Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

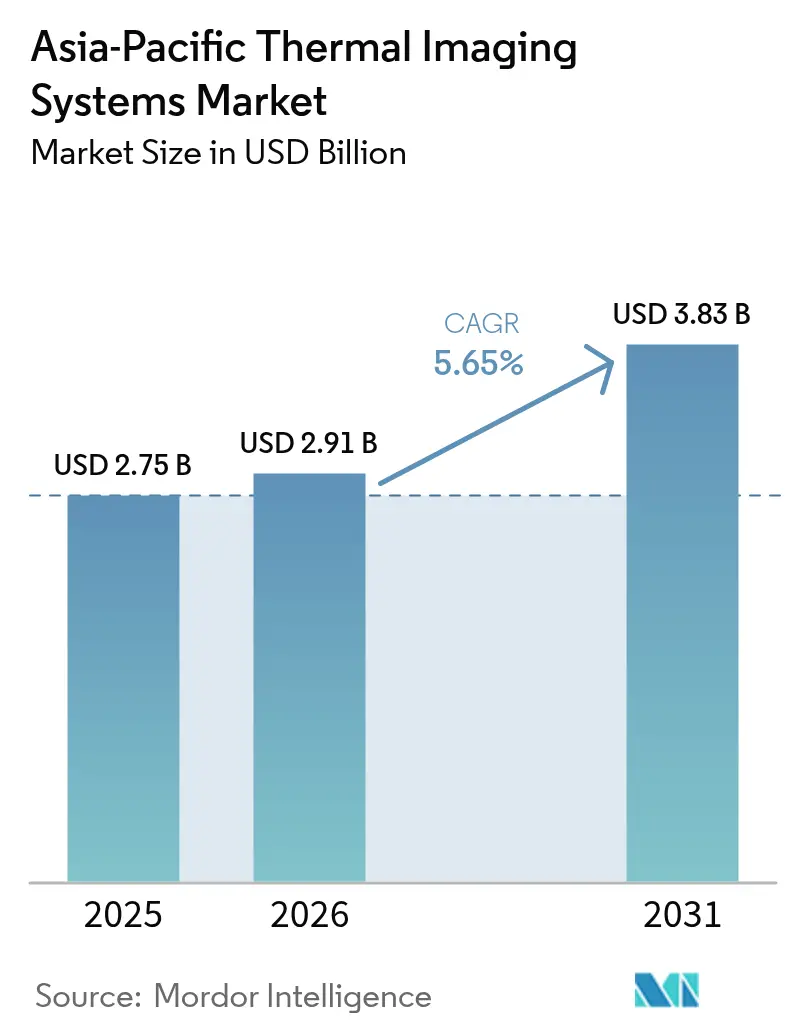

| Base Year Market Size (2025) | USD 2.75 Billion |

| Market Size (2026) | USD 2.91 Billion |

| Market Size (2031) | USD 3.83 Billion |

| Growth Rate (2026 - 2031) | 5.65% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Thermal Imaging Systems Market Analysis by Mordor Intelligence

The Asia-Pacific thermal imaging systems market size was valued at USD 2.75 billion in 2025, rose to USD 2.91 billion in 2026, and is forecast to reach USD 3.83 billion by 2031, registering a 5.65% CAGR from 2026 to 2031. A broadening customer mix is moving demand beyond defense-only procurement toward automotive advanced driver-assistance, industrial predictive maintenance, and livestock bio-security mandates. Automotive manufacturers now specify thermal modules for night-time pedestrian detection, while factories embed uncooled sensors in condition-monitoring networks to prevent costly outages. Chinese suppliers leverage vertically integrated fabs to cut detector prices, giving the Asia-Pacific thermal imaging systems market a cost advantage even as Western incumbents focus on premium cooled arrays. Governments continue to fund border-surveillance programs, but commercial adoption now shapes the competitive dialogue and opens white-space opportunities in veterinary health and smart-city infrastructure.

Key Report Takeaways

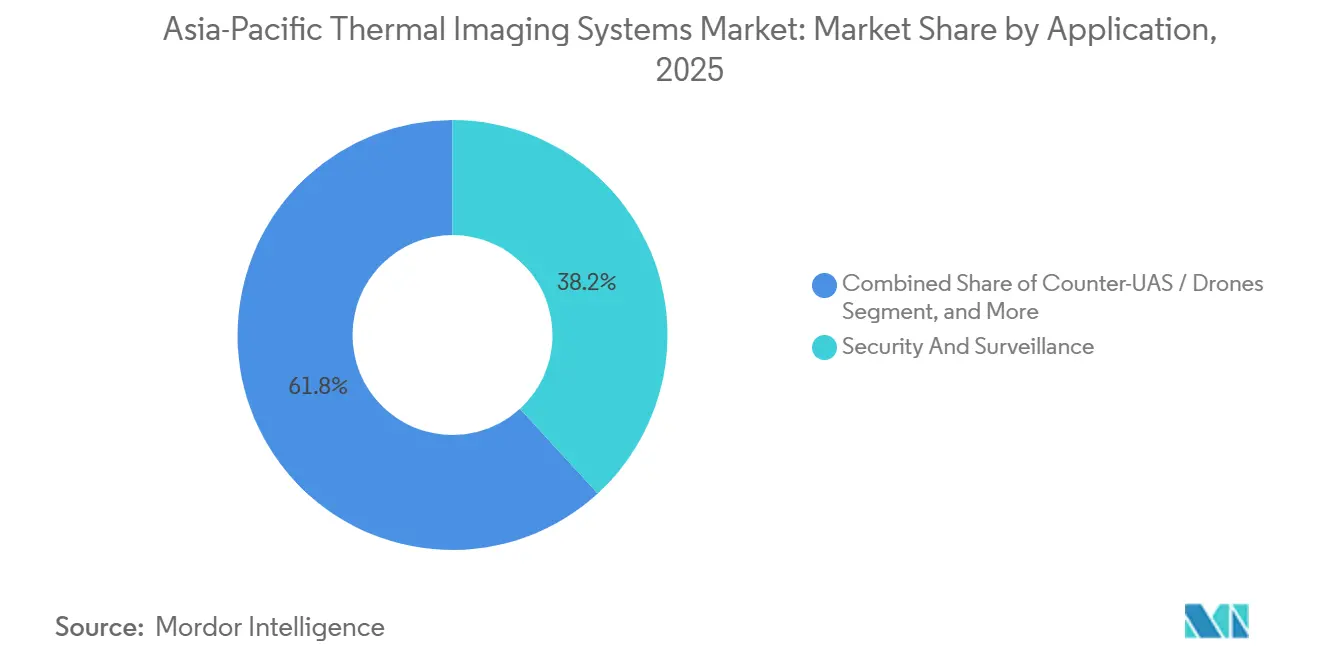

- By application, security and surveillance led with a 38.19% share of the Asia-Pacific thermal imaging systems market in 2025, while counter-UAS recorded the fastest projected 5.91% CAGR through 2031.

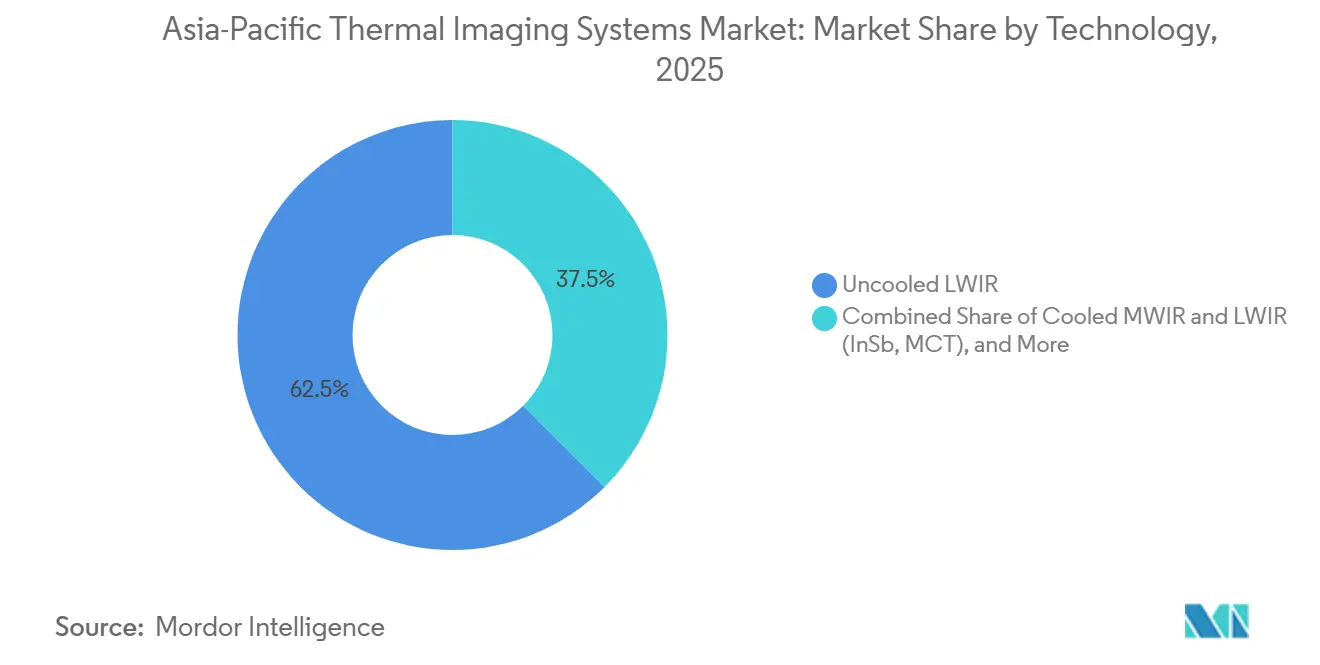

- By technology, uncooled long-wave infrared detectors captured 62.51% of the Asia-Pacific thermal imaging systems market size in 2025; short-wave infrared and multispectral systems are advancing at a 6.01% CAGR to 2031.

- By product, thermal cameras held 46.78% of the Asia-Pacific thermal imaging systems market share in 2025, yet thermal modules and cores are forecast to expand at a 5.88% CAGR to 2031.

- By end-user, aerospace and defense contributed 41.83% revenue in 2025, whereas automotive and mobility is poised for the highest 6.47% CAGR through 2031.

- China commanded 32.13% regional revenue in 2025, but India is projected to post a 6.66% CAGR, the fastest among Asia-Pacific economies.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Thermal Imaging Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining Cost of Uncooled Micro-Bolometer Sensors | +1.20% | Global, with strongest uptake in China, India, Southeast Asia | Short term (≤ 2 years) |

| Rising Defence and Border-Security Spending in Asia-Pacific | +1.50% | China, India, Japan, South Korea, Australia | Medium term (2-4 years) |

| Industrial Predictive-Maintenance Adoption | +0.80% | China, Japan, South Korea, Australia and New Zealand | Medium term (2-4 years) |

| Smartphone, Drone and ADAS Integration of Thermal Cores | +1.00% | China, Japan, South Korea, with spillover to Southeast Asia | Short term (≤ 2 years) |

| Livestock Bio-Security Mandates Using AI-Thermal Analytics | +0.40% | Australia, New Zealand, India, China | Long term (≥ 4 years) |

| Chalcogenide Optics Easing Germanium Supply Risk | +0.30% | Global, early adoption in Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining Cost of Uncooled Micro-Bolometer Sensors

Twelve-inch wafer processing and automated focal-plane assembly have cut vanadium-oxide detector prices by about 30% since 2020. Consumer-grade modules now retail below USD 200, opening doors for smartphone attachments and hobby drones. Chinese fabs ship more than 500,000 cores yearly, raising scale while 12-µm pixel pitches double array density with minimal cost penalty. Premium suppliers still deliver lower noise-equivalent temperature difference, yet commercial buyers find the newer mid-tier sensors sufficient for thermography and security uses.[1]IEEE Xplore, “Thermal Imaging and Microbolometer Technology Research,” ieeexplore.ieee.org

Rising Defense and Border-Security Spending in Asia-Pacific

Regional outlays on electro-optical and infrared systems rose 18% between 2024 and 2025 as nations strengthened maritime domain awareness and land-border surveillance. India approved thermal driver night sights for infantry vehicles under a USD 8 billion modernization package, while Japan budgeted USD 52 million for counter-drone arrays in fiscal 2026. South Korea finished a border-sensor upgrade in 2024, and Australia fielded ITAR-free thermal drones in 2025, signalling sustained institutional demand.[2]Japan Ministry of Defence, “Fiscal Year 2026 Budget Allocation for Counter-Drone Systems,” mod.go.jp

Industrial Predictive-Maintenance Adoption

Factories in China, Japan, and South Korea integrate handheld and fixed thermal cameras into Industry 4.0 workflows. Early hotspot detection prevents bearing failures, steam-trap losses, and switchgear fires, improving uptime and energy efficiency. Oil and gas regulators mandate quarterly thermographic audits, while camera vendors expand ISO-accredited training centers to address a scarcity of certified thermographers.[3]Fluke Corporation, “Industrial Thermography Training and Certification Programs,” fluke.com

Smartphone, Drone and ADAS Integration of Thermal Cores

Automakers embed thermal modules in sensor-fusion stacks to mitigate radar and visible-camera blind spots at night or in fog. Raytron began mass-production shipments to six Chinese brands in August 2025, offering 150-300 m detection ranges via automotive-grade Ethernet. Consumer drones outfitted with 640 × 512 cores cut search-and-rescue costs tenfold, and new sub-50 mW sensors now suit battery-powered wearables.[4]Raytron Technology, “Mass Production Partnerships for Automotive Thermal Modules,” raytrontek.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost and Export-Licence Constraints for Cooled Cameras | -0.70% | Global, acute in Southeast Asia, India, and smaller APAC markets | Medium term (2-4 years) |

| Scarcity of Certified Thermography Service Providers | -0.30% | Southeast Asia, India, smaller APAC markets | Long term (≥ 4 years) |

| Semiconductor-Grade VOx / InSb Wafer Supply Fragility | -0.40% | Global, with secondary effects in China, Japan, South Korea | Short term (≤ 2 years) |

| Smart-City Privacy Rules Limiting Thermal Surveillance | -0.20% | China, Singapore, with emerging constraints in India, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost and Export-Licence Constraints for Cooled Cameras

Cooled indium-antimonide or mercury-cadmium-telluride systems often exceed USD 50,000 per unit and require U.S. export licences for frame rates above 60 Hz or arrays over 111,000 pixels. Approval cycles run six to twelve months, forcing Southeast Asian militaries to favour ITAR-free mid-performance alternatives despite reduced detection range. Vendors sometimes throttle frame rates to 9 Hz to avoid licensing, but that limits dynamic tracking capability.

Scarcity of Certified Thermography Service Providers

Asia-Pacific hosts fewer than 5,000 ISO 9712 Level II and III thermographers, far short of demand from 200,000 factories and 50,000 large buildings. Limited expertise raises inspection fees to USD 150-300 per hour, placing thermal audits out of reach for many small enterprises. AI-based anomaly detection lowers analyst workload, yet insurance regulations in Japan and South Korea still mandate human sign-off, prolonging the talent gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Security Dominates, Counter-UAS Surges

In 2025, security and surveillance generated 38.19% of Asia-Pacific thermal imaging systems market revenue, buoyed by border monitoring and critical-infrastructure protection needs. Counter-unmanned-aerial-system projects are projected to log a 5.91% CAGR, reflecting new priorities along contested land and maritime boundaries. The Asia-Pacific thermal imaging systems market size tied to counter-UAS is set to climb as militaries integrate thermal sensors with acoustic and RF jammers for layered defense. A complementary trend is maritime agencies using unmanned surface vessels with thermal payloads for illegal-fishing patrols, allowing 24-hour operation at a fraction of conventional crewed vessel costs.

Thermography applications continue to expand as manufacturers link uncooled cameras to digital-twin software, diagnosing equipment faults weeks in advance. Fire-fighting brigades upgrade helmets with hands-free thermal overlays, while smartphone and medical uses diversify revenue beyond traditional safety markets. Urban utilities deploy fixed cameras at substations, reducing false alarms versus motion sensors. Collectively, these shifts position commercial verticals to overtake defense in market share before the forecast horizon ends.

By Product: Embedded Modules Outpace Stand-Alone Cameras

Thermal cameras captured 46.78% revenue in 2025, remaining the tool of choice for handheld inspections and fixed surveillance where real-time viewing is critical. Yet the share of modules and cores, now 5.88% CAGR, is rising as automotive and drone manufacturers demand board-level components without housings or displays. This embedded trend trims the bill of materials by roughly 40% and avoids export-licence delays. The Asia-Pacific thermal imaging systems market share for modules will widen further as consumer electronics adopt ultra-low-power 50 × 50-pixel sensors in smart-home devices.

Scopes and sights maintain specialized traction among armed forces and law-enforcement units seeking ruggedized optics compatible with existing weapons. Optical companies emphasize pixel-pitch miniaturization and AI-assisted image enhancement, but broader volume growth will stay with modular cores that can be soldered onto motherboards across industries, from robotics to agritech.

By Technology: Uncooled Sensors Anchor Growth, SWIR Gains a Foothold

Uncooled long-wave infrared detectors delivered 62.51% of 2025 revenue thanks to mature vanadium-oxide fabs and affordable pricing. The Asia-Pacific thermal imaging systems market size tied to SWIR and multispectral platforms, however, is expanding 6.01% CAGR because these wavelengths see through fog and particulate matter in automotive environments. Research into germanium-tin detectors that work at 240 K could remove cryocooler costs and swing market economics further toward SWIR.

Cooled mid-wave systems still dominate high-altitude and maritime reconnaissance, where kilometer-class detection trumps cost, but export regulations and USD-50,000-plus prices restrict their civilian uptake. As automotive sensor fusion mashes visible, radar, lidar, and thermal data, OEMs find that pairing SWIR with LWIR lifts pedestrian-classification accuracy by 25%, encouraging adoption even at premium prices.

By End-User Vertical: Automotive Moves to Center Stage

Aerospace and defense represented 41.83% of 2025 revenue, yet growth now tilts toward automotive and mobility, forecast at a 6.47% CAGR. Thermal cores below USD 300 allow mainstream vehicle models above USD 30,000 to integrate night-vision functions, especially in China where six brands signed Raytron supply pacts. Industrial plants and utilities also expand spending, installing fixed sensors that feed IIoT networks and simulate equipment wear in real time.

Livestock biosecurity illustrates new horizons: AI-assisted infrared scans detect bovine respiratory disease two days before symptoms, reducing herd mortality by 30%. Smartphone accessories offering fever screening and energy audits signal consumer-level diffusion. Collectively, these diverse buyers will shift share further toward non-military uses, accelerating commercialization of the Asia-Pacific thermal imaging systems market by decade’s end.

Geography Analysis

China remained the largest geography with 32.13% share in 2025, fuelled by vertically integrated suppliers that now hold more than 60% of the domestic Asia-Pacific thermal imaging systems market. Guide Infrared logged 68% year-over-year revenue growth and 907% profit expansion during H1 2025, while Hikvision opened a 200,000 m² plant to consolidate lens and detector production. Automotive tie-ups with Zeekr, BYD, and Geely fast-track thermal adoption in driver-assistance suites, positioning China to dominate the sensor-fusion landscape by 2028.

India is forecast to expand at 6.66% CAGR, anchored by border-surveillance upgrades and make in India policies that require 60% domestic content. Tonbo Imaging wins handheld and weapon-sight deals by under-pricing Western rivals and promising local support. Industrial plants in Gujarat and Maharashtra begin quarterly thermal audits, and dairy farms employ cameras to spot mastitis early, a use case that resonates with government campaigns for milk-yield improvement.

Japan controls roughly 18% of regional revenue, sustained by high equipment quality standards and mature calibration services. The Ministry of Defence budgeted USD 52 million for counter-drone arrays, and Teledyne FLIR shipped Star SAFIRE turrets for maritime helicopters. Research breakthroughs in germanium-tin SWIR detectors could halve cooled system costs, yet local automakers still favour radar and lidar, leaving potential upside if thermal modules hit parity in the next product cycle.

Southeast Asia expands on infrastructure security and illegal-fishing patrols. Singapore deployed unmanned surface vessels with thermal cameras for harbour defense, and the Philippines evaluates similar assets for fisheries. South Korea’s border program wrapped its first phase in 2024, while Australia and New Zealand collectively hold 10% share on the back of drone-based reconnaissance sourced through ITAR-free procurement.

Regulatory Landscape

Export-control compliance constrains higher-performance thermal imaging systems in Asia-Pacific. Dual-use controls under the Wassenaar Arrangement, together with U.S. ITAR/EAR thresholds that commonly affect higher frame-rate and higher-pixel-count cooled imagers, extend procurement cycles and influence product configurations, including detuning measures such as lower frame-rate variants to ease licensing and shipments into Southeast Asia and other price-sensitive markets.

In parallel, suppliers and integrators calibrate product and service delivery to national and international standards linked to industrial inspection and screening applications. In China, thermal inspection and NDT-related practices often reference GB/T 19870-2018 and GB/T 38238-2019, while public-security use can be shaped by sector standards such as GA/T 1708-2020. For human temperature screening and medical-adjacent deployments, Singapore SS 582 and IEC 80601-2-59 provide performance and safety anchors, and fire and life-safety requirements continue to evolve, including ISO progress in March 2026 when the final draft international standard (FDIS) for ISO/FDIS 7240-33 (thermal imaging fire detectors) entered formal approval steps.

Competitive Landscape

The Asia-Pacific thermal imaging systems market features moderately concentrated competition: the top five suppliers claimed nearly 55% revenue in 2025. Western incumbents Teledyne FLIR, L3Harris Technologies, and BAE Systems retain strongholds in cooled, high-performance arrays sold to U.S. allies, yet their share in commercial segments erodes under price pressure from Wuhan Guide Infrared, Hikvision, and Raytron. Export-control regimes reinforce this dual-tier market, with ITAR-free Chinese products favoured in Southeast Asia and India.

Emerging disruptors include Israeli firms Opgal and Elbit, offering mid-tier sensors without U.S. licensing, and South Korean groups Samsung and Hanwha that leverage semiconductor fabs to develop detectors in-house. Technology differentiation centers on 12-µm pixel designs and AI-assisted noise suppression that squeezes more performance from low-cost cores. Patent activity in 2025 spotlighted chalcogenide optics, trimming lens prices by up to 30%, and germanium-tin detectors that promise uncooled SWIR operation. Suppliers with ISO 9001 processes and IEC 62446 calibration credentials command premiums in aerospace and medical niches, though cost-sensitive buyers increasingly accept commercial-grade alternatives.

Asia-Pacific Thermal Imaging Systems Industry Leaders

Opgal Optronic Industries Ltd.

Fluke Corporation

LYNRED

Teledyne FLIR LLC

Testo SE and Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Embedded thermal modules and local integration capabilities are lowering deployment friction for automotive, drones, and factory automation. Asia-Pacific OEM demand is showing up in automotive-grade module supply activity, including Raytron mass-production shipments to multiple Chinese brands starting August 2025, and the June 2026 partnership between Suntek Global and Teledyne FLIR to expand technical support for thermal imaging integration in Taiwan, which supports a services-and-integration pathway for industrial and mobility deployments.

Process internalization and manufacturing capacity are also helping suppliers maintain supply for high-volume programs. In December 2025, South Korea-based Edge Foundry reported that it set up a mass production system for infrared sensors and a thermal imaging module, targeting 5,000 QVGA-class uncooled sensors per month, and added wafer-level vacuum packaging and related processes in-house. The ecosystem is reinforced by the CES 2026 platform announcement from LYNRED, Novatek, and ViewSEC for a thermal core platform, pointing to deeper on-device analytics and bundling opportunities across cooled and uncooled solutions.

Recent Industry Developments

- June 2026: Suntek Global partnered with Teledyne FLIR to develop a local thermal imaging ecosystem in Taiwan and broaden technical support services for thermal integration. The collaboration strengthens regional deployment capability for industrial and mobility use cases by pairing platform-level hardware with local engineering support and integration know-how.

- August 2025: Raytron began mass-production shipments of infrared sensor modules to multiple Chinese brands, supporting scaled supply of uncooled sensor cores for automotive and industrial applications. This expansion backs broader regional adoption and integration with system-level solutions, including on-device analytics and module bundles.

- September 2024: Teledyne FLIR announced a contract worth up to USD 20.8 million to deliver Star SAFIRE 380-HLD multi-spectral imaging systems to the Japan Maritime Self-Defense Force for SH-60L helicopters. The program reflects ongoing maritime surveillance modernization and sustained demand for premium EO/IR capabilities in airborne platforms.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenue generated from thermal imaging systems sold and deployed across Asia Pacific, including cameras and related imaging solutions used to detect heat patterns for monitoring, inspection, safety, and security use cases.

Scope exclusions: We exclude basic temperature screening tools that do not provide true thermal imaging outputs, along with general visible-light cameras sold without thermal functionality.

Segmentation Overview

- By Application

- Thermography

- Maritime and Coastal Surveillance

- Border Surveillance

- Counter-UAS / Drones

- Critical Infrastructure Security

- Other Applications (Fire-Fighting, Smartphones, Medical, PVS)

- By Product

- Thermal Cameras

- Thermal Scopes / Sights

- Thermal Modules / Cores

- By Technology

- Uncooled LWIR (VOx / a-Si)

- Cooled MWIR and LWIR (InSb, MCT)

- SWIR and Multispectral

- By End-User Vertical

- Aerospace and Defence

- Law-Enforcement and Public Safety

- Healthcare and Veterinary

- Automotive and Mobility

- Oil and Gas and Process Industries

- Manufacturing and Utilities

- Other End-User Verticals

- By Country

- China

- Japan

- India

- Southeast Asia

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a clean fact base on demand triggers and supply availability across Asia Pacific. We referred to public sources such as defense budget releases and procurement portals, trade statistics from customs authorities, industrial safety and electrical standards bodies, and research publications on infrared sensors and thermography use.

To keep assumptions practical, we also reviewed company annual reports, investor presentations, and product catalogs to understand typical system pricing bands and replacement cycles. Where it helped, we used a paid subscription for company financials and news to track plant expansions, export restrictions, and contract wins that can shift regional demand. This desk research list is not exhaustive, and many other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test desk assumptions and fill gaps that are common in this market, especially around average selling price movement, lead times, and real adoption rates by end users. We spoke with a mix of manufacturers, component ecosystem participants, distributors, system integrators, and large buyer groups across key Asia Pacific countries so the sizing reflects both supply push and actual procurement behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 13% | |

| Mid tier: 54% | Functional/Unit leaders: 35% | |

| Smaller Players: 19% | Managers: 52% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where regional demand pools were reconstructed from defense and public safety procurement patterns, industrial production activity, and the installed base of inspection and monitoring programs, and then split into thermal imaging system spending. To avoid over-relying on one macro series, results were cross-checked with selective bottom-up approximations, such as sampled country level pricing by form factor and a supplier plus channel roll-up for high-visibility use cases.

Inputs used in the model included, as examples, defense modernization cycles, critical infrastructure security spending, growth in factory predictive maintenance adoption, construction and utilities inspection intensity, and the mix shift between cooled and uncooled systems that changes price points. Where country data was thin, gaps were handled through proxy indicators (for example, using neighboring market adoption patterns and import trends) and then corrected based on interview feedback.

Forecasts were derived using scenario analysis supported by simple trend fitting, with separate cases for procurement timing swings, ASP compression from local production, and faster adoption in industrial and automotive safety use cases. Assumptions were kept transparent so a client can trace each number back to a demand driver and a pricing logic.

Data Validation & Update Cycle

Model outputs were validated through triangulation across independent signals, and then reviewed for large variances at the country and application level before sign-off. When an estimate looked off, we revisited the input driver, rechecked the conversion logic (unit volumes to value), and re-contacted experts if a procurement cycle or pricing shift seemed to be the cause.

Each report is refreshed annually, and interim updates are made when material events occur, such as export control changes, major contract awards, or sudden pricing moves in sensors and modules. Before delivery, a final analyst pass is completed so clients receive the most current view aligned to the latest available data and interviews.

Mordor Intelligence's Asia Pacificthermal Imaging Systems Market Market Size Measured Against Other Published Estimates

Published market sizes for Asia Pacific thermal imaging often do not match because groups define the product boundary differently and do not always treat country coverage, currency timing, and pricing changes in the same way. Differences also come from whether the figure is a base year snapshot or a forward year projection, which can look larger or smaller depending on the procurement calendar.

The main gap drivers in this market are usually scope (systems versus modules versus broader infrared devices), the treatment of defense programs that are announced but not yet awarded, and how fast average selling prices are assumed to decline as local manufacturing scales. Some estimates also mix Asia Pacific with parts of nearby geographies, or they convert currencies using different averaging windows, which shifts the USD value even when unit demand is similar, a discipline applied in our baseline numbers near the end of modeling, including the specific inclusions and exclusions used by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.75 B (2025) | |

| Regional Consultancy A | USD 3.80 B (2025) | This figure typically runs higher when broader infrared hardware is grouped into the same bucket, and when announced public programs are counted earlier even if award timing is not confirmed for the base year. |

| Trade Journal B | USD 2.15 B (2031) | This number is a forward-year projection and can look lower if it focuses on camera sales only and applies faster ASP decline assumptions without consistent checks against procurement cycles and import trends. |

The spread across sources is mainly explained by what is included as a thermal imaging system, the year being referenced, and how price erosion is treated as volumes rise. By keeping scope rules explicit and tying assumptions to observable signals like procurement timing, industrial activity, and trade flows, our approach gives a steady figure that can be repeated and updated without hidden steps.

Key Questions Answered in the Report

What is the forecast value of the Asia-Pacific thermal imaging systems market by 2031?

The market is projected to reach USD 3.83 billion by 2031, growing at a 5.65% CAGR from 2026.

Which application is expanding fastest in regional demand?

Counter-UAS solutions show the highest 5.91% CAGR, driven by border and exclusive economic zone security needs.

Why are thermal modules gaining share over stand-alone cameras?

Automotive, drone, and IoT manufacturers prefer board-level modules that lower bill-of-materials costs and avoid export-licence hurdles.

Which country will record the quickest growth through 2031?

India is forecast to post a 6.66% CAGR on the back of border-modernization spending and Make in India localization goals.

How do export regulations affect cooled camera adoption?

U.S. and Wassenaar controls extend procurement cycles up to a year and lift prices, steering many Asia-Pacific buyers toward ITAR-free uncooled alternatives.

What technological breakthrough could reshape SWIR usage?

Germanium-tin detectors operating near 240 K may eliminate cryocoolers, potentially halving total system cost and spurring wider SWIR adoption.

Page last updated on: