Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

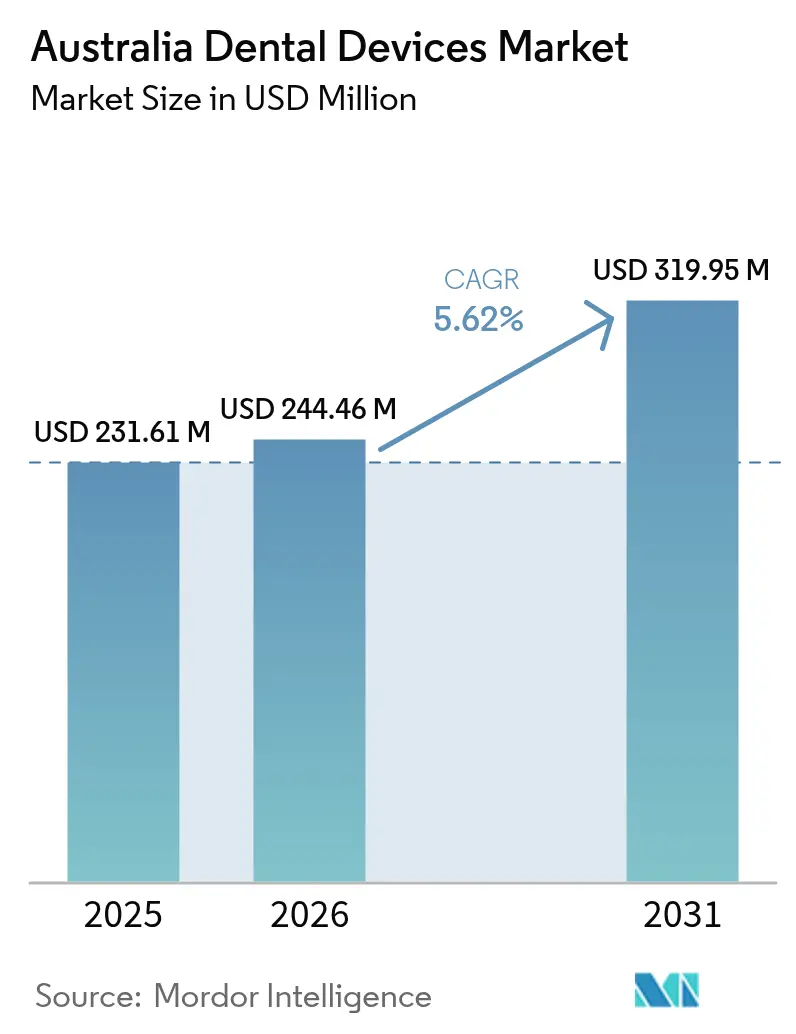

| Base Year Market Size (2025) | USD 231.61 Million |

| Market Size (2026) | USD 244.46 Million |

| Market Size (2031) | USD 319.95 Million |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

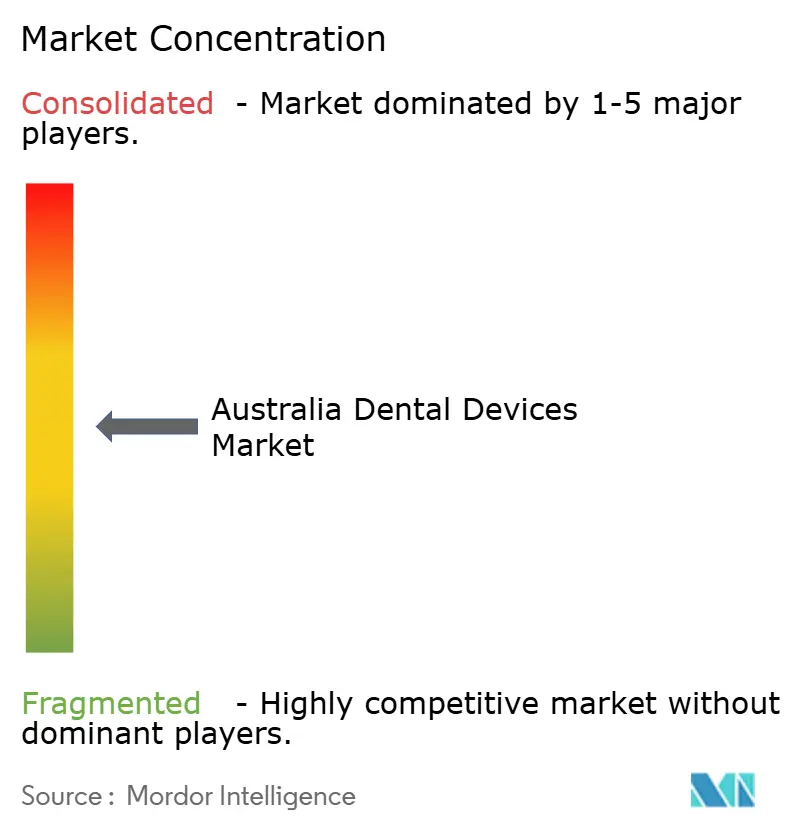

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Dental Devices Market Analysis by Mordor Intelligence

The Australia Dental Devices Market size was valued at USD 231.61 million in 2025 and is estimated to grow from USD 244.46 million in 2026 to reach USD 319.95 million by 2031, at a CAGR of 5.62% during the forecast period (2026-2031).

Private health insurance coverage of 43.6% in 2024 continues to underpin high-value restorative and orthodontic volumes, while the Child Dental Benefits Schedule cap of AUD 1,132 (USD 733) strengthens demand for routine consumables. Clear-aligner launches by Align Technology and Straumann are intensifying competition in premium orthodontics, and corporate consolidation among clinic chains is accelerating the uptake of CAD/CAM and 3D-printing workflows. Federal grants worth AUD 323.4 million (USD 210 million) between 2023-2026 are underwriting hospital purchases of CBCT scanners, digital radiography units, and bulk sterilizers. At the same time, circular-economy rules adopted in 2024 are nudging manufacturers toward modular, repairable product designs that lower waste and align with national advanced-manufacturing priorities.

Key Report Takeaways

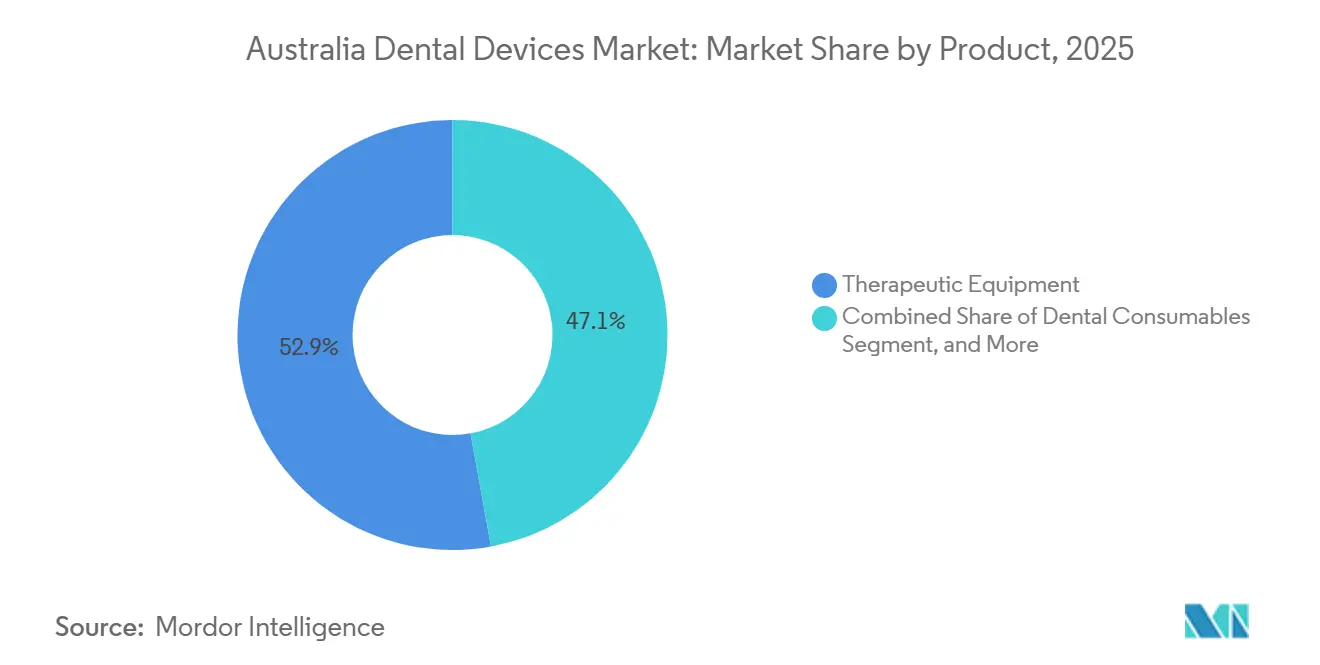

- By product category, therapeutic equipment led the Australian dental devices market with 52.88% market share in 2025, while dental consumables are advancing at a 6.29% CAGR through 2031.

- By treatment, prosthodontics accounted for 38.09% of the Australian dental devices market size in 2025, and orthodontics is expanding at a 7.99% CAGR to 2031.

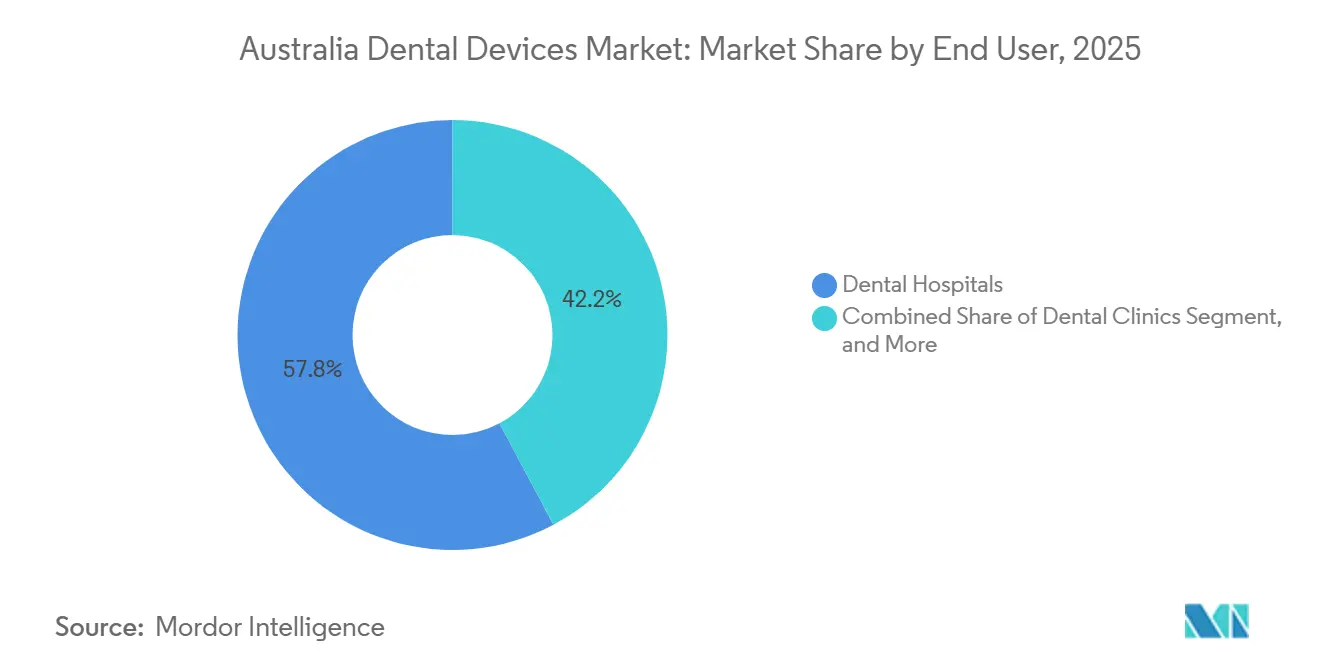

- By end user, dental hospitals accounted for 57.78% of revenue in 2025, and dental clinics are projected to grow at a 9.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Dental Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapidly Ageing Population Boosting Prosthetic & Implant Demand | +1.2% | National, concentrated in NSW, Victoria, Queensland | Long term (≥ 4 years) |

| Expansion of Commonwealth & Private-Insurance Dental Coverage | +0.9% | National, with stronger uptake in metropolitan areas | Medium term (2-4 years) |

| Accelerated Adoption of Digital Dentistry (CAD/CAM, 3-D Printing) | +1.5% | National, early gains in corporate clinic chains and university teaching hospitals | Medium term (2-4 years) |

| High Prevalence of Untreated Dental Caries Necessitating Restorative Devices | +0.8% | National, elevated in remote and socioeconomically disadvantaged communities | Short term (≤ 2 years) |

| Emergence of Zirconia-Based Chairside Milling Materials | +0.6% | National, concentrated in practices with existing CAD/CAM infrastructure | Medium term (2-4 years) |

| Circular-Economy Regulations Spurring Low-Waste Device Designs | +0.3% | National, with pilot programs in Victoria and NSW | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapidly Ageing Population Boosting Prosthetic & Implant Demand

One in four Australians will be 65 or older by 2031, and the cohort averages 13.7 missing teeth.[1]Australian Institute of Health and Welfare, “Dental workforce 2023,” AIHW.GOV.AU This reality is fuelling purchases of chairside milling units, zirconia blocks, and titanium implants that shorten treatment cycles for fixed and removable prosthetics. A 2020 practitioner survey found that 65.5% already perform implant dentistry and 59% routinely use CBCT for planning; trends now transferring from specialists to general practices. Suppliers such as Straumann and Nobel Biocare dominate guided-surgery kits, while ISO 13356 conformity testing reassures clinicians about longevity for older patients. As digital workflows compress appointment schedules, practices can command premium pricing that offsets equipment depreciation.

Expansion of Commonwealth & Private-Insurance Dental Coverage

Federal transfers of AUD 323.4 million (USD 210 million) through 2026 are benchmarked to Dental Weighted Activity Units, rewarding throughput in public hospitals and clinics. Private health-fund members spent USD 1.6 billion on dental care in 2023 and are twice as likely to request elective prosthodontic and orthodontic services.[2]Australian Bureau of Statistics, “Patient Experiences 2024-25,” ABS.GOV.AU The Parliamentary Budget Office valued full Medicare inclusion of dental at USD 29.5 billion over the forward estimates, illustrating latent demand. Any incremental broadening of eligibility will cascade into higher consumables turnover and larger installed bases of diagnostic imaging and sterilization equipment across both sectors.

Accelerated Adoption of Digital Dentistry

Chairside systems that combine intraoral scanning, CAD software, and 3D printers are moving from early adopters to the mainstream. Planmeca’s Emerald S scanner, Creo C5 mill, and Viso G7 CBCT debuted in 2024, while Carestream released the CS 3800 wireless scanner the same year.[3]Planmeca, “Product launches 2024,” PLANMECA.COM Capital expenditure remains steep, CBCT units list at USD 52,000-97,000, but equipment leasing at 5-10% interest spreads costs over 7 years. Recent state regulatory updates add CBCT to standard radiation licences, trimming approval delays in Queensland and encouraging wider uptake. Digital accuracy reduces remake rates, further improving return on investment.

High Prevalence of Untreated Dental Caries

Forty-two percent of 5-10-year-olds have decay in primary teeth, and 25% of adults carry untreated caries. National clinical guidelines published in 2024 endorse annual checks for Indigenous children and fluoride varnish every six months for high-risk groups. These protocols translate into steady volume demand for restorative materials, burs, and endodontic files. Manufacturers such as GC Corporation introduced G-aenial A'CHORD composites and Fuji PLUS glass-ionomer to balance durability with affordability in high-throughput community clinics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Advanced Equipment for Smaller Clinics | -0.7% | National, most acute in regional and rural practices | Short term (≤ 2 years) |

| Shortage of Trained Dental Technologists in Regional Areas | -0.5% | Regional and remote areas, particularly Northern Territory, Tasmania, and inland Queensland | Medium term (2-4 years) |

| Stringent TGA Registration & Post-Market Vigilance | -0.3% | National | Medium term (2-4 years) |

| Import-Dependent Supply Chains Vulnerable to Asia-Pacific Shocks | -0.4% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Advanced Equipment for Smaller Clinics

A full practice fit-out ranges from AUD 250,000 to AUD 500,000 (USD 162,000-324,000), with single CBCT scanners priced at USD 52,000-97,000. For solo practitioners, this equals 12-18 months of net profit, delaying the switch to digital impressions and in-house milling. Although leasing eases cash flow, rising equipment price lists Dentsply Sirona announced increases effective January 2026, which threaten operating margins for small practices.

Shortage of Trained Dental Technologists in Regional Areas

Only about 2,000 dental technicians serve the entire country, and the pipeline of graduates is thin. Regional practices face 2-3-week laboratory queues, prompting some to ship cases offshore or invest in chairside mills. Government service plans acknowledge the gap yet omit firm recruitment targets, leaving rural clinics dependent on interim solutions that stretch treatment times and patient satisfaction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Therapeutic Equipment Retains the Largest Slice While Consumables Gather Pace

Therapeutic equipment accounted for 52.88% of 2025 revenue, anchored by handpieces, lasers, and ultrasonic scalers, which are found in every general or periodontal operatory. The Australia dental devices market size attributed to this segment benefited from NSK’s Ti-Max Z95L launch in 2024 and BIOLASE’s Waterlase iPlus gains among minimally invasive dentists. Continuous improvements in tip ergonomics and torque delivery justify seven-year replacement cycles.

Dental consumables are on track for a 6.29% CAGR through 2031, outpacing growth in the total Australian dental devices market as infection-control standards such as AS 5369:2023 make single-use items more attractive in busy clinics. Gloves, suction tips, and matrix bands now represent a predictable recurring revenue stream for distributors that bundle them with autoclave service contracts.

Diagnostic equipment ranks second in value, driven by CBCT upgrades and the shift from film to digital sensors. Planmeca’s Viso G7 multi-FOV unit, released in 2024, enables practices to combine orthodontic planning with implant assessment in a single scan session. Other equipment, such as compressors and autoclaves, shows slower turnover but remains indispensable; Henry Schein’s 2024 partnership with MELAG brought a new sterilizer line to market, giving hospital buyers local service coverage.

By Treatment: Prosthodontics Dominates Revenue, Orthodontics Leads Growth

Prosthodontics accounted for 38.09% of Australia's dental device market share in 2025 as ageing patients seek implant-borne and full-arch solutions. OSSIX Volumax collagen membranes, cleared in December 2025, support ridge augmentation, enabling predictable implant placement in older jaws with reduced bone volume. High-cost biomaterials and precision titanium parts keep average procedure values elevated. Orthodontics is forecast to grow at a 7.99% CAGR, the quickest of all treatment lines. Align Technology’s palatal expander and Straumann’s Low Trimline aligners broaden clear-aligner indications to early interceptive care and adult relapse cases. AI-supported image-analysis platforms such as EM2AI, adopted by 1,100 clinics, streamline case selection and progress reviews, shortening chair time and enhancing throughput.

Endodontic cases rely on nickel-titanium rotary systems and apex locators that shorten shaping time, while periodontic and preventive procedures use ultrasonic scalers and diode lasers. Both segments exhibit steady but slower expansion, reflecting stable disease prevalence and periodic equipment refreshes.

By End User: Hospitals Still Rule Purchases, Clinics Turbo-charge Growth

Public dental hospitals accounted for 57.78% of 2025 spending, buoyed by federal block grants tied to activity units that mandate high-throughput care. Procurement committees favor robust, compliance-ready devices bundled with multi-year service guarantees, making vendors’ local after-sales capacity a key tender criterion.

Dental clinics will expand at a 9.35% CAGR to 2031, outstripping the broader Australian dental devices market. Pacific Smiles’ takeover of National Dental Care and Genesis Capital’s 2025 bid created scale economies, resulting in a 136-site network with centralized purchasing and negotiating power. Chains standardize equipment lists—often scanner-mill bundles to simplify staff training and maintenance, driving bulk orders that lift distributor volumes.

Academic institutes purchase smaller quantities but influence the preferences of graduating dentists, indirectly shaping future demand. Mobile services and aged-care providers round out the market, demanding portable X-ray units and simple sterilization solutions for on-site care.

Geography Analysis

New South Wales, Victoria, and Queensland concentrate most practitioners and therefore dominate Australia dental devices market revenue. NSW alone drew AUD 34.37 million (USD 22.3 million) in federal adult-dental funding for 2023-2025, underwriting major imaging upgrades in metro hospitals. Victoria and Queensland followed with AUD 26.88 million and AUD 21.66 million, respectively, mirroring population share. Queensland’s 2025 radiation-licence reform specifically included CBCT in the standard schedule, making adoption paperwork easier and signalling likely double-digit scanner growth over the next three years.

Western Australia, South Australia, and Tasmania remain smaller but strategically important owing to remote mining and island populations that require fly-in services. Federal allocations of USD 9-6 million per state support basic diagnostic and restorative devices in public clinics. Suppliers that offer ruggedized portable chairs and battery-operated X-ray generators capture these tenders.

The Northern Territory and the Australian Capital Territory represent the smallest slices of Australia dental devices market size yet embody policy priority for Aboriginal and Torres Strait Islander oral health. Annual fluoride-varnish guidelines and planned teledentistry pilots will drive purchases of varnish kits, intraoral cameras, and tele-consultation stations. The National Oral Health Plan 2025-2034, finalized after 235 stakeholder submissions, emphasizes equity and prevention, and suggests funding streams for preventive device categories beginning in 2027.

Regulatory Landscape

Dental devices in Australia are regulated by the Therapeutic Goods Administration (TGA) under the Therapeutic Goods Act 1989 and the Therapeutic Goods (Medical Devices) Regulations 2002. Most dental devices must be included on the Australian Register of Therapeutic Goods (ARTG) unless exempt or excluded, and manufacturers and sponsors are required to demonstrate compliance with the TGA Essential Principles for safety and performance (including maintaining scientific, clinical, and engineering evidence), alongside post-market vigilance obligations.

Regulatory updates affecting the dental pipeline include changes around personalised medical devices, where patient-matched devices continue to use transition arrangements with an ARTG inclusion endpoint of 1 July 2029. This shapes compliance planning for dental laboratories and in-clinic manufacturing. Mandatory Unique Device Identification (UDI) requirements commence on 1 July 2026, adding labeling and data-management work for suppliers across diagnostics, therapeutic equipment, and consumables. The Therapeutic Goods (Medical Devices, Specified Articles) Amendment Instrument 2025 took effect from 1 January 2026, clarifying which borderline products are regulated as medical devices and tightening ARTG expectations for specified articles used in dental practice.

Competitive Landscape

Global majors Dentsply Sirona, Align Technology, Straumann, 3M, Henry Schein, Planmeca, Ivoclar Vivadent, GC Corporation, NSK, and Carestream vie for position in a moderately fragmented Australia dental devices market. Imports supply 98% of the value, with the United States, Germany, Thailand, Switzerland, and Ireland accounting for 62% of inbound shipments. Vendors pursue ecosystem lock-in by pairing scanners, mills, and proprietary materials exemplified by Dentsply Sirona’s Primescan-CEREC chain and Straumann’s SIRIOS X3-ClearCorrect suite.

Technology releases remain the primary battleground. Carestream’s CS 3800 offers real-time feedback, while Ivoclar’s ZirCAD Prime balances translucency and strength, each commanding price premiums. AI tools such as EM2AI reduce diagnostic variability, creating another moat for early adopters. Regulatory conformity to ISO 13356 aging protocols, AS 5369:2023 reprocessing, and TGA post-market vigilance is a threshold rather than a differentiator; however, alignment with 2024 circular-economy policies gives first movers an edge in public tenders.

Niche innovators also shape the field. Keystone Dental’s 2025 acquisition of Osteon Medical imported digital implant expertise from Melbourne into a global portfolio, and Orthocell’s Striate Plus licensing deal validated home-grown regenerative devices. STERIS’s USD 787.5 million dental-segment divestiture in 2024 freed rivals to capture autoclave share. Consolidating clinic chains magnify purchaser clout, pressuring unit prices yet guaranteeing volume for vendors that meet service-level agreements.

Australia Dental Devices Industry Leaders

Carestream Health Inc.

Dentsply Sirona

Envista Holdings Corporation

GC Corporation

3M

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Digital dentistry and connected-care enablement remains an area where suppliers can differentiate, supported by national digital-health programs and professional guidance on clinical informatics and AI use. The Australian Digital Health Agency National Digital Health Strategy 2023-2028 and the Australian Government Digital Health Blueprint and Action Plan 2023-2033 emphasize interoperability, virtual care, and data use, creating room for vendors that can integrate intraoral scanning, imaging, CAD/CAM, and practice software into auditable workflows that fit broader health-system data requirements. The Australian Dental Association policy positions on Dental Informatics and Digital Health, and Artificial Intelligence in Dentistry, further reinforce the shift toward interoperable devices and responsible AI in patient care.

Compliance requirements also create opportunities in personalised and patient-matched device manufacturing and distribution. TGA requirements for practitioners who make or adapt personalised medical devices, together with the transition period ending on 1 July 2029, support demand for compliant production workflows, documentation, and quality systems that can be adopted by dental labs, corporate clinic chains, and teaching hospitals. Distributors and service providers with local footprints, including Henry Schein Australia and Dentsply Sirona Australia, as well as equipment infrastructure specialists such as Cattani Australasia, can expand value-added offerings around installation, maintenance, digital integration, and compliance support, instead of competing only on unit pricing.

Recent Industry Developments

- July 2026: Dentsply Sirona announced the integration of the VDW brand into its Endodontics portfolio. The consolidation clarifies endodontic positioning and simplifies portfolio navigation for dental practices and distributors. It strengthens the company’s chairside workflow offering in a category with recurring consumable pull-through.

- July 2025: Griffith University introduced Nuralyte, a light-therapy device designed to accelerate healing after oral procedures by enhancing mitochondrial respiration and gene expression in bone-forming stem cells. The development points to active R&D and commercialization pathways in regenerative dentistry. It supports demand for adjunctive therapeutic devices in clinics and academic settings.

- September 2024: The TGA permitted sponsors to rely on conformity assessments from comparable overseas regulators to support Australian approvals for eligible medical devices. This change reduces duplicative assessment burden for multinational dental-device suppliers. It can shorten time-to-market for eligible innovative diagnostic and restorative systems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the annual value of dental devices sold and used in Australia for diagnosis, treatment, restoration, and routine oral care in professional settings, including capital equipment and regularly purchased dental consumables.

Scope exclusions: Over-the-counter oral care products bought directly by consumers are excluded from this market sizing.

Segmentation Overview

- By Product

- Diagnostics Equipment

- Dental Laser

- Radiology Equipment

- Dental Chair & Equipment

- Therapeutic Equipment

- Dental Consumables

- Other Dental Equipments

- Diagnostics Equipment

- By Treatment

- Orthodontic

- Endodontic

- Periodontic

- Prosthodontic

- By End User

- Dental Hospitals

- Dental Clinics

- Academic & Research Institutes

- Other End Users

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the factual base for the model, and then to cross-check whether the final outputs make sense for Australia. We relied on public sources such as the Australian Institute of Health and Welfare for health system context, the Australian Bureau of Statistics for population and income indicators, and the Department of Health and Aged Care for policy signals that can affect dental utilization.

To anchor trade and supply-side movement, we also reviewed customs and trade statistics and product classification notes from sources such as the Australian Border Force, along with reference material from dental and medical device associations and peer-reviewed dentistry journals for technology adoption and procedure trends. Company annual reports, investor presentations, and credible press were used to confirm product focus and timing of launches, and a paid subscription covering company financials and a patent database were used selectively to fill gaps on smaller entities and to understand innovation intensity. The sources listed are illustrative, and many other public references were also reviewed for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary interviews and surveys were run with a mix of manufacturers, distributors, dental clinic operators, lab decision-makers, and procurement stakeholders to stress-test demand drivers and pricing logic for Australia. Inputs were used to confirm what gets counted as dental devices versus consumer oral care, and to validate adoption of imaging, CAD/CAM workflows, implants, and recurring consumable purchasing across major states and metro and non-metro catchments.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 17% | |

| Mid tier: 41% | Functional/Unit leaders: 25% | |

| Smaller Players: 21% | Managers: 58% |

Market-Sizing & Forecasting

Sizing starts with a top-down reconstruction of the addressable dental care activity in Australia, and then it is translated into device and consumable demand through penetration and usage rates. For this, we connected indicators such as dentist and clinic density, procedure mix (for example, restorative and prosthodontic intensity), implant and orthodontic case volumes, and replacement cycles for chairside equipment and imaging systems.

After the demand pool is formed, average selling prices are applied using a blended approach that reflects procurement channel mix and typical price bands discussed in interviews. The totals are then corroborated with selective bottom-up approximations, including a roll-up of sampled supplier revenues in Australia and distributor channel checks for high-value categories, which helps adjust for under-reporting in fragmented segments. Where direct inputs were missing, gaps were handled by using adjacent-category ratios (such as consumables-to-equipment spending patterns) and then re-checked with practitioners and trade participants.

Forecasting was built using scenario analysis supported by an ARIMA trend line on the historical series, and key assumptions were tuned based on expert views on equipment replacement timing, technology upgrades (digital imaging and CAD/CAM), and changes in patient affordability and clinic throughput.

Data Validation & Update Cycle

Validation is done through several passes so the final number is not dependent on one data stream. We compare model outputs against independent signals such as dental service utilization trends, import patterns for relevant device classes, and the implied spend per active dental chair, and then any variance is investigated before sign-off.

Outliers are flagged when growth rates, implied prices, or category shares move beyond what interviews and public signals support, and analysts re-contact sources when a correction would change the total market meaningfully. Reports are refreshed annually, and interim updates are made when material events occur, such as regulatory changes, major reimbursement shifts, or step-changes in equipment adoption. Before delivery, a final review pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Australia Dental Devices Market Size Compared Against Other Published Estimates

Published market values for Australia dental devices can look far apart because each publisher draws the line around different product baskets and buying channels, and then applies different pricing and timing assumptions. Differences also come from the base year chosen, the exchange rate timing for imported equipment, and how fast adoption of digital workflows is assumed to move.

Some external estimates fold in a wider dental supplies universe and sometimes include consumer oral care or broader medical consumables in the same bucket. In Mordor Intelligence, the total is limited to professional dental equipment plus dental consumables purchased by clinics, hospitals, and academic settings, and it excludes over-the-counter oral care sold to consumers.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 231.61 M (2025) | |

| Global Data Book A | USD 135.30 M (2023) | This figure is limited to dental equipment categories and excludes dental consumables, which pushes the total lower even before considering different base-year timing. |

| Regional Research Publisher B | USD 1.50 B (2023) | The scope appears broader and includes dental materials in a way that can overlap with wider dental supplies, and the higher total is also influenced by an earlier base year and more aggressive growth assumptions. |

The spread in the table is mainly explained by scope and counting rules, not by a simple disagreement on growth. By keeping inclusions tied to professional purchasing and then checking the result against procedure activity, replacement cycles, and price bands discussed in interviews, the estimate stays traceable to clear inputs that can be re-tested each year.

Key Questions Answered in the Report

What is the forecast dollar value of Australia’s dental-device demand by 2031?

The Australia dental devices market is projected to reach USD 0.32 billion by 2031.

Which treatment category is expanding fastest?

Orthodontics is growing at a 7.99% CAGR on the back of clear-aligner uptake.

Why are clinic chains investing heavily in CAD/CAM?

Consolidated groups spread equipment cost across many chairs, cut lab fees, and speed same-day restorations.

How do circular-economy rules affect device procurement?

Public buyers now factor modular, repairable designs into tenders, favoring suppliers with take-back or recycling programs.

Which three states dominate public-sector purchasing?

New South Wales, Victoria, and Queensland receive the largest federal dental-funding allocations.

Page last updated on: