Taste Modulators Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

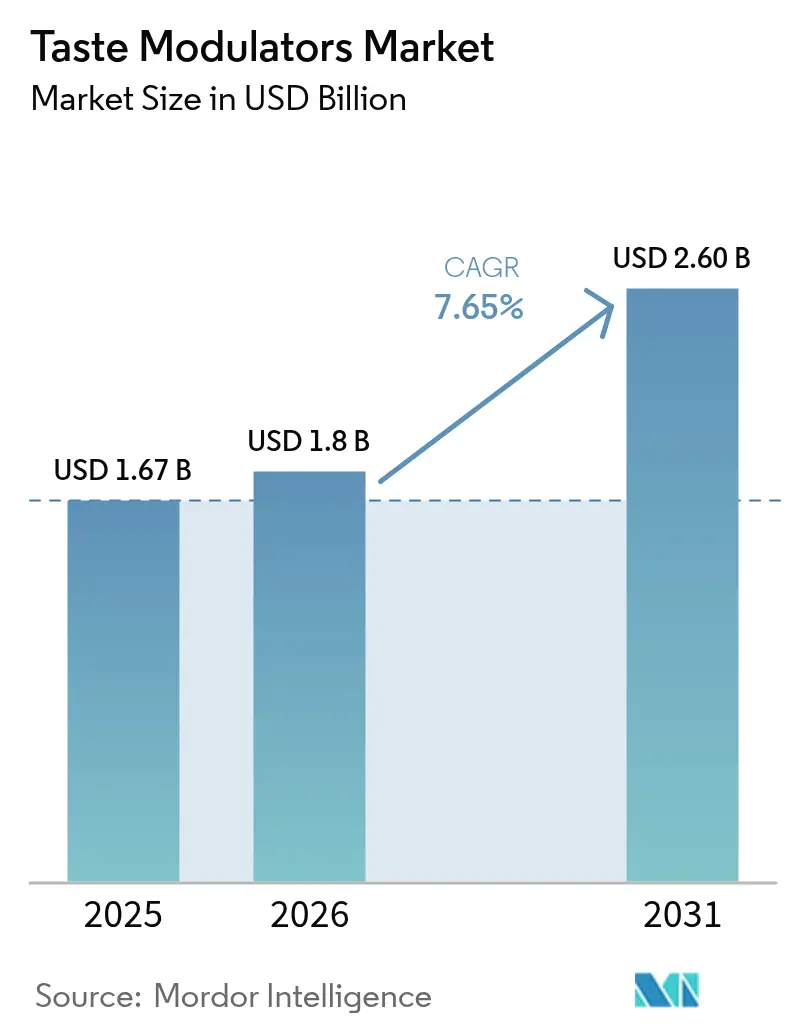

| Market Size (2026) | USD 1.8 Billion |

| Market Size (2031) | USD 2.6 Billion |

| Growth Rate (2026 - 2031) | 7.65% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Taste Modulators Market Analysis by Mordor Intelligence

The taste modulators market size is expected to grow from USD 1.67 billion in 2025 to USD 1.8 billion in 2026 and is forecast to reach USD 2.6 billion by 2031 at 7.65% CAGR over 2026-2031. The market growth stems from manufacturers transitioning from basic sugar substitutes to sophisticated taste modification technologies. Taste modulators allow food manufacturers to control sweetness, saltiness, mouthfeel, and aroma while reducing calories and sodium content. Regulatory measures by the U.S. Food and Drug Administration (FDA) on added sugars and sodium, combined with the World Health Organization's (WHO) recommendation to limit free sugars below 10% of total energy intake, have accelerated product reformulation across food, beverage, and pharmaceutical industries. These factors have established taste modulators as crucial ingredients in contemporary product development. Additionally, the growing consumer demand for healthier and low-calorie food and beverage options has further fueled the adoption of taste modulators.

Key Report Takeaways

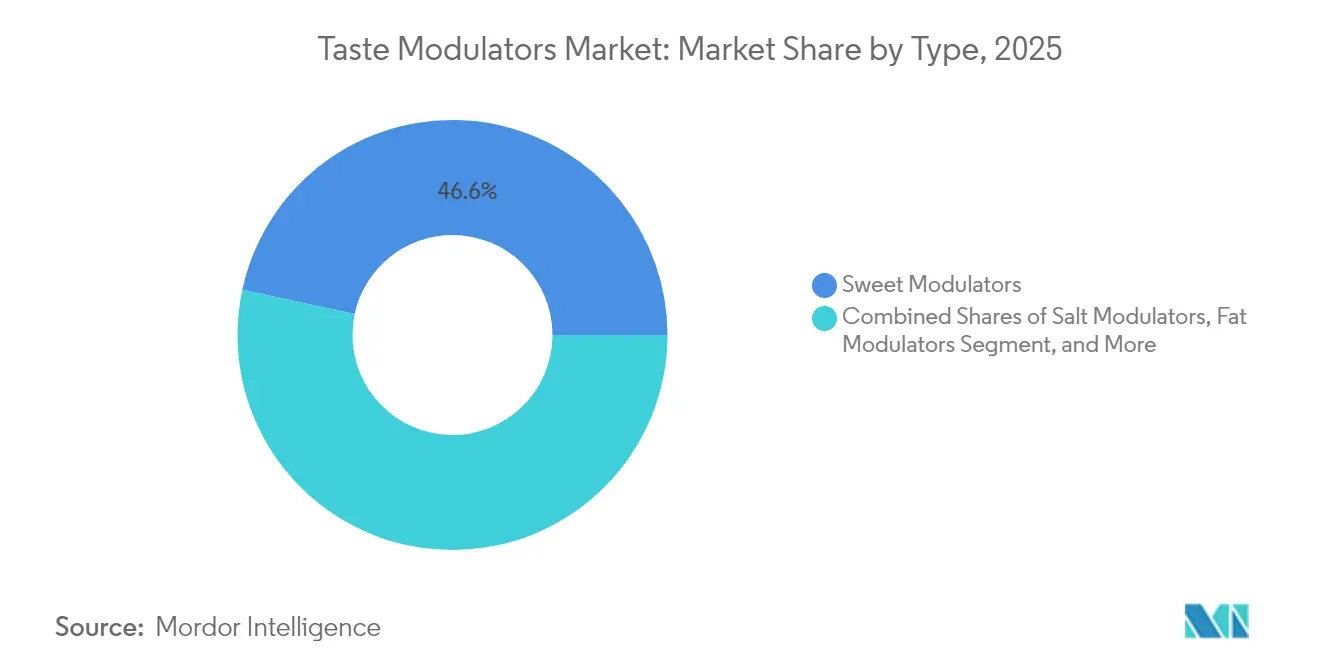

- By type, sweet modulators led with a 46.62% share of the taste modulators market in 2025; salt modulators are projected to expand at 9.32% CAGR through 2031.

- By source, natural ingredients captured 56.21% market share in 2025 and are expected to grow at a CAGR of 9.78% through 2031.

- By form, powders accounted for a 65.79% share of the taste modulators market in 2025, whereas liquids are set to record a 9.11% CAGR to 2031.

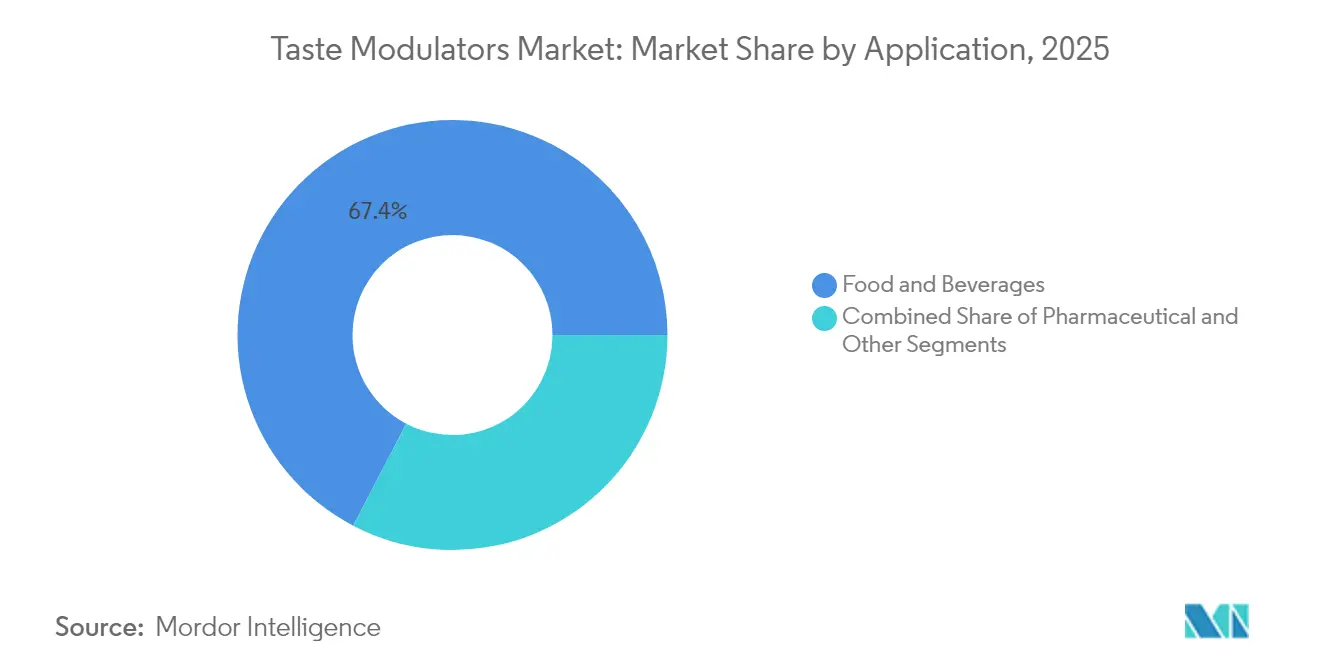

- By application, food and beverages generated a 67.35% share of the taste modulators market in 2025, yet pharmaceutical uses will post the quickest 9.02% CAGR over the period.

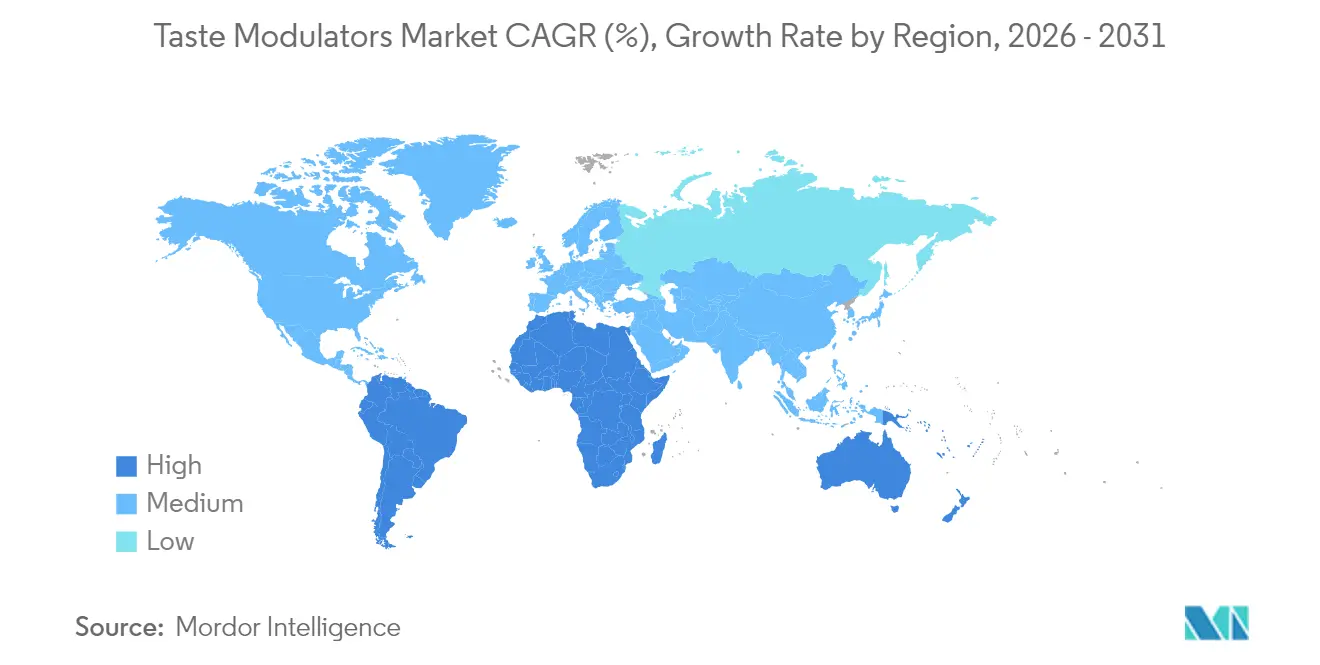

- By geography, Asia-Pacific commanded 34.52% share of the taste modulators market in 2025, and South America is poised for a 9.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Taste Modulators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for sugar-reduced and low-calorie products | +1.8% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Growing adoption in functional foods and sports nutrition | +1.2% | North America, Europe, Asia-Pacific urban centers | Long term (≥ 4 years) |

| Advancements in research and developments for natural taste modulators | +0.9% | Global, concentrated in innovation hubs | Long term (≥ 4 years) |

| Rising consumer preference for clean-label and healthier foods | +1.4% | North America, Europe, Australia | Medium term (2-4 years) |

| Expansion of personalized nutrition and functional ingredients | +0.7% | North America, select APAC markets | Long term (≥ 4 years) |

| Increasing use in plant-based and meat-alternative products | +1.1% | North America, Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Sugar-Reduced and Low-Calorie Products

Regulatory changes in nutritional definitions, including the FDA's updated "healthy" criteria, are requiring brands to reduce added sugars while maintaining product taste and texture [1]U.S. Food and Drug Administration, “Definition of ‘Healthy’ Claims for Food Labels,” fda.gov. The growing adoption of glucagon-like peptide-1 weight-loss medications is increasing consumer demand for low-calorie indulgent products. In response, manufacturers are adopting sugar modulators that can substitute up to 100% of sucrose while maintaining essential properties like browning, viscosity, and shelf life. Kerry's Tastesense product line demonstrates effectiveness across beverages, bakery items, and dairy products, enabling premium pricing strategies. In developed markets, where sugar taxes and front-of-pack warning labels drive product reformulation, consumers show increased willingness to pay more for healthier alternatives.

Growing Adoption in Functional Foods and Sports Nutrition

The expanding market for protein-rich beverages and bars faces significant taste challenges, as protein ingredients inherently create bitter and astringent flavors that deter consumer acceptance. Companies like Firmenich have developed advanced flavor modulation technologies that effectively mask these undesirable taste elements while maintaining the products' nutritional integrity and caloric content. The substantial increase in high-protein beverage launches this decade demonstrates both market demand and the critical need to address these sensory barriers. Innovation in personalized nutrition, led by companies such as Panaceutics, has enabled precise taste customization at the batch level by combining individual genetic profiles with sophisticated modular flavor systems. This technological advancement, coupled with the growing overlap between sports nutrition and mainstream wellness markets, sustains the continuous demand for versatile taste modulation solutions that enhance product palatability.

Advances in Research and Developments for Natural Taste Modulators

Research advances in plant-derived and fermentation-based compounds are transforming food ingredient development. Cyclodextrins, enzymatically produced compounds, effectively address two key challenges in meat alternatives: they capture unwanted flavor compounds and enhance moisture retention [2]PLoS ONE Editors, “Cyclodextrin Glucanotransferase Improves Flavor of Plant-Based Meats,” plos.org. These compounds maintain their stability during cooking processes and avoid classification as additives in numerous regulatory frameworks. The EU's approval of β-cyclodextrin (E 459) and its U.S. GRAS status marks a significant regulatory milestone, enabling broader commercial applications. Advanced extraction technologies have improved the bioavailability of steviol glycosides, while specialized fermentation processes now create targeted umami enhancers for plant protein applications.

Rising Consumer Preference for Clean-Label and Healthier Foods

Consumer demand for natural ingredients continues to rise, with shoppers examining ingredient lists and favoring brands that reduce synthetic components. The natural ingredients market growth is driven by transparency initiatives and environmental commitments. Natural raw materials present procurement challenges due to seasonal variations and quality fluctuations. In response, manufacturers invest in predictive agriculture and blockchain tracking systems to maintain consistent phytochemical profiles. Product success depends on matching synthetic formulation performance, with European consumers accepting minor taste variations while North American markets require identical taste profiles, compelling suppliers to enhance masking technologies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Challenges in developing effective taste modulators | -0.8% | Global, particularly in emerging markets | Medium term (2-4 years) |

| Regional variations in sensory preferences | -0.6% | Global, with highest impact in diverse markets | Long term (≥ 4 years) |

| Stringent regulatory approvals and labeling requirements | -1.1% | North America, Europe, Asia-Pacific developed markets | Short term (≤ 2 years) |

| Volatility in raw material supply for natural modulators | -0.9% | Global, concentrated in agricultural regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Challenges in Developing Effective Taste Modulators

The development of multi-functional taste modulators requires understanding complex receptor interactions across sweet, salty, bitter, and umami pathways. In pharmaceutical applications, bitter-tasting active ingredients continue to affect patient compliance, especially among children, requiring comprehensive taste-masking and delivery solutions. While electronic tongue technology enhances measurement capabilities, it cannot accurately predict cultural taste preferences, which extends research and development timelines. The high costs of establishing pilot sensory laboratories create barriers for small companies, giving established firms with global research facilities and trained sensory panels a competitive advantage.

Stringent Regulatory Approvals and Labeling Requirements

Regulatory bodies require extensive safety documentation. The FDA's draft rule on GRAS notifications requires companies to submit public safety data, limiting previous self-affirmation pathways. In the European Union, Regulation (EC) No 1333/2008 requires proof of technological necessity for new additives, while China's GB 2760-2024 enforces a positive list system, extending the time-to-market. Natural compounds with multiple bioactive components present challenges in toxicological assessment and labeling. These regulatory timelines can impact product launch schedules, making early regulatory consultation and alignment of cross-regional documentation essential [3]European Commission, “Regulation (EC) No 1333/2008 on Food Additives,” eur-lex.europa.eu.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Expanding Beyond Sweetness

Sweet modulators dominated the taste modulators market with a 46.62% share in 2025, as food manufacturers increasingly adopted sugar-reformulation initiatives to meet consumer demand for healthier products. The salt modulator segment is experiencing rapid growth at a 9.32% CAGR through 2031, driven by WHO guidelines limiting daily sodium intake to 2,000 mg and rising consumer awareness about the health risks associated with high salt consumption . The taste modulators market for salt solutions is expected to grow significantly as food processors in snacks, soups, and ready meals aim to reduce sodium content while maintaining flavor profiles.

Fat replacers and umami enhancers contribute to market growth through complementary functions. Bitter blockers are essential in functional beverages and pediatric medications, using encapsulation and receptor-antagonist technologies to neutralize bitter compounds. The approval of Advantame for both sweetening and flavor enhancement demonstrates regulatory acceptance of ingredients with multiple functions. The ongoing diversification within ingredient categories requires suppliers to maintain comprehensive portfolios covering sugar, salt, and bitter taste modification.

By Source: Natural Ascendancy with Supply Vigilance

Natural sources accounted for 56.21% share of the taste modulators market in 2025 and are expected to grow at a CAGR of 9.78% through 2031. Stevia varieties grown in Mediterranean regions demonstrate variations in genetic composition and harvest timing that affect steviol glycoside production. The market size for natural taste modulators depends on agricultural consistency and extraction efficiency at scale.

Synthetic modulators continue to play an essential role where predictable costs and consistent functionality are prioritized over clean-label requirements. The FDA evaluated 57 GRAS notifications in 2024, including D-psicose and the sweet protein brazzein, demonstrating continued synthetic development. Combined solutions that integrate natural flavoring compounds with synthetic carriers offer potential for balancing sensory effectiveness and label transparency.

By Application: Food and Beverage Core, Pharma Rising

Food and beverages accounted for 67.35% of the market share in 2025. In this segment, manufacturers of non-alcoholic beverages utilize high-intensity sweetener modulators to optimize acid-sugar ratios, while dairy producers implement modulators to reduce whey protein bitterness without increasing lactose content.

The pharmaceutical segment is experiencing the highest growth rate at 9.02% CAGR, driven by the importance of taste in medication adherence. Manufacturers incorporate modulators through hot-melt extrusion in pediatric acetaminophen suspensions to improve taste. In the nutraceutical segment, vitamin gummies combine fruit-flavored modulators to eliminate metallic aftertastes. The strong presence in both sectors provides market stability against volume fluctuations in individual segments.

By Form: Powder Dominance Meets Liquid Momentum

Powder formulations accounted for 65.79% market share in 2025 due to their ease of dispersion in dry mixes and efficient logistics. This format enables microencapsulation technology that protects volatile compounds and provides controlled release properties. The powder segment maintains steady growth in bakery, confectionery, and instant beverage applications.

The liquid segment is expected to grow at a 9.11% CAGR, driven by beverage innovations and syrup systems for coffee chains and quick-service restaurants. Liquid cyclodextrin complexes improve solubility and immediate mouthfeel in low-alcohol cocktails, while pharmaceutical syrups benefit from precise dosing capabilities. Manufacturers are investing in dual-form production lines, enabling customers to alternate between spray-dried powders and liquid concentrates without requiring reformulation.

Geography Analysis

Asia-Pacific holds a 34.52% market share in the global taste modulators market. China's updated regulation GB 2760-2024 specifies permitted taste-enhancing additives, requiring local manufacturers to implement advanced modulators for regulatory compliance while meeting the demands of the expanding middle class. Japan maintains a structured list of approved additives, providing a clear framework for new modulator introductions. The market growth in India, Indonesia, and Vietnam is driven by increasing disposable incomes and health consciousness, although regional taste preferences necessitate specific flavor-masking solutions.

South America demonstrates the highest growth rate at 9.24% CAGR, driven by functional beverages that combine regional botanicals with taste modulators aligned to local preferences. Givaudan's South American operations growth in 2024, indicating significant market potential in Brazil and Colombia.

North America maintains a developed market where FDA sodium reduction guidelines encourage food manufacturers to implement salt-blocking modulators. Beverage manufacturers utilize natural sweetness modulators to reduce high-fructose corn syrup usage, while the sports nutrition segment implements bitterness blockers to support plant protein product development. Market growth continues as manufacturers respond to sugar taxation and mandatory added-sugar disclosure requirements.The European market exhibits stable growth, governed by EFSA regulations and consumer preference for natural ingredients. European manufacturers focus on modulators with established sustainability practices, particularly favoring fermentation-based umami enhancers.

Competitive Landscape

The taste modulators market demonstrates moderate consolidation, with industry leaders Givaudan, IFF, and Kerry Group leveraging extensive proprietary sensory databases and global application laboratories. These capabilities enable them to develop customized solutions through collaborative innovation with customers, addressing specific taste challenges across food and beverage applications.

Mid-sized specialized companies drive technological advancement in targeted segments. Firmenich advances the development of receptor-targeted bitter blockers through molecular research, while Sensient capitalizes on its advanced botanical extraction expertise to produce natural taste modulators that meet clean-label demands. Large ingredient manufacturers Cargill and ADM utilize their robust integrated supply chains to maintain consistent supply of critical raw materials like stevia and monk-fruit, effectively managing agricultural volatility and ensuring supply security.

Research and development investments prioritize artificial intelligence-assisted formulation systems that analyze and predict complex flavor interactions, significantly reducing product development cycles. Strategic collaborations with biotechnology companies accelerate the development of fermentation-based taste modulators, particularly for replicating authentic animal-protein flavors in plant-based alternatives. The competitive landscape effectively balances operational scale advantages with rapid innovation capabilities, creating opportunities for new market entrants to solve specific sensory challenges through targeted technological solutions.

Taste Modulators Industry Leaders

Cargill Inc.

DSM-Firmenich

International Flavors and Fragrances Inc.

Archer Daniels Midland Company

Kerry Group plc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: DSM-Firmenich introduced pharmaceutical taste solutions that combine flavors, taste maskers, and sensory enhancers to improve drug palatability, enabling pharmaceutical companies to develop more patient-friendly medications and accelerate their market entry.

- January 2025: MANE introduced the "SENSE CAPTURE" Precision Taste Modulation program, which addresses taste dimensions in complex food and beverage products. The program enhances desired taste perceptions while reducing unwanted taste elements.

- July 2024: HealthTech Bio Actives (HTBA) introduced a high-purity natural sweetness modifier at the IFT FIRST annual meeting in Chicago. The company states that this modifier can help manufacturers address taste challenges while meeting consumer demand for healthy products with improved taste profiles.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global taste modulators market as the sale value of ingredients purposely engineered to enhance or suppress sweetness, saltiness, bitterness, fat sensation, or umami without adding meaningful calories or sodium to finished food, beverage, and pharmaceutical products.

Scope Exclusion: Bulk nutritive sweeteners, generic flavor enhancers that do not work via receptor-level modulation, and table-top sweetener sachets are kept outside the valuation.

Segmentation Overview

- By Type

- Sweet Modulators

- Salt Modulators

- Fat Modulators

- Umami Enhancers

- Bitter Blockers

- By Source

- Natural

- Synthetic

- By Form

- Powder

- Liquid

- By Application

- Food and Beverages

- Bakery and Confectionery

- Dairy Products

- Snacks and Savory

- Meat and Poultry

- Beverages

- Other Food Products

- Pharmaceutical

- Other Applications

- Food and Beverages

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- United Kingdom

- Germany

- Spain

- France

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed food scientists at flavor houses, procurement heads at regional snack manufacturers, and regulatory consultants across North America, Europe, and Asia-Pacific. These conversations validated usage rates in zero-sugar beverages, clarified pricing spreads between natural and synthetic modulators, and flagged upcoming WHO sodium-reduction timelines that could shift demand.

Desk Research

We began with structured reviews of open datasets issued by bodies such as the US FDA, WHO nutrition databases, Eurostat trade panels, and the UN Comtrade shipment logs, which reveal flows of high-intensity sweeteners and specialty flavor chemicals. Industry associations, including the International Food Additives Council and the American Beverage Association, offered adoption statistics and reformulation counts, while public company 10-Ks and investor decks provided average selling price clues. Paid resources from D&B Hoovers and Dow Jones Factiva helped us cross-check revenue splits. This list is illustrative; many additional public and paywalled sources informed gap filling and sense checking.

Market-Sizing & Forecasting

A top-down "production-and-trade reconstruct" of specialty sweetener and flavor precursor volumes established the initial demand pool, which is then corroborated with selective bottom-up supplier roll-ups and channel checks. Core model drivers include per-capita sugar intake trends, the share of low- or no-sugar product launches captured via Mintel GNPD, WHO regional sodium targets, average selling prices by modulator type, and new beverage capacity additions. Multivariate regression links these variables to historical revenue, enabling five-year forecasts under a baseline scenario reviewed by interviewed experts. Gaps in bottom-up data, for instance, private-label volumes, are bridged by applying validated penetration ratios from analogous categories.

Data Validation & Update Cycle

Outputs pass a multi-layer review where analysts compare totals against independent trade values, flag anomalies above ±5%, and rerun queries in paid databases if needed. Reports refresh annually, while material events such as new sodium legislation trigger interim updates before client delivery.

Why Mordor's Taste Modulators Baseline Inspires Confidence

Published figures often diverge because firms pick different inclusion rules, price assumptions, and update cadences.

Key gap drivers revolve around whether fat modulators are counted, the handling of pharmaceutical demand, and how average selling prices adjust for the rapid shift toward natural extracts. Mordor's clearly documented scope, annual refresh, and dual check of trade flows and supplier revenues mitigate these variances.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.67 B (2025) | Mordor Intelligence | - |

| USD 1.56 B (2024) | Global Consultancy A | Excludes pharmaceutical uptake and uses uniform ASP across regions |

| USD 1.80 B (2025) | Industry Data Service B | Counts bulk flavor enhancers alongside modulators, inflating base |

| USD 2.06 B (2024) | Trade Journal C | Applies forecast-year exchange rates retroactively and omits natural vs synthetic split |

In summary, the disciplined variable selection, transparent gap handling, and yearly validation loop mean Mordor's numbers give decision-makers a balanced, reproducible baseline they can rely on when sizing opportunities or benchmarking performance.

Key Questions Answered in the Report

What is the current size of the taste modulators market?

The taste modulators market is valued at USD 1.8 billion in 2026 and is projected to hit USD 2.6 billion by 2031.

Which region holds the largest share of the taste modulators market?

Asia-Pacific leads with 34.52% share due to stringent Chinese and Japanese additive standards and growing middle-class demand.

Which application segment is growing the fastest?

Pharmaceutical taste masking is forecast to grow at 9.02% CAGR between 2026-2031 as patient adherence becomes a top priority.

What role do natural ingredients play in this market?

Natural sources account for 56.21% share and are expanding at 9.78% CAGR, but they require resilient supply chains to handle crop variability and traceability demands.

Page last updated on: