Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

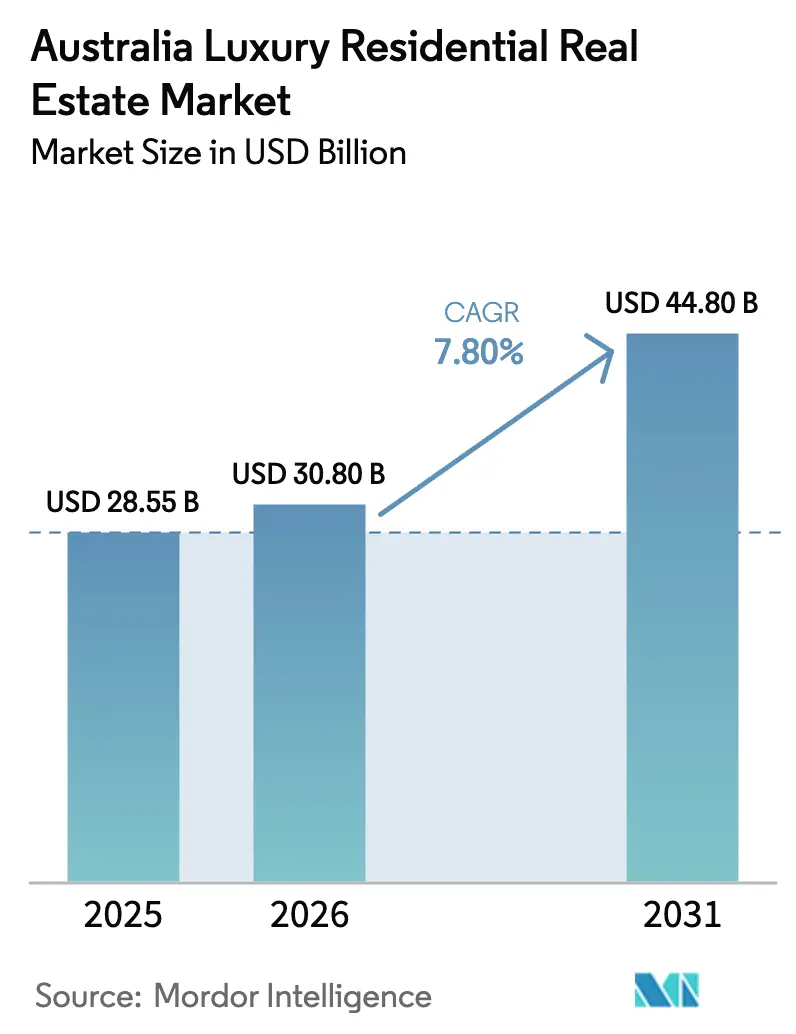

| Base Year Market Size (2025) | USD 28.55 Billion |

| Market Size (2026) | USD 30.80 Billion |

| Market Size (2031) | USD 44.80 Billion |

| Growth Rate (2025 - 2031) | 7.80% CAGR |

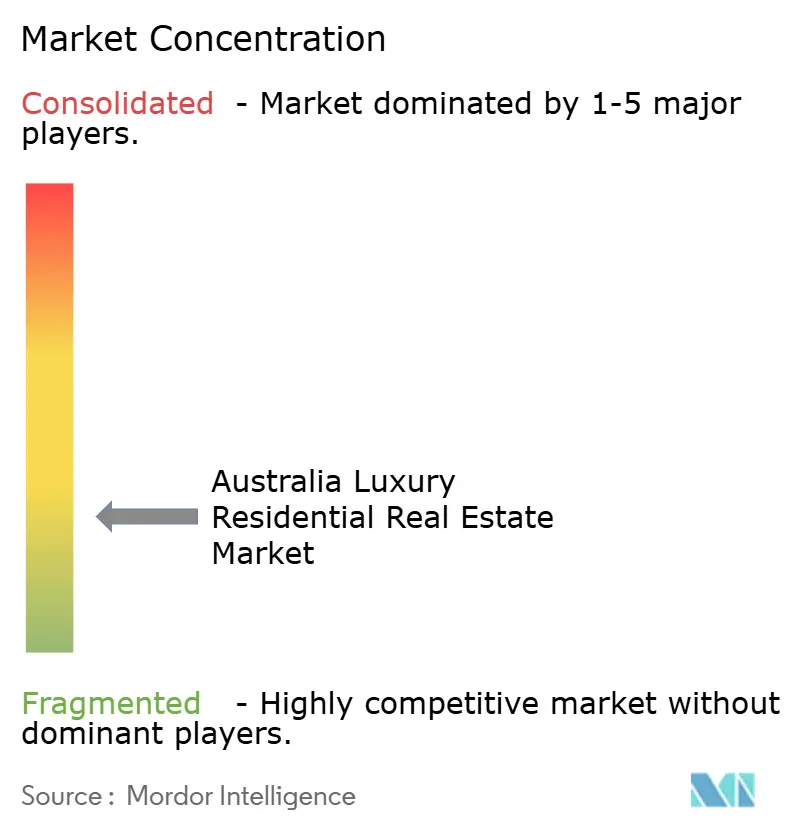

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Luxury Residential Real Estate Market Analysis by Mordor Intelligence

The Australia luxury residential real estate market size is expected to grow from USD 28.55 billion in 2025 to USD 30.80 billion in 2026 and is forecast to reach USD 44.8 billion by 2031 at a 7.8% CAGR over 2026-2031[1]Reserve Bank of Australia, “Monetary Policy Decision – February 2026,” rba.gov.au. Elevated demand from ultra-high-net-worth buyers across Asia-Pacific, combined with tight new-build pipelines in Sydney and Melbourne, is underpinning price resilience even as the Reserve Bank of Australia’s cash rate stands at 3.85%. Developers are reacting by pivoting toward branded residences and sustainability-led projects that can command premiums. Downsizers insulated from rate pressures continue to absorb well-located stock, while foreign capital is funnelled into primary schemes because established-dwelling purchases remain restricted. Institutional investors are simultaneously accelerating their entry through build-to-rent platforms, broadening the income profile of the Australian luxury residential real estate market.

Key Report Takeaways

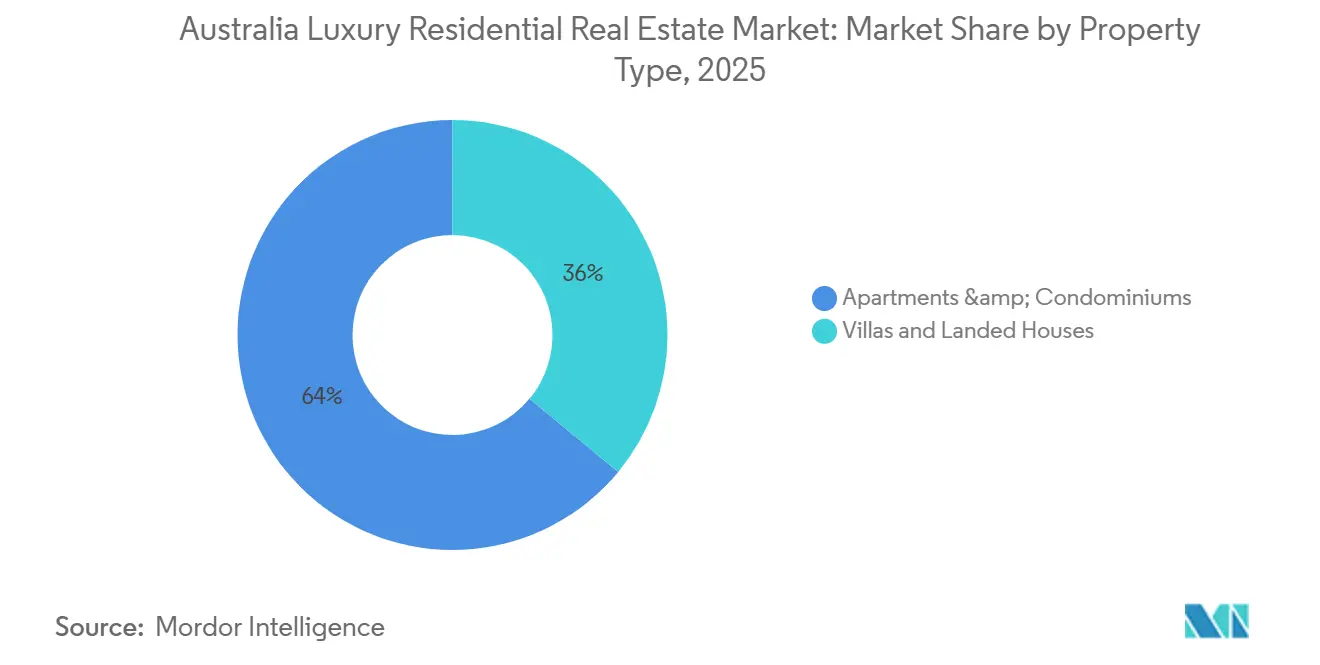

- By property type, apartments and condominiums led with 64% of Australia luxury residential real estate market share in 2025, whereas villas and landed houses are projected to advance at a 9.0% CAGR through 2031.

- By business model, the sales channel held 81% of the Australia luxury residential real estate market size in 2025, while the rental segment is expanding fastest at 8.4% annually to 2031.

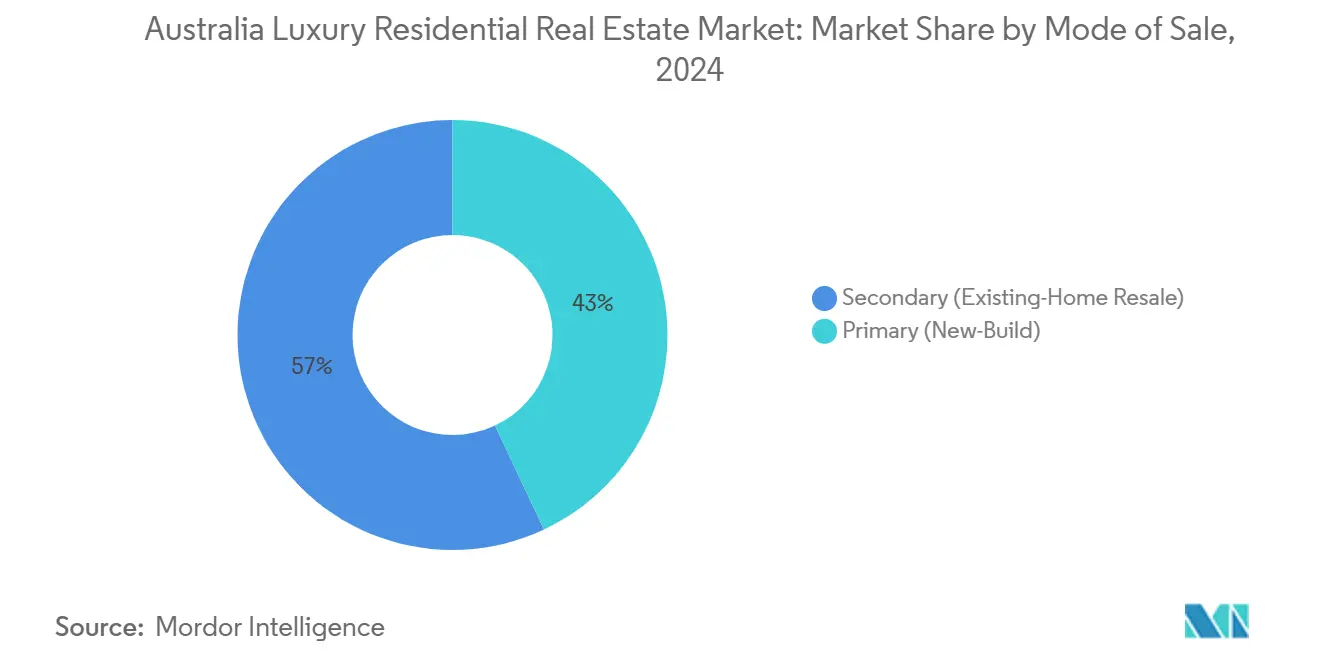

- By mode of sale, secondary transactions controlled 57% of value in 2025, yet the primary market is forecast to grow at 8.55% a year through 2031.

- By geography, Sydney captured 40% of 2025 revenue; Brisbane is on course for the quickest expansion with a 9.2% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Luxury Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise of branded-residence schemes | +1.4% | Brisbane, Sydney CBD, Melbourne Southbank, Gold Coast | Long term (≥ 4 years) |

| Continued inflow of UHNWIs from Asia-Pacific | +1.2% | Sydney, Melbourne, Brisbane | Medium term (2–4 years) |

| Premium on green-rated luxury stock | +1.1% | National | Medium term (2–4 years) |

| Remote-work wealth repatriation by expatriates | +0.9% | Sydney eastern suburbs, Melbourne inner-ring, Perth coastal | Medium term (2–4 years) |

| Streamlined Significant Investor Visa pathways | +0.7% | Sydney, Melbourne | Short term (≤ 2 years) |

| Tokenized / fractional ownership platforms | +0.5% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Continued Inflow of UHNWIs From Asia-Pacific (Post-COVID Border Reopening)

Net overseas migration has rebounded, and wealthy buyers from Hong Kong, Singapore, and mainland China have redirected portfolios toward Australian trophy homes. Sydney’s Point Piper logged a USD 87 million sale in 2024, while Bellevue Hill posted USD 53 million, both attributed to Asia-Pacific purchasers. Knight Frank counts 42,789 Australians worth more than USD 10 million, a cohort projected to grow 5.3% by 2028. These inflows tighten already-scarce prime inventory in Sydney and Melbourne, driving competitive bidding. Currency diversification and transparent legal frameworks reinforce Australia’s safe-haven appeal. As a result, competition for limited waterfront and inner-ring properties is set to intensify over the forecast horizon.

Remote-Work Wealth Repatriation by Australian Expatriates

Professionals stationed in London, New York, and Singapore increasingly retain offshore roles while resettling in Australia. Favorable exchange rates boosted their local buying power through 2025, and the downsizer super-contribution scheme further lubricates capital transfers into high-end dwellings[2]Department of Home Affairs, “Migration and Visa Programs,” homeaffairs.gov.au . Prestige auctions in Mosman, Toorak, and Peppermint Grove now feature a heightened expatriate presence, many purchasing without financing contingencies. The six-year capital-gains-tax rule lets returnees keep former principal residences abroad, adding portfolio flexibility. Combined, these factors enlarge the domestic buyer pool exactly as higher interest rates sideline some leveraged residents.

Streamlined Significant Investor Visa Pathways

Regulatory tweaks in 2024 tilted SIV mandates toward venture capital, yet qualifying entrants continue to park a portion of the required USD 3.3 million minimum into luxury apartments. Because the Foreign Investment Review Board bans second-hand home purchases until March 2027, new-build towers like One Darling Point enjoy predictable offshore demand. Developers now include concierge desks, multilingual staff, and culturally resonant interiors to capture visa-linked capital quickly. With average application approvals running six months, inflows should remain brisk in the near term.

Rise of Branded-Residence Schemes With Five-Star Hotel Operators

Projects pairing luxury dwellings with hotel services have surged. Melbourne’s USD 1.5 billion STH BNK integrates a Four Seasons hotel plus branded residences stretching 1,000 ft skyward. Brisbane’s St Regis Gold Coast and Sydney’s recently opened Waldorf Astoria homes replicate the template, promising owners perks such as priority dining, housekeeping, and rental pools. Family offices rate these hybrids highly for liquidity and professional management. The model is expected to capture a rising slice of the Australia luxury residential real estate market as service-oriented living gains favor.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated cost of capital from RBA rate hikes | −1.1% | National | Medium term (2–4 years) |

| Escalating foreign-buyer stamp-duty surcharges | −0.8% | New South Wales, Victoria | Short term (≤ 2 years) |

| Near-term oversupply risk in Brisbane prime pipeline | −0.6% | Brisbane CBD, South Brisbane, Fortitude Valley | Short term (≤ 2 years) |

| Heightened AML scrutiny lengthening deal cycles | −0.4% | National | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Escalating Foreign-Buyer Stamp-Duty Surcharges

New South Wales lifted its foreign-buyer surcharge to 9% in 2025, while Victoria maintains an 8% levy[3]Revenue NSW, “Foreign Purchaser Surcharge Duty,” revenue.nsw.gov.au. On a USD 6.7 million Sydney apartment, duties top USD 600,000, denting internal rates of return. Many offshore purchasers, already restricted to new builds, now negotiate developer incentives such as rental guarantees or turnkey furnishing to blunt added costs. The upshot is deeper bifurcation: foreign funds concentrate in tower launches, whereas existing mansions lean ever more on domestic liquidity.

Near-Term Oversupply Risk in Brisbane Prime-Apartment Pipeline

More than 6,000 luxury units are scheduled to settle across Brisbane’s CBD corridors by 2027, yet pre-sales momentum weakened during 2025 amid cost-of-living concerns. Should buyer uptake stall, developers may postpone stages or discount inventory, pressuring valuations citywide. Infrastructure wins like Cross River Rail offset some risk, but absorption hinges on broader rate relief. Market participants, therefore, monitor construction progress closely before committing deposits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Villas Maintain Scarcity-Driven Pricing Power

Villas and landed houses accounted for only 36% of 2025 turnover yet captured 45% of total value, reflecting premium per-asset pricing within the Australia luxury residential real estate market. Supply barriers, heritage overlays in Sydney’s eastern suburbs and height caps in Melbourne’s inner ring—keep new stock minimal. Perth’s coastal enclaves logged 20% average appreciation in 2024 as mining dividends fueled cash purchases. Over 2026-2031, villas are forecast to expand at a 9.0% CAGR, the fastest among property types, supported by family buyers and expatriates seeking space and privacy.

Apartments and condominiums, while slower growing, remain the volume backbone because foreign purchasers are limited to off-the-plan options. Branded-residence towers such as Waldorf Astoria Sydney and Four Seasons Melbourne ensure this segment retains liquidity. Downsizers favor boutique blocks near transit, leveraging the downsizer super-contribution to redeploy equity after selling suburban family homes. Consequently, the Australian luxury residential real estate market size generated by apartments will still exceed USD 25 billion by 2031, even as villas outpace in growth.

By Business Model: Rental Platforms Race Ahead

Sales transactions captured 81% of 2025 value, yet luxury rentals are scaling more rapidly as global investors hunt defensive yield. Institutional players are assembling build-to-rent portfolios, buoyed by sub-2% vacancy in inner-Sydney and Melbourne CBDs. The rental segment is on track for an 8.4% annual increase to 2031, reflecting both absolute supply growth and inflation-linked escalations baked into premium leases.

Meriton’s serviced-apartment arm illustrates the model’s appeal: occupancy averaged 85% in 2025 across 13 locations, while room rates climbed 6.5% year-on-year. By comparison, traditional owner-occupier sales depend more heavily on mortgage affordability and stamp-duty settings. As interest rates begin their expected descent post-2026, some pent-up purchase demand will re-emerge, but the institutional presence in rentals is now entrenched, cementing a dual-track future for the Australia luxury residential real estate market.

By Mode of Sale: Primary Schemes Dominate Foreign Demand

Secondary dwellings represented 57% of 2025 activity, yet new-build (primary) inventory is projected to post an 8.55% CAGR, outstripping resale stock. FIRB restrictions prohibit non-residents from buying established homes until at least 2027, redirecting offshore funds into branded and green-rated towers. Developers respond by advertising six-star energy credentials and offering rental guarantees, tactics that cut through higher duty costs.

Victoria’s off-the-plan stamp-duty concession, effective since 2024, shaved up to USD 27,000 from average transaction outlays, propelling Mirvac to pre-sell 80% of its 45-story riverside tower within 24 hours. In contrast, private-treaty trophy homes reliant on a narrower domestic buyer base now circulate longer before exchange. Nevertheless, the secondary channel will retain a slim majority because heritage assets in Point Piper, Toorak, and Peppermint Grove possess irreplaceable land scarcity that no tower can replicate.

Geography Analysis

Sydney commanded 40% of the Australian luxury residential real estate market in 2025, thanks to deep liquidity and a pipeline of landmark towers such as One Darling Point. A record 100 transactions above USD 10 million closed in 2024, totaling USD 1.586 billion, with waterfront suburbs, Point Piper, Vaucluse, Mosman, dominating headline numbers. Rate-sensitive buyers have thinned, but cash purchasers still support pricing, and ongoing transport megaprojects like Metro West underpin confidence.

Melbourne trailed in share yet showcases the nation’s most ambitious branded-residence stack, including the USD 1.5 billion STH BNK and Riverlee’s Seafarers. While top-tier values dipped 4% in 2024 on higher financing costs, Victoria’s stamp-duty incentives revived momentum, evidenced by rapid sell-outs of riverside towers. The city’s leafy zones, Toorak, Brighton, continue to command premiums among expatriates eager for international-school catchments.

Brisbane is the forecast growth leader with a 9.2% CAGR to 2031, propelled by Olympic-driven infrastructure upgrades and a relative affordability edge over southern capitals. Short-term oversupply risk lurks as CBD completions peak in 2026-2027, yet long-run fundamentals, interstate migration, and lifestyle appeal remain intact. Perth, buoyed by resources revenue, posted 20% luxury price expansion in 2024 and ranks 16th globally for prime growth. Coastal precincts such as Cottesloe and Dalkeith have scant developable land, meaning any slowdown elsewhere may have muted local impact. Secondary lifestyle markets, Gold Coast, Adelaide Hills, also flourish as remote-work flexibility endures, rounding out a geographically diversified Australia luxury residential real estate market.

Competitive Landscape

Competition intensified when Knight Frank and Bayleys acquired a controlling stake in McGrath Estate Agents in June 2024, forming a 140-office, 2,400-staff east-coast powerhouse. Scale enables superior global referral pipelines and compliance bandwidth, crucial under stricter AML reporting. Rival agencies—CBRE, Sotheby’s International Realty, Ray White—respond by enhancing virtual tours and AI-driven buyer-matching to capture tech-savvy UHNWIs abroad.

On the development side, Lendlease, Mirvac, and Gurner spearhead branded, ESG-aligned towers while outsourcing risk via joint ventures. Their shortlisting for the USD 1.5 billion Sydney Metro over-station project in 2026 underscores the appetite for public-private tie-ups that bundle transport access with luxury air-rights. Smaller firms such as Time & Place and Pallas Group carve niches in adaptive-reuse and boutique low-rise blocks, leveraging design artistry where scale alone cannot compete.

Regulatory friction favors larger players possessing dedicated AML and FIRB compliance desks. CBRE’s Q1 2025 valuer survey revealed 43% of specialists anticipate further capital appreciation this year, a sentiment stronger among those marketing turnkey green-rated stock. With tokenization pilots gathering pace, early-adopter brokerages that can navigate ASIC guidance may unlock incremental fee streams, adding a fresh competitive dimension to the Australia luxury residential real estate market.

Australia Luxury Residential Real Estate Industry Leaders

Lendlease

Mirvac

Crown Group

Gurner™

Frasers Property Australia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Waldorf Astoria Sydney inaugurated its branded-residence collection, adding 43 serviced sky-homes above Circular Quay.

- January 2026: Lendlease and Mirvac jointly shortlisted for the USD 1.5 billion Sydney Metro over-station scheme, signaling deeper collaboration on transit-oriented luxury precincts.

- January 2025: West End Luxury Tower Proposal, Brisbane - A 16-level residential tower featuring a rooftop pool, gym, and 199 car spaces was proposed in Brisbane’s West End. The design retains a heritage façade, though the project has raised community concerns about congestion and infrastructure strain.

- July 2024: Gurner partnered with Qualitas on the USD 2.75 billion Jam Factory overhaul in Melbourne. The alliance pairs local design expertise with institutional capital to deliver one of the city’s largest high-end mixed-use precincts.

Australia Luxury Residential Real Estate Market Report Scope

By Business Model

| Sales |

| Rental |

Residential (Sales Model) Size & Forecasts

| By Property Type | Apartments & Condominiums |

| Villas & Landed Houses | |

| By Mode of Sale | Primary (New-Build) |

| Secondary (Existing-Home Resale) | |

| By Key Cities | Sydney |

| Melbourne | |

| Brisbane | |

| Perth | |

| Rest of Australia |

| By Business Model | Sales | |

| Rental | ||

| Residential (Sales Model) Size & Forecasts | By Property Type | Apartments & Condominiums |

| Villas & Landed Houses | ||

| By Mode of Sale | Primary (New-Build) | |

| Secondary (Existing-Home Resale) | ||

| By Key Cities | Sydney | |

| Melbourne | ||

| Brisbane | ||

| Perth | ||

| Rest of Australia | ||

Key Questions Answered in the Report

How large will Australia’s luxury residential sector be in 2031?

It is forecast to reach about USD 44.8 billion by 2031, expanding at a 7.8% CAGR from 2026.

Which city is growing fastest for luxury homes?

Brisbane leads with a projected 9.2% CAGR through 2031, lifted by Olympic-linked infrastructure and relative affordability.

What segment attracts most foreign capital today?

Primary new-build apartments dominate because non-residents remain banned from purchasing established dwellings until 2027.

Are branded residences gaining traction?

Yes, schemes tied to hotels like Waldorf Astoria and Four Seasons are proliferating and enjoy strong absorption among time-poor UHNWIs.

How are higher interest rates influencing the market?

Elevated borrowing costs sideline leveraged buyers and developers, but cash-rich purchasers keep trophy transactions buoyant.

Page last updated on: