Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

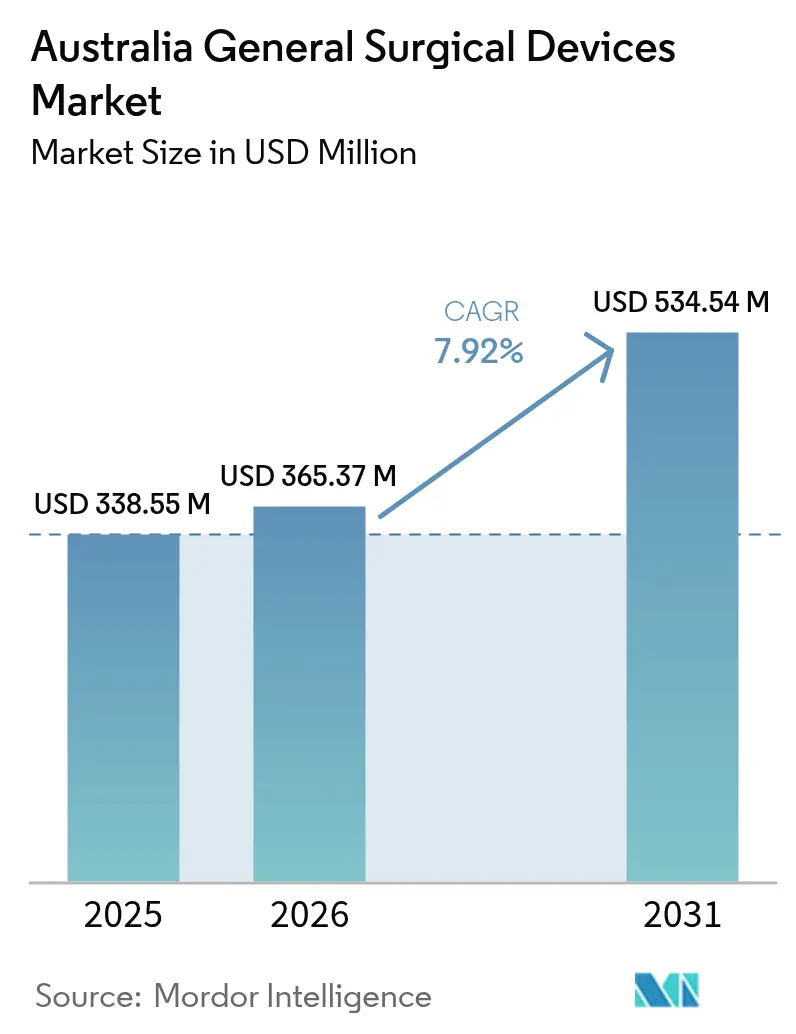

| Base Year Market Size (2025) | USD 338.55 Million |

| Market Size (2026) | USD 365.37 Million |

| Market Size (2031) | USD 534.54 Million |

| Growth Rate (2026 - 2031) | 7.92% CAGR |

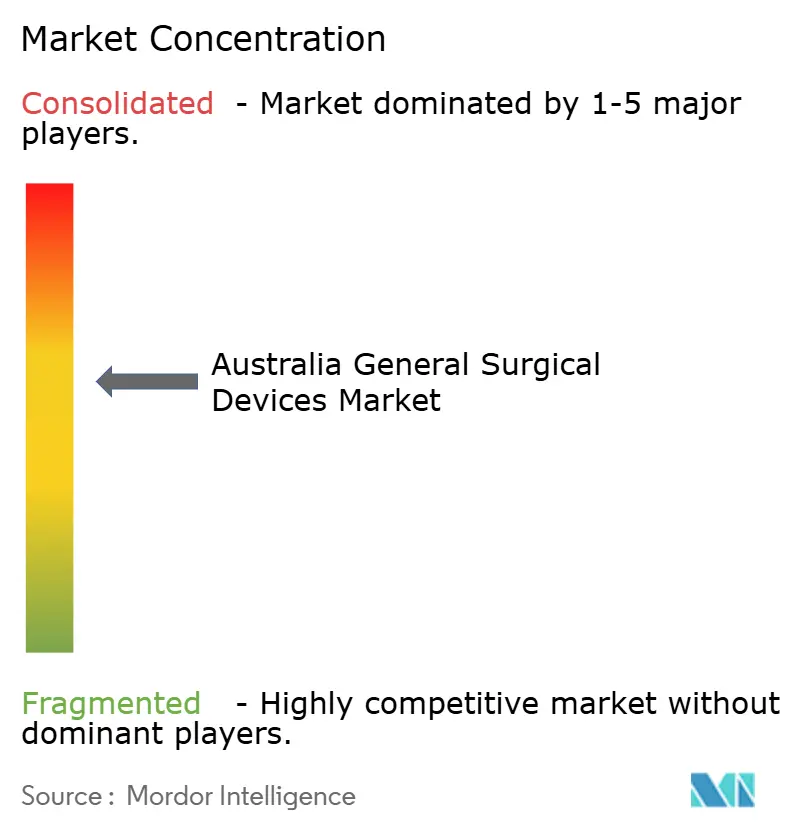

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia General Surgical Devices Market Analysis by Mordor Intelligence

Australia General Surgical Devices Market size in 2026 is estimated at USD 365.37 million, growing from 2025 value of USD 338.55 million with 2031 projections showing USD 534.54 million, growing at 7.92% CAGR over 2026-2031. Steady procedure growth arises from a population aged 65 and over that will expand by 60% by 2030, amplifying demand for orthopedic, cardiovascular and oncologic interventions. Hospitals are investing in minimally invasive and robotic solutions to shorten recovery times, lower complications and optimise workforce utilisation, while ambulatory surgical centres (ASCs) scale rapidly to ease elective-surgery backlogs. Import-driven supply chains, which cover the majority of devices, expose providers to currency swings and geopolitical risk, yet also keep global innovation pipelines open. Regulatory reforms by the Therapeutic Goods Administration (TGA) add compliance intensity but harmonise local rules with peer markets, encouraging faster adoption of devices already cleared in the United States or Europe.

Key Report Takeaways

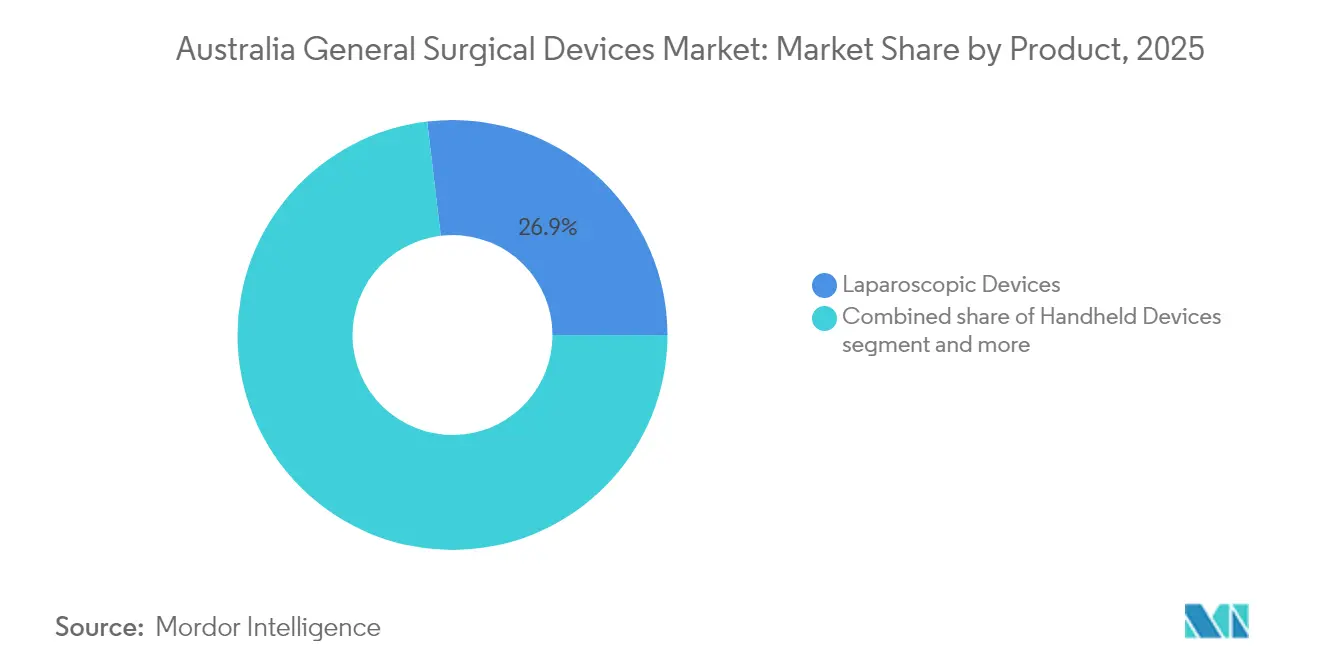

- By product: Laparoscopic devices led with 26.88% of Australia general surgical devices market share in 2025, while robotic and computer-assisted systems record the highest projected CAGR at 9.28% through 2031.

- By procedure approach: Minimally invasive surgery accounted for a dominant 69.76% share of the Australia general surgical devices market size in 2025; the segment is advancing at a 9.31% CAGR to 2031.

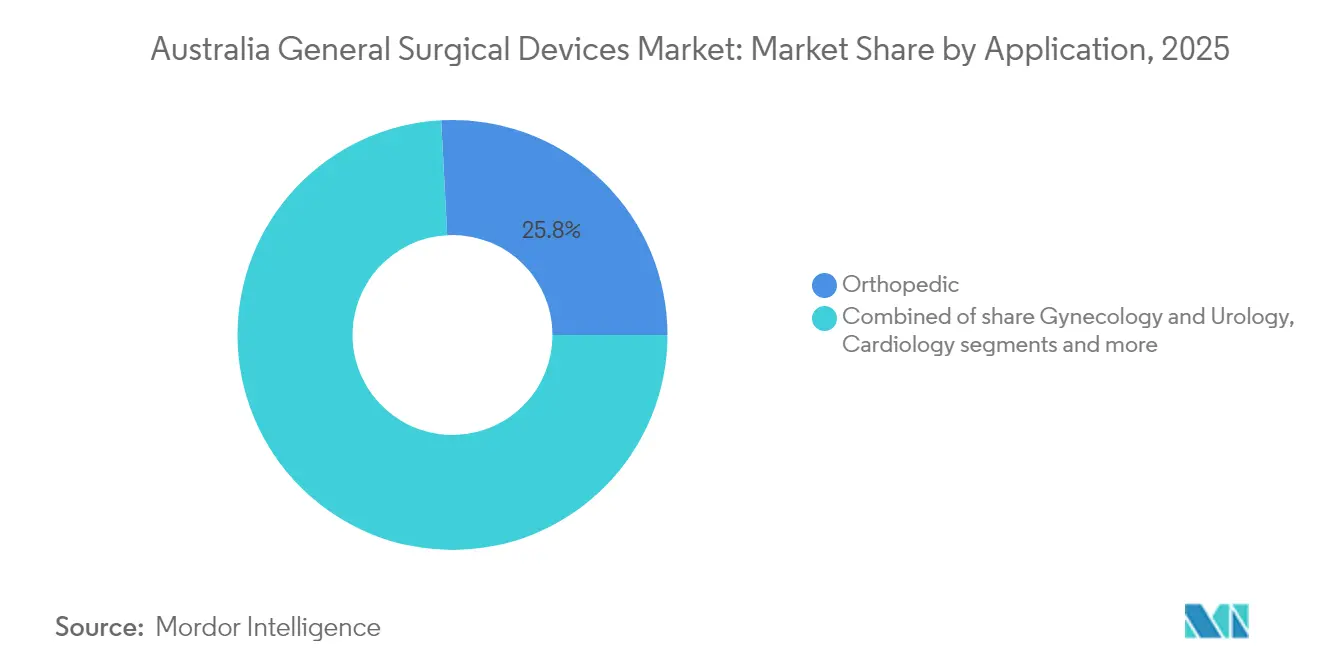

- By application: Orthopedic procedures captured 25.84% of Australia general surgical devices market share in 2025, whereas gynecology and urology applications are projected to expand at 9.95% CAGR between 2026-2031.

- By end user: Hospitals held 71.98% of the Australia general surgical devices market size in 2025 and remain the volume anchor; ASCs show the fastest growth at 10.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia General Surgical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for minimally-invasive procedures | +2.1% | National, with concentration in major metropolitan areas | Medium term (2-4 years) |

| Growing incidence of trauma & accident cases | +1.3% | National, with higher impact in regional trauma centers | Short term (≤ 2 years) |

| Rapid adoption of advanced energy & stapling platforms | +1.8% | Metropolitan hospitals and specialized surgical centers | Medium term (2-4 years) |

| Aging population fuelling surgical volumes | +2.4% | National, with pronounced impact in outer metropolitan areas | Long term (≥ 4 years) |

| Expansion of same-day surgery centres | +1.7% | Metropolitan and regional centers | Medium term (2-4 years) |

| Shift toward single-use sterile instruments post-COVID | +1.2% | National healthcare facilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Minimally Invasive Procedures

Over the past decade, laparoscopic volumes have risen sharply, mirroring New Zealand data where appendicectomy laparoscopy moved from 83% to 95% of cases. Australian surgeons highlight faster patient recovery and lower complication rates as key benefits, and hospital administrators see reduced bed-days and lower cost per case. Demand translates into sustained orders for trocars, flexible scopes and energy platforms compatible with small-incision techniques. AI-driven image guidance, now under pilot evaluation, promises further gains in intraoperative accuracy. These factors collectively lift utilisation rates of products that enable 1-cm or smaller access ports, consolidating minimally invasive leadership in the Australia general surgical devices market.

Growing Incidence of Trauma & Accident Cases

Outdoor recreation and dispersed road networks contribute to trauma complexity, making specialised surgical airway and haemostasis tools indispensable. Emergency surgical procedures, particularly front-of-neck access interventions, are critical for trauma centers but are infrequent, creating training and equipment challenges.[1]Source: Journal of Trauma Resuscitation and Emergency Medicine, “Emergency Surgical Airway Experience,” doi.org An Alfred Hospital registry found emergency cricothyroidotomy at 0.22% of intubations, underscoring the need for rare but readiness-critical instruments. Direct costs of major trauma average AUD 78,000 per episode, justifying investment in devices that shorten operative time and curb complications. Regional centres favour portable kits with versatile clamps and suction as they must treat time-sensitive injuries without tertiary-hospital infrastructure. Government initiatives to verify trauma systems nationwide are spurring procurement upgrades, amplifying opportunity for suppliers of core general surgery sets.

Rapid Adoption of Advanced Energy & Stapling Platforms

Hospitals increasingly specify ultrasonic and bipolar devices that seal vessels while cutting tissue in a single step. Ethicon’s HARMONIC and ENSEAL families report USD 101 savings per case by shaving minutes off theatre time and reducing length of stay. Electrosurgical innovations, such as the Anovo system, deliver thermal precision comparable to legacy handpieces with reduced lateral thermal spread. Stapler platforms evolving toward robotic compatibility ride the same efficiency wave, supported by 9.2% projected regional CAGR in advanced stapling solutions. Occupational health regulations around surgical smoke extraction also push theatres to adopt integrated energy consoles that pair cutting performance with air filtration.

Aging Population Fuelling Surgical Volumes

Australians aged 65 and above will approach 22% of the national total by 2026, and this cohort consumes six times more health expenditure than younger groups. Joint-replacement backlogs, accentuated during the pandemic, now require 16% annual growth in case throughput to return to pre-COVID trajectories. Older patients with multimorbidity demand instruments accommodating fragile tissue and osteoporotic bone, such as low-profile retractor systems and cementless implant tools. Hospitals respond by allocating more lists to orthopedic and oncologic specialties, fuelling double-digit procurement growth. Device makers that tailor ergonomic handles and torque-controlled drivers to senior anatomy gain competitive advantage in the Australia general surgical devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent TGA regulatory approvals | -1.4% | National regulatory compliance requirements | Medium term (2-4 years) |

| Limited reimbursement for several device categories | -0.9% | National, with variations across public and private sectors | Long term (≥ 4 years) |

| High capital cost of advanced surgical systems | -1.1% | Metropolitan hospitals and specialized surgical centers | Medium term (2-4 years) |

| Import-dependence driven supply-chain risks | -0.8% | National, with higher impact on regional healthcare facilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent TGA Regulatory Approvals

The TGA’s audit expansion subjects higher-risk devices to detailed dossier reviews, adding six-month delays and compliance costs that can exceed AUD 100,000 per submission. Recent withdrawals of spinal cord stimulators highlight intensified post-market surveillance, prompting manufacturers to set aside greater contingency budgets. Smaller innovators struggle to fund clinical data generation and may prioritise other Asia-Pacific countries with lighter regulation. While mutual recognition of European CE marks eases some burden, requirements for local representative offices and ongoing performance reports still lengthen commercialisation timelines.

Limited Reimbursement for Several Device Categories

Medicare and private health schedules do not yet reimburse items such as facial prostheses or advanced orthotic constructs, leaving an estimated AUD 13 million annual funding gap for 2,000 patients needing cranio-maxillofacial implants. Absence from the Prostheses List forces hospitals to source via capital budgets, slowing adoption of novel tools that lack immediate tariff codes. Variability among insurers adds administrative burden for device firms that must negotiate item-level benefits. Advocacy groups press for list reforms, but near-term prospects remain cautious, tempering revenue projections for premium-priced implants and robotic accessories in the Australia general surgical devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Robotics Drive Innovation Wave

Laparoscopic instruments retained USD 91.02 million revenue and 26.88% Australia general surgical devices market share in 2025, underlining their role as the core toolkit for abdominal, thoracic and pelvic procedures. Robotic and computer-assisted systems, though smaller in base, are forecast to expand at a 9.28% CAGR as hospitals integrate multi-port and single-port platforms certified by the TGA. The Hugo system’s inaugural inguinal hernia repair signalled Australia’s transition toward modular robotics that reduce docking time and broaden anatomical reach. Electrosurgical generators capture volume via bundled contracts with hand instruments, and wound-closure devices evolve through barbed sutures and bio-absorbable clips aimed at lowering infection risks.

Handheld devices stay relevant because nearly every procedure begins with scalpels or scissors that surgeons know intimately. Port access systems continue to upgrade sealing technology to preserve pneumoperitoneum during instrument exchange. In “other devices,” Australian centres trial AI-enabled force-sensing graspers that warn of tissue stress, reflecting a shift toward data-rich operating theatres. St Vincent’s Hospital’s adoption of the Symani robot for microsurgery underscores domestic appetite for precision platforms even in sub-specialties such as lymphatic repair. Combined, these product trends confirm a steady pivot to smarter, energy-efficient and ergonomic tools within the Australia general surgical devices market.

By Procedure Approach: Minimally Invasive Dominance

Minimally invasive surgery generated USD 236.19 million, representing 69.76% of Australia general surgical devices market size in 2025, and is expected to grow at 9.31% CAGR through 2031. Conversion-to-open rates continue to fall as surgeons gain proficiency with articulating staplers, articulated scopes and 3-D visualisation towers. Hospitals justify investments by pointing to 1.5-day median reductions in length of stay and lower wound-site infection rates. Endoscopic retrograde procedures, once the domain of gastroenterologists, now often involve general surgeons, expanding the installed base of flexible endoscopes.

Open surgery retains importance for trauma, oncologic debulking and adhesiolysis where adhesions complicate minimal access. Yet its overall share is likely to slip below 20% by 2031 as robotic arms replicate wrist-like motion inside the body and single-incision ports mature. Training bodies mandate proficiency standards that phase residents through laparoscopic to robotic curricula, ensuring a pipeline of skilled users. The trend entrenches minimally invasive orientation as the default pathway in the Australia general surgical devices market.

By Application: Orthopedics Lead, Gynecology Surges

Orthopedics contributed USD 87.49 million and 25.84% Australia general surgical devices market share in 2025, fuelled by knee and hip arthroplasty demand among the aging yet active population. Robotic-arm-assisted resurfacing and patient-specific 3-D printed jigs illustrate how engineering advances align with surgeon goals of alignment accuracy and rapid mobilisation. Implant suppliers partner with instrument makers to deliver integrated trays that cut set-up time.

Gynecology and urology, projected to grow by 9.95% CAGR, benefit from higher diagnosis rates of endometriosis and prostate hyperplasia. Single-port laparoscopy for hysterectomy reduces scarring and recovery intervals, raising instrument turnover in reproductive health centres. Smith+Nephew’s foot-and-ankle launch shows crossover innovations where suture-bridge constructs move from sports medicine into pelvic floor repair. Neurology and cardiovascular segments add incremental volume through hybrid‐OR adoption, strengthening diversified application demand in the Australia general surgical devices market.

By End User: Hospitals Dominant, ASCs Accelerating

Hospitals held 71.98% of Australia general surgical devices market size in 2025, reflecting their role as referral hubs with intensive care and imaging back-up. Teaching hospitals lead early-adopter behaviour by trialling “digital twin” simulations that pre-plan resections, locking in long-term vendor relationships. Capital-purchase cycles typically run five years, aligning with TGA shelf-life certifications and allowing predictable tender calendars.

ASCs expand at a projected 10.18% CAGR as payers incentivise same-day discharge for procedures such as cholecystectomy and ACL repair. Nexus Hospitals reports that day and short-stay models underpin private health sustainability by trimming bundled costs. These centres specify compact, multi-functional instrumentation to manage tight sterilisation timelines. Specialty clinics, though smaller, require bespoke sets for bariatric or colorectal niches, adding steady secondary demand. Workforce shortages emphasise the importance of intuitive devices that cut training time, reinforcing technology uptake across all end-user tiers in the Australia general surgical devices market.

Geography Analysis

Metropolitan hubs such as Sydney, Melbourne, Brisbane and Perth account for majority of procedure volumes, thanks to dense populations and tertiary facilities equipped for complex surgery. New South Wales alone houses more than 60 registered hospitals with robotic systems, drawing referral flows from neighbouring states.

Regional centres in Queensland, South Australia and Tasmania face logistic challenges yet gain traction through modular theatres and remote mentoring. Pilot 5G-enabled telesurgery demonstrated safe gastrectomy between Adelaide and a rural site 150 km away, proving feasibility for complex care decentralisation. Such connectivity accelerates transfer of robotics know-how, boosting Australia general surgical devices market penetration beyond capital cities.

Remote Indigenous communities depend on fly-in surgical teams that carry lightweight electrosurgical units and portable suction, creating niche demand for battery-powered devices. Supply-chain resilience remains critical because the majority of instruments are imported; distributors have set up state-based warehouses to hold three-month safety stock against maritime delays. State procurement frameworks vary in tender periods and localisation quotas, so vendors often partner with accredited Aboriginal enterprises to fulfil social procurement targets. Overall, geographic diversification supports steady national uptake and cushions macroeconomic shocks for the Australia general surgical devices market.

Competitive Landscape

The Australia general surgical devices market features moderate concentration, with multinationals such as Medtronic, Johnson & Johnson, Stryker and Olympus holding strong footprints via long-standing distributor alliances and direct sales teams. Johnson & Johnson’s USD 1.3 billion global spend on surgical instruments in 2024 funds pipeline expansion into advanced energy and AI-guided stapling. Medtronic leverages its Hugo platform approvals to cross-sell trocars and electrosurgical tools, strengthening account stickiness in private hospitals.

Australian innovators add competitive spark. Convergence Medical attracted AUD 5 million to commercialise its VO1 arthroscopic robot aimed at sports medicine suites. Trewavis Surgical emphasises “Australian-made” branding on bone wires and diathermy pencils, appealing to buyers seeking alternative supply sources during shipping disruptions. Nanosonics and Device Technologies support infection-control portfolios that bundle probes and instrument reprocessing systems, exploiting hospitals’ zero-tolerance stance on cross-contamination.

Strategic moves focus on education, data and sustainability. Stryker’s Melbourne innovation centre provides virtual reality training for Mako robotic joint replacement, while Olympus partners with universities to run endoscopy fellowships. Several vendors pledge carbon-neutral operations by 2030, investing in recyclable packaging and re-manufacturing loops for metal hand instruments. Together, these tactics underline an ecosystem where service depth and environmental credentials carry as much weight as device performance in the Australia general surgical devices market.

Australia General Surgical Devices Industry Leaders

Boston Scientific Corporation

Johnson & Johnson (Ethicon & DePuy Synthes)

Medtronic plc

B. Braun SE

Stryker Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The Australian government commits USD 3.05 million to introduce a surgical robot at Launceston General Hospital in Tasmania.

- May 2025: Noosa Hospital launches a new surgical system for breast-cancer treatment.

- February 2025: Alfred Hospital in Melbourne deploys the da Vinci Xi system, nicknamed “Royce,” for minimally invasive cancer and cardiothoracic procedures.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the Australia general surgical devices market includes all reusable and single-use instruments, such as handheld tools, laparoscopic sets, electrosurgical generators, wound-closure aids, trocars, and robotic or computer-assisted platforms, employed across open or minimally invasive procedures in hospitals, ambulatory surgery centers, and specialty clinics. Value figures reflect ex-factory revenues in U.S. dollars, net of distributor mark-ups and GST.

Scope exclusion: veterinary, dental-only kits, and purely diagnostic endoscopes are outside this study.

Segmentation Overview

- By Product

- Handheld Devices

- Laparoscopic Devices

- Electrosurgical Devices

- Wound-Closure Devices

- Trocars and Access Systems

- Robotic and Computer-Assisted Systems

- Other Devices

- By Procedure Approach

- Open Surgery

- Minimally Invasive Surgery

- By Application

- Gynecology and Urology

- Cardiology

- Orthopedic

- Neurology

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centres

- Specialty Clinics

Detailed Research Methodology and Data Validation

Primary Research

Interviews and structured surveys with theater nurses, biomedical engineers, procurement leads, and regional clinical-affairs managers across New South Wales, Victoria, and Queensland validated unit volumes, average selling prices, and adoption curves for stapling, energy, and robotic systems. Insights clarified uptake barriers, such as capital cost and reimbursement gaps, and confirmed forecast drivers uncovered during secondary research.

Desk Research

Mordor analysts first compiled supply-side baselines from open datasets issued by the Australian Institute of Health & Welfare, Therapeutic Goods Administration device registers, UN Comtrade surgical-instrument tariff codes, and hospital procedure statistics from the Independent Hospital Pricing Authority. Trade-body white papers, such as the Medical Technology Association of Australia, and peer-reviewed journals on operating-room trends complemented these. Paid libraries, notably D&B Hoovers for company revenues and Dow Jones Factiva for deal tracking, helped map vendor footprints. The sources cited illustrate our evidence base; many additional references informed granular checks.

Market-Sizing & Forecasting

A top-down reconstruction began with procedure counts by specialty, linked to device utilization coefficients derived from hospital item-number data; these volumes were then multiplied by blended ASPs to reach the baseline. Bottom-up cross-checks, including supplier revenue roll-ups and sampled ASC purchase invoices, aligned totals within an acceptable range. Key variables feeding the model include laparoscopic penetration rates, day-surgery share, aging population growth, device replacement cycles, capital budget allocations, and TGA approval timelines. Multivariate regression, supplemented by ARIMA smoothing, projects each driver through the forecast period; scenario tweaks from primary experts bound optimistic and conservative cases. Gaps in invoice coverage were bridged by applying validated ASP ranges to missing volume cells.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance flags, peer analyst audit, and senior-lead sign-off. Models refresh annually, with interim updates triggered by regulatory shifts or mergers; a final checkpoint occurs just before client delivery to ensure figures remain current.

Why Mordor's Australia General Surgical Devices Baseline Stands Reliable

Published estimates often differ because firms diverge on year-zero selection, product basket, and inflation treatment.

Key gap drivers are (a) inclusion of consumable sutures and implants by some publishers, inflating totals; (b) exclusion of high-ticket robotic platforms by others, compressing value; and (c) inconsistent currency conversions or older base years. Mordor sets a consistent 2025 anchor, applies real-world ASPs, refreshes annually, and blends top-down with selective bottom-up tests, thereby delivering a balanced baseline decision-makers can repeat.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 338.55 M (2025) | Mordor Intelligence | - |

| USD 316.8 M (2023) | Global Consultancy A | Older base year; excludes robotics and energy platforms. |

| USD 792.0 M (2023) | Industry Tracker B | Broad basket adds sutures, implants, and OR furniture. |

| USD 520.8 M (2024) | Regional Consultancy C | Uses top-down import data only; limited ASP verification. |

Taken together, the comparison shows that once scope and time frames are aligned, Mordor's disciplined variable selection and annual refresh cycle provide the most transparent, reproducible starting point for investment or go-to-market planning.

Key Questions Answered in the Report

What is the current size and growth outlook of the Australia general surgical devices market?

The market stands at USD 365.37 million in 2026 and is on track to reach USD 534.54 million by 2031, delivering an 7.92% CAGR.

Which product segment is expanding the fastest?

Robotic and computer-assisted systems show the highest momentum, with a projected 9.28% CAGR through 2031.

Why are ambulatory surgical centres important to device suppliers?

ASCs are the fastest-growing end-user group, advancing at a 10.18% CAGR, so they drive demand for compact, versatile instruments that support same-day discharge.

What major driver is shaping hospital purchasing decisions?

Minimally invasive procedures dominate with 69.76% market share in 2025 and a 9.31% CAGR, prompting hospitals to prioritise laparoscopic, robotic and advanced energy platforms.

How do TGA regulations affect market entry for new devices?

High-risk products undergo detailed audits that can add around six months to approval timelines and cost near AUD 100,000 in compliance work, requiring careful planning by manufacturers.

How concentrated is the competitive landscape?

The top five suppliers control a little over 60% of national revenue, giving the sector a concentration score of 6 and leaving space for emerging local innovators.

Page last updated on: