Australia Senior Living Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

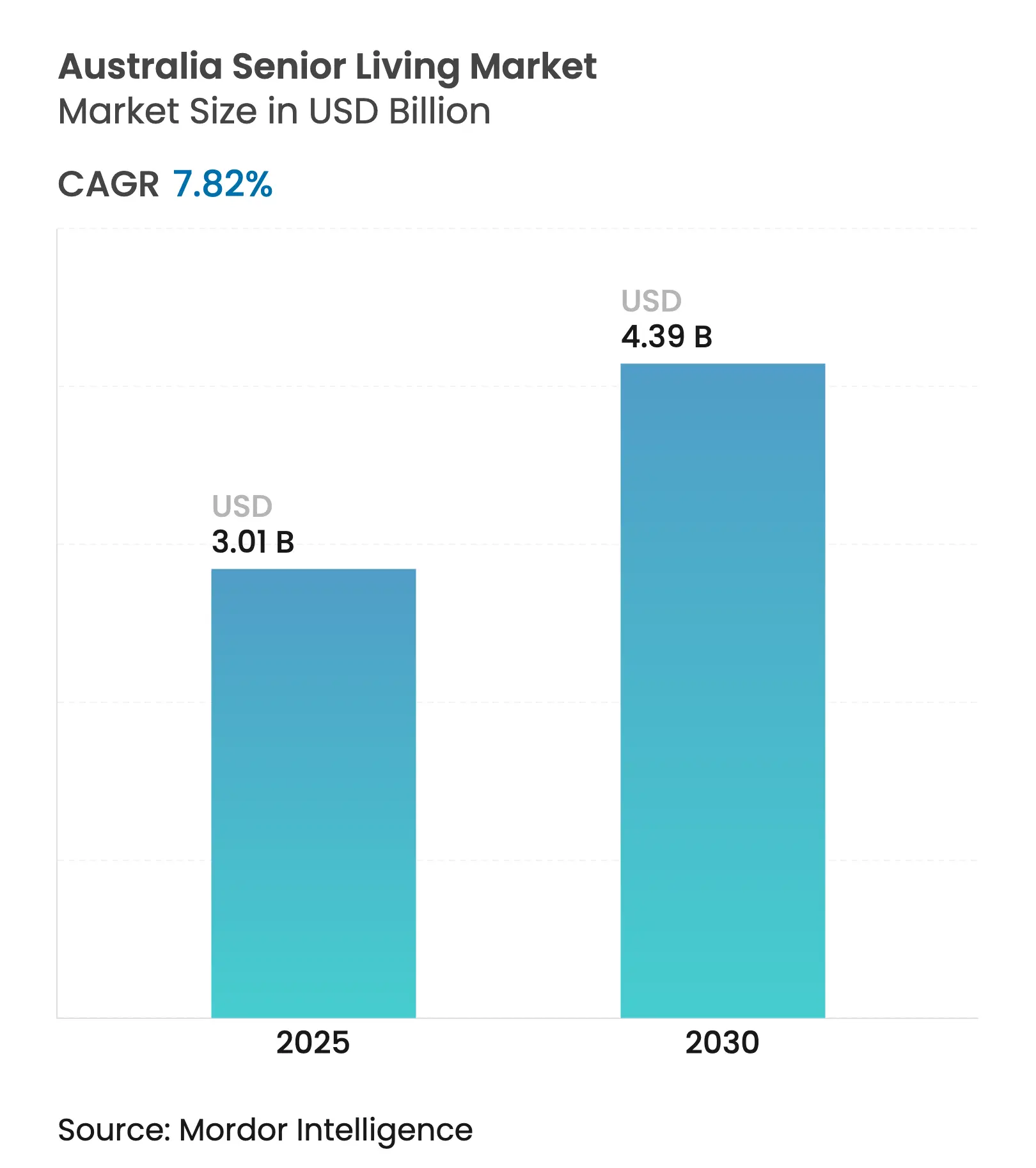

| Market Size (2025) | USD 3.01 Billion |

| Market Size (2030) | USD 4.39 Billion |

| Growth Rate (2025 - 2030) | 7.82 % CAGR |

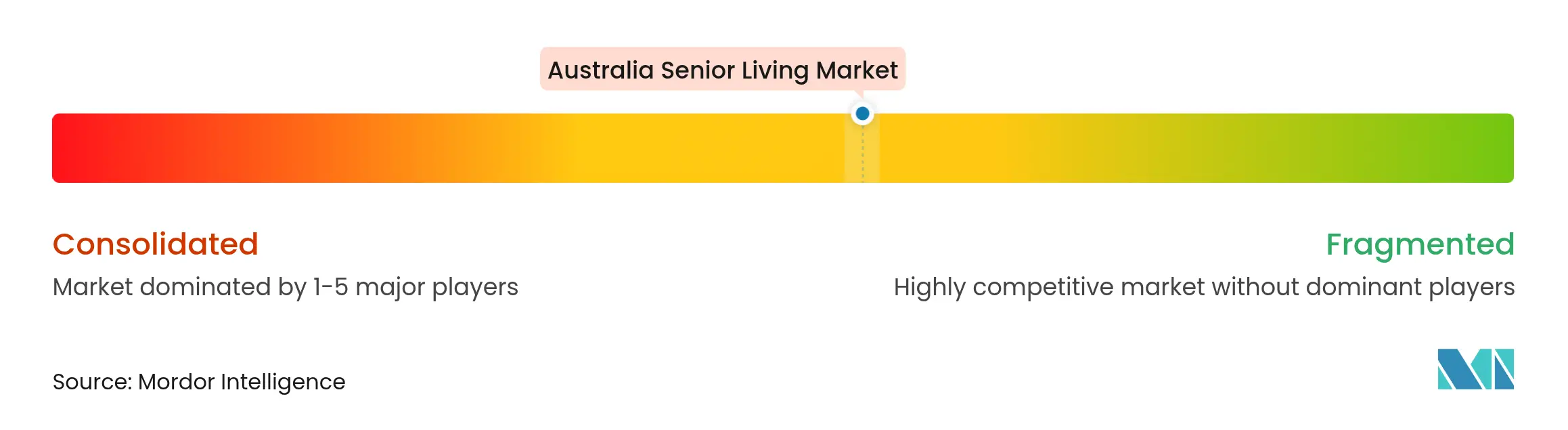

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Australia Senior Living Market Analysis by Mordor Intelligence

The Australia senior living market size stands at USD 3.01 billion in 2025 and is forecast to reach USD 4.39 billion by 2030, translating into a 7.82% CAGR. Recent gains stem from a steady rise in Australians aged 65 years and older, climbing from 17% of the population in 2022 toward an expected 25%-27% share by 2071. Independent Living retains clear dominance, yet Memory Care shows the fastest uptake as dementia prevalence rises. Rental formats are winning residents who value flexibility, and coastal migration flows draw retirees into emerging villages. Digital health pilots, tighter quality rules, and stepped-care funding channels combine to reshape supply and demand conditions across the Australia senior living market.

Key Report Takeaways

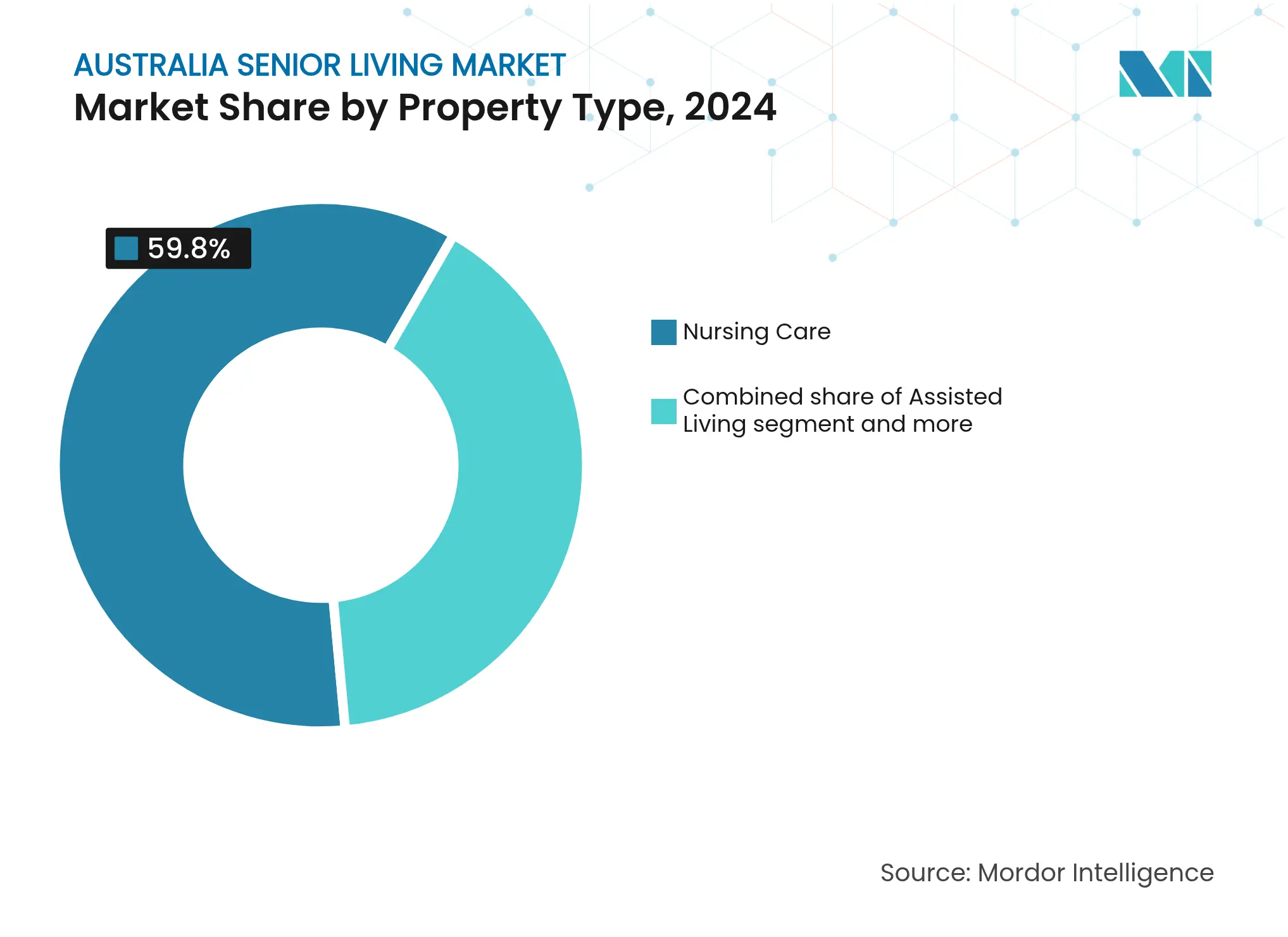

- By Property Type, Independent Living captured 59.8% of Australia senior living market share in 2024. Memory Care is projected to expand at an 8.43% CAGR through 2030.

- By Business Model, Outright Sale (Freehold) based contracts held 58.9% share of the Australia senior living market size in 2024, while Hybrid (Sale + Lease) models record the highest forecast CAGR at 8.65%.

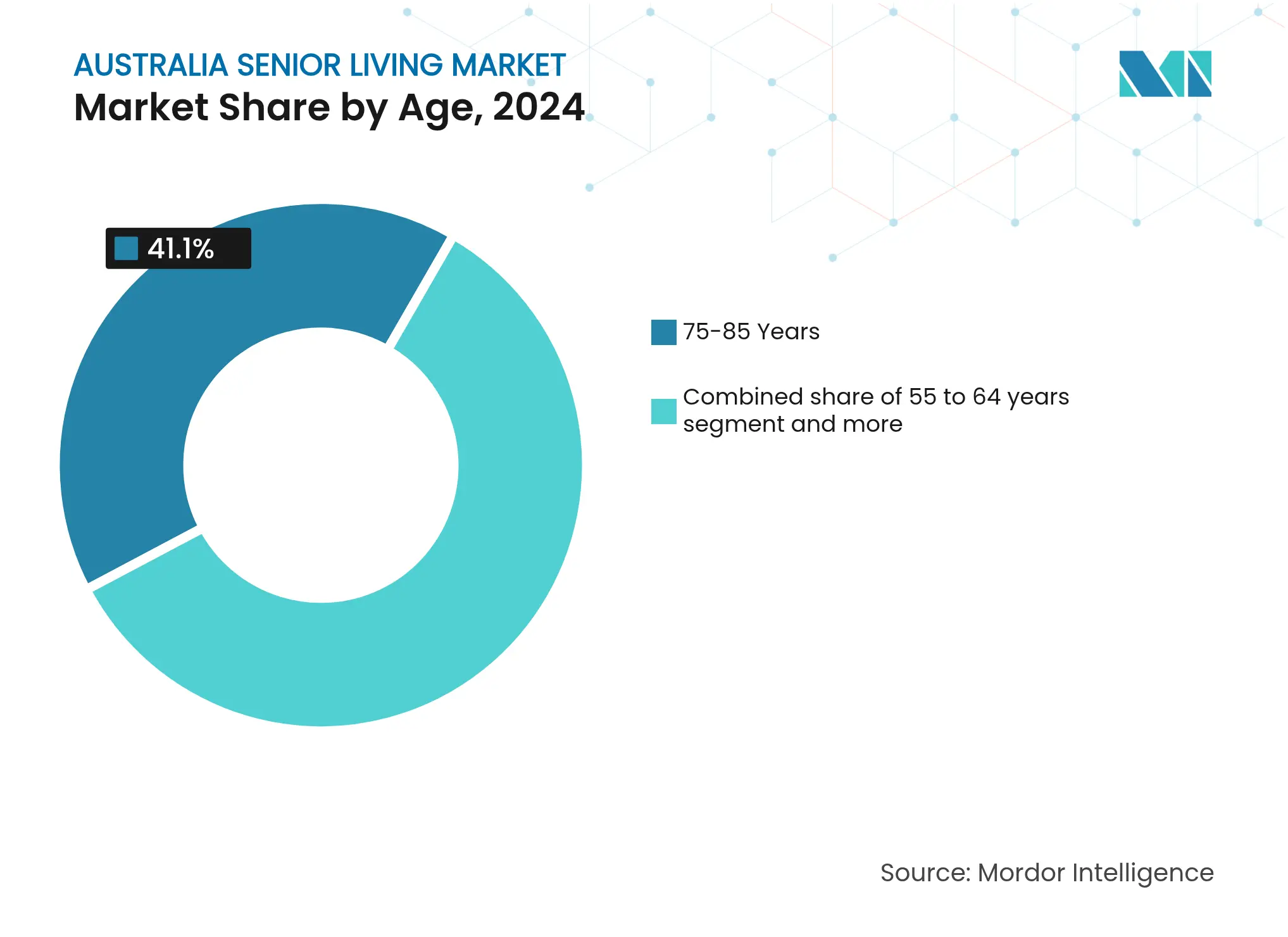

- By Age, the 75-85 years band accounted for 41.1% share of the Australia senior living market size in 2024; the Above 85 years cohort is on course to grow at 9.03% CAGR.

- By Geography, Sydney led with 20.4% of Australia senior living market share in 2024; Perth is advancing at a 9.32% CAGR.

Australia Senior Living Market Trends and Insights

Drivers Impact Analysis

| Drivers | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Accelerating

aging demographics and rising longevity underpinning multi-decade demand

Accelerating

aging demographics and rising longevity underpinning multi-decade demand

| +2.1% | Global, with concentration in Sydney, Melbourne, Brisbane | Long term (≥ 4 years) | ( ~ ) %

Impact on CAGR Forecast:

+2.1%

|

Geographic

Relevance

:

Global,

with concentration in Sydney, Melbourne, Brisbane

|

Impact

Timeline

:

Long

term (≥ 4 years)

|

Mature

retirement village/land-lease models with strong resident services and

amenity focus

Mature

retirement village/land-lease models with strong resident services and

amenity focus

| +1.8% | National, with early gains in coastal Queensland, NSW | Medium term (2-4 years) | |||

Home

Care Packages and healthcare integration supporting step-up/step-down care

pathways

Home

Care Packages and healthcare integration supporting step-up/step-down care

pathways

| +1.5% | National, spill-over to regional centers | Medium term (2-4 years) | |||

Downsizing

to coastal and infill metro locations driving premium village demand

Downsizing

to coastal and infill metro locations driving premium village demand

| +1.3% | Coastal regions, inner-metro Sydney, Melbourne, Perth | Short term (≤ 2 years) | |||

Growing

adoption of smart-home and wellness technologies improving resident

experience

Growing

adoption of smart-home and wellness technologies improving resident

experience

| +0.8% | Metro areas initially, expanding to regional centers | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Accelerating aging demographics

Australia’s population is moving firmly into older age brackets, lifting the baseline demand for purpose-built residences. The 60 years-plus cohort is forecast to reach 9.69 million, or 30.1% of citizens, by 2050. Life expectancy now sits at 83.7 years and is still edging upward, making longevity a structural demand engine. Family sizes are shrinking, and fertility rates are at 1.55 babies per woman, reducing the pool of informal caregivers. Wealthier baby boomers also express clear lifestyle expectations that favor high-service communities. These factors provide the Australia senior living market with multi-decade growth visibility[1]United Nations Department of Economic and Social Affairs, “World Population Prospects 2024,” United Nations, un.org.

Mature retirement village and land-lease models

Established operators have optimized shared-equity and land-lease formats that lower entry costs while funding top-tier amenities. The typical independent living unit carries an upfront price of USD 361,200 after currency conversion, well under median house values in major capitals. Residents gain clubhouses, wellness suites, and concierge support that match aspirational preferences. Replicable development templates shorten construction lead times and spread overheads. As projects cluster near coastlines and inner-ring suburbs, brand recognition reinforces trust and boosts presales, feeding the expansion pipeline.

Health-care integration and step-up pathways

The Support at Home scheme, active from November 2025, allocates quarterly budgets ranging from USD 1,925 to USD 13,650 across eight need levels. A single national assessment cuts red tape when residents move between independent, assisted, and nursing settings. A restorative grant of USD 4,200 over 12 weeks promotes recovery at home, and an end-of-life allowance of USD 17,500 supports palliative care in familiar surroundings. Operators that can bundle these streams unlock new revenue while providing seamless care journeys. Tele-nursing pilots and virtual monitoring tools further expand outpatient coverage[2]Australian Government Department of Health and Aged Care, “Support at Home Program Overview 2025,” Department of Health and Aged Care, health.gov.au.

Downsizing to coastal and infill metro locations

Retirees continue to swap large family dwellings for compact units in lifestyle-rich areas. Research highlights “scene-changer” and “local-adapter” pathways, which both favor beachside or vibrant inner-city precincts. Queensland has earmarked USD 245 million to accelerate such projects, acknowledging their role in alleviating hospital pressure and freeing up suburban stock for younger buyers. Councils report uplift in local spending as cashed-up retirees settle, spurring further retail and medical investment. Overall, the trend enlarges the premium tier of the Australia senior living market.

Restraints Impact Analysis

| Restraints | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Regulatory

reforms and compliance scrutiny increasing operating complexity

Regulatory

reforms and compliance scrutiny increasing operating complexity

| -1.2% | National, with heightened impact in NSW, VIC | Short term (≤ 2 years) | ( ~ ) %

Impact on CAGR Forecast:

-1.2%

|

Geographic

Relevance

:

National,

with heightened impact in NSW, VIC

|

Impact

Timeline

:

Short

term (≤ 2 years)

|

Construction

cost inflation and trades shortages impacting feasibility

Construction

cost inflation and trades shortages impacting feasibility

| -0.9% | National, acute in Sydney, Melbourne, Brisbane | Medium term (2-4 years) | |||

Consumer

sensitivity to fee transparency and contract structures affecting sales

velocity

Consumer

sensitivity to fee transparency and contract structures affecting sales

velocity

| -0.7% | National, particularly VIC due to land lease reforms | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Regulatory complexity intensifies burdens

The Aged Care Act 2024 introduces six risk-based registration tiers, three-year license cycles, and rigorous suitability checks. Fresh quality standards cover clinical care, nutrition, and environmental safety; non-compliance attracts public star-rating downgrades. Mandatory daily care minutes rise to 215 by late 2024, compelling many facilities to recruit extra registered nurses. Whistle-blower channels and an independent Inspector-General layer on further oversight. Compliance systems, digital rostering, and audit readiness lift fixed costs, challenging smaller providers and slowing new entrants into the Australia senior living market[3]Aged Care Quality and Safety Commission, “Strengthened Quality Standards Draft,” Aged Care Quality and Safety Commission, agedcarequality.gov.au.

Construction cost escalation constrains feasibility

National residential build costs climbed 3.4% during 2024 and have risen 30.8% since pre-pandemic baselines. Wage agreements add annual inflation near 5%, while skilled trades remain scarce ahead of marquee projects like the 2032 Brisbane Olympics. Regional disparity persists as Sydney and Melbourne record the sharpest spikes. The USD 74.9 million Blue Haven Bonaira facility ultimately sold for USD 66.5 million, illustrating margin erosion in over-budget ventures. Developers now phase releases, trim unit footprints, or pivot to lighter-build park-home concepts to defend returns.

Segment Analysis

By Property Type: Memory Care Drives Growth While Independent Living Dominates

Independent Living posted 59.8% of Australia senior living market share in 2024. Demand rests on autonomous residents seeking resort-style amenities and social programs. Village designs now feature cafés, gyms, and allied health suites that lengthen healthy life years. The Australia senior living market size for Memory Care is projected to widen at an 8.43% CAGR, propelled by dementia’s rising incidence and family preference for purpose-built environments. Regulatory design codes stress natural lighting, quiet zones, and access to outdoor areas. Operators integrate these standards early to speed approvals and command premium prices.

Assisted Living and Nursing Care remain essential parts of the continuum, capturing residents whose health shifts suddenly. The Support at Home classifications allow a smooth upgrade path, reducing exit churn. Providers, therefore, co-locate independent villas, assisted apartments, and high-care beds on shared campuses. The model preserves community ties and enables cross-selling of home-care packages, strengthening occupancy resilience across the Australia senior living market.

Note: Segment shares of all individual segments available upon report purchase

By Business Model: Hybrid (Sale + Lease) Momentum Builds as Sales Model Matures

In the Australia senior living market, the Outright Sale (Freehold) model is driven by strong demand from financially independent retirees seeking ownership security, asset appreciation, and long-term stability. Rising household wealth among the 55+ age group, supported by equity release from downsizing and favorable property value trends, continues to fuel purchases in freehold retirement communities. Additionally, cultural preferences for homeownership, low-interest-rate environments in previous years, and growing availability of integrated lifestyle villages offering ownership flexibility have further boosted the appeal of outright sale models over rental or deferred management fee structures.

The Hybrid (Sale + Lease) segment in Australia’s senior living market is growing at a robust CAGR of around 8.65%, driven by increasing demand for flexible ownership options among retirees. This model appeals to seniors who prefer a balance between capital preservation and lifestyle affordability—allowing partial ownership while reducing ongoing financial burdens through lease arrangements. The growth is further supported by evolving consumer preferences toward mixed-tenure communities, developer initiatives to enhance affordability, and rising interest from mid-income retirees seeking lower entry costs without compromising access to healthcare, amenities, and community living standards.

Hybrid models address concerns over traditional land leases by offering equity participation and operational efficiency. The "Support at Home" program allows pricing flexibility until July 2026, enabling providers to innovate by integrating residential and care services. Regulatory actions by Consumer Affairs Victoria and legal challenges to exit fees are driving transparency and contract standardization, potentially accelerating hybrid model adoption as operators seek competitive advantages.

By Age: Above 85 Years Cohort Shows Strongest Growth

Residents aged 75-85 years formed 41.1% of Australia senior living market share in 2024, mirroring the front edge of the baby-boomer wave. Their relatively strong health and savings nurture demand for larger units and leisure-rich settings. The above-85 years segment is poised for a 9.03% CAGR because life expectancy pushes more citizens into high-support brackets. Personalized care, on-site allied health, and memory-friendly layouts cater to advancing needs, ensuring lengthier stays and higher revenue per occupied bed.

Younger retirees between 65-74 years provide the funnel for future growth. Early exposure through day-stay wellness clubs and short-term respite stays familiarizes them with village life, easing the eventual transition. Active-age residents also shape programming choices, encouraging operators to add maker spaces, EV charging, and community gardens that refresh the appeal of the Australia senior living market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Sydney commands 20.4% of Australia senior living market share in 2024 on the back of concentrated wealth, dense health-care networks, and long-established village precincts in the northern beaches and Hills district. Premium developers acquire infill sites, recycle redundant industrial parcels, and add vertical towers that suit shrinking land supplies. Construction cost tension is highest here, yet resale uplift underpins feasibility.

Melbourne follows a similar demographic arc but is constrained by cost escalation stemming from planning compliance, green-star construction targets, and skilled labor shortages. Developers pivot toward outer growth corridors, aligning with downsizing preferences for lower-maintenance suburban living near extended family members. Council design overlays promote inclusive streetscapes, expanding walkability around senior hubs.

Perth records the fastest expansion pace at 9.32% CAGR across the forecast window. Lower median home values allow retirees to release equity, while coastal amenities and mild winters attract interstate migrants. Local planning schemes encourage community-title models that share clubhouses and landscaped open space, compressing per-unit land cost. The Australia senior living market size in Perth, therefore, rises quickly even though its current unit base is smaller.

Brisbane and the wider South-East Queensland corridor benefit from a projected regional population of 6 million by 2046. The massive housing need includes senior dwellings, with policy allocating quotas for affordable and social units. Developers leverage relatively flat topography and favorable climate to deliver single-level bungalows and hybrid land-lease estates. Accessibility to Gold Coast health campuses enhances appeal.

Regional centers such as Armidale, Ingham, and Hervey Bay welcome increasing retiree inflows. Cheaper land enables generous green buffers and hobby facilities, while proximity to tertiary hospitals reassures families. Community opposition sometimes arises, as seen in Kingscliff where locals question project scale. Engagement programs and staged delivery help smooth approvals and keep the national pipeline aligned with demographic demand.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

The Australia senior living market tilts toward moderate concentration. Not-for-profit operators hold the lion’s share of residential and home-care places, yet large corporate groups continue to expand. South Korea’s National Pension Service, with partner Scape, paid USD 2.695 billion for Aveo Group, signaling strong foreign institutional conviction. Stockland acquired USD 742 million in master-planned sites and USD 147 million in land-lease villages to deepen its nationwide footprint.

Lendlease plans to divest twelve projects and release USD 3.15 billion in capital to reinvest in growth sectors, a move that highlights the portfolio-optimizing trend among diversified groups. Mid-tier firms secure regional niches by offering culturally tailored services or veterans’ hubs. RSL LifeCare obtained USD 3.81 million from government grants to build a veteran wellbeing center that is integrated into its retirement village in Queanbeyan.

Technology partnership strategies gain prominence. Levande pilots AI companions for end-of-life planning, enhancing resident engagement while easing family stress. Operators that embed data analytics across workforce scheduling, medication management, and predictive maintenance lower costs and satisfy quality inspectors. The net effect is a rising barrier to entry for small standalone homes, nudging the sector toward scaled platforms capable of continuous investment.

Australia Senior Living Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: National Pension Service and Scape finalized the USD 2.695 billion Aveo Group purchase covering 65 villages across four states.

- November 2024: Stockland closed a USD 742 million deal for 12 master-planned communities and a USD 147 million purchase of five land-lease villages.

- November 2024: Levande commenced a digital AI companion pilot with charity Violet focused on advance-care planning.

- January 2024: RSL LifeCare won USD 3.81 million in federal funding to open a Veteran Wellbeing Hub in Queanbeyan.

Table of Contents for Australia Senior Living Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Accelerating aging demographics and rising longevity underpinning multi-decade demand

- 4.2.2Mature retirement village/land-lease models with strong resident services and amenity focus

- 4.2.3Home Care Packages and healthcare integration supporting step-up/step-down care pathways

- 4.2.4Downsizing to coastal and infill metro locations driving premium village demand

- 4.2.5Growing adoption of smart-home and wellness technologies improving resident experience

- 4.3Market Restraints

- 4.3.1Regulatory reforms and compliance scrutiny increasing operating complexity

- 4.3.2Construction cost inflation and trades shortages impacting feasibility

- 4.3.3Consumer sensitivity to fee transparency and contract structures affecting sales velocity

- 4.4Value / Supply-Chain Analysis

- 4.5Policy & Regulatory Framework (state guidelines, licensing, incentives)

- 4.6Insight on Upcoming and Ongoing Projects

- 4.7Insights on Digital & Tech Enablers (telemedicine, smart amenities)

- 4.8Insights on Business Model & Operator Evolution

- 4.9Insights on Investment & Financing Trends

- 4.10Insights Sustainability & Design Innovation

- 4.11Porter’s Five Forces

- 4.11.1Bargaining Power of Suppliers

- 4.11.2Bargaining Power of Buyers/Consumers

- 4.11.3Threat of New Entrants

- 4.11.4Threat of Substitutes

- 4.11.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Property Type

- 5.1.1Assisted Living

- 5.1.2Independent Living

- 5.1.3Memory Care

- 5.1.4Nursing Care

- 5.2By Business Model

- 5.2.1Outright Sale (Freehold)

- 5.2.2Long-Lease / Rental

- 5.2.3Hybrid (Sale + Lease)

- 5.3By Age

- 5.3.155 to 64 years

- 5.3.265 to 74 years

- 5.3.375 to 85 years

- 5.3.4Above 85 years

- 5.4By Key Cities

- 5.4.1Sydney

- 5.4.2Melbourne

- 5.4.3Brisbane

- 5.4.4Perth

- 5.4.5Rest of Australia

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, and Recent Developments)

- 6.3.1Stockland

- 6.3.2Lendlease

- 6.3.3Aveo

- 6.3.4Oak Tree Group

- 6.3.5IRT Group

- 6.3.6RSL LifeCare

- 6.3.7Living Choice

- 6.3.8Anglican Retirement Villages

- 6.3.9Gannon Lifestyle Group

- 6.3.10The Village Retirement Group

- 6.3.11Bolton Clarke

- 6.3.12RetireAustralia

- 6.3.13Lifestyle Communities

- 6.3.14Eureka Group Holdings

- 6.3.15Australian Unity

- 6.3.16Aware Super (Oak Tree platform)

- 6.3.17BaptistCare NSW & ACT

- 6.3.18Regis Aged Care

- 6.3.19BlueCare

- 6.3.20Arcare Aged Care

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Australia Senior Living Market Report Scope

Senior living is a concept that refers to various housing and lifestyle options for senior citizens that are adapted to the challenges of aging, such as limited mobility and susceptibility to illness. A complete background analysis of the Australia Senior Living Market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact is included in the report.

The Australian senior living market is segmented by property type (assisted living, independent living, memory care, and nursing care) and by cities (Sunshine Coast, Hobart, Melbourne, Perth, South Coast, and Other Cities). The report offers market size and forecasts in value (USD) for all the above segments.