for regional zones. SAN remains relevant where deterministic IO trumps cost, yet vendors revamp firmware to reduce idle draw and add inline encryption that satisfies EU sovereignty rules.

By Storage Type: HDD arrays yield to flash acceleration

HDD arrays controlled 42.30% revenue in 2025, yet energy levies and performance demands steer budgets toward flash. All-flash arrays expand at 6.09% CAGR as operators quantify performance-per-watt. Hybrid tiers persist where workload IO patterns are mixed; caching algorithms stretch flash benefits across slower platters. The Austria data center storage market size tied to flash arrays rises alongside immersive cooling retrofits in Vienna. CFOs now evaluate five-year total cost rather than sticker price, and flash wins when power savings outstrip depreciation.

Reliability motives reinforce the switch. Controllers employ advanced wear-leveling and end-to-end data-integrity checks valued by auditors. Vendors offer migration bundles that clone HDD volumes into flash pools overnight, minimizing downtime. HDD still thrives in tape-adjacent archives where capex minimization eclipses performance. As flash price per terabyte narrows, HDD’s domain contracts mostly to backup and video archives.

By Data-Center Type: Colocation steadiness versus hyperscaler surge

Colocation locked in 46.30% share in 2025 and remains the backbone for regional enterprises, missing capital for owned facilities. Operators tailor cage-level compliance services, including guided audits and encrypted backup vaults. Hyperscaler footprints, however, widen fastest at 6.98% CAGR because data residence rules compel cloud majors to set up local zones. These firms favor standardized platforms that integrate NVMe shelves at scale, driving bulk purchases from global OEMs. The Austria data center storage market continues to bifurcate: colocation for regulated workloads that need bespoke controls, and hyperscaler for elastic tasks that tolerate uniform architectures.

The colocation segment innovates to stay competitive. Operators pilot liquid-cooled racks and commit to 100% renewable power badges by 2027, enabling clients to meet scope-3 reporting requirements. Hyperscalers, meanwhile, ask suppliers for carbon-intensity disclosures at the component level. Vendors that certify chain-of-custody data and offer end-of-life recycling lock in multiyear frameworks.

By End User: BFSI outpaces core IT spending

IT and telecommunications contributed 24.40% of 2025 revenue as 5G rollouts generated caching and analytics needs. Yet BFSI rises at 6.18% CAGR on the back of digital banking adoption that demands tamper-proof audit logs. The Austria data center storage market size attached to BFSI grows as banks deploy AI for fraud detection, lifting latency-sensitive flash requirements. Government agencies keep steady demand for secure repositories supporting e-services and tax portals.

Media incentives fuel spikes in object storage for post-production houses in Vienna and Salzburg. Healthcare providers consider edge clusters to meet telemedicine latency targets, while manufacturers in Upper Austria route industrial IoT telemetry into hybrid tiers. Vendors position sector-specific reference architectures with preloaded compliance templates, shortening project timelines.

By Form Factor: Disaggregated architectures gain traction

Rack-mounted arrays held 60.80% share in 2025 but composable platforms record 6.79% CAGR as Austrian firms embrace cloud-native patterns. Disaggregated designs allow independent scaling of compute and storage, reducing stranded capacity under energy-cost pressure. The Austria data center storage market size for disaggregated nodes benefits from software layers that pool NVMe drives across chassis.

Blade enclosures remain popular in space-constrained sites, especially where smart-city edge nodes reside on rooftops or street cabinets. Vendors integrate liquid or immersion cool plates to maintain thermal envelopes without raising facility PUE. Modularity appeals to colocation landlords that monetize square-meter density through higher power circuits sold to tenants.

By Interface: NVMe ascends while SAS/SATA hold the base

SAS/SATA commanded 45.20% of shipments in 2025, thanks to extensive installed footprints. NVMe climbs at 5.19% CAGR as AI and real-time analytics prioritize microsecond latency. The Austria data center storage market share linked to NVMe rises due to its favorable performance-per-watt ratio, aligning with national carbon goals. Fibre Channel survives where unchanged SAN setups run core financial apps. iSCSI endures in SMB appliances seeking simplicity.

Transition plans emphasize dual-protocol controllers that protect legacy investments. Vendors roll out firmware enabling NVMe-over-TCP, letting customers reuse Ethernet fabrics. Protocol gateways steer mixed traffic while security modules enforce encryption keys at line rate. These features ease NVMe adoption without forklift upgrades.

Geography Analysis

Vienna anchors most capacity, driven by carrier hotels, skilled labor, and direct cloud on-ramps. Electricity premiums and limited parcels nudge operators toward taller bays and immersion tanks that squeeze more drives per square meter. The Austria data center storage market in Vienna therefore, skews to high-density flash and NVMe shelves tailored for mixed tenancy.

Graz forms the secondary pole, fueled by digital-twin research grants tied to its technical university cluster. Pilot factories stream sensor data into hybrid arrays that blend local flash with long-term cloud vaults. Storage vendors partner with regional integrators to meet domestic-content rules included in R&D subsidies. Salzburg attracts media workloads, leveraging film tax incentives that spur uptake of object storage platforms supporting large video files. Edge nodes dot the surrounding alpine towns, backhauling data via fiber corridors into Vienna.

Competitive Landscape

The market is moderately concentrated around a global core of Dell Technologies, Hewlett-Packard Enterprise, NetApp, Pure Storage, and Infinidat. These suppliers blend hardware with consulting that guides clients through GDPR and AI-rule audits. Dell commits EUR 45 million to expand its Viennese service lab that validates compliant architectures, signaling long-term engagement. Pure Storage anchors growth on flash arrays tuned for low-energy operation, positioning against Austria’s tariff backdrop.

Hyperscale incursions pressure hardware vendors as Amazon Web Services and Microsoft Azure favor integrated storage services. OEMs counter with as-a-service contracts and pay-per-use billing deployed inside customer cages. Niche players such as Kingston Technology boost enterprise credibility through ISO-27001 badges, while Fujitsu gains mindshare by joining the national digital-twin consortium in Graz

Austria Data Center Storage Industry Leaders

Dell Technologies

Hewlett Packard Enterprise

NetApp

Huawei Technologies

Lenovo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Dell Technologies announced a EUR 45 million expansion of its Austrian service center focused on AI-optimized storage and compliance consulting.

- February 2025: Pure Storage launched FlashArray//C for European data-sovereignty use cases, adding encryption and audit features.

- January 2025: Hewlett Packard Enterprise partnered with A1 Telekom to deploy edge storage for Vienna smart-city traffic analytics.

- December 2024: NetApp acquired Austrian software firm DataCore to strengthen regional software-defined storage capabilities.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Austria data center storage market as the value generated each year from purpose-built, rack-mountable storage subsystems, covering SAN, NAS, DAS, and all-flash arrays, deployed inside commercial colocation, hyperscale, and enterprise data centers operating within Austrian borders. Consumer USB drives, edge gateways, and public-cloud software fees sit outside this scope.

Home-office HDDs, personal SSDs, and any storage supplied as part of end-user devices are excluded.

Segmentation Overview

- By Storage Technology

- Network Attached Storage (NAS)

- Storage Area Network (SAN)

- Direct Attached Storage (DAS)

- Object and Tape Storage

- By Storage Type

- Traditional HDD Arrays

- All-Flash Arrays (AFA)

- Hybrid Storage

- By Data Center Type

- Colocation Facilities

- Hyperscalers/Cloud Service Providers

- Enterprise and Edge

- By End User

- IT and Telecommunication

- BFSI

- Government and Public Sector

- Media and Entertainment

- Healthcare and Life Sciences

- Manufacturing

- By Form Factor

- Rack-mounted

- Blade and Modular

- Disaggregated / Composable

- By Interface

- SAS / SATA

- NVMe

- Fibre Channel and iSCSI

Detailed Research Methodology and Data Validation

Primary Research

To ground the desk findings, we interviewed facility operators in Vienna and Graz, procurement leads at BFSI and telecom firms, and regional storage architects from three global vendors. Their insight on flash adoption rates, NVMe price curves, and upcoming colocation builds sharpened assumptions and closed data gaps.

Desk Research

Mordor analysts compiled capacity, price, and trade indicators from open Austrian sources such as Statistik Austria, the Energy Control Commission, the Vienna Chamber of Commerce, and the European Data Centre Association, along with company 10-Ks and press releases. Select paid databases, D&B Hoovers for supplier revenues and Dow Jones Factiva for deal flow, supplied cross-checks on vendor shipments and investment news. These sources illustrate typical rack counts, power tariffs, and ASP trends but are not exhaustive; additional public datasets were also assessed.

Market-Sizing & Forecasting

A pragmatic top-down model starts with installed and planned IT-load capacity (MW) and typical terabytes per megawatt, reconstructed from grid connection filings and construction permits, then values demand using blended $/TB. Bottom-up samples of vendor sales and channel checks finetune totals. Key variables include rack density evolution, flash penetration, new MW additions, average $/TB, and GDPR-driven data residency spending. A multivariate regression projects each driver, and scenario analysis adjusts for power-price swings. Where supplier roll-ups under-report, gaps are bridged with sampled ASP×volume benchmarks before reconciliation.

Data Validation & Update Cycle

Outputs face two-layer analyst review; anomaly flags trigger call-backs with sources, and values are compared with independent price indices and shipment logs. Reports refresh annually; material events prompt interim updates, ensuring clients receive the freshest baseline.

Why Mordor's Austria Data Center Storage Baseline Inspires Confidence

Published figures often diverge because firms pick different component mixes, currency years, and refresh cadences.

Key gap drivers here include: some publishers limit scope to SAN hardware only or fold servers and networking into storage totals; others inflate totals by applying global ASPs without Austria's high-electricity cost discounts; a few rely on 2023 shipment data with no primary validation for 2025 price drops.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 180 M (2025) | Mordor Intelligence | - |

| €170 M (2025) | Regional Consultancy A | Narrow scope, minimal primary checks |

| €350 M (2023) | Trade Journal B | Combines servers and storage, older baseline |

This comparison shows that Mordor's disciplined variable selection, annual refresh, and dual-path validation deliver a balanced, transparent figure clients can trace back to clear, replicable steps.

Key Questions Answered in the Report

What is the current size of the Austria data center storage market?

The market is valued at USD 189.27 million in 2026 and is forecast to reach USD 243.33 million by 2031, reflecting a 5.15% CAGR.

How do Austria’s electricity costs influence storage adoption?

Above-average tariffs push operators toward energy-efficient flash arrays and immersion cooling, accelerating the migration away from traditional HDD systems

Why is compliance a major storage purchasing factor in Austria?

GDPR and forthcoming EU AI rules demand extensive audit trails and data lineage, favoring storage systems with built-in encryption, WORM snapshots, and certified retention features.

Which end-user segment is growing fastest?

BFSI workloads expand at 6.18% CAGR as digital banking and AI-assisted fraud detection drive demand for high-performance, secure storage.

Page last updated on: